Abstract

Externalities comprise economic, social and/or environmental impacts arising from the activities of an entity that are borne by others, at least in the short term. As they do not feedback directly into immediate financial consequences for the entity, they tend to be outside the remit of financial reporting. A dispersed academic accounting literature on externalities has hitherto developed separately from concerns about what information is appropriate to report on corporate performance. This paper develops insights into accounting for, and reporting of, externalities that are intended to improve the use of externalities information in breaking down silos between the traditionally discrete domains of financial reporting and sustainability reporting, and between silos within sustainability reporting. Challenges in such use of externalities information are explored, including difficulties inherent in the quantification of externalities. The paper also highlights ways in which externalities can progressively become internalised, thereby bringing them more readily within the domain of economically focused financial reporting practices. An agenda for further research to help enhance the accounting for, and reporting of, externalities is also proposed.

1. Introducing the issues and framing the debate

For most companies, interactions with nature … are not visualized on a company's profit and loss statement or on their balance sheet. They remain ‘externalities’, or issues without internal consequence. However there are several potential drivers that may lead to such externalities being internalized in the future including increasing regulatory or legal action, market forces and changing operating environments, new actions by and relationships with external stakeholders, plus an increasing drive for transparency or voluntary action by businesses because they recognize the significance of transparency to future success. (NCC Citation2016a, p. 2)

The domain of corporate reporting has expanded considerably over the last two decades. While financial reporting to investors about organisations’ predominately short-term economic performance and position remains the primary concern of corporate reporting, there has also been a surge in policy frameworks and corporate engagement with sustainability reporting to a broader range of stakeholders (Bebbington et al. Citation2014, Deegan and Unerman Citation2011). Much of this sustainability reporting encompasses issues that are not captured in, or are external to, the financial dimensions of transactions and events as communicated in financial reporting.

These externalities comprise social, environmental and broader economic impacts arising from the activities of an entity that are borne by others and do not feedback directly into short-term financial consequences for the entity. They are, therefore, outside the remit of financial reporting, although they may have longer term financial consequences for the entity (Hopwood et al. Citation2010). However, as externalities are a product of market failures (Mildenberger Citationforthcoming), and as financial prices from market transactions underlie most financial reporting data, financial reporting information will be flawed and incomplete in the almost inevitable presence of externalities. Accordingly, for financial reporting to provide a representationally faithful portrayal of an entity's performance and position, additional information needs to be provided about material externalities that are not reflected in financial reporting's market-derived financial data.

While sustainability reports provide information about many aspects of material externalities, these reports often take a rather siloed approach to individual issues instead of clearly articulating connections between different areas of impact. This leads to the financial dimensions of many externalities being, at best, opaque in much sustainability reporting. The potential financial impacts of externalities are, therefore, not usually systematically communicated in either sustainability or financial reports.

To more systematically and effectively communicate these financial impacts of externalities, silos between the domains of financial reporting and sustainability reporting, and those within sustainability reporting itself, need to be broken down. Breaking down these silos should enable connections between economic, social, environmental and financial impacts of externalities to be better understood. This, in turn, could help preparers of financial reports draw on the elements of externalities information that are currently (partially) captured within sustainability reports in articulating the material financial consequences that potentially accompany these externalities.

Although the IIRC's International Integrated Reporting Framework (IIRC Citation2013) sought to break down some of these silos, implementation of this reporting framework by corporations has tended to focus on financial value and capital while marginalising social and environmental factors (Humphrey et al. Citation2017, Zappettini and Unerman Citation2016). Integrated reporting has, therefore, not been particularly effective in practice in breaking down silos between financial and sustainability reporting. However, development and use of concepts within accounting for externalities may have the potential to help break down these silos by making explicit the connections between financial and non-financial impacts.

With a recent KPMG (Citation2017) survey of the corporate responsibility (sustainability) reporting practices of 4900 large companies in 49 countries showing three quarters of these companies engaging in such reporting, including 93% of the world's largest 250 companies (by revenue), there are significant policy issues in the quality of externalities information underlying such reports. The same survey showed a substantial growth in the number of these companies now reporting sustainability-related data within their annual (financial) reports (78% of the largest global companies in 2017, up from 44% in 2011) ‘indicating that they believe [such] data is relevant for their investors’ (KPMG Citation2017, p. 21). As more systematic accounting for the financial impacts of externalities has the potential to improve the effectiveness of both sustainability reports and the reporting of sustainability information within financial reports, the growth of both practices as highlighted by the KPMG survey demonstrates the importance of developing more effective accounting for externalities.

While there has been a burgeoning of research into many aspects of sustainability reporting in recent years (Bebbington et al. Citation2014, Thomson Citation2014), little of this research has focused on systematic recording or articulation of the financial impacts of externalities. The limited number of studies into accounting for externalities have been sporadic and fragmented, with little connection in insights across this body of literature (Pajuelo Moreno Citation2013, Russell et al. Citation2017), thus restricting the usefulness of this academic evidence for policy-makers. In seeking to redress this, the aim of this paper is to develop insights into accounting for, and reporting of, externalities that can help in advancing the effective use of externalities information in both financial and sustainability reporting. Although externalities information can be useful to a range of stakeholders, to provide focus in addressing this paper's aims, the paper specifically explores the potential of externalities information for those stakeholders seeking to more fully understand an entity's financial performance, position and prospects. This leaves space for a lively discussion elsewhere regarding the use of externalities information in a range of other applications, such as activists’ use of data in confronting corporations.

Many decision-making processes used to evaluate financial performance draw heavily on monetised metrics. A dominant policy discourse in reporting social and environmental impacts of externalities also stresses and reinforces the ideal of monetised data (Humphrey et al. Citation2017, KPMG Citation2017). However, the nature of the complexities underlying many types of externalities makes it problematic to develop reliable or meaningful metrics to monetise the financial dimensions of these impacts. This poses a particular challenge in developing accounts of externalities that can contribute to a fuller picture of corporate performance in the presence of market failures underlying market-derived financial reporting information. In addressing its aims, this paper therefore also explores the possibilities, challenges and limitations of quantifying and monetising externalities.

To achieve its aims, the paper traces connections between accounting for, and reporting of externalities, theorises the role accounts of externalities can play in corporate reporting and proposes a research agenda to provide evidence to help motivate effective policy interventions. The paper's insights are developed through a review and synthesis of the academic literature, augmented with information about current practices in both accounting for, and reporting of, externalities. This information about current practices has been partly derived from a series of 13 interviews with expert observersFootnote1 of non-financial reporting practices. Analysis of these interviewsFootnote2 has informed insights throughout the paper and, where appropriate, quotes from the interviews have been used to further clarify points made.

The paper proceeds as follows: Section 2 explains the concept of externalities. Section 3 analyses the characteristics externalities data needs to possess to underpin effective corporate reporting. Section 4 reviews the limited accounting for externalities academic literature for lessons on identification and quantification of externalities in practice. Section 5 then explores issues around commensuration that need to be understood in evaluating the reliability of quantification and monetisation of externalities. To address problems of effective monetisation, Section 6 develops a continuum illustrating how externalities can progressively become financially internalised. The concluding section summarises key points from the paper and sets out a research agenda in provision of an evidence base to inform policy and practice on accounting for, and reporting of, externalities.

