ABSTRACT

This paper focuses on lessons related to the development of viable medium, small and micro-enterprises (SMMEs) based on non-timber products in East Nusa Tenggara (ENT), Indonesia, that are relevant to the international aid shift towards private sector development and women’s economic empowerment. Most of the products traded in the 11 428 market stalls surveyed in informal-sector market places in ENT were not from forests or agroforests, but were vegetables, second-hand clothes and other products. Most of the forest and agro-forestry products being sold were low entry-point, low-value products, sold as part of people’s survival or coping strategies. Nevertheless, a few specialist products, such as indigo, hand-woven textiles, Symplocos leaf mordants and Lygodium fern baskets, have been remarkably successful in reaching global markets. Developing business partnerships with local producer groups and entrepreneurs is easier said than done, and requires strategic choices. In addition, enterprises need to be economically viable. At first, palm sugar from Borassus flabellifer, for example, seemed to be a viable product, but the costs of the fuelwood used to boil palm sap to produce palm sugar is the major constraint on palm sugar producers and household income. Ten barriers facing entry of non-timber products into commercial markets are identified that should be taken into account if long-term enterprise development based on these products is to succeed in the long term.

Introduction

In Indonesia, micro-enterprises are considered to be those with 1–4 workers (excluding the owner), while small enterprises have 5–19 workers, medium enterprises 20–50 workers, and those with more than 50 workers are considered large enterprises (Tambunan Citation2005). This review focuses on small, medium and micro-enterprises (SMMEs) based on trade in a diversity of non-timber forest products (NTFPs).

Although the Indonesian government has supported small and medium enterprises (SMEs) because they can play a role in job creation and the production of exports (Tambunan & Cant Citation2009), the informal industry sector should also be considered. By definition, informal-sector activities are part of a ‘hidden economy’ that is neither taxed nor monitored by national governments. Yet, self-employment in the informal sector is a particularly significant economic opportunity for low-income households, and for women with limited employment options or earning power (Woller Citation2004; Tambunan & Cant Citation2009). Unlike the example of the furniture industry in Jepara, Java, where a cluster of 15 271 wooden furniture production units employs about 170 000 workers (Roda et al. Citation2007), fewer ethnobotanical studies have been done of NTFPs traded in informal-sector market places, exceptions being the study of Arman (Citation1996) of fruits sold in Pontianak, West Kalimantan, and the recent study of Cunningham et al. (Citation2011a) in East Nusa Tenggara (ENT), which provides the quantitative basis for this policy-oriented paper.

Indonesia’s largest donor of bilateral aid, Australia, has shifted away from the donor–recipient model to one aimed at a more efficient approach, with a focus on private sector development (PSD) and women’s economic empowerment (DFAT Citation2015). Although interest in PSD and public–private partnerships (PPP) has increased since the 1980s (Reed & Reed Citation2009), PPP have been applied mostly to mainstream agribusiness (such as global coffee and cocoa supply chains), and far less to non-timber products. This is not surprising for several reasons, including the fact that the terms ‘non-timber products’ or ‘non-timber forest products’ confuses many policy makers and potential business partners. Over a decade ago, Belcher (Citation2003) pointed out that the term NTFPs is confusing precisely because it is a negative term that refers to what NTFPs are not (i.e. non-timber), rather than what they actually are. In the 1980s, as Peters (Citation2011, p. v) points out, ‘there seemed to be an unstated assumption that somehow the NTFP acronym – as well as the people that collect them and the markets through which they are sold – represented a distinct and relatively homogenous category of products and processes’. Being faced with complexity and diversity rather than homogeneity puts many people off, including potential funders in the agribusiness sector who are used to clearly defined, mainstream commodities. To compound the problem, unrealistic expectations of the economic value of NTFPs, stimulated in the late 1980s by an influential paper by Peters et al. (Citation1989), resulted in disillusionment about NTFPs as an economic alternative to unsustainable logging of tropical forests (Sheil & Wunder Citation2002; Belcher & Schreckenberg Citation2007). Nevertheless, as Ruiz-Perez et al. (Citation2004) pointed out after an analysis of 61 traded NTFPs, specialisation, supplemented for some NTFPs by intensive management and agroforestry production, can make a significant difference to household income. In Indonesia, in common with the economic success of the timber furniture trade from Jepara (Roda et al. Citation2007), there are vibrant clusters of small-scale enterprises that process and export NTFPs. These include rattan blinds and furniture (Smyth Citation1992), a vibrant traditional medicines (jamu) market (Phillip Capital Citation2014), and Lygodium circinnatum fern basketry (Cunningham et al. Citation2011a).

Australia’s shift in foreign aid policy was stimulated by the fact that, from a macro-economic perspective, rapid economic growth and industrialisation have made Indonesia a middle-income country and the world’s sixteenth-largest economy. Yet ENT, Indonesia’s driest and poorest province, is a world away from bustling industrial centres of Java or the tourist hub of Bali. Most of ENT’s 5.1 million people are involved in small-scale farming, and depend on timber and NTFPs, as well as off-farm income during the long annual dry seasons and frequent droughts. Due to the complexity and diversity of the NTFP sector, the current focus of Australian aid for PSD needs a nuanced understanding of what ‘business’ can (and cannot) offer as ‘development agents’ when it comes to NTFPs. A clear understanding about how businesses operate is also needed at the village level. Under these circumstances, it is worth asking whether NTFPs, which are either wild-harvested from forests or more intensively produced in agroforestry systems, can play an important role in poverty alleviation in ENT, and if so, how this can be done?

Our paper is structured as follows. First, the methods used to assess different categories of trade in non-timber products from forests and agroforests over the past decade are described. Second, the results are presented, differentiating products according to the geography of trade (local, inter-island, national and international export) and gender aspects of trade, discussing species sold in both large-scale and niche markets. In particular, products that offer a greater chance for enterprise development are highlighted. Third, a framework for improving the efficiency of development aid delivery focused on PSD related to NTFPs is suggested.

Methods

The quantitative data and qualitative information presented come from nine methods and approaches used over the past decade. First, systematic surveys of local marketplaces were conducted (Cunningham et al. Citation2011a). This is widely acknowledged as a method for gaining insights into which plant species have commercial value in local livelihoods, and increasing understanding of the characteristics of traders (Cunningham Citation2001). Data on the informal-sector trade in local marketplaces on Flores, Savu, Sumba and in West Timor were collected, including counting the number of women and men selling products in the different marketplaces. Systematic classification of these marketplaces, their schedules and the types of traders within them was an important step in understanding the network of harvesting and trade in products such as Areca catechu (pinang) and Piper betle (sirih). Three markets were surveyed on Flores (Bajawa, Ende and Maumere); two on the small, remote island of Savu (Seba and Lobohede); six on Sumba (Waitabula, Waingapu, Waikabubak, Melolo, Lewa and Kananggar); and 17 in West Timor (Naikoten and Oeba markets in Kupang; Oinlasi, Oesau, Niki Niki, Maubesi, Kapan, Soe, Eban, Camplong, Betun, Baun, Batu Putih, Baru Kefa and Lama Kefa in Kefamenanu; Atambua and Tarus) (). Together, these markets form a major outlet for informal-sector marketing of agricultural crop surplus, agroforestry and forest products, but not high-value products such as sandalwood (Santalum album), gaharu (Aquilaria malaccensis) and Indian screw-tree fruits (Helicteres isora) that are generally only observed in separate ‘ethnic supply chains’.

Figure 1. Sizes of markets on Flores, Sumba and West Timor. (a). Informal sector daily markets. (b). Periodic (weekly) markets. Sizes of circles indicate number of sellers.

