Abstract

This study provides a guide to accounting research on private firms with an emphasis on the European setting. We start by providing an overview of private firm financial reporting regulation in Europe and indicate how this institutional framework can be used to identify promising research settings that in part generalise beyond the European setting. Next, we discuss the availability of private firm accounting data and the underlying data generating process that involves private firms’ original reports, governmental and private data aggregators, and commercial data providers. We show how this process generates insightful data, but at the same time causes complex sample selection issues that researchers should take into account when assessing prior findings and developing new research projects. Finally, we identify potential areas of future work by reviewing the extant literature along the three main motivations for conducting private firm work: (i) to learn more about private firms per se, (ii) to learn more about what distinguishes private firms from public firms, and (iii) to obtain insights from private firms that generalise across all firms.

1. Introduction

Private firms are a cornerstone of global economic activity. Entrepreneurs usually start small and most firms stay private over their lifetime, even after growing out of their entrepreneurial stage. It, therefore, is no surprise that private firms are vital for any jurisdiction and represent a large proportion of economic activity worldwide. For the European Economic Area (EEA), data from Amadeus, a popular research database on European public and private corporations maintained by Bureau van Dijk, shows that the overwhelming majority (99.87%) of firms are private. Moreover, these private firms represent 42.8% of aggregated corporate assets and 61.8% of the total workforce in Europe.Footnote1

Given the importance of private firms, there is a strongly growing interest in research on private firms in general and on private firm accounting in particular. Besides a multitude of questions with respect to the peculiarities of private firms and their comparability to public peers, studying private firms can also yield answers to questions of general interest given their distinctive characteristics regarding agency issues, business context, and regulatory settings. In this paper, we discuss the financial reporting environment for European private firms, review the extant literature, and outline research perspectives. We believe this to be insightful for a wide range of scholars, but we especially designed this overview to serve as a point of reference for PhD students and academics that are new to the private firm accounting literature.

While, in principle, private firms are a relevant study subject worldwide, we put particular emphasis on the European setting. The reason for this is primarily data availability. While in most countries no disclosure requirements for private firms exist, a large proportion of European firms is required to publicly disclose their financial statements, enabling researchers to study their reporting behaviour. We are convinced that this does not only apply to researchers that are interested in the European setting per se, but is also beneficial for everyone interested in more general accounting question as European private firms present a highly attractive ‘laboratory’ for studying the determinants and consequences of accounting and transparency.

We start by giving a concise overview of the heterogenous financial reporting requirements for European private firms and describe the different EU Member States’ applications of local GAAP versus International Financial Reporting Standards (IFRS). Understanding the peculiarities of this framework is essential for conducting informative research on private firms for two reasons: First, it determines the availability and nature of private firm accounting data across firms, time, and countries. Second, its heterogeneity across jurisdictions and time presents fruitful settings for various research questions.

Next, we describe available data sources for private firm accounting data. We discuss the role of official data repositories and private information intermediaries such as credit bureaus. Additionally, we focus on commercial data vendors and highlight important data peculiarities in popular commercial data sources that are partly driven by the data generating process and partly by data aggregation and presentation choices. Understanding these issues helps developing apt research designs with private firm accounting data. We close this first part of the paper by highlighting research questions specifically related to data availability and the selection issues caused by the data generating process.

The second part of the paper presents a structured review of the extant global private firm accounting literature and identifies potential topics for future research regarding private firm accounting in Europe and beyond. We organise this discussion along what we identify as the three main motivations for conducting private firm accounting research: (i) understanding private firms per se, (ii) understanding how private firms differ from public firms, and (iii) using private firms as a setting to obtain insights that generalise across private and public firms. At the end of each of these sections, we outline specific research perspectives.

In addition, we provide the opportunity to dive deeper into the literature by using an online extension of this guide that contains detailed bibliographic and topical information on all 121 references that underly our structured review (https://trr266.de/pfirmacclit). Using this web page, readers can interactively perform bibliographical analyses and explore the common themes and links that define the body of private firm accounting literature catered to their own preferences or research focus.

Not surprisingly, various aspects of the literature on private firm accounting have been reviewed before. Bar-Yosef et al. (Citation2019) provide a topical overview of the private firm accounting literature by classifying and summarising the main contributions from 95 research papers. A similar task has been taken on by Habib et al. (Citation2018), who surveyed 34 studies starting from 1999. Vanstraelen and Schelleman (Citation2017) consolidate the literature on the potential costs and benefits of auditing private firms’ accounts. Minnis and Shroff (Citation2017) provide theoretical arguments on why private firm public financial reporting and audit regulation may both be warranted and corroborate these views with survey results from standard setters and corporate representatives. Further, Hope and Vyas (Citation2017) discuss how private firms’ debt, equity, and trade credit decision relate to their financial reporting practices.

Our study complements these related studies by providing a holistic introduction to private firm accounting research along three dimensions: (1) We present the European institutional private firm financial reporting framework that researchers have to familiarise themselves with, (2) we extensively discuss the European data environment, and (3) we systematically explore the existing literature, reviewing not only studies about private firms but also studies using private firms that tackle broader research questions. We believe that, taken together, knowledge along these three dimensions is essential and will enable researchers to contribute further to the rich and growing field of private firm accounting research.

2. Private firm financial reporting in Europe: institutions and data

In this section, we review data availability and the institutional environment underlying the data generating process for European private firm accounting data. Europe has a long-standing tradition of financial reporting obliging both public and private firms to periodically disclose their financial statements. This feature makes Europe a convenient setting for private firm studies, as is also reflected in the geographical representation of countries in the literature review (69 of the 121 studies use European data). Europe, however, not just provides a convenient, but also a factually attractive setting to study private firm accounting for a number of reasons. First, while all countries of the European Economic Area (EEA) are classified by the World Bank as high-income countries (except for Bulgaria), the GDP per capita of EEA countries shows wide variation from the 58th to the top percentile of countries worldwide. Therefore, European evidence can be regarded as being informative for developed economies in general. Second, financial reporting rules in the EEA faced various changes and updates over the past decades, often generating cross-country regulatory differences that are helpful to identify causal effects of disclosure regulation. Third, the European setting, while mandating financial disclosure for many private firms, also generally exempts especially small limited and most unlimited liability private firms from mandatory disclosure, allowing researchers to study incentives and effects of voluntary disclosure by benchmarking firms under a voluntary disclosure regime with firms that are subject to mandatory disclosure in the same jurisdiction.

On the other hand, there are also potential limitations to the European setting, mostly regarding economies that are not comparable to Europe. First, we can learn little from European private firms about the role of private firm accounting in developing economies. Second, since political regimes in Europe are democratic and relatively stable, current-day European insights might not generalise to countries with different political regimes. This point, however, could partly be addressed by studying historical European settings like the transformation process of socialist to market-oriented regimes. Third, as prior work has documented that the role of private firm accounting likely varies with the prominence of public equity markets (Minnis and Shroff Citation2017, Gassen Citation2017) and given that these markets are rather average-sized in most European countries, only some countries (e.g. the U.K. and Switzerland) can be regarded as being fully representative of the role of private firm accounting in equity-market dominated economies. On the other end of the spectrum, there is not much that we can learn from European data about countries with underdeveloped or non-existent capital markets.

Taken the pros and cons together, we believe that the institutional richness and data availability for private firms across Europe provides researchers with a powerful combination to identify determinants and consequences of accounting and reporting transparency. To take full advantage of this setting, researchers need to embrace this institutional richness and familiarise themselves with the peculiarities of the data environment. We, therefore, start in Section 2.1 by giving an overview of reporting requirements for European private firms and especially focus on cross-country variation in the use of local GAAP versus IFRS. Next, we discuss available data sources for private firm accounting data in Section 2.2, and highlight specific data features that are influential for the choice of research designs.

2.1. The European regulatory reporting environment

2.1.1. Reporting requirements

In Europe, most limited liability firms, independent of their listing status, are required to prepare and publish financial statements. The 4th Company Law Directive (78/660/EEC) introduced the requirement to prepare unconsolidated (individual) financial statements in Citation1978, and the 7th Company Law Directive (83/349/EEC) introduced the requirement to prepare consolidated financial statements for companies (parent) that control another entity (subsidiary) in Citation1983.Footnote2

Since the initial publication of the directives, which had to be transformed into national law by the EU Member States, various amendments had been made, and Directive Citation2013/Citation34/EU ultimately repealed Directives 78/660/EEC and 83/349/EEC. This latest directive, which Member States had to incorporate into national law by 20 July 2015, aims at increasing the comparability across the European Union and at easing the reporting burden for very small ‘micro entities’. Other than the ‘micro’ category, the directives require different levels of disclosure for ‘small’, ‘medium’, and ‘large’ firms.Footnote3 Member States are allowed regulatory discretion, for example, to permit medium-size firms to file abridged financial statements and small companies even to omit the filing of income statements altogether. These national discretions have led to variation in disclosure requirements across Member States. Germany, for example, allows small firms to omit income statements (§326 of the German Commercial Code), while Italy requires small firms to file income statements and only allows few exceptions for small and micro firms (Art. 2435 bis. Italian Civil Code).Footnote4

To get a better understanding of the extent of differences across jurisdictions, we use the availability of income statements for ‘small’ or ‘micro’ entities as an example. In jurisdictions where such firms are allowed to omit the income statement, we should observe only a small fraction of them to report sales information voluntarily, whereas in jurisdictions that require income statements for small firms, we expect sales information to be universally available. In , we use Bureau van Dijks’ Amadeus database to report the percentage of firms that provide sales information separately for the different size categories (based on total assets).Footnote5 We observe substantial variation across countries. Whereas in some countries virtually all small firms report sales (Croatia, Czech Republic, Greece, Italy, Malta, Norway, Romania, Slovakia, and Switzerland), the ratio of small firms reporting sales is below 6% in Ireland, the Netherlands, and the UK. These stark differences point at the significant heterogeneity of disclosure requirements in the EU.Footnote6 The resulting variation in available line items is relevant for all studies requiring income statement data in cross-country settings as it implies varying sample coverage across countries. Examples for topics that require the use of income statement data include the cost-asymmetry literature, studies assessing the profitability of private firms, or studies that use unconsolidated data to determinant the amount of tax-motivated profit shifting.

Table 1. Private firms in the European Union by size.

Compared to limited liability firms, unlimited liability firms generally do not have to make their financial statements publicly available based on EU regulations. However, it is noteworthy that the EU limited liability regulations also apply to unlimited liability firms when all shareholders are limited liability entities themselves (e.g. Société en Nom Collectif in France, Par. 264a German Commercial Code). In addition, some EU countries have regulations in place that require unlimited liability firms to publicly disclose financial statement data when these are above a specific size threshold. Examples include Belgium (for general partnerships, ordinary limited partnerships, or co-operative companies with unlimited liability) and Germany (regarding the provisions in the Publizitätsgesetz (PublG)). Other countries do not apply specific size criteria but may still require unlimited liability companies to report financial statements in the case of multiple shareholders (e.g. Sociedad Comanditaria par Acionas in Spain).

2.1.2. IFRS vs. local GAAP

While public firms in Europe have to apply International Financial Reporting Standards (IFRS) if listed on an EU-regulated market (Regulation EC/Citation1606/Citation2002),Footnote7 EU Member States mostly require private firms to report under domestic Generally Accepted Accounting Principles (GAAP). Country-specific rules to require, permit, or prohibit the use of IFRS differ for consolidated statements and unconsolidated statements.Footnote8

The majority of countries allow, but do not require private firms to adopt IFRS voluntarily for their consolidated financial statements (Cyprus is the only country that requires private firms to adopt IFRS for consolidated statements). However, some Member States require specific private firms to adopt IFRS, such as large companies in Malta or large subsidiaries of publicly listed companies in Croatia, Spain, and Greece. Voluntary adoption of IFRS is overall relatively low. For instance, Bassemir (Citation2018) documents that less than 10% of German firms voluntarily adopt IFRS for their consolidated statements.

For unconsolidated financial statements – also referred to as individual, single, or statutory accounts – the use of IFRS is more restricted. For example, Austria, Belgium, France, Germany, Romania, Spain, and Sweden require private firms to use local GAAP for unconsolidated financial statements, often due to a strong link between financial accounting and tax accounting or because of dividend payout rules. Other countries, including Denmark, Estonia, Ireland, Italy, the Netherlands, Norway Slovenia, and the UK, do permit the use of IFRS also for unconsolidated accounts. Again, only Cyprus requires IFRS for unconsolidated accounts, and Malta, Croatia, and Greece require IFRS for larger firms or significant subsidiaries of listed groups.

The introduction of IFRS for public firms motivated national standard setters to adapt local GAAP systems. For example, in 2009 Germany passed the Accounting Law Modernization Act (Bilanzrechtsmodernisierunggesetz), which introduced several elements of IFRS into German GAAP (Fülbier et al. Citation2017). Nonetheless, local GAAP in Germany as well as in several other countries (such as Belgium, France, and Italy) still differs substantially from IFRS. The reason for this is that the local GAAP systems in these jurisdictions are still predominantly guided by specific considerations such as taxation or creditor protection. In contrast, local GAAP systems in other EU countries, including Croatia, Denmark, Finland, Greece, Malta, Poland, Portugal, and Slovenia are generally more aligned with IFRS and local legislators explicitly refer to IFRS standards. We are, however, not aware of any comprehensive survey allowing the in-depth comparison of current national GAAP systems. Such a granular overview would be particularly helpful in facilitating the analysis of alternative GAAP systems and their economic consequences.Footnote9

2.2. Data availability

2.2.1. Local business registers

Data availability is crucial for accounting research and is predetermined by the national disclosure regulation that, as discussed in the previous section, varies across time, jurisdictions, and firm characteristics. One possibility to obtain private firm financial reporting data is to directly access the national business registers. This is a direct outcome of EU Directive Citation2009/Citation101/EC, which requires all Member States to disclose company information including financial statements in line with the 4th and 7th Company Law Directive (Directive Citation2009/Citation101/EC, Article 2 (f)). For this purpose, each Member State has to establish a central register where all limited liability companies have to disclose their information electronically (including an option to file scanned copies). Documents filed before 31 December 2006, however, are not required to be included in the registers (Article 3 (3)). The Directive prescribes that the access to these files should be at a minimum cost, i.e. should not exceed the administrative costs to obtain a copy. We summarise all company registers of the EU Member States in the Online Appendix.Footnote10

The obvious disadvantage of obtaining data directly from the business register is that it requires laborious hand-collection of data. However, directly accessing the national business registers provides unique opportunities for in-depth research. First, the national business registers are useful for double-checking data that is provided in commercial databases (e.g. when it is not clear whether a database reports modified or as-is accounting data). Second, researchers can get access to the notes to the accounts, which are regularly not included in commercial databases. Pierk and Weil (Citation2016), for example, hand-collected data from the German business register to identify which private firms adopted a major German GAAP reform early. Similarly, Kaya and Pronobis (Citation2016) hand-collect data on XBRL adoption status from the homepage of the Central Balance Sheet Office of the National Bank of Belgium.

2.2.2. Commercial data providers

A more common way to gather private firm data in accounting research is to use commercial data providers. An important source of firm-level data on private firms is Bureau van Dijk, which offers several databases on public and private firms at the country, world region, and global level. The Orbis database covers countries worldwide (Cascino and Gassen Citation2015, Haga et al. Citation2018, Downes et al. Citation2018, Beuselinck et al. Citation2019), while the Amadeus database covers European countries only.Footnote11 Especially Amadeus is widely used in the accounting literature (e.g. Bernard Citation2016, Bernard et al. Citation2018, Burgstahler et al. Citation2006, Peek et al. Citation2010, Minnis and Shroff Citation2017).

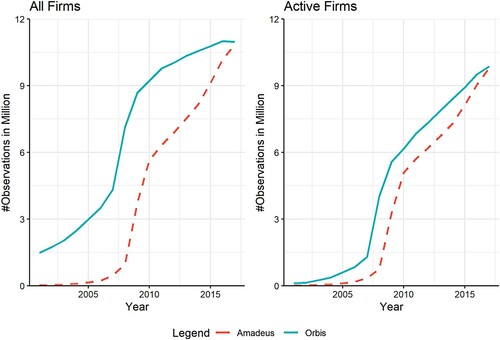

Interestingly, although some researchers use the worldwide Orbis database, they often also limit the sample to European firms or even just one single country.Footnote12 For example, Haga et al. (Citation2018) only include UK firms in their sample, and Downes et al. (Citation2018) focus on European firms. It appears that the Orbis and Amadeus databases are often used interchangeably and the choice of the researchers is most likely driven by institutional data availability. It is, however, important to note that although the data is provided by the same data provider, the database composition differs. This data coverage gap between both databases is illustrated in and depicts the time-series of coverage for the entire universe of unconsolidated financial statements accessed through the Wharton Research Data Service (WRDS) for the period 2001–2017.

Figure 1. Comparison in data coverage – Orbis versus Amadeus. Note: This figure shows the number of firms of the European Economic Area as reported in the Amadeus database (dashed line) and the Orbis database (solid line) between 2001 and 2017 (Download: 3 September 2020). The data represents the universe of unconsolidated financial statements accessed through the Wharton Research Data Service (WRDS). In the Orbis database, we require the consolidation code (conscode) to be ‘U1’ or ‘U2’ and in the Amadeus database, we require the reporting basis (repbas) to be ‘Unconsolidated Data’. We only consider firms with non-missing and non-negative total assets.

shows that data coverage in the European Economic Area is generally higher in the Orbis database compared to the Amadeus database. To a large extent, this difference is driven by non-active firms. While the Orbis database includes these firms, they are often not included in the Amadeus database. Depending on the research question, this different treatment of survivorship can potentially bias the results. We, therefore, encourage researchers to be aware of and to discuss the consequences of database choice.

For single country studies, a country-specific database may be better suited. Bureau van Dijk offers such country-specific databases as well, such as Bel-first for Belgium and Luxembourg (e.g. Andries et al. Citation2017, Beuselinck et al. Citation2008, Citation2009, De Meyere et al. Citation2018, Gaeremynck et al. Citation2008); Fame for the U.K. and Ireland (e.g. Ball and Shivakumar Citation2005, Citation2008, Dedman and Lennox Citation2009, Dedman and Kausar Citation2012, Dedman et al. Citation2014, Peel Citation2018); or Dafne for Germany (e.g. Bigus and Hillebrand Citation2017, Bigus and Häfele Citation2018).Footnote13 The benefit of using country-specific datasets is that they provide more detailed information including country-level GAAP characteristics which are not available in cross-country databases (see Section 2.2.3 on Data Aggregation).

The commercial databases usually obtain data from local data providers, which themselves often directly collect the data from the local business registers. displays the country-specific data sources for Bureau van Dijk’s Amadeus database (as reported for 2018). These data providers fall into roughly two categories: Official agencies like central banks or statistical bureaus, and credit agencies. It seems likely that the data collection methods vary between these two groups. While the former collect data based on legal criteria such as corporate structures or size thresholds, the latter cover firm information for which there is demand from suppliers and credit providers. Consequently, a comparison of firm coverage in Amadeus with that of the World Bank’s Entrepreneurship Survey (columns (3) and (5) of ), which relies exclusively on administrative data, reveals that Amadeus regularly covers less than 75% (and sometimes less than 50%) of firms in a given country. Understanding the nature of the different data suppliers and their variation across countries is therefore relevant for the correct interpretation of the data. These differences also might provide further motivation for researchers to source data directly from the local data providers to yield access to additional details that would not be available otherwise.

Table 2. Yearly average of new firms – Amadeus and World Bank.

2.2.3. Important data features

2.2.3.1. Parent companies, subsidiaries, and stand-alone firms

Researchers need to clearly define the set of firms and financial statements that should be used to answer their research question. European data covers different sets of financial statements. Business groups usually consist of the (ultimate) parent company and the respective subsidiaries. For the parent company, the consolidated financial statements (group accounts) and unconsolidated financial statements are available. For subsidiaries, usually only unconsolidated statements are available, as subsidiaries that are themselves a business group are exempt from publishing consolidated financial statements (unless in the rare case that the subsidiary is publicly listed). Stand-alone firms only provide unconsolidated statements.

Prior literature on private firms often uses ‘independent’ firms only, which means the sample only includes consolidated statements of business groups and unconsolidated statements of stand-alone firms (e.g. Burgstahler et al. Citation2006). Thus, subsidiaries are not included. However, even the choice to include business groups and stand-alone firms simultaneously might affect the results of a paper (Bonacchi et al. Citation2019). In contrast to using ‘independent’ firms only, there might also be reasons for only including unconsolidated data of subsidiaries and/or stand-alone firms. For instance, Beuselinck et al. (Citation2019) use unconsolidated data of subsidiaries to study earnings management behaviour within multinational firms. Unconsolidated data is also often used in the area of taxation, as it is commonly the starting point to determine the tax liability. De Simone (Citation2016), for example, uses unconsolidated financial statements only to study the effect of IFRS adoption on tax-motivated profit shifting. Similarly, Markle (Citation2016) uses unconsolidated data to study tax avoidance incentives based on the home country tax system of multinational firms.

Related to the question of firm independence, it is important to note that the public filing requirement in Europe also affects legal structures that do not clearly match our economic understanding of a ‘firm’. For example, interim holdings, legal shells, or dormant firms without business activities might be included. Further, business groups may have tax minimising objectives so that subsidiary entity financial statements merely reflect tax incentives. Further, it is commonplace for individuals to reorganise private assets into limited liability structures for tax reasons. All these legal structures might show up as data points in company registers and commercial databases and the frequency of how often they do is likely to vary over jurisdictions and time. Given their effect on the distributional properties of key accounting measures like earnings, they will affect many research designs that use private firm data, in particular when inference is based on distributional properties such as for studies investigating conservatism or small loss avoidance.

