?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This article studies whether nudges – that is, gentle alterations of people’s behaviour – increase audit quality. Although the utility of nudges is well-established in behavioural sciences, their applicability and efficacy have been less studied in accounting and auditing. To bridge this knowledge gap, the study extends nudge theory to financial audits, offering experimental evidence of the impact of social norms and justification nudges on auditor behaviour. A factorial 2 × 2 between-subject experiment (social norms and justification) shows that nudges amplify professional skepticism, a critical indicator of audit quality. A follow-up eye-tracking experiment involving an audit task identifies the underlying cognitive mechanism of this effect; nudges heighten auditors’ visual attention to pertinent information, thereby refining their evaluations of audit evidence and increasing their professional skepticism.

1. Introduction

Despite changes to regulatory frameworks designed to improve audit quality, regulators’ reporting shows that audit deficiencies – epitomised by auditing debacles such as WireCard and Carillio – remain (PCAOB Citation2022). Regulatory authorities often attribute such deficiencies to auditors’ insufficient professional skepticism. Skepticism thus seems crucial for ensuring audit quality (PCAOB Citation2018, Citation2023), and professional skepticism is needed in the auditing process.

There are many definitions of professional skepticism in academic research and professional standards. The International Auditing and Assurance Standards Board (IAASB) clearly defines it as ‘an attitude that includes a questioning mind, being alert to conditions which may indicate possible misstatement due to error or fraud, and a critical assessment of evidence.’ Professional skepticism is a multifaceted construct that includes both trait and state characteristics (Hurtt et al. Citation2013, Eutsler et al. Citation2018, Mohammad and Oczkowski Citation2021). Visual attention, as a type of heightened concentration, is one of its fundamental components. According to the eye–mind hypothesis, visual attention is a cardinal component in information processing (Just and Carpenter Citation1980, Rose et al. Citation2022). We propose that to bolster auditors’ assimilation of information, the use of nudges – that is, gentle alterations of behaviour – can amplify visual focus on critical aspects of decision-making. That is, nudges can enhance auditor performance and improve overall audit quality.

Nudges are elements in choice architectures that alter behaviour – such as by gently encouraging them to adopt responsible behaviours – without forbidding specific options or significantly changing the economic consequences (Thaler and Sunstein Citation2008). According to Schubert (Citation2017), the influence of nudges depends on agents’ cognitive biases. Through the design of choice environments, and usually with little expense, they attract attention to certain factors that incite people to make predictable decisions (Hilton et al. Citation2018). If a nudge fails, no harm results (Thaler and Sunstein Citation2008). Along with strategic prompts, decision aids (Kachelmeier and Messier Citation1990, Bowlin Citation2011), mindset manipulations (Griffith et al. Citation2015), and priming (Durkin et al. Citation2020), nudges improve auditors’ performance by using their personal heuristics and biases, subtly and without coercion (Thaler and Sunstein Citation2008). For this study, we investigate two debiasing nudges that might improve auditors’ professional skepticism: the social norms nudge and the justification nudge (Hilton Citation2001, Larrick Citation2004, Dolan et al. Citation2012).

Social norms make auditors aware of the need to practice accountability, objectivity, and integrity. Auditors’ fears of being reported for misconduct incite them to strengthen their professional skepticism and uncover misstatements resulting from error or fraud. Justification requires auditors to validate their critical judgments rationally and in an evidence-based manner, which reinforces their professional skepticism and ensures it is based on objective evidence and sound reasoning rather than biases, heuristics, or assumptions. We propose that together, social norms and justification contribute to auditors’ professional skepticism.

To test our predictions, we conduct an online experiment and a laboratory experiment. In the former, we establish that nudges exert strong effects on professional skepticism. In the latter, an eye-tracking experiment, we show the effect of nudges on professional skepticism is mediated by visual attention. Across the two experiments, we find that nudges positively affect professional skepticism, which we consider a marker of audit quality. Nudged conditions are associated with greater visual attention, measured as higher fixation counts and revisits to assessments of the audit evidence. The conditions also feature lower time-to-first fixation (TTFF), such that increased visual attention has a significantly positive impact on professional skepticism. As we demonstrate, nudges improve professional skepticism through the mediating effect of visual attention.

This evidence makes several contributions to auditing literature. First, amid a lack of research on the impact of nudges in auditing, we establish a foundation for novel research into how nudges can be used in the field of auditing. We go beyond work by Nolder et al. (Citation2022) to explore a mechanism that explains the effectiveness of nudges in auditing. Second, we add to rich literature pertaining to professional skepticism in auditing by providing a perspective on professional skepticism from a visual attention standpoint. We demonstrate that concepts and techniques from other disciplines such as psychology and neuroscience can be applied to improve the auditing practice. Third, from a managerial perspective, we highlight the need to identify the cognitive make-up of individual auditors, to personalise the choice architectures they encounter in their work interfaces and use nudges to encourage acceptable levels of professional skepticism. Fourth, we suggest that managers and partners in audit firms should be aware of how informal social norms in the professional environment affect the activities of audit firms. Overall, we submit that because audits require a great deal of concentration, there is an increasing need for applications of nudges to enhance the visual attention of auditors.

Our study is organised as follows: In Section 2, we review prior literature to frame and inform our hypotheses. In Section 3, we report the results of the online experiment, and in Section 4, we develop an eye-tracking experiment in the lab. Section 5 concludes.

2. Literature review and hypothesis development

2.1. Professional skepticism and aggressive reporting

Auditors make skeptical judgments when they recognise potential issues, thereby generating more work, review, or effort (Hurtt et al. Citation2013). For example, auditors likely are skeptical when they find evidence of aggressive financial reporting, so they devote more effort to investigation. Although some research assumes professional skepticism involves presumptive doubt or a conservatism bias (McMillan and White Citation1993, Nelson Citation2009), we characterise it differently, such that it implies that auditors require sufficient support and evidence in a timely manner (Hurtt Citation2010). The International Standards on Auditing require that audits be performed with professional skepticism (ISA Citation2016–2017). Following audit failures, regulators regularly cite a lack of professional skepticism (Ray Citation2015, Grenier Citation2017). In this sense, professional skepticism in audits is indispensable.

We define aggressive financial reporting as accounting practices that overstate company performance and fall outside generally accepted accounting principles (Johnstone et al. Citation2002). These practices might manifest as early revenue recognition, extensive cost capitalisation, lengthy amortisation periods, or understatement of expenses (AICPA Citation1988). Regardless of its form, the effects of aggressive financial accounting are devastating for firms, managers, and auditors. Feroz et al. (Citation1991) find that firms that engage in aggressive financial reporting likely underperform, suffer negative market returns following the announcement of accounting irregularities, and are subject to negative market perceptions and regulatory investigations. Moreover, auditors who miss such reporting can suffer sanctions such as monetary penalties and temporary or even permanent suspension of their licenses (De Fuentes et al. Citation2015).

To avoid these negative outcomes, auditors must have sufficient levels of professional skepticism. Our proposal that nudges can be used to encourage such skepticism is grounded in auto-motive theory (Bargh and Barndollar Citation1996), which states that the environment can directly activate a goal that becomes operative and guides cognitive processes in the environment.

