Abstract

There is a wide-spread and growing dissatisfaction with the relevance and usefulness of financial report information, particularly among investors and corporate executives. The dissatisfaction is corroborated by extensive research which consistently documents a growing gap between capital market indicators and financial information, more so for reported earnings. The reported earnings of most firms no longer reflect enterprise performance. I trace the deterioration of the usefulness of financial information to: (1) the abandonment by accounting standard-setters of the traditional income statement (matching) model in favour of a balance sheet (asset valuation) model, and (2) standard-setters’ failure to adjust asset recognition rules to the fundamental shift in corporate value-creating resources from tangible to intangible assets. I conclude this paper with change proposals to restore the usefulness of financial information to investors.

There is a widespread dissatisfaction with the relevance and usefulness of corporate financial report information to investors. The dissatisfaction is corroborated by empirical evidence which consistently documents a decreasing ability of financial information, and earnings in particular, to reflect enterprise performance, predict future performance, and explain share prices and returns. Surveys reveal that many financial executives believe that financial reporting has ‘degenerated’ into an ever-more-burdensome ‘compliance exercise,’ rather than an endeavour to inform stakeholders. Consequently, corporate executives, well-aware of the continuous loss of financial information relevance, increasingly disclose non-GAAP operating data (e.g. on the product pipeline of pharma and biotech companies, or detailed customer and churn data by Internet service providers, media & entertainment firms, and insurance enterprises), and provide alternative, non-GAAP earnings numbers by adjusting reported earnings and other financial data for various one-time items and questionable expenses, like assets and goodwill write-offs. Investors, too, routinely perform various adjustments to financial information (often called ‘Street earnings’) and increasingly seek more reliable and timely information sources for valuation purposes (like monthly same-store sales of retailers, or weekly prescription sales of Pharma companies). Regulators, in the US and abroad, also aware of financial reports’ loss of relevance, are continuously engaged in ‘financial reporting effectiveness’ projects aimed at enhancing financial information relevance and understandability.

The widespread and increasing dissatisfaction with financial information, corroborated by empirical evidence, is highly perplexing given almost half a century of concerted effort by accounting standards-setters (primarily FASB and IASB) to improve the usefulness and relevance of accounting and financial reporting to investors. Where is the improvement? It's definitely not showing up in the empirical research. We seem to have reached a regulatory impasse: More, and ever-more-complex new accounting and reporting rules – reflected, among other things, in the doubling of the length of financial reports in the past two decades, mostly due to the extended discussion of new accounting regulations (Dyer et al. Citation2017) – don't reverse, or even slow down the deterioration, both perceived and actual, of the relevance of financial information to investors. Evidently, there are fundamental obstacles to the improvement of financial information usefulness which current regulatory efforts fail to overcome, and perhaps even to recognise.

I address below this accounting impasse, and argue, based on empirical evidence, that the major reasons for the deterioration in financial information relevance are: (1) the shift of standard-setters during the 1980s from the traditional income statement approach, aimed at generating high-quality reported earnings by closely matching revenues with real expenses, to the so called balance sheet model, which emphasises assets and liability fair valuation, and, even more damaging, (2) a flawed application of the balance sheet (asset valuation) model during the dramatic shift of corporate value-creating resources from tangible to intangible assets, resulting in an increasing mismatch between revenues and expenses, and the absence of the most important, value-creating enterprise resources from the balance sheet. The result: A largely uninformative balance sheet, except, perhaps for those of financial firms, and an income statement which fails to live up to its major purpose: reflecting enterprise performance and the quality of management. In the final part of this study, I outline the corrective measures which, in my opinion, are capable of reversing the deterioration in financial information relevance.

I. The winter of our discontentFootnote1

No one seems to be satisfied these days with financial information, as evident by the following sample statements from those who know a thing or two about accounting:

‘FASB rules produce financial statements that virtually no one understands’ (the CEOs of the six largest accounting firms, Citation2006).

‘There is a strong feeling that financial reporting has hardened into a compliance exercise instead of evolving as a means to innovate and experiment to provide the best information to constituents’ (CFO survey, Dichev et al. Citation2013, p. 30).

‘There is a widely-held view that financial reporting disclosures need to be reformed … few people seem to be happy with the current position’ (Institute of Chartered Accountants of England and Wales Citation2013).

‘Some disclosure requirements are no longer necessary … there is a growing concern about disclosure overload … disclosure should benefit from a broader principles-based approach’ (SEC Citation2014).

‘The lack of transparency in financial reporting – especially when it occurs in financial institutions – creates a vicious cycle, with implications for investors’ trust and their willingness to invest’ (CFA Institute Citation2013).

‘Most elements of goodwill are highly uncertain and subjective and they often turn out to be illusory’ (Hoogervorst, IASB Chairman Citation2012).

And my all-time favourite, from the CFO of a large public US company:

‘My investors don't understand the accounting, nor do they care’ (Private communication).

Similar criticism of accounting and financial reporting in the US and abroad is often voiced by both preparers and users of financial reports and by capital market regulators. The criticism isn't, of course, new. Already in 1929, A.C. Littleton, an early, influential accounting thinker, was alarmed with the proliferation of subjective managerial estimates underlying financial information, and warned: ‘Accounting … is concerned only with realities … When accounting is loosed from this anchor of fact it is afloat upon a sea of psychological estimates which … are beyond the power of accounting, as such, to express’ (p. 150). What, I wonder, would Littleton say today about the proliferation of largely unreliable accounting estimates, such as ‘Level 3’ fair values, or assets and goodwill impairments populating financial reports? The ‘winter of discontent’ is indeed a long one with no end in sight, given the failure of standard-setters to reverse, or even slow down, the deterioration in financial information usefulness.

Perhaps, though, the dissatisfaction with financial reporting is just a common malaise: people grumble about the weather, politics, or their workplace, so why not about accounting? Criticism without substance? Far from it. In fact, solid empirical evidence indicates systemic failure of accounting rule-making, and highlights a continuous deterioration in the usefulness of financial information to investors, thereby corroborating the winter of accounting discontent.

II. Evidence supporting the discontent with financial information

A comprehensive survey of the empirical evidence, in the US and abroad, of the usefulness of financial information and the effectiveness of standard-setters is obviously beyond the confines of this study. Accordingly, I will focus on a few recent, rather comprehensive effectiveness studies.

A. Evaluating the FASB's impact

Khan et al. (Citation2017) recently examined the capital market impact of all the accounting standards issued by the FASB from its inception (1974) through 2009, and remarkably found that:

A full 75% of the 138 standards examined had no impact whatsoever on the share prices of the firms implementing the standards; while 13% of the standards were, in fact, associated with a shareholder value loss; and only 12% of the standards saw share price increases. Thus, at least from investors’ point of view, the first 25 years of FASB standard-setting was a series of non-events.

The more nuanced examination by the researchers was equally disturbing: The FASB standards associated with the largest shareholder value loss were those requiring significant managerial estimates – particularly the various fair value and asset impairment standards – and those that defy economic logic, primarily the R&D expensing standard (SFAS No. 2). Fair value and asset impairment standards were, of course, the primary focus of the FASB and IASB in the past two decades.

The research confirmed what most people maintain: Principle-based standards created more shareholder value than rules-based standards. However, given the recent FASB's 607-page super rules-based revenue recognition standard, and the equally complex and detailed 491-page new lease standard, the FASB and IASB can hardly be characterised as moving towards principles-based standard-setting.