2. Defining externalities

Economists have long recognised the concept of externalities as:

one of the classic cases of market failure … [where] production or consumption of a certain good by an agent either confers benefits or imposes costs on others which are not accounted for in the market price of the good … Externalities [include] the uncompensated-for costs certain exchanges impose on third parties. (Mildenberger Citationforthcoming, pp. 2 and 4)Footnote3

Reliable and usable information about externalities is needed to highlight the extent of such market failures and inform decisions about how persistent externalities might be addressed.

From a short-term and narrow economic perspective, negative externalities occur when a third-party individual or organisation suffers financial costs flowing from a transaction between other parties and for which there is no recourse for the third party to recoup these financial costs from the transacting parties. Positive externalities result in financial benefits for the third party. Where financial reporting information is aggregated from underlying transaction records that use market-derived prices or values, this information for the transacting parties disregards these economic externalities. While excluding externalities from decisions informed by financial reporting might not be problematic for decisions targeting solely short-term economic ends, economic decisions with longer time horizons risk being sub-optimal where the externalities ignored by transactional data have longer term financial impacts on the transacting parties themselves. Organisations will also be subject to risks and costs arising from other organisations’ externalities, such as climate change risks (TCFD Citation2017).

Over recent decades, an increasing range of external social and environmental impacts have been identified which arise from organisational decisions that were made based on short-term economic factors (Bebbington et al. Citation2014). The UN Sustainable Development Goals have recently provided a framework that has broadened understanding of the nature of these externalities (Bebbington and Unerman Citation2018). These social and environmental externalities can have longer term economic impacts – both for organisations that took decisions initially based on short-term economic factors, and for a range of third-party stakeholders (Hopwood et al. Citation2010, O’Dwyer and Unerman Citation2016, TCFD Citation2017, Unerman and Chapman Citation2014).

To illustrate these points, consider pharmaceutical companies making decisions on developing new antibiotics to fight antimicrobial drug resistance. A review commissioned by the UK Government estimated that up to 10 million deaths globally each year could result from failure to stem antimicrobial resistance (Review on Antimicrobial Resistance Citation2014). A 2017 World Bank report estimated that by 2050 the social and economic dislocation from such growing antimicrobial resistance could lead to an annual reduction in global GDP of between 1.1% and 3.8% (World Bank Citation2017). These impacts comprise externalities in economic terms (reductions in GDP) while also having non-economic impacts (such as social costs from antimicrobial resistance). In a strict financial sense, the pharmaceutical sector's economic performance would likely be negatively affected to some degree by these reductions in global GDP. However, for a variety of complex reasons,Footnote4 it is not usually in the short-term economic interests of pharmaceutical companies currently producing antibiotics to develop new antibiotics requiring less use but that are needed to help reduce antimicrobial resistance (see: Review on Antimicrobial Resistance Citation2015). Thus, although:

Many countries have stepped up campaigns to inform citizens about the risks of over-reliance on antibiotics … a market failure has long plagued the development of new antibiotics. Pharmaceutical companies have little incentive to develop antibiotics that are designed to be taken as little as possible. (Leatherbury Citation2017)Footnote5

While increased global levels of antimicrobial resistance might be an externality from short-term profit-maximising decisions made by some executives of pharmaceutical companies, the above insights indicate that substantial longer term negative social and economic impacts are likely to flow from antimicrobial resistance linked to any resulting high levels of antibiotic use. These externalities are unlikely to be captured within pharmaceutical companies’ internal bookkeeping records or to be reflected in their financial reporting. However, they could (i) have a longer term negative economic impact on the pharmaceutical companies through a weaker global economy restricting funds available for procuring drugs and (ii) could result in reputational damage for pharmaceutical companies where powerful stakeholders come to disapprove of short-term profit maximisation being placed ahead of ethical responsibilities for the long-term health of society.

This is just one example from a wide range of social, environmental and economic externalities that can flow from (trans)actions of organisations. A challenge for corporate reporting is to provide information about these externalities to a range of stakeholders in a way that allows data about an entity's financial performance, position and risks (traditionally the domain of financial reporting) to be understood alongside, and in the context of, information about social, environmental and wider economic impacts (traditionally covered by sustainability reporting). Developing such an understanding requires corporate reporting information about externalities to have appropriate characteristics.

3. Characteristics needed for accounts of externalities to support corporate reporting

The form and substance of financial reporting are largely regulated by accounting standards, with standard-setters establishing conceptual frameworks to guide the development and setting of their standards. Although contested, these conceptual frameworks aim to help ensure that financial reporting will be useful in informing investment decisions, with a particular criterion being comparability of information disclosed across different reporting organisations (Deegan and Unerman Citation2011, IASB Citation2015, Nobes and Stadler Citation2017). In addressing these aims, conceptual frameworks establish qualitative characteristics that financial reporting information should possess to be useful in supporting investors’ economic decision-making.

For example, the International Accounting Standards Board's (IASB's) draft revised conceptual framework (IASB Citation2015) sets out the two ‘fundamental qualitative characteristics [of] relevance and faithful representation’ (p. 27, emphasis in original) that reported information needs to possess for it to be useful in supporting investor decision-making. The IASB consider information to be relevant if it can be used to predict future outcomes and/or confirm past outcomes. For this purpose, the information must be material to the types of decisions that are likely to be based on a financial report and, where estimates of value are used, lower levels of ‘measurement uncertainty’ (p. 28) can increase the relevance of reported information to decision-makers (investors). The IASB's criteria for representationally faithful information are that it should be as ‘complete, neutral and free from error’ (p. 29, emphasis in original) as is possible in each situation. The IASB's framework also sets out four ‘enhancing qualitative characteristics [of] comparability, verifiability, timeliness and understandability’ (p. 30, emphasis in original) which need to ‘be maximized to the extent possible’ (p. 32) in any item of reported financial information.

In practice, in situations where it is not possible to maximise every desirable characteristic for a particular type of disclosure, there is likely to be some trading-off between these different characteristics. However, it is clear from the IASB's conceptual framework (and those of other financial reporting standard-setters) that monetisation in either historical or current values is considered crucial in the effective provision of comparable information within corporate financial reports, with quantification based on observed market exchanges being the ideal (IASB Citation2015). Although externalities impacts may flow from the reporting entity's market exchanges, by definition they are not part of the economic values captured in these transactions’ observable market-derived prices as recorded in its financial bookkeeping.

To address this gap in recorded information, various experiments with full cost accounting (explored in Section 4 of this paper) have attempted to systematically capture and record specific externality impacts flowing from actions of individual organisations in order to aid decision-making within these organisations and/or inform stakeholders. However, comparison of this externalities information between organisations is hindered because of the many acceptable and defendable methodologies for quantifying and financially internalising externalities, which provide widely differing measures of economic impacts from one methodology to another. The Natural Capital Collation (NCC) reinforce this point in their Natural Capital Protocol, stating:

while the Protocol does provide a standardized process, it also remains flexible in the choice of measurement and valuation approaches used, which means that results may not be comparable within or between different businesses and applications. (NCC Citation2016a, p. 2)

This highlights a challenge for externalities information disclosed within corporate reporting: while it can inform decisions, meaningful inter-organisational comparability may be problematic unless standard quantification and monetisation approaches are developed and used. Despite the lack of standardised measurements, other desirable characteristics of information are set out in many corporate reporting frameworks that cover non-financial reporting.