2.2. Social norms nudge

Because people are fundamentally social in nature, they tend to organise their work activities in groups (Young Citation2008) that share social norms and understanding of what constitutes appropriate behaviour (Thogersen Citation2006). To avoid rejection, people conform with the values and norms of the groups to which they belong (Young Citation2013). To be influenced by social norms, people first must be part of a group and have a legitimate sense of attachment to it (Asch Citation1956, Cialdini et al. Citation1990). According to social identity theory, people group themselves with others according to their similarities (Tajfel Citation1978, Bauer Citation2015); they are more likely to internalise the group’s norms (Bamber and Iyer Citation2007) and develop a sense of who they are based on their group membership (Tajfel Citation1978).

Social norms also should exert cognitive impacts on auditors, who belong to professional groups and identify themselves accordingly. Most audits are performed by teams of auditors, who pool their knowledge and expertise to undertake audit tasks. The group as a whole should influence each individual auditor, either consciously or unconsciously, willingly or unwillingly. Because most audit teams also adopt hierarchical structures, influence can be vertical or horizontal. Although audit teams assemble to meet the particular needs of projects, resource-based theory (Gardner et al. Citation2012) acknowledges that firms can be defined by the resources they control (Litz Citation1996). The distinct human resources available to audit firms could lead to unique social norms being developed and applied across firms or their teams. Moreover, many auditors join professional bodies, such as the American Accounting Association, American Institute of Certified Public Accountants, and the Association of Chartered Certified Accountants, that can be sources of influence.

Across these settings, social norms should lead to compliance and conformity. For example, Bobek et al. (Citation2007) find that social norms affect tax compliance, and Kelly and Murphy (Citation2021) show that they influence decisions related to aggressive accounting. According to Blay et al. (Citation2019), social norms that prioritise honesty and responsibility can capture auditors’ potential for moral reasoning. Callen and Xiaohua (Citation2020) show that firms located in U.S. counties with more liberal local gambling norms exhibit higher audit fees. According to Westermann et al. (Citation2015), during the early years of their professional careers, auditors undergo a process of professional socialisation and learn the social norms of their employing firms. Cardinaels and Jia (Citation2016) determine that social norms have strong effects on the level of truthful reporting when reporting decisions are audited.

Evidence of the impact of social norms on accounting and auditing is diverse, and the mechanism by which social norms function is controversial. According to Dolan et al. (Citation2012), normative influences are partly conscious and deliberate and partly unconscious, because of the lack of awareness or rationality among people engaged in conformist behaviour. Young (Citation2013) asserts that social norms work through a heuristic process similar to herding, but they also might involve a more elaborate cognitive process, mediated by persuasiveness. Melnyk et al. (Citation2011) add that people who are cognitively invested in the process of understanding social norms are less susceptible to their influence, and Bauer (Citation2015) finds that professional identity, which is a construct similar to social norms, can improve professional skepticism in auditors.

Peer groups influence social norm conformity (Cialdini et al. Citation1999, Cialdini and Goldstein Citation2004); peer group research indicates that age group (Asirvatham et al. Citation2014, Qin et al. Citation2022) and profession (Drake and Martin Citation2020, Ruiz and Sirvent Citation2022) are important drivers of conformity. They work due to individual affiliation goals and positive self-maintenance goals (Cialdini and Goldstein Citation2004). Wetmiller (Citation2022) finds that staff auditors with peer team members who engage in dysfunctional audit behaviour (DAB) are more likely to engage in DAB. Because staff auditors are new to the teams and are trying to learn appropriate courses of action from others, they are more likely to be influenced by peers. Therefore, we predict that participants will find a nudge most compelling if it suggests that skepticism is a norm among their age- and profession-based peers:

H1a: Implementation of a social norms nudge increases auditors’ professional skepticism.

2.3. Justification nudge

Because justification techniques require people to offer reasoned explanations for their choices (Hilton Citation2001), they should prompt more careful analysis and less reliance on cognitive shortcuts. Authors refer to justification as accountability or reasoned-based choice (Buchman et al. Citation1996, Lerner and Tetlock Citation1999, Hilton Citation2001, Geoffroy and Eliaz Citation2012, Dalla Via et al. Citation2019) that might be internal and related only to the self or else external and involve other people (Simonson Citation1989). Because optimal decision-making generally entails complex processes, accounting for systematic reasoning in audits should be beneficial.

When auditors execute audits, they make various decisions, individually or collectively, that reflect various criteria. Even in the presence of rules, guidelines, or best practices to aid the decision-making process, people must take multiple dimensions into consideration. The dilemma regarding how much to trade one dimension against another is difficult to resolve. Therefore, people often resort to simple heuristics (Geoffroy and Eliaz Citation2012). The need to justify prevents such shortcuts.

Kramer et al. (Citation1993) cite an impressive body of empirical evidence that justification improves decision-making behaviour. For example, Pilkington and Parker-Jones (Citation1996) show that trainee doctors learn more when they have to offer justifications, and Misra et al. (Citation2019) indicate that the need to justify leads tax consultants to perform deeper searches. Moreover, according to Tetlock and Boettger (Citation1989), people adjust their opinions to reflect the views of a source of justification, and Lord (Citation1992) finds that auditors who are subject to justification demands, compared with those who are not, issue more qualified opinions.

Decision makers can use various means to justify their decisions, and the sources they select are likely to influence their decisions, due to differences in their levels of clarity, pressure, or preference (Bagley Citation2010). Seta et al. (Citation1989) caution that the use of multiple justifications in auditing can cause negative emotions that harm task performance in low-complexity, but not high-complexity, audits.

For a justification nudge to increase the level of professional skepticism, it should include three elements. First, it should engage people to offer reasoned explanations of their choices (Geoffroy and Eliaz Citation2012) and prompt them to practice more careful analysis and rely less on cognitive shortcuts (Kennedy Citation1993, Hilton Citation2001). Second, the source of the justification should be clear and well known for its advocacy of professional skepticism (e.g. regulators or top hierarchy). Bagley (Citation2010) finds that the source of justification influences the decisions made. Third, the nudge should contain pertinent information that encourages auditors to make the right decisions (Thaler and Sunstein Citation2008). This element encompasses the first two elements and provides further clarification of what is expected of auditors in the particular contexts in which they find themselves. We hypothesise:

H1b: Implementation of a justification nudge increases auditors’ professional skepticism.

2.4. Nudges and visual attention

Attention is the cognitive process of selectively focusing on one aspect of the environment while ignoring other elements (Posner Citation2012). The attentional process involves a set of cognitive operations that enable processing of relevant information while filtering out non-essential stimuli. Eye–mind theory posits that human information processing is contingent on eye fixations (Just and Carpenter Citation1980), so fixations can gauge visual attention (Rose et al. Citation2022). Increased information processing requires more fixations (Just and Carpenter Citation1980).

Nudges serve as subtle cues or changes in how choices are presented that can unconsciously direct attention toward certain elements. By enhancing visual attention, nudges can improve decision-making quality. For example, in the automobile industry, nudges enhance drivers’ focus on road conditions and safety parameters (Dwoskin and Ramsey Citation2016). On the basis of such insights, we predict:

H2a: Implementation of a social norms nudge increases the levels of auditors’ visual attention.

