Figures & data

Figure 1. St. Louis fed Taylor rule.

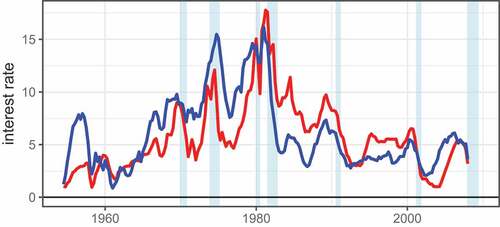

Figure 2. 1954–2008.

Table 1. Summary of literature review on identifying and analyzing monetary policy regimes

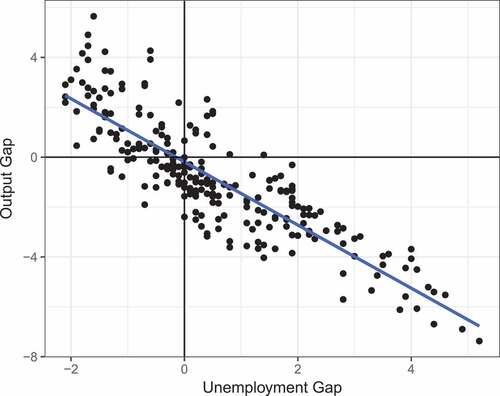

Figure 3. Gap version of Okun’s law 1954–2008.

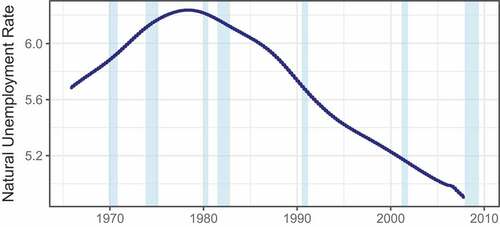

Figure 4. Monthly natural rate of unemployment.

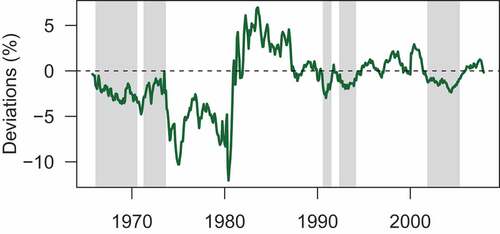

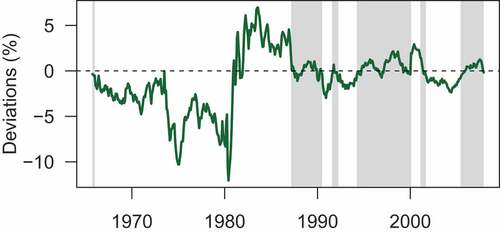

Figure 5. Real-Time , 1965–2008.

Table 2. Tukey HSD:St. Louis rule

Table 3. Tukey HSD: Bernanke rule

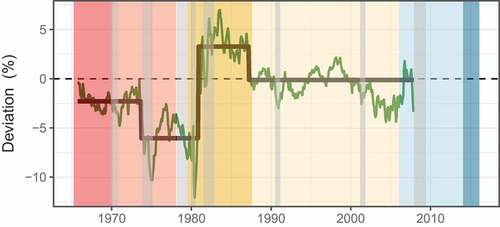

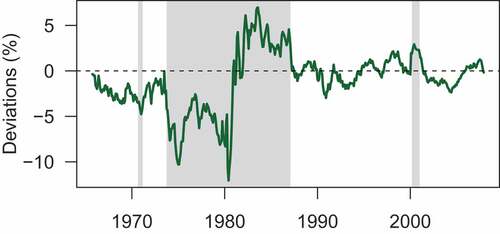

Figure 6. Fitted regimes with Fed Chairman tenure periods, 1965–2008.

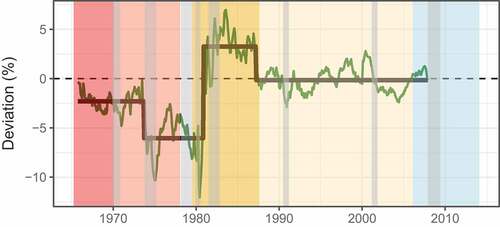

Figure 7. Fitted Regimes using PCE rather than CPI inflation target from 2000 to 2008.