These are disturbing findings indeed, but why is the capital market impact of accounting standard-setting a relevant test of regulators’ effectiveness? First, and foremost, because by the FASB's own declaration, investors are the primary intended users of financial reports.Footnote2 And if accounting standards are deemed useful by investors, they will react positively to the deliberation on and the enactment of the standards. Thus, for example, if the fair value standards indeed decrease investors’ cost of information search (e.g. rather than individual investors spending resources on adjusting historical costs of asset to current values, the firm reports credible current values on the balance sheet), and/or if the standards enhance the reliability (precision) of financial information, thereby decreasing investors’ ‘information risk,’ then the news that regulators are contemplating new fair value rules, and, particularly the actual enactment of the rules should be welcomed by investors of the impacted companies and reflected by share price increases. And that's exactly what Khan et al. (Citation2017) set to find out by tracing carefully the total impact of each FASB standard, from the first time investors learned about rule-makers’ intention to develop the standard through its final enactment, on the share prices of the firm's subject to the standards (e.g. R&D-intensive firms in the case of SFAS 2), compared with firms unaffected by the standards. Alas, the research findings, summarised above, failed to detect significant share price impacts (investors’ reaction) of essentially the entire 1974–2009 FASB's rule-making effort. (I will comment on the IASB market impact, shortly.)Footnote3

B. Empirical assessment of financial reporting usefulness

Perhaps the Khan et al. (Citation2017) adverse verdict is too hasty and harsh? Maybe the focus on share price reaction to standard-setters’ deliberations and decisions is too narrow? What if it takes more time for investors to comprehend the effectiveness of the new rules, and they do react to the new information only upon actual disclosure by firms and the incorporation of these disclosures by analysts in investment models? Obviously, expanding the scope of information usefulness analysis is called for, and that's what I did with my co-author Feng Gu, by using a wide array of statistical methodologies for assessing the impact and usefulness of US financial report information to investors (Lev and Gu Citation2016). Using a long, 60-year span of financial reporting history we examined: (1) The association between key financial report items with share prices and returns. This is the traditional, and still the most common methodology to assess the relevance of financial information to investors. It's simple and straightforward, but this approach suffers from a serious flaw: Association isn't necessarily causation, as everyone knows. Suppose, for example, that analysts revised their earnings forecasts for a certain firm two months before quarter-end, leading investors to adjust share prices accordingly. Three months later, the firm released its earnings which were largely in line with the forecasts. The firm's share price already impounds much of the earnings information from investors’ reaction to analysts’ forecast revision, and will, therefore, be highly ‘correlated’ with reported earnings, but the earnings release ‘came late to the game.’ Analysts’ forecast revisions, in fact, informed investors, long before the firm did. So, if the question is: Do financial reports provide timely, actionable information to investors, correlation studies will generally provide inflated results.

This led us to the second methodology: (2) A narrow-window (a few days around the financial report release) study of the impact of financial information on share prices, relative to other information sources, such as analyst's forecasts, firms’ non-accounting filings with the SEC, and managers’ guidance. This ‘event methodology’ provides a more reliable signal than association studies about the unique (incremental) contribution of financial information to investors. Still, it can be argued that share prices don't fully capture the usefulness of financial information (usefulness to creditors, say). We thus used a third approach: (3) Examining the ability of current and past earnings to predict future earnings; thereby testing directly the major use of earnings by investors: predicting future firm performance.Footnote4 (4) To cover all bases, we also examined the uncertainty or ambiguity of financial analysts – the expert users of financial information – about the future performance of companies, as reflected by the dispersion (variance) of analysts’ earnings forecasts around the consensus estimate. Finally, (5) we documented the changes over time in the informativeness of share prices about future firms’ performance. Obviously relevant and transparent financial information will render share prices more informative (predictive) about firms’ future performance. We thus used in the first part of The End of Accounting (2016) five different methodologies to assess financial report usefulness during the past 5–6 decades.

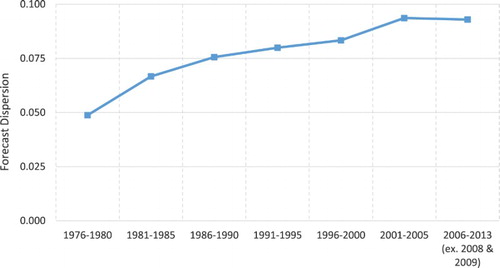

An example of our fourth methodology – examining the uncertainty (‘forecast dispersion’) of financial analysts about firms’ future performance – is reproduced above. The figure, based on all US companies followed by analysts, shows vividly that despite significant improvements in analysts’ access to technology and information, their uncertainty, or ambiguity about future firm performance is on the rise (to reduce the impact of abnormal years, we eliminated from the figure the particularly hard-to-predict 2008–2009 financial crisis years). Analysts’ main information source – financial reports – is at least partly to blame for their ambiguity increase ().

Figure 1. Analysts’ ambiguity on the rise. Five-year median analysts’ dispersion (standard deviation) around the consensus estimate, 1976–2013 (2008 and 2009 omitted). Source: Lev and Gu (Citation2016).

Notably, our comprehensive, multi-methodology, 60-year research into the usefulness to investors of financial report information yielded a surprisingly consistent, yet disheartening conclusion: Over the past half century, and particularly during the recent 2–3 decades, the usefulness of financial information has rapidly deteriorated. Intriguingly, our calculations indicate that currently, financial reports provide about 5% only of the information used by investors. While having a certain confirmatory value, financial reports are largely devoid of new, actionable information for investors. These obviously sobering findings are consistent with the ‘The Winter of Our Discontent’ (Section I), and are particularly disappointing given the substantial effort and cost (including auditing) of complying with accounting and reporting rules.Footnote5

C. And what about the narrative in financial reports?

Perhaps it's the discussion or narrative of financial reports (e.g. footnote disclosure, MD&A), rather than just the numbers, that clearly and faithfully inform investors about the performance and financial condition of business enterprises? No such luck, unfortunately. A burgeoning research ‘industry’ examining the readability and understandability of financial reports, using advanced linguistic software going by the newfangled names of ‘fog’ and ‘bog,’ yields a uniform conclusion: The clarity and understandability of financial reports is on a slippery slope. One study even concludes that financial reports are outright ‘unreadable’ (Bonsall et al. Citation2017), which, of course, is the experience of practically anyone who pours over these documents. The only aspect that ‘improves’ is the length of the reports: US financial reports more than doubled! in the past 20 years, mainly due to required elaboration on compliance with new accounting and reporting rules (Dyer et al. Citation2017). A text's length is of course positively correlated with increasing challenges to readability and understandability. And all this deterioration of narrative usefulness, despite the 1998 SEC extensive directive to enhance ‘plain English’ in financial reporting; the AICPA establishing in 2013 a centre for Plain English, and the FASB's designation of understandability as an important qualitative characteristic of financial reports. All, apparently to no avail.

Thus, the widespread investors’ and managers’ perceptions of serious deficiencies in financial reports (Section I) are strongly supported by comprehensive research documenting a deterioration in the usefulness to investors of financial information.Footnote6

III. IFRS's adoption impact

Much of the research on the usefulness of financial information uses US data, but most of the rest of the world adopted International Financial Reporting Standards (IFRS). Do IFRS-based financial reports provide investors with more useful information than GAAP reports? IFRS adoption is a relatively recent phenomenon, and, therefore, long-term studies of usefulness, like those of GAAP, are premature. But there is quite a voluminous research on the consequences of IFRS gradual adoption around the world. Most of the research focuses on the switch from prior, mostly inferior accounting rules in the various adopting countries to the uniform IFRS system. So, it's not surprising that several of the IFRS adoption studies report improvement in various aspects of information usefulness, such as the relation of financial variables with share prices, changes in discretionary accruals (suggesting the extent of earnings management), or analysts’ forecast accuracy. That is definitely a positive and welcome finding.

Surprisingly, however, a comprehensive survey of the IFRS adoption research effort provides a mixed verdict. Ahmed et al. (Citation2013) conducted a statistical meta-analysis – not your regular literature survey – of no fewer than 57 IFRS studies and report that:

‘ … the value relevance of book value of equity [namely, the balance sheet summary information] generally decreases [after IFRS adoption] but remains significant’ (p. 196). This is particularly intriguing, given the balance sheet model (more on this later) followed by both the IASB and the FASB.