H2b: Implementation of a justification nudge increases the levels of auditors’ visual attention.

Diminished visual attention to a focal target could denote distraction (Büttner et al. Citation2014) and reduced capacities to concentrate or conduct high-quality audits (Breger and Edmonds Citation2016), which may mean diminished professional skepticism (Glover and Prawitt Citation2014). Distraction, as indicated by increased fixations on diverse stimuli, could suggest inefficient pursuit of target information (McMillan and White Citation1993, Holmqvist et al. Citation2011). In contrast, financial auditors who display high levels of professional skepticism often exhibit elevated degrees of information search (Robinson et al. Citation2018). The theoretical foundation for these empirical findings is the concept of covert attention, as proposed by Posner and Petersen (Citation1990). Covert attention encompasses three core abilities:

Capacity to orient and reorient attention,

Readiness to anticipate and remain alert for forthcoming events, and

Ability to manage attention.

To encourage more professional skepticism, nudges therefore should fulfil three functions: guide auditors to concentrate on the tasks at hand, encourage them to maintain alertness while evaluating audit evidence, and help them control their attention. According to Collings and Eaton (Citation2019), covert-attention orienting and oculomotor control are interdependent systems that select specific targets and steer saccades (Awh et al. Citation2006, MacLean et al. Citation2015). Oculomotor movements can be monitored using eye-tracking methodologies. Therefore, combining this evidence, we predict:

H3: The positive effect of nudges on auditors’ professional skepticism is mediated by visual attention.

To test these hypotheses, we conducted two experiments: an online experiment and an in-depth, eye-tracking laboratory study, designed to uncover the underlying attentional mechanisms of the predicted processes.

3. Online experiment

3.1. Methods

3.1.1. Participants

We recruited 100 young professional auditors from France, with an average age of 23 years, 44% of whom were women. Following Hauser and Schwarz’s (Citation2016) recommendations, we included attention checks to ensure their attention during the experiment.

shows that all participants had master’s degrees with specialisations in accounting and auditing. All participants had work experience of three months to one year in the field of auditing. Because the experiment involved humans, we received approval from the institution at which the experiment took place (Comité d’Ethique de la Recherche, HEC Montréal, 2020-3791–186 – Largo Winch). Participants received a fixed renumeration fee of €10, to prevent the money from influencing their skepticism.

Table 1. Socio-demographic information of participants.

3.1.2. Experimental design

To test our hypotheses, we conducted a fully randomised experiment using a 2 × 2 between-subject design. Participants were presented with pieces of audit evidence and assigned to one of four experimental conditions: control (C), social norms nudge (S), justification nudge (J), and social norms and justification (SJ). The text of the social norms nudge was

Very important Information: A recent study in accounting indicates that individuals of your age perform very well on audits. The study explains that this is the case because individuals of this age range pay a great deal of attention to detail and take note of evidence of aggressive financial reporting when conducting audits.

Very Important Information: Audits are scrutinized by your superiors and the regulators. In similar audit tasks, some auditors have recently been sanctioned for not being able to identify items indicative of aggressive financial reporting. Imagine for this exercise that you will be accounting personally for your audit opinion to the top hierarchy and possibly the regulators.

We measured professional skepticism, our dependent variable, by asking: ‘Please evaluate the client’s financial reporting as a whole,’ followed by a description of aggressive financial accounting practices (cf. A.1.5). Participants answered on a 10-point scale ranging from ‘not aggressive at all’ to ‘very aggressive.’ In line with previous research (Bamber and Bylinski Citation1987, Cohen and Kida Citation1989, Bauer Citation2015), we used higher response scores as proxies for skepticism.

3.1.3. Materials

The audit evidence material we used was based on two well-known cases of aggressive financial reporting: Trueblood Case 91-1 (Touche Citation1991) and United States Surgical Corporation (Johnson et al. Citation1993). We developed 14 items of evidence that captured the key features of each client’s financial statements, with each item self-contained and able to be analyzed independently. Of the 14 items, three were indicative of aggressive financial reporting (trade receivables, shareholders’ equity, accounts payable and accrued liabilities), one served as an attention check, and the remaining 10 items were indicative of non-aggressive financial reporting. We adapted this approach to constructing audit evidence material from Phillips (Citation1999).

3.1.4. Manipulation checks

To verify that the nudges manipulated the intended concepts, we submitted our materials to a sample of 40 auditing professionals whom we recruited online. We asked if they agreed that the text of each nudge was effectively evoking the underlying concept we intended to manipulate (social norms and justification). We also asked them to judge two filler items. For each concept, participants chose their level of agreement with the concepts on a scale of 1 (‘not at all’) to 7 (‘completely’). Participants correctly indicated higher levels of agreement with the concept associated with the nudge to which they were exposed, compared with the other options. Answers for the social norms nudge averaged 4.17, well above the midpoint response and significantly higher than the filler items (t = 2.02; p = 0.05). Answers for the justification nudge averaged 5.13, again well above the midpoint response and significantly higher than the filler items (t = 2.63; p = 0.01).

We took the manipulation check approach from Oppenheinmer et al. (Citation2009). It provides an indirect measure of satisficing and is well suited to our experiment, in that the materials are relatively basic and it reflects the level of expertise of participants.

3.1.5. Procedure

Participants accessed an online experiment through a link. Prior to participating, they were required to read and accept the terms and conditions. They were then presented with instructions for an exercise that involved reviewing, at their own pace, audit evidence about a fictitious company. Background information about the company and the audit, including the level of materiality and the accounting year, was provided before participants proceeded with the exercise. After participants read the instructions and background information, they were randomly assigned to one of four experimental conditions. During the audit task, they carefully examined 14 pieces of audit evidence and provided a general assessment of the level of financial reporting on a scale from 1 (‘not aggressive at all’) to 10 (‘very aggressive’). Participants also provided demographic data. Please refer to Appendix A.1.4 for more details on the audit task instructions and Appendix A.1.5 for the financial reporting scale used.

3.2. Results

3.2.1. Effect of nudges on professional skepticism

The average duration of the experiment was 36 min. We employed a 2 × 2 between-subject analysis of variance (ANOVA) to examine the impact of the social norms nudge (S) and the justification nudge (J) on professional skepticism. presents descriptive statistics for each condition.

Table 2. Descriptive statistics by nudge condition.

The ANOVA revealed a significant effect of the nudges on professional skepticism, F(3, 81) = 2.4, p = 0.07. That is, the nudges influenced professional skepticism at a 10% significance level. Specifically, the combined nudge condition (SJ) exhibited the highest mean level of professional skepticism (M = 7.19, standard deviation [SD] = 1.33), followed by the social norms nudge (S: M = 6.50, SD = 1.36), the control (C: M = 6.43, SD = 1.71), and the justification nudge (J: M = 6.20, SD = 1.80).

Tukey HSD post hoc comparisons in show that the mean score for the double nudge condition (SJ) differed significantly from the no-nudge control condition. However, neither the social nudge nor the justification condition differed significantly from the control condition. We therefore offer some evidence in support of H1a and H1b. The social norm nudge and the justification nudge can increase professional skepticism, but only if they are used together.

Table 3. Post-hoc comparisons of skepticism under the nudge versus control condition.

To consolidate our findings and gain a deeper understanding of the underlying mechanisms of the observed effects of nudges, we conducted a second experiment in a laboratory setting, using eye-tracking technology during the audit task. This approach allowed us to identify the attentional mechanisms involved by observing how auditors responded to nudges during their audit tasks. It also addressed the limitation of declarative measures and used a more objective measure of skepticism based on the detection of aggressive financial reporting elements. By combining these objective measures with eye-tracking data, we aimed to provide a more precise understanding of the mechanisms underlying the effects of nudges on skepticism.

The results of the online experiment presented limitations that we addressed in the lab experiment. Because of the subjective nature of the skepticism measure (see also Griffith et al. Citation2015, Nolder et al. Citation2022), it might have been difficult to establish a normative reference point. Arguably, higher scores might not necessarily indicate higher professional skepticism. However, the baseline we used to measure the effectiveness of the nudges was the control condition, which should be a normative reference point. Moreover, this measure of professional skepticism appeared appropriate, because we gathered it online, making it impossible to supervise participants.

4. Eye-tracking lab experiment

4.1. Methods

4.1.1. Participants

Participants in the lab experiment were young auditing professionals, with varying levels of work experience, based in Canada. Of the 20 participants, 70% were women (). Because the experiment involved humans, we received approval from the institution where the experiment took place (Comité d’Ethique de la Recherche, HEC Montréal, 2020-3791 – 186 – Largo Winch). All participants had master’s degrees with specialisations in accounting and auditing, and all had work experience of three months to one year in the field of auditing. Participants received a fixed fee of $30 CDN. The use of a fixed fee for all participants prevented the money from having an influence.

4.1.2. Experimental design

As in the online experiment, the participants examined pieces of audit evidence, but the experimental design differed somewhat. We used a 2 × 2, within-subject design in a controlled laboratory setting. To avoid cross-contamination of the nudges, we use a semi-randomised design. We presented the control condition with no nudge first, followed by three manipulations: the social norms nudge, the justification nudge. and a combined nudge, randomised for each participant. All participants saw the control condition before being exposed to the nudge conditions. Appendix A.1.3 presents the manipulation conditions.

4.1.3. Materials

The materials are the same as those detailed for the online experiment, with two changes. The audit task still consisted of 14 pieces of evidence, three of which represented cases of aggressive financial reporting (Task A: Fixed Assets, R&D and Engineering Expenses, Intangible and Other Assets; Task B: Inventories, Cost of Goods Sold, Sales; Task C: Trade receivables, Shareholders’ Equity, Accounts Payable and Accrued Liabilities; Task D: Inventories, Fixed Assets, Marketing and Administration Expenses) and 11 of which represented non-aggressive financial reporting. The texts used for the social norms and justification nudge were the same as in the online experiment. However, we adopted a behavioural measure of professional skepticism instead of the declarative measure. In line with Glover and Prawitt (Citation2014) and Nelson (Citation2009), we asked participants to detect aggressive items in the audit task.

As a second change, we measured visual attention during the experiment using eye-tracking technology (Red 250, SensoMotoric Instruments GmbH, Teltow, Germany). We defined areas of interest (AOIs) corresponding to each piece of evidence. The eye-tracking technology tracked eye movements and changes in pupil size at specific points in time (Lynch and Andiola Citation2019, Manzon Citation2020) in relation to the AOIs. The resulting data provided measures of various constructs, including processing levels, mental states, and perceptual fluency (Wedel and Pieters Citation2008, Holmqvist et al. Citation2011, Lynch and Andiola Citation2019, Meissner and Oll Citation2019), each of which helped reveal participants’ cognitive processes.

We recorded measures at a sampling frequency of 60 Hz throughout the experiment. Fourteen AOIs were placed on the page, reflecting the 14 financial account items. Because items on the page were randomised, the AOIs varied across participants and attempts. Prior to each session, participants underwent a calibration process using a 9-point predefined calibration grid (Just and Carpenter Citation1976) to ensure an average deviation of no more than 0.5. The use of eye-tracking technology and AOIs allowed us to capture participants’ visual attention to specific aspects of the financial account items precisely.

To quantify participants’ visual attention during the audit task, we used a ratio of dwell time to revisits. Dwell time is the total viewing time of the areas of interest (AOIs), and revisits are the number of times the participant returned to those AOIs. With this ratio, we can consider both time and count metrics (Yusuf et al. Citation2007, Lynch and Andiola Citation2019). By measuring time spent viewing an AOI and the frequency with which the AOI was revisited, we capture the dynamics of participants’ visual attention during the audit task.

4.1.4. Procedure

Each participant inspected a series of four sets of 14 items of audit evidence, reflecting 14 distinct accounts in the financial statements. To prepare participants and mitigate learning effects, each series started with a short presentation of the company in question, as well as basic information needed for the audit, such as materiality and the audit year. After examining all 14 pieces of audit evidence for the first series at their own pace, participants moved to the next page to identify financial reporting items they adjudged aggressive (see Appendices A.2.4 and A.2.5). To mitigate any effect of prior knowledge of the business or anchoring effects, the four descriptions featured different fictitious businesses. We also obtained demographic data for control purposes and renumerated the participants.

4.1.5. Variables

We measured the dependent variable, professional skepticism, by the total number of aggressive items detected (from 0 to 3). The independent variables were the social norms and justification nudge conditions. To account for visual attention, we included the dwell-to-revisit ratio from the eye-tracking measures as a mediating variable, reflecting both the fixation count and the time elapsed between two revisits of an AOI (Doherty et al. Citation2010, Hofmaenner et al. Citation2021). As we noted previously, the dwell-to-revisits ratio captured the average time elapsed between two revisits of an AOI and also the average time the participant took to return to an AOI. The shorter the time, the greater the participant’s concentration on an AOI, and the stronger the visual attention.

4.2. Results

4.2.1. Effect of nudges on skepticism

The average duration of the experiment was 41 min. To consolidate the findings from the online experiment, in the lab experiment we conducted a one-tailed t-test to evaluate the effects of the social norms nudge and the justification nudge on professional skepticism. Results showed a significant increase of professional skepticism in the nudged conditions (M = 1.4, SD = 1.06) compared with the control condition (M = 0.93, SD = 0.8) at the 5% level, t(39) = 1.72, p = 0.04. Thus, we can confirm the effectiveness of nudges when we used a behavioural measure of skepticism and a Canadian sample, rather than the declarative measure of skepticism and French sample in the online experiment.

4.2.2. Nudges and visual attention

Descriptive statistics in indicate increased skepticism and decreased dwell-to-revisits for all nudged conditions. For the test of H2a and H2b, we used linear regression with a random intercept model of the dwell-to-revisits ratio to consider whether nudges significantly affected visual attention.

Table 4. Descriptive statistics for experiment 2.

Consistent with our hypothesis, the results in reveal that after being nudged, the auditors exhibited better visual attention to their audit tasks. Compared with the no-nudge condition, all nudged conditions produced significantly lower dwell-to-revisits ratios: social norms nudge condition (p = 0.02), justification nudge condition (p < 0.01), and combined nudge (p = 0.01). Nudged participants, compared with non-nudged participants, returned more quickly to AOIs. As previously mentioned, the ratio expresses the time elapsed between two revisits, or the time a participant took before returning to an AOI; the shorter the time, the greater the auditor’s concentration on an AOI.Footnote1

Table 5. Effect of social norms and justification nudges on visual attention.

To verify the robustness of our findings, we analyzed three more eye-tracking measures: fixation counts, revisits, and time-to-first fixation (TTFF). The metrics used in the robustness checks applied to all AOIs. We included fixation counts (M = 16.81, SD = 14.04) and revisits (M = 3.98, SD = 3.40) in negative binomial regression models, because both were counts and overdispersed. We included TTFF in the linear regression with a random intercept.

The nudges affected TTFF. Compared with the no-nudge condition, all nudged conditions led to significantly lower TTFF: social norms nudge (p = 0.01), justification nudge (p < 0.01), and combined nudge (p = 0.01). Therefore, in nudged conditions, less time elapsed before the participants fixated on audit items, which we can interpret as an efficient use of time, because the time is maximised for fixations. Furthermore, we observed higher fixation counts when audit tasks followed nudges: social norms nudge (p = 0.01), justification nudge (p < 0.01), and combined nudge (p = 0.01), compared with the no-nudge condition. This result also was corroborated by the revisits metric. Compared with the no-nudge condition, all nudged conditions prompted significantly more revisits: social norms nudge (p = 0.01), justification nudge (p < 0.01), and combined nudge (p = 0.01).

Overall, our findings imply that in the presence of nudges, auditors focus more visual attention on elements they examine during audit tasks. This outcome is very important; heightened visual attention to audit items should reduce the possibility that an auditor might miss key details that determine the quality of a report. Moreover, after initially examining all elements initially, the auditors reexamined them, which is an important way to build a general picture of an audit.

4.2.3. Mediating effect of visual attention on professional skepticism

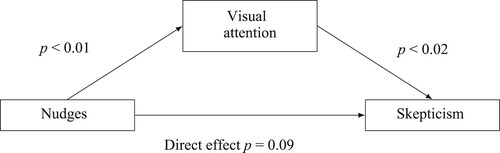

After observing that nudges increase visual attention, we examined whether increased visual attention mediated the link between nudges and professional skepticism. In H3, we predicted that the positive effect of nudges on professional skepticism would be mediated by visual attention. To test this mediating effect, we used Baron and Kenny’s (Citation1986) statistical approach. With a path analysis, we determine whether visual attention mediated, at least in part, the effect of nudges on professional skepticism. Then, in accordance with Kenny et al. (Citation1998), we estimated path coefficients (standardised beta weights) using regression analyses. As shown in , the paths from nudges to visual attention () and from visual attention to professional skepticism () both were significant. The direct path from nudge to professional skepticism (after partialling out the effect of visual attention) remained significant (). Overall, the path analysis confirmed that visual attention acted as a mediator of the nudges.

Figure 1. Path model of mediation of the effect of nudges on skepticism through visual attention.

Table 6. Path of visual attention (dwell-to-revisits) to professional skepticism.

Table 7. Direct path of nudge to skepticism.

As reported in , nudges increased visual attention, such that the TTFF and dwell-to-revisit ratio both decreased when auditors viewed nudges. The fixation count and number of revisits also seemed to increase when participants were nudged. Although these relationships were coherent, the significant effects of mediation were limited to the dwell-to-revisits ratio. and show that the auditors exhibited greater professional skepticism when they were nudged, seemingly because they devoted more visual attention to the audit task.

5. Summary and conclusion

In this study, we evaluate the impacts of nudges on financial auditors’ professional skepticism. We focus on how a social norms nudge, a justification nudge, and a combination of those nudges influence professional skepticism. The results consistently indicate that nudges enhance the visual attention – and thus the professional skepticism – of auditors.

Our study extends accounting literature, especially as it relates to professional skepticism, by detailing how nudges improve audit quality. Although nudge theory is popular and extensively applied in economics and finance, we find few parallel applications in behavioural auditing settings. In addition to showing that social norms and justification nudges help increase professional skepticism, our study identifies visual attention as the mechanism through which this improvement occurs.

Our finding of the role of visual attention substantiates our prediction based on covert attention theory (Posner and Petersen Citation1990). The theory emphasises the crucial functions of orienting and reorienting attention, remaining alert for impending events, and controlling attention – all of which the implemented nudges appeared to fulfil. Auditors can maintain focused attention, remain vigilant while examining audit evidence, and effectively manage their attention, thereby reducing distraction and enhancing professional skepticism. The finding could be related to the notion that humans process information with eye fixations (Just and Carpenter Citation1980), and more fixations due to nudges amplifies information processing. In this context, our results reflect Mrkva et al.’s (Citation2019) finding that the degree of visual attention varies among auditors. The finding is corroborated by research on oculomotor control (Awh et al. Citation2006, MacLean et al. Citation2015) and research that shows financial auditors with high levels of professional skepticism exhibit higher degrees of information search (Robinson et al. Citation2018). Our results contribute to this body of literature by identifying the mechanism by which nudges enhance auditors’ professional skepticism.

Evidence of the importance of social norms corroborates the professional identity construct proposed by Bauer (Citation2015). The evidence that justification nudges increase professional skepticism confirms claims by Misra et al. (Citation2019), but in the different context of auditing. A possible interpretation of the effect is provided by the economics of convention (Boltanski and Thévenot Citation1987, Thévenot and Boltanski Citation1991), which refer to a system of reciprocal behavioural expectations between people. Auditors who justify their behaviours generate expectations from others, thereby affecting the auditors’ own professional skepticism. Because others are now more demanding of the auditors’ behaviours, the auditors try to meet those demands by becoming increasingly skeptical.

Our study has some limitations. Although our sample includes Canadian and French participants, offering some variation across the experiments, the findings might not hold for auditors with different cultural values. Reactions to nudges tend to vary across cultures (Loibl et al. Citation2018, Pe’er et al. Citation2019). The effects of nudges we observed might not be completely generalisable. Another limitation pertains to the nature of the experimental instrument; though it is firmly grounded in real-life occurrences, its simplification and abstract nature also may constrain generalizability. Furthermore, though our participants reviewed the evidence provided, they were not able to search freely for other evidence (Phillips Citation1999), nor could they interact with clients, which might have affected their levels of skepticism. Finally, there are other approaches to measuring skepticism (Choo Citation2000, Shaub and Lawrence Citation2002, Nelson Citation2009, Robinson et al. Citation2018).

Nevertheless, our results have practical implications. It is important for auditors to know that visual attention mediates the effect of nudges. This finding helps them understand how nudges affect their behaviour. By understanding that nudges influence their visual attention, they can become more aware of their bias and take steps to mitigate it. Auditors also can personalise the choice architectures available through their user interfaces, using nudges to help achieve acceptable levels of professional skepticism. Our findings can inform the design of nudges that orient visual attention to important information, which should increase professional skepticism and improve decision-making.

Finally, we note some opportunities for further research. Recognising the importance of heuristics and cognitive biases to nudge theory (Thaler and Sunstein Citation2008, Sunstein Citation2015), we recommend tests to examine which cognitive biases are influenced by nudges and how they subsequently influence professional skepticism. Audit researchers could explore the visual attention characteristics associated with auditors who appear to be subject to cognitive biases.

Supplemental Material

Download PDF (3 MB)Acknowledgements

This research was funded in whole or in part by the National Research Agency (ANR) under the project ANR-21-CE26-0012-01. The authors thank Tech3Lab, HEC Montreal for their technical support of this project. They also express their profound gratitude to researchers who provided feedback at various conference presentations (European Accounting Association 2022 (Bergen), Francophon Accounting Association 2022 (Bordeaux), French Finance Association 2022 (Saint-Malo), EIASM 2022 (Milan), JIRF 2022 (Lyon)) and research seminars (Lyon, Dijon). Special thanks to Sabri Boubaker, Shang Lin Chen and Yves Rannou for their comments. The auditing professionals who took part in the experiments also are acknowledged for their contributions.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes

1 We chose to combine all AOIs into a mean dwell-to-revisit ratio per condition, independent of their aggressiveness. This mean value was a composite score that reflected broad patterns of visual attention, which aligns with our research objective to study the effect of nudges on general behavioral trends rather than the nuanced differences between individual AOIs.

References

- AICPA, 1988. Statement on auditing standards no. 53: the auditor’s responsibility to detect and report errors and irregularities. American Institute of Certified Public Accountants New York: AICPA.

- Asch, S.E., 1956. Studies of independence and conformity: I. A minority of one against a unanimous majority. Psychological Monographs: General and Applied, 70 (9), 1–70.

- Asirvatham, J., Nayga, R.M., and Thomsen, M.R., 2014. Peer-effects in obesity among public elementary school children: A grade-level analysis. Applied Economic Perspectives & Policy, 36 (3), 438–459.

- Awh, E., Armstrong, K.M., and Moore, T., 2006. Visual and oculomotor selection: links, causes and implications for spatial attention. Trends in Cognitive Sciences, 10, 124–130.

- Bagley, P.L., 2010. Negative affect: a consequence of multiple accountabilities in auditing. Auditing: A Journal of Practice & Theory, 29 (2), 141–157.

- Bamber, E.M., and Bylinski, J.H., 1987. The effects of the planning memorandum, time pressure and individual auditor characteristics on audit managers’ review time judgments. Contemporary Accounting Research, 4 (1), 127–143.

- Bamber, E.M., and Iyer, V.M., 2007. Auditors’ identification with their clients and its effect on auditors’ objectivity. Auditing: A Journal of Practice & Theory, 26 (2), 1–24.

- Bargh, J.A., and Barndollar, K., 1996. Automaticity in action: the unconscious as repository of chronic goals and motives. In: P.M. Gollwitzer and J.A. Bargh, eds. The Psychology of Action: Linking Cognition and Motivation to Behavior. New York, NY: Guilford Press, 457–481.

- Baron, R.M., and Kenny, D.A., 1986. The moderator-mediator variable distinction in social psychological research: conceptual, strategic, and statistical considerations. Journal of Personality and Social Psychology, 51 (6), 1173–1182.

- Bauer, T.D., 2015. The effects of client identity strength and professional identity salience on auditor judgments. The Accounting Review, 90 (1), 95–114.

- Blay, A.D., Gooden, E.S., Mellon, M.J., and Stevens, D.E., 2019. Can social norm activation improve audit quality? Evidence from an experimental audit market. Journal of Business Ethics, 156 (2), 513–530.

- Bobek, D.D., Roberts, R.W., and Sweeney, J.T., 2007. The social norms of tax compliance: evidence from Australia, Singapore, and the United States. Journal of Business Ethics, 74 (1), 49–64.

- Boltanski, L., and Thévenot, L., 1987. Centre d'études de l'emploi (Paris). Programme de recherche et d'opérationalisation sur les topiques de l'équité et de l'équivalence. Les économies de la grandeur. Paris: Presses Universitaires de France.

- Bowlin, K., 2011. Risk-based auditing, strategic prompts, and auditor sensitivity to the strategic risk of fraud. The Accounting Review, 86 (4), 1231–1253.

- Breger, D., and Edmonds, M., 2016. The impact of audit room noise on audit quality: a theoretical inquiry. The Journal of Theoretical Accounting Research, 11 (2), 78–93.

- Buchman, T.A., Tetlock, P.E., and Reed, R.O., 1996. Accountability and auditor’s judgments about contingent events. Journal of Business Finance & Accounting, 23 (3), 379–398.

- Büttner, O.B., Florack, A., Leder, H., Paul, M.A., Serfas, B.G., and Schulz, A.M., 2014. Hard to ignore: impulsive buyers show an attentional bias in shopping situations. Social Psychological and Personality Science, 5 (3), 343–351.

- Callen, J.L., and Xiaohua, F., 2020. Local gambling norms and audit pricing. Journal of Business Ethics, 164 (1), 151–173.

- Cardinaels, E., and Jia, Y., 2016. How audits moderate the effects of incentives and peer behavior on misreporting. European Accounting Review, 25 (1), 183–204.

- Choo, F., 2000. Instruction, skepticism, and accounting students’ ability to detect frauds. Journal of Business Education, 1, 72–87.

- Cialdini, R.B., and Goldstein, N.J., 2004. Social influence: compliance and conformity. Annual Review of Psychology, 55, 591–621.

- Cialdini, R.B., Reno, R.R., and Kallgren, C.A., 1990. A focus theory of normative conduct: recycling the concept of norms to reduce littering in public places. Journal of Personality and Social Psychology, 58 (6), 1015–1026.

- Cialdini, R.B., Wosinska, W., Barrett, D.W., Butner, J., and Gornik-Durose, M., 1999. Compliance with a request in two cultures: the differential influence of social proof and commitment/ consistency on collectivists and individualists. Personality and Social Psychology Bulletin, 25, 1242–1253.

- Cohen, J., and Kida, T., 1989. The impact of analytical review results, internal control reliability, and experience on auditors’ use of analytical review. Journal of Accounting Research, 27 (2), 263–276.

- Collings, R.D., and Eaton, L.G., 2019. Covert attention, temperament, and looking: a novel approach to studying attention in the social world. Psychological Reports, 122 (6), 2220–2241.

- Dalla Via, N., Perego, P., and Van Rinsum, M., 2019. How accountability type influences information search processes and decision quality. Accounting, Organizations and Society, 75, 79–91.

- De Fuentes, C., Illueca, M., and Pucheta-Martinez, M., 2015. External investigations and disciplinary sanctions against auditors: the impact on audit quality. Journal of the Spanish Economic Association SERIEs, 6 (3), 313–347.

- Doherty, S., O’Brien, S., and Carl, M., 2010. Eye tracking as an MT evaluation technique. Machine Translation, 24, 1–13.

- Dolan, P., Hallsworth, M., Halpern, D., King, D., Metcalfe, R., and Vlaev, I., 2012. Influencing behaviour: the mindspace way. Journal of Economic Psychology, 33 (1), 264–277.

- Drake, K.D., and Martin, M.A., 2020. Implementing relative performance evaluation: the role of life cycle peers. Journal of Management Accounting Research, 32 (2), 107–135.

- Durkin, M.P., Rose, J.M., and Thibodeau, J.C., 2020. Can simple metaphors be used as decision aids to promote professional skepticism? Journal of Information Systems, 34 (1), 47–60.

- Dwoskin, E., and Ramsey, M., 2016. Car makers test technology to make you pay attention to the road. The Wall Street Journal, March 11, 2016.

- Eutsler, J., Norris, A.E., and Trompeter, G.M., 2018. A live simulation-based investigation: interactions with clients and their effect on audit judgment and professional skepticism. Auditing: A Journal of Practice & Theory, 37 (3), 145–162.

- Feroz, E.H., Park, K., Pastena, V.S., DeFond, M.L., and Smith, D.B., 1991. The financial and market effects of the SEC’s accounting and auditing enforcement releases; discussion. Journal of Accounting Research, 29, 107–142.

- Gardner, H.K., Gino, F., and Staats, B.R., 2012. Dynamically integrating knowledge in teams: transforming resources into performance. Academy of Management Journal, 55 (4), 998–1022.

- Geoffroy, D.C., and Eliaz, K., 2012. Reason-based choice: a bargaining rationale for the attraction and compromise effects. Theoretical Economics, 7 (1), 125–162.

- Glover, S.M., and Prawitt, D.F., 2014. Enhancing auditor professional skepticism: the professional skepticism continuum. Current Issues in Auditing, 8 (2), 1–10.

- Grenier, J.H., 2017. Encouraging professional skepticism in the industry specialization era. Journal of Business Ethics, 142 (2), 241–256.

- Griffith, E.E., Hammersley, J.S., Kadous, K., and Young, D., 2015. Auditor mindsets and audits of complex estimates. Journal of Accounting Research, 53 (1), 49–77.

- Hauser, D.J., and Schwarz, N., 2016. Attentive Turkers: Mturk participants perform better on online attention checks than do subject pool participants. Behavior Research Methods, 48 (1), 400–407.

- Hilton, D., Treich, N., Lazzara, G., and Tendil, P., 2018. Designing effective nudges that satisfy ethical constraints: the case of environmentally responsible behaviour. Mind & Society, 17 (1–2), 27–38.

- Hilton, D.J., 2001. The psychology of financial decision-making: applications to trading, dealing, and investment analysis. Journal of Psychology & Financial Markets, 2 (1), 37–53.

- Hofmaenner, D., Herling, A., Klinzing, S., Wegner, S., Lohmeyer, Q., Schuepbach, R.A., and Buehler, P., 2021. Use of eye tracking in analyzing distribution of visual attention among critical care nurses in daily professional life: an observational study. Journal of Clinical Monitoring and Computing, 35 (6), 1511–1518.

- Holmqvist, K., Marcus, N., Richard, A., Richard, D., Halszka, J., and Van de Weijer, J., 2011. Eye Tracking: A Comprehensive Guide to Methods and Measures. Oxford: Oxford University Press.

- Hurtt, R.K., 2010. Development of a scale to measure professional skepticism. Auditing: A Journal of Practice & Theory, 29 (1), 149–171.

- Hurtt, R.K., Brown-Liburd, H., Earley, C.E., and Krishnamoorthy, G., 2013. Research on auditor professional skepticism: literature synthesis and opportunities for future research. Auditing: A Journal of Practice & Theory, 32 (Supplement 1), 45–97.

- ISA, 2016–2017. Overall objective of the independent auditor, and the conduct of an audit in accordance with international standards on auditing statement on auditing standards. In: Handbook of International Standards on Auditing and Quality Control. New-York: International Auditing and Assurance Standards Board, 79–108. ISBN number : 978-1-60815-318-3.

- Johnson, P.E., Grazioli, S., and Jamal, K., 1993. Fraud detection: intentionality and deception in cognition. Accounting, Organizations and Society, 18 (5), 467–488.

- Johnstone, K.M., Bedard, J.C., and Biggs, S.F., 2002. Aggressive client reporting: factors affecting auditors’ generation of financial reporting alternatives. Auditing: A Journal of Practice & Theory, 21 (1), 47–65.

- Just, M., and Carpenter, P., 1976. Eye fixations and cognitive processes. Cognitive Psychology, 8, 441–480.

- Just, M., and Carpenter, P., 1980. A theory of Reading: from eye fixations to comprehension. Psychology Review, 87, 329–354.

- Kachelmeier, S.J., and Messier, W.F., 1990. An investigation of the influence of a nonstatistical decision aid on auditor sample size decisions. The Accounting Review, 65 (1), 209.

- Kelly, K., and Murphy, P.R., 2021. Reducing accounting aggressiveness with general ethical norms and decision structure. Journal of Business Ethics, 170 (1), 97–113.

- Kennedy, J., 1993. Debiasing audit judgment with accountability: a framework and experimental results. Journal of Accounting Research, 31 (2), 231–245.

- Kenny, D., Kashy, D.A., and Bolger, N. 1998. Data analysis in social psychology, In: D.T. Gilbert, S.T. Fiske, and G. Gardner, eds. The Handbook of Social Psychology, 4th ed., Boston: Oxford University Press, 233–265.

- Kramer, R.M., Pommerenke, P., and Newton, E., 1993. The social context of negotiation effects of social identity and interpersonal accountability on negotiator judgment and decision making. The Journal of Conflict Resolution (1986–1998), 37 (4), 633–654.

- Larrick, R.P. 2004. Debiasing. In: D.J. Koehler and N. Harvey, eds. Blackwell Handbook of Judgment and Decision Making. Hoboken: Blackwell Publishing, 316–338. https://doi.org/10.1002/9780470752937.ch16

- Lerner, J.S., and Tetlock, P.E., 1999. Accounting for the effects of accountability. Psychological Bulletin, 125 (2), 255–275.

- Litz, R.A., 1996. A resource-based-view of the socially responsible firm: stakeholder interdependence, ethical awareness, and issue responsiveness as strategic assets. Journal of Business Ethics, 15 (12), 1355–1363.

- Loibl, C., Sunstein, C.R., Rauber, J., and Reisch, L.A., 2018. Which Europeans like nudges? approval and controversy in four European countries. The Journal of Consumer Affairs, 52 (3), 655–688.

- Lord, A.T., 1992. Pressure: a methodological consideration for behavioral research in auditing. Auditing: A Journal of Practice & Theory, 11 (2), 89–108.

- Lynch, E.J., and Andiola, L.M., 2019. If eyes are the window to our soul, what role does eye-tracking play in accounting research? Behavioral Research in Accounting, 31 (2), 107–133.

- MacLean, G.H., Klein, R.M., and Hilchey, M.D., 2015. Does oculomotor readiness mediate exogenous capture of visual attention? Journal of Experimental Psychology: Human Perception and Performance, 41, 1260–1270.

- Manzon, E., 2020. Eye tracking technology in the marketing classroom: an experiential learning method. Marketing Education Review, 30 (2), 105–111.

- McMillan, J.J., and White, R.A., 1993. Auditors’ belief revisions and evidence search: the effect of hypothesis frame, confirmation bias, and professional skepticism. The Accounting Review, 68 (3), 443–465.

