Figures & data

Figure 1. Left side: Signature pattern of MM(1) process with . It is shown in Zhang and Smith (Citation2010) that signature patterns will occur infinitely many times in a moving maxima processes. Right side: The loading constant α is replaced with a uniform random variable on the interval [0, 1] to remove the signature pattern.

![Figure 1. Left side: Signature pattern of MM(1) process with . It is shown in Zhang and Smith (Citation2010) that signature patterns will occur infinitely many times in a moving maxima processes. Right side: The loading constant α is replaced with a uniform random variable on the interval [0, 1] to remove the signature pattern.](/cms/asset/a3930847-2a85-4fbc-8ff4-bae236a2f055/tstf_a_1346852_f0001_b.gif)

Figure 2. Simulation of models (Equation4(4) ) (left) and (Equation5

(5) ) (right) with size = 1000, (C, ψ, β, τ) = (0.001, 2, 1.5, −0.5) and α = (0.5, 0.3, 0.2). The horizontal lines are the 90th percentiles.

Figure 3. Simulation of model (Equation4(4) ) with size = 1000, (β, τ) = (1.5, −0.5) and α = (0.5, 0.3, 0.2). Left side: First 50 realisations, t = 1 : 50. Right side: 901st to 950th realisations, t = 901: 950.

Figure 4. Simulation of models (Equation4(4) ) (left) and (Equation5

(5) ) (right) with size = 1000, (C, ψ, β, τ) = (0.001, 2, 0.7, 0.5) and α = (0.5, 0.3, 0.2). The horizontal lines are the 90th percentiles.

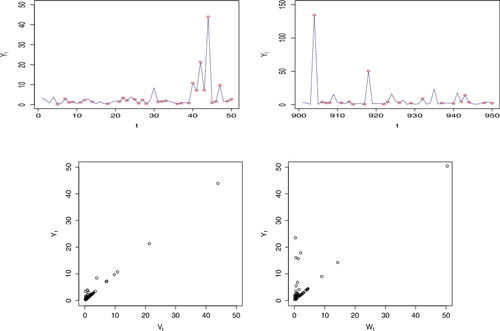

Figure 5. Simulation of model (Equation4(4) ) with size = 1000, (β, τ) = (0.7, 0.5) and α = (0.5, 0.3, 0.2). Left side: First 50 realisations, t = 1 : 50. Right side: 901st to 950th realisations, t = 901: 950. (Y30, Y904, Y918, Y943) = (110.2, 36749.2, 4545.1, 320.9) are out of the y-axis limits.

Figure 6. Simulation Result 2.1: Graph of MCMC results for all parameters of model (Equation5(5) ), showing time plot, estimated posterior distribution and autocorrelation.

Table 1. Results of estimation for simulation example of model (Equation5(5) ).

Table 2. Results of convergence test for simulation example of model (Equation5(5) ).

Table 3. Results of sensitivity analysis for simulation example of model (Equation5(5) ).

Table 4. Results of estimation for 500 simulation examples, using median values of the parameters from each simualtion. [Int. C.P. means Interval Coverage Probability.]

Table 5. Results of estimation for simulation example of model (Equation5(5) ).

Figure 7. Intra-daily maxima of the US Dollars vs. Japanese Yen 3-minute negative log-returns. The horizontal line is the 90th percentile.

Figure 8. Real data analysis of USD vs JPY: Graph of MCMC results for transformation parameters of model (Equation5(5) ), showing time plot, estimated posterior distribution and autocorrelation.

Figure 9. Real data analysis of USD vs JPY: Graph of MCMC results for alpha parameters of model (Equation5(5) ), showing time plot, estimated posterior distribution and autocorrelation.

Figure 10. Quantile-quantile plots using estimated mean values on left and median values on right.

Table 6. Results of estimation for real data example of intra-daily maxima of 3-minute negative log-returns of USD vs. JPY.

Figure A1. Simulation result: Graph of MCMC results showing rapid fluctuation of parameters.

Figure A2. Simulation result: Graph of MCMC results showing scatter plot of parameters.

Figure A3. Unit Fréchet density (left) and Fréchet(β, 1, τ) density (right). Left: β = 1.5 and τ = −0.5. Right: β = 0.7 and τ = 0.5.

Figure A4. Simulation Result 2.2: Graph of MCMC results for all parameters of model (Equation5(5) ), showing time plot, estimated posterior distribution and autocorrelation.