Based on share price studies (regressing the levels of share prices on earnings), ‘ … the value relevance of earnings is highly significant with the significance increasing after IFRS adoption’ (p. 197). However, for the generally better-specified change regressions (stock returns on earnings changes): ‘We find a decrease in the value relevance of earnings … in the post-IFRS adoption period … (p. 206).

For discretionary accruals – a proxy for earnings management – studies: ‘The overall meta-analysis of 29 studies does not suggest that discretionary accruals reduce significantly post-IFRS adoption’ (p. 207). And lastly,

‘ … the results suggest that IFRS adoption is associated with an improvement in analysts’ earnings forecast accuracy’ (p. 208).

I conjecture that the improvement in analysts’ forecast accuracy has more to do with the increasing frequency of firms providing forward-looking information (earnings and revenue guidance) with their financial results than with IFRS adoption.Footnote7 The gradual adoption of IFRS across countries creates mechanically, I suspect, a spurious correlation between IFRS adoption and an improvement in analysts’ forecasts, where the latter is mainly due to the increasing disclosure of forward-looking information released with financial reports.Footnote8

The evidence on IFRS improvement over erstwhile accounting regimes is thus mixed, with the improvements being more pronounced in countries with effective regulatory and enforcement systems. Definitely good news. Regarding IFRS vs. GAAP, I am not familiar with studies which comprehensively compare trends in the informativeness and usefulness to investors of the two systems. I doubt, however, whether the current usefulness to investors of IFRS-based reports is substantially higher than GAAP-based reports, because at their core, the two accounting and reporting regimes are very similar, and getting increasingly so.Footnote9

Summarising, given the consistent research findings about the deteriorating usefulness of financial information and doubts about the effectiveness of accounting standard-setters’ work product, it's not surprising that widespread dissatisfaction with financial information lingers on. This protracted ‘Winter of Accounting Discontent’ raises the important question of why hasn't the extensive effort of well-meaning accounting regulators resulted in a noticeable improvement in the usefulness of financial report information? What are the stumbling blocks for such improvement? I turn next to this question.

IV. Reasons for the financial reporting relevance lost

The pervasive and protracted deficiencies of financial information can be mainly attributed, in my opinion, to two factors: (1) standard-setters’ switch in the 1980s from the traditional income statement (matching) model to the balance sheet model, and (2) their failure to adjust accounting and financial reporting to the dramatic change in the value-creating resources of business enterprises, from tangible to intangible assets. I will start with the switch of standard-setting models.

A. The traditional income statement (matching) model

The income statement model, operationalised by the careful matching of revenues with expenses, was defined and rationalised as early as 1940 by William Paton and A.C. Littleton (Citation1940) in their classic monograph, An Introduction to Corporate Accounting Standards, which ‘easily qualifies as the academic writing that has been most influential in accounting practice’ (Storey and Storey Citation1998, p. 28).Footnote10 Paton and Littleton put forward the fundamental premises of accounting as:

Periodic income determination is the central function of financial accounting – the business enterprise is viewed as an organisation designed to produce income,Footnote11 and

Accounting is not essentially a process of valuation, but the allocation of historical costs and revenues to the current and succeeding fiscal periods’ (p. 23, emphasis mine).

Paton and Littleton elaborated:

The fundamental problem of accounting, therefore, is the division of the stream of costs incurred between the present and the future in the process of measuring periodic income. The technical instruments used in reporting this division are the income statement and the balance sheet … . The income statement reports the assignment [of revenue and costs] to the current period; the balance sheet exhibits the costs incurred which are reasonably applicable to the years to come. (p. 67)

And why is proper revenue–cost matching so critical to the measurement of earnings? Because it determines the quality of earnings, namely the ability of current and past earnings to portray enterprise performance and predict future earnings – or cash flows – which is the major use of earnings by investors. The crucial importance of revenue–cost matching is not a relic of the past; when asked what are the accounting policies that are likely to produce high quality earnings, a full 92% of the CFOs surveyed in 2012 (highest response rate in the survey) said: ‘policies that match expenses with revenues.’Footnote12 Thus, the closer the revenue cost matching, the higher the quality of reported earnings. That's what we still teach students in Accounting 101.

If revenue–cost matching is a necessary condition for high quality earnings, which are obviously the focus of investors,Footnote13 and if investors are the main intended users of financial reports, as claimed by the FASB, then the income statement (matching) model should obviously be the guiding light of accounting standard-setting. This is a no-brainer, and yet, the FASB begged to differ.

B. The switch to the balance sheet model

From inception, FASB members viewed the matching principle with scepticism and unease, according to Storey and Storey (Citation1998), faithful chroniclers of the FASB thought process:

Many of the responses [to the mid-1970s R&D Discussion Memorandum] indeed were vague, and it soon became clear that proper matching and distortion of periodic net income were largely in the eye of the beholder … To Board members, the arguments for including in the balance sheet items that could not possibly qualify as assets or liabilities [deferred costs and revenues] … sounded a lot like excuses to justify smoothing of reported income, thereby decreasing its volatility. (p. 53)Footnote14

Those [matching] notions seemed to be open ended; no one could explain the limits, if any, on matching or nondistortion [of earnings] procedures or how to verify that proper matching or nondistortion has been achieved.Footnote15 The experience [with the R&D Discussion Memorandum] made most, if not all, Board members highly skeptical about arguments that the need for proper matching to avoid distortion of periodic net income was the ‘be-all and end-all of financial accounting’ with little or no concern expressed about whether the residuals left over after matching actually were assets or liabilities. Among other things, those early experiences had graphically demonstrated to Board members that once accountants had come to perceive assets primarily as deferred costs, they often failed to distinguish assets in the real world from the entries in the accounts and financial statements. (p. 62, emphasis mine)

The items in financial statements represent things and events in the real world, placing a premium on representational usefulness and verifiability of accounting information … . (Storey and Storey Citation1998, p. 71)

The fundamental elements of financial statements are assets and liabilities because all other elements depend on them. [And] Because liabilities depend on assets – liabilities are obligations to pay or deliver assets – assets are the most fundamental element of financial statements. (Storey and Storey Citation1998, p. 72)

Gone was the traditional emphasis on the matching process underlying reported earnings – still investors’ most highly sought item – replaced by a focus on the valuation of assets in accounting standard-setting, which relegates earnings to an outcome of the assets/liabilities’ valuation process. As expected, this drastic standard-setting shift didn't sit well with accounting constituents. After all, how many investment models and valuation methodologies are centred on assets? Very few, I venture. Indeed, as late as 1998, Storey and Storey (p. 83) lamented: ‘The revenue and expense view is still deeply ingrained in many accountants’ minds [and I would add: investors’ minds too], and their first reaction to an accounting problem is to think about “proper matching of costs and revenues.”’Footnote16 And: ‘ … that assets and liabilities are the fundamental elements of financial statements – still is undoubtedly the most controversial, and the most misunderstood and misrepresented, concept in the entire conceptual framework’ (p. 76). ‘Controversial,’ for sure and for very good reasons, but ‘misunderstood’? The balance sheet model isn't ‘string theory’ in physics, it's facile and straight forward. Misunderstanding isn't the real problem of the balance sheet model. The problem is a misguided focus on asset valuation while neglecting the revenue–cost matching which articulates the universal business model: expending resources in the process of generating revenues. Very few investors ask: ‘How did firm operations affect assets’ or liabilities’ values?’ Most are interested in how operations affected earnings.

Unhindered by the widespread preference of preparers and users for the income statement approach, the two Boards pursued vigorously the balance sheet model in accounting and reporting standard-setting.Footnote17 Most of the consequential standards enacted in the past quarter century – adjusting assets and liabilities to fair values, recognising impairments of assets and goodwill, etc. – focused on the valuation of assets and liabilities, particularly those of financial institutions, while the adverse impact of the fair value adjustments on the income statement – leading to mismatched revenues and costs – were largely ignored by standard-setters. These adverse income statement effects of the balance sheet approach could not, of course, be ignored by managers and investors. One of the most serious unintended consequences of the balance sheet approach is the proliferation of ‘non-GAAP earnings’ releases – by 90% of S&P 500 companies (USA Today, 2 February 2017) – which are primarily attempts by managers to cleanse reported earnings from transitory, one-time items created by the balance sheet approach, (e.g. goodwill and asset impairments).