Second, the ‘hidden’ supply chains that are separate from the trade in local marketplaces were assessed through field observation and interviews with people along the supply chain—from harvesters and middlemen to major traders. Specifically, these supply chains involve trade in some medicinal plants, such as Helicteres isora (locally known as usakneo or kayu ules), Usnea (Spanish moss, known as tai anggin or kayu anngin), candlenuts (Aleurites moluccana, kemiri), Tamarindus indica (asem) pulp and seeds and, to a lesser extent, in dyes (Maclura cochinchinensis (kayu kuning)). These are often sold through kinship networks of traders who consolidate products bought from smallholder producers by ‘papalele’ (buyers of these products at the farm-gate), where Indonesian entrepreneurs of Chinese descent usually play a leading role in the consolidation process. Similar trade networks are recorded for trade in rattans, sandalwood, Aquilaria resin (gaharu) and swiftlet ‘bird’s’ nests, but as these have been studied by others (for example: Smyth Citation1992; Soehartono & Newton Citation2001; McWilliam Citation2005; Yoder Citation2011; Idris et al. Citation2014) they were not a focus of this work.

Third, available trade data for forestry and agroforestry products was analysed. As project partners, the staff of the Forestry Research and Development Agency (FORDA) office in West Timor collated official statistics on agroforestry products and NTFPs (such as honey and lac). In addition, Threads of Life (ToL)—an organisation that supports and promotes Indonesian textile weavers—provided access to their data on sales of high-quality baskets and hand-woven textiles.

Fourth, international trade data were obtained from published literature and from websites that record international trade (such as www.zauba.com). In the case of baskets woven from Lygodium circinnatum (fern stems in Indonesia that are exported globally), prices were recorded from websites of wholesalers in Japan (www. rakuten.co.jp), the USA (for example http://www.alaskafurexchange.com and http://www.alaskaantler.com) and, at the final point in the value chain, in Alaska, USA.

Fifth, the harvest of specific products, such as Canarium nuts, Symplocos leaves (for mordants) and Lygodium stems for basketry fibre, was observed, and interviews undertaken with both harvesters and producers of specific products. This included discussions on prices, processing methods, quantities of a product that harvesters generally collected in a day and, where relevant, whether resource shortages were or were not becoming a constraint.

Sixth, discussions were held with small-scale producers, traders and consolidators about prices and value-chain dynamics of products (ranging from tamarind pulp and candlenuts to seed oils, dyes, mordant plants and textiles). These discussions were important, for as Kanji et al. (Citation2005) point out, value-chain analysis does not give a comprehensive perspective of market interactions.

Seventh, based on knowledge of natural products, marketing and value-adding opportunities for NTFPs in ENT were identified.

Eighth, the appropriate production and marketing partners were identified to realise these opportunities. Some of the products from the seventh step—for example lontar (Borassus flabellifer) palm sugar—have not developed further at this stage.

Lastly, community-based businesses were initiated for NTFPs in different markets using a range of business models and over individualised timeframes. Domestic trade and international wholesale trade of Symplocos cochinchinensis leaf powder as a natural dye mordant was facilitated for two communities in central Flores; virgin coconut oil production was initiated in one community in Timor for the local domestic market; and indigo paste production was initiated in four villages in Timor for use by local natural dyers and for export to Bali.

Results

The results are explored in two ways: through an analysis of the characteristics of markets at different points in the value chain, and through case studies drawn from the research.

Characteristics of markets

The surveys of trade in products from forests and agroforests carried out during this study enable the characterisation of the different types of trade. In particular, this enables a far better understanding of the hidden economy based around trade in the informal sector, with trade being grouped into three main categories: informal-sector trade in local marketplaces; intra-island and inter-island trade; and exports from ENT to national and international markets.

Informal-sector trade in local marketplaces

Of the 11 428 market stalls surveyed, over half were occupied by female sellers (53.8%), with men occupying 44.9%, and men and women sharing the stalls in 1.3% of stalls. Most of the stalls (9365; 81.9%) were in permanent (daily) markets, characteristic of larger towns ()), and the remainder (2063; 18.1%) were in weekly markets ()) in more remote rural areas or rural villages. In terms of types of seller, the majority of sellers in all markets were middlemen (9512; 83.2%), followed by producer-sellers (farmers marketing their own farm products) (1639; 14.3%). There were relatively few bulk sellers or travelling merchants (who move from one weekly market to another (236; 2.1%)), and very few itinerant sellers (only 5 people). The lack of itinerant traders in the sample is probably due to the survey method, which was focused on local marketplaces, while most itinerant sellers market farm products (such as vegetables) or fresh Borassus flabellifer (lontar) palm wine by doing the rounds of local neighbourhoods in larger towns. In both the wet and dry seasons, the focal categories of interest in this study (forest and agroforestry products) were outnumbered by vegetable sellers and clothes sellers (). The majority of people selling agroforestry products (n = 1918), forest products (n = 204), and spices and cultivated medicinal plants (n = 563), had either not attended school or had elementary school education.

Figure 2. Numbers of men and women selling a range of products, from building materials (bahan bangunan), ducks (bebek), agricultural products (jagung (beans), beras (rice) and sembako (‘sembilan bahan pokok’, which as we explain in this paper, refers to nine (sembilan) commodities that are considered basic household needs) and then products from agroforestry systems, forests, and non-timber forest products, such as firewood (kayu api), the pinang/sirih combination (Areca catechu (betel nut, pinang) palm fruits and Piper betle flowers/leaves (sirih), coconut oil (minyak kelapa), Borassus flabellifer palm sugar (gula merah) and forests (including minyak kayu putih (Melaleuca oil), obat/bumbu (medicines and spices)) in relation to other products, such as vegetables and clothes].

![Figure 2. Numbers of men and women selling a range of products, from building materials (bahan bangunan), ducks (bebek), agricultural products (jagung (beans), beras (rice) and sembako (‘sembilan bahan pokok’, which as we explain in this paper, refers to nine (sembilan) commodities that are considered basic household needs) and then products from agroforestry systems, forests, and non-timber forest products, such as firewood (kayu api), the pinang/sirih combination (Areca catechu (betel nut, pinang) palm fruits and Piper betle flowers/leaves (sirih), coconut oil (minyak kelapa), Borassus flabellifer palm sugar (gula merah) and forests (including minyak kayu putih (Melaleuca oil), obat/bumbu (medicines and spices)) in relation to other products, such as vegetables and clothes].](/cms/asset/5690bd16-20b7-483c-b732-16578c2e1edb/tfor_a_1329614_f0002_oc.jpg)

The most commonly sold agroforestry products were the combination of pinang (Areca catechu) and sirih (Piper betle). Wild-harvested forest products were sold by spice and traditional medicine sellers, generally including bark of kayu manis (cinnamon, Cinnamomum burmannii) and kayu hamoi (a Litsea species). Throughout Sumba, sellers (mainly from Bima in West Nusa Tenggara) generally sell clothes and everyday needs such as rice, sugar, cooking oil and salt from sembako stalls, while Savunese generally sell raw materials for dyes and, in the Melolo area of Sumba, palm sugar (gula lempeng—palm sugar in flat rounds or discs). The term sembako, widely used in Indonesia, is a shortened form of sembilan bahan pokok. This refers to nine (sembilan) commodities that are considered basic household needs–eggs, milk, salt, granulated sugar, kerosene (or alternatively, liquefied petroleum gas (LPG)), rice (or cassava), cooking oil (or margarine), beef (or chicken meat) and maize (or, in some areas, sago). Agroforestry products are also sold by sembako sellers.

In West Timor, at Atambua market, apart from many local sellers, others originate from Rote (an island south of West Timor), Kupang, East Timor or Java; or are Bugis or Chinese Indonesians. Local people generally sell surplus crops from their home gardens, as well as cassava, sweet potatoes and other vegetables. Throughout Timor, local producer-sellers typically sell out in the open, and are poorer farmers who make a subsistence income from sales.

Sellers from Rote, Savu and Bugis traders in semi-permanent areas and have more stock to sell, with a larger variety of products. Sellers at these permanent locations sell goods that are relatively long-lasting, like household cooking products, spices, salted fish, betel nut (pinang) and tobacco.

In terms of the gender of market sellers, the proportion of women selling fruits, vegetables, obat/bumbu (medicines/spices), coconut oil (minyak kelapa) and dried fish was significantly different.

