Abstract

This experimental essay constructs a conversation between systems thinking and financial reporting. First, general ideas of system and ecology are introduced and used to inform a review of three overlapping clusters of accounting research. Each of these clusters assumes and emphasises different system characteristics. Second, these characteristics are blended within the model of the financial reporting system as a risk cycle. Third, critical challenges in modelling the financial reporting system are considered, with a focus on the position of a financial reporting regulator. Finally, in a thought experiment, the perspective of a hypothetical non-executive director on the board of a regulator with system-wide responsibilities is adopted. The essay proposes some questions that such a director could expect a model of the financial reporting system would help to answer. Borrowing from ecology, it is argued that any model of the financial reporting system must: be as simple as possible without being too simple; be dynamic and focused on relationships rather than static entities; and embrace risk and uncertainty to avoid ‘illusions of control’.

1. Introduction

Large corporate failures and scandals, like Carillion in the United Kingdom, inevitably generate reflection on wider issues (House of Commons Citation2018). It is not simply that a large public organisation has been badly managed, with poor strategic processes and inadequate risk management. Rather, the spotlight inevitably falls on the regulatory framework and on the different agencies which act as gatekeepers for the quality of company reporting and behaviour. It is often asked why weaknesses at the organisational level are not understood and acted upon by these gatekeepers, such as external auditors. Retrospective diagnoses have pointed to ‘systemic flaws’ (House of Commons Citation2018, p. 6) and problems with the ‘quality of the system as a whole’ (Brydon Review Citation2019, p.71). In short, investigations of individual scandals and events invariably point towards systemic issues, and to the actors who seem to be responsible, not least among which are regulators like the Financial Reporting Council (FRC) in the UK (Kingman Review Citation2018).

At the time of writing this essay, the UK government has launched a major consultation, synthesising and building on prior reviews, on the reform of audit and corporate governance (BEIS Citation2021). Yet, such demands for change to the system of corporate accountability are hardly new. The Royal Mail case in the late 1920s ushered in an entirely new Companies Act in the UK with increased accounting responsibilities for Directors (Bircher Citation1988). The collapse of the Maxwell empire gave birth to the Cadbury Code in 1992 (Spira and Slinn Citation2013). And the failures of Enron and Worldcom in the United States pointed the spotlight at the whole system of financial reporting, and gave rise to the far reaching requirements of the Sarbanes-Oxley legislation (Ge and McVay Citation2005). These and other examples, and the landscape of policy reforms that they engendered, are readily familiar to us and provide a steady and renewable stream of case studies for students. However, the concept of ‘system’, which is embedded in these policy reactions and their discourses, is not further specified in any depth.

How can reforms to a system be proposed and enacted without a clear understanding of that system and its dynamics? Is system-talk any more than a series of loose metaphors used cheaply by policy makers after high profile investigations, part of their rhetoric of reform? Or is there indeed an underlying financial reporting ‘system’ which exists, can be represented, and can inform meaningful reforming interventions? Of course, we know a great deal about the visible actors of the system – auditors, boards, standard setters – who are part of what has come to be called the ‘financial reporting supply chain' and who interact and collaborate in networks (Knechel et al. Citation2020). This is obvious to any practitioner. However, we know much less about how these interactions and relationships add up to, and continuously perform, something we could call a ‘financial reporting eco-system’ (Center for Audit Quality Citation2021). Accordingly, in this experimental essay I endeavour to set up a conversation between ‘systems thinking’ (Senge and Sterman Citation1992, Checkland Citation1999, Holling Citation2001) and financial reporting.

In the next section, I briefly review systems thinking with a view to developing its potential applicability to financial reporting. This is followed by a selective review of different streams of accounting research in order to tease out their latent system assumptions. Drawing on work in political science, these assumptions are integrated to suggest that the financial reporting system can be meaningfully represented as a risk cycle drawing on the framework of ‘risk regulation regimes’ (RRRs) (Hood et al. Citation1999). Three core challenges for system specification as a risk cycle are identified: boundaries, granularity and rationality. The argument then considers the implications for regulation. If regulators like the FRC in the UK and its proposed successor body, the Audit, Reporting and Governance Authority (ARGA), choose to engage in the work of mapping/modelling the financial reporting system, they must contend with further issues: how to think about their own role in a system in which they are not necessarily at the controlling centre; how to represent the multi-levelled complexity of relations and interactions between and within multiple system components; and how to balance the costs and benefits of building such a model of the system. Finally, the argument takes a more explicitly prescriptive stance by using the construct of an imaginary non-executive director with oversight responsibilities for the financial reporting system as whole. We consider what such a ‘system steward’ would need from a model of the financial reporting system and, in particular, some of the key questions and issues that such a model should help to address. That the financial reporting system is a complex ecology comprising multiple and diverse sources of risk regulation is not a particularly surprising or original conclusion of this analysis. The policy question is whether regulatory agencies should engage in structural interventions in this system without investing more in representing its dynamics, not least to understand better its inherent self-organising properties which are often invisible.

2. Systems thinking in brief

A system is understood as a whole with a function and comprises interacting elements in support of that function (Arnold and Wade Citation2015). The more numerous these elements and sub-systems then the more complex the system, and some sub-systems may be critical to the functioning of the whole (Holling Citation2001, p. 391). For systems theorising in biology and ecology, the self-organising or autopoietic properties of complex systems are important, properties which can be significantly disrupted under conditions of man-induced climate change. Eco-systems must be both adaptive to conserve themselves in their environments but also innovative and opportunistic. Holling (Citation2001) argues that both natural and social systems consist of layers of adaptive cycles in what he calls a panarchy. The different sub-system layers are characterised by different speeds for their adaptive cycles. Thus, accounting practice at the organisational level; standard setting at the regulatory level; and conceptions of the purpose of financial statements at the institutional or cultural level can be imagined as linked adaptive cycles with different speeds of change and renewal in the face of experience.

Holling’s model of system complexity shows how adaptive cycles pass through phases of growth and accumulation leading to increased interconnectedness which in turn generates vulnerability and disconnectedness. A loss of tight connectedness in a system creates resilience, but also opportunities for reconstruction and innovation which stimulate growth again. An adaptive cycle like this at one level is protected by the levels above it which move at slower speeds of change. Ecosytems ‘transfer, test and store experience in the form of self-organized patterns that repeat themselves’ (Holling Citation2001, p. 401). We might ordinarily call these self-organised patterns institutions and they are the outcome of ideas being incorporated into slower parts of the different sub-system levels. However, there can also be sub-system pathologies which threaten sustainability. Forms of reconstruction in a cycle can have a perverse resilience which ensures survival but smothers innovation, resulting in a ‘rigidity trap’. External forces can also damage a cycle, producing low connectedness but also low creative potential and resilience, namely a ‘poverty trap’. And both these traps at the sub-system level can be transmitted to other levels of the system, with catastrophic consequences for natural and institutional sustainability. As an example, in the UK it is argued (BEIS Citation2021) that the financial auditing system has not evolved (rigidity trap) to the point where its resilience is also at risk (poverty trap).

The sociologist Niklas Luhmann constructed an entire theory of society in terms of systems (he was not alone in this – see also Parsons Citation1951). According to Luhmann (Citation1995), society is composed of sub-systems one of which is the law. These sub-systems are essentially communicative in nature and process communication according to their own binary code or logic (e.g. legality/illegality in the case of law). Different systems with different codes never interact because these codes are incommensurable, but they can come into relations with, and ‘irritate’, one another and become what he calls ‘structurally coupled’. Borrowing from evolutionary biology, Luhmann suggests that systems react to the irritation of being structurally coupled in terms of their internal organising logic.