C. Wait, aren't the balance sheet and income statement models identical?

Since, by definition, earnings (income) equal the periodic change in net assets (adjusted for capital flows), it shouldn't make any difference whether earnings are measured as the difference in the values of net assets at two points in time (the balance sheet approach), or directly by matching revenues to costs. So, what's all this agonising about the choice between the balance sheet and income statement approaches? Who cares?

Well, investors definitely care, because the choice between the income statement and balance sheet models is also a choice between the following two very different views of the purpose of reported earnings:

The balance sheet model: earnings reflect the change in net assets (equity) between two points in time (adjusted for capital changes).

The income statement model: earnings is an indicator of the periodic performance of the enterprise and the quality of its management, as measured by revenues matched to expenses.

The former (balance sheet) definition of earnings, widely known as ‘comprehensive income,’ assumes that earnings is a byproduct of the valuation of assets and liabilities, and therefore should reflect all the assets and liability changes, whether they are related to current enterprise performance or not. Thus, for example, goodwill write-off or restructuring costs recognised in a given period are often the consequences of past managerial blunders and have little to do with current or future enterprise performance.Footnote18 In contrast with the balance sheet approach to earnings measurement, the income statement-based earnings, derived by a process of carefully matching revenues recognised over the period with all the costs incurred in their generation, follow closely the business model of the enterprise. Such earnings faithfully reflect enterprise performance, and provide a solid basis for predicting future performance. As Dichev (Citation2017, p. 6) states:

… it [earnings derived from net assets change] obtains by construction but it has little real meaning … If one looks to find the economic roots of ‘where does income come from?’ the answer ‘from change in equity’ is not helpful. A better answer is that income comes from ‘earning more [adjusted] cash than what was invested,’ and that is the essence of the income statement approach … The logic of accounting should follow the logic of the business it reflects.

Not surprisingly, 92% of surveyed CFOs concur, stating that: ‘policies that match expenses with revenues’ are essential for high quality earnings (Dichev et al. Citation2013, Table 8, p. 20).

Some, primarily standard-setters, believe that one can get the ‘best of all worlds’ by following the valuation-based balance sheet approach, while designating in the income statement the unmatched, one-time items, thereby allowing investors to adjust reported earnings by eliminating these items. This is illusory on two levels: From a practical point of view, many unmatched income statement items are embedded in cost of sales and SG&A, rather than flagged as such in the income statement.Footnote19 Moreover, it has been shown that firms often ‘manage earnings’ by misdesignating various regular cost items as ‘one-time.’Footnote20 Investors are, therefore, unable to cleanse the income statement from many, valuation-related transitory items.

Abandoning the matching principle and dumping on the income statement a host of valuation-adjustment items, whether related to current performance or not, was bad enough. But this dwarfs compared with the damage to financial information from a major misapplication of the balance sheet (asset valuation) model: ignoring the most important value-creating resources of modern enterprises: intangible assets.

V. The perfect storm: while standard-setters took their eyes off the income statement, intangibles rose to strip the meaning of reported earnings

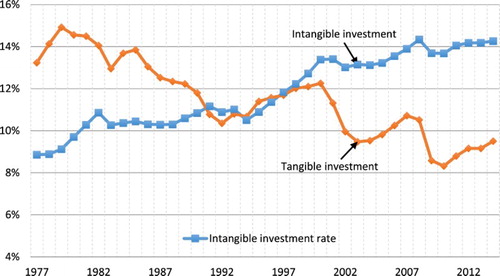

, based on Corrado et al. (Citation2009), and extended at my request, portrays the dramatic transformation of the productive resources of business enterprises during the past four decades: The aggregate investment of the US business sector in intangible assets (R&D and patents, computer software and digital systems, business designs and the Internet, brands and unique business processes, investment in human resources, etc.), has been rising dramatically, reaching, by Corrado and Hulten's estimates, the astounding amount of $2 trillion (yes, trillion) annually. In sharp contrast, business enterprises’ investment in tangible assets – those ‘fundamental elements,’ using the FASB's terminology, which are recognised on balance sheets – has been on a downward spiral, and the gap between the intangibles and tangible investment rates keeps growing.Footnote21 clearly reflects a fundamentally transformed economy, dominated by intangibles which are currently the prime value-creators of business enterprises.Footnote22 Tangible assets (plant, machinery, equipment, structures) are, by and large, ‘commodities,’ available to all competitors, and therefore rarely able to create value in a competitive environment. It is important to note that intangibles are the major resources of all competitive firms, not just high tech and science-based enterprises. Brands and trademarks are the major assets of durable and nondurable (e.g. Coca-Cola) manufacturers, IT systems enable the unique business processes of telecom, Internet service providers, and media and entertainment companies, and new product development (service sector R&D) distinguishes successful financial firms from laggards. Intangibles are literally everywhere in the business world.

Figure 2. The intangibles revolution. US private sector investment in tangible and intangible capital (relative to gross value added), 1977–2014. Source: Courtesy of Corrado and Hulten.

The well-known deficient accounting treatment of intangibles – expensing internally generated intangible investments, while capitalising the functionally identical acquired intangibles – decreases substantially the usefulness of reported earnings as a measure of performance and value creation, as the following evidence shows.Footnote23 And all this occurred while standard-setters took their eyes off the income statement focusing on the fair values of assets. Ironically, the wrong assets.

VI. Intangibles up, earnings usefulness down

Dichev and Tang (Citation2008) examined the extent of revenue–cost matching in income statements. Adequate matching, crucial to the quality of earnings, manifests itself in a high contemporaneous correlation between revenues and expenses, whereas poor matching (income statement expenses unrelated to revenues, and vice versa) detracts from the revenue–cost correlation. Computing the 40-year (up to 2003) annual revenue–cost correlations of the 1000 largest US firms, the researchers reported: ‘ … a clear and economically substantial trend of declining contemporaneous correlation between revenues and expenses’ (p. 1425). The adverse impact of this decline on the quality of earnings was, according to Dichev and Tang, serious:

Earnings volatility has nearly doubled while the underlying volatilities of revenues and expenses have remained roughly the same [meaning that it's not macro or industry revenue or expense volatility increases that raised earnings volatility; rather it's the self-inflicted deteriorating matching that did the damage]. Earnings persistence [a necessary condition for the ability of earnings to predict firm performance] has substantially declined from [an intertemporal earnings association of] 0.91 to 0.65 during this period. (p. 1426)

Thus, the abandonment of the income statement (matching) model by standard setters had serious consequences, leading Dichev and Tang to conclude:

… if investors use reported earnings primarily to assess firms’ long-run profitability, the temporal trends identified in this study suggest that earnings have become considerably less useful in that regard over the last 40 years. In addition, the prevailing philosophy and the specific current agenda of both the FASB and IASB suggest that this trend is going to continue, and thus a future in which reported earnings have evolved into something which is divorced from their classic role as a gauge of long-term value looks highly probable in the next 30 to 50 years. (pp. 1426–1427)

I concur, as my research indicates that reported earnings are already largely divorced from long-term value changes (Lev and Gu Citation2016).

