Figures & data

Table 1. Coefficient of variation of the variables

Table 2. ADF and PP Unit Root Test for Mean stationery of RERs of 468 Obs

Table 3. Estimation results of Time Varying-Cointegration Coefficients for CPI

Table 4. Estimation results of Time Varying-Cointegration Coefficients

Table 5. Hurst exponents of the real exchange rate in absolute form

Table 6. Johansen’s trace and maximal eigenvalue test statistics for the cointegration of countries in the study using the US as a base

Table 7. Johansen’s trace and maximal eigenvalue test statistics for the cointegration of countries in the study using Japan as a base

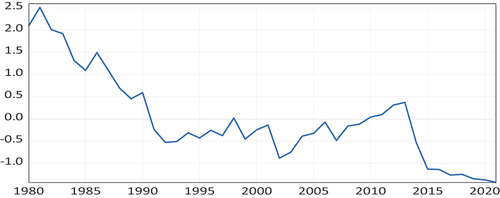

Figure 1. Time-varying cointegration coefficient on the CPI using the US as a base country.

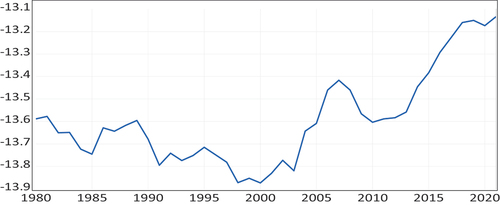

Figure 2. Time-varying cointegration coefficient on a foreign exchange using the US as a base country.

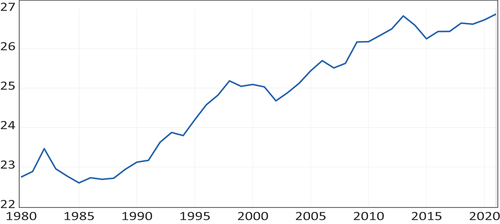

Figure 3. Time-varying cointegration coefficient on the CPI using Japan as a base country.

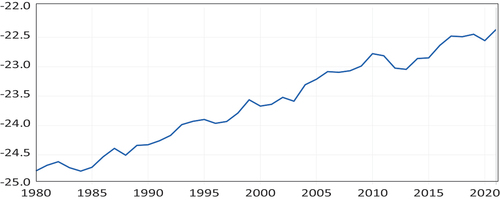

Figure 4. Time-varying cointegration coefficient on a foreign exchange using Japan as a base country.