The objectives and target readership of sustainability reporting differ between these different frameworks – and from those of financial reporting. For example, whereas the IASB's reporting standards aim to provide financial information to help investors make economic investment decisions, the Global Reporting Initiative's (GRI's) reporting standards:

create a common language for organizations and stakeholders, with which the economic, environmental, and social impacts of organizations can be communicated and understood. The Standards are designed to enhance the global comparability and quality of information on these impacts, thereby enabling greater transparency and accountability of organizations. (GRI Citation2016, p. 3)

As the objectives and target readership of financial and sustainability reporting differ, the principal desirable characteristics of information reported in each type of reporting framework may also differ. To identify such differences, compares the qualitative characteristics of information in the IASB’s Citation2015 draft update of its Conceptual Framework for Financial Reporting (IASB Citation2015); the GRI's reporting principles within its 2016 Sustainability Reporting Standards (GRI Citation2016); the International Integrated Reporting Council's (IIRC's) 2013 International Integrated Reporting Framework (IIRC Citation2013); the 2017 fundamental principles of the Task Force on Climate-Related Financial Disclosures (TCFD Citation2017); the Sustainability Accounting Standards Board's (SASB's) 2017 Conceptual Framework (SASB Citation2017) and the Climate Disclosure Standards Board's (CDSB's) 2015 Environmental and Natural Capital Reporting Framework (CDSB Citation2015). These reporting frameworks were selected based on their centrality to financial reporting (IASB), their longevity (in the case of GRI), their desire to bridge financial and sustainability reporting (IIRC and TCFD) as well as their role in mediating across specific aspects of impact (TCFD, SASB and CDSB).

Table 1. Principal qualitative characteristics of externalities information in reporting frameworks.

All of the reporting frameworks analysed in specify that reported information should possess elements of what the IASB's framework characterises as relevance, although materiality is the only principal relevance characteristic specified across all frameworks. Each framework also specifies all three of the IASB's principal representational faithfulness characteristics of completeness, neutrality and accuracy. Comparability/consistency is the only other characteristic common across all reporting frameworks.

In contrast to the IASB conceptual framework's focus on quantitative information, all of the other reporting frameworks recognise that both quantitative and qualitative information is likely to be necessary to fulfil their objectives for reporting. However, a dominant discourse among policy-makers and practitioners urges the development and use of quantified data, and especially monetised data, as most likely to fulfil the objectives of externalities reporting that each framework addresses (Humphrey et al. Citation2017, KPMG Citation2017).

Just as financial bookkeeping is a key source of monetised information in compiling an organisation's financial reports to meet these qualitative characteristics, entity-level data captured in accounts of externalities can be an important source of information to fulfil these criteria when reporting externalities. Academic insights on such accounting for externalities are discussed in the next section.

4. Review of accounting for externalities academic literature

Within accounting practice and academic literature, as awareness developed of the variety and potential severity of social and environmental externalities arising from organisational actions, a concern with externalities translated into a sub-field of accounting focused on supporting internal management decision-making (with the possibility of this work informing externally orientated discussion of appropriate responsibilities). This sub-field was most commonly described as full cost accounting. Bebbington et al. (Citation2001) codified four steps in a full cost accounting exercise:

Defining the object and level that will be subject to the full cost accounting exercise, such as a product, a process or the whole organisation.

Establishing the scope of analysis. This is the subset of all possible externalities to be evaluated, and at what level of resolution these impacts arise.Footnote6

Identifying and measuring the externalities in physical terms, thus linking each activity and its externality by direct or indirect measurement. Often governments have data of this nature for their decision-making, which can be drawn upon to help calculate entity-level accounts of externalities. For example, an entity can use the number of kilowatt hours of electricity it consumes in conjunction with government published carbon multipliers to estimate how much pollution was emitted (on average) to generate the electricity it has used.Footnote7

Monetisation of the impacts, where there are often a wide variety of measurement techniques that can yield widely differing monetised accounting for externalities data (Antheaume Citation2004).

Each of these steps requires judgements that have a material impact upon the outcome of the externalities account. The complexity and indeterminacy involved in monetisation resulted in some full cost accounting experiments stopping at step (3). For example, Herbohn (Citation2005) and Lamberton (Citation2000) both concluded their projects before monetisation, while Gasparatos et al. (Citation2009), Frame and O’Connor (Citation2011), Bebbington et al. (Citation2007), Frame and Brown (Citation2008) and Bebbington and Larrinaga (Citation2014) discussed why caution should be exercised in monetisation.

Cutting across the above steps, there have been four distinct phases of accounting practice, policy and academic research in full cost accounting (see also Antheaume Citation2007). We are aware, however, that more externalities accounts have been developed than those to be found in the public domain. Contentiousness of the techniques, the likely quantum of costs associated with the externalities and ramifications of externalities data (A4S Citation2012) all provide reasons for some cautious but innovative organisations to keep confidential, for internal use, these experiments and the data they produce. This nervousness around internal accounts of externalities can be explained by any such accounts feeding directly into responsibility and accountability debates (Jones and Dugdale Citation2001).

The first of the four phases of accounting for externalities began in the 1970s when the early social audit movement sought to provide information about the wider consequences flowing from corporate behaviour (see Gray et al. Citation2014, pp. 237–257 for an introduction to this work). This is an early example of accounting for externalities, albeit one not self-consciously using this language (Milne Citation1996, also makes this link), as the audits highlighted various externalities. In a similar fashion, the de-industrialisation and plant closure audits analysed by Harte and Owen (Citation1987) can be considered an early version of full cost accounting, as they estimated negative economic externalities from plant closures borne by the social security system, and invited public authorities to strategically support private sector entities so as to avoid these costs.

The second phase of accounting for externalities, in the form of full cost accounting, was prompted by a wave of experimentation. Some of these experiments were undertaken by organisations themselves, such as BSO/Origin (Citation1990–Citation1995), Ontario Hydro – published by the United States Environmental Protection Agency (Citation1996), Manaaki Whenua/Landcare Research – published by Bebbington and Gray (Citation2001) and Interface Europe – published by Howes (Citation2000). The outcomes of these accounts were used for various purposes. For example, BSO/Origin used their account to change how they assigned consultants to projects so as to reduce the firm's travel footprint. Ontario Hydro was selling electricity to the USA from Canada and wished to charge a price that incorporated the negative health externalities of fossil fuel combustion that would fall on Canadians while the energy benefits of production were enjoyed by US consumers. Others were experiments in full cost accounting methodologies undertaken by consultants addressing particular issues that firms faced (Bent Citation2006, Macaulay Citation1999, Rubenstein Citation1994, Stranger et al. Citation2002). Bebbington et al. (Citation2001) summarised this work (see, also, Davies Citation2014) and codified a best practice guide on how to approach full cost accounting. Some of these experiments dealt with especially intractable practical and ethical questions such as the extent of negative social externalities arising from alcohol consumption (Bent Citation2006) or how much sustainable forestry would cost (Rubenstein Citation1994).