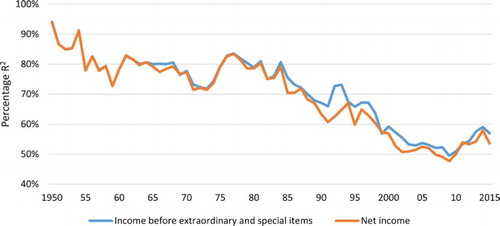

What caused the deterioration in the revenue–cost matching and the quality of earnings: the proliferation of one-time items in the income statement, resulting from the fair value and impairment standards, or the failure of standard-setters to adjust accounting to the fundamental economic changes portrayed by ? Dichev and Tang dismiss the first cause: ‘First, we find that the same pattern of results [declining matching] exists after controlling for the well-known large temporal increase in the frequency of one-time items and losses’ (1426). A similar view of the impact of one-time items on earnings usefulness is obtained from the R2 of annual regressions of market values on earnings, which is reported in . The patterns of decreasing R2s for reported earnings and those adjusted by eliminating special and extraordinary (one-time) items evidently are very similar. So, while a nuisance, one-time items are not the major cause of the revenue–cost (matching) deterioration, and the consequent earnings relevance lost.

Figure 3. One-time items are not the cause of the deteriorating relation between earnings and market values.

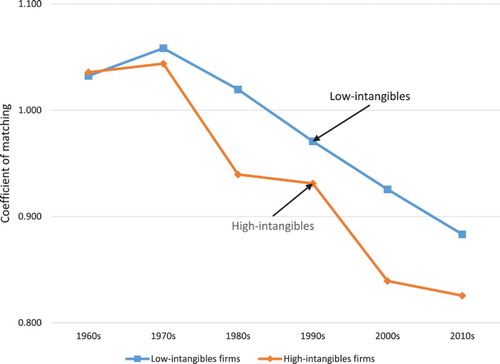

As made clear by , the intensity of intangible investments, expensed in the income statement, is the major reason for the deteriorating revenue–cost matching and the consequent quality of earnings decline.Footnote24 portrays the cross-sectional annual revenue–cost correlations (cost = revenues minus earnings) for the 1000 largest US firms classified by intangibles intensity: firms with above-industry median R&D + SG&A over sales ratios, and those with below-industry median R&D + SG&A over sales ratios.Footnote25 It is evident from that while the revenue–cost correlations (matching) of both groups were fast deteriorating over the past five decades, the correlations of intangibles-intensive firms are consistently and substantially lower than those of less intangible-intensive firms. It is thus the indiscriminate expensing of intangibles in the income statement that adversely affects earnings message and quality.Footnote26

Figure 4. Declining matching between revenue and expenses over time: Low-intangibles vs. high-intangibles firms.

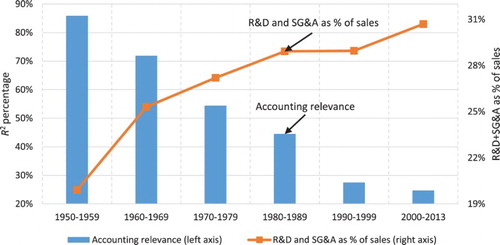

Finally, a different perspective of the impact of intangibles on financial information relevance is portrayed in (from The End of Accounting, 2016). Feng Gu and I linked directly the increase in intangible investment (proxied by R&D and SG&A expenses) to the relevance of earnings and book values to investors. portrays the average R2s from annual regressions of firms’ market values on the earnings and book values of US firms becoming public in each of the past six decades: the 1950s, 1960s, 1970s … , 2000s. The upward-sloping curve in portrays the increasing intangibles-intensity of successive vintages of new firms entering the market, while the fast-decreasing bars indicate the consequent decline in the relation between market values and the two key financial report variables: earnings and book values. This then is a major reason for financial reports’ relevance lost: The failure of asset-focused standard-setters to recognise the major value-creating assets of twenty-first-century enterprises.Footnote27 But intangibles are not the only reason for financial reports’ relevance lost. Keep reading please.

Figure 5. R2s of regressions of market values on earnings and book values of companies entering the public market in successive decades, 1950–2013. Source: Lev and Gu (Citation2016).

VII. Accounting: fact or fiction

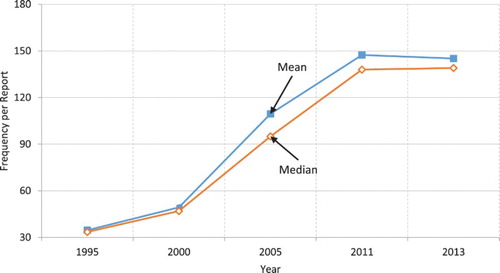

As if the damage to the usefulness of financial information from the indiscriminant expensing of intangibles was not enough, the increasing proliferation of subjective managerial estimates and projections in financial reports – a direct consequence of standard-setters’ focus on the fair valuation of assets and liabilities – eroded further financial information relevance. Recall A.C. Littleton’s Citation1929 warning mentioned earlier: ‘When accounting is loosed from this anchor of fact it is afloat upon a sea of psychological [subjective] estimates which … are beyond the power of accounting, as such, to express.’ And I would add: afloat upon a sea of frequently manipulated estimates.Footnote28 Standard setters’ shift to the balance sheet model, with the valuation of assets and liabilities at its core, increased exponentially the number and impact of subjective managerial estimates and projections underlying financial information. , from Lev and Gu (Citation2016), portrays the mean and median number of mentions of the term estimates and related terms (assumptions, forecasts, etc.) in the financial reports of S&P 500 companies.Footnote29 The five-fold increase in the frequency of estimates mentioning in the reports, from 30 per firm in 1995 to 150 in 2013, is the obvious outcome of pursuing the balance sheet model of fair valuation.

Figure 6. Increasing frequency of estimates-related terms in financial reports. For a sample of 50 S&P 500 companies. Source: Lev and Gu (Citation2016).

Standard-setters are, of course, aware of the proliferation of estimates in financial reports: ‘To a large extent, financial reports are based on estimates, judgements, and models rather than exact depictions’ (FASB Concept No. 8, Citation2010, p. 3). They require that estimates be described as such in the reports, that the nature and limitation of the estimation process be explained, and that no errors are made in selecting an appropriate process for developing the estimates. But these requirements primarily deal with representation issues, and don't mitigate the adverse consequences of accounting estimates on the quality of financial information. Estimates increase the noise and error in financial information, particularly when they are made by persons (i.e. managers) having strong incentives to affect the perceptions of investors. The fact that the impact of estimates on key financial report variables, such as sales and earnings, is not disclosed,Footnote30 and that investors are unable to verify ex post the accuracy of most financial report estimates – no data on realisations are provided for most estimates – decrease significantly managers’ incentives to carefully develop and use high quality and unbiased estimates.Footnote31

No wonder then, that the evidence directly links the frequency of accounting estimates to the decreasing quality of financial information. Thus, for example, Sloan (Citation1996) reports that the estimates-intensive accruals portion of earnings has a substantially lower association with future earnings (i.e. is less predictive of earnings) than the cash portion of earnings. Chen and Li (Citation2017) note that the financial report items with the largest number of underlying estimates are, not surprisingly, those related to fair values of assets, and report that the estimates-based accruals map less accurately into past, current, and future cash flows than the cash component of earnings. The researchers also report a lower association between current and future earnings (lower earnings persistence) for firms with a greater amount of financial report estimation, and a lower mapping of accruals to future cash flows. Thus, accounting estimates adversely impact the quality of earnings. In support, Lev and Gu (Citation2016, pp. 100–101) report that predicting future earnings from current and past earnings is less accurate for firms with an above-median number of estimates mentioning than for firms with a below-median number of estimates. Finally, a different perspective on the adverse effect of the proliferation of accounting estimates on the quality of financial information is provided by Roh (Citation2017), who examined the relation between the frequency of the use of estimates and related terms in financial reports (in the MD&A and footnotes of annual reports) and the informativeness of share prices, namely the ability of share prices to predict future firm performance. Roh concludes that greater intensity of estimation in financial reports is associated with a lower share price informativeness.. The evidence thus indicates that accounting estimates detract from earnings quality; particularly from earnings’ ability to predict future earnings and cash flows, thereby lowering the informativeness (efficiency) of share prices.