Luhmann’s thinking is well known to be challenging and is relatively unused by accounting researchers, in part because its empirical implications are unclear. Yet his vision of a system which is constantly transacting communicatively with its environment (which are other societal sub-systems) and which is processing these transactions in terms of its own code, is an initially appealing one when thinking about financial reporting. Society has developed by creating ever more of these discrete, specialised and relatively autonomous sub-systems. Intuitively, we can think of financial accounting as one such sub-system with its own ‘code’ (Hessling and Pahl Citation2006). For example, the rules of recognition which determine whether an asset or liability can enter primary financial statements is a possible candidate for such a system-constituting code. However, building this idea in a meaningful way is challenging, not least because corporate reporting is much more than the annual production of primary financial statements. It is characterised by formal and informal communications throughout the year and managers may be motivated to selectively disclose information. The production of financial statements is also intertwined with legal institutions, not least in the legal requirements for audit (Freedman and Power Citation1991). And in 2021, so-called ‘voluntary’ disclosures of key non-financial performance indicators are on the rise. Does it make sense and is it useful to follow Luhmann to suggest that all these aspects of real-world financial reporting conform to a communicative code that is the essential logic of the system?

Formal systems theory broadly distinguishes between open and closed systems. There are theoretical debates in different fields about the nature of this openness and closure. For Luhmann, as noted already, all social sub-systems have a principle of closure embedded in terms of their code, but they are also open to all manner of irritation from other systems in their environment, not least from the law (Bromwich and Hopwood Citation1992) and economics (Power Citation2010). The calculation of distributable profits is one area of explicit system intersection (Leuz et al. Citation1998, ICAEW Citation2017).

Biological conceptions of open systems have greatly influenced the social sciences. Indeed, in the wake of the financial crisis of 2009, regulators interested in the conservation of the financial system turned to epidemiological models to improve their understanding of systemic risk (Haldane and May Citation2011) – somewhat ironic given the pandemic which began in 2020. Critics have suggested that this biologism imports a conservative bias – the function of a system is to survive and reproduce – into social science. This was the essence of the debate between Luhmann and his Marxist critics (Bausch Citation1997). However, Holling’s eco-system model of adaptive cycles shows how they can be both conserving and innovating at the same time, allowing also for the rare conditions of revolution under which innovation destroys the existing system.

An important issue for the potential transfer of biological insights about systems to organisational settings is that of perspectivism. In short, social systems like financial reporting may contain many real components but they are also representations which may be constructed for specific purposes by different human audiences. Thus, Luhmann’s systems theory is a specific way of representing society and its dynamics as we saw above. If we think of ‘the railway system’ as a paradigm case, it seems real enough if we begin with the physical network of rails and rolling stock. This is how an engineer would think of the system. But equally a lawyer might view it as a network of contracts for the delivery of services. Thus, system specification may be perspectival; judgements about what is and is not part of a system or infrastructure is relational and depends on the interests of the observer (Star Citation1999, p. 380). These issues become more acute when we think about the financial reporting system. For example, Knechel et al. (Citation2020) argue for a conception of the financial reporting eco-system which highlights how ‘audit quality’ is co-produced by distributed agencies and is not solely a function of the auditor. Social systems specification will highlight the forms of connectedness that the specifier considers to be important.

Rather than engage in debate about the reality of systems given different perspectives, the issue before us is a more pragmatic one, namely whether it is useful to think about financial reporting ‘as if’ it is a discrete system, as others have done at the organisational level for management information systems (Checkland Citation1999). Proponents of such systems thinking argue normatively that it is methodologically valuable to shift the analytical mindset from specific events, such as the financial reporting scandals of recent years which attract so much attention, to the overall structures, system processes and recurrent patterns within a definable whole. To understand a system, and the flows of information and people which constitute it, requires a normative philosophical shift in thinking and a commitment to map dynamic relationships rather than static entities. That all social and economic life takes place in systems is something of a given for enthusiasts of systems thinking – it is only our conventional modes of thought which have prevented us from seeing this. Systems thinking is promoted as a fresh way to address problems and to learn. It is focused on finding and analysing underlying connectedness (Senge and Sterman Citation1992). As Ball (Citation2008, p. 431) puts it in the setting of financial reporting, ‘we tend to take the system we grew up with for granted, so we tend not to scrutinize its very foundations’.

What is clear from this brief exploration of systems theorising and thinking is that they require an intellectual shift from mapping the financial reporting system as a static inventory of entities to the modelling of dynamic relationships and adaptive processes within and between levels with different temporalities or cycle speeds. We need to attend, as Foucault (Citation1980) argues, to the ‘the system of relations that can be established between these elements … . [and the] nature of the connection that can exist between these heterogeneous elements’. We now turn in more detail to academic research in accounting to see how, if at all, systems thinking is evident.

3. The financial reporting system: three perspectives

Despite the increased prevalence of the idea of a financial reporting and auditing eco-system, there are relatively few academic studies which directly focus on systems issues (Ball Citation2001, Bushman and Smith Citation2001, Mennicken Citation2010, Knechel et al. Citation2020), although more which focus on comparative institutional contexts for financial reporting (e.g. Leuz Citation2010). One reason for this may be methodological: empirically it is easier to study parts of a complex system, and to control for, or ignore, other parts, than it is to examine the behaviour of system components as if they were an integrated whole. Furthermore, the very idea of system raises inherently difficult issues of boundary specification, which can be sidestepped to some extent by identifying boundaries with national jurisdiction or simplified by adopting stylised and constrained game-theoretic approaches (cf. Stocken and Verrechia Citation2004). Even organisational-level studies of internal control or risk management systems face this specification problem, often shading into fuzzier notions of ‘control’ or ‘risk’ culture. So while the metaphor of system may be attractive to use in diagnoses of corporate failures calling for change, being more precise poses challenges to scholars and practitioners alike. In what follows, we search for latent systems thinking – what we might call the imaginary of a financial reporting system – in three related bodies of work on financial reporting: capital markets oriented research; political economy; studies of intermediaries as gatekeepers.

3.1. The financial reporting system as an information ecology

The financial reporting system is a complex multi-incentive infrastructure which shapes financial reporting practice and is shaped in turn by its institutional environment. For example,

Financial accounting information is the product of corporate accounting and external reporting systems that measure and publicly disclose audited, quantitative data concerning the financial position and performance of publicly held firms. Financial accounting systems provide direct input to corporate control mechanisms, as well as providing indirect input to corporate control mechanisms by contributing to the information contained in stock prices. (Bushman and Smith Citation2001, emphases added)

An economically efficient public financial reporting and disclosure system requires the following infrastructure: training an audit profession of adequate numbers, professional ability, and independence from managers to certify reliably the quality of financial statements; separating as far as possible the systems of public financial reporting and corporate income taxation, so that tax objectives do not distort financial information; reforming the structure of corporate ownership and governance to achieve an open-market process with a genuine demand for reliable public information; establishing a system for setting and maintaining high-quality, independent accounting standards; and, perhaps most important of all, establishing an effective, independent legal system for detecting and penalizing fraud, manipulation, and failure to comply with standards of accounting and other disclosure, including provision for private litigation by stockholders and lenders who are adversely affected by deficient financial reporting and disclosure. The scope of these requirements is unavoidably wide, because the accounting infrastructure complements the overall economic, legal, and political infrastructure in all countries. (Ball Citation2001, emphases added)

Within what can be broadly called market-based accounting research (MBAR) system ideas are largely implicit (e.g. Lev and Ohlson Citation1982). Here the research approach, primarily grounded in the economics of information and finance theory, seeks to understand the role of accounting in price formation – the ‘value relevance’ agenda – and also in contracting, such as performance evaluation, within capital markets (Holthausen and Watts Citation2001). We can think of such studies as focusing on slices of the financial reporting system and seeking econometrically robust associations between some system elements, or their proxy constructs, while controlling for the influence of others. As with many empirical studies in social science, there are often posited theoretical relationships between variables which are then investigated, drawing upon large data sets. One strand of this work is concerned with the quality of financial reporting, understood in terms of the problem of ‘earnings management’ (Healy and Wahlen Citation1999). In broad terms, accounting enters into MBAR both as an independent variable associated with dependent features of price formation, such as analysts’ forecasts, and as a dependent variable which is influenced by factors such as auditor, regulator and manager incentives.

