Abstract

The puzzle of how Nokia lost the smartphone wars has intrigued recent scholarship. Despite Nokia’s dominant position in the mobile phone industry and its technological capabilities and reputation for strategic agility, it was completely wiped out from the market, only a few years after the launch of Apple’s iPhone. The article provides a comparative, historical and institutional account on the smartphone industry by focusing on three key players: Nokia, Apple, and Samsung. This perspective enriches earlier accounts that were overly focused on explaining Nokia’s decline by looking at internal organisational design and conflicts. We propose a two-pronged explanation focused on the reconfiguration of industry platforms and financialisation. The article suggests that single company histories could be enriched by integrating a comparative perspective that examines additional cases. We discuss opportunities for further research to understand how success or failure in technological innovation is embedded in a wider societal and institutional context.

1. Introduction

Nokia appears as an intriguing puzzle of corporate failure in the mobile phone industry. The company was well endowed with resources for technological innovation, as it was embedded in the Finnish innovation system (Castells & Himanen, Citation2002); it was well ahead of competitors in the industry (Giachetti & Marchi, Citation2010); and was hailed as an exemplar of ‘strategic agility’ (Doz & Kosonen, Citation2008). Nokia managed to successfully navigate intense technological change in the industry for nearly two decades and became a pioneer in smartphone devices starting with the Nokia Communicator in 1996. Yet, only a few years after the release of Apple’s iPhone in 2007, Nokia’s position dramatically declined and the company exited the industry in 2014 (Lamberg et al. Citation2021).

Several scholarly and popular works have attempted to explain this puzzle. We group these explanations into two broad categories.Footnote1 The first one alludes to the role of technological innovation and specifically Apple’s superior products and innovative capabilities. It attributes the decline of Nokia to its technological choices and reduced capabilities for innovation (Ali-Yrkkö et al. Citation2013; Lamberg et al. Citation2021). Seen from this perspective, Nokia’s corporate failure is a result of new and more innovative technology replacing older technology (Ali-Yrkkö et al. Citation2013; Van Rooij, Citation2015). The sunk costs in the Symbian OS, and an inability to come up with an iPhone alternative, are considered as profound contributors to Nokia’s decline (Lamberg et al. Citation2021).

These arguments have some plausibility, but they are deemed a priori as insufficient explanations, as they suffer from an implicit technological determinism. They perceive corporate success as a relatively deterministic outcome of better technology that wipes out alternatives. Yet, business historians know all too well, from the triumph of VHS over Beta (Cusumano et al. Citation1992) and Apple over Xerox (Graham, Citation2017), that being a technological pioneer is not a necessary and sufficient condition for success; there are also ‘bandwagon effects’ (Cusumano et al. Citation1992, p. 56) and fast followers that compete for success. In addition, technologically-focused explanations tend to downplay the wider institutional context and, specifically, the role of institutions, networks, and their underpinning relations of power (Dobbin, Citation2005; Graham, Citation2017).

The second group of explanations alludes to intra-organisational design issues and conflicts, which tend to focus heavily on Nokia’s internal problems. Doz and Wilson (Citation2017, pp. 111–131) emphasise the failure of the matrix organisational structure creating silos and barriers to innovation, which spurred internal conflicts, constant reorganisation and inefficiencies. Similarly, as Lindén (Citation2021, p. 202) puts it, Nokia ‘… was a company plagued by bureaucracy and turf wars, where important concepts, such as agile and lean, were memories of the past’. Vuori and Huy (Citation2016) tend to overplay the culture of ‘fear’ and the leadership’s aggressive temper as the root cause of Nokia’s failure. Finally, Lamberg et al. (Citation2021) also assign blame on faulty management and leadership decisions, internal infights, bad communications, and more generally the ‘disunited’ organisational design.

The problem with these explanations is that they seek to analyse the case of Nokia in isolation from its external environment. Although the strategic choices of individuals are important, they tend to ignore or downplay the role of contextual factors. Departing from this perspective, we argue that business history narratives about corporate success and failure (Graham, Citation2017; Van Rooij, Citation2015) need to be enriched with comparative perspectives that integrate the interplay between actors’ strategies and the competitive and institutional environment (Kornelakis, Citation2015, Kornelakis, Citation2018, Whitley, Citation2010).