In terms of outfitters, most were men (many from Bima). Men also dominated the fresh fish trade and sales of livestock and hardware (such as machetes and other locally smithed tools). Only a small proportion of the products sold in local marketplaces are wild-harvested from natural forests, most products being derived from agroforestry systems. The relative proportions of people selling these three product categories were similar across Flores, Sumba, Savu and West Timor (Cunningham et al. Citation2011a).

Intra-island and inter-island trade within ENT

Within ENT, complex intra-island and inter-island supply chains occur over both short distances (such as trade in palm syrup from Savu to Raijua and Sumba) or over longer distances (such as from Flores to Bali). It is clear that cultural preferences are an important driver of local and inter-island trade in many products from forests and agroforestry systems. Trade in textiles, the betel nut combination of Areca catechu (pinang) and Piper betle (sirih), and plants used in traditional medical systems (such as Acorus calamus rhizomes and Litsea bark (kayu hamoi)) are good examples.

Exports from ENT for national and international markets

Counts of all the traders in different categories also provided a background context to the relative importance of forest and agroforestry products compared with other categories (such as vegetables, fish or second-hand clothes). A total of 11 428 market sellers were surveyed: 3242 on Flores (28.4%), 2192 on Sumba (19.2%), 5874 in West Timor (51.4%) and 120 on Savu (1%). All interviews with sellers and traders were conducted either in local languages or in Bahasa Indonesia.

Exports from ENT to other parts of Indonesia include trade in two main categories: the more visible market chains, which are at least partially recorded in official statistics, such as trade in Aleurites moluccana (kemiri) and Areca catechu (pinang) fruits; and the hidden market chains for high-value, wild-harvested products. These are sold in the national market and internationally. Good examples are the national and international trade in Aquilaria (gaharu) resin, Pemphis acidula (santigi) (one of the world’s best tree species for bonsai, with single individuals selling for 30 million IDR (AUD 3300)), Lygodium circinnatum fern stems for basketry, Usnea (Spanish moss) and Helicteres isora fruits (both ingredients for jamu).

Case studies

Each of the case studies has been analysed based on the barriers to entry for each product in a specific location with respect to the three broad levels of the market chain. Ten parameters were developed with which to perform the analysis of the barriers to entry in these markets:

Resource base needs

Capital needs

Scale needs

Quality needs

Market knowledge needs

Trade network needs

Inventory turnover needs

Policy and regulation needs

Marketing partner needs

Producer support needs.

These needs, and the associated barriers to entry, vary according to whether trade is into local markets, intra-island or inter-island trade, or international markets. When presented in a framework, the results aid in decision-making about which products have potential, where that potential lies, and what is needed to develop that potential within a market level and when transitioning between market levels. Example analyses are presented in and .

Table 1. Barriers to entry for different markets for virgin coconut oil (VCO) production in Timor, Indonesia

Table 2. Barriers to entry for different markets for indigo dye paste production in Timor, Indonesia

Traditional textile weavers’ groups

Within local markets, the vast majority of traditional textiles are made with synthetic dyes. These are profitably traded across intra-island and inter-island markets, but do not command sufficiently high retail prices in the international market to encourage trade partnerships directly with producers. However, beside the local markets there is a hidden trade in natural-dyed textiles that are made for use in customary ceremonies, for personal use by the weaver and her extended family, or for direct sale to members of the community with ceremonial needs for traditional cloth. As the price on the international market for a natural-dyed textile can be ten times the price of a synthetic-dyed equivalent, there is a market niche for high-quality, high-value, handmade, natural-dyed, traditional textiles that are marketed based on the personal stories and cultural integrity of the weavers and dyers. ToL was established in this market niche in 1998 and now works directly in the field with over 1000 producers across 12 Indonesian islands, where the textiles are made with locally sourced natural dyes from forest and agroforestry systems. In terms of the above framework, the unusual aspects of the enterprise are the depth of focus applied to resource base and producer support issues, developing sufficient supplies of dye plants, and facilitating the continued transmission of traditional dye recipe knowledge.

Lygodium circinnatum baskets

The international trade in baskets from the climbing fern Lygodium circinnatum is particularly interesting. Initially, basket makers in Tenganan, East Bali, traditionally used L. circinnatum fibre to weave just four basket types for a small-scale, local trade. In terms of the resource base, barriers to entry were low, quality was high, and financial requirements for basket production were low. Today, through the initiative of a few local innovative ‘champions’, Tenganan has become a global hub for fine basketry design and trade, with hundreds of basket designs. The basket production process has changed, so that Tenganan is the marketing hub, with decentralised basket production across the Kabupaten (Regency) of Kerangasem. Some villages specialise in a single, intricate, high-value basket type while other baskets, such as handbags, are produced in a ‘conveyer belt’ sequence across different villages, some weaving the basket, others weaving straps or fixing Japanese cloth inside the baskets before they are returned by motorbike to Tenganan for packing and export.

The impressive market knowledge of Tenganan’s ‘champions’ has been fed by a ‘made-to-order’ sensitivity to export markets, where marketing partners, such as Japanese importers, suggest particular designs that will sell well in Japan. Exports are mainly to Japan (c. 70%), but also to Europe and North America. Even with current non-selective harvesting of L. circinnatum stems, a harvester is able to collect ten bundles (each of 70–100 stems) per day, selling these for 5000 IDR per bundle (an income of AU$5 per day), which is above the average daily income for the area. These are sold to traders who re-sell bundles of fern stems in Lombok and at Bebandem market in East Bali, where they are bought by local farmers who supplement their income by weaving fine-quality baskets.

Prices vary with the size and intricacy of basket design. Small baskets tend to have a higher mark-up than larger baskets. This reaches an extreme in the USA export market, where a ‘fruit basket’ style basket for which the weaver is paid 50 000 IDR (around AU$5) ()) retails for AU$117 in Alaska ()). Unlike the Japanese retail market, where L. circinnatum baskets from Bali are advertised as such (see www. rakuten.co.jp), those sold in Alaska are commonly marketed as ‘smoked grass’ baskets ‘embellished’ by Inuit people without mention of basket origin (). Yet even the iconic ‘Alaskan’ carved bone ornaments used as embellishments (such as salmon, bald eagle heads or hump-back whale tails) are carved in Bali (,)). In addition, these high-quality baskets are in demand at tourist centres, such as Kuta, Sanur and Ubud, driving a large-scale intra-island trade.

Figure 3. Complexity and value-chains. (a). ‘Fruit basket’ woven of Lygodium circinnatum fibre in Bali for which the weaver gets AU$5. (b). The same basket type embellished by Inuit with a carved whale tail (retail price AU$117). (c). A soap-box-style L. circinnatum basket from Bali. (d). A Balinese basket embellished with a carving of an Inuit. (e). A made-to-order enterprise at a cluster carving Native American and Inuit style carvings in Bali. (f). Bags of carved humpback whale tails and bald eagle heads produced in Bali that are similar to those used to embellish Bali baskets sold in Alaska. Photos: A.B. Cunningham.

This commercial success and high trade turnover has resulted in commercial depletion of large L. circinnatum stems in forests of East Bali, increasing the cost of the resource on which this commercial trade is based. Bundles of stems are wild-harvested in montane forests of Flores, Sumbawa and Central Kalimantan, and then sent to Bebandem market and Tenganan. In this case, both significant needs relate to the resource base. The first resource-based need is to raise awareness along the supply chain that digging up the base of the stems to get the dark section near the rhizome (that is used to weave a pattern into some baskets) has a high impact on individual L. circinnatum plants and is inadvisable if continued harvests are to be sustained. The second need is to raise awareness among middlemen and harvesters that selective cutting of L. circinnatum stems is preferable to cutting all stems. Selective cutting of only straight stems would leaving large crooked stems to continue to grow and would shorten the recovery time after harvest. Offering harvesters double the price for graded (straight) stems (i.e. IDR 10 000 per bundle) would make little difference to the final sale price, but a big difference to resource recovery times.

