Figures & data

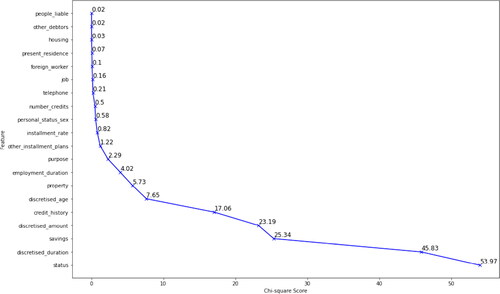

Figure 1. Variation in Chi-square values across all features in the credit dataset.

Table 1. Chi-square score and p-values for the various features in the credit dataset.

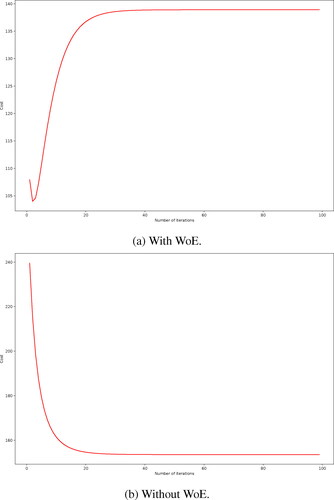

Figure 2. Cost function minimisation for the logistic regression model.

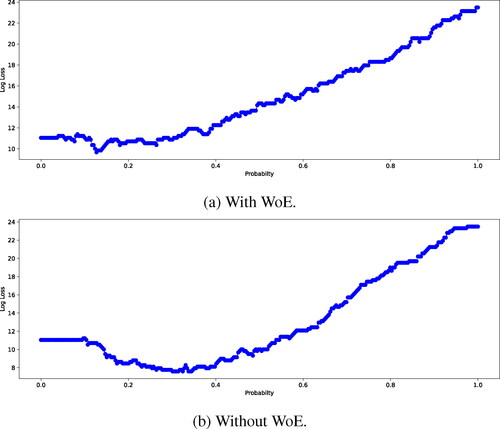

Figure 3. Log loss for various threshold probabilities for the logistic regression model.

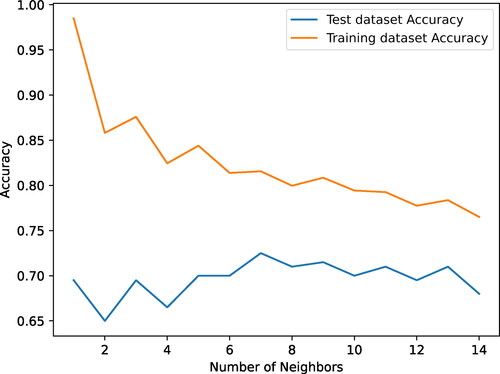

Figure 4. Training and test accuracy of different neighbour values used in the KNN model.

Table 2. Classification scores for all models.

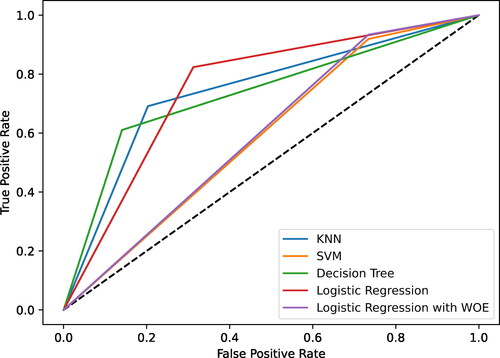

Figure 5. Receiver operating characteristic curve for all five models.

Supplemental material

LatexSourceRev.zip

Download Zip (4 MB)Data availability statement

The data used in the paper can be provided on request.