Against this backdrop, we examine Nokia in a comparative perspective and put forward an alternative explanation that is two-pronged. First, we bring to the fore the innovation-finance nexus (Lazonick, Citation2008, Citation2010) understood as the trade-off between spending resources on R&D and spending to boost shareholder-value. Financialisation as a concept has many different dimensions and manifestations (Dore, Citation2008; Gospel et al. Citation2014; Lazonick, Citation2010), but our approach coheres with Lazonick’s (Citation2010, p. 680) definition of the concept:

…By financialization, I mean the evaluation of the performance of a company by a financial measure, such as earnings per share. The manifestation of the financialization of the U.S. economy is the obsession of corporate executives with distributing “value” to shareholders, especially in the form of stock repurchases, even if they accomplish this goal at the expense of investment in innovation…

Second, we bring in the role of industry platforms and the power relationships between key actors. This concept draws on the innovation ecosystem approach, and an industry platform is defined as:

the foundation upon which outside firms can develop their own complementary products, technologies or services. (Gawer & Cusumano, Citation2014, p. 418)

2. Research design and methods

To understand how Nokia moved from a tremendous success to a colossal failure, our overall research design follows the comparative method (Mahoney, Citation2004; Ragin, Citation1987), looking also at the cases of Apple and Samsung. Samsung’s experience helps us to take a first step considering how could Nokia’s performance have evolved, had it taken steps to access the new platform through an alliance with Google, while Apple’s case is important as it reshaped the entire industry of smartphones. The analysis of the different conditions that led to variable outcomes is based on non-probabilistic logic of necessary and sufficient causes (Mahoney, Citation2000). The comparative method sheds light on the companies’ wider environment and therefore pushes historians away from explanations focused on the role of individuals. For instance, Elop, who was the last CEO of Nokia, was accused of being an ineffective and poor leader or even as conspiracy theoristsFootnote2 suggested ‘a Trojan horse sent by Steve Ballmer of Microsoft’ (Lindén, Citation2021, p. 205). By using the comparative method, we move beyond the heroic role of CEOs and focus our attention on how strategic choices interacted with other actors’ behaviour in the broader institutional environment.

The case selection is theoretically motivated and historically informed. The three companies were embedded into significantly different institutional contexts from which they drew resources, especially relying on R&D investment patterns in their national innovation systems (Miozzo & Walsh, Citation2006, pp. 141–165) to boost their technological capabilities and competitiveness. Drawing on the comparative capitalism literature (Dore et al. Citation1999; Hall & Soskice, Citation2001; Whitley, Citation2010; Witt et al. Citation2018), we explore the key players in their contexts: Nokia in the context of Nordic capitalism (Fellman et al. Citation2008; Moen & Lilja, Citation2006); Apple in the context of US capitalism (Lazonick, Citation2010; Whitley, Citation2011); and Samsung in the context of South Korean capitalism (Murillo & Sung, Citation2013; Witt, Citation2014). We also document that Nokia was the first mover in smartphones, but Apple disrupted the industry via ‘architectural innovation’ (Henderson & Clark, Citation1990), while Samsung was a fast follower to Apple’s disruption, thus providing a useful comparator case to Nokia.

The data and sources for this article come from a wide range of primary and secondary sources. For Nokia, we reviewed fifteen works looking either at Nokia’s success until mid-2000s (Ali-Yrkkö & Hermans, Citation2002; Castells & Himanen, Citation2002; Doz & Kosonen, Citation2008; Giachetti & Marchi, Citation2010; Häikiö, Citation2002; Moen & Lilja, Citation2006; Skippari & Ojala, Citation2008; Solvell & Porter, Citation2011) or recent work trying to explain Nokia’s rapid decline (Alcacer et al. Citation2014; Ali-Yrkkö et al. Citation2013; Argyres et al. Citation2019; Doz & Wilson, Citation2017; Laamanen et al. Citation2016; Lamberg et al. Citation2021; Lindén, Citation2021; Siilasmaa, Citation2018; Van Rooij, Citation2015; Vuori & Huy, Citation2016). We reviewed ten additional works for the secondary cases: Apple and Samsung (Cain, Citation2020; Chandler et al. Citation2005; Froud et al. Citation2012; Kahney, Citation2013; Khanna et al. Citation2011; Kong, Citation2011; Lazonick et al. Citation2013; Song et al. Citation2016; Yoffie & Slind, Citation2007; Yoo & Kim, Citation2015). Further, we complemented the existing works with a range of primary documentary sources. We relied on archives from major databases with press articles (Factiva and ProQuest), and reviewed more than 60 articles and media interviews, spanning a period from 1988 to 2018, including reputable sources such as: The Economist, The Wall Street Journal, Bloomberg, and Forbes. We also consulted industry reports, annual reports, press releases and announcements from Nokia, Apple, Samsung, Moody’s, and Fitch Ratings. Finally, we relied on historical data of global market shares from Statista (1997–2014) and credit ratings from Standard & Poor’s (1993–2013) and Fitch (2006–2016).