While most MBAR studies may not be routinely concerned with the totality of the financial reporting system, indirectly they are relevant. For example, the data sets utilised by scholars, such as high frequency trading data or data in regulatory filings, are in effect the traces of information flow within the financial reporting system and support the theorisation of the financial reporting system as consisting of ‘information channels’ (e.g. Bushman and Smith Citation2001, p. 294). Accounting information is assumed to flow, often selectively, to and from different agents (companies, analysts, auditors). Studies provide increasingly refined and rich insights into the mutual influences and associations between features of financial reporting, capital markets and the economic performance of firms and their management.

The foundational paper by Ball and Brown (Citation1968) implies that accounting data is just one source of information among others for market actors engaged in price formation activity. Relatedly, it has been argued that the decision-usefulness of accounting is declining as these other sources of information about firm value increase in significance (Lev and Zarowin Citation1999). In other words, the information ecology of capital markets is much larger than the formal and visible financial reporting system (Miller and O’Leary Citation2000). On one reading, this view challenges the relevance of conventional accounting information to security price formation, and regulators and academics have responded by seeking to improve the ‘value relevance’ of accounting. These efforts range from emphasising the measurement convention of ‘fair value’ to the promotion of entirely new forms of value reporting (Eccles et al. Citation2002). But such a challenge to the informational relevance of financial accounting does not mean that the financial reporting system as whole is dispensable. It is indirectly important to market actors in a myriad of other ways, such as for debt monitoring and other contracting purposes, as a discipline over managerial opportunism (Holthausen and Watts Citation2001, Lambert, Citation2001) and as baseline informational hygiene which contributes to trust and thereby to the liquidity of capital markets (Sunder and Cyert Citation1997, p. 105).

Accounting scholars have also engaged implicitly with systems thinking in the form of comparative studies of national accounting systems, seeking to correlate the quality of reported earnings with institutional features at the national level. In particular, examinations of national variations in the institutional contexts of financial reporting and auditing focus on the role of legal and corporate governance ‘systems’ as independent variables associated with the quality of financial reporting (e.g. Ball et al. Citation2003, Leuz et al. Citation2003, Leuz Citation2010). This work also focuses on variation in institutional arrangements for the enforcement of financial reporting and governance standards, rather than the adoption of accounting frameworks, which are often similar.

These and other studies position national level financial reporting as an embedded sub-system of a larger financial system and its legal institutions (Leuz and Wüstemann Citation2004). Indeed, studies of transitional economies in eastern Europe in the 1990s suggest that state reform, capital market building involving new legal frameworks, and financial reporting transformation were all mutually interdependent projects (Dutia Citation1995). Thus, the financial reporting and auditing system contributes to capacity building in specific phases of economic reconstruction (for the case of China see Macve Citation2020). Yet, while the nation state and its legal system is likely to be the appropriate unit of analysis for thinking about financial reporting enforcement, this may not be the case for other elements of the system which have their own distinct histories. For example, Power (Citation2009a) draws on world system theory to suggest that accounting, by analogy with lex mercatoria, evolved from the self-regulatory practices of merchants before it became a concern for the legal and financial institutions of nation states.

3.2. The political economy of the financial reporting system

A second perspective on the financial reporting system emerges from the political economy of accounting. These studies broadly argue that accounting is non-neutral in its representation of economic performance and systemically prioritises the interests of investors over workers. It is argued that the academic focus on price formation and contracting discussed above ignores the manner in which financial reporting is systemically selective about what it does and does not account for (Hines Citation1988, Tinker Citation1991). Indeed, Marxist critics argue that financial reporting is implicated in: the expropriation of surplus value from labour (Cooper and Sherer Citation1984, Lehman and Tinker Citation1987), environmental degradation (Tinker Citation1985, Gray and Bebbington Citation2001), gender discrimination (Tinker and Neimark Citation1987), and slavery (Annisette Citation2000). Within this broad critique, the large accounting firms are conceptualised as intermediaries with high economic stakes in the capitalist system, and accounting and audit regulators are captured by powerful interests (Humphrey and Loft Citation2009, Humphrey et al. Citation2009). In short, the financial reporting system is a system defined fundamentally by power relations and entrenched economic interests (Perry and Nolke Citation2006, Arnold Citation2012).

From this political economy perspective, Carillion in the UK and other failures are not the aberrations of the financial reporting system that we are led to believe. Rather such failures are features of how it actually operates. In other words, the political economy of financial reporting looks beyond immediate corporate failures to focus on the forms of structurally embedded managerial and financial power (Coffee Citation2006, Botzem Citation2012) which define capitalism. Financial reporting and its regulators are the more or less captured agents of this system, both economically and intellectually. In ecosystem terms, political economy theorists would argue that the system is in a rigidity trap (Holling Citation2001) which both stifles innovation and is also hostage to this managerial power.

Elements of the political economy viewpoint, if not their grounding in critical social theory, are gaining policy traction and even becoming mainstream. Section 172 of the UK Companies Act 2006 which requires company directors to ‘have regard’ for a variety is stakeholders is being activated after many years of being merely law ‘on the books’. This is part of an emerging focus on corporate purpose, on sustainability and on non-economic values which the 2020 pandemic has accelerated. Environment, Social and Governance (ESG) performance metrics have become key topics for corporate boardrooms, and the reality of climate change is no longer seriously debated. There now seem to be convergent efforts to pluralise the interests which inform financial reporting. For example, the FRC Laboratory in the UK proposed a new model of financial reporting (FRC Citation2020) which suggests that the financial reporting system must become more explicitly responsive to a wider menu of interests. And yet, the necessity of this systemic connectivity of accounting and auditing to society was already expressed fifty years ago (e.g. Flint Citation1971). The political economy perspective is a persistent reminder of the accumulated power of economic interests which wish to conserve the financial reporting system more or less as it is.

3.3. The financial reporting system as a network of gatekeepers

The third perspective or lens on the financial reporting system overlaps to a large extent with both political economy and information approaches but adopts an explicit agency-theoretic emphasis. It focuses primarily on the interests and incentives of the actors whose actions ‘perform’ the system as it actually works, namely, directors, auditors, analysts, accounting regulators and many others. Whereas pure political economy approaches emphasise the structurally embedded nature of interests in regulatory systems – making regulation a site where social conflicts and power are played out – ‘positive accounting theory’ (Watts and Zimmerman Citation1979) and its variants focus on the role of interests and incentives at the level of specific classes of agent. The underlying model is that of the economics of agency and the risks of adverse selection which foreground actors’ incentives to preserve their tenure and the economic benefits which accrue to that. This agency-theoretic literature is extensive and underpins a great deal of academic work on private information, discretion and voluntary disclosure (Stocken and Verrechia Citation2004) and the contracting function of financial reporting (Lambert Citation2001).