Virgin coconut oil

As with indigo (see below), the biggest barriers between markets for virgin coconut oil are at the transition between the local and the intra-and-inter-island markets, though with this product the transition needs to be between market partners as ToL does not have the expertise needed above the local market level. ToL could facilitate connections with local entrepreneurs but did not have the means to develop national-level contacts in essential oil markets within the project timeframe. A business plan for the local market was therefore developed based on the participants’ data on coconut supplies, their material costs, and local retail prices for virgin coconut oil. As for many such businesses, initial capital would be converted to inventory before sales generated a profit. The imperative of avoiding negative cash flow in the inventory-heavy stage of this process meant that daily wages were based on the opportunity costs of participants’ other income-generating activities. Participants would be paid both as workers when they worked and as shareholders at the year-end. Though the shareholder income could double the wage income, the most difficult aspect of the facilitation was getting participants to accept this model; they wanted the double wage at the time of work.

This highlights the second major reason for focusing on the local market first: a producer group needs to traverse the learning curve of running a business at a small scale before there is any likelihood of success in more competitive, price-sensitive and time-sensitive national markets. Price was a particular issue beyond the local market where an export market price of US$12–15 per litre (IDR 150 000–200 000) compares poorly to a farm-gate price of IDR 170 000 (US$13) per litre. Taken together, the analysis pointed to a best option of a good-quality product offered at local market prices with no market-chain intermediaries.

Indigo

Identifying the barriers to entry for each level of the indigo market also identifies the barriers for progression between different market levels. From the analysis of entry barriers for the indigo paste producers in Timor, it is clear there is a significant gap between the barriers to entry into the local market and the barriers to entry to intra-and-inter-island markets. The most significant gap is in the areas of indigo cultivation, quality control, price, and speed of delivery, and the capacities of the marketing and production support partners. From this, the need for a new market segment bridging the local and intra-and-inter-island markets was suggested. This segment would need to be tolerant of more variation in product quality, a higher price, and a slower speed of delivery than the intra-and-inter-island markets. The ToL dye studio in Bali has initiated a new business offering week-long natural dye classes to international dyers, and will use indigo dye paste from the Timorese producers whenever it is available, thus providing a flexible bridging market.

Lontar palm (borassus flabellifer) products

Across South-East Asia, B. flabellifer palms provide multiple products to households (Fox Citation1977; Davis & Johnson Citation1987; Borin & Preston Citation1995; Cunningham et al. Citation2011a). These include low-cost housing (thatch and construction timber), food supplements from the fruits and sap, basketry for a wide range of purposes, and pig food. Lontar sap products are commercially most important. Borassus flabellifer palm sugar yields can be 18 tonnes ha–1 (Khieu Citation1996) compared with coconut palm sugar production of 19 tonnes ha–1 (Jeganathan Citation1974) and sugarcane production (5–15 tonnes of sugar ha–1) (Dalibard Citation1999).

In ENT there is a long history of attempts to add value to lontar products, and no other agroforestry or forest product can match the diversity of value-added commercial products as those from lontar (Cunningham et al. Citation2011a). Barriers to entry are relatively low, yet there is significant potential for increased lontar palm sugar trade within Indonesia. In Java, for example, a rising middleclass and coffee culture has driven up the price for gula lempeng, the palm syrup that is poured into palm-leaf rings (R. Achdiawan, pers. comm. 2016). In Bali, lontar palm syrup could be a definite winning product, ‘the maple syrup of Asia’, poured over ice-cream and pancakes in hundreds of restaurants.

At first glance, tapping is sustainable and the resource base seems secure. Based on a review of palm-tapping technologies (Cunningham Citation1990) and field observation in tropical Africa and Asia, the palm-tapping techniques used on Savu, Raijua and Rote are the most sophisticated and sustainable tapping methods used anywhere. Palm sap tappers, all of them men who are local farmers, tap the palm flower stalks, collecting the sap that excretes from the wound. This is generally done twice a day, once in the morning and once in the afternoon. There are two seasons, one with low yields (late April – August) and one with high yields (Sept – early November). The resource management issue is the quantity of firewood needed to boil palm sap into palm sugar in already fuelwood-scarce landscapes of Savu, Raijua and West Timor, so fuelwood costs are the major constraint on palm sugar producers and household income.

This has had a knock-on effect in terms of quality needs. In some parts of Savu, women add sodium bicarbonate to the palm syrup before it is reduced to its final stage. This is done to thicken it more quickly, but the shelf life of the palm syrup is shorter and its quality reduced. At the moment, most of this palm syrup is sold to Raijua or Sumba, but if export of organically certified palm syrup develops, then quality control at various stages of the supply chain will be needed.

In addition to competing with local household fuelwood requirements, the growth in the specialist smoked Timorese pork (sei babi) industry in West Timor and large-scale pollarding of Schleichera oleosa trees on Rote and Sumba by lac producers has also affected stocks of this tree species.

An additional potential problem is that sustainable use depends not only on the natural resource base, but also on customary knowledge and skills. If there is no incentive to pass these skills down to the next generation, then those techniques and knowledge will be lost. This process of change is facing lontar palm tapping on Raijua, and possibly on Rote, due to a clash of economies between seaweed production and lontar sap tapping. For the last two years, people have been selling palm syrup to Raijua in large quantities. This is related to the seaweed business, which developed to a large scale on Raijua since 2006. Many people have therefore stopped tapping lontar, particularly near the port. This is obvious from the flowers of male palm trees, which are uncut (Cunningham et al. Citation2011a).

A further significant hurdle to trade is competition from other palm sugars. Palm sugar is not only produced from Borassus flabeliifer, but also from Arenga pinnata, coconut palms (Cocos nucifera) and Caryota urens. Coconut palm sugar in markets in Europe and USA, imported from Cambodia, Thailand and India, is cheaper than Borassus palm sugar. This could be circumvented through certification, but this has high annual costs, for example through Ecocert costs would be between AU$5000–7000 per year.

In terms of policy and regulatory needs, a bottleneck constraining lontar palm syrup exports to Darwin, Australia, is the prohibitively high insurance costs for shipping any products (including palm syrup) between Indonesia and Australia. Therefore, product and marketing support needs would be, firstly, to start with the palm syrup market in Bali and the gula lempeng market in Java, dealing with pricing issues and improving quality and traceability along the value-chain, and then, secondly, to test appropriate technologies used for producing palm sugar and palm syrup that are either very fuel-efficient or use solar technology.

In Cambodia, it is estimated that the 20 000 people producing palm sugar use 120 000–144 000 tons of fuelwood per year (GERES Citation2009). In Cambodia, and probably in ENT, this is the second highest usage after domestic cooking. The problem of fuelwood shortages facing palm sugar production is not a new one and solutions have been implemented in various parts of south and south-east Asia over the past 60 years. In India in the 1950s, Khanna (Citation1957) and Mathur and Khanna (Citation1957) developed a solar cooker for palm sugar production. In Cambodia, the palm sugar exporter Eco-Biz introduced Vattanak stoves to improve the fuel efficiency of palm sugar production. These stoves, developed by Groupe Energies Renouvelables, Environnement et Solidarités (GERES), reportedly use 30% less fuel. Whether they are more efficient than the multi-pot stoves locally developed in West Timor needs to be tested.

The third step in addressing the product and marketing needs, once the conventional market for palm syrup has developed, would be to conduct a cost-benefit analysis for organic certification.

Discussion

Ten barriers to entry were identified through the case studies as a framework of needs for long-term enterprise development. These are discussed individually below.

Resource base

The potential supply of an NTFP must be compared with the product’s potential markets; a product that has commercial viability at one scale in one market may not be viable at another scale in a broader market. The key is to avoid undermining the resource base. In many cases, natural resource-based enterprises become victims of their own success, where demand exceeds supplies of the natural resource on which marketed products are based. Concerns about timber shortages undermining the otherwise successful furniture industry of Jepara in Java, which consumes between 1.5 and 2.2 million m3 of round-wood per year (Roda et al. Citation2007), can equally apply to NTFPs, such as Lygodium circinnatum fern stems for basketry.