To analyse our cases we followed the method of historical process-tracing (George & Bennett, Citation2005, pp. 205–232; Hall, Citation2006). The aim was to accurately represent the sequence of events and interactions between key actors and to construct the ‘narrative’ of corporate success and failure (Popp & Fellman, Citation2017; Rowlinson et al. Citation2014). Theoretically, we started from the conceptual lenses of comparative capitalism (Witt et al. Citation2018), the innovation-finance nexus (Lazonick, Citation2010; Whitley, Citation2010), and industry platforms for ecosystem innovation (Gawer & Cusumano, Citation2014) to understand how the context influenced the industry dynamics and final outcomes. Complementary explanations were grouped together to form the set of competing explanations, and theory-based alternative explanations were developed.

The analysis stage was an iterative process between data and sources, on the one hand, and existing explanations and alternative hypotheses, on the other. We read and reread the data and existing works to engage in a dialogue between theory and evidence. After several iterations and following the model of narrative organisational history (Rowlinson et al. Citation2014, p. 260) we represent the historical events, and the construction of the narrative led us inductively to our proposed explanations. The ability to navigate the pressures of financialisation, and the power shift between industry platforms, both overlooked contextual factors by earlier literature, not only help explain Nokia’s fall, but also Apple’s and Samsung’s success.

Finally, the timeframe of the article is grounded in the period between 1996 and 2014. In 1996 Nokia launched the Nokia Communicator, which was the first ever technological innovation that combined a telephone and a wide screen, with capabilities for internet and email. It is widely considered as the precursor to contemporary smartphones also by Häikiö’s official history of NokiaFootnote3 (Häikiö, Citation2002, pp. 42–43). By 2014 Nokia exited the smartphone industry. The start and end point clearly delineate the timeframe of the analysis. For the construction of the narrative we take a periodisation approach (Rowlinson et al. Citation2014, pp. 258–259) into three distinct periods: 1996–2002: the period when Nokia had the ‘first mover’ advantage in technological innovation; 2002–2008: the period when Apple started developing a new product until it launched the first iPhone; and 2008–2014 the period when Nokia failed to launch an ‘iPhone-killer’, whereas Samsung succeeded.

3. Historical background

Nokia was founded in 1865 as a timber company, grew into a pulp and paper manufacturer and by the late 1960s merged with Finnish Cable Works stepping into electronics (Van Rooij, Citation2015, p. 209). The company produced the first radiotelephones for the police, fire brigade and armed forces (Alcacer et al. Citation2014) and in 1979 established a joint venture, Mobira Oy, to develop mobile phone handsets. Transnational regulation helped in the early years, as the 1981 launch of the Nordic Mobile Telephone (NMT) network, which was the first transnational mobile network, gave Nokia (Finland) and Ericsson (Sweden) a head-start in penetrating the global market for mobile handsets (Burton, Citation1991). In 1982 Nokia introduced the world’s first car phone for the NMT analogical standard (Lamberg et al. Citation2021, p. 578).

Nokia foresaw the opportunities that the new regulatory landscape presented, and decided to proceed with the mobile phone segment, despite making losses in the early years. It was riding on the wave of introduction of the GSM standard in Europe, which was later followed by other regions in the rest of the world (Rowlands, Citation1990). In 1992, the CEO Jorma Ollila made the strategic decision to create a new Nokia and the vision for reinventing the Finnish conglomerate was to reposition it as a global telecom company focused on high value-added products (Moen & Lilja, Citation2006). The company launched the Nokia 1011, which was the first mass produced GSM (2G) phone, and partnerships with other actors in the industry were important at this early stage. Nokia allied itself with the US-based AT&T to develop technology for digital signalling; but also new entrants among mobile operators, like Orange in Britain and E-Plus in Germany (later acquired by Telefónica) and competed aggressively with traditional telecom suppliers (Fox, Citation2000).

