Figures & data

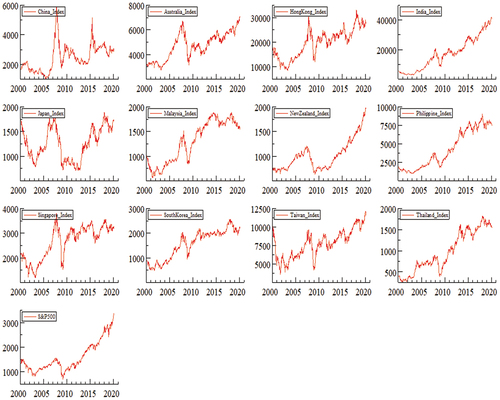

Figure 1. Exhibits weekly price index trends for the entire sample.

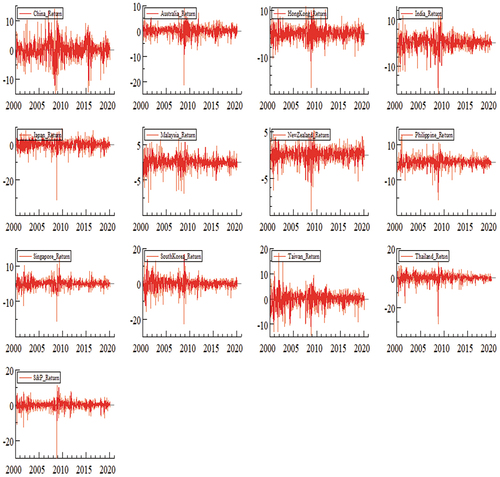

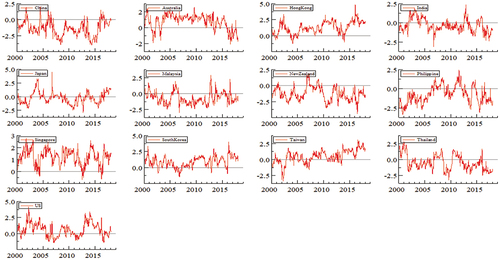

Figure 2. Exhibits weekly price movements for the entire sample.

Table 1. Descriptive statistics of all stock markets using weekly return data

Table 2. Presents the calculated result of the ARMA (1, 1)-DECO-GARCH (1, 1) model

Figure 3. Dynamic equicorrelation across all stock markets.

Table 3. Diagnostic tests

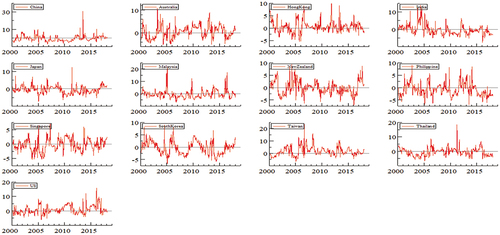

Figure 4. Conditional variances for each stock market using ARMA(1,1)- DECO-GARCH(1,1) model.

Table 4. Dynamic Connectedness Return spillovers across all sample stock markets

Table 5. Dynamic Connectedness conditional variance volatility spillovers across all sample stock markets

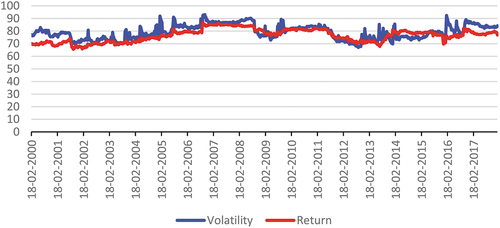

Figure 5. Dynamic total connectedness return and conditional variance volatility for all stock markets.

Figure 6a. A Net return Spillovers.

Figure 6b. Net volatility spillovers.

Table 6. Performance of optimal portfolios’ hedge ratios

Table 7. Performance optimal portfolios’ weights