Risks of destructive harvest or resource depletion need to be addressed, either through managed wild harvest or through agroforestry, or both. Historical trade in Maclura cochinchinensis (kayu kuning), aromatic Aquilaria malaccensis (gaharu) resin-impregnated wood, and Symplocos leaves (often wrapped in destructively harvested bark) for use as a mordant, also has a long history in the region and was built on resource mining of what used to be substantial wild stocks of these species. Only remnant populations of the above tree species remain in the region today (for example, Soehartono & Newton Citation2001; McWilliam Citation2005; Yoder Citation2011).

ENT also has recent examples of local resource being over-exploited and food security undermined due to unintended consequences. Two examples related to a single multiple-use tree species, Schleichera oleosa, illustrate this point. The first unintended consequence was the introduction of lac insects (Laccifera lacca) and a push for a commercial lac industry in 1992. This resulted in a serious decline in the edible S. oleosa fruits in East Sumba and on Rote, ignoring the fact that these trees also produce an economically valuable oil-seed, and leaves that are an edible vegetable also used as fodder for livestock. The second unintended consequence is the growth in the specialist smoked Timorese pork (sei babi) industry in West Timor, which preferentially uses S. oleosa wood to smoke the pork. This has resulted in felling of S. oleosa trees on a massive scale around Kupang, eroding local livelihood security in the process.

These examples hold useful lessons for wild harvest and for diversifying agroforestry systems. In the Symplocos case, cultivation is difficult. Wild stocks are therefore the main supply source. Consequently, community-based forest management and a shift away from bark exploitation and tree felling to collection of the aluminium-rich fallen leaves is the viable solution for sustainable harvest for both local demand and exports of this natural mordant. The management plan developed for the forest with remnant Symplocos populations (YPBB Citation2008) is a positive example of this approach (Cunningham et al. Citation2011b).

Capital

Building business requires capital accumulation, but the private accumulation of wealth, without sharing it with one’s community, is considered anti-social in the traditional rural ENT societies where NTFPs are found. A whole community needs economic development if any one member of the community is to develop economically, otherwise the individual capable of developing an enterprise will leave the village for the relative freedom of the city. Planning and practice accommodate this social reality by developing producer groups, which tend to form from extended family networks, groups of neighbours, or members of a particular social stratum.

This can facilitate elite capture, where politically or economically powerful individuals grab opportunities at the expense of the majority. If the details of the social context within a community are not understood, elite capture can ensue. As Mansuri and Rao (Citation2003, p. 42) point out: ‘Even in the most egalitarian societies involving the community in choosing, constructing and managing a public good is a process that will almost always be dominated by elites because they tend to be better educated, have fewer opportunity costs on their time, and therefore have the greatest net benefit from participation’. Members of traditional aristocracies, those already at an economic advantage, and those with good government contacts, can end up monopolising an opportunity. This is not to say that powerful elites should be barred from participation. Their involvement is often crucial, but any tendency to dominate should be mitigated where possible. In the cases where there is elite capture of market chains for natural products, elite capture occurs at various levels and in different forms during production, transport, processing or manufacture. But although elite capture is widespread, it does not mean it cannot be avoided. If development agencies and donors are serious about enterprises that benefit poorer rural people, particularly women, then strategies to reduce or avoid elite capture are necessary.

Scale

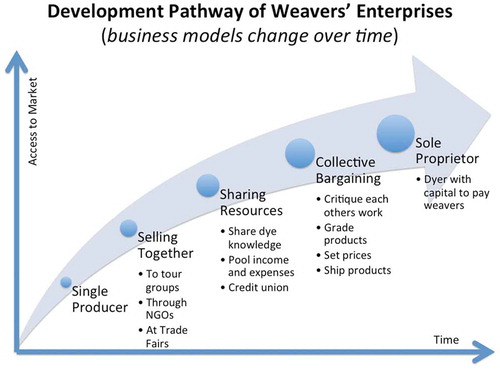

There are several relevant issues concerning scale. It is important not to underestimate the time required to build businesses that work. Building up from micro levels takes a decade, and enterprise partners may change as scale develops. Large scale is not always the right scale; it is strategic to appreciate cases where small-scale producers have advantages. Furthermore, dynamism in an enterprise can be more important than an initial scale where economies of scale can be realised through clustering. Based on the case studies presented above, a step-wise process is needed to cross the ‘missing middle’ between the starting point of local production and the needs of an external market. What is required are dynamic business pathways rather than static business models. Finally, it is useful (though not always easy) to measure results by where participants end up in the long term, not by what they achieve in the short term. Developing SMMEs in remote rural areas is not a sprint to the common donor funding cycle deadline of 3–5 years, but a challenging long-distance marathon on an 8–12 year time-scale (or sometimes longer). The development of a weavers’ cooperative in ENT illustrates this concept well, with five stages of participation identified over the course of ToL’s fieldwork since 1998 ().

Figure 4. Use of appropriate technologies to add value to natural resource-based enterprises. (a). A loom used to weave traditional textiles. (b). Testing a macadamia nut-cracker developed in Australia for cracking candlenuts (from Aleurites moluccana). (c). The traditional method of cracking candlenuts, using a tool made from a strip of Areca catechu palm spathe. (d). Using a seed-oil extraction press at a village in West Timor (press built in Java for this project). (e). Stems of the climbing fern Lygodium circinnatum. (f). A bottle top with holes: the local technology to trim fern stems L. circinnatum strips a consistent diameter for a high-quality end product. (g). A wooden frame for weaving complex straps for exported L. circinnatum baskets. Photos: A.B. Cunningham (A–D, F, G) and (h). Cunningham (E).

Some groups go through all these five stages; some reach and maintain one of the stages; some will reach a peak stage, and then drop down a level or two, before achieving a higher level again at a later time. Each stage of participation can be characterised as exhibiting a new level of shared confidence in organisational capability and income from the market. At first, the weavers are all single producers, selling to ToL as individuals. Members of ToL would go door-to-door in a village and buy directly from the weavers. But this takes a lot of time and reduces how much ToL can buy per visit, so they looked for someone around whom a group can be established—usually be a master weaver or master natural dyer with a recognised status and authority. If this woman is willing to host a group of her peers in her house, ToL ask her to invite weavers to come and sell to ToL there.

This begins the second stage, selling together. Though they might meet ToL as a group, the women still sell as individuals and the bargaining with each woman begins from scratch, even though most of the women will have very similar textiles for sale. What is saved is social time: the coffee and small talk would have been required at each household before getting down to business is now done only once, giving ToL much more time to buy.

The third stage is a long one. As trust builds within the group and shared challenges and concerns are identified, a degree of sharing may emerge. If many of the women have similar problems with dye recipes, the master dyer may share her knowledge, or communal workdays may be organised with the women meeting once a week to spin or dye together. After ToL has taught simple bookkeeping, and encouraged a small percentage (3–5%) of sales to be set aside to pay for the running of the group (covering costs of snacks and beverages for meetings, and mobile phone charges for customer communications), a significant amount can start to accumulate in the group’s petty cash. For women without ready access to credit, this capital can become the seed funding for a members’ savings and credit association. All through this third stage, sales are still organised as in stages one and two, with textiles being bargained for one-by-one with their owner-makers.

The watershed event that precipitates stage four’s collective bargaining is a willingness among the women to critique each other’s work. This is avoided in the early stages to prevent conflict, but, as the women learn what the market wants, they can start to comment on how a piece is likely to be valued, as a way of indirectly passing judgment. Once this begins, ToL can then ask the group to grade textiles of like kind and similar quality into separate piles and, once the sorting has been checked, one price for all the pieces in a pile can be negotiated. A smart group will learn to sort and set a price for the pieces in each pile before ToL arrive. The encouragement for them to do this is that it opens the way for the group to ship product to ToL in Bali, which dramatically increases their sales and improves their cash flow, rather than wait for ToL’s semi-annual buying trips to their village.