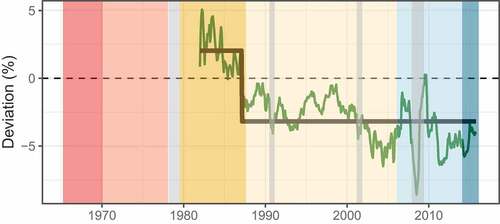

Figure 8. Fitted regimes using university of michigan 1-year inflation expectations for the inflation gap rather than CPI or PCE from 1982 to 2015.

Figure 9. Markov Switching: Regime 0 (“Loose”).

Figure 10. Markov switching: regime 1 (“Tight”).

Figure 11. Markov switching: regime 2 (“Inconsistent”).

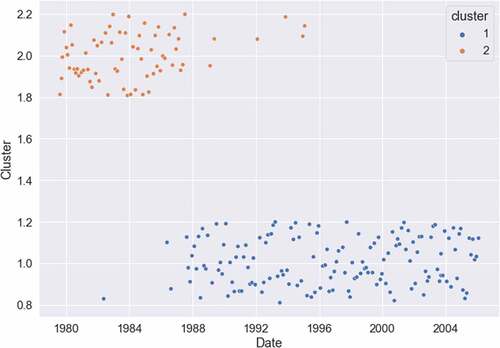

Figure 12. Clustering results of FOMC transcripts: 2 clusters.

Table 4. Mean deviation from the Taylor rule: By clusters

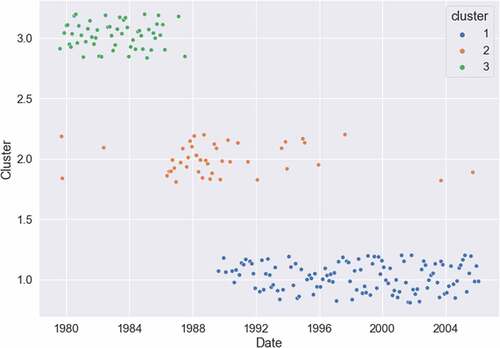

Figure 13. Clustering results of FOMC transcripts: 3 clusters.

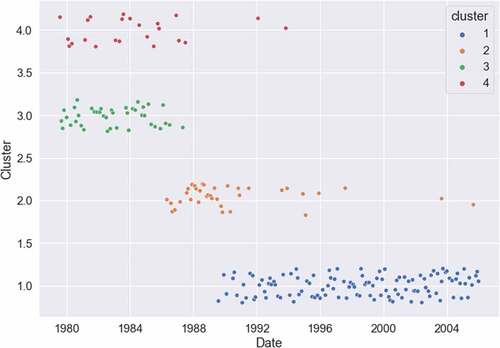

Figure 14. Clustering results of FOMC transcripts: 4 clusters.

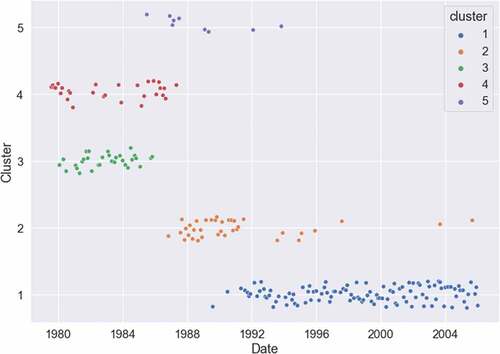

Figure 15. Clustering results of FOMC transcripts: 5 clusters.

Figure 16. Wordcloud of the top texts in cluster 1 (regime from roughly from 1990 to 2007).

Figure 17. Wordcloud of the top texts in cluster 2 (regime from roughly from 1987 to 1990).

Figure 18. Wordcloud of the top texts in cluster 3 (regime from roughly from 1979 to 1986).

Figure A1. Within Groups Sums of Squares.