2.2.3.2. Data aggregation

Research papers regularly use international databases such as Orbis or Amadeus even when the research design addresses a country-specific research question. The obvious advantage of using these databases is that data entries are standardised and easily accessible. The disadvantage, however, is that the standardisation comes at the cost of losing information. As an illustration, in the Appendix, we compare the 2018 consolidated financial statements of Volkswagen AG as published in the German Federal Gazette with data provided by Bureau van Dijk’s databases Orbis (worldwide data), Amadeus (European data), and Dafne (German specific data). The financial statements filed with the official German register show 23 asset line items, 26 equity and liability line items, and 20 line items in the profit and loss statement. Due to the classification procedures of Bureau van Dijk, however, Amadeus and Orbis aggregate this data and only provide 10 different asset line items, 12 equity and liability line items, and 14 line items in the profit and loss statement.Footnote14

The relevant country-specific database Dafne, however, provides much more detailed data. In total, the database provides 28 asset line items, 20 equity and liability line items, and 17 profit and loss line items. In addition, the Dafne database also provides more detailed information for some line items, e.g. maturity information for loans and liabilities. This data can potentially be used to address research questions that cannot be answered with standardised cross-country data.

In addition, the Appendix reveals that the aggregation rules differ between Amadeus and Orbis, an issue that to the best of our knowledge has not been acknowledged nor addressed by prior research. As data aggregation garbles information, the varying amounts of aggregation across databases can affect findings related to the information content of private firm accounting. In particular research designs that rely on the number of reported line items to assess the quality of the provided information (Chen et al. Citation2015) can be expected to be substantially affected by database choice.

2.2.3.3. Time-invariant data items

A relevant problem specifically for researchers that want to use private firm data from Bureau van Dijk’s databases is that for certain items only data from the most recent update is available, i.e. certain information is time-invariant in the database, but might change over time in reality. This is especially the case for listing status, ownership data, and auditor information. Depending on the research question, researchers must be aware of these static data points as this may be an obstacle to their research designs. One way to overcome these data limitations is to acquire Bureau van Dijk’s historical data snapshots to construct time-series data. Alternatively, researchers can use the recently constructed flat-file data feeds provided by Bureau van Dijk that contain the full history of Bureau van Dijk financial data. Where access to neither the historical snapshots nor the relatively expensive Orbis data-feed is available, a commonly used alternative is to limit the sample to the subset of recent years as a robustness test with a low likelihood of significant data changes over time (e.g. Markle and Shackelford Citation2012, Minnis and Shroff Citation2017).

2.2.3.4. Data coverage

Sufficient data coverage is an essential prerequisite for inferences that are generalisable to the broader population of private firms. To illustrate if and how data coverage changes over time, displays the number of independent European private firms covered in the Amadeus database between 2012 and 2019.Footnote15 We only include independent firms (i.e. firms that are not controlled by any other higher-level shareholder), because this is a common selection made in the literature. In 2019, most European observations are from the UK (around 36%) and Italy (around 15%). The overall number of firms as reported by Amadeus increased remarkably from 1,428,792 in 2012 to 2,050,051 in 2019, an increase of around 44%.Footnote16 Individual countries display an increase in covered firms of more than 200% (e.g. Poland). Given that the reasons for individual coverage are mostly unknown, an important takeaway from the drastic growth in the number of observations is that conclusions from private firm studies that were conducted several years ago could potentially be affected by changes in sample representation. As an example, for the UK, one of the most comprehensively examined countries in the literature covered in this review, the number of private firms covered by Amadeus almost doubled over the past decade.

Table 3. Private firms in the European Union as reported in Amadeus.

These coverage issues directly affect descriptive studies that seek to be representative of the underlying population of European firms. In addition, they are relevant for studies that base inference on time (e.g. event studies, interrupted time series or difference-in-differences designs) and that employ unbalanced panels.

2.2.4. Non-EU data

In the interest of completeness, in this section, we provide an overview of exemplary non-EU data sources used in the literature. A few studies use the Sageworks database (Minnis and Sutherland Citation2017, Minnis Citation2011, Hope et al. Citation2013, Citation2017), which covers U.S. private firms. Although sample sizes here can be relatively large, smaller firms are less likely to be covered because the data was obtained from auditors and thus excludes firms that do not use an auditing firm. At the same time, the largest private firms tend to not be covered as well, as the Big 4 auditors did not contribute to the Sageworks database. Furthermore, Sageworks has discontinued its reporting activities, and the last year available is 2009 (Hope et al. Citation2017). Another potential source of data for private firms in the U.S. is regulatory filings, e.g. for banks (Beatty et al. Citation2002) or insurance companies (Beaver et al. Citation2003), or (confidential) tax filings with the IRS (Lisowsky and Minnis Citation2020).

Other papers use survey data provided by the World Bank. Francis et al. (Citation2008) and Francis et al. (Citation2011) use the World Business Environment Survey, which was conducted in the late 1990s and early 2000s, and Chen et al. (Citation2011) use the 2002–2005 World Bank’s Enterprise Survey. Cassar (Citation2009) examines data from the 2005–2011 Panel Study of Entrepreneurial Dynamics (PSED) to gather entrepreneurial reporting initiatives in the US, but this data is highly specific and not used in other accounting studies. Cassar and Gibson (Citation2008) use the Business Growth and Performance Survey by the Australian Bureau of Statistics to observe variation in the use of budgets and internal accounting preparation. Such data is unique and typically not available in commercial databases, so it can yield innovative new insights on fine-grained discussions on reporting decisions in private firms. Cassar et al. (Citation2015) use data from the 2003 Survey of Small Business Finance (SSBF) administered by the U.S. Federal Reserve and Small Business Administration.

Finally, another common method of obtaining information about private firms’ reporting environment within and outside the EU are self-developed, customised surveys (Penno and Simon Citation1986, Cloyd et al. Citation1996, Davila and Foster Citation2005, Citation2007, Sandino Citation2007, Indjejikian and Matějka Citation2009, Guerreiro et al. Citation2012, Niemi et al. Citation2012, Svanström Citation2013) or expert interviews (Gassen Citation2017, Bourveau et al. Citation2020). provides an overview of the data sources used in papers included in this overview study. A complete list of all data sources can be found in our online database.

Table 4. Frequently used databases.

2.3. Research perspectives

Some research questions arise directly from the regulatory framework as well as from our discussion of the availability of private firm reporting data. The overarching takeaway is that while public and commercial databases allow nearly complete coverage of all public firms in an economy, researchers need to be aware of generally overlooked selection issues regarding private firm coverage. Similar to the question of going public vs. staying private, these issues offer research opportunities centred on the question for which private firms, and to what extent, financial accounting data can be observed in the first place.

First, disclosure regulation plays an essential role in private firm reporting, and firms can circumvent disclosure regulation by choosing legal forms that are generally not (or less) subject to regulation. For example, partnerships and sole proprietorships are not required to publish financial statements in Europe and, consequently, are usually not covered by commercial databases. One research avenue could potentially target the determinants of voluntary disclosure of such legal entities and examine whether growth ambitions or financing needs are driving their reporting decisions (similar to, e.g. Beuselinck et al. Citation2008). Second, regulatory reporting thresholds often determine the quantity of accounting information provided by firms. For instance, as outlined in Section 2.1, the amount of disclosure requirements in Europe depends on whether firms are classified as micro-firms, small, medium, or large corporations. Research can shed light on the perceived cost of disclosure by investigating potential size management around specific thresholds prior to versus post such size classification changes (similar to, e.g. Bernard et al. Citation2018). Third, little is known about the determinants of compliance with private firms’ financial reporting requirements. Public enforcement agencies, which were set up with the introduction of IFRS in Europe, only enforce the IFRS statements of public firms, but are not responsible for private firms’ financial statements. There exists descriptive country-level evidence that stricter enforcement of financial statement disclosure for private firms has increased compliance in Germany (e.g. Laschewski and Nasev Citation2017). An appealing avenue for future research could focus on the channels of enforcement and the determinants of their effectiveness in the absence of capital market oversight. Evidence on potential non-compliance can again further our understanding of the costs of disclosure for private firms.

In addition to these questions regarding the actual production of financial information in the first place, researchers need to take into account the extent to which this information is covered in their data sources. For instance, database providers rarely collect private firms’ financial reports themselves but instead rely on information intermediaries such as credit bureaus. Where there is no demand from the credit bureaus’ customers regarding certain private firms, likely, these firms are also not covered in their databases (see and Section 2.2.2). Insights on the determinants of inclusion in such credit registers can help to understand the nature of the demand for private firm’s public financial accounting.

A related point is that, as outlined above, the coverage of private firms in commercial databases has changed substantially across jurisdictions and over time, which might be associated with a systematic bias of earlier findings if newly covered firms differ from those included in the past. Researchers should therefore critically question the generalisability of earlier results to the general population of private firms, and studies that document database coverage bias by revisiting prior studies or by using alternative data sources would be particularly important. Similarly, several well-cited studies in the literature are based on single-country data (e.g. from Belgium and the UK) or are limited to single industries (e.g. banks). It may be interesting to examine whether it is possible to reconcile their sometimes conflicting results based on sample selection.

Additionally, we encourage researchers to tap innovative datasets beyond commercial data providers, e.g. by using local business registers or based on manual data collection. Despite the potential efforts in data collection, the creation of such innovative datasets avoids any data loss due to aggregation and standardisation of data providers and can yield novel insights beyond what we could grasp from commercial databases (e.g. detailed footnote disclosure are often not included in commercial databases).

3. State of the literature and research avenues

After discussing the regulation of private firm financial reporting in Europe and the availability as well as peculiarities of private firm financial accounting data, in this section, we present a structured review of the global private firm accounting literature. After briefly presenting the methodology of our review, we structure our discussion along what we identify as the three main motivations for conducting private firm accounting research: (i) to understand private firms per se, (ii) to understand how private firms differ from public firms, and (iii) to use private firms as a setting to obtain insights that generalise across private and public firms. At the end of each of these sections, we outline potential research perspectives.

3.1. Methodology

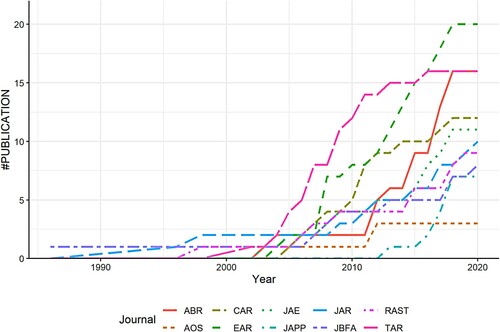

We preselect the papers in this literature review over a 35-year time window (1986-2020) from a list of 10 journals as the premier category of academic peer-reviewed business journals that welcome studies on any accounting-related subject and which embrace various research methodologies.Footnote17 For each of these journals, we screen titles and abstracts for variations of the keyword ‘private firm’ to identify potentially relevant studies. We then manually inspect all flagged papers to determine whether they fall explicitly within the scope of this review. In particular, we require that the inclusion of private firms is an essential and explicit part of the research question or research design, and not just an artefact of data collection. For example, we do not include studies that simply happen to use a pooled sample of private and public firms without following up on this distinction (e.g. Chi et al. Citation2012).Footnote18 Further, we exclude a subset of papers that focus on firms that have both features of a public and private firm status, for instance when they have private equity but hold public debt (e.g. Badertscher et al. Citation2014, Givoly et al. Citation2010). We complement these selection steps with a snowballing procedure that includes studies from other journals which were referred to at least five times in the originally selected papers. This procedure ensures that we cover contributions that have proven to be impactful in the accounting community even when not published in the core journals. We do, however, not include studies in our literature review that were not (yet) subject to peer review, regardless of their impact, but include examples when discussing research perspectives. The final sample includes 121 studies that have been published between 1986 and 2020. shows the cumulative development of published papers over time by journal. Despite different growth rhythms across journals, the general trend shows that papers on private firms are continuously being published in nearly all outlets.Footnote19

Figure 2. Publications over time. Note: This figure shows the cumulative number of publications covered in the literature review over time by our core list of 10 accounting journals. Studies from other journals that were identified via snowballing are not included.

In the following subsections, we classify the identified literature along the three guiding research questions outlined in the introduction. More specifically, we distinguish between three broad categories of research papers. First, a core stream of the literature looks at research questions that study private firms per se, for example, reporting incentives in IPO settings, or consequences of the involvement of Private Equity investors (Section 3.2). Studies in the second category analyze cross-sectional differences between public and private firms (Section 3.3). Finally, studies in the third category are not only interested in private firms per se, but are concerned with research questions that apply to a wider range of firms (Section 3.4).

3.2. Private firms: specific research questions

The literature covered in this section is concerned with research questions that cannot be generalised to public firms, as they address topics that only apply to private firms or that have an explicit descriptive focus on private firms only. We broadly structure studies in this section along the private firm lifecycle from early-stage start-ups that seek equity financing to exit options like IPOs and private takeovers.

3.2.1. Legal form choice

One of the first decisions a new firm faces is the choice of the legal form. We are only aware of one paper that addresses accounting issues around this decision. Bigus et al. (Citation2016) investigate whether financial accounting choices made by German private firms depend on legal form. In line with the agency argument of debt, they observe that corporations exhibit higher levels of income smoothing, conservatism, and small positive profits compared to partnerships and one-person businesses.

3.2.2. Reporting in startup firms

Cassar (Citation2009) studies a sample of 200 U.S. firms in the process of starting up a business to analyze financial reporting decisions in the absence of regulatory oversight. He finds that external financing, venture scale, and the level of competition are positively associated with the intended frequency of financial statement preparation. In a related study, Cassar and Gibson (Citation2008) find for a large sample of privately held small Australian firms that internal accounting report preparation significantly improves internal revenue forecast accuracy, but only for the subset of firms that operate in high uncertainty environments. Allee and Yohn (Citation2009) document that small privately held businesses that are not subject to SEC regulation with audited financial statements benefit in the form of greater access to credit and that firms with accrual-based financial statements benefit in the form of a lower cost of credit. Similarly, Cassar et al. (Citation2015) study small, privately held U.S. companies and document that higher third-party credit scores, but not the use of accrual accounting, decrease the likelihood of small business loan denial. Yet, accrual accounting does help corporations in reducing the cost of debt after debt approval. A related stream of literature studies determinants and consequences of adopting management accounting systems in start-up firms (Sandino Citation2007, Davila and Foster Citation2007, Davila et al. Citation2015).

3.2.3. Private equity financing and financial reporting

With respect to equity financing decisions, several studies investigate the choice of private equity (PE) and venture capital (VC) funding, which allows firms to recapitalise without being publicly listed on a stock exchange, and how this choice potentially affects the financial reporting process and outcomes. Armstrong et al. (Citation2007) study a sample of U.S. private venture-backed firms and observe on average pessimistic short-term management forecasts and optimistic longer-term management forecasts. Beuselinck et al. (Citation2008) investigate a sample of Belgian private firms and document that PE investors do not necessarily target firms that signal their potential superior quality through voluntary disclosure initiatives. However, once PE investors are on board, firms disclose more financial information voluntarily. Using the same PE-backed private firms dataset, Beuselinck et al. (Citation2009) document that PE involvement also results in higher quality financial reporting (as operationalised by the timeliness of loss recognition). These combined results suggest that the enhanced information environment structure post-PE involvement results in better reporting quality.

3.2.4. Initial public offerings and earnings properties

Several studies investigate how private firms’ reporting quality is shaped by the decision to go public. Largely, this literature has evolved from arguments in studies such as Teoh et al. (Citation1998), who document that IPO firms report inflated earnings prior to the IPO event in an attempt to positively impact IPO pricing. Ball and Shivakumar (Citation2008) question this finding and document for a sample of UK IPOs that upward-biased estimates of discretionary accruals around large transactions and events are potentially causing the results. They show that IPO firms in fact report earnings of a higher quality and explain their results by the higher demand for high-quality reporting post-IPO and by the higher monitoring efforts by auditors, corporate boards, financial press, rating agencies, and other information intermediaries. Fan (Citation2007) studies theoretically and empirically how ownership retention and reported earnings jointly signal IPO quality. She finds empirical evidence that the trade-off between both signals depends largely on the uncertainty over future earnings. In a more recent study using quarterly earnings data, Sletten et al. (Citation2018) document abnormal positive accruals only for the quarter before and for the lockup expiration quarter, but find no evidence of income-increasing earnings management before the IPO event itself, suggesting that narrower time-frame analyses provide a better identification strategy. Alhadab et al. (Citation2015) examine real and accruals earnings management in relation to IPO failure risk. They document that firms do apply real and accruals earnings management in the IPO year and that opportunistic earnings management is associated with a higher IPO failure risk ex-ante. Their results seem to be strongest for those observations with the highest real earnings management during IPO years, confirming that real earnings management is a potentially more harmful management practice for long-run firm survival.

3.2.5. Value relevance of private firms' financials

Hand (Citation2005) examines the value relevance of financial statement information before firms go public and shows that financial information is equally relevant in private markets and in public equity markets. Relatedly, Armstrong et al. (Citation2006) document that financial statement information explains a sizable component of the levels and changes in valuation in both the Pre-IPO and Post-IPO periods. De Franco et al. (Citation2011) revisit the notion of a private company valuation discount and examine the importance of hiring a Big 4 auditor. Their evidence confirms that Big 4 auditor engagements yield higher sale proceeds of controlling interests in U.S. private firms. Finally, Elnathan et al. (Citation2010) document for a sample of Israeli firms that experts rely substantially on private firms’ reported earnings for valuation and transaction services despite the possible threat of manipulation of these data in a private firm context.

3.2.6. IFRS for SMEs

Two other papers are concerned not with firm’s reporting choices, but with the country-level decision to implement IFRS for SMEs. Kaya and Koch (Citation2015) find that countries without their own national GAAP system or that allow full IFRS implementation for private firms are more likely to also allow IFRS for SMEs. Gassen (Citation2017) complements these findings and provides descriptive evidence about the state of international implementation of IFRS for SMEs from a country-level series of expert interviews.

3.2.7. Research perspectives

Understanding the role of financial reporting in the life cycle of private firms is of high relevance. Due to data availability, almost all studies investigate limited liability companies. However, financial accounting and disclosure regulation can already affect the decision to incorporate as a limited liability company. If a start-up firm is highly concerned about proprietary costs, it might decide not to incorporate and therefore, at least in the European Union, avoid public disclosure of financial statements. Studies on these early-stage decisions may prove to be valuable in understanding the usefulness of accounting information production for private firms.

Successful startups usually face the challenge of how to finance their growth opportunities. While there is some evidence on the role of accounting in private lending relationships, little is known about how early-stage firms communicate with their shareholders and how this communication might differ between various types of shareholders, e.g. private shareholders, venture capital firms, or private equity funds. Although we have some evidence on this topic (e.g. Beuselinck et al. Citation2008), more research is warranted.

While these questions relate to the early years of a private firm, we also do not have a good understanding of the role of financial accounting regarding the exit options of private firm investors. Generally, the exit options for a private firm investor are to go public or to sell the shares in a private-to-private transaction. Some studies have been concerned with financial accounting in the IPO setting, but there is little evidence about its role in the detection and, in particular, valuation of private M&A targets except some small-sample studies in selected industries (Hand Citation2005, Armstrong et al. Citation2006). For example, potential areas of future research could be whether and how the value relevance of financial accounting information varies with private firm maturity, institutional characteristics, or accounting comparability to public peer firms.

Another important, but often neglected stage of the firm life cycle is declining and dying firms as well as firms in financial distress. Given that insolvency, bankruptcies and liquidations are everyday events, the literature on private firm accounting is surprisingly scarce on this topic. We believe that studies on how the relatively extreme incentives in these situations interact with the accounting regulatory framework, the insolvency framework, and the actual outcome would be potentially impactful. While for publicly listed firms, insolvency cases are relatively rare and are often resolved via delistings and restructurings, for private firms, insolvency cases are frequent and thus allow a more high-powered analysis. Given the complex nature of national insolvency laws, we also expect national settings that exploit these settings in detail to be promising in that regard. Importantly, many of these research perspectives are particularly suited for alternative data sources and research methods that do not rely on large archival databases. For instance, for early-stage private firms, financial reporting data is not generally available, and early customer and financing relationships are likely to rely on private information channels. Data from original or external surveys (Cassar Citation2009, Cassar and Gibson Citation2008, Cassar et al. Citation2015) or case studies can help to shed light on the provision and usage of financial reports for such firms. Likewise, the confidential nature of VC financing rounds and acquisitions by corporate or PE investors warrants in-depth analyses to gauge, e.g. the relevance of financial reporting relative to other sources of information in the due diligence process (Wangerin Citation2019). For firms in distress, on the one hand, financial reporting is a potential channel for stakeholders to learn about and react to the firm’s difficulties (i.e. it can accelerate bankruptcy), while on the other hand, financial reporting and disclosure can be a tool to manage or mislead stakeholders’ perceptions. Qualitative insights regarding the usage of information in the run-up to corporate failures can help to substantiate priors about the role of financial accounting in this intricate process. Finally, given the general lack of mandated financial reporting for private firms outside the EU, research on these countries by definition requires alternative ways of data generation, which can be particularly fruitful and allow the in-depth analysis of phenomena less present in Europe.

3.3. Private versus public firms

While accounting-related comparisons of public and private firms are concerned with different topics, a common theme is that the absence of complex agency structures and capital market demand in private firms reduces incentives for high-quality reporting. However, at the same time, more complex agency structures and capital market pressure for public firms also introduce incentives for strategic manipulation of accounting numbers in the first place. Consequently, it is a priori not clear which effect will prevail in shaping private versus public firm reporting behaviour.

3.3.1. Financial reporting characteristics and accounting quality

3.3.1.1. Earnings quality

In one of the most widely cited contributions of the private firm accounting literature, Burgstahler et al. (Citation2006) find that private firms in Europe show higher levels of earnings management than public firms. Hope et al. (Citation2013) confirm these findings studying accruals quality for a sample of U.S. companies, but additionally document that public firms’ higher level of accounting quality is conditional on their specific (mis)reporting incentives and market demand for financial information. Bigus and Hillebrand (Citation2017) show that a low number of bank relationships negatively affects accounting quality of private firms, but no such effect is observed for public firms. Shuto and Iwasaki (Citation2015) find for a Japanese sample that firms with tight relationships with their banks are more likely to manage earnings to report slightly positive earnings. In particular, the authors document that this relationship is more pervasive for private firms than public firms.

Other studies find conflicting results and suggest that private firms have a higher level of earnings quality than public firms. Beatty and Harris (Citation1998) and Beatty et al. (Citation2002) document that private banks in the U.S. engage less in earnings management than their public peers. This is consistent with Beaver et al. (Citation2003), who find that only public insurers manage their loss provisions to avoid small losses, and Kim and Yi (Citation2006), who document that Korean private firms engage less in earnings management through discretionary accruals. Regarding real earnings management, Haga et al. (Citation2018) find that UK public firms engage more in managing sales, discretionary expenses, and production, while Hall (Citation2016) suggests that U.S. public banks have a stronger inclination than private banks to adjust their labour cost to meet reporting targets.

So far, there have been only few attempts to reconcile these contradictory findings. An exception is a recent study by Bonacchi et al. (Citation2019), who show that the lower earnings quality of private firms is driven by private standalone firms, while private business groups have even higher earnings quality than publicly listed business groups.

3.3.1.2. Conservatism

While one of the earliest studies in our review finds that private firms are less likely to choose certain income-increasing accounting alternatives than public firms (Penno and Simon Citation1986), later work almost consistently suggests a higher level of conservatism among public relative to private firms. Ball and Shivakumar (Citation2005) find that loss recognition is less timely for private than for public firms in the UK. Similarly, Ball and Shivakumar (Citation2008) observe that IPO firms from the UK report more conservatively than both their private and public peers. Peek et al. (Citation2010) provide evidence that more conservative public firm reporting is driven by public firms’ creditors’ relatively stronger demand for asymmetric loss recognition. Nichols et al. (Citation2009) find that U.S. public banks show a higher degree of conditional conservatism in loan loss provisions relative to their private counterparts, and Gormley et al. (Citation2012) document that foreign bank market entry causes higher levels of conservatism for Indian firms.

3.3.1.3. Other aspects of financial reporting

Few papers have compared other financial reporting characteristics among private and public firms. Yoo et al. (Citation2018) provide evidence that during the 2007/2008 financial crisis, Korean public firms were more likely to adopt the Fair Value option for PP&E, hinting at more market demand for public fair value information with diversified shareholders. Aerts (Citation2005) finds that in corporate narratives like the director’s report, both acclaiming and defensive self-presentational tendencies are more pronounced in listed companies, pointing at the role of impression management as a reaction to market pressure. DiGabriele (Citation2008) documents that the private firm discount increases post the implementation of the Sarbanes-Oxley (SOX) Act, suggesting that SOX had detrimental consequences for private firms.

3.3.2. Audit

While there is extensive literature on auditing among private firms (see Section 3.4.3), only a few studies directly compare public and private firms. A common argument in these studies is that litigation and reputation risk is lower for private relative to public audit clients, potentially leading to lower levels of scrutiny. Against this backdrop, Bell et al. (Citation2015) provide evidence that in contrast to public firms, internal assessments of audit quality decrease with long tenure for private clients. Lennox and Li (Citation2012) find that audit firms that become limited liability companies (instead of full liability partnerships) are more willing to accept the more risky public clients, and Clatworthy and Peel (Citation2007) show that public UK firms pay higher audit fees than their private counterparts. Brivot et al. (Citation2018) provide interview evidence that the understanding of ‘audit quality’ differs across private and public firm auditors, with the latter focusing more on technical perfection and complete documentation than on professional judgment and value added to the audit client. Finally, Allee and Wangerin (Citation2018) suggest that private M&A targets are being perceived as less transparent, leading to a higher value of auditor verification of earnout provisions.

3.3.3. Tax

Several studies explore the differential importance of tax incentives across private and public firms, generally suggesting that, for example, capital market pressure and overall visibility reduce public firms’ inclination for tax aggressiveness. Results from a survey by Cloyd et al. (Citation1996), which have been later confirmed with actual tax return data by Mills and Newberry (Citation2001), suggest that the nontax costs of book-tax conformity for aggressive income-decreasing tax treatments are higher for public firms, which therefore are less likely to choose conformity even when it makes it easier to defend aggressive tax treatments against the IRS. Lin et al. (Citation2013) show that private firms display more intertemporal income shifting when faced with a tax rate change. Similarly, Beuselinck et al. (Citation2015) find that private multinationals engage more in income shifting to low tax subsidiaries. Hoopes et al. (Citation2018) argue that the cost of tax disclosure is higher for private firms and find that when tax disclosures were introduced in Australia in 2015, private firms engaged more in avoiding such disclosures.

3.3.4. Research perspectives

While we observe that papers comparing private and public firms are among the most cited work in our overview, we are still lacking a good understanding of the decision of private firms to go public, and in particular of the role of financial reporting in this context.Footnote20 For instance, tighter disclosure regulation, more visibility, and higher levels of scrutiny from supervisors and information intermediaries in public markets might discourage firms from going public. There are a variety of possible sources of the increased cost of reporting such as, for example, proprietary costs, or an insufficient internal reporting environment. Such questions are highly relevant per se, but in addition, they raise concerns about self-selection and endogeneity both when directly comparing public and private firms and when studying common research questions regarding private or public firms in isolation.

Next, the partially contradicting findings regarding, for example, differences in financial reporting quality across public and private firms warrant research that reconciles prior evidence and explains differences on a more granular level. In particular, a textured analysis of stakeholder structures beyond the dichotomous public/private split can potentially shed light on the exact sources of reporting incentives in various agency settings. An example of such an approach is the recent study by Bonacchi et al. (Citation2019), who examine variation across private groups and standalone firms. A related promising avenue of research is to examine the role of stakeholders other than direct capital providers such as shareholders and banks. For example, we know little about the role of trade credit, an important source of funding for smaller private firms, and corresponding information intermediaries like information bureaus and rating agencies.

Further, differences in the visibility of public and private firms also likely influence information demand from non-investment stakeholders regarding the disclosure of non-financial information, e.g. regarding environmental or CSR activities, and the consequences of these disclosures. In a similar vein, the effect of the public/private distinction on the external monitoring of tax aggressiveness is not well understood. There is also emerging literature on how visibility shapes regulators’ incentives for supervisory action (Kleymenova and Tomy Citation2021). Comparisons between public and private firms open promising perspectives to assess the interplay of financial and non-financial reporting, market discipline, and supervisory behaviour in regulated industries.

Corresponding to a closer examination of the impact of various stakeholder groups, there is a need to better understand differences in the channels through which those stakeholders might influence reporting incentives. An obvious example is executive compensation and, potentially, profit distributions. By definition, compensation for private firm executives cannot be based on market value and likely has to rely more on accounting numbers, which could exacerbate incentives for earnings management.

Further, so far there is also very limited knowledge on the role of the internal information environment and management accounting systems for private firms. In particular, an avenue for future research could be whether differences in internal resources drive observable differences in external reporting outcomes, or whether mandatory reporting requirements for public firms have positive spillover effects on the quality of internal controls in private firms, and which in turn may affect the latter’s decision-making.