The greater access to market that stage four generates can be founded on: improved communication and commercial skills that overcome a remote community’s isolation; improved infrastructure, which reduces that isolation; or the improved notoriety of the village’s weaving tradition that the weavers’ group reputation establishes. As individual confidence increases and the sense of isolation decreases, the incentives that motivated the establishment of the cooperative may diminish. Some weavers may see themselves as better off outside the group, and this initiates stage five. Using capital they have accumulated by working with the group, they employ other weavers to work for them and establish a personal connection with external markets. Stage five is similar to stage one in that weavers are working and selling alone, but the level of market expertise has increased significantly.

While these stages suggest a path or progress, they can also mark the steps of regress. Social problems within the group or wider community can erode the mutual trust and shared confidence on which the collaborative enterprise grows. Key members may leave or die. Mismanagement or misappropriation can shatter trust. The group may be co-opted by some other agency for another purpose, and commitment to growing the business may decline. As the early adopters are seen to be doing well, a sudden surge in membership can occur, but if production then exceeds what the market can absorb, a precipitous drop can ensue.

In each of these stages, it is precisely the producers’ smallness of scale that affords their competitive advantage. Across the developing world, smallholder farmers not only have access to land and labour, but also have the local knowledge to manage complex agroforestry and farming systems in ways that are not possible in large-scale monocultures (Smart & Hanlon Citation2014). Local people also have traditional skills that produce some high-quality, handmade items for which there are a growing demand in an increasingly industrialised world that is saturated with sameness. Even though ENT covers a relatively small geographic area of Indonesia, for example, it has 40–50 local languages that reflect the cultural richness that gives depth to diverse carving designs, textile motifs or basketry styles that are highly marketable, as ToL (www.threadsoflife.com) has shown.

In his insightful analysis of Indonesian SMEs, Tambunan (Citation2005) classified enterprises into four categories that reflected how active they were:

artisanal: mainly micro-enterprises that were local market-oriented, had passive marketing and were stagnant, with low productivity and low income

active: enterprises that had more skilled workers and better technology, with active marketing, supplying national and export markets with good networking, both internally and externally

dynamic: enterprises with strong international networks and internal heterogeneity within clusters with regard to their size and use of technology

advanced: enterprises with a high level of inter-firm co-operation and specialisation; these enterprises networked strongly with raw material and component suppliers, traders, distributors and banks, also cooperating with local, regional or even national government.

In the NTFP sector, virtually all enterprises in local marketplaces would fit into the artisanal category. But, with careful selection based on outside knowledge and suitable business partners, there are ‘wild card’ products that could be viable, such as extraction of polysaccharides from tamarind seeds (Cunningham et al. Citation2011a). In ENT, most of the active, dynamic and advanced enterprises link to markets in other parts of Indonesia (mainly Bali and Java) or internationally. Outside of the textile, basketry and salt-making sectors, enterprise clusters are less common in ENT than in Bali and Java. With proper support and appropriate technology (), such as presses for extraction of high-quality seed oils ((d)), it is possible to stimulate production clusters. However, choice of location is crucial, not only in terms of the natural resource base, but for social reasons as well. In too many cases in bi-laterally funded projects, locations are chosen for other reasons, with consequent increased risk of failure.

Quality

A perennial problem in working with small-scale producers is in the maintenance of quality. This is often closely related to issues of scale, in that when a market opportunity is identified there is a tendency for producers to think that more is better, and in aiming to produce more, quality can suffer. If one design of traditional textile sells well, quality of work tends to decrease in order to increase production of that pattern, which can drop the product out of the market niche it was aiming for. In the case of virgin coconut oil, if it has been raining a lot and the copra is mouldering before it has dried, there is no point in going ahead with production as the oil will have too high a water content to be sold. Marketers and producer support organisations must be emphatic about the market’s quality standards, and must not buy sub-standard product, no matter how much producers grumble and no matter how strong the marketers’ compulsion to buy as an act of charity. The important thing is to make a long-term commitment to a producer group: people do learn, but they need experience from which to draw their lessons.

Market knowledge

It is worthwhile investing time in choosing the products that are most likely to succeed, starting with the 3–5 categories of ‘low-hanging fruit’. Which plant species or plant products, among the diverse flora of ENT, have the most potential for enterprise development today? Although the flora of ENT is poorly known and under-collected by botanists, we are spoiled for choice. In the Wallacea bio-geographic region within which ENT is located, Conservation International (Citation2008) estimated there were about 10 000 species of vascular plants, with roughly 1500 endemic species (15%) and at least 12 endemic genera. From a bio-geographical perspective, the largest island (Timor) has the highest endemism (10.3%; Monk et al. Citation1997), but how much of this is split between West and East Timor is unknown.

It is well known from quantitative ethnobotanical studies in the tropics that a high proportion of indigenous species are useful, and Indonesia is no exception. In one of the few quantitative studies of use values in Indonesia, Banilodu (Citation1998) found that between 92.3% and 100% of species were useful to people in the six communities around Gunung Mutis forest (Fatumnasi, West Timor). On Timor alone, for example, traditional textile weavers use at least 79 plant species from 38 plant families at different stages of the textile production process (Cunningham et al. Citation2014). So an assumption of 8000 useful plant species in ENT is probably conservative. And there may be more then 50 species with commercial potential. But it is important to focus on 3–5 indigenous species at a time that are most likely to lead to commercially viable new products (). In addition to these indigenous species, there has been a very long history of introduction and adoption of plants into farming systems in ENT, including Areca catechu (pinang), Piper betle (betel vine, sirih) and Aleurites moluccana (candlenut or kemiri) that are traded and have additional potential.

Figure 5. Development over time: five stages of participation in the development of a weavers’ cooperative

What is clear is that strategic choices need to be made (). If the goal is viable enterprises that go beyond subsistence income, then relying solely on participatory processes to identify winning species will be misleading. Some local people are very knowledgeable about local plants. But local villagers cannot be expected to know about external markets or value-added processes, whether these are for avocado oils or polysaccharides extracted from tamarind seeds. Selection of products in demand in external markets requires outside insights coupled with a knowledge of which plant resources are available locally.

Figure 6. Conceptual model for choosing 3–5 species most likely to succeed for enterprise development, from the diversity of species that have traditional uses. Redrawn and modified from the approach used in the natural products enterprise development program of Namibia’s Indigenous Plants Task Team (IPTT).

In order to minimise failure rates, it is advisable to link with existing markets and get business advice on the right products from the right type of business people. Development agencies and donors need to make well-informed decisions that increase the likelihood of enterprise success in the local context and that minimise the fall-out effects of failure. Small businesses anywhere face many challenges, even in urban areas of developed countries, and failure rates are high. Common reasons why businesses fail are a lack of awareness of existing markets, and a failure to produce a product of the right quality, on time, in sufficient quantity, and at the right price. In any society, business failure reduces people’s confidence to try again. In small-scale farming societies where people prefer to minimise risk rather than maximise gain, loss of confidence can be particularly high. Failures also reduce the trust of the business partners.

The costs of doing business in Indonesia are high in comparison to most other countries. Singapore, for example, is the easiest place to do business (ranked 1 out of 189 countries), whereas Indonesia is ranked at 109th (World Bank Citation2016). Research in both developed (Bruderl et al. Citation1992; Stokes & Blackburn Citation2002) and developing (Rogerson Citation2004) countries has assessed why firms fail or succeed, enabling policy makers and small business advisors to better serve the small business sector. Most farmers in ENT are ‘price-takers’, with limited bargaining power. For some products, this needs to remain the case in order for new enterprises to remain competitive; however, in several other cases, value-added processing and price negotiations by business advisors working with producer associations can enable producers to get better prices and returns well above average local daily wage rates.