I do not suggest, of course, to eliminate all estimates from financial reports. Some estimates, like the bad debt or warranties provisions, can be reasonably reliable, if based on solid historical data and modified by unbiased forecasts of economic changes. Many other estimates, however, like the fair values of non-traded assets, or the impairment of assets and particularly of goodwill, are often no better than mere guesses, and are prone to manipulation. Standard-setters’ acknowledgement that ‘ … financial reports are based on estimates, judgements, and models … ’ does not mitigate their adverse effect on the usefulness of financial information. I will have more to say about estimates in the next section.

Summarising Sections VI and VII, the wide-spread dissatisfaction of preparers and users with financial information, consistent with the empirically proven decline in the usefulness to investors of this information, and of reported earnings in particular, are attributed, in my opinion, to a combination of self-inflicted wounds: (1) Standard-setters’ abandonment of the income statement rule-making model and its operating principle: revenue–cost matching, exacerbated by their failure to recognise the dramatic shift of corporate productive resources from tangible to intangible assets. The indiscriminant expensing of the latter largely stripped reported earnings of their ability to inform on enterprise performance and signal managerial capabilities. (2) Standard-setters’ shift to the balance sheet model, which increased exponentially the number and impact of subjective managerial estimates underlying financial information. A fair number of these estimates are of low quality and are sometimes manipulated, further eroding the usefulness of financial information. A sad state of accounting affairs, to be sure, but can anything be done about it?

VIII. Restoring the usefulness of financial information

Here are, in brief, my proposals for restoring the value-relevance of financial information to investors: (1) Improve the revenue–cost matching in the income statement by capitalising and amortising expenditures on value-creating assets (to be discussed in this section), and (2) Taking measures to enhance the reliability of accounting estimates (Section IX).

A. Veering back towards the income statement (matching) model

There is no denying that the income statement, and its bottom line in particular, are at the core of investors’ attention and interest. With the exception of short-term lenders, few investors are concerned with the current (fair) values of assets and liabilities, particularly so for nonfinancial enterprises, comprising 80–85% of the US economy.Footnote32 This then calls for a serious reassessment of the balance sheet model pursued for three decades by accounting standard-setters. Surely, no additional tweaking of the fair values of asset or expanded impairment rules – which, the evidence shows, cause the largest loss of value to shareholders (Khan et al. Citation2017) and generate the highest number of accounting estimates (Chen and Li Citation2017) – will reverse the decline in financial report relevance to investors.

I am aware, of course, that standard-setters contend that the balance sheet approach is a useful and disciplined guide to accounting rule-making not only because it enhances the relevance of the balance sheet, but also because it improves the measurement of earnings. If that were the case, then the relevance of reported earnings to investors should have increased over the past three decades. Alas, I am not familiar with a single study reporting an earnings usefulness increase, or even no decrease. Practically all the available evidence, some of which I have presented above, indicates a deterioration in earnings usefulness to investors. Given such consistent evidence, a veering back of accounting rule-making towards the income statement model and its matching operating principle is called for.Footnote33

B. Improving the revenue–cost matching

To recap: The overriding objective of the matching principle is to assure the reporting of high quality earnings, namely an earnings figure which will faithfully reflect the enterprise's periodic performance and managers’ capabilities, as well as provide a solid basis for predicting future enterprise performance – the main use of reported earnings by investors. For many firms, these objectives are not met by currently reported earnings, due to an increasing revenue–cost mismatch.Footnote34 There is obviously a sharp disconnect between Tesla's $336 million second-quarter 2017 loss (almost $3 billion accumulated losses), and its current market value of about $50 billion, as well as a strong vote of confidence by institutional (sophisticated) investors evidenced by a 62% ownership. Or, the less known Kite Pharma, reporting $630 million accumulated losses (mainly from R&D expensing), and its recent acquisition by Gilead Sciences, a leading biotech company, for $12 billion. Obviously, investors don't consider these massive accounting losses, due to the expensing of long-term investments, as an indication of corporate value change or future performance. And this applies not only to early-stage firms: The 23-year old Amazon missed over the past five years almost half of the quarterly analyst consensus forecasts, while becoming one of the most valuable firms in the world. Uninformative accounting earnings to be sure.

I therefore propose a substantive rule change required to restore matching in the income statement: Firms’ expenditures on identifiable long-term investments (R&D, IT, customer acquisition costs, etc.) should be capitalised and amortised, thereby eliminating these investments in growth from the income statement, simply because there are no current revenues to match against them.

My proposed criteria for intangibles capitalisation are:

The entity has a legal ownership of the intangible through patents, copyrights, trademarks, etc., or has a sole access to the intangible (namely, can restrict others from using the intangible) through a proprietary development process (e.g. internal R&D).

The intangible is scarce, that is, in limited supply (e.g. wireless spectrum), and competitors cannot easily copy or imitate it.

The intangible is expected, under normal circumstances, to produce benefits, either directly (like licensed patents) or indirectly, alone, or in combination with other firm resources.

The entity is able to identify the investment (expenditure) in the intangible.

The fourth criterion excludes from capitalisation certain intangibles, particularly those related to ‘organisational capital’ – the value-creating business processes and procedures, like Amazon's and Netflix's widely successful customer recommendation algorithms – because the expenditures related to their development are difficult to trace. Same with on-the-job employee training, and most ‘big data’ developments. So, the capitalised intangibles under my proposal should be restricted to those whose expenditures are clearly identifiable.

Along with the proposed capitalisation of certain intangibles, there should be a considerable enhancement of the disclosure of investments in long-term, value-creating assets. Currently, there is an inexplicable ‘conspiracy of silence’ concerning these investments. With the exception of R&D, all other expenditures on intangibles (IT, brand enhancement, employee training, artistic designs, etc.) are ‘buried’ in SG&A and cost of sales items. Go figure: investment in tangible capital is clearly disclosed, while the far more consequential investment in, say, IT is concealed from investors. Shining light on these crucial innovative activities will significantly improve investors’ information.

Limited-life capitalised intangibles on the balance sheet should, of course, be subject to periodic amortisation and impairment rules. The frequently capitalised acquired intangibles provide useful, time-tested industry amortisation standards. Thus, for example, Cisco Systems’ 2016 report specifies the following useful lives of its acquired intangibles: Technology – 5 years, Customer Lists – 6–7 years, Others – 2–3 years, and In-Process R&D – 10–11 years. I doubt whether such industry-based intangibles amortisation rates are less reliable than those that are currently applied to fixed assets, such as electronic equipment, which are subject to unforeseen technological changes. In extreme cases of a total loss, such as when the firm's asset is disrupted by a new technology, a write-off will be called for, as is applied now to goodwill.

My proposal is similar to Ohlson’s (Citation2006) earnings model. Ohlson identifies the ‘problems inherent in GAAP to be avoided’ (pp. 272–273) as: the existence of nonrecurring or special charges in the income statement, inconsistent and arbitrary capitalisation rules, arbitrary complexity inherent in certain standards, and the ambiguous concept of ‘other comprehensive income.’ A mouthful of accounting problems, indeed. He then advances various sensible change proposals to improve the income statement, the most radical, and the closest to my proposal is:

Capitalize and expense [amortize] the [future] sales sustaining expenditures: … In terms of the balance sheet, we introduce a ‘master account’ of unamortized Sales Sustaining Expenditures. Thus, there is full consistency as to the balance sheet and the income statement. (p. 276)

Important to note: there is no pretence in Ohlson's and my proposal that the capitalised value-creating (‘sales sustaining’) investments on the balance sheet represent the fair or current values of these asset. Indeed, some of these capitalised expenditures may not even have a realisation value. The proposed intangibles capitalisation is just a tool to achieve a better matching in the income statement, the overriding concern of accounting, in my, and most investors’ opinion. I am aware, of course, that current standard-setters will be uneasy, to put it mildly, with balance sheet assets having no fair values. But this is what it takes to restore the relevance of the income statement. And since the capitalised assets will be clearly identified as ‘deferred costs’ on the balance sheet, investors questioning their validity or value could easily ignore them (subtract from equity), as many do now with goodwill.Footnote35 There is also nothing novel in presenting capitalised expenses and revenues on the balance sheet. Current balance sheets often contain multiple capitalised items, such as prepaid expenses and deferred revenues, among other assets and liabilities. Most importantly, irrespective of whether investors will consider the capitalised long-term investments on par with other assets, or not, they will definitely find the new reported, properly matched earnings a vast improvement over current GAAP earnings in terms of performance evaluation and the prediction of future enterprise performance.Footnote36

C. Intangibles capitalisation is consistent with standard-setters’ asset definition

My proposal to capitalise and amortise value-creating investments is perfectly consistent with the Boards’ (FASB, IASB) asset definition. The most recent definition (2010), tentatively adopted by the Boards is as follows:Footnote37

Asset definition. The Boards have tentatively adopted the following working definition of an asset: An asset of an entity is a present economic resource to which the entity has a right or other access that others do not have … An economic resource is something that is scarce and capable of producing cash inflows or reducing cash outflows, directly or indirectly, alone or together with other economic resources.

