Figures & data

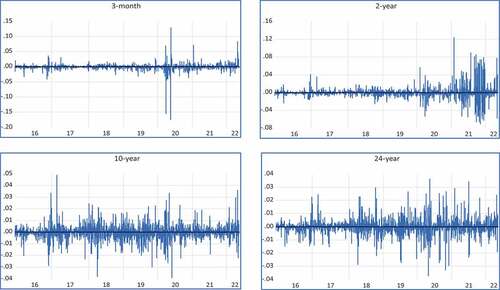

Figure 1. Sovereign bond yield series graphs at first difference.

Table 1. Descriptive statistics (across maturities)

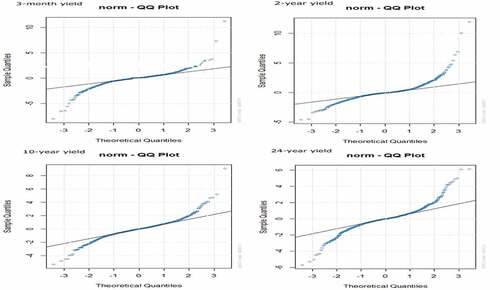

Figure 2. QQ plots of the EGARCH residuals.

Table 2. Descriptive statistics (macro-economic indicators and sovereign yields at quarterly frequency)

Table 3. Unit root test results

Table 4. Unit root test results for macroeconomic variables

Table 5. ARCH LM test results

Table 6. EGARCH results

Table 7. Distribution selection under EGARCH

Table 8. EGARCH results during pre-COVID-19

Table 9. EGARCH results during the COVID-19 era

Table 10. Granger casualty test for the linkage between sovereign bond yield volatility and inflation

Table 11. Granger casualty test for the linkage between sovereign bond yield volatility and money market volatility