Figures & data

Table 1. The table depicts a review of the empirical literature on MDF and its stability and covers the authors’ details, countries, sample covered, methodology, and findings of the studies

Table 2. Variables’ description used for dynamically simulated ARDL model

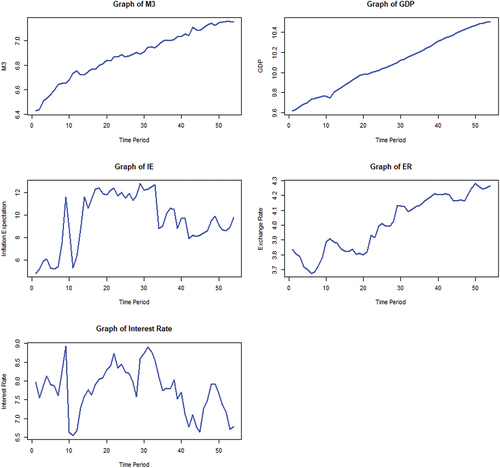

Figure 1. Plots of underlying time series variables for the period 2006: Q3 to 2019: Q4.

Table 3. Descriptive statistics

Table 4. Unit root test results

Table 5. Results of bounds test for cointegration, diagnostic testing, and parameter stability test

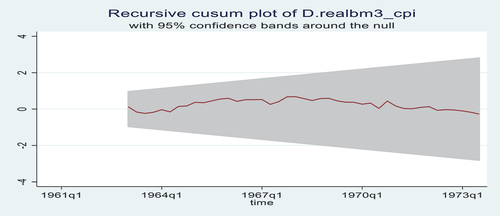

Figure 2. Plot of recursive CUSUM.

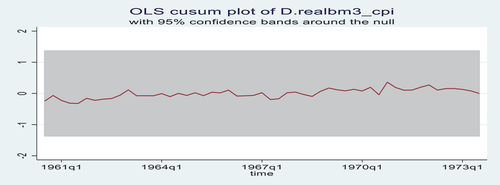

Figure 3. Plot of OLS CUSUM.

Table 6. Dynamically simulated ARDL results

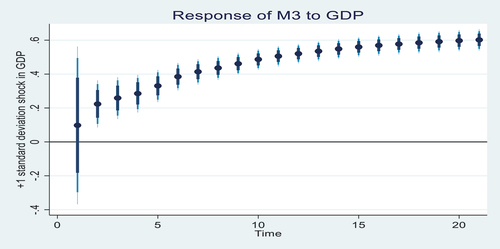

Figure 4. The impulse response plot for GDP.

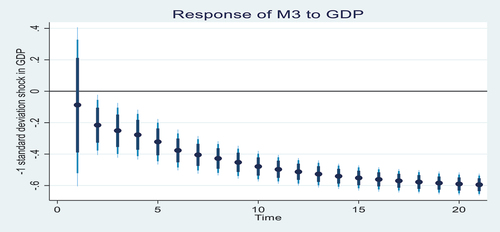

Figure 5. The impulse response plot for GDP.

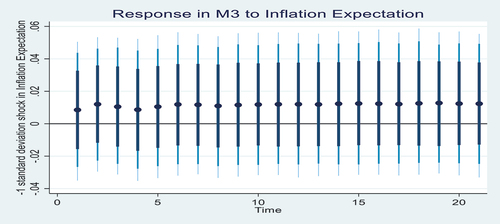

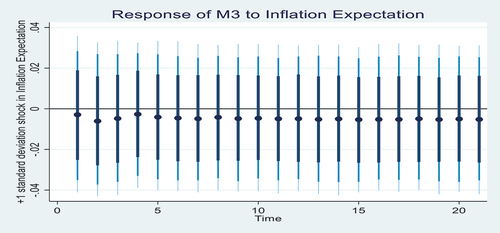

Figure 6. The impulse response plot for inflation expectation.

Figure 7. The impulse response plot for inflation expectation.