Building on the agency-theoretic emphasis, the financial reporting system can be conceptualised as a network of inter-related ‘gatekeepers’ (Kraakman Citation1986). Such gatekeepers are intermediaries whose institutionally defined purpose is to provide assurance about the quality of financial reporting and hence the trustworthiness of management as the primary agent. The theory is that their pledge of reputational capital in discharging their function e.g. auditing, alleviates the basic principal-agent problem of shareholder capitalism. Their incentive alignment with the larger goals of the financial reporting system is critical to this gatekeeping process. Coffee (Citation2001, Citation2006) argues that the financial reporting scandals and corporate failures of the late 1980s and 1990s up to Enron reflected the systemic failure of this alignment. Auditors, analysts and credit rating agencies were under-incentivised to exercise their capacity to veto or criticise management representations of earnings. In addition, although nominally independent, they tended to acquiesce to client pressure because the economic, legal and reputational costs of doing so were low. In the USA the Sarbanes-Oxley legislation of 2002 (SOX) was largely a reaction to gatekeeper failure and requires explicit reporting and certification of internal controls over financial reporting by the senior officers of a company. Many of the concerns of the early 2000s remain evident in the UK Kingman and Brydon reports, which also focus on the quality of gatekeepers, including regulatory bodies, and their enforcement capabilities and incentives. Indeed, two decades after the USA, the UK is debating SOX style internal control reporting (BEIS Citation2021).

Financial reporting gatekeeping agents can also be imagined as ‘lines of defence’ (Davies and Zhivitskaya Citation2018). Originating in safety policy and practice, the lines of defence idea suggests the interdependency of gatekeepers in which the failure of one to detect and act upon poor quality financial reporting is compensated in theory by the vigilance of the other. Importantly, the model places the first line of defence in the business itself – its control processes and culture, thereby expanding the population of actors who can be regarded as a gatekeeper. In the setting of financial reporting this first line of defence exists in financial reporting departments in organisations populated by professionals whose ethics are regulated by professional institutes and overseen by finance directors. This less visible gatekeeping function at the organisational practice level is as much a part of the financial reporting system as the board and external auditors, who largely rely on it.

The gatekeeping perspective is also consistent with the notion that the financial reporting system is a multi-agent ‘financial reporting supply chain’ (production, communication, consumption) consisting of gatekeepers and other agents with incentives at different points along the chain to monitor and assure the quality of the process (Knechel et al. Citation2020). The metaphor of the supply chain directs our attention to the nature and strength of the integration between the actors at each point in that chain. It follows that the financial reporting system is nothing more than this architecture of agents who perform the system in their daily work. If we want to study that system and represent it as a system, we would need to study these actors, to follow them and to trace what they do (Latour Citation2005).

To summarise, this section has explored three overlapping perspectives on the financial reporting system which appear to be implicit in three research clusters. The literature review has been non-systematic and selective. In particular, we have not discussed studies which are antithetical to the whole idea of system and its functionality (as articulated by Parsons and Luhmann). For example, ‘Garbage can’ (Cohen et al. Citation1972) and more ‘emergentist’ (Elder-Vass Citation2007) theories suggest that the very idea of a financial reporting system implies more coherence and rationality than really exists. However, subject to the limitations of the literature analysis, summarises the argument of this section and contrasts the three systems thinking perspectives on financial reporting in terms of the implied ‘purpose’ of the system and the nature of the interconnectivity of its elements. draws attention to the fact that the question ‘what is the financial reporting system?’ may have more than one answer depending on the optic of the observer.

Table 1. Research perspectives on the financial reporting system.

Each of the three research clusters implies a different focus on the core purpose of the system, namely information for price formation and contracting, conservation of power, and production of trust by a network of agents. Yet these three perspectives are clearly intertwined and we can make this more explicit by drawing on political science and the notion of a risk regulation regime.

4. The financial reporting system as a risk cycle

Hood et al. (Citation2001) utilise cybernetic ideas to construct a framework for the comparative analysis of what they call risk regulatory ‘regimes’ (RRRs). RRRs are conceptualised in terms of three levels or sub-systems: Directing or standard setting, Detecting or monitoring; and Deterring or enforcing. It is a simple but compelling representation of a regulatory system. Regulatory standards of performance are set which express the purpose of the system; organisational and individual compliance with these standards is monitored; deviance and non-compliance are sanctioned. The system is also characterised by continuous feedback between the sub-system levels leading to potential reform and learning at each level. This ideal-typical schema is used to map different regimes for regulating risks and their sub-system components. The mapping process reveals different institutional configurations and the analytical task is to explain these differences (Hood et al. Citation1999). For example, the analysis helps to explain why, for example, we regulate background radiation from radon in an institutionally different way from dangerous dogs.

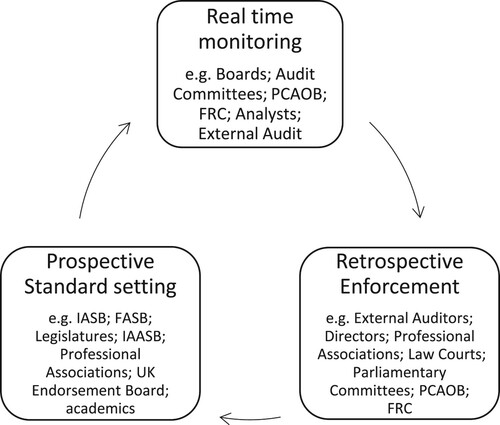

This RRR framework can be represented dynamically as a ‘risk cycle’ (Hardy et al. Citation2020) of connected sub-systems with different temporal orientations. Thus, standard setting agencies manage the risks to financial reporting prospectively. Monitoring agencies manage the risks to the financial reporting as it is practiced in real time. Enforcement agencies manage the risks to financial reporting system retrospectively, sometimes producing major reports and inquiries like Brydon and Kingman in the UK which, in theory, lead to system learning. These three different temporal orientations are intertwined as an ecology of connected sub-systems and agencies with different speeds of adaptation and change.

Each sub-system in this risk cycle is populated by different institutional agencies (gatekeepers) with their own interests. The cycle is dependent on the flow of information both within and between the three sub-systems. And the multi-actor cycle as a whole is a network of power relationships. visualises this cyclical conceptualisation of the financial reporting system and thereby integrates the three research lenses developed in the previous section.

Figure 1. The financial reporting system as a risk cycle.

For illustrative purposes, each sub-system of the financial reporting system in is populated by a number of agencies, some of which straddle sub-systems. A regulator like FRC appears in each sub-system, reflecting its role as a ‘system’ actor with overall responsibilities for system functioning. External auditors are likely to figure in, and span, both monitoring and enforcement sub-systems and can be evaluated in terms of their contribution to each sub-function. In short, key actors in a system do not always operate only in one functional sub-system.

Many of the agencies listed in are unsurprising and well-known (Bushman and Smith Citation2001, Ball Citation2008, ICAEW Citation2019). Yet even this simple and incomplete cyclical representation of the system raises critical issues. For example, the sources of standards for practice are varied and internally multi-levelled. Here agencies of direction are not only the usual institutional actors, such as IASB and FASB, but include the law, professional and industry associations and the technical departments of accounting firms, all operating at different system speeds (Holling Citation2001) and with varying degrees of connectedness to each other. Even significant individuals, such as authors of Kommentare in Germany, who may also be academic accountants, operate in a market for interpretations and can also be included within the financial reporting system (Barth Citation2000, Power Citation2004). Formal accounting standards may be produced by standard setters, but we know that standardised forms of accounting also emerge de facto from voluntary disclosure practices at the level of industrial fields and individual organisations. Thus, specifying the agencies which produce rules and direct the financial reporting system may require looking beyond formal standard setting bodies.