The early seeds of the financialisation of the company can been traced at this point. Nokia needed big money fast and the place to find such money was the US financial system. Nokia started with a $100 m placement with a few US institutional investors in 1993 (Dahl, Citation1993). Then, in 1994 it raised about $415 m in new capital through an offering of new shares, making Nokia the first Finnish company to be listed on the NYSE (Reuters, Citation1994). To strengthen its focus on core consumer electronics, the company got rid of other segments (e.g. rubber and toilet paper) despite being profitable (Pope, Citation1994). By 1997 most Nokia shares have been in American hands. As the share price increased by a staggering 2,300% in just five years, it was evidently ‘a wonderful ride’ for the shareholders (Fox, Citation2000).

In the meantime, the pattern of innovations continued. In 1994 the company launched the first phones to enable Nokia ringtones and dynamic soft keys, as an innovative user interface. For the funding of these innovations, Nokia benefitted significantly from resources available in the Finnish innovation system, especially from Tekes and Sitra. Tekes and Sitra formed an institution that helped innovation in the country, holding the role of the ‘biggest venture capitalist in Finland’ (Castells & Himanen, Citation2002, pp. 50–54). Funding from Tekes contributed annually to Nokia’s R&D expenditure, although the level of funding was more significant in the early years, and decreased as Nokia became a global giant. In 1980 Tekes funding comprised 26.3% of Nokia’s total R&D expenditure, in 1991 Tekes funding stood around 5% and by 1999 it dropped to 1% of total R&D (Ali-Yrkkö & Hermans, Citation2002).

Samsung entered the market of mobile handsets in 1988 launching its first mobile phone, the Samsung SH-100. Samsung Electronics was founded in 1969 and quickly became one of the most important chaebols in Korea, as the ‘company alone accounted for 20% of Korean exports’ (Witt, Citation2014, p. 221). Naturally, it benefitted from the system of government subsidies, which rewarded good export performance (Murillo & Sung, Citation2013). In the global mobile industry, however, the company was a ‘follower’, and the ‘Big 5’ were Nokia, Motorola, Ericsson, Panasonic and Siemens (Giachetti & Marchi, Citation2010). Samsung wanted to move up-market, but production quality issues hindered this move. In 1995 almost one in eight Samsung phones produced were faulty and had to be returned to carriers or the manufacturer (Cain, Citation2020, p. 90). Hence, Samsung seemed an unlikely contender for Nokia’s dominance.

Financialisation hit Samsung as well in the 1990s. Amid the 1997 Asian economic crisis, Samsung was deep in debt and was heading towards bankruptcy. Bankruptcy of one of the big chaebols was unthinkable, and to avoid this Samsung was forced to undertake a massive restructuring. The South Korean government’s medicine to treat the diseases of overcapacity and over-indebtedness included allowing a maximum debt-equity ratio of 200% (Witt, Citation2014, p. 219), swapping businesses between chaebols and forcing the banks to forgive debt (The Economist, Citation1998). Around 30% of employees lost their jobs as the company slimmed down and sold more than 100 businesses, as part of the government program to lower debt-to-equity ratios (The Economist, Citation2005). Samsung’s reliance on bank debt and government support was an important buffer to protect the company from the upheavals in global financial markets, a cushion for financialisation, which helped the company later.

4. The early smartphones period, 1996–2002

4.1. Nokia

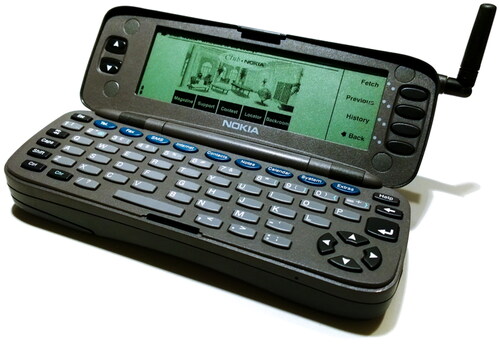

In 1996 Nokia launched the Communicator 9000, which is one of the first devices that combined a Personal Digital Assistant (PDA) and a mobile phone. The Nokia Communicator ‘was a totally new mobile phone concept’ and included voice, data and telecom features that made it a real ‘pocket computer’ (Häikiö, Citation2002, p. 43). The strong emerging trend towards the ‘digital convergence’ of mobile phones; computers and TV into some type of ‘information appliance’ was part of Nokia’s strategic priorities. By 1998 the company was the indisputable global leader in the mobile handset industry, surpassing Motorola (Fox, Citation2000) ().

