Figures & data

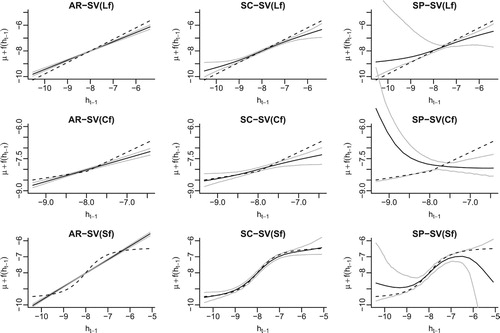

Figure 1. Estimated autoregressive function f for the unleveraged SV models based on a single simulated dataset. The dashed line in each graph shows the true functional form of f and the solid lines represent the posterior average of f as well as the 95% credible bands. For the semiparametric models SC-SV and SP-SV, the 20-knot-interval version is presented.

Table 1. For the three true unleveraged SV models (Lf , Cf and Sf ), a summary of the MSE and MAE of the log volatilities,  , obtained from fitting five different SV models. The averages and standard errors are multiplied by 100, and are based on 200 replicate series.

, obtained from fitting five different SV models. The averages and standard errors are multiplied by 100, and are based on 200 replicate series.

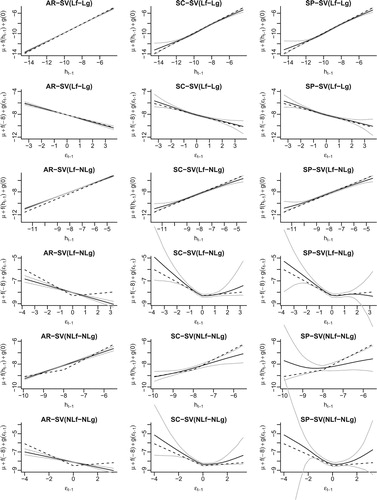

Figure 2. For the three true leveraged SV models (Lf-Lg, Lf-NLg and NLf-NLg), the estimated autoregressive function f (odd rows) and leverage function g (even rows) in different fitted models (columns). The legends are the same as in Figure .

Table 2. For the three true leveraged SV models (Lf-Lg, Lf-NLg and NLf-NLg), a summary of the MSE and MAE of the log volatilities, , obtained from fitting five different SV models. The averages and standard errors are multiplied by 100, and are based on 200 replicate series.

Table 3. Predictive log likelihood of daily returns from November 1, 2010 to October 31, 2013 using six different SV models. (u) – unleveraged; (l) – leveraged. The results of the best performing model (those with the largest predictive log likelihood) are in bold face.

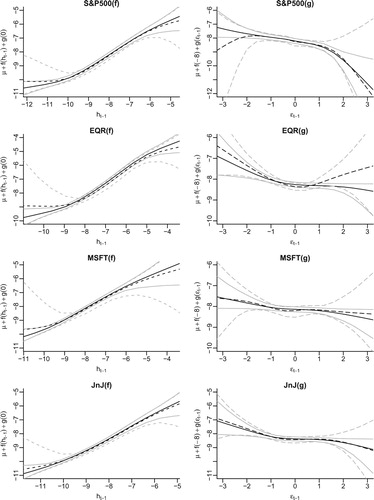

Figure 3. Fitted autoregressive function f and leverage function g for the daily returns of the S&P500, EQR, MSFT and JnJ. The solid lines show the posterior means and 95% credible bands of the fitted functions in the leveraged semiparametric models with shape constraints while the dashed lines represent the posterior means and 95% credible bands in the leveraged semiparametric models without shape constraints.