After the second phase's full cost accounting activity of the 1990s and early 2000s, organisation-wide full cost accounting disappeared from the accounting literature. A third phase developed in its place, which focused on a project evaluation tool to explore similar issues regarding externalities (for a summary of this tool, see Bebbington Citation2007). This work started with a case study in BP (Baxter et al. Citation2004) which resulted in the development of the Sustainability Assessment Model. Ideas behind this work were subsequently applied, for example, in built environment settings (see Xing et al. Citation2009) and in different problem settings in New Zealand (see Frame and Cavanagh Citation2009, Fraser Citation2012) where they had some practical impact in terms of changing public sector decision-making. At the same time, this tool was politically problematic (as Fraser Citation2012, documents) as it did not allow users to say they were ‘sustainable’ but, rather, highlighted the gap between rhetoric and reality. The use of this particular tool has declined, but it is likely that organisations still try to make assessments about externalities outside of researchers’ gaze.

In the past decade, a variety of accounting for externalities practices is evident that can be broadly divided into four strands. In the first, externalities accounts have developed on thematic grounds, primarily in the area of carbon and biodiversity accounting. For example, Davies and Dunk (Citation2015) sought to identify higher education's carbon emissions externalities from overseas students coming to study in the UK and their friends and families visiting them during their studies. Davies and Dunk (Citation2015) estimated these emissions to be potentially of a similar magnitude as the totality of estate-based emissions from all UK universities. Davies (Citation2014) provides an example of how externalities data might assist in biodiversity management for organisations while noting that, presently, species-level valuation data are not available but initiatives such as TEEB (The Economics of Ecosystems and Biodiversity – see http://www.teebweb.org/) suggest that this data might eventually be developed.

In the second strand of this fourth phase, sustainability consultants and some accountancy professional services firms developed tools their clients could use to identify and quantify externalities. For example, PwC developed a Total Impact Measurement and Management (TIMM) tool that aims to help companies place a value on their social, environmental, taxation and economic impacts (PwC Citation2013).Footnote8 In explaining the need for and importance of this accounting for externalities tool, PwC (Citation2017) draw on arguments that resonate with insights discussed in this paper:

Traditional financial metrics are a given in decision making, but now non-financial measures are a must too. Putting a true value or true price on the impacts of business activity such as economic, environmental, social and tax is just as important as calculating potential revenue streams or profit. Altogether, they provide insight into the total impact of a business activity, operation or strategy.

The third strand of the fourth phase involved innovations from individual corporations. For example, The Prince's Accounting for Sustainability Project (A4S) reported on Danone's incorporation of carbon emissions data in product-level financial management information, South West Water's incorporation of environmental benefits and costs in capital investment decisions, and PUMA's 2011 publication of an Environmental Profit and Loss Account (Citation2012). In 2012, PUMA also provided a full cost account for a small number of specific products (PUMA Citation2012, p. 39). A more recent example in this strand is the Crown Estate's ‘total contribution’ methodology that seeks to calculate the value created by the organisation on a multiple capitals framework (The Crown Estate Citation2017).

The final strand of the fourth phase has involved networks of practitioners and policy-makers developing frameworks that help to identify, record and report externalities. Among these networks, A4S's CFO Network has developed a series of guides designed to help organisations incorporate sustainability considerations into business decision-making (A4S Citation2017). Another network, focusing on environmental externalities, is the NCC whose mission is to:

harmonize approaches to natural capital, getting solutions to scale quickly … promote a shift in behaviour that enhances rather than depletes natural capital … [and] support the evolution of an enabling environment that both aids natural capital thinking and integrates it into other initiatives. (NCC Citation2017)

In accounting for environmental externalities, an important part of the NCC's model promotes recognition of dependencies that organisations have on natural capital, along with the costs and potential benefits arising from the impacts of an organisation's activities on natural capital. To support the more systematic identification of these dependencies and impacts, the NCC has developed its Natural Capital Protocol as a ‘framework designed to help generate trusted, credible, and actionable information that business managers need to inform decisions’ (NCC Citation2016a, p. 2). However, the protocol does not propose standardisation of such information provision:

because the choice of tools will be dependent on business context, resources, and needs. Further, natural capital measurement and valuation is evolving and new approaches and methodologies become available all the time. (NCC Citation2016a, p. 2) (echoing Davies Citation2014)

We should look into some standardized approaches … for some of the very basic things [where] we feel there is a degree of confidence and consensus within a community … comparability can only exist once we can all report using the same classifications, the same concepts, the same way that we display the data, the same methods to obtain the data.

In seeking to identify how meaningful quantification in the reporting of externalities might be achieved (noting severe reservations expressed by Antheaume Citation2004, Frame and O’Connor Citation2011, Gasparatos et al. Citation2009, Herbohn Citation2005), the next section of this paper explores the problem of comparable quantification conceptually – from the perspective of commensuration.

5. Commensuration and the credibility of externalities quantification

In line with academic literature that emphasises the constitutive effect of accounting practices (Miller and Power Citation2013), reporting of externalities draws attention to how the economic system distributes costs and benefits. As noted above, the existence of externalities indicates markets are not ideally constituted but have dysfunctional effects, for example, through market failures (Mildenberger Citationforthcoming). Accounting for externalities (including full cost accounting) can contribute to ameliorating these market imperfections and enhancing responsibility and accountability. In this role, articulation of externalities in financial form is a particular strength because it suggests the size of selected externalities (for example, the Davies and Dunk Citation2015 account is arresting because of its magnitude) in a language (monetised values) that is already used widely within business to convey the success (or otherwise) of activities. Where realised, this potential strength of accounting for externalities could imbue the reporting of externalities with power from its ability to create visibility for what is often hidden.

Within a growing range of tools developed to help organisations financially internalise their externalities, a familiar exhortation is that effective management requires effective measurement through clear metrics. In common with many areas of management, metrics are seen as powerful instruments in setting targets and assessing performance (Arjaliès and Mundy Citation2013, Henri and Journeault Citation2010, Lisi Citation2015, Pajuelo Moreno Citation2013), with monetised metrics often regarded as the most effective. As an example of this importance of measurement and valuation of externalities in corporate reporting protocols, the foundation stages of the processes set out for accounting, management and reporting of externalities by the NCC focus on measurement and valuation (NCC Citation2016b, p. 11). However, also in common with other areas of management, recognition of the benefits of quantification can lead to a focus on accounting and reporting of those externalities that are most readily amenable to quantification. This risks crowding-out management of externalities that are less readily quantifiable.

Furthermore, the non-economic nature of many social and environmental externalities, with no observable values from market exchanges, often makes it difficult to estimate a non-controversial and/or reliable financial measure. Antheaume (Citation2004) highlights the large ranges of estimates for externalities that emerge from various monetisation techniques. For non-monetised metrics, any lack of underlying comparability between measurement bases of different items also restricts the usefulness of metrics. However, reported metrics are often interpreted by users as objective and comparable measures, with little or no questioning of the processes or assumptions underlying each metric (Miller and Power Citation2013). Some of the problems flowing from this are illustrated in the following quotes from this study's interviews:

The metrics themselves give you a snapshot of the situation … you can have a very simple metric to say, ‘we emit X effluent into a freshwater body’, for example … behind that, then you need to be thinking about what your intervention is … what does it mean in terms of … are they changing their behaviour? … or are they literally just saying, ‘look, these are our weaknesses … ’

How do you value a life? A life hasn't an equivalent anywhere. In some places life is cheap. If you’re importing Nepalese or Indian workers to work in Qatar, for example, I don't know how many hundreds of them have been killed with no consequence … So, if those construction companies were producing proper accounts … we’d all be appalled … There's no monetary equivalent. So, I think we have to use other values there. We have to attach stigma and we have to say that certain things enhance brand value, but without necessarily putting a monetary value on it.