Fixed capital, of which the characteristic is, that it affords a revenue or profit … , included machines, buildings, land and ‘the acquired and useful abilities’ of individuals. (Citation1976, p. 282)Footnote38

Note Adam Smith's inclusion of human capital in his definition which opens the door to include other intangibles in the definition of assets.

My proposed capitalisation of value-creating investments (mostly intangibles) is thus perfectly consistent with the Boards’ asset definition. To emphasise this point, consider the following – currently expensed – expenditures:

Internally generated patents and copyrights

Internally developed information technology (software)

developing ‘big data’ on customers

designing unique business processes (e.g. Amazon's recommendation algorithms)

internally generated customer lists

customer acquisition costs of telecom and Internet-services providers

All of the above intangibles are controlled by the enterprise and their access or use by competitors is restricted. And all of the above are scarce (in limited supply), and they are definitely capable of generating cash flows or reducing cash outflows, alone or with other assets. They are definitely consistent with the Boards’ asset definition

The above and similar intangible investments even comply with the requirement of ‘probable benefits’ dropped from previous asset definitions. Why would rational managers massively invest in these intangibles if their benefits were not probable? Unlikely benefits mean a negative present value of cash flow. So I am not breaking new grounds with my capitalisation proposal – it's perfectly consistent with the fundamental asset definition of the currently asset-focused standard-setters.

D. Supporting empirical evidence

Given the near uniformity of fundamental accounting and reporting rules across developed economies, and the virtual absence of any experimentation (trial and error) in accounting standard-setting, the empirical examination of alternative accounting rules is severely restricted. My proposed intangibles capitalisation is, however, a rare exception since important lessons can be learned from the first step taken by the IASB in requiring the capitalisation of development costs, under several conditions (project passing a feasibility test, availability of funds for project completion, etc.). The early research on these IFRS capitalisations is definitely encouraging. For example, Chen et al. (Citation2017), comparing Israeli firms which capitalised R&D under IFRS with US-listed Israeli firms which expensed all R&D under GAAP, conclude: (1) The capitalised R&D on the balance sheet is considered an asset by investors (it is highly correlated with market values), laying to rest the oft-heard argument that capitalised intangible costs will be ignored by investors, and (2) R&D capitalising firms voluntarily disclose to investors valuable R&D-related information collected in the process of testing for capitalisation (e.g. on the products’ target market, or the sufficiency of funds for completion), and the extent of this voluntary disclosure was substantially larger for R&D capitalisers than for the R&D expensing GAAP firms. Dinh et al. (Citation2016) report that some firms strategically capitalise R&D to beat earnings targets, like analyst forecasts. Reassuringly, however, investors see through these manipulations and disregard those capitalised R&D costs. Importantly, the researchers find: ‘On the other hand, the market values R&D capitalisation positively for well-performing firms, for which capitalisation does not matter to beat an earnings benchmark (about half of the overall sample)’ (p. 373). Oswald et al. (Citation2017), examining R&D capitalisation under IFRS in the UK, conclude:

In summary, we find that R&D capitalization has information value, confirming Healy et al.’s (Citation2002) simulation analysis. In other words, R&D capitalization passes the relevance vs. objectivity trade-off. An important source of capitalization's information is the decomposition of R&D expenditures into their capitalized vs. expensed components … (Abstract)

Thus, the early experience with IFRS development cost capitalisation rule is encouraging and supports my intangibles capitalisation proposal.

E. Finally, debunking widespread misconceptions

The accounting for intangibles has been debated for decades, with strong opinions on both sides (expensing vs. capitalisation). Over the years I encountered several widespread objections to intangibles capitalisation which I address below.

Standard-setters tread lightly on intangibles presumably because the fair values of these assets are not readily ascertained. True, there are no organised markets in intangibles,Footnote39 and comparables (like in ‘Level 2 assets’) are hard to come by because most intangible are unique to their owners (Pfizer's drug patents bear no resemblance to Merck's). But this shouldn't be an excuse for inaction on the accounting for intangibles. As I made clear above, the main purpose of changing the accounting for intangibles is to improve the revenue–cost matching in the income statement, and this requires only the capitalisation (and amortisation) of intangibles. No fair values are called for. Perhaps, in time, given the rapid growth of intangible assets, organised markets in intangibles will develop and fair values will become available, but there is no need to wait for that. As for the balance sheet, even the capitalised values of intangibles will be an improvement over today's void (zero values). Profitability ratios, like ROE and ROA, will become much more meaningful when the denominators include capitalised intangibles.

Another excuse for inaction on the accounting for intangibles is based on the argument that while the balance sheet doesn't reflect the values of internally generated intangible assets, both the investment in (e.g. R&D) and the output of intangibles are fully reflected in the income statement. So, no harm done by expensing intangibles, say the supporters of the status quo. That's, of course, a misconception. If income statements were prepared once, say, in 20 years, then the total investment in intangibles (expensed R&D, information technology, brand investments, etc.) would be matched with the 20-year revenues from these investments. Alas, income statements are prepared quarterly and the mismatch between the expensed intangibles, whose benefits will accrue in future periods, and the recognised quarterly revenues from past investments, is glaring and seriously detrimental to the quality of earnings.Footnote40 Add to this the serious inconsistency created by the current requirement to capitalise and amortise acquired intangibles, whereas the functionally identical internally generated intangibles are immediately expensed. Consequently, the financial performance of firms in the same industry following different innovation strategies – internal generation vs. acquisition – cannot be meaningfully compared. Thus, the argument that current financial reports provide adequate information on intangibles to investors is vacuous.Footnote41

‘But intangibles are uncertain’ say the status quo advocates. That's true. Not only are the benefits of most intangible investments uncertain, some of these investments are even sunk costs when they fail. Nothing left to recover. Intangibles are definitely different from tangible assets. But note, certainty of benefits is not a requirement by standard-setters of asset recognition. Moreover, uncertainty is a matter of degree. Most technology-based tangible assets (computer hardware, robots, laboratory equipment, etc.) are subject to frequent and unforeseen technological disruption, causing considerable uncertainty and even sunk costs. So, I don't believe that the higher uncertainty of intangible investments should disqualify them from capitalisation.

IX. Enhancing the reliability of accounting estimates

Currently, there are no effective incentives for managers to spend time and resources on generating high quality and unbiased estimates for the calculation of assets and earnings values. The ex post realisations of most estimates are not reported to investors, and managers are not required to explain the deviations between estimates and realisations. No responsibility for misestimation – intended or inadvertent – is a recipe for unreliable estimates.

