Figures & data

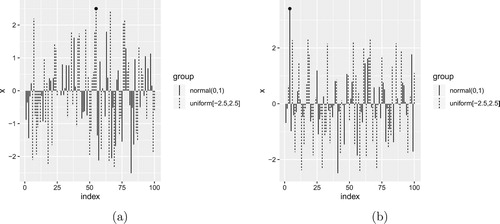

Figure 1. Simulated mixed sequences from normal and uniform distributions and their maxima (marked with black dots). In (a), the maximum is from the uniform distribution; in (b), the maximum is from .

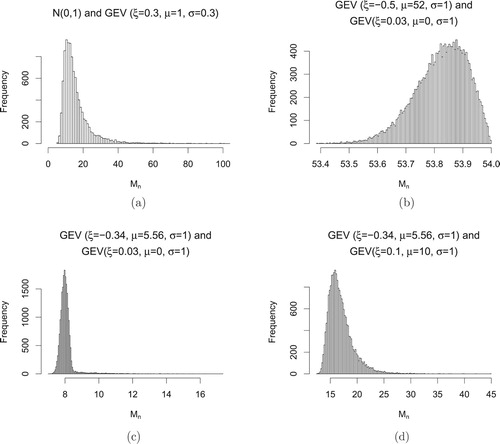

Figure 2. (a) Histogram of from

and

. (b) Histogram of

from

and

.

![Figure 2. (a) Histogram of Mn from N(0,1) and U[−2.2,2.2]. (b) Histogram of Mn from N(0,1) and U[−2.8,2.8].](/cms/asset/302fdf89-2a88-41c8-a54c-bb68ea846ca9/tstf_a_1846115_f0002_ob.jpg)

Figure 3. Histograms of combinations of from

and

. (a)

,

. (b)

,

.

![Figure 3. Histograms of combinations of Mn from N(0,0.9) and U[−2,2]. (a) n1=100, n2=200. (b) n1=200, n2=100.](/cms/asset/f1399af6-7e8c-4177-8e2b-2c1bf04e1b24/tstf_a_1846115_f0003_ob.jpg)

Figure 4. Histograms of . (a)

and Fréchet combination. (b)–(d) Some combinations of Fréchet and Weibull.

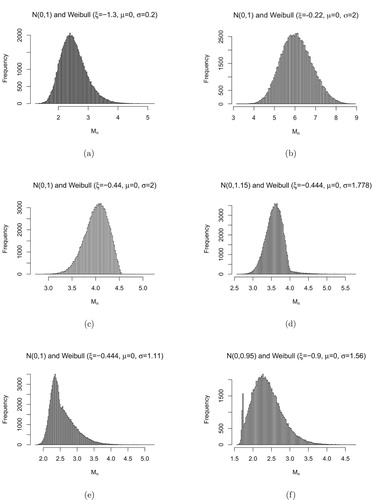

Figure 5. Histograms of , with combinations of normal distribution and Weibull distribution.

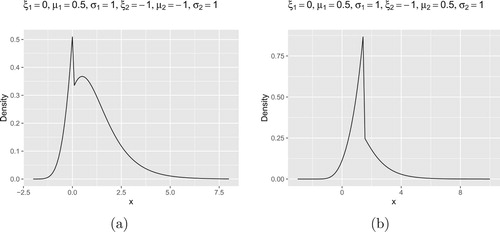

Figure 6. Density plots of the accelerated max-stable distributions with Weibull-Gumbel combinations. (a) ,

,

,

,

,

. (b)

,

,

,

,

,

.

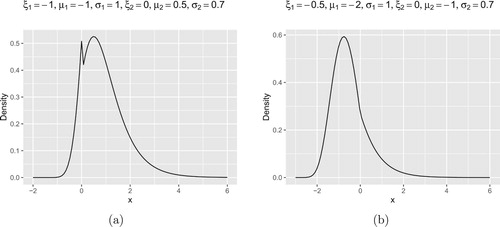

Figure 7. Density plots of the accelerated max-stable distributions with Weibull-Gumbel combinations. (a) ,

,

,

,

,

. (b)

,

,

,

,

,

.

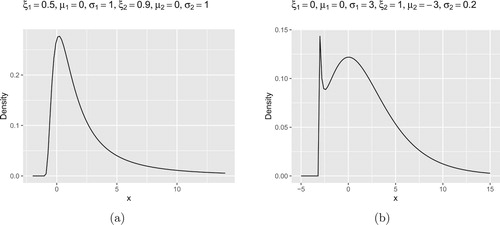

Figure 8. (a) Density plot of the accelerated max-stable distribution with Fréchet-Fréchet combinition. ,

,

,

,

,

. (b) Density plot of the accelerated max-stable distributions with Fréchet-Gumbel combinition.

,

,

,

,

,

.

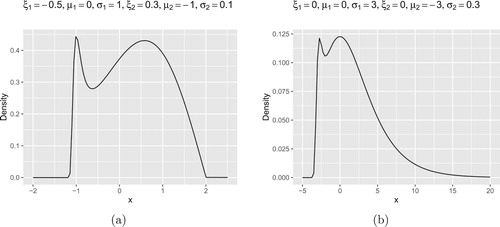

Figure 9. (a) Density plot of the accelerated max-stable distribution with Weibull-Fréchet combination. ,

,

,

,

,

. (b) Density plot of the accelerated max-stable distribution with Gumbel-Gumbel combinition.

,

,

,

,

,

.

Table 1. The proportions of the simulated data based on the fitted accelerated max-stable distributions and GEV distributions that exceeds the 90th, 95th and 99th percentiles of the original data .

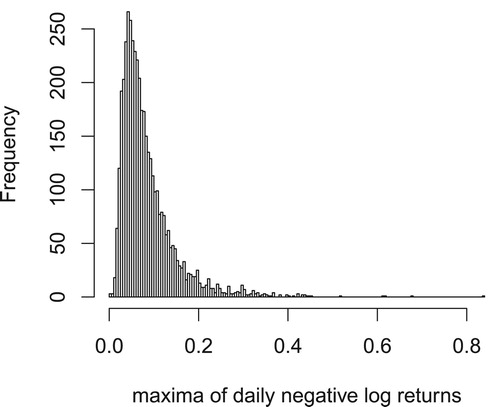

Figure 10. The histogram of the daily maxima of negative log returns of 330 stocks in the S&P 500 companies list.

Table 2. The proportions of the simulated samples generated from the fitted distributions that exceed the 90th, 95th, and 99th sample percentiles of the maximal daily negative log returns.