Abstract

Most companies disclose risk factors using vague, boilerplate language. Regulators are concerned that this vagueness reduces the decision-usefulness of the information; hence, they are encouraging companies to be more specific rather than generic. However, little is known about the impact of specificity on investment judgments. The results of this experimental study suggest that regulators’ concern may be justified. Non-professional investors who read a generic disclosure react less strongly immediately after reading it than those who read a more specific disclosure when prior information about the disclosed risk factor is available in their memory immediately before reading the risk disclosure. In addition, on realisation of the risk, they are more surprised than their counterparts who read a more specific disclosure, and lower their credibility judgments accordingly. These investors correct their judgments after the risk realisation to a greater extent than those who have read a more specific disclosure. The study has implications for regulators, managers, non-professional investors and researchers.

1. Introduction

The style of information conveyed by companies’ risk disclosures varies. For example, in their 2009 annual reports, Yahoo (Citation2009) specifically named Google, Microsoft, AOL and Facebook as its main competitors, whereas Google (Citation2009) broadly stated its competitors to be general-purpose search engines, social networking sites, and providers of online products and services. However, Yahoo has since started to use less specific language, and although some companies, such as Booking Holdings Inc., owner of booking.com, are still using more specific language (Booking Holdings Citation2020), generic language is increasingly being used in risk disclosures. More specific risk disclosures are those that explicitly state the nature of risks that are particular to a company by identifying precise facts or circumstances as prevalent sources of risk, while less specific disclosures are those that do not tailor the identified sources of risk to the company, but rather disclose more general facts and circumstances that may be common to other companies as sources of risk.

Regulators seem to be concerned about the use of generic information in risk disclosures. For example, the UK’s Financial Reporting Council (FRC) has sought to encourage disclosure of risks specific to the entity rather than common to the industry or all businesses (FRC Citation2011a), yet after nearly a decade it reports that boilerplate disclosures remain a problem in corporate reporting (FRC Citation2019). Use of boilerplate information is also seen as problematic elsewhere, including the USA (SEC Citation2019a,Citationb, Deloitte Citation2013). Using an experimental methodology, this study attempts to understand the effect of specificity on non-professional investors’ judgments, and validate regulators’ concerns about the decision-usefulness of boilerplate risk disclosures.

Previous accounting research on risk disclosures has focused on the determinants, content and usefulness of risk disclosures. Studies have found that size is an important determinant, as larger companies issue greater risk disclosures (Linsley and Shrives Citation2006), and that most risk disclosures contain narrative rather than quantitative content (Dobler Citation2008). Accounting research also reveals that managers make strategic choices about their disclosures (see Merkl-Davies and Brennan Citation2011, Hogan et al. Citation2017). For example, Dobler (Citation2008) suggests that managers are not incentivised to provide verifiable risk information. Other studies find that many risk disclosures lack useful firm-specific details (Kravet and Muslu Citation2013, Bao and Datta Citation2014), and that managers try to minimise disclosure of negative information (Yang and Liu Citation2017).

Nevertheless, risk disclosures are generally found to be useful to investors. In a European setting, Bozzolan et al. (Citation2009) find that the quantity of forward-looking risk disclosures is positively related to forecast accuracy, while Dia and Zéghal (Citation2008) find that measures of risk drawn from risk disclosures in Canada are reasonable proxies for traditional financial and accounting measures. The usefulness of risk disclosures is also confirmed in US settings (Kravet and Muslu Citation2013, Campbell et al. Citation2014, Hope et al. Citation2016).

In summary, accounting research finds that narrative risk disclosures, which account for the bulk of disclosures, are useful to investors but have some limitations. Companies vary in the extent to which they provide risk information and how they provide it, stemming from factors such as size, corporate governance and managerial incentives. Regulators’ concern that risk disclosures are too generic arises particularly from the fact that this may decrease the decision-usefulness of the information (FRC Citation2018). Previous research confirms the overall lack of firm-specific details in risk disclosures. However, little is known about how specific language impacts on investors’ judgments and decisions, and in which contexts, if any. Hope et al. (Citation2016) examine the market’s reaction to the specificity of risk disclosures, but their focus is on the absolute value of returns, and they make no directional predictions on how investors react to specific risk disclosures.

In seeking to fill this gap, this paper explores, in an experimental setting, some possible implications of companies choosing to be more or less specific in their risk disclosures. Drawing on the literature on cognition and perception in the general field of psychology, this study examines the effect of specificity on non-professional investors’ directional judgments, such as whether or not it decreases their likelihood of investing, risk perceptions and credibility perceptions, and its interaction with previous knowledge of the risk factor, as well as the extent to which these investors are surprised by the realisation of the risk. The paper addresses these research questions through the lens of theoretical constructs such as vividness and signalling, and finds that the higher level of vividness attributable to specific rather than generic disclosures impacts on how the specificity of a disclosure influences non-professional investors’ judgments and decision making. Although previous psychological studies have examined the effects of vivid information in a wide variety of contexts, their results are mixed, providing no clear evidence that vivid information impacts on investors’ judgments (Hales et al. Citation2011).

Specificity is different from, yet related to, vividness. The specificity of a risk disclosure refers to the extent to which managers explicitly choose to state precisely the nature of risks particular to their companies. Explicitness and precision make specific disclosures more vivid than their counterparts, so vividness is a quality of specific information, although not all vivid information is more specific. For example, Hales et al. (Citation2011) manipulate the vividness of information in news flashes without manipulating its specificity, to examine the validity of a concern that vividness may exacerbate swings in investor sentiment during bull and bear markets. In focusing on the style of risk disclosures over which management has discretion, this paper complements Hales et al. (Citation2011) by suggesting how managerial choices impact on investors’ judgments, and how these choices in turn influence the decision-usefulness of information.

Hales et al. (Citation2011) find that vivid information impacts on investors’ judgments only when the underlying information is preference-inconsistent rather than preference-consistent. The current research complements their study by examining another condition affecting non-professional investors’ judgments, namely whether or not they have any general information about the risk factor prior to reading the disclosure. Examining this condition is important, since if a risk factor is known to the market because of its macroeconomic implications, popularity or importance, investors are likely to have some knowledge of the risk before reading the disclosure.

This study also examines the impact of the specificity of risk disclosures on credibility judgments. This is an important issue because previous literature suggests that management credibility benefits companies by eliciting stronger reactions to management announcements, and by decreasing companies’ cost of equity (see Jennings Citation1987, Hirst et al. Citation2007). The popular press also suggests that companies benefit from having credible managers. For example, Forbes cites management credibility as one of the most important factors considered by potential investors, based on a survey of 321 institutional investors (Kelley Citation2013).

This study reveals that less specific disclosures significantly increase non-professional investors’ likelihood of investing before a risk is realised only when they have some prior general information about the disclosed risk factor. Furthermore, once the risk has been realised, non-professional investors who read less specific disclosures are more surprised and perceive managers to be less credible, and subsequently correct their investment and credibility judgments to a greater extent than those who read more specific disclosures. Examining non-professional investors’ reactions after the risk realisation is important, as the extent to which they are surprised and correct their judgments provides important insights into the informativeness of risk disclosures. If investors are well-informed about a risk, they are less likely to be surprised and correct their earlier judgments when it is realised. Hence the results suggest that boilerplate risk disclosures are less decision-useful than specific disclosures. Boilerplate language is also found to have an asymmetric effect on non-professional investors’ credibility judgments: while it has no significant effect before the risk realisation, it has a significant adverse effect after the risk realisation.