Describing the monitoring and enforcement sub-systems within the cycle raises similar challenges. In reality, each sub-system comprises loosely-coupled agencies. Some may be national and others may be transnational in the scope of their work. While external auditors attract regulatory and analytical attention because of their role in assuring the quality of financial reporting, slower to change climates of compliance, generated in part by professional associations’ ethical codes, underpin operational internal control as the ‘first’ line of defence. For this reason, a more complete version of for financial reporting must include the internal as well as the external auditor.

All the various components of the financial reporting system have emerged and developed in different ways over time. The system is therefore less coherent and integrated than suggests. However, the cyclical model of the system is useful in generating issues for further investigation. For example, as the Kingman Review (Citation2018) noted, standard setting at the IASB level is institutionally disconnected from national modes of monitoring and enforcement. Arguably this disconnection was a deliberate choice to create a standard setting body which was independent of ‘politics’ i.e. one with weak relational links to the monitoring and enforcement parts of the system, which we know to be jurisdiction-specific (Leuz Citation2010). More generally, the risk cycle model provokes critical systems thinking about the strength of relations within, and between, different sub-system levels.

also provides a risk optic on the question of the purpose of the financial reporting system, which in theory drives the design of standards. But which risk is being managed by the financial reporting system – risks to decision usefulness and/or to stewardship (Gjesdal Citation1981)? And for whom? Shareholders, debtholders, or prospective investors? These are not new questions about the purpose of financial reporting, but systems thinking shines a new light on them. Paradoxically, while multiple purposes at different sub-system levels initially suggest weakness and incoherence, from an ecology point of view this may be a source of system resilience in complex environments, allowing the system to be selectively responsive to different pressures. Systems thinking and mapping of the system as a risk cycle could also facilitate researcher and regulator attention to the actual functions which may be at risk.

From the MBAR point of view, the deep purpose of the system is to generate financial reporting information enabling investors to be well informed about management performance by holding managers to contractual account as well as by supporting the complex process of fair price formation. Earnings management, shading into fraud, is one of the risks to these purposes which must be mitigated. From a political economy point of view, the risk is that financial reporting preserves existing structures of power and fails to represent interests other than those of shareholders. And from the gatekeeper point of view, the risk is primarily a principal-agent problem of aligning the gatekeeper’s interests with their institutionally defined sub-system function leading to failure to produce the required trust via the exercise of their enforcement rights.

In summary, this section provides a preliminary conceptualisation of the financial reporting system in terms of an architecture of interconnected sub-systems in a risk cycle. In effect, this is a risk-based and cyclical version of the financial reporting supply chain. Each sub-system has its own primary temporal mode for managing the risks to the purposes of financial reporting, but prospective, real-time and retrospective modes necessarily overlap. This map of the financial reporting system invites a focus on its dynamic characteristics and on the interactions and dependencies linking the many agencies in play. Yet also generates challenges of specification. I select three for discussion below, namely: boundaries, granularity, and rationality.

4.1. System boundaries

How should we delineate the boundaries of the financial reporting system? Which organisations and agencies are included within it and which are part of the external environment or ecology of the system? For example, are the technical departments of the large professional service firms part of the system or not? Are analysts, internal auditors and even hedge funds to be included? Do they fulfil material directing, detecting or enforcement roles? The role of law in financial reporting provides a specific illustration of the challenge. Some parts of law are deeply embedded in financial reporting, such as the regulation of distributable profits, insolvency and audit (Freedman and Power Citation1991). Yet other aspects of law and regulation play a more indirect role in constituting the cultural climate for governance and the enforcement of rules. For example, the new ‘Senior Manager’ regulations in UK financial services overlap with the longstanding responsibilities of professional institutes for the conduct of their members. This wider legal and governance infrastructure, indeed cultural respect for the rule of law itself, is important to financial reporting (Ball Citation2001), but should it be represented as part of the financial reporting system or not? In addition, there is the challenge of the transnational character of parts of the system. While monitoring and enforcement are likely to be at the level of national jurisdictions, standard setters like IASB are transnational.

Fuzziness in system boundaries and jurisdictions is hardly surprising given that the institutional architecture within which financial reporting operates has not been consciously designed but is heterogeneous and emergent. At best we can say that the financial reporting system is a sub-system of the equally fuzzy system of corporate governance. Yet fuzzy boundaries may also support the openness of the system to diverse influences, not least pressure for change in financial reporting to encompass the emerging ESG and sustainability agendas (FRC Citation2020). In theory, healthy systems are continually responsive and adaptive to changes in wider society (Holling Citation2001). The financial reporting system and its subsystems are connected to each other but are also linked to other systems – law, financial regulation, economy, politics, academia – which constitute ‘linked ecologies’ (Abbott Citation1988, Citation2005, Mennicken Citation2010). The theory of linked ecologies suggests that areas of fuzziness are likely to be points of important linkage between financial reporting as a relatively discrete sub-system and other systems which are its immediate significant neighbours.

Abbott (Citation2005) argues that if there are too many of these links, such that there seems to be no boundary at all between two systems, then it is questionable whether there are they really two systems which interact as opposed to one with some internal complexity. This issue is relevant to how we think of financial reporting in relation to corporate governance and draw the boundary between them. reminds us that specifying boundaries is likely also to depend on the perspective and interests of the system-modeller. Whatever system boundary is chosen is necessarily a construct and is likely to reflect institutional definitions of the scope of regulatory responsibility. Social systems like financial reporting are therefore observer constructs and political representations. We return to this point later in this essay when we adopt the formal regulators’ point of view.

4.2. System granularity

Even if there can be agreement about the agencies and boundaries of the financial reporting system, reveals a further decision to be made, namely the level of granularity in specifying subsystems as units of analysis. Holling (Citation2001, p. 391) argues that a representation of an ecology should have a ‘requisite level of simplicity’ – excessive complexity obfuscates the benefits of systems thinking and loses sight of the structural dynamics. Thus, a systems approach to financial reporting must specify the smallest useful unit of sub-system analysis. Should this unit be clusters of organisations with common functions (e.g. auditors), individual organisations, or even specific human beings who play system roles (e.g. specific members of IASB)? There is clearly a trade-off between the realism of ‘zooming in’ on system elements and the excessive complexity this creates in which underlying structures and material interconnections are hard to see distinctly. For example, as we zoom in on the enforcement function, the granularity of units of interest could in principle increase from the audit profession, to the Big 4, to Firm A’s audit practice, to Firm A’s FTSE 100 Financial Services lead audit partner. As we do this, what emerges is less describable as a ‘system’ of financial reporting and more of a complex network or assemblage. This may be its ultimate reality but the price of this realism is a lost sense of the whole and its structures. The choice of sub-system granularity for mapping an RRR is therefore an important one and suggests that systems thinking about financial reporting requires methodological care.

4.3. System rationality

The third initial challenge for specifying the financial reporting system concerns its rationality. Systems thinking in many areas has been motivated by dreams of machine-like control (Mirowski Citation2002). The cyclical version of Risk Regulation Regime (RRR) model in preserves the functional rationality of this system dream i.e. given a system function to manage a specific risk, it focuses on how it generates standards, monitors their implementation, imposes sanctions for non-compliance and learns how to self-regulate more effectively in the face of shocks and events. However, the more rationalistic and machine-like the specification of the system, the less realistic and descriptive it is likely to be, leading to misplaced practical expectations as well as theoretical overstatement. And the more granular and liberal the specification of sub-systems, the less that their functional rationality can be presumed and the more that ‘garbage can’ metaphors of self-organisation are descriptive. From a political economy approach, the functional rationality of the system as whole is hostage to the rationality of highly distributed agencies looking to maintain their power and economic rents as intermediaries. Indeed, more granularity may increase the relevance of political economy and agency-theoretic approaches to financial reporting and their focus on power and incentives respectively. Furthermore, the focus on rationality reveals how the very notion of ‘system’ presumes a coherence and unity of purpose which is aspirational but which may not be possible.