Where a reporting protocol prioritises measuring and valuing externalities, it therefore risks marginalising the management and reporting of externalities that may have a major impact but that are not readily quantified or monetised. As recognised in the sustainability reporting frameworks summarised in , capturing and reporting of both quantifiable and non-quantifiable externalities can thus be crucial in informing better decisions. To help explain why non-quantified information needs to be embraced in accounting for, and reporting of, externalities, this section explores the challenges that commensurability poses for quantification of externalities.

The impression that quantification provides far superior knowledge than other forms of evidence has long been cultivated within many societies. For example, the leading nineteenth century scientist Lord Kelvin famously stated: ‘when you cannot express it in numbers, your knowledge is of a meagre and unsatisfactory kind’ (Kelvin Citation1891, p. 80). Although Kelvin was addressing qualities of knowledge in the physical sciences, the superiority of quantification is often an unquestioned assumption in social sciences, despite humans having agency in causal relationships that is not present in the physical sciences. Monetisation that is at the core of much traditional financial and management accounting practices is a powerful way of summarising and comparing performance information both historically and in forecasts, budgets and targets (Miller and Power Citation2013).

A strength of some forms of accounting for externalities (as discussed in Section 4), therefore, is they seek to attach monetary values to externalities, thus helping their management through adaptation of metric-based techniques developed for managing more conventional economic impacts. However, as also recognised in Section 4, comparable quantification of externalities is problematic. These concerns are explored in Frame and O’Connor (Citation2011) who propose the idea of a ‘Monetisation Frontier’ and note ‘the necessary conditions for establishing monetary commensuration are very restrictive’, with the consequence that some valuations might be ‘robust and useful’ while others are of low ‘scientific quality and of doubtful pertinence’ (p. 3). With this in mind, they develop the idea of a frontier that ‘marks the boundary between analytical rigour and narrative clarity, between quantitative measurement and metaphor’ (p. 4) and suggest that data on both sides of this frontier are valuable, but there has to be clarity about which side of the boundary the data is drawn from in order to make sound judgements about measurements and what they might imply.

The effectiveness of metrics in accounting for externalities relies upon them possessing the types of qualitative characteristics set out by the various reporting frameworks analysed in Section 3. In broad terms, these assume the metrics are objective and neutral.Footnote9 However, although there might be widespread consensus around the way many economic transactions are recorded in bookkeeping entries and summarised into figures in a corporate report, this consensus does not imbue these figures with objectivity. Rather, such apparent objectivity is an illusion, as elucidated by Huff (Citation1954, p. 63) when discussing quantification in graphs: ‘[they] contain … no adjectives or adverbs to spoil the illusion of objectivity’. For meaningful and comparable accounting, management and reporting of externalities, this illusion of objectivity needs to be recognised.

Instead of being objective, many accounting metrics are intersubjective. This is the term used for subjective items where there is widespread consensus around the judgments that are appropriate in reaching a subjective understanding of the item, such that sufficient people agree that this understanding or perception is the correct and only appropriate way of knowing the item (McKernan Citation2007). While knowledge and understanding of an item might, therefore, appear to be objective because few, if any, dissent from it, it is not actually an objectively factual representation. However, the more widespread the intersubjective consensus that develops around an evaluation and understanding of any item, the more likely it is to be regarded by many as an objective fact.

Nevertheless, as intersubjectively agreed metrics are not actually objective but merely possess an illusion of objectivity, questions arise as to their comparability where the (sometimes unspecified) assumptions underlying each metric might vary. Recognising that intersubjectivity is not the same as objectivity raises questions about the use of such metrics. As Hiss (Citation2013, p. 240) observes:

numbers go beyond the mere recording of data and the neutral and objective reproduction of economic fact; rather, numbers significantly interfere with the reproduction of social order, and the comparability of numbers is the precondition for embedding situations and organizations in a comprehensive global social order. (See also Espeland and Stevens Citation2008, Samiolo Citation2012)

Commensuration is the use of a metric that can reliably and effectively compare and evaluate items with different characteristics (Espeland and Stevens Citation1998, Samiolo Citation2012):

Commensuration transforms qualities into quantities, difference into magnitude. It is a way to reduce and simplify disparate information into numbers that can easily be compared. This transformation allows people to quickly grasp, represent, and compare differences. One virtue of commensuration is that it offers standardized ways of constructing proxies for uncertain and elusive qualities. Another virtue is that it condenses and reduces the amount of information people have to process, which is useful for representing value and simplifying decision-making. (Espeland and Stevens Citation1998, p. 316)

Intersubjective consensus is a necessary factor in meaningful commensuration using any metric. For example, there are many different greenhouse gases, each with its own impact on global warming and endurance in the atmosphere. There is also strong scientific consensus about the impact that a given volume of emissions of each type of greenhouse gas has on global warming (IPCC Citation2014). The strength of this consensus is sufficient for the global warming impact of each greenhouse gas to be expressed in terms of a common metric – in this case the equivalence in terms of the number of tonnes of carbon dioxide that would have the same impact on global warming as one tonne of the other greenhouse gas (IPCC Citation2014, MacKenzie Citation2009). Furthermore, the existence of markets on which carbon permits are traded (de Alegría et al. Citation2016, Welfens et al. Citation2017), although strongly contested by some (Aldred Citation2012, Knox-Hayes Citation2013), appears to have allowed sufficient intersubjective consensus to develop around measurement of the current economic value of one tonne of carbon dioxide emissions to be able to use this to commensurate greenhouse gas emissions in monetised metrics in countries with such markets. These figures can then be used as inputs to monetised accounting for, and reporting of, greenhouse gas emissions.

While the above example demonstrates the commensurability of carbon emissions such that they can plausibly be expressed in monetary terms that may meet the qualitative characteristics of corporate reporting information (as explored in Section 3), many other environmental and social externalities cannot be so readily commensurated. For example, while the volume of water used to manufacture (or grow) a product might be measurable with a high degree of accuracy and be uniform irrespective of where and when the product is produced, the social, environmental and economic impacts from the use of this volume of water (or from its lack of availability to be used for other purposes) will vary significantly between production in a region with high rainfall and production in an arid region (Russell and Lewis Citation2014, Unerman and Chapman Citation2014). There can also be considerable seasonal variations in these impacts in regions that are subject to water shortages in some seasons and plentiful water in others. So while the volume of water used can be measured, the social, environmental and economic impacts of the use of each litre of the water used may vary considerably between contexts (Hazelton Citation2015). This makes water's commensuration in accounts of externalities problematic, as a broad enough intersubjective consensus on the externalities impacts of water is unlikely to have been reached and, indeed, may be impossible to achieve given the underlying physical realities outlined above. However, any weak processes and assumptions underpinning a metric can be obscured because of the objectification cloak provided by reporting a numerical value (Miller and Power Citation2013).