In the remainder of this paper, Section 2 reviews the related literature, Section 3 develops hypotheses, Section 4 describes the experimental design, Section 5 reports the results, and Section 6 draws conclusions.

2. Background

2.1. Risk disclosures

This study examines non-professional investors’ reactions to risk disclosures in companies’ filings. In many jurisdictions, risk disclosures are mandated by law or other regulations (El-Haj et al. Citation2020). For example, in the UK, the genesis of risk disclosures goes back to 1993, when the UK’s Accounting Standards Board (ASB) published a voluntary disclosure framework, the Operating and Financial Review, encouraging directors to discuss and analyse factors underlying the performance and financial position of their businesses (ASB Citation1993) to help readers to assess their likely future performance. The ASB particularly suggested that this should include principal risks and uncertainties. Interest in risk disclosures intensified following the corporate scandals of the early 2000s (Linsley and Shrives Citation2005), and The Companies Act 2006 mandated companies’ disclosure of principal risks and uncertainties in their annual reports (UK Government Citation2006).

Current regulations (UK Government Citation2013) mandate the disclosure of risk information in strategic reports. The FRC, which provides guidance on how strategic reports should be written, suggests that disclosures should include entity-specific information and that boilerplate information is of limited use to shareholders (FRC Citation2018). It defines specific information as particular facts or circumstances that may affect or have affected an entity (FRC Citation2018). It also suggests that investors find principal risk disclosures most decision-useful when they are specific to the company, allowing sufficiently detailed identification of risks (FRC Citation2017). Regulators in other jurisdictions afford similar importance to specificity. For example, in the US, according to Regulation S-K (SEC Citation2005, Citation2019a), companies should not present risks that might apply to any issuer or offering, but should explain how a particular risk affects the issuer or the securities being offered. In addition to principal risk disclosures, many other sections in company filings also include risk disclosures. For example, notes to financial statements refer to taxes and legal proceedings.

Two attributes of specific information are evident from the regulators’ definitions above: specific disclosures should be particular to a company, and should be sufficiently detailed to differentiate them from information attributable to broader groups of companies. For instance, in its 2009 annual report, Yahoo specifically identified Facebook as a competitor attracting more online time and thus increasing its share of online advertising dollars. This information was specific in naming a competitor and explaining why it posed a risk to Yahoo. In contrast, Google disclosed general social networking sites as its competitors, and did not explain which were a risk to Google and why. In other words, it failed to explicitly identify in sufficient detail the risk factors to which it was vulnerable. Some social networking websites may be a risk factor for a large number of companies for various reasons, whereas many others may pose no risk at all.

At the opposite end of the specificity continuum are generic or boilerplate disclosures. In its Guidance to the Strategic Report, the FRC (Citation2018) used the terms ‘generic’ and ‘boilerplate’ as antonyms of specific disclosures:

Information on how a particular fact or circumstance might affect, or has affected, the development, performance, position or future prospects of the entity and how it is responding to that fact or circumstance provides insightful information that can be used in the assessment of the entity’s future prospects. The inclusion of generic or ‘boilerplate’ information on its own is of limited use to shareholders.

2.2. Factors affecting risk perceptions based on specificity levels of risk disclosures

Fischoff et al. (Citation1993) posit that how risk is communicated is important because people may be misled by inaccurate risk perceptions. Based on the psychology literature, I argue that two factors relating to the level of risk disclosure specificity affect investors’ judgments: vividness and signalling.

2.2.1. Vividness

One of the most important determinants of reactions to possible future outcomes is the vividness with which those outcomes are described or represented mentally (Damasio Citation1994). Nisbett and Ross (Citation1980) define vividness as (a) emotionally interesting, (b) concrete and imagery-provoking, and (c) proximate in a sensory, temporal or spatial way. By giving explicit details particular to a company, specific information makes the images inherent in these details readily available to readers, making them more vivid.

Several studies suggest that vividness impacts on individuals’ judgments (for a review, see Slovic et al. Citation2004). For example, Johnson et al. (Citation1993) find that people are willing to pay more for airline travel insurance covering death from terrorist acts (a highly imaginable event) than death from all possible causes, which would implicitly subsume terrorist acts amongst the range of causes but would not bring fear-provoking mental images to mind. The results of previous psychological studies are mixed, providing no clear evidence that vivid information impacts on individuals’ judgments (Hales et al. Citation2011), although experimental studies in accounting suggest that, under certain circumstances, vividness (Hales et al. Citation2011) or its components (Sedor Citation2002, Riley et al. Citation2014, Elliott et al. Citation2015) may do so.

2.2.2. Signalling

Research on semiotics has examined how choosing a particular format of language when other formats are available reflects the speaker’s ‘active plan’ to communicate desired impressions to recipients of the message (see Sebeok Citation2001, Von Uexküll Citation1982). Previous accounting research indeed suggests that variations in the placement or descriptive content of information may signal its meaning or significance to decision makers (Koonce and Mercer Citation2005). Nelson and Pritchard (Citation2016) find that under a voluntary disclosure regime, firms subject to greater litigation risk use less boilerplate information in their risk disclosures. Kasznik and Lev (Citation1995) examine management disclosures and investors’ reactions to them in the face of an earnings surprise, and find that the bigger the earnings disappointment, the more concrete the warnings. They also find that firms tend to warn only of permanent earnings disappointments, and that the combined reaction to the warning and the subsequent earnings announcement is significantly more negative for firms that have warned investors than for firms that have not. A suggested explanation for these findings is that when a firm issues a warning, investors receive a signal that the earnings disappointment is permanent. Thus, in the styles they choose for their disclosures, managers appear to provide signals to investors, and investors appear to understand those signals.

3. Hypotheses

3.1 Effect of specificity on investment judgments

I argue that more specific risk disclosures are more vivid than less specific ones. Since more specific risk disclosures often give real-world examples with more explicit and concrete details than less specific disclosures, the former are potentially more interesting, concrete and image-provoking, and thus more vivid than the latter (Nisbett and Ross Citation1980).

Although information disclosed using less specific language may comprise at least the same information as, and possibly more than, that disclosed using more specific language (just as death from all possible causes subsumes terrorist attacks as well as other causes), specific information makes it easier for individuals to imagine what might happen under certain conditions. Information similar to that disclosed by Yahoo using more specific language (potential online advertising revenue losses arising from competition with Facebook) was captured in Google’s disclosure using less specific language (potential revenue losses arising from competition with social networking sites), but the latter was conveyed much less vividly.

Previous research (Nisbett and Ross Citation1980) suggests that vividness is the most important source of the availability heuristic, whereby people predict the probability of an event based on how easily an example can be brought to mind (Tversky and Kahneman Citation1973). Thus, the vividness of a more specific risk disclosure is likely to increase the availability of information, which will, in turn, increase the perceived seriousness of the risk factor, and thus decrease the likelihood of investment in the company.

Hales et al. (Citation2011) argue that vivid information affects investors’ judgments more than pallid information only when investors process the information deeply. Previous market-based research suggests that risk disclosures are taken seriously by investors (Kravet and Muslu Citation2013, Campbell et al. Citation2014, Hope et al. Citation2016); therefore, I expect investors’ decisions to be impacted by the specificity of risk disclosures.

Kasznik and Lev (Citation1995) find that managers use more concrete information in their warnings when the risk is more serious, and that investors appear to understand such signals. Based on this previous research, I contend that investors may believe that a manager disclosing more specific information signals that the disclosed risk is an important one for the company. However, extant research does not yet appear to provide direct evidence that investors’ signalling perceptions depend on the specificity of narrative risk disclosures.

In summary, I predict investors to be less likely to invest in a company because they perceive a risk to be more serious when the information is disclosed using more specific rather than less specific language. Thus, my first hypothesis is:

H1: Non-professional investors who read more specific risk disclosures are less likely to invest in a company than those who read less specific risk disclosures.

3.2. Interaction of prior risk knowledge and specificity with investment judgments

Kisielius and Sternthal (Citation1984, Citation1986) argue that elaboration of information increases the persuasiveness of vividness, and Petty and Cacioppo’s (Citation1986) elaboration likelihood model, in turn, suggests that the likelihood of elaboration is determined by motivation and ability to evaluate the information presented. Researchers suggest that prior knowledge not only increases one’s ability to evaluate information (Petty and Cacioppo Citation1986, Dochy et al. Citation1999), but also sparks further interest in the subject, both of which increase motivation to elaborate on the information (Tobias Citation1994).

As discussed for H1 above, vividness is the most important source of the availability heuristic (Nisbett and Ross Citation1980). According to Nisbett and Ross (Citation1980), the availability of information is likely to be enhanced by the numbers of units of information encoding the same conceptual fact and of sensory pathways storing the information. Similarly, Petty and Cacioppo (Citation1986) argue that prior knowledge creates a schema about an issue in individuals’ minds, which is cognitively bolstered when an external communication confirming this schema is presented. Kisielius and Sternthal (Citation1984, Citation1986) suggest that the greater the increase that vividness creates in associations between the message’s content and what is available in memory, the greater the effect of vividness on individuals’ judgments, thus explaining the link between availability of information and the effect of vividness on judgments.

In this study, the information that participants read in the prior information condition about competition being a risk within the industry was aligned with the message they read later in the risk disclosure. Therefore, they were more likely to elaborate on factors that increase competitive risk than their counterparts who did not have this prior information, and more elaboration increases the impact of vividness on judgments. When general risk information about a business is immediately available in the memory, additional details given in a specific disclosure are more likely to increase the number of associations between these details and what is already in memory. Indeed, Begg et al. (Citation1985) find that individuals are more persuaded about new details on familiar topics than on unfamiliar topics.

Thus, it is likely that when general risk information is already available in investors’ memory, specificity will have a greater impact on their judgments through its vivid characteristics, leading to my second hypothesis:

H2: The specificity of a risk disclosure has a greater impact on investment likelihood judgments for non-professional investors who have some prior information about the disclosed risk factor than those who have none.

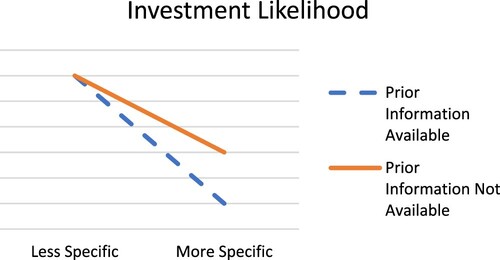

Figure 1. Predictions-H1 and H2. This figure presents predictions for the measures used in my experiment to capture participants’ investment likelihood judgments.

3.3. Implications of less specific versus more specific disclosure after a risk is realised

As I expect investors who receive a less specific risk disclosure to perceive the risk to be lower than investors who receive a more specific disclosure, I also expect them to be more surprised when the disclosed risk is later realised.

Schlenker et al. (Citation1994) posit that people are held responsible for an event to the extent that they seem to be connected with it, especially if they seem to have had personal control over it. In my study, the event referred to cautioning investors about a risk that had now been realised. Because managers have personal control over the specificity of disclosures, investors are likely to hold them responsible for these disclosures. Hence, I expect investors to blame managers who disclose a risk less specifically for communicating it inadequately. Indeed, Libby and Tan (Citation1999) find that failure to warn impairs management credibility, and Mercer (Citation2005) finds that immediately after the realisation of bad news, investors respond to less forthcoming disclosures by worsening their credibility judgments of managers.

Previous accounting research also suggests that investors lower their credibility judgments for less forthcoming managers only when they understand the financial reporting implications of the disclosure (Krische et al. Citation2014). If investors who receive less specific disclosures perceive the risk to be lower before the risk is realised, and are hence more surprised about its realisation, as previously predicted, they are likely to understand both the financial statement implications of the risk disclosure and management’s inadequate warning about such implications after the risk is realised. Therefore, on risk realisation, I expect investors to perceive managers who provide less specific disclosures as less credible than those providing more specific disclosures.Footnote1

In summary, since I expect non-professional investors who receive less specific disclosures to be more surprised on realisation of the risk, I predict that this will lead to lower credibility judgments for less specific managers. Therefore, my third hypothesis is:

H3: Non-professional investors who read less specific disclosures have lower credibility judgments of managers after risk realisation than those who read more specific disclosures.

4. Research method

I employed a two-by-two between-subjects experimental design.Footnote2 Participants read information about a hypothetical company and made judgments about their likelihood of investing in the company, as well as its riskiness and the credibility of its management. My research questions elicited non-professional investors’ reactions to the specificity of risk disclosures, and how specificity interacted with having some information about the risk factor prior to reading the disclosure. This experimental methodology allowed me to isolate these effects, which are confounded in the real world by other factors and disclosures.

4.1. Participants

In this study, 200 participants were recruited as proxies for non-professional investors via Prolific, a UK crowdsourcing site through which individuals are paid to complete academic surveys or experiments. Five participants did not complete the instrument, and 25 subjects failed one of the manipulation checks, as discussed in Section 5.1, leaving 170 participants.Footnote3 Peer et al. (Citation2017) compare Prolific and AMT, a similar crowdsourcing site, with more traditional participants and find both sites to be reliable in terms of the quality of attention and replication of previous results obtained from more traditional participant populations. Extant accounting research also supports the use of a crowdsourcing site (AMT), particularly for examining the judgments of less sophisticated investors (Rennekamp Citation2012, Buchheit et al. Citation2018).

The appropriateness of a particular group of participants depends on whether they have sufficient knowledge for the task (Libby et al. Citation2002). The task in this study involved judgments and decision making that required no specific expert knowledge. The dependent variables were not technical, and participants were asked questions about their likelihood of investing in the company, their perceptions of the risk, the credibility of management and the extent to which they were surprised about the realisation of the risk. The risk disclosures and news articles, which were the main areas of interest in the design, were written in plain English. The results reveal that participants had no difficulty in understanding the main manipulation. Therefore, the subject pool was deemed to be appropriate.Footnote4

Nevertheless, since the context is related to a financial disclosure, before seeing the manipulations, participants were given some financial information and background information about the company. Some expertise may have come into play in this section, as some participants may have been more financially literate than others. To ensure that the results were not impacted by such differences, I asked participants a pre-manipulation question about how attractive they found the company, and controlled its effect whenever this pre-manipulation response impacted on their later decisions (see Section 4.4). Furthermore, previous business education and investment experience had no significant effect on any of the dependent variables (all p-values > 0.1, two-tailed, untabulated). Sixty-nine per cent either had previous investment experience or were planning to invest in the future.Footnote5 In terms of demographics, 45% of participants were female and 55% male, and 61% had a bachelor’s degree or higher.

Previous market-based literature shows that small investors, who are typically non-professional, are influenced by variations in the language used in 10-Ks (Miller Citation2010),Footnote6 and that risk disclosures are used by investors and incorporated into their decisions (Kravet and Muslu Citation2013, Campbell et al. Citation2014). Importantly, this paper aims to be of relevance to regulators, who are concerned about generic disclosures (FRC Citation2018, Citation2017, Citation2011a, SEC Citation2013a) and who take particular account of non-professional investors in drafting their regulations (FRC Citation2011b, SEC Citation2013b).

4.2. Task

All participants received background information and excerpts from the financial statements of a hypothetical company, HiddenEscapes Inc., and were asked to assess the company’s overall attractiveness as an investment. At the beginning of the experiment, some randomly-assigned participants received an excerpt from an article published in a major business magazine which suggested intense competition amongst online travel agencies, and answered a question relating to the article (prior information condition). Other participants did not see this article (no prior information condition). All participants then received an excerpt from the company’s annual report about its competition risk.Footnote7 Some randomly-assigned participants received a more specific disclosure, and the rest a less specific risk disclosure.

After reading the risk disclosures, all participants evaluated their likelihood of investing, the riskiness of the company and the credibility of management. They then answered some demographic questions, which served as a distraction task and allowed some time to elapse before the next section of the study (risk realisation). The risk disclosure warned participants that competition might adversely affect the company and impact negatively on its revenues, so the risk realisation would be an adverse consequence of competition, such as a drop in market share and subsequent drops in revenues or share prices. Therefore, in the risk realisation stage, participants read a news item from the financial press about the company’s declining revenues and stock price due to a substantial loss of market share (risk realisation), following which they re-evaluated their likelihood of investing and management’s credibility. They also indicated how surprised they were by the adverse news.

Next, the participants answered an essay question in which they described any perceived attempts by management to signal insights beyond the facts given in the risk disclosure. They then answered some questions regarding the vividness and specificity of the information they had read.

4.3. Independent variables

The predictions were tested using a two-by-two experimental design that manipulated the company’s risk disclosure (less specific versus more specific), and whether or not participants had some information about the risk factors prior to reading the risk disclosure (prior information versus no prior information).

4.3.1. Specificity

Based on random assignment, half the participants received a less specific and the other half a more specific disclosure. The less specific disclosure broadly identified the parties comprising the source of competition risk (e.g. online specialist travel agencies) and how they might threaten the company (e.g. through greater brand recognition). The more specific disclosure explicitly identified the competitor parties (two hypothetical companies, FarEscapes Inc. and ExclusiveEscapes Inc.) and explained how they might threaten the company (e.g. one of the competitors had started to advertise on TV). The specificity levels in this study were based on real-world examples of more and less specific disclosures and the vividness literature, and were manipulated as follows.

Participants in the less specific condition received the following information:

We face intensive competition in every aspect of our business. We currently compete with other online travel agencies, other travel information providers on the web, and traditional travel agencies who can reach certain customers more easily. Some of these competitors have more financial resources than us, and can or are using these resources in a variety of ways to compete with us, including improving their brand recognition. It is likely that competition risk will adversely affect us in the future. If that occurs, competition will have a considerably negative impact on our revenues.

Participants in the more specific condition received the following information:

We face intensive competition in every aspect of our business. We currently compete with other online travel agencies, such as FarEscapes Inc. and ExclusiveEscapes Inc., internet search engines offering travel itineraries and recommendations, and traditional travel agencies who can reach elderly customers more easily. Some of these competitors have more financial resources than us, and can use these resources in a variety of ways to compete with us. For example, one of our competitors has started to advertise on television. It is likely that competition risk will adversely affect us in the future. If that occurs, competition will have a considerably negative impact on our revenues.

Two hypothetical online travel agencies were named as competitors in the more specific condition, whereas in the less specific case, no specific competitor names were given. Therefore, in the less specific case, it was up to the participants to bring to mind specific competitor online travel agencies.

In the less specific case, other travel information providers on the web were identified as a source of competition, which by definition included internet search engines offering travel itineraries and recommendations, although these were not explicitly mentioned; whereas in the more specific case, a type of business within that group was explicitly mentioned, namely internet search engines offering travel itineraries. Therefore, in the more specific case participants would have been able to call to mind general-purpose internet search engines such as Google and Bing, as well as specialist search engines such as Kayak and Expedia. On the other hand, participants in the less specific case would have been able to envisage Google, Kayak, Expedia, etc. as competitors, but would also have been able to call to mind travel websites providing reviews, such as TripAdvisor and airline companies, as all these companies provide travel information on the web.

In the more specific case, elderly customers were explicitly stated as a type of customer that traditional travel agencies can reach more easily; however, for the less specific group, no explicit definition was offered, and the participants were simply told that traditional travel agencies can reach ‘certain customers’ more easily, leaving it to them to imagine who these customers might be, whether elderly people, business people, other people, or a combination.

Lastly, in the less specific case, participants were told that some competitors were able to use, or were actually using, their financial resources to improve their brand recognition. The more specific case gave the example of advertising on television to improve brand recognition, whereas in the less specific case it was up to the participants to visualise ways of improving brand recognition. They might imagine TV advertising, as stated in the more specific condition, as well as radio, internet or newspaper advertising, loyalty programmes, price discounts, or a combination.

Since the less specific case defined the risk in broader terms, it actually suggested more ways than the more specific case in which competition might be a threat to the company. Therefore, ex ante the effects of vividness and signalling, there was no reason for participants to view the risk described in less specific disclosures as less serious than that described in more specific disclosures. See Appendix for more detail on the manipulation of specificity.

4.3.2. Prior knowledge of risk information

Participants in the prior information condition received some information about the industry’s competition risk by reading an article about the company’s risk disclosure from a major business magazine. This suggested that online travel agents were facing intense competition:

Online travel agencies are facing intense competition in their business. The internet continues to strongly influence the world in which we live. This has led to a substantial increase in the number of companies offering online travel services; consumers now have a lot of options which they can choose through online travel agents and third-party comparison sites.

4.4. Control variable

Investors’ assessments of companies differ because they are subjective judgments. These differences may stem from many factors that have nothing to do with the manipulations, such as individuals’ cognition, experiences or expertise in analysing financial information. This heterogeneity may cause large error variances in ANOVA if it has a significant effect on the variables (Kutner et al. Citation2005).

To combat this issue, I included a pre-manipulation measure. After giving the participants some general information about HiddenEscapes Inc. and its financial statements, but before providing any of the manipulations, participants were asked to rate ‘How attractive is HiddenEscapes Inc. as a potential investment?’ on an 11-point scale ranging from ‘1-Not attractive at all’ to ‘11-Very attractive’. I performed a bivariate Pearson correlation between participants’ pre- and post-manipulation judgments and identified variables that were significantly correlated with the pre-manipulation measure.

To control for the effect of the pre-manipulation judgment, I added the pre-manipulation measure (pre-attractiveness judgments) as a covariate into the model for variables that correlated significantly with the pre-manipulation measure, and hence used ANCOVA rather than ANOVA for analyses relating to these variables.

4.4. Dependent variables

The dependent variables used in my analyses before risk realisation were participants’ likelihood of investing and their assessments of the disclosed risk. The dependent variables after risk realisation were judgments of managers’ credibility and of investment likelihood, differences in these judgments before and after risk realisation, and the extent to which participants were surprised by the realisation of the risk.

5. Results

5.1. Manipulation and comprehension checks

Prior knowledge of risk information was actively manipulated in the prior information condition by giving participants information about the disclosed risk before they read the disclosure. After reading the information, they answered a question relating to it while they had access to the information. This was to ensure that they could call this information to mind while answering questions about the dependent variables. Asking a question about the information also encouraged them to pay appropriate attention to it, and served as a check to ensure that they had understood it. The question read: ‘Please explain in a few words what the article you just read was about.’ The aim was to make participants aware of competition in the industry, which was the subject of the risk disclosure that they would later read about. Therefore, participants’ answers were coded as ‘0’ if they did not mention competition and ‘1’ if they did; 73.4% of participants did mention competition and the rest did not. A t-test revealed that the mean answer was significantly different from 0 (p-value < 0.01, two-tailed, untabulated), suggesting that my manipulation had been successful overall. For robustness, I excluded participants who did not pass this manipulation test from my analyses.

In order to measure whether specificity had been manipulated successfully, I asked the participants three questions and conducted an ANOVA, setting specificity judgments as the dependent variable, and specificity and prior information as the independent variables. All questions were measured on an 11-point scale. The first question referred to the regulator’s definition of specificity, being entity-specific (FRC Citation2018, SEC Citation2009b). The second measured specificity in terms of the extent to which the information explicitly stated the nature of the risk by identifying the circumstances comprising its source (SEC Citation2009b, FRC Citation2018). The third related to the outcome of being specific: if a disclosure discloses risks that are unique to the company and is explicit about the nature of the risk by identifying the circumstances that comprise its source of risk, it is likely to include some details of the risk factor (FRC Citation2017). Mercer (Citation2005) posits that providing details is a part of forthcomingness. Therefore, my fourth question was on the extent to which participants found more specific managers to be more forthcoming.

Participants found the more specific disclosure to be significantly more entity-specific (mean: 7.17 versus 6.14), explicit (mean: 8.45 versus 7.42) and detailed (mean: 7.07 versus 5.80), and management to be more forthcoming (mean: 8.46 versus 7.97) than participants in the less specific condition (all p-values for disclosures < 0.01; p-value for management forthcomingness = 0.09, two-tailed, untabulated), suggesting that the specificity manipulation was successful.

To measure participants’ comprehension, I asked them three true/false questions to measure correct detection of a group of competitors, a competitive disadvantage of the company, and one possible competitive advantage of the competitors. I then took the average of these three comprehension questions. The average of correct answers was 93.7% across all participants, suggesting that they had paid sufficient attention to the disclosures. None of the independent variables had a significant effect on the number of correct answers, and there were no significant differences across conditions (p-values > 0.1).

5.2. Hypothesis tests

5.2.1. Judgments before risk realisation

H1 examined whether the specificity of risk disclosures impacts on non-professional investors’ judgments of their likelihood of investing, and H2 examined whether specificity has a stronger impact on the likelihood of investing when some prior information about the disclosed risk factor is available in non-professional investors’ memories before reading the risk disclosure. I measured participants’ likelihood of investing by asking: ‘What is the likelihood you would consider HiddenEscapes Inc. as a potential investment?’

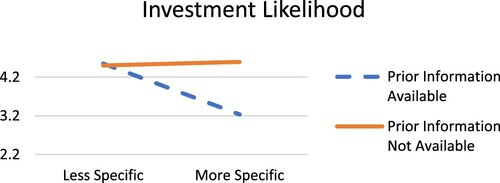

Panel A of reports the descriptive statistics, Panel B reports the marginal means, and Panel C reports the results of the ANCOVA using investment likelihood judgments as the dependent variable, specificity, availability and their interaction as the independent variables, and participants’ pre-attractiveness judgments as the covariate.Footnote9 The results suggest that the specificity of risk disclosures impacted on participants’ investment judgments (p < 0.01, two-tailed): they were less likely to invest when the disclosure was more specific than when it was less specific. Furthermore, availability of prior information interacted significantly with specificity (p < 0.01, two-tailed). Panel D of reports the results of the simple effects test. Specificity had a significant impact on participants’ judgments of their likelihood of investing when they had some prior information about the disclosed risk factor, (p < 0.01, two-tailed), but not when they did not have that information (p = 0.723, two-tailed).

Table 1. Tests for hypotheses H1 and H2.

H1 and H2 are built on the assumptions that more specific risk disclosures increase non-professional investors’ risk assessments, and that this effect is stronger when some prior information is available in their memories. Following previous accounting research (Koonce et al. Citation2005b), I measured participants’ overall risk assessments with the question, ‘How serious a risk do you believe HiddenEscapes Inc. faces from competition?’Footnote10

An ANOVA using the risk judgments as the dependent variable, and specificity and prior information as the independent variables suggested that the specificity of the risk disclosure impacted on participants’ riskiness judgments (p < 0.01, two-tailed, untabulated): they perceived more riskiness when the disclosure was more specific (mean = 8.35, untabulated) than when it was less specific (mean = 7.73, untabulated).Footnote11 As in the likelihood of investing judgments, availability of prior information interacted significantly with specificity (p = 0.08, two-tailed, untabulated). Furthermore, a simple effects test revealed that when participants had some prior information about the disclosed risk factor, specificity impacted significantly on their risk judgments (p < 0.01, two-tailed, not tabulated), whereas it had no significant effect when they did not have that information (p = 0.544, two-tailed, not tabulated).

The results reveal that specificity has a significant impact on non-professional investors’ judgments only when they have some prior information about the disclosed risk factor. See for a graphical depiction of the results.

Figure 2. Results for H1 and H2. This figure presents the estimated marginal means of the measures used in my experiment to capture participants’ investment likelihood judgments.

This result differs somewhat from the predictions depicted in . Specificity had no effect on the participants’ judgments when they had no prior information before reading the disclosures – the line in this condition is almost flat. In other words, the significant effect of specificity is driven solely by the prior information condition. This contrasts with previous evidence on management’s beliefs about the impact of specificity on investors’ judgments, which suggests that companies prefer to make less specific rather than more specific disclosures because they are concerned that the latter will decrease investors’ likelihood of investing (Kasznik and Lev Citation1995, Rolfe and Troob Citation2001). My results suggest that this effect is context-specific and only occurs when non-professional investors have some prior information about the risk factor before reading the risk disclosure.

5.2.2. Judgments after risk realisation

The first two hypotheses relate to participants’ judgments before the realisation of the risk, whereas the last hypothesis focuses on judgments after the risk realisation. As the previous hypotheses predicted that non-professional investors would react less to generic risk disclosures before the realisation of the risk, I expected participants who had read generic disclosures to be more surprised on realisation of the risk than those who had read more specific disclosures. This expectation was confirmed by an ANCOVA using participants’ surprise rating as the dependent variable, obtained in response to the question ‘How surprised were you by the news about HiddenEscapes Inc.’s market share decline?’, specificity and prior information levels as the independent variables, and pre-manipulation attractiveness as the covariate.Footnote12 Untabulated results showed a significant impact of specificity on the dependent variable in the predicted direction (p < 0.01, two-tailed): participants who had received the less specific risk disclosure were significantly more surprised (mean = 4.24) than those who had received the more specific risk disclosure (mean = 3.15).

H3 predicted that, after a risk has been realised, non-professional investors’ credibility judgments will be lower when management has used less specific information in a disclosure than when more specific information has been used. Following previous accounting research, I measured credibility judgments with a composite measure of trustworthiness and competence (Mercer Citation2005). Having posed the questions ‘How trustworthy is HiddenEscapes Inc.’s management?’ and ‘How competent is HiddenEscapes Inc.’s management at providing risk disclosures?’, both before and after the risk was realised, I took an arithmetic average of trustworthiness and competence judgments to construct my credibility variable for both before and after the risk realisation. I conducted an ANCOVA using pre-manipulation attractiveness judgments as the covariate, the credibility construct after risk realisation as the dependent variable, and availability of prior information and specificity as the independent variables.Footnote13 The results presented in support my hypothesis: participants in the more specific risk disclosure condition made significantly higher credibility judgments after risk realisation than those in the less specific disclosure condition (p = 0.07, two-tailed).

Table 2. Test for hypothesis H3.

Importantly, specificity had no significant impact on the credibility construct before risk realisation (p = 0.754, two-tailed, untabulated), suggesting that specificity has an asymmetric effect on non-professional investors’ credibility judgments. Although being less specific has no significant effect on credibility judgments before risk realisation, it has a significant adverse effect on judgments after risk realisation.

I expected a lower level of corrections to judgments on risk realisation when non-professional investors receive a more decision-useful risk warning than a less decision-useful risk warning. To investigate the decision-usefulness of the risk disclosures for credibility judgments, depending on the level of specificity, I analysed whether participants who had read the less specific disclosures updated their credibility judgments after the risk realisation more than those who had read the more specific disclosures. I conducted an ANOVA using the difference between the credibility construct taken before and after the risk realisation as the dependent variable, and specificity and availability as the independent variables.Footnote14 The results tabulated in Panel D of suggest that specificity had a significant effect on the decrease in credibility judgments after risk realisation (p = 0.05, two-tailed). Participants who had read the less specific disclosure lowered their credibility judgments on risk realisation (mean = 0.78) significantly more than participants who had read the more specific disclosure (mean = 0.26, untabulated).

Similarly to credibility judgments, to explore the decision-usefulness of more versus less specific disclosures for investment likelihood judgments, I conducted an ANCOVA using the difference in investment likelihood judgments before and after risk realisation as the dependent variable, specificity and availability as the independent variables and pre-attractiveness judgments as the covariate. The results show that specificity had a significant effect on this measure (p = 0.052, two-tailed, untabulated): the decrease in investment likelihood after risk realisation was significantly smaller for participants who had read the specific risk disclosures (mean = 0.83) than those who had read the generic risk disclosures (mean = 1.34; means untabulated). This suggests that generic risk disclosures are less decision-useful than specific risk disclosures for investment likelihood judgments.

The analyses after risk realisation reveal that participants who had read the less specific judgments were more surprised on risk realisation and corrected their investment and credibility judgments significantly more than those who had read the more specific risk disclosures. Moreover, specificity has an asymmetric effect on non-professional investors’ credibility judgments before and after the risk realisation. While being less specific has no significant effect on credibility judgments before risk realisation, it has a significant adverse effect on judgments after risk realisation. As previous accounting research suggests that credibility benefits companies in the long term (Jennings Citation1987, Tucker Citation2007), and that consistent behaviour that serves investors’ interests pays off in the long run (Pfarrer et al. Citation2010), being less specific may have a more adverse effect on investors’ judgments in the long term.

Although participants lowered their investment likelihood judgments on risk realisation more when they read a generic rather than a specific disclosure compared with their judgments before risk realisation, investment likelihood judgments after risk realisation did not differ significantly between participants who had read more versus less specific disclosures, despite the significant positive impact of specificity on their credibility judgments. An ANCOVA was conducted using participants’ likelihood of investment judgments after the risk realisation as the dependent variable (measured by the question ‘What is the likelihood you would consider HiddenEscapes Inc. as a potential investment?’ measured on an 11-point scale from ‘1-Not at all likely’ to ‘11-Very likely’), specificity and prior information as the independent variables, and participants’ pre-manipulation attractiveness judgments as the covariate.Footnote15 This revealed that specificity does not have a significant impact on investment likelihood judgments after risk realisation (p = 0.725, two-tailed, untabulated).

This result is in line with the finding of previous research that being forthcoming does not immediately improve investment judgments, and that judgments focus on the valence of the news (Kasznik and Lev Citation1995, Elliott et al. Citation2011). On reading the news about the risk realisation, namely a drop in management earnings forecasts as a result of a loss in market share due to competition, participants indeed seemed to focus on the negative news about the earnings in the short term.

5.4. Additional analysis: vividness, signalling, and mediation

5.4.1. Vividness

Previous psychology literature suggests that vivid disclosures are more interesting, concrete and easier to imagine than pallid disclosures (Nisbett and Ross Citation1980). I took several steps to measure whether participants perceived more specific information to be more vivid. I asked participants (1a) how easy it was to visualise HiddenEscapes Inc.’s competitors; (1b) how easy it was to visualise how HiddenEscapes Inc. could compete; (2) how concrete was the disclosure; and (3) how interesting was the disclosure. I conducted an AN(C)OVA series using vividness component judgments as the dependent variable, and specificity and prior information as the independent variables.Footnote16 All questions were measured on an 11-point scale. The results indicate that the participants perceived the more specific disclosures to be more interesting, concrete and easier to imagine than the less specific disclosures, showing a significant effect of the level of specificity on vividness judgments (p < 0.04, two-tailed for all components, untabulated).

I conducted a principal component analysis on participants’ vividness judgments, which gave me a single underlying factor for vividness, explaining 65% of the variance, with an eigenvalue of 2.602. I then ran an ANOVA using the vividness factor as the dependent variable, and specificity and prior information as the dependent variables.Footnote17 Similarly to the individual measures, specificity had a significant effect on the vividness factor (p < 0.01, two-tailed, untabulated).

5.4.2. Signalling

Previous accounting research suggests that variations in the placement or description of information may signal its meaning or significance to decision makers (Koonce and Mercer Citation2005). Indeed, it is suggested that companies typically signal their riskiness through more specific disclosures to avoid litigation, and that investors appear to understand these signals (Kasznik and Lev Citation1995, Nelson and Pritchard Citation2016).

To explore whether or not participants perceived any management signalling in my setting, I measured their signalling perceptions with the following open-ended question:

Some managers try to signal to investors some additional insights about their companies’ future prospects by the language they use in their disclosures beyond the facts given in the risk disclosure. Do you think HiddenEscapes Inc.’s management tried to signal any additional insights beyond the facts given in the risk disclosure? If so, what do you think they tried to signal?

I coded the answer as 0 if a participant stated that there was no signalling, and as 1 otherwise. I then conducted a binary logistic regression, setting the coded signalling opinion as the dependent variable, and specificity, prior information and their interaction as the independent variables.

Untabulated results showed that none of the variables had an impact on participants’ signalling judgments (all p-values > 0.1, two-tailed), suggesting that the specificity of disclosures had no impact on participants’ signalling perceptions. However, these results should be interpreted with a caveat. To ensure that the question did not interfere with the measures used to test the hypotheses, the measure was taken after the participants had been made aware that the risk had been realised. The participants may have perceived some management signalling depending on the specificity of the disclosure before the risk realisation. Indeed, more than 65% of participants thought that management had signalled something, and many participants under each condition talked in their answers about a drop in the market share, as given in the news pertaining to the risk realisation (for example, ‘They tried to signal a drop in market share and profits’), suggesting that news of the realisation brought some noise to this measure.

5.4.3. Mediation

The discussions pertaining to H1 and H2 suggest that specificity has an impact on non-professional investors’ judgments through vividness and possibly through signalling. The results suggest that specificity impacted on participants’ vividness judgments, but not on their signalling judgments. Furthermore, since participants assessed their likelihood of investing in the company after reading the risk disclosures, one would expect their risk judgments to affect their investment likelihood judgments, as suggested in Section 3.1. Overall, my theoretical model and results suggest that (1) vividness mediates the relationship between specificity and risk perceptions, and (2) risk perceptions mediate the relationship between vividness and investment likelihood judgments.

Following extant accounting literature (e.g. Rennekamp Citation2012, Farrell et al. Citation2017), I conducted the mediation analyses mentioned above using the bootstrapping method developed by Preacher and Hayes (Citation2008). Bootstrapping generates a sampling distribution of the indirect effect (of the independent variable on the dependent variable through the mediator variable) from re-samples of the data with a replacement and generates a confidence interval for its value. For each analysis, I conducted 2,000 iterations and used confidence intervals at a 90% significance level; the lack of 0 in an interval suggests significance at that level or above.

My first analysis measured the indirect effect of specificity on risk perceptions via vividness (specificity and risk judgments mediated by vividness). The independent variable was specificity, the dependent variable was participants’ overall risk perceptions, and the mediator was vividness judgments measured as the vividness factor underlying participants’ perceptions of the individual vividness components, as explained in Section 5.4.1. Availability of prior information, its interaction with specificity, and pre-attractiveness judgments were the covariates used in the analysis. The analysis generated a confidence interval of 0.123–0.520. A significant p-value (< 0.01) suggested that vividness mediated the relationship between specificity and risk judgments.

My second analysis measured the indirect effect of vividness on investment likelihood judgments via risk perceptions (vividness and investment likelihood judgments mediated by risk perceptions). The independent variable was vividness judgments, the dependent variable was participants’ judgments of their likelihood of investing in the company, and the mediator was overall risk perceptions. Specificity, availability of prior information, their interactions, and pre-attractiveness judgments were the covariates in the analysis. The analysis generated a confidence interval of −0.219 – −0.059. A significant p-value (< 0.01) suggested that risk perceptions mediated the relationship between vividness and investment likelihood judgments.

6. Conclusions

More specific disclosures are those that explicitly state the nature of risks by identifying the parties or circumstances comprising the source of risk, whereas less specific risk disclosures do not explicitly identify the source of risk. The generic nature of risk disclosures has long been of concern to regulators. This paper has examined the possible implications for companies of choosing to make more or less specific risk disclosures in the context of non-professional investors’ decision making.

The study reveals that more specific disclosures significantly increase non-professional investors’ risk perceptions and decrease their likelihood of investing only when they have some prior information about the disclosed risk factors before reading the risk disclosures, and that specificity has no impact on their credibility judgments of managers at this point. However, once a risk is realised, non-professional investors who read less specific disclosures lower their judgments of credibility and likelihood of investing more than those who read more specific disclosures, and are more surprised by realisation of the risk. These results suggest that less specific risk disclosures are less decision-useful to non-professional investors than more specific disclosures.

As far as I am aware, this study provides the first evidence that boilerplate disclosures are less decision-useful than more specific ones. Regulators have long been concerned about this, and my results from a non-professional investor context suggest that their concern is justified. My study is also relevant to managers and non-professional investors, as it shows some adverse consequences of providing and reading boilerplate disclosures.

The results speak to Hope et al.’s (Citation2016) finding that investors react more strongly to more specific disclosures, but do not make any directional inferences. On the one hand, Hope et al. (Citation2016) concur that more specific risk disclosures may impact negatively on returns through how they change investors’ perceptions. On the other hand, they argue that the precision of the more specific disclosures may decrease the cost of equity. My study complements Hope et al. (Citation2016) by providing some evidence in relation to both arguments: specific risk disclosures, at least in certain contexts, increase non-professional investors’ risk perceptions at the time that they read them, but improve management credibility after realisation of the disclosed risk, which in turn has a negative impact on cost of equity (Jennings Citation1987).

The results may be of interest to regulators, since they suggest that more guidance may be needed from regulators to help companies make their risk disclosures more decision-useful. Indeed, extant research finds that the decision-usefulness of financial information has been deteriorating (Lev Citation2018).

Previous research suggests that managers generally provide risk disclosures lacking firm-specific details (e.g. Kravet and Muslu Citation2013) and try to minimise disclosures of negative information (Yang and Liu Citation2017). Therefore, decisions to issue generic risk disclosures may result from management’s expectation of adverse investor reactions to specific disclosures. However, research on ‘scripted’ or planned decision making underlines that although scripted decision making is an efficient tool reflecting the likely outcomes of a decision from the perspective of the decision maker, it does not always lead to appropriate decisions because it may fail to take account of fine yet important details (Gioia and Poole Citation1984). Indeed, this study suggests that although, in some contexts, generic risk disclosures lead to lower risk perceptions than their specific counterparts, they have an adverse asymmetric effect on non-professional investors’ credibility perceptions. Being less specific does not impact on the extent to which non-professional investors perceive managers to be credible before a risk is realised, but does have a significant adverse effect on credibility judgments after a risk is realised. Hence, the results of this study should be of interest to managers.

The results suggest that non-professional investors may react less strongly to a less specific disclosure than to a more specific disclosure. Differential inferences in decisions based on the format of information may hinder investors’ ability to make informed decisions if their inferences are incorrect (Koonce et al. Citation2005a). Therefore, investor education programmes might focus on the impact of specificity on non-professional investors’ inferences, and aim to encourage them to reflect on and critique their inferences.

As with any experimental research, this study has limitations. The experimental materials did not fully represent what would normally be available when investors make decisions, as asking participants to evaluate a greater volume of material would have required more time than could realistically be requested.

As is typical of experimental designs, to maximise the strength of the relationship between cause and effect, an artificial environment was created that isolated many other potentially important factors that were not the focus of this study but are confounded in natural environments. Hence, there should be no expectation that the results will be replicated every time a non-professional investor reads a risk disclosure, because in natural environments additional information competes for investors’ attention. The specificity of risk disclosures is one of these influential factors that impact on investors’ decision making, and its effect on ultimate investment judgments or decisions may be weaker in natural environments where other competing factors are simultaneously present. However, studying one of these factors in isolation contributes to our understanding of how non-professional investors make decisions, as investment decisions are driven by a combination of factors.

In experiments, participants’ attention is inevitably steered toward what is being examined, such as risk disclosures as in this study. Therefore, evidence suggesting that these disclosures impact on investors’ judgments in natural environments where such attention steering is absent is important. Previous studies of risk disclosures in natural environments (e.g. Kravet and Muslu Citation2013, Campbell et al. Citation2014, Hope et al. Citation2016) all confirm that these disclosures influence investment judgments, corroborating the importance of the focus in this study.

To avoid asking too many questions and distracting the participants, signalling perceptions were measured in this study with a single question after all other measures, including participants’ reactions to the risk realisation, had been collected. The results suggest that participants anchored on the realisation of the news while answering the question, which brought some noise to the results. In addition, signalling perceptions are inherently context-dependent (Hogarth and Einhorn Citation1992). Future researchers might combat these issues by developing different measures to examine the impact of specificity on signalling judgments, and by testing signalling in different contexts, such as in interactive settings where signalling is more prevalent.

Accounting research indicates that credibility is particularly beneficial for companies in the long term (Jennings Citation1987, Pfarrer et al. Citation2010), whereas this paper examines the impact of specificity on non-professional investors’ judgments in the short term. Future research might examine if and how being consistently specific impacts on judgments in the long run.

Both anecdotal evidence and previous studies suggest that although managers tend to avoid specific risk disclosures, there are exceptions. Therefore, researchers might examine what factors encourage managers to disclose their risks more specifically. Previous studies have found that riskier firms provide lengthier risk information (Campbell et al. Citation2014, Nelson and Pritchard Citation2016). However, the relationship between company riskiness and the specificity of risk disclosures in a mandatory risk disclosure regime appears to be an as yet unexamined area for future research.