In summary, efforts to think of financial reporting as a risk-based system, drawing upon systems and ecology theory, must confront: issues of boundary specification and linkages to other systems; the granularity of sub-system specification; and assumptions about the rationality and controllability of any system. But who is likely to have an interest in addressing these issues and modelling the financial reporting system in the first place? This is the pragmatic issue which concerns the remainder of this essay.

5. Implications for regulators: representing and intervening

So far our engagement with systems theory and system thinking has been at a level of abstraction. In the remainder of this essay we address the practical implications of these reflections for the work of a regulatory agency like FRC in the UK and its proposed successor ARGA (BEIS Citation2021). As noted at the outset of this essay, recent policy reactions to corporate scandals in the UK have appealed to ideas of system and eco-system. The logic of such retrospective diagnoses is implicitly inductive, moving from the specific case to its general implications, from the event to the necessary reform at the level of system. But how can a formal body which is given system responsibilities by the legislature know whether its reactions to events are proportionate, and whether proposed reforms and interventions will be effective, if it does not understand the interconnections and dependencies which characterise the system and its sub-systems in the first place?

This is a live question for any organisation with formal regulatory responsibilities. The daunting intellectual task of understanding the system may explain why there is a tendency for reforms to be incremental rather than fundamental. Yet, a serious interest in the financial reporting system requires that regulators embrace systems thinking more substantially, see themselves as part of a RRR, and engage in mapping/modelling it with a view to enhancing their interventions. Indeed, to borrow from the philosopher Ian Hacking (Citation1983) we might assert that the task of a regulator of financial reporting is to ‘represent and intervene’, to represent the domain to be regulated and to intervene in it on the basis of that representation according to its objectives. If this can be done for the macro-economy, then why not for the financial reporting system?

Financial reporting regulators have always operated with one or more implicit models of the financial reporting system. But if and when they make this model explicit, a number of further challenging issues arise in addition to those already noted above. Three key issues for the practical mapping of the financial reporting system are considered below: positioning the regulator itself ‘within’ the system; dealing with system complexity and indeterminacy; and estimating the costs and benefits of any mapping/modelling exercise.

5.1. Regulators in the system

One of the first tasks in mapping/modelling the financial reporting system is for a regulator to reflect on its own ‘position’ and capability within the system. Politicians may imagine a regulatory organisation to be in a central ‘steering’ role somehow outside of the system – the risk regulation regime – observing it and controlling its operations. Indeed, our regulatory language of ‘oversight’ implies this kind of model of hierarchical/external control of the system. Yet, societal expectations of regulatory organisations are known to overestimate their capacity for control. ARGA is proposed to replace FRC yet it will most likely inherit even greater expectations of control and steering of the financial reporting system. Regulators usually understand that they have few hard levers of control and that there are likely to be different perspectives on how a system should operate. They face reputational risk and worse arising from this gap between perceived and real capacity.

Regulatory theories challenge the hierarchical oversight model, developing instead ‘decentred’ and ‘distributed’ models of regulation (Baldwin et al. Citation2012). These models share a common rejection of command and control regulatory styles and recognise the multi-perspectival, multi-level, and distributed nature of regulatory activity. These theories are also more consistent with eco-system models which focus on the self-organising and adaptive properties of systems. In effect, there is a lot of distributed ‘regulatory’ activity (‘Lines of defence’) in the financial reporting system and the regulatory organisation, knowing this, can seek to influence it as well as explicitly direct.

In summary, in mapping the financial reporting system as whole, suggests that formal regulators will be just one source of regulatory activity among others. Yet, if the regulation of financial reporting risk is widely dispersed across diverse agencies and actors then, borrowing from ecology thinking, this diversity and low interconnectedness may in fact contribute to system resilience. A formal financial reporting regulator with system responsibilities can, if society via the legislature will allow it, operationalise its purpose in terms of monitoring these system dynamics and promoting and nurturing this distributed regulatory diversity. Indeed, notwithstanding the invention of new regulatory powers and ‘big sticks’ with which to retrospectively discipline company directors and auditors (BEIS Citation2021), a financial reporting regulator has no choice but to cooperate prospectively with professional bodies to nurture resilient first lines of defence at the level of professional conduct and ethics.

5.2. System complexity

A second related challenge for a regulator is system complexity. As noted above, the more realistic and granular the specification of the system and its sub-systems, the more numerous are the connections within and between these sub-systems. The specification of the financial reporting system must be as simple as possible but also have enough complexity to capture the material interacting features of the system. It must be capable of representing the demand for, and supply of, financial reporting which defines the supply chain or infrastructure (Ball Citation2001) and the risks at each material point of this chain. It may be that an initially detailed and complex map is important to disrupt conventional thinking by highlighting mutually dependent components which contribute to the regulation of financial reporting risk, and which cannot be changed independently of one another. From this starting point, model complexity can be refined to map key sub-systems (Holling Citation2001, p. 391). In this way, critical points of failure and weakness in the supply chain may come into view and acquire focus. Regulators would have to decide how to combine a focus on entities and individuals as ‘natural’ units of enforcement with a focus on sub-systems and their interconnectedness. Research provides numerous tools for doing the latter, such as social network analysis which is more aligned with emergentist, rather than functionalist, conceptions of system (Scott Citation1988). Network defined ‘distance’ between agencies; flows of information and/or people; measures of centrality (power) and marginality in a network could all be applied to the financial reporting system with potentially interesting results. For example, network visualisation techniques could ‘test’ intuitions about the significance of a specific regulator or of auditors in the system. It could also reveal how the financial reporting system and the financial system are ‘linked ecologies’ (Mennicken Citation2010) and the nature and location of critical inter-system connections.

5.3. Cost–benefit of system mapping

While modelling and mapping the financial reporting system is interesting for its own sake, regulatory organisations must also consider how much time, intellectual effort and money to invest in mapping and modelling the system of financial reporting. What might the costs and benefits of such an exercise be? Here their work could be usefully informed by efforts to model systemic risk in the wake of the 2009 financial crisis, when interconnectedness in the interbank market was poorly understood and risks to the financial system had incubated invisibly. Is it possible to build an analytical model for financial reporting, as others have done for systemic risk in the banking system (e.g. Hautsch et al. Citation2015)? Holling (Citation2001, p. 391) argues that such an integrated model of an ecology will only be useful if it is: as ‘simple as possible but no simpler’ (a phrase attributed to Einstein); is ‘dynamic and prescriptive not static and descriptive’; and, crucially, embraces ‘uncertainty and unpredictability’. At the time of writing, we may have the first of these qualities in our understanding of the financial reporting system, but not the second and third.

A key cost–benefit issue is the prescriptivity and actionability of any system model. Would it improve the existing capacity to regulate? Would it enhance early warning capabilities of system monitoring in real time? Would it prospectively nurture valuable system changes? In short, could system mapping be additive to existing regulatory interventions in the same way that models of the economy have influenced the formation of macroeconomics and related interventions? Using models to represent and intervene in fields is fraught with challenges because they are necessarily simplifications of complexity – they are ‘mini worlds’ (Morgan Citation2012). However, any model of the financial reporting system would be a means to a defined end or purpose; it may not require a perfect model to target key sub-system functions.