Years ago, Lundholm (Citation1999) proposed a sensible and easy to implement procedure to enhance significantly the incentives of managers to generate reliable and unbiased (nonmanipulated) estimates and projections: Require firms to periodically provide a comparison of the five-seven key estimates that had the largest impact on earnings with subsequent realisations (facts).Footnote42 Managers will obviously be asked to explain large and particularly persistent misestimations (e.g. a bad debt expense that was lower every quarter than the respective write-off), a highly embarrassing task, and obviously harmful to managers’ credibility. Imagine the strong incentives for serious and honest estimation created by Lundholm's requirement. Surprisingly, such a sensible change proposal was never implemented. Time to adopt Lundholm's proposal, despite the expected opposition by some managers.Footnote43

X. Concluding observations

I conclude the paper with several general observations related to the issues raised above: (1) The evidence-based decline in the usefulness and relevance of financial information, (2) the major causes of this relevance lost which are rooted in standard-setters’ guiding models and practices, and (3) my suggested remedies to restore the relevance of financial information.

A. Externalities of financial reports’ relevance lost

Financial reports are aimed at informing investors, big and small, active and passive, about the periodic performance of enterprises and their financial condition, as well as enabling investors and other stakeholders to monitor the activities and capabilities of managers. As such, financial reports should contribute significantly to capital market efficiency and the optimality of investors’ and firms’ funds allocations. Current financial reports, regrettably, fall far short of achieving these lofty objectives.

As I have shown above, the reported earnings of most firms fail to reflect real enterprise performance, balance sheets are still a mixed bag of historical, fair, and some highly questionable (e.g. goodwill) values, and the narrative of financial reports is increasingly complex, confusing, and sometimes misleading. No wonder that the evidence consistently shows an increasing chasm between market values and financial data. Investors abandon financial information (by Lev and Gu’s (Citation2016, p. 45) estimate, financial reports provide about 5% of investors’ total information).

This wouldn't have mattered much if there were readily available, low cost alternatives to financial reports. But, as the evidence on the increasing ambiguity of financial analysts () and the decreasing informativeness of share prices shows, alternative, comprehensive information systems are not available. This leads to seriously adverse consequences:

Corporate managers, being well aware of the deteriorating usefulness of financial information, increasingly resort to the publication of non-GAAP earnings and a plethora of operational data (e.g. the product pipeline of pharma and biotech companies, or customer data for telecom, Internet, and media firms). This could have been a good thing, but the current non-GAAP disclosures are inconsistent across firms and time, unaudited, and sometimes even manipulated. As such, these non-GAAP disclosures are of limited use to investors, and definitely don't fill the information void created by the relevance-challenged financial reports.

Moreover, accounting-based financial information is often used for managerial decisions: mergers & acquisitions, corporate restructuring, or compensating employees. Unless properly adjusted, the deeply flawed financial information likely adversely affects the quality and consequences of these managerial decisions.

Analysts and fund managers still rely on earnings-centred valuation models. Their complex spreadsheets are aimed at predicting earnings, and they actively seek earnings guidance from managers. But this is a futile exercise since reported earnings, by and large, no longer reflect enterprise performance and value changes. The proof: In a recent paper, Feng Gu and I (Citation2017) showed that even a perfect prediction of quarterly consensus hits and beats does not yield much these days. The likely consequences of these accounting-based valuation models are poor investment decisions, consistent with recent years’ flight of funds from managed to index funds.

Securities valuation models, as well as business school valuation courses, should shift, in my opinion, from the decades old (essentially, since Ben Graham in the 1930s) and largely obsolete earnings-centred methodologies to a systematic valuation of the investment in and performance of the value-creating, strategic assets of businesses (patents, brands, customer franchise, etc.), as outlined in Gu and Lev's ‘Time to Change Your Investment Model’ (Citation2017).

Financial reports were supposed to be the ‘big equaliser’ across investors, levelling their playing field. The current largely uninformative and obscure financial reports hurt particularly individual investors. Big money and fund managers can overcome some of the reports’ deficiencies by heavily investing in alternative information search and analysis, and by securing privileged access to management, leaving all other investors at a great disadvantage. Rational individuals in this case will obviously withdraw from active investment, opting for index funds or alternative investments.

Given such harmful consequences and the fact that there are no good alternatives to relevant financial reports, considerable efforts should be aimed at restoring the usefulness and effectiveness of these reports, which is the main purpose of this paper.

B. New research approaches

Financial report usefulness research primarily relies on associations between capital market indicators and financial statement variables. It seems that we are close to exhausting this ‘low hanging fruit’ methodology. Time has come to expand the scope of research and explore new, deeper approaches to gauging the relevance of accounting and financial reporting to investors and other constituents, as well as proposing substantive changes to the accounting system. Here are some interesting areas worth exploring:

Changing accounting standard-setting. The FASB is approaching the mature age of 45, and the IASB isn't much younger. They are operating without major changes since inception. Time to explore new approaches to revitalise accounting standard setting.

For example, by and large, accounting standards, even demonstrably poor ones like the R&D expensing rule, are enacted and rarely terminated. We should consider experimentation – trial and error – in standard setting, like controlled experiments where certain firms implement a new accounting rule while a control group doesn't implement it. Over a certain period, the impact and consequences of the new rule will be evaluated against the control group, and the rule will be either generally applied, modified, or abandoned. Other approaches to invigorate the accounting standard-setting process like ‘natural experiments,’ which gains momentum in economics, should be explored.

New reporting modes and structures. Hard to believe, but the current reporting system of a balance sheet and an income statement is centuries old, unaffected by the revolutionary changes in communication and information technology. Aren't there more effective modes of reporting on business activities and conditions? I am aware of only one serious proposal for change in recent decades: Ijri's thought provoking proposal of momentum accounting and triple-entry bookkeeping (Citation1989). Regrettably, this proposal was never seriously considered by standard-setters, and is now largely forgotten. It is time to vigorously explore new modes and techniques for financial communication with investors. A wild speculation: In the spirit of ‘open source,’ perhaps we don't need standard financial reporting anymore, just allow investors to access firm fundamental information data, securing, of course, certain highly confidential databases.

Who is using financial information? This has been a mystery to me for quite some time. Investors’ funds are constantly flowing from active to passive management, which must decrease substantially the demand for financial information. Given the size, complexity, and obscurity of financial reports, I cannot imagine any individual investors delving into them. Sophisticated investors are increasingly using more relevant and accurate information sources, such as weekly prescription sales by drugstores, or satellite imaging of retailers’ parking lots to assess demand. So who is a serious user of financial reports? A few financial analysts? Who is benefitting from the activities of the FASB, IASB, PCAOB, and the armies of auditors? Is the financial report user an endangered species? We need answers to these questions, but no one seems to care.

Why the complacency? The deficiencies of financial information are obvious and increasing, and yet, there is no outcry for change from executives, investors, or accountants. These constituencies seem complacent with the status quo, perhaps even preferring, in the case of executives, the current lack of financial transparency. This raises interesting questions: Why don't the accounting constituents – managers, investors, accountants – actively strive to improve financial reporting? Are accounting regulators ‘captured’ by the regulated? And most importantly: where will the necessary change come from? Who may be the agents of change? And why isn't there a public debate about the adequacy of financial information and regulation similar to the vigorous debates about other regulatory systems (environmental, food and drug, etc.)? Why the public apathy concerning accounting and financial reporting?

C. And what about us, academics?

We, accounting researchers, by and large, stand on the sidelines of the most important activity in accounting: standard-setting. We prefer to investigate more ‘glamorous’ issues, like corporate governance, managerial compensation, debt contracting, or the perennial earnings management. Here and there, an accounting standard is empirically examined – usually by recording investors’ reaction to the new information – but this is ‘too little, too late.’ I am not aware of a single case where such ‘regulatory research’ (including mine) led to a rule change.

It is as if legal scholars would avoid research on the effectiveness and consequences of new legislation, or economists shying away from investigating environmental, food and drug, or intellectual property regulatory systems. Only accounting and financial reporting regulators, having a vast mandate over the disclosures of practically all public companies in the world, are immune to serious research and criticism.

Admittedly, standard-setting research is not easy, and, from personal experience, regulators’ response to criticism is not particularly welcome. But the rewards, in terms of actually affecting financial disclosure, are as great, if not greater than any other accounting research. The research needed, in my opinion, is primarily ex ante, before standards are enacted, while rule-making can still be affected. Here are two examples: