Figures & data

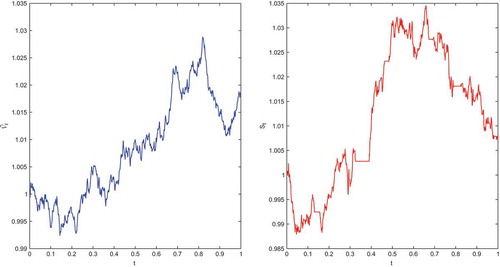

Figure 1. Comparison of the spot exchange rate’ sample paths in the model (left) and the subdiffusive

model (right) for

.

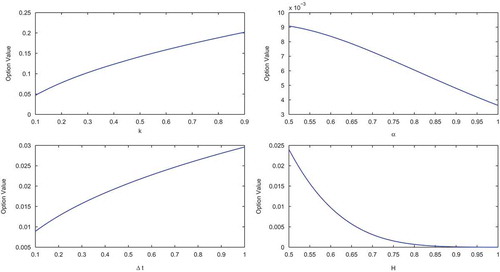

Figure 2. Call currency option values.

Figure 3. Relative difference between the ,

, and subdiffusive

models for the in-the-money case.

Figure 4. Relative difference between the ,

, and subdiffusive

models for the out-of-the-money case.