Acknowledgements

This paper is based on my dissertation at the University of Illinois at Urbana Champaign. I thank the members of my dissertation committee for their valuable guidance and support: Kevin Jackson (chair), Jessen Hobson, Sharon Shavitt, and Steve Smith. I appreciate the constructive comments of two anonymous reviewers and suggestions of Frank Hartman (Associate Editor). I also thank Fiona Anderson-Gough, Carolyn Cordery, Ivo De Loo, Louise Gracia, Susan Krische, Justin Leiby, David Marginson, Marc Painter, Kristina Rennekamp, Brian White, and participants at the ABO Research Conference, Aston University Accounting Department brown bag, accountancy workshops at University of Illinois at Urbana-Champaign and University of Warwick for their helpful comments and suggestions. I devote this manuscript to the loving memory of Huseyin Leblebici without whose mentoring and wisdom its publication would not have been possible.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Notes

1 I have no hypothesis about the impact of specificity on investors’ credibility judgments before risk realisation, as negative warnings create two counteracting forces (Libby and Tan Citation1999). On the one hand, management’s forthcomingness may improve investors’ credibility judgments, while on the other hand, the increase in the perceived riskiness of the company may decrease investors’ credibility judgments.

2 Ethical approval was obtained to use human subjects for the experiment.

3 Forty-nine per cent of participants resided in the UK, 32% in the USA and 19% in other countries. Their current residence had no impact on any of the reported statistical tests.

4 An additional quality control measure was to recruit participants who had a previous approval rating of at least 90%, who would direct appropriate attention to the experimental task.

5 These were measured by asking participants whether they had bought or sold a company’s common stock or debt securities, or planned to do so.

6 Form 10-K, an annual report that must be filed by public companies in the US, provides a comprehensive overview of the company’s business and financial condition, including audited financial statements (SEC Citation2009a).

7 Competition risk is a frequently reported risk factor, but most such disclosures are quite generic, akin to other risk disclosures (Bao and Datta Citation2014).

8 Investors may also receive specific information about a risk factor, such as a competitor’s entry into the market, before reading risk disclosures. Depending on its prevalence, this information may swamp all the language effects, as well as creating information differences between participants. Therefore, this study focused on general rather than specific prior information.

9 As explained in Section 4.4, ANCOVA was used because the correlation between pre-attractiveness judgments and investment likelihood was significant (p < 0.01).

10 Previous research suggests that the probability and size of the outcome are the most prominent dimensions of risk (Slovic and Lichtenstein Citation1968). Therefore, I measured participants’ perceptions of these two factors separately, and took their arithmetical averages to set up a construct representing these dimensions. A Cronbach’s alpha of 0.73 between this construct and participants’ overall risk perceptions confirmed an adequate level of internal consistency between the two (Nunnally Citation1978).

11 As explained in Section 4.4, an ANOVA was used since the correlation between risk judgments and pre-attractiveness judgments was not significant (p = 0.227).

12 An ANCOVA was used since the correlation between the surprise variable and pre-attractiveness judgments was significant (p < 0.01).

13 An ANCOVA was used since the correlation between the credibility construct after risk realisation and pre-attractiveness judgments was significant (p = 0.01).

14 An ANOVA was used since the correlation between the difference in credibility construct before and after risk realisation and pre-attractiveness judgments was insignificant (p = 0.464).

15 An ANCOVA was used since the correlation between post-realisation investment likelihood judgments and pre-attractiveness judgments was significant (p < 0.01).

16 ANCOVA was used when the correlation between a component and pre-attractiveness measure was significant; otherwise ANOVA was used (p-values of the correlations untabulated). The questions asked to measure the dependent variable, with the means for specific and less specific conditions respectively, were: ‘When you first read the disclosure, how easy was it for you to visualise HiddenEscapes Inc.’s competitiors?’ (8.40 vs. 7.66); ‘How easy was it for you to visualise how HiddenEscapes Inc.’s competitors could compete with HiddenEscapes Inc.?’ (8.58 vs. 7.84); ‘How abstract or concrete is HiddenEscapes Inc.’s risk disclosure?’ (7.80.vs. 7.06); and ‘How interesting is HiddenEscapes Inc.’s risk disclosure?’ (7.18 vs. 6.28).

17 An ANOVA was used since the correlation between the vividness factor and pre-attractiveness was not significant (p = 0.283).

References

- ASB, 1993. Operating and Financial Review. London: The Accounting Standards Board.

- Bao, Y., and Datta, A., 2014. Simultaneously discovering and quantifying risk types from textual risk disclosures. Management Science, 60 (6), 1371–1391.

- Begg, I., Armour, V., and Kerr, T., 1985. On believing what we remember. Canadian Journal of Behavioural Science / Revue Canadienne des Sciences du Comportement, 17 (3), 199–214.

- Booking Holdings, 2020. Booking Holdings Inc.: Form 10-K. https://sec.report/Document/0001075531-20-000011/.

- Bozzolan, S., Trombetta, M., and Beretta, S., 2009. Forward-looking disclosures, financial verifiability and analysts’ forecasts: a study of cross-listed European firms. European Accounting Review, 18 (3), 435–473.

- Buchheit, S., Doxey, M., Pollard, T., and Stinson, S.R., 2018. A technical guide to using Amazon’s mechanical Turk in behavioral accounting research. Behavioral Research in Accounting, 30 (1), 111–122.

- Campbell, J.L., Chen, H., Dhaliwal, D., Lu, H., and Steele, L.B., 2014. The information content of mandatory risk factor disclosures in corporate filings. Review of Accounting Studies, 19 (1), 396–455.

- Damasio, A.R., 1994. Descartes’ Error: Emotion, Reason, and the Human Brain. New York, NY: Putnam.

- Deloitte, 2013. SEC Comment Letters Including Industry Insights: Constructing Clear Disclosures. London: Deloitte Development LLC. http://deloitte.wsj.com/riskandcompliance/files/2013/12/SEC-Comment-Letters-2014-Including-Industry-Insights-2014-Constructing-Clear-Disclosures.pdf.

- Dia, M., and Zéghal, D., 2008. Fuzzy evaluation of risk management profiles disclosed in corporate annual reports. Canadian Journal of Administrative Sciences/Revue Canadienne des Sciences de l’Administration, 25 (3), 237–254.

- Dobler, M., 2008. Incentives for risk reporting — a discretionary disclosure and cheap talk approach. The International Journal of Accounting, 43 (2), 184–206.

- Dochy, F., Segers, M., and Buehl, M., 1999. The relation between assessment practices and outcomes of studies: the case of research on prior knowledge. Review of Educational Research, 69 (2), 145–186.

- El-Haj, M., Alves, P., Rayson, P., Walker, M., and Young, S., 2020. Retrieving, classifying and analysing narrative commentary in unstructured (glossy) annual reports published as PDF files. Accounting and Business Research, 50 (1), 6–34.

- Elliott, W.B., Hobson, J., and Jackson, K., 2011. Disaggregating management earnings forecasts to reduce investors’ susceptibility to earnings fixation. The Accounting Review, 86 (1), 185–208.

- Elliott, W.B., Rennekamp, K.M., and White, B.J., 2015. Does concrete language in disclosures increase willingness to invest? Review of Accounting Studies, 20 (2), 839–865.

- Farrell, A.M., Grenier, J.H., and Leiby, J., 2017. Scoundrels or stars? Theory and evidence on the quality of workers in online labor markets. The Accounting Review, 92 (1), 93–114.

- Fischoff, B., Bostrom, A., and Quadre, M.J., 1993. Risk perception and communication. Annual Review of Public Health, 14 (1), 183–203.