Market knowledge also extends to an appreciation that there is an internal market within a producer group. In a usual market interaction between smallholder producers and a trader, as sellers and buyer, they will hold different initial positions with respect to the terms of the transaction. The sellers will want to minimise risk to ensure income by being paid in advance or upon delivery at as high a price as possible. The buyer will also want to minimise risk to achieve a profit by paying on consignment or arrears at as low a price as possible. Buyers and sellers negotiate from these positions to find a compromise upon which an agreement can be reached. However, the ability to leverage compromise assumes equal power in the negotiation, and in rural Indonesia this is seldom the case. In order to achieve profits where margins can be wafer-thin, traders establish territories in which they dominate their trade. A Prisoners’ Dilemma-style stand-off (Rappoport & Chammah, Citation1965) results, in which the buyer offers a low, take-it-or-leave-it price because the product he receives is adulterated, and in which the sellers adulterate their products because of the low price they are offered.

A common attempted solution to this dilemma is to increase the sellers’ leverage in the market by organising a community business. Indeed, as a larger seller, the community organisation can reach beyond the local trader into the wider market place and achieve better terms. It is often not appreciated that this solution sets up a new internal market between the community business and its members. The dynamics of this market are slightly different from the open market, as the buyer in this case is working in the seller’s interests. While the seller’s position is unchanged—wanting to minimise risk, maximise income, and get paid at the latest upon delivery—the buyer’s position has evolved. Ideally, the community business will seek not the lowest price possible, but the lowest price it can pay and still ensure delivery of marketable product from its members. The key is for members to see that postponed gratification can become increased gratification. Many community businesses fail because they do not follow this maxim, and allow members to set high prices that mean the enterprise’s margins are so low that cash flow is compromised and insolvency follows. Effectively, the community business then pays members an advance on their dividend before the dividend has even been earned. This occurs because of a failure to recognise that members hold two roles: they are both suppliers to the business and shareholders in the business, and stand to get paid both ways if the business succeeds. First, they will be paid for their product as suppliers. Second, they stand to receive dividends from any profits the business generates.

For the community business to thrive, its members must set optimal prices and agree on optimal terms that balance their short-term personal gain and the long-term financial viability of their enterprise. This negotiation of optimal prices and terms defines the internal market within the community business. The results of this negotiation depend on how members evaluate the risks and rewards of postponing short-term income for long-term profit, and there are three high-probability scenarios under which members will see the risks of postponing their profit as being too high:

Members may look at those organising their community enterprise, or the organisations supporting them, and justifiably prioritise the short-term, having correctly seen that the competence needed to run the business and realise the promised profits are not there.

From past experience, members may surmise that either the support organisation will at some point withdraw, causing the business to fail, or that the more they fail the more support they will get from the support organisation: either conclusion leading to short-termism. Furthermore, if donors and support organisations do not appreciate when above-market farm-gate prices are making a community business unsustainable, they will keep subsidising non-viable enterprises, potentially distorting a market to the detriment of other local producers.

Finally, and most destructively, because long-held habits of mistrusting business and adulterating product can lead to an internalisation of the Prisoners’ Dilemma (Rappoport & Chammah Citation1965), a significant part of the long timeline needed to establish a community business is required for the development of trust within this internal market.

A community business will succeed to the degree to which it can address these three risk scenarios, and a best-fit business model will be one that sets up an internal market that responds well to the external market in which the business is trading.

Trade networks

There is a role for foreign buyers to positively influence trade networks. Almost 20 years ago, Saxenian (Citation1999, p. 54) pointed out how ‘new transportation and communications technologies allow even the smallest firms to build partnerships with foreign producers to tap overseas expertise, cost-savings, and markets’ and that ‘the scarce resource in this new environment is the ability to locate foreign partners quickly and to manage complex business relationships across cultural and linguistic boundaries’. That was Silicon Valley, California—a world away from ENT. Nevertheless, a key lesson from the analysis of Berry et al. (Citation2002) of Indonesian SMEs remains true for NTFPs, including those from ENT. Linking with foreign investors was a key success factor in the wooden furniture, rattan and garment industry sectors (Berry et al. Citation2002), and this applies in ENT to a range of products, such as bamboo laminate production from Flores (see www.indobamboo.com) and traditional textiles (through ToL), to Lygodium basketry marketed out of Tenganan, Bali, where the ‘made-to-order’ approach has brought Japanese design components to Balinese baskets.

There is also power in business groups and co-ethnic networks that can be tapped. Although people commonly think of business groups as a feature of East Asia (the chaebol of Korea or keiretsu of Japan), India (business houses) or Latin America (the Grupos Económicos), they are a global phenomenon (Rauch Citation2001). Indonesia is no exception. The kinship networks of Indonesian Chinese and Javanese businesses, such as the jamu industry (Rademakers Citation1998), or from ENT the trade in bird’s nests, tamarind, candlenuts, sandalwood, Aquilaria resin wood (gaharu) and Helicteres isora, are relevant examples. For smallholder producers outside of these networks, this poses a significant invisible ceiling to vertical integration in existing supply chains. But this is not an insurmountable challenge for three reasons:

All businesses appreciate good quality products, provided at the right time, in sufficient quantity at the right price.

Some highly successful Indonesian businesses that buy plant products, such as the Martha Tilaar Group (MTG), not only buy NTFPs but also pioneered Corporate Social Responsibility in Indonesia (the company founder and chairwoman, Martha Tilaar, helped develop the UN’s Global Compact—the strategic policy initiative coordinated by the former UN Secretary-General Kofi Annan in 2000).

With good products available, it may be possible for researchers in ACIAR-funded projects to help broker and develop relationships that open a market for quality products from ENT with businesses committed to Corporate Social Responsibility, particularly when this substitutes for a product (such as Helicteres isora fruits) that in part is imported from India into Indonesia.

Speed of inventory turnover

Our market research of value chains for tamarind pulp and candlenut kernels in ENT found that many mid-market traders—the kind of trader that the establishment of a producers’ enterprise is intended to cut from the market chain—operate to very fine gross margins and extremely fast turnover times. With gross margins for sub-district or regency-level traders as low as 8% (mixed broken and whole candlenut kernels), they must receive, sort, repackage and ship product quickly (between 12 hours and 7 days) to ensure market price fluctuations do not go against them. Their business models are based on rapid turnover and the compounding of very small profits upon frequent transactions over long periods. Small-scale producers and their businesses have neither the capacity nor the nerve to operate to this model within these constraints. It is therefore necessary to pick products and markets that match the producers’ capacities for delivery fulfilment, and project business development pathways that accommodate likely improvements in fulfilment capability in a realistic way.

Policy and regulation

Strategic policy interventions need to stimulate rather than constrain enterprise development. The opposite is often the case, where policy interventions set in place complex and often costly bureaucratic requirements that are a major barrier to smallholder farmers (Maryudi et al. Citation2015). For PSD to successfully stimulate rural enterprises requires careful navigation between avoiding elite capture (as discussed above), meeting required regulations, and avoiding policy bottlenecks. Although the Millennium Development Goal on the global partnership for development calls for an open trading system that is rule-based, predictable and non-discriminatory, yet one that recognises the special needs of the least-developed countries in relation to tariff-free and quota-free access for their exports, this goal is far from being achieved (IFAD Citation2004). Export success is directly affected by government policies within both producer countries and importing countries, and this needs to be carefully considered on a case-by-case basis. In the case of NTFPs from ENT, for example, policy reforms could encourage import substitution (to stimulate buying of Helicteres isora from ENT rather than India), or reduce shipping insurance tariffs to facilitate export of Borassus palm sugar from Kupang, West Timor, to Australia (Cunningham et al. Citation2011a). Additional examples are technology support and matchmaking with private enterprise partners to add considerable value to low-value products, such as tamarind seeds for commercial extraction of colloids (at present the seeds are fed to pigs), and extraction of gamma-linoleic oils to market as a tropical ‘evening primrose oil’ equivalent from Aleurites moluccana (kemiri) oil currently sold from ENT to national and export markets, which both have potential. Furthermore, donor support can help level this playing field.

