Figures & data

Table 1. List of countries with corresponding region and stock market indices

Table 2. Statistics on COVID-19 pandemic until 7 April 2022

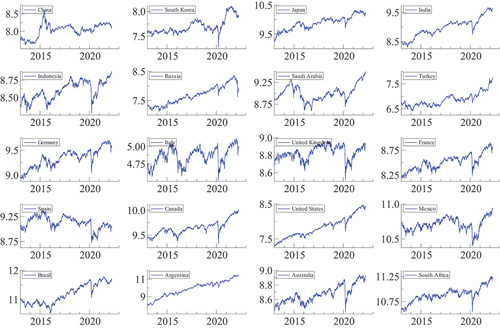

Figure 1. Evolution of G20 stock market indices.

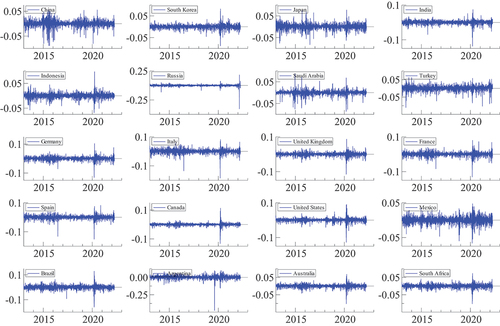

Figure 2. Evolution of G20 stock market returns.

Table 3. Descriptive statistics of stock market returns over all period

Table 4. Descriptive statistics of stock market returns for each subperiod

Table 5. Linear correlation coefficients for each subperiod

Table 6. Estimation results of time-varying SJC copulas for each subperiod

Table 7. Estimation results of time-varying SJC copulas for each subperiod

Table 8. Mean of lower and upper tail dependence coefficients of time-varying SJC copula for each subperiod