Insights from interviews undertaken for this study provide additional reasons for caution in seeking to commensurate using monetised externalities metrics, for example:

valuation in monetary terms is often far less useful than indicators of impacts on human development … for example impact on health indicators like [a] reduction in fish stocks having an impact on human nutritional status of people who rely on coastal fishing, or disease risk when you have an increased risk of infectious diseases because of changes in wetlands. So, you’ve got much more nuanced views of the kinds of value metrics that are relevant and I think that the sustainable development goals frame that very nicely, and that as businesses are committing to achieve these goals, they should be increasingly thinking about multiple metrics of value, not just dollar values.

Where efforts to reduce many externalities into metrics do not include a process of widespread intersubjective consensus-building, the resulting objectified externalities accounts risk being misleading as well as non-comparable. Use of this data in corporate reporting as if it were objective could also lead to sub-optimal decisions by investors and other stakeholders; a counterproductive outcome from seeking to use accounting for externalities to bridge sustainability and financial reporting domains in this poorly-informed manner.

Frame and O’Connor (Citation2011) suggest a potential resolution to this problem whereby those elements that can be internalised (and where sufficient intersubjective consensus exists) should be, while other externalities data may remain at the level of a narrative that prompts reflection. This requires skills in recording, reporting and interpreting qualitative information across a range of externalities. Over time, however, many externalities might be expected to become financially internalised through the processes set out in the next section, hence moving across the monetisation frontier.

6. Progressive financial internalisation of externalities

This section provides a more dynamic sense of when and how externalities might become internalised in monetised terms. As will become apparent, evolving social contracts as well as market-based incentives provide the context within which externalities become financially internalised.

6.1. Externalities from a societal perspective

Understanding and social acceptability of externalities are dynamic processes. The impacts of social and ecological risks on society will change both as scientific and sociological knowledge develops to provide greater clarity on the longer term outcomes of these risks and as societal values change. The former influences both understandings of the ecosphere's capacity to absorb environmental impacts from human activities and understandings of various impacts on society. The former and latter combine to change the terms of an organisation's societal licence to operate – its social contract (Demuijnck and Fasterling Citation2016, Gray et al. Citation1988, Shocker and Sethi Citation1974). This view is illustrated in the following quote from an interview for this study:

20 years ago, anything outside environment, health and safety wasn't material and they were externalities … over a period of time, externalities become material issues, so it's almost like saying, what are the externalities that have yet to become material issues?

Social contract theory distinguishes between what is legal and what is acceptable to the societies in which an organisation operates (Deegan Citation2014). Just because a particular action is legal does not mean it will be considered morally acceptable to an organisation's stakeholders (and vice versa). Changes in laws in any country may lead or lag changing societal values. Where an organisation relies on the approval of a group of stakeholders for its financial survival, failure to change its behaviour to accord with evolving values held by this powerful group of stakeholders (or failure to convincingly appear to have changed behaviour) risks these stakeholders switching allegiance to competitors who act more closely in accordance with the stakeholders’ values (Deegan Citation2014). This is irrespective of whether the organisation's behaviour complies with the law.

For example, until relatively recently there was limited concern within UK society about large companies seeking to avoid tax through schemes engineering financial structures to minimise tax while complying with the letter of tax laws. Both the legality and lack of widespread social disapproval of this behaviour seemed related to a distinction between illegal tax evasion and legal tax avoidance (Kirchler et al. Citation2003). However, over the past few years more widespread disapproval has developed of large multinationals aggressively avoiding paying what is regarded by many in society as their fair share of taxation – albeit by using legal tax avoidance measures (Martindale Citation2017, Payne and Raiborn Citation2018). Defences that claim a corporation has paid all the taxes it is legally required to pay in each country in which it operates no longer appear to resonate with many stakeholders whose changed values have moved to seeing aggressive tax avoidance in a similar light as tax evasion. In the face of calls for customer boycotts of some companies whose UK taxes appeared to be disproportionately low in comparison to the size of their UK operations, some companies voluntarily changed their structures to make a higher proportion of their global income subject to UK taxation (Houlder Citation2016). Although the UK and other governments were acting to develop regulations to protect their tax bases (Marriage Citation2017), some multinationals appear to have recognised changed societal values in this arena and acted ahead of, and/or beyond, the requirements of changed tax laws. In terms of externalities, well-functioning societies provide the context within which greater profits can be earned, and taxation provides the resources necessary for many crucial elements of a well-functioning society (Bird and Davis-Nozemack Citationforthcoming). In the words of the US Supreme Court Justice Oliver Wendell Homes in 1904 (as inscribed on the US IRS headquarters building in Washington, DC): ‘Taxes are what we pay for a civilized society’.

Businesses engaging in aggressive tax avoidance reduce funding available, for example, for education spending. This, in turn, can contribute to a lower skilled workforce in the future with all the negative social and economic consequences that flow from this, resulting in a more difficult future context within which these tax-avoiding companies would be seeking to operate. These externalities from aggressive tax avoidance may be too ambiguous to recognise, monetise and record within the companies’ accounting for externalities, but shorter-term impacts on reputation and brand value from aggressive tax avoidance becoming morally unacceptable to many stakeholders can be more identifiable. Brand and reputation risks and their probable financial impacts may be estimated (A4S Citation2012). In this way, what was previously a largely ignorable externality for tax-avoiding companies can become financially internalised through changes in the social contract caused by changing societal values.

6.2. The progressive internalisation of externalities

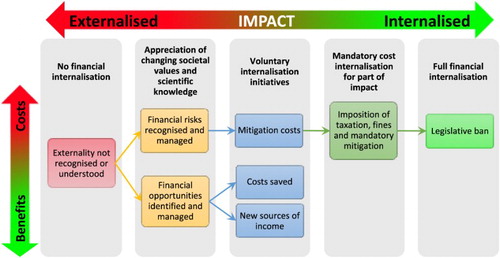

Social contract theory, in conjunction with greater clarity arising from developing scientific and sociological knowledge, suggests a continuum whereby positive and negative externalities can progressively become financially internalised over time, as shown in .

Figure 1. Internalising externalities continuum.

At the start of the continuum, an externality will be largely ignorable by the entity responsible for its production because it is not apparent that (or how) the externality will feedback into financial impacts for the entity. An assessment by the entity of low risk from the externality (or its failure to have even registered as a potential source of risk to the entity) will be from a combination of (1) lack of scientific or sociological awareness of the existence and/or impacts flowing from the externality and (2) lack of sufficient concern among the entity's economically powerful stakeholders in respect of the externality. For example, several decades ago there was limited awareness of global warming or the impact of human and organisational activities on global warming, and limited awareness of the potential impacts of global warming on economic prosperity. Therefore, at that time, it is unlikely that the contribution a manufacturing company's greenhouse gas emissions made to global warming would have begun to register as a negative externality or a potential associated financial risk for many companies. Although we now know that these greenhouse gas emissions endure in the atmosphere for a long period, such that many will still be contributing to severe global warming (IPCC Citation2014), at the time there was not sufficient scientific knowledge or societal concern for most businesses to recognise, record or act upon the externality of greenhouse gas emissions.

