Figures & data

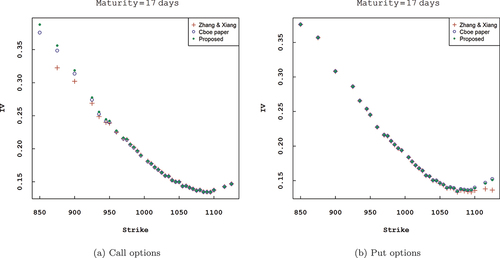

Figure 1. Comparison of the implied volatility obtained from the three approaches for SPX call and put options that mature on 21 November 2003.

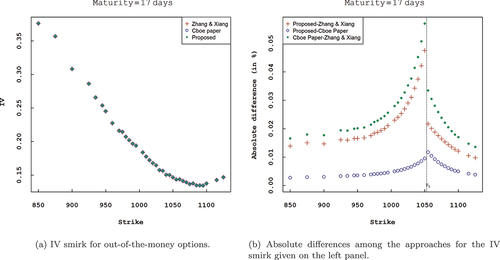

Figure 2. Comparison of the IV smirk for out-of-the-money options obtained from the three approaches that mature on 21 November 2003.

Table 1. Parameter estimation results on the market data of SPX options (standard) maturing on 17 February 2023, 17 March 2023, 21 April 2023, 19 May 2023, 21 July 2023, and 19 January 2024. DFzx represents the discount factor obtained via the approach in (Zhang & Xiang, Citation2008) and is calculated using the one-month, two-months, three-months, four-months, six-months and one-year treasury yield curve rates given respectively by 4.69%, 4.64%, 4.72%, 4.75%, 4.8% and 4.68%. DFzx and DFkm are the implied discount factors obtained using the approach in the Cboe paper and our proposed approach, respectively

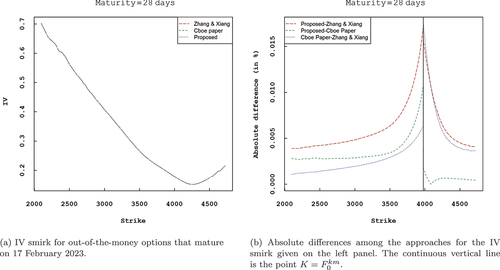

Figure 3. Comparison of the IV smirk for out-of-the-money options obtained from the three approaches for SPX call and put options that mature on 17 February 2023.

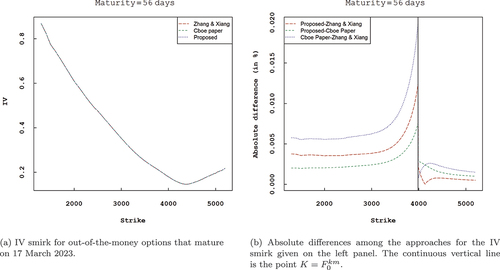

Figure 4. Comparison of the IV smirk for out-of-the-money options obtained from the three approaches for SPX call and put options that mature on 17 March 2023.

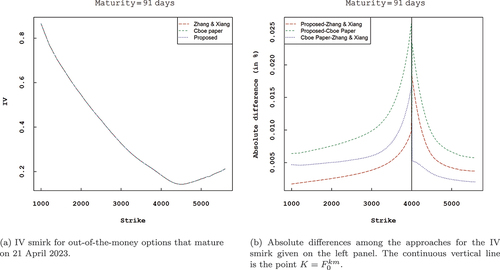

Figure 5. Comparison of the IV smirk for out-of-the-money options obtained from the three approaches for SPX call and put options that mature on 21 April 2023.

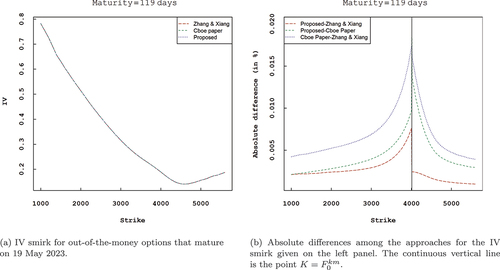

Figure 6. Comparison of the IV smirk for out-of-the-money options obtained from the three approaches for SPX call and put options that mature on 19 May 2023.

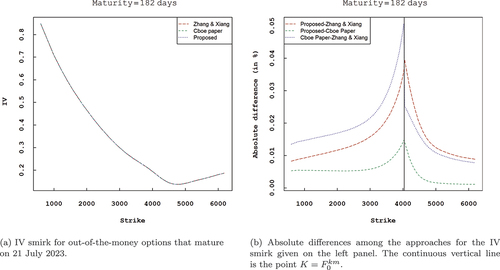

Figure 7. Comparison of the IV smirk for out-of-the-money options obtained from the three approaches for SPX call and put options that mature on 21 July 2023.

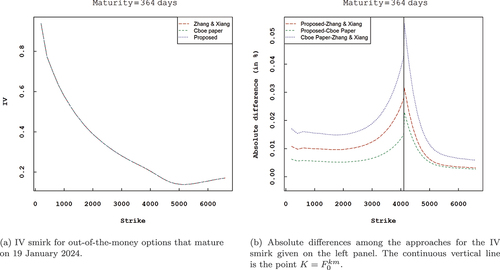

Figure 8. Comparison of the IV smirk for out-of-the-money options obtained from the three approaches for SPX call and put options that mature on 19 January 2024.