A final problem is the tendency to use measurement concepts calibrated for public firms when assessing accounting outcomes for private firms. While the informativeness of measures like discretionary accruals, conservatism, and earnings smoothness is debatable even for public firms, the sparse data that private firms provide in their financials and their further aggregation by data vendors make their construct validity even more questionable. Only very rarely do private firms publish cash flow statements so that accruals have to be estimated based on balance sheet data. As many firms also do not publish income statements and line items in balance sheets are often highly aggregated, the measurement-induced noise in typical earnings attributes can be expected to be substantial. In addition, it is likely to be mechanically related to firm size (because of disclosure regulation) and voluntary disclosure incentives (as firms have substantial degrees of freedom on how aggregated to report their financial information). A potential way forward is to first revisit the economic construct that one aims to measure. Based on this, one can then construct measures that make good use of the financial accounting data that private firms provide while optimising construct validity. As an example: If one is interested in assessing the quality of financial reporting by private firms, it might be more insightful to study the reporting lag of private firms and the count of reported line items as well as the extensiveness of their notes disclosures than calculating discretionary accruals based on rudimentary balance sheet data (Clatworthy and Peel Citation2016). To inform such an approach it would also be important to explore the actual usage of private firm reporting information, e.g. by creditors, competitors, customers/suppliers, or tax authorities to understand which aspects of private firm reporting they actually value as useful. Survey studies and expert interviews could provide suitable methods.

3.4. Private firms: general research questions

Studies in this section use private firm data to address research questions that in substance equally apply to public and private firms and serve a dual purpose. First, they make statements about private firms and within private firm variation and therefore allow implicit comparisons to corresponding research on public firms to highlight differences between private and public firms similar to the studies presented in Section 3.3. Second, using private firm data often allows a cleaner setting to revisit established general research questions.

There are various reasons why a private firm setting might be desirable. For example, the absence of capital market incentives allow for a clearer analysis of other determinants of reporting behaviour (e.g. Kosi and Valentincic Citation2013). Another important aspect of the private firm setting is the role of regulation. Private firms sometimes allow clean identification due to regulatory settings that apply only to private firms (e.g. size-dependent disclosure rules in Breuer et al. Citation2018), or that are confined to countries with limited public markets (e.g. several studies on Belgian data such as Carcello et al. Citation2009). In a similar spirit, researchers can also exploit regulations that do not apply to private firms, either by using private firms as a within-country control group for affected public firms (e.g. Cascino and Gassen Citation2015), or by utilising within-private firm variation in voluntary compliance with rules that are mandatory for all public firms, such as voluntary audits in Lennox and Pittman (Citation2011), or bank-requested financial statement verification in Lisowsky et al. (Citation2017).

3.4.1. Disclosure of financial statements

The specific design and partial absence of rules mandating disclosure of financial statements make private firms an interesting laboratory to explore first-order incentives for and effects of public financial reporting. Chi et al. (Citation2013) exploit the fact that Taiwan rescinded mandatory financial reporting for private firms in 2001 to identify firms with high reporting incentives (which continued to voluntarily provide public financial statements) and firms with low reporting incentives (which ceased to report). They find that firms with high reporting incentives have better corporate governance practices and higher reporting quality in the pre-2001 era.

Dedman and Lennox (Citation2009) combine a survey with data from FAME for UK private firms that can choose to disclose abbreviated instead of full financial statements. They show that managers are more likely to withhold information when the perceived competition is high. In a similar vein, Bernard (Citation2016) uses a sample of German private firms that failed to disclose mandated public financial statements until fines for non-compliance were increased to a meaningful level and documents that disclosure was avoided by financially constrained firms in order to avoid product market predation by competitors. Bernard et al. (Citation2018) exploit size thresholds for mandated disclosures for European private firms. They find that firms with large proprietary costs are willing to sacrifice growth and profit to avoid disclosure and that the cost of disclosing an income statement is perceived as being similar to the cost of a mandatory audit. Lisowsky and Minnis (Citation2020) use confidential tax return data to provide large-sample evidence of accounting choices for U.S. private firms, and observe that standard explanations for financial reporting incentives (e.g. a primary focus on debt financing) are not conclusive in explaining firms’ observed reporting behaviour.

Regarding the consequences of public financial statements, Breuer et al. (Citation2018) also exploit discontinuous disclosure around size thresholds of German firms and show that mandated financial statements provide relevant information for banks, and that affected firms move from relationship lending towards arms-length banking relationships. Using U.S. data, Chen (Citation2019) finds that the mandated disclosure of private M&A target firms’ financial statements that exceed certain size thresholds disciplines management decisions and leads to more efficient M&A decisions, pointing at the role of public information in facilitating investor monitoring.

Finally, Shroff et al. (Citation2017) exploit that private firms in the U.S. do not have to issue public financial statements to explore the effect of peer information on a firms’ cost of capital. Private firms that issue public debt for the first time pay lower bond yields, and IPO firms display lower initial bid-ask spreads in industries with a richer public peer information environment. This effect phases out as more firm-specific information becomes available over time and suggests the spillover of peer information to less transparent firms.

3.4.2. Financial reporting characteristics and accounting quality

3.4.2.1. Earnings quality

In the absence of capital market regulation, Hope et al. (Citation2017) explore the determinants of accruals quality among a large sample of private U.S firms and find that it is driven by demand for informative financial reporting from non-managing shareholders, debtholders, and suppliers. Gassen and Fülbier (Citation2015) document that debt-agency incentives are associated with smoother earnings streams for European private firms and that this association is moderated by the country-level infrastructure of contract enforcement and bankruptcy regulation. Bigus and Häfele (Citation2018) look at shareholder loans as a specific source of funding common for private firms in Germany, and document that the dual stakeholder role of shareholders granting loans mitigates agency conflicts from excessive leverage and decreases earnings smoothing.

Regarding the consequences of accounting quality, using data from the World Bank’s Enterprise Survey, Chen et al. (Citation2011) document that accruals quality is associated with investment efficiency even for private firms from emerging countries, and in particular when they rely more on bank financing, but less so when incentives for tax avoidance prevail. De Meyere et al. (Citation2018) find for Belgian private firms that higher financial reporting quality facilitates access to long term debt financing, while in contrast, Mafrolla and D’Amico (Citation2017), using data from Italy, Portugal, and Spain suggest that firms engaging in earnings management have easier access to debt, yet also pay higher interest.

3.4.2.2. Conservatism and write-offs

Garrod et al. (Citation2008) and Kosi and Valentincic (Citation2013) study the role of tax incentives for aggressive write-offs using a large sample of private firms in Slovenia. Their sample allows to abstract from financial reporting incentives, as sample firms are less affected by agency conflicts and show high conformity between tax accounting and financial accounting. The results provide evidence that obtaining tax savings is an important objective for private firms’ financial reporting choices. For a sample of German private firms that are larger, and thus might have dispersed ownership and agency issues, Szczesny and Valentincic (Citation2013) document that private firms use more asset write-downs when they are more profitable (to build reserves), have higher leverage (because banks prefer conservative reporting) and pay dividends (because majority shareholders try to limit the pool of financial resources available for pay-outs). Haw et al. (Citation2014) find for a sample of Korean firms that private firms with public debt show a higher degree of conditional conservatism compared to private firms without such debt, in particular when they exhibit high information asymmetry and high credit risk.

3.4.3. Audit

Audit research likely represents the most developed stream of literature on private firms (see Vanstraelen and Schelleman (Citation2017) for an extensive overview). While public firms are generally mandated to have their financial statements audited, the lack of such regulation for certain private firms allows for a better identification of the determinants of demand for and the benefits of voluntary audits. A significant number of papers also revisit research questions on differences between Big N and other auditors in the private firm context.

3.4.3.1. Demand for voluntary audit engagements