Moving along the continuum, changing ethical values among economically powerful stakeholders, whereby a number begin to develop concerns about a particular type of externality and disapprove of organisations responsible for this type of externality, may result in that externality becoming recognised in the entity's risk register. This is furthered where scientific knowledge develops to provide more certainty about impacts from the externality. However, societal concern may not be at a level where the externality is considered so detrimental by society that it is banned or regulated.

Nevertheless, it may progress further along the continuum to a point where a potential financial impact on reputation and brand value may be recognised in externalities accounts by some organisations (A4S Citation2012). For such externalities which are likely to have a financial impact, business-case reasoning can be used to highlight how they are relevant to business decision-making – both internally and by investors, and hence of relevance to financial markets (Hopwood et al. Citation2010). Returning to the example of greenhouse gas emissions, scientific knowledge developed to show that increasing concentrations of greenhouse gases in the atmosphere were contributing to dangerous climate change (IPCC Citation2014, USGCRP Citation2017, WMO Citation2017). This fuelled ethical concerns about climate change from human activities. These factors linked externalities of greenhouse gas emissions and long-term financial consequences for organisations (IPCC Citation2014), and also changed the terms of organisations’ social contracts where sufficient of their economically powerful stakeholders developed strong moral concerns over the social and environmental impacts from greenhouse gas emissions (Bebbington et al. Citation2014). As the balance changed, more organisations recognised and acted to reduce or mitigate their greenhouse gas externalities, with forms of quantification (not necessarily monetised) helping to ascertain and manage the greenhouse gas emissions from an organisation's different activities.

In parallel to the above stages associated with risks from externalities, financial opportunities can also be realised from recognition of some types of externalities: such as reducing costs and/or providing new sources of income through new products or service lines. For example, developments in the circular economy now value waste as a commodity to sell to other organisations (as an input into their processes) whereas previously it was regarded as a cost (of disposal).

Moving further along the continuum, much greater societal disapproval of a particular type of externality (and not just disapproval by stakeholders who have greatest economic power over the reporting entity) risks state, regional and/or local forms of taxation or fines being imposed on organisations, and/or mandatory requirements for organisations to take action to reduce or mitigate damage from the externality. Organisations are thereby forced through regulations to financially internalise some elements of the negative economic, social and/or environmental impacts for which they are responsible. This leads to much clearer and direct negative financial impacts feeding back onto the entity responsible, and much greater clarity in recording these impacts in transaction-based financial accounting and reporting. In the example of greenhouse gas emissions, the imposition of forms of carbon tax provides observable economic data for the organisations subject to these taxes to use as monetised metrics in accounting and reporting. By definition, the costs imposed on the organisation will be internalised in the organisation's financial performance so will no longer be externalities, but elements of the externality might still not be financially internalised where the taxes, fines and/or mitigation do not fully cover the social, ecological or broader economic impacts.

At the end of the continuum is a position where negative social, environmental and/or broader economic impacts of a particular action are considered very widely within a society to be so unacceptable that legislation is enacted to ban the action. This tends to happen for highly damaging externalities with a high level of intersubjective consensus regarding their undesirability and with relatively clear ways to avoid the externality. Relevant to the greenhouse gas example, to meet governmental commitments to intergovernmental accords, such as the December 2015 Paris Agreement, governments may need to severely curtail or ban certain sources of greenhouse gas emission, for example through policies adopted by some governments to eventually ban the sale of petrol and diesel powered cars (DEFRA Citation2017, Pickard and Campbell Citation2017).Footnote10

A key implication of the above internalising externalities continuum is that the further along the continuum a particular type of externality advances, the greater is the need for organisations responsible for this type of impact to actively manage it and internalise its impacts in financial decisions. With progressively greater financial internalisation, the former externalities should come clearly into the domain of financial accounting and reporting.

6.3. Organisational practices and financial internalisation of externalities

Another way to conceptualise the progressive financial internalisation of externalities is to link them to the qualitative characteristics of reporting outlined in Section 3. Producing a complete or comprehensive depiction of corporate performance requires material externalities data to be presented in a way that provides a context for understanding current impacts and future risks in the event that externalities should become financially internalised. This can be framed (using the thinking behind the Natural Capital Protocol) as a way of understanding the current dependencies an organisation has for future operations. The possible financial impact (value-relevance in conventional accounting terms) of these externalities is likely to relate to the nature of externalities as well as the probability that externalities will become financially internalised via the type of legal, fiscal or other means set out in the continuum in Section 6.2.

A monetised account of externalities (should it be possible to calculate within a range of accuracy) therefore might be important for developing a comprehensive depiction in financial reporting of the fair values of assets and liabilities of an organisation, the need for which is captured under the qualitative characteristic of representational faithfulness. Where externalities cannot be reliably monetised and/or if the likelihood of financial internalisation is low, one might not expect to see such externalities figures reported in financial reporting metrics, so narrative reporting drawing on externalities information traditionally within the domain of sustainability reporting becomes important.

Critically, given the framing of this issue in this paper around commensuration, the incommensurability of much externalities data, and gaps between current financial performance data and externalities data, leads to greater understanding that current financial reporting may be inaccurate (or misleading) in some key dimensions (which are unknown beyond published accounting for externalities experiments). What remains a challenge, therefore, is how accounting for externalities can help bridge this gap between information missing from financial reporting but that is currently partially provided in sustainability reporting. This is especially the case where externalities have a significant impact and/or where there is a process of progressive financial internalisation in play. As is evident from this paper, there are many examples of accounting for, and reporting of, externalities to draw from in starting the process of breaking down silos between financial and sustainability reporting, and between silos within sustainability reporting.

7. Summary and a research agenda

Externalities are an inherent feature of market economics. By their nature they can be elusive to identify in time and space and their ‘ownership’ is contested. In some cases, markets may continue to operate ignoring externalities. However, many externalities eventually make their presence felt. For example, it took some years for the link between tobacco sales and its health effects to be traced, acknowledged and financially internalised (at least to some extent via tobacco taxation and class action lawsuits). Externalities are also part of the ongoing dialogue between business and society about the nature of business responsibilities and allied duties of accountability.

Within the context of a rapidly growing relevance of externalities to corporate strategy and a need to bridge the gap between the reporting of externalities in the traditionally distinct domains of sustainability and financial reporting, the aim of this paper was to develop insights into accounting for, and reporting of, externalities that can help in advancing the effective use of externalities information in both financial and sustainability reporting for stakeholders seeking to more fully understand an entity's financial performance, position and prospects. There was a specific focus on the possibilities, challenges and limitations of quantifying externalities. Most corporate reporting frameworks indicate information should be comparable, complete, neutral and free from material error. While sustainability reporting frameworks recognise an important role for reporting of both qualitative and quantitative externalities data, quantified (and ideally monetised) data are often considered as ideal in meeting the criteria of comparability and neutrality. Externalities accounts are a potential source of such data – albeit with significant caveats.