6. Discussion

As noted in the introduction, this paper is an experiment. It is an attempt to initiate a conversation between systems thinking and financial reporting. Some readers will see all this as wasted effort since they know very well what the constitutive elements of the financial reporting system are – legislatures, standard setters, board directors, financial regulators, professions, auditors (See ICAEW Citation2019). And in some ways they would be right. A model of the financial reporting system without these agencies would lack credibility. Yet, as we try to specify and represent this system in greater detail, paying attention to subsystems with different speeds of change and function, to boundary issues and to interconnectedness both internally and across ecologies, it is much less straightforward.

Despite these challenges, systems thinking is usefully critical and forensic in intent. Its purpose is to question accepted ways of looking at things. Thus, a valuable map or model of the financial reporting system could reveal areas which have been neglected or which have received disproportionate attention. Systems thinking also goes beyond a conventional and static focus on independent organisational entities and begins from the presumption of their mutual dependence within layered sub-systems. Arguably, the formal organisational independence of external auditors has preoccupied regulators at the expense of a systems-based understanding of their operational dependencies (Power Citation2009b). In addition, the linked ecologies approach could reveal how users of different kinds are, or are not, attached to the financial reporting system, and the dynamics of this attachment. In effect, bringing to life the ‘stakeholder capitalism’ features of s.172 of the UK Companies Act is a project of enhancing linkages between reporting and stakeholders, including but not restricted to investors. These links are sources of innovation and change in the financial reporting system.

Both political economy approaches and the economics of agency remind us that systems and sub-systems are populated by intermediaries with varying abilities to protect their own interests at the expense of the purpose of the system. In this sense, the financial reporting system is pervaded by power and politics (e.g. Arnold Citation2012, Botzem Citation2012, Correia Citation2014). This politics means that the financial reporting system will never conform to the cybernetic functionalist ideal of an RRR risk cycle with clear standards of performance which are monitored and enforced, leading to regular feedback and system adjustment. However, the RRR template is a useful way to think about system architecture. The fit is not perfect but it surfaces questions which may not otherwise get asked from an organisational entity perspective. Regulators must find a way to include power relations in any model, not least the power of large corporations.

To conclude, the test of the benefit in modelling the financial reporting system is whether it enhances the oversight and action capacities of the regulatory function, which is part of the self-organising ecology of the system, both to promote improvement and manage risk. So let us now engage in a thought experiment and imagine the role of a non-executive director of the future regulator ARGA, which is responsible for the financial reporting system. She sits on the newly formed risk committee of ARGA with oversight responsibilities for that system and is intent on realising the benefits of modelling the system. Such a director will value any map or model less for its purity or realism and more for the issues it makes visible, the questions it enables to be asked, and the actionability it generates. In terms of the risk cycle architecture depicted in , the imaginary NED will wish to answer at least some of the following questions.

6.1. Standard setting sub-system (prospective mode)

Where in this sub-system are the different purposes of the system represented and how is this communicated to other parts of the system and agreed upon? (The Brydon Review in the UK suggests that the concept of the ‘true and fair view’ is no longer a helpful characterisation of the purpose of financial statements, requiring a change in the law).

What are the key interfaces, gateways or linkages which enable the financial reporting system to be responsive to changes in society and business, and to the overall societal goal of supporting successful, sustainable organisations and safe and fulfilling workplaces? Can we play a role in strengthening those linkages to inform the prospective view of the system?

What is the quality of our oversight of the production of accounting standards? In the UK, much will depend on how the Endorsement Board, formed in 2021, will operate.

Understood as a risk regulation regime, what are the key risks in the system? Is it possible to articulate a tolerance for entity failure at the level of the financial reporting system as a whole which informs the work of sub-systems? Do we understand clearly why the failure of Carillion was not considered to be within that risk tolerance?

Are we confident about our understanding of all the gatekeeping functions in the system, their responsibilities for managing financial reporting risk, their co-dependencies and their enforcement capacity? What can be learned from the way Germany is dismantling its financial reporting enforcement system?.Footnote1

How well do we understand our own role within the system and our dependencies? Do we have the capacity to observe the system and its dynamics, including the effects of our own interventions?

How can we avoid ‘illusions of control’ (Langer Citation1975) and accept we are not fully in control of a self-regulating eco-system, despite public expectation? Where are the optimal points of possible nudge and intervention and do we have the right tools for this?

6.2. Monitoring sub-system (real time mode)

Are we investing enough in our capacity to monitor compliance? Where in the system do we need ‘safe harbours’ to unblock and incentivise crucial information flow?

Where in the financial reporting system do we find early warning tools for fraud, earnings management and bankruptcy? Are they in the optimal institutional locations and how do we design information channels for early warnings which avoid the risk of self-fulfilling prophecy?

Do we have an adequate line of sight into the foundational sources of risk regulation which exist in ‘first line of defence’ activities? How can we improve our understanding of the role of professions and the values of professionalism in underpinning the system?

Do we understand the role of internal auditing and internal control as sources of continuous self-regulation of the system? Does the model help to understand the role of both internal and external auditors in the production of trust?

How often should we ‘run’ the model of the financial reporting system in order to understand how components and relationalities are changing over time? Does the model reveal where there are different speeds and potential pressures for change in the system? Does our model enable a better understanding of critical points of heightened risk or weakness in the financial reporting system in order to direct monitoring?

6.3. Enforcement sub-system (retrospective)

Are sanctions against individuals and firms within the system sufficiently graduated and robust to be credible levers of behaviour modification? Where in the system are the key interfaces with legal remedies and are they effective?

How are the sub-systems of the financial reporting system evolving? Is the system becoming more complex and fragmented? How are power relations shifting?

Is this a ‘productionist’ system which is primarily driven by accountants and preparers? Is it a closed, homogenous ‘system of thought’ focused on standard setting and auditing institutions?

How, in the face of disruptive events like the collapse of Carillion, can we use the model to discriminate between system failure and failure within a sub-system? How can we avoid overreacting to single instances of even large corporate failure by calling the entire financial reporting system into doubt?

How can the financial reporting system learn and innovate? How can ARGA encourage and nurture biodiversity of sources of self-organisation across all sub-systems?

This list of questions that a NED of ARGA may wish to address is indicative rather than comprehensive. However, the questions suggest how a model of the financial reporting system for a regulator can sharpen the focus on key relations, activities and gaps, which existing static representations of entities cannot provide. The goal of modelling is to represent the complex ecology of financial reporting sufficiently clearly to enable meaningful enquiry, reflection and intervention. Importantly, a model also provides regulators with the intellectual resources to resist political pressure to rush into reform and spend public money on creating new institutions and new rules, when what may be needed is to make the existing system work more effectively.

7. Conclusion

‘The financial reporting system – what is it?’ In this essay I have argued that to begin to answer this question seriously it is necessary to explore what is meant by ‘system’ and then determine its possible application to the field of financial reporting. Accordingly, rather than providing a clear cut answer to the question, we have focused more on how financial reporting might be usefully represented as a system and on the methodological challenges of doing this. First, we looked at system theories including ecology. Then we searched for systems ideas in three overlapping clusters of accounting research, concluding that they emphasise different systems characteristics. We sought to blend these characteristics within the model of a ‘risk regulation regime’ which could be applied to financial reporting. At this point critical challenges in modelling the financial reporting system were considered, especially for financial reporting regulators. A model which represents a system must have a point, and must be actionable. Finally, in a thought experiment, we adopted the standpoint of a hypothetical non-executive director with system-wide responsibilities and considered the questions that they would hope to address using a model of the financial reporting system. Systems thinking and modelling are likely to be a non-trivial investments for a regulator of financial reporting, but could be important in enabling such a body to explicitly embrace uncertainty and avoid illusions of control.

