Figures & data

Table 1. Basic statistics

Table 2. Statistical tests

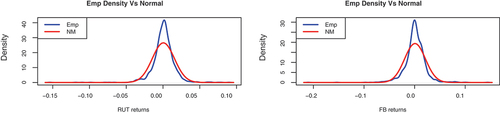

Figure 1. Empirical densities.

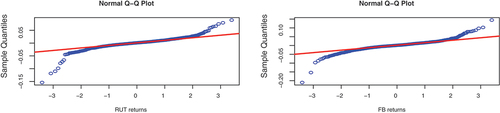

Figure 2. Q-Q plots.

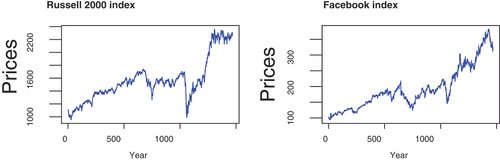

Figure 3. Adjusted stock index prices.

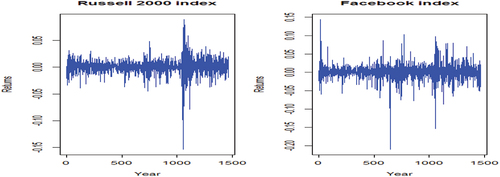

Figure 4. Index returns.

Table 3. MLE parameter estimates

Figure 5. Smoothed probability for Russell 2000 index.

Figure 6. Smoothed probability for Facebook index.

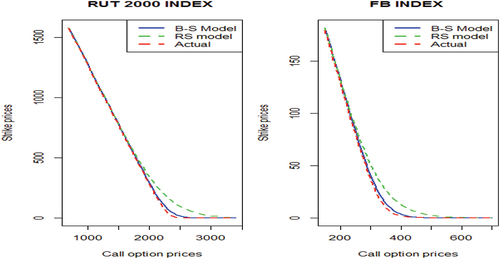

Figure 7. Options.

Table 4. Call option prices for Russell 2000 and Facebook indices

Table 5. RMSE for the black-Scholes and regime-switching models