This paper discerned four phases of accounting for externalities since the 1970s that aimed to identify and quantify an entity's externalities. These have moved from social audits through full cost accounting experiments and project evaluation tools to the most recent phase, characterised by thematic foci (including carbon and biodiversity accounting) and development of tools and frameworks to help identify, quantify, record and report externalities. The substantial complexities of interacting environmental, social and economic impacts indicate a need for contextual information to inform interpretation and understanding of externalities impacts (and risks). They also make it problematic to quantify many externalities in ways that are comparable, complete and neutral. This problem was explored in this paper from the perspective of commensuration and the implausibility of developing necessary levels of intersubjective consensus for metrics alone to convey meaningful information about the financial impacts of many externalities. The urgency of action on several externalities is unlikely to afford the time needed to develop adequate levels of intersubjective consensus for meaningful commensuration in this regard.

An approach which could more rapidly bring many current externalities more firmly within the domain of financial reporting is to recognise processes whereby externalities progressively become financially internalised. Drawing on social contract theory, this paper sketched a continuum of these processes. As societies become more aware of the urgency for meaningful action in many areas of sustainable development, it is possible, and perhaps even likely, that governments will intervene in ways that rapidly transform through regulation many current externalities into financial internalities.

For example, achievement by 2030 of many of the 169 targets within the UN's 17 Sustainable Development Goals, which all UN member states have supported, may necessitate urgent action at a pace that requires legislation. As many corporations and professional accountancy bodies are strongly committed to achievement of the Sustainable Development Goals, and accounting and reporting has a key role to play in their achievement (Bebbington and Unerman Citation2018), there may be considerable support within the profession for economically internalising many current externalities. The continuum set out in this paper could help inform further innovation in such interventions.

Regardless of whether or not quantification and monetisation techniques are used, current levels of production of sustainability and corporate responsibility reports implies that responsibility for the production of externalities is becoming ever more widely recognised, with implications for the need to reflect some of this information also in financial reporting. Effectiveness of sustainability reporting (and linked financial reporting) depends, however, upon the extent to which stakeholders use these reports as sources of information about externalities. While there is strong evidence from policy-makers that investors and other stakeholders are demanding greater levels of non-financial information within corporate reporting (see, for example, ICAEW Citation2017), interviewees for this study gave mixed messages on this point. For example, some viewed sustainability reporting as more of a ceremonial than substantive practice:

The mechanism of reporting is, in my opinion, one of the worst ways to fulfil a transparency and accountability obligation … there is a certain value to your first report internally … [but the value of] reports depreciate because there's rarely any consequences from that first report to the second report, third report, fourth report, fifth report, by the time you’re seventh to tenth to fifteenth report, the CEO isn't reading them anymore, … because there have been no consequences, good or bad … Reports are objectiveless … nobody knows what reporting is for and nobody does the kind of discipline and rigour of return on investment that they would do with anything else in business. Reporting is distinctly unbusiness-like in how it's fulfilled.

I generally gave up reading those reports quite a long time ago … issues that we care about are [often considered by managers as] not material to ongoing strategy, and are, therefore, … not include[ed] at all, or subjugate[ed] to a corporate sustainability report. … these are strategically important issues of material availability; pricing; legislation. Any decent corporate strategist that can't raise their eyes above a three-year horizon, and can't see the materiality of these issues, shouldn't be in the job.

7.1. Suggested future research directions

Drawing from the insights provided in this paper, the following research foci are suggested to form part of a research programme providing evidence to advance the effectiveness with which externalities information breaks down silos within which the traditionally discrete domains of financial reporting and sustainability reporting operate, and also changes siloed approaches within sustainability reporting itself. This is not an exhaustive list:

The usefulness and sufficiency in practice of existing sustainability reporting standards and frameworks for different types of externalities.

The impact of varied processes through which information on the financial impacts of externalities becomes integrated in, and affects, internal decision-making.

Case studies on innovative company experiments with accounting for externalities. These could, for example, use ethnographies to understand how accountants engage with and seek to develop accounts of externalities and report such externalities. A particular focus could be insurance companies, as a sector for which the externalities impacts of others is now recognised as a major financial risk in terms of much higher insurance claims (for example, the global reinsurance firm Aon Benfield has estimated that there were insured losses of US$132bn globally in 2017 from weather disasters (Aon Benfield Citation2018)).

The effectiveness of new non-financial reporting regulations, such as the 2014 EU Directive or its equivalent in other jurisdictions, in supporting provision of more extensive and sophisticated externalities information to markets.

Processes through which externalities information is integrated into investment decision-making, including how investment vehicles with long-term investment objectives such as pension funds are using externalities information.

The role of monetisation in commensurating externalities impacts that appear to be incommensurable in volume terms, and issues that arise from such attempts.

Ways in which innovations in technology and data analytics can be harnessed to produce more reliable and open externalities information. For example, investigating the potential of blockchain technology to provide open ledgers of individual types of externalities impacts, with accounting for externalities data from these blockchain ledgers being used in compiling full cost accounts by organisations at many stages of a supply chain.

The nature of silos in sustainability reporting between social, environmental, economic and financial impacts, and organisational change challenges in seeking to break down these silos.

Implications for assurance of corporate reports from frequent and broader recognition and reporting of externalities.

Changes needed in the training of accountants to equip them with skills necessary to develop and take forward accounting for, and reporting of, externalities, and to use this information in their trusted advisor capacity.

In addressing these and other questions raised by the challenges of accounting for, and reporting of, externalities, the conceptual difficulties of commensurating many social and environmental impacts (as highlighted in this paper) create tensions for researchers seeking to use methods that assume quantified proxies for social and environmental performance are objective. As externalities represent instances of market failure (Mildenberger Citationforthcoming), it might also be problematic to use market prices as objective variables in research into the accounting for, and reporting of, externalities. This implies there may be a restricted role for purely quantitative research into accounting for, and reporting of, externalities, with researchers needing to embrace the large range of rigorous methods available from the toolkit of qualitative and interpretative research (Broadbent and Unerman Citation2011) in undertaking impactful research into the complexities of accounting for, and reporting of, externalities.

High quality evidence and insights from academic research in these areas should help the accounting profession develop innovative and impactful interventions for the opportunities and risks associated with sustainable development. Growing awareness within many societies of the numerous types of negative externalities impacts on society, the natural environment and the economy arising from organisational activities, coupled with reducing tolerance for these impacts, makes organisational actions to reduce externalities ever more urgent and likely. It can also help transform these externalities into financial internalities, especially for (former) externalities that are captured within the growing momentum for legislative actions to tackle unacceptable impacts. This increases the relevance to investors of information on the financial consequences (including risks) for an entity from the social, environmental and broader economic impacts from its actions. These factors highlight the importance and urgency of continual innovations in corporate reporting for the provision of useful, comprehensive and comparable information on externalities.

Acknowledgements

We are very grateful to Paul Druckman, Chris Chapman, Mark Clatworthy, Juan Manuel Garcia Lara, Edward Lee, Robert Hodgkinson, Alison Dundjerovic and Gillian Knight for feedback in shaping and refining this paper, to the experts in non-financial reporting who gave their time and valuable insights in interviews for this study, and to participants at the ICAEW 2017 Information for Better Markets Conference for their comments and insights. We are also very grateful to Richard Spencer, Francesca Sharp and Chris Humphrey for their encouragement and support. All errors remaining in this paper are a result of our own unassisted work.

Disclosure statement