Acknowledgements

An earlier version of this paper was presented at the ‘Information for Better Markets Conference’, 14th of December, 2020, organised by the Institute of Chartered Accountants in England and Wales (ICAEW). The author is grateful for the helpful comments of Stefano Cascino, Robert Hodgkinson, Richard Macve, Andrea Mennicken, Laura Spira and an anonymous reviewer.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Notes

1 ‘Germany to overhaul accounting regulation after Wirecard collapse.’ Financial Times 28th of June 2020.

References

- Abbott, A., 1988. The System of Professions: An Essay on the Division of Expert Labor. Chicago: University of Chicago Press.

- Abbott, A., 2005. Linked ecologies: States and universities as environments for professions. Sociological Theory, 23 (3), 245–274.

- Annisette, M., 2000. Imperialism and the professions: the education and certification of accountants in Trinidad and Tobago. Accounting, Organizations and Society, 25 (7), 631–659.

- Arnold, P.J., 2012. The political economy of financial harmonization: the East Asian financial crisis and the rise of international accounting standards. Accounting, Organizations and Society, 37 (6), 361–381.

- Arnold, R.D., and Wade, J.P., 2015. A definition of systems thinking: a systems approach. Procedia Computer Science, 44, 669–678.

- Baldwin, R., Cave, M., and Lodge, M., 2012. Understanding Regulation: Theory, Strategy, and Practice. Oxford: Oxford University Press.

- Ball, R., 2001. Infrastructure Requirements for an Economically Efficient System of Public Financial Reporting and Disclosure. Vol. 1. Washington, DC: Brookings-Wharton Papers on Financial Services, 127–169.

- Ball, R., 2008. What is the actual economic role of financial reporting? Accounting Horizons, 22 (4), 427–432.

- Ball, R., and Brown, P., 1968. An empirical evaluation of accounting income numbers. Journal of Accounting Research, 6 (2), 159–178.

- Ball, R., Robin, A., and Wu, J.S., 2003. Incentives versus standards: properties of accounting income in four East Asian countries. Journal of Accounting and Economics, 36 (1-3), 235–270.

- Barth, M.E., 2000. Valuation-based accounting research: implications for financial reporting and opportunities for future research. Accounting & Finance, 40 (1), 7–32.

- Bausch, K.C., 1997. The Habermas/Luhmann debate and subsequent Habermasian perspectives on systems theory. Systems Research and Behavioral Science, 14 (5), 315–330.

- BEIS, 2021. Restoring Trust in Audit and Corporate Governance. Consultation on the Government’s Proposals. London: Department for Business, Energy and Industrial Strategy.

- Beyer, A., Cohen, D.A., Lys, T.Z., and Walther, B.R., 2010. The financial reporting environment: review of the recent literature. Journal of Accounting and Economics, 50 (2-3), 296–343.

- Bircher, P., 1988. The adoption of consolidated accounting in Great Britain. Accounting and Business Research, 19 (73), 3–13.

- Botzem, S., 2012. The Politics of Accounting Regulation: Organizing Transnational Standard Setting in Financial Reporting. Cheltenham, UK: Edward Elgar Publishing.

- Bromwich, M., and Hopwood, A.G. eds., 1992. Accounting and the Law. London: Prentice Hall.

- Brydon Review, 2019. Report of the Independent Review into the Quality and Effectiveness of Audit. Available from: https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/852960/brydon-review-final-report.pdf.

- Bushman, R.M., and Smith, A.J., 2001. Financial accounting information and corporate governance. Journal of Accounting and Economics, 32 (1-3), 237–333.

- Center for Audit Quality, 2021. A changing financial reporting ecosystem, Sunday, March 8, 2020. Available from: https://www.thecaq.org/cii/ [Accessed 15 March 21].

- Checkland, P., 1999. Systems thinking. In: W. Currie and B. Galliers, eds. Rethinking Management Information Systems: An Interdisciplinary Perspective. Oxford: Oxford University Press, 45–56.

- Coffee, J.C., 2001. Understanding Enron: it's about the gatekeepers, stupid. The Business Lawyer, 57, 1403–1420.

- Coffee, J.C., 2006. Gatekeepers: The Professions and Corporate Governance. Oxford: Oxford University Press.

- Cohen, M.D., March, J.G., and Olsen, J.P., 1972. A garbage can model of organisational choice. Administrative Science Quarterly, 17 (1), 1–25.

- Cooper, D.J., and Sherer, M.J., 1984. The value of corporate accounting reports: arguments for a political economy of accounting. Accounting, Organizations and Society, 9 (3-4), 207–232.

- Correia, M.M., 2014. Political connections and SEC enforcement. Journal of Accounting and Economics, 57 (2-3), 241–262.

- Davies, H., and Zhivitskaya, M., 2018. Three lines of defence: a robust organising framework, or just lines in the sand? Global Policy, 9, 34–42.

- Dutia, T., 1995. The restructuring of the system of accounting in Romania during the period of transition to the market economy. European Accounting Review, 4 (4), 739–748.

- Eccles, R.G., Herz, R.H., Keegan, E.M., and Phillips, D.M., 2002. The Valuereporting Revolution: Moving Beyond the Earnings Game. New York: John Wiley & Sons.

- Elder-Vass, D., 2007. Luhmann and emergentism: competing paradigms for social systems theory? Philosophy of the Social Sciences, 37 (4), 408–432.

- Flint, D., 1971. The role of the auditor in modern society: an exploratory essay. Accounting and Business Research, 1 (4), 287–293.

- Foucault, M., 1980. Confessions of the flesh. In: C. Gordon, ed. Michel Foucault – Power/Knowledge: Selected Interviews and Other Writings 1972–1977. New York: Pantheon Books, 194–228.

- FRC, 2020. A Matter of Principles: The Future of Corporate Reporting. London: Financial Reporting Council.

- Freedman, J., and Power, M., 1991. Law and accounting: transition and transformation. The Modern Law Review, 54 (6), 769–791.

- Ge, W., and McVay, S., 2005. The disclosure of material weaknesses in internal control after the Sarbanes-Oxley Act. Accounting Horizons, 19 (3), 137–158.

- Gray, R., and Bebbington, J., 2001. Accounting for the Environment. Thousand Oaks, CA: Sage.

- Gjesdal, F., 1981. Accounting for stewardship. Journal of Accounting Research, 19 (1), 208–231.

- Hacking, I., 1983. Representing and Intervening: Introductory Topics in the Philosophy of Natural Science. Cambridge: Cambridge University Press.

- Haldane, A.G., and May, R.M., 2011. Systemic risk in banking ecosystems. Nature, 469 (7330), 351–355.

- Hardy, C., Maguire, S., Power, M., and Tsoukas, H., 2020. Organizing risk: organisation and management theory for the risk society. Academy of Management Annals, 14 (2), 1032–1066.

- Hautsch, N., Schaumburg, J., and Schienle, M., 2015. Financial network systemic risk contributions. Review of Finance, 19 (2), 685–738.

- Healy, P.M., and Wahlen, J.M., 1999. A review of the earnings management literature and its implications for standard setting. Accounting Horizons, 13 (4), 365–383.

- Hessling, A., and Pahl, H., 2006. The global system of finance: scanning Talcott Parsons and Niklas Luhmann for theoretical keystones. American Journal of Economics and Sociology, 65 (1), 189–218.

- Hines, R.D., 1988. Financial accounting: in communicating reality, we construct reality. Accounting, Organizations and Society, 13 (3), 251–261.

- Holling, C.S., 2001. Understanding the complexity of economic, ecological, and social systems. Ecosystems, 4 (5), 390–405.