Figures & data

Table 1. Coverage probabilities for ARMA(1,1) models.

Table 2. Coverage probabilities for ARFIMA(1,d,0) models.

Table 3. Coverage probabilities for ARFIMA(2,d,0) models.

Table 4. Coverage probabilities for ARFIMA(0,d,1) models.

Table 5. Coverage probabilities for ARFIMA(0,d,2) models.

Table 6. Coverage probabilities for ARFIMA(1,d,1) models.

Table 7. Performance of point estimates of the autoregression parameter ϕ in AR(1) under model misspecification.

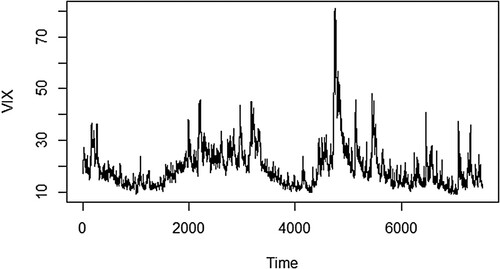

Figure 1. The SP 500 VIX series.

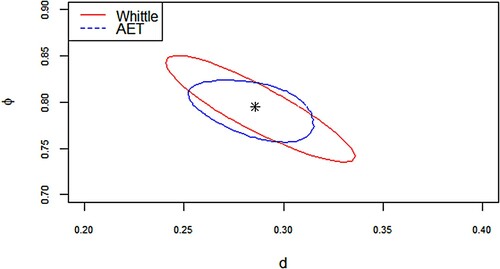

Figure 2. 95% confidence region of the parameters for fitted ARFIMA(1,d,0) of the S&P 500 VIX series.

Table 8. Point estimates of the parameter vector by the three methods.