Marketing partners

Marketing is more than just promotion. Marketing aims to satisfy customer needs in order to make a profit, to ensure repeat sales, and to develop a pool of satisfied customers who will spread the word about you because they trust you and your products. The four stages of effective marketing are: determining your customer needs and values; analysing your competitive advantage; targeting your market segment; and using your marketing mix of products and services, pricing, distribution systems, and promotion to satisfy customer needs (Dodd Citation1998).

Relevant to the NTFPs and products under discussion, ToL’s experience indicates that there are two significant levels of marketing interaction to consider here. These are between the producers and marketer, and between the market and customers. Together, these two levels require six marketing stages:

Identify customer needs and values.

Identify where producer needs and values are aligned with customer needs.

Engage marketing partners aligned with the needs and values of both customers and producers.

Identify actual or potential competitive advantages of producers and market partners with respect to the customers’ needs and values.

Identify the market segments in which the producers and market partners have a competitive advantage, and develop a strategy for communicating the shared needs and values of producers and marketers to customers in this segment.

Establish a marketing mix (products and services, pricing, distribution systems, promotion) to fulfil these shared needs, communicate shared values, and harness producers’ and market partners’ competitive advantages for the profit of both producers and marketing partners.

The lack of a suitable marketing partner can be a significant barrier to entry for an NTFP product into a marketplace. As we have seen from the examples in the results section, the lack of such a partner is a deal-breaker, while the presence of an appropriate partner can be the key to success.

Producer support

While an appropriate marketing partner is necessary, it is not sufficient for success. It is all very well identifying customers’ needs, but the producers must then go out and fulfil those needs. This is seldom possible without outside support in terms of technical production assistance, financial and business training, producer group facilitation and motivation, and sufficient oversight of producer activities. Such support usually comes from local or international NGOs with donor support, or from government agencies. However, there is often a significant cultural gap between these agents and potential marketing partners. The culture of the marketer addresses the customers’ needs, while the culture of the support organisation addresses the producers’ needs. This can leave the market partner facing in the opposite direction from the producers and their support organisation. Even with shared values, conflict can arise from the support organisation prioritising producer needs, and the marketing partner prioritising customer needs. One can argue about who should turn around to face in which direction, and ideally the chosen marketing partner should be able to face both towards the market and the producer, but the market reality means that it is the support organisations and the producers who must turn around most if they are to sell their products to their intended customers.

It will be seen from the examples cited that the path chosen in this applied research was to engage in business opportunities where the marketing partner is also the producer support organisation: the journey of ToL’s development as a business has been one of also learning to be a support organisation. This is an ideal situation, but it is by no means a requirement for success.

Conclusions

Surveys of informal-sector markets are useful in terms of understanding what people are selling, who is involved in sales, and along which value chains. However, our data from these informal-sector market places showed that most products being sold are not from forests or agroforests, while most of the forest and agroforest products being sold are low entry-point, low-value products, sold as part of a survival or coping strategy. Nevertheless, we were able to identify some products where, with suitable partners and technologies, significant value adding is possible. As Ruiz-Pérez et al. (Citation2004) point out, products sold to specialist markets are characterised by more intensive management with higher incomes to producers. In this case, with indigo and Morinda citrifolia dye sources, there already is intensive management. Also for sandalwood, gaharu, Maclura cochinchinensis (kayu kuning), and Lygodium circinnatum, intensive management and potentially good returns could be realised under the right systems of tenure (i.e. rights of access to resources and/or the land on which those resources occur).

Our experience suggests that identifying winning products that offer opportunities for higher value-adding and higher income requires deliberate matchmaking between entrepreneurs, the appropriate technologies for value-adding, and motivated communities. If donor agencies are serious about a shift to private sector development and public-private partnerships, then they need to focus on addressing the identified barriers to entry that NTFP producers experience when attempting to enter new markets.

Acknowledgements

Funding from the Australian Centre for International Agricultural Research (Project numbers SMAR/2006/011 and FST/2012/039) is gratefully acknowledged, as is the help from the many textile weavers, plant harvesters and informal-sector traders in local marketplaces who continue to provide so much food for thought on the realities of enterprise development in East Nusa Tenggara.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

References

- Arman S. 1996. Diversity and trade of market fruits in West Kalimantan. In: Padoch C and Peluso NL, editors. Borneo in transition: people, forests, conservation and development. 3rd ed. Selangor, Malaysia: Oxford University Press. p. 308–318.

- Banilodu L. 1998. Implikasi Etnobotani Kuantitatif dalam Kaitannya dengan. Konservasi Gunung Mutis, Timor [Unpublished PhD thesis]. [Bogor]: Program Pascasarjana.

- Belcher B. 2003. What isn’t an NTFP? International Forestry Review. 5:161–168.

- Belcher B, Schreckenberg K. 2007. Commercialisation of non-timber forest products: a reality check. Development Policy Review. 25:355–377.

- Berry A, Rodriguez E, Sandee H. 2002. Firm and group dynamics in the small and medium enterprise sector in Indonesia. Small Business Economics. 18:141–161.

- Borin K, Preston TR. 1995. Conserving biodiversity and the environment and improving the well-being of poor farmers in Cambodia by promoting pig feeding systems using the juice of the sugar palm tree (Borassus flabellifer). Livestock Research for Rural Development. 7:25–30.

- Bruderl J, Preisendorfer P, Ziegler R. 1992. Survival chances of newly founded business organizations. American Sociology Review. 57:227–242.

- Conservation International. 2008. Biological diversity in Wallacea. Encyclopaedia of earth. Environmental Information Coalition, National Council for Science and the Environment. [cited 2014 Jul 12]. Available from: www.eoearth.org/article/Biological_ diversity_in_Wallacea

- Cunningham AB. 1990. Income, sap yield and effects of sap tapping on palms in south-eastern Africa. South African Journal of Botany. 56:137–144.

- Cunningham AB. 2001. Applied ethnobotany: people, wild plant use and conservation. London: Earthscan.

- Cunningham AB, Ingram W, Kadati WD, Howe J, Sujatmoko S, Refli R, Liem JV, Maruk T, Robianto N, Sinlae A, et al. 2011a. Hidden economies, future options: trade in non-timber products from forests and agroforestry systems in eastern Indonesia. Canberra: ACIAR Technical Report.

- Cunningham AB, Kadati WD, Ximenes J, Howe J, Maduarta IM, Ingram W. 2014. Plants as the pivot: the ethnobotany of Timorese textiles. Chapter 2. In: Hamilton R and Barrkmann J, editors. Textiles of Timor, island in a woven sea. Los Angeles: UCLA University of California Press.

- Cunningham AB, Maduarta IM, Howe J, Ingram W, Jansen S. 2011b. Di Ambang Kepunahan: proses mordan dengan menggunakan logam dari tumbuhan dalam pembuatan kain tradisional di Indonesia. Economic Botany. 65:241–259.

- Dalibard D. 1999. Overall view on the tradition of tapping palm trees and prospects for animal production. Livestock Research for Rural Development. 11. Available from: http://lrrd.cipav.org.co/lrrd11/1/dali111.htm

- Davis TA, Johnson DV. 1987. Current utilization and further development of the palmyra palm (Borassus flabellifer L., Arecaceae) in Tamil Nadu state, India. Economic Botany. 41:247–266.

- Department of Foreign Affairs and Trade (DFAT). 2015. Aid investment plan: indonesia 2015/16 – 2018/19. Australian Government, Department of Foreign Affairs and Trade, Canberra. [cited 2016 Jul 26]. Available from: http://dfat.gov.au/about-us/publications/Documents/indonesia-aid-investment-plan-2015-19.pdf

- Dodd G. 1998. Business basics: a microbusiness startup guide. Oregon, US: Oasis Press.

- Fox JJ. 1977. Harvest of the palm: ecological change in eastern Indonesia. Cambridge Massachusetts: Harvard University Press.

- GERES. 2009. Vattanak stoves to improve palm sugar producers’ livelihood. Available from: www.nexus-c4d.org/projects/project/9-vattanak-stove