- Meissner, M., and Oll, J., 2019. The promise of eye-tracking methodology in organizational research: a taxonomy, review, and future avenues. Organizational Research Methods, 22 (2), 590–617.

- Melnyk, V., van Herpen, E., Fischer, A., and van Trijp, H.C.M., 2011. To think or not to think: the effect of cognitive deliberation on social norm influence. Advances in Consumer Research, 38, 495–496.

- Misra, F., Sugiri, S., Suwardi, E., and Nahartyo, E., 2019. Accountability pressure as a debiaser for confirmation bias in information search and tax consultant’s recommendations. Journal of Indonesian Economy and Business, 34 (1), 57–74.

- Mohammad, J.K., and Oczkowski, E., 2021. The link between trait and state professional skepticism: a review of the literature and a meta-regression analysis. International Journal of Auditing, 25 (2), 558–581.

- Mrkva, K., Westfall, J., and Van Boven, L., 2019. Attention drives emotion: voluntary visual attention increases perceived emotional intensity. Psychological Science, 30 (6), 942–954.

- Nelson, M.W., 2009. A model and literature review of professional skepticism in auditing. Auditing: A Journal of Practice & Theory, 28 (2), 1–34.

- Nolder, C.J., Ratzinger-Sakel, N.V.S., and Theis, J.C., 2022. Nudging auditors’ unconscious to improve performance on an accounting estimate task. International Journal of Auditing, 26 (2), 78–93.

- Oppenheinmer, D., Meyvis, T., and Davidenko, N., 2009. Instructional manipulation checks: detecting satisficing to increase statistical power. Journal of Experimental Social Psychology, 45 (4), 867–872.

- Pe’er, E., Feldman, Y., Gamliel, E., Sahar, L., Tikotsky, A., Hod, N., and Schupak, H., 2019. Do minorities like nudges? The role of group norms in attitudes towards behavioral policy. Judgment and Decision Making, 14 (1), 40–50.

- Phillips, F., 1999. Auditor attention to and judgments of aggressive financial reporting. Journal of Accounting Research, 37 (1), 167–189.

- Pilkington, R., and Parker-Jones, C., 1996. Interacting with computer-based simulation: the role of dialogue. Contemporary Accounting Research, 27 (1), 1–14.

- Posner, M.I., 2012. Attention in a Social World. New-York: Oxford University Press.

- Posner, M.I., and Petersen, S.E., 1990. The attention system of the human brain. Annual Review of Neuroscience, 13, 25–42.

- Public Company Accounting Oversight Board (PCAOB), 2018. Auditing Accounting Estimates, Including Fair Value Measurements and Amendments to PCAOB Auditing Standards. Available from: https://pcaobus.org/Rulemaking/Docket 043/2018-005-estimates-final-rule.pdf.

- Public Company Accounting Oversight Board (PCAOB), 2022. Staff Update and Preview of 2021 Inspection Observations. Available from: https://pcaob-assets.azureedge.net/pcaob-dev/docs/default-source/documents/staff-preview-2021-inspection-observations-spotlight.pdf?sfvrsn=d2590627_2/.

- Public Company Accounting Oversight Board (PCAOB), 2023. Professional Competence and Skepticism are Essential to Quality Audits. Available from: https://pcaobus.org/documents/competence-and-skepticism-spotlight.pdf.

- Qin, F., Mickiewicz, T., and Estrin, S., 2022. Homophily and peer influence in early-stage new venture informal investment. Small Business Economics, 59 (1), 93–116.

- Ray, T., 2015. Auditors still challenged by professional skepticism: certified public accountant. The CPA Journal, 85 (1), 21–27.

- Robinson, S.N., Curtis, M.B., and Robertson, J.C., 2018. Disentangling the trait and state components of professional skepticism: specifying a process for state scale development. Auditing: A Journal of Practice & Theory, 37 (1), 215–235.

- Rose, A.M., Rose, J.M., Rotaru, K., Sanderson, K.-A., and Thibodeau, J.C., 2022. Effects of uncertainty visualization on attention, arousal, and judgment. Behavioral Research in Accounting, 34 (1), 113–139.

- Ruiz, J.L., and Sirvent, I., 2022. Benchmarking within a DEA framework: setting the closest targets and identifying peer groups with the most similar performances. International Transactions in Operational Research, 29 (1), 554–573.

- Schubert, C., 2017. Exploring the (behavioural) political economy of nudging. Journal of Institutional Economics, 13 (3), 499–522.

- Seta, J.J., Seta, C.E., Crisson, J.E., and Wang, M.A., 1989. Task performance and perceptions of anxiety: averaging and summation in an evaluative setting. Journal of Personality and Social Psychology, 56 (3), 387–396.

- Shaub, M.K., and Lawrence, J.E., 2002. A taxonomy of auditors’ professional skepticism. Research on Accounting Ethics, 9, 167–194.

- Simonson, I., 1989. Choice based on reasons: the case of attraction and compromise effects. Journal of Consumer Research, 16 (2), 158–174.

- Sunstein, C.R., 2015. The ethics of nudging. Yale Journal on Regulation, 32 (2), 413–450.

- Tajfel, H., 1978. Differentiation Between Social Groups: Studies in the Social Psychology of Intergroup Relations. London: Academic Press.

- Tetlock, P.E., and Boettger, R., 1989. Accountability: a social magnifier of the dilution effect. Journal of Personality and Social Psychology, 57 (3), 388–398.

- Thaler, R.H., and Sunstein, C.R., 2008. Nudge: Improving Decisions About Health, Wealth, and Happiness. New Haven: Yale University Press.

- Thévenot, L., and Boltanski, L., 1991. De la justification. Les économies de la grandeur. Paris: Gallimard.

- Thogersen, J., 2006. Norms for environmentally responsible behaviour: an extended taxonomy. Journal of Environmental Psychology, 26 (4), 247–261.

- Touche, D., 1991. The Robert M. Trueblood Accounting and Auditing Case Study Series. Wilton, CT: Deloitte & Touche Foundation.

- Wedel, M., and Pieters, R., 2008. A review of eye-tracking research in marketing. Review of Marketing Research, 4, 123–147.

- Westermann, K.D., Bedard, J.C., and Earley, C.E., 2015. Learning the “craft” of auditing: a dynamic view of auditors’ on-the-job learning. Contemporary Accounting Research, 32 (3), 864–896.

- Wetmiller, R.J., 2022. The copycat effect: do social influences allow peer team members’ dysfunctional audit behaviors to spread throughout the audit team? Journal of Applied Accounting Research, 23 (2), 362–380.

- Young, D., 2013. Anticipating Human Behavior: How Social Norms and Social Ties Influence Compliance with Financial Reporting Standards. Ph. D. thesis, Emory University.

- Young, S.N., 2008. The neurobiology of human social behaviour: an important but neglected topic. Journal of Psychiatry & Neuroscience, 33 (5), 391–392.

- Yusuf, S., Kagdi, H., and Maletic, J.I., 2007. Assessing the comprehension of uml class diagrams via eye tracking. In: 15th IEEE International Conference on Program Comprehension (ICPC ‘07), 113–122.