Figure 1. The first Nokia smartphone, Nokia 9000 Communicator. Source: https://commons.wikimedia.org/wiki/File:Nokia_Communicator_9000_Opened_01.jpg. CC-BY

In 1998 Nokia co-founded Symbian to create a new Operating System for PDAs and ‘smart’ mobile phones. Symbian Ltd. was a platform in partnership with other key actors: Psion, Nokia, Ericsson, Motorola and Sony, not only to prepare the ground for the digital convergence, but also as a joint effort to prevent Microsoft from extending their Windows monopoly into mobile devices (Greene et al. Citation2001). Interestingly, at the time the threat seemed to come from Microsoft rather than Apple.

By 2001 Nokia’s turnover increased five times; from €6.5bn to €31bn in five years (Fox, Citation2000). The company was well ahead of the game in technological innovations, it released the Nokia 9210 Communicator running Symbian OS. The product innovation momentum continued and in 2002 it launched the first camera phone, the Nokia 7650. Nokia was the largest smartphone hardware maker and Symbian the largest software maker in the world and in 2002 it co-founded the Open Mobile Alliance (OMA) as an international industry platform to develop open standards for the global mobile phone industry (Greene et al. Citation2001). While Nokia was the platform leader of the OMA network, other key actors included the incumbent telecommunications firms (AT&T, NTT, Orange, T-Mobile, Verizon); equipment and mobile systems manufacturers (Ericsson, ZTE, Nokia, Qualcomm, Rohde & Schwarz); and some smaller software firms (Grøtnes, Citation2009).

The seeds of financialisation had already grown roots during this period and resulted in significant ownership change, assisted also by the Finnish capital market’s liberalisation of the 1980s. Traditionally, Nokia owners included Finnish institutional investors, such as Finnish banks owning major stakes and holding seats in the company board, but ownership shifted to US institutional investors (pension funds) and retail investors. Indicatively, the number of individual US retail shareholders jumped from an initial number of 30,000–1.5 m by the second half of 2001 (Häikiö, Citation2002, pp. 219–221). The changes in ownership created a critical juncture, that shifted from ‘patient capital’ of the Finnish institutional investors and banks, to the primacy of US shareholders. This is further warranted by former CEO Ollila, who already in the late 1990s expressed concerns that the changes deprive the company of a ‘safe haven’, a shelter against storms in equity markets, which were driven by share price development, dividend pay-out and analysts’ recommendations (Häikiö, Citation2002, p. 221).

4.2. Apple

A series of unsuccessful initiatives and mistakes diminished Apple’s market share in the computer business, and in early 1996, the press reported that Apple was desperately looking for a buyer (Mossberg, Citation1996). In December 1996, Apple announced that it would acquire NeXT Software and Steve Jobs would return to Apple (Lohr, Citation1997). NeXT’s operating system, was a promising solution to Apple’s problems and difficulties with its operating system (Yoffie & Slind, Citation2007). While the media and press has over-played the role of Steve Jobs in turning around Apple (The Economist, Citation2007), solid academic research has debunked this myth, showing that the US innovation system has played a significant role in taking the risks for these innovations, since ‘virtually every technology that one finds in an Apple iPod or iPhone, originated in a government-run or government-funded investment project’ (Lazonick et al. Citation2013, p. 264). Following the return of Jobs, one of the first moves was to make an alliance with an ex-archenemy, Microsoft. On 6 August 1997, it was announced that Microsoft had agreed to invest $150 m in Apple and had also reaffirmed its commitment to develop products such as MS Office for the Mac (Yoffie & Slind, Citation2007).

Apple might appear at first glance as an irrelevant player for the mobile phones market. But the commercial success of the iPod, which helped to revive Apple, was clearly a product that was part of the ‘digital convergence’. Along with others in the industry, Apple was conscious that consumers would want one device to replace an MP3 player, phone, and BlackBerry and that other devices would begin to add MP3 features, as competitors were moving to that direction, e.g. Palm with its Treo 600, which combined a phone, PDA and BlackBerry all in one (Vogelstein, Citation2008).

Apple first considered developing a phone in the early 2000s, but it stumbled upon some overwhelming technical obstacles. The speed of mobile data was slow, and a new operating system (OS) was needed for such a device. Nokia was ahead of the game with the Symbian OS. Apple had ‘sunk costs’ in the operating systems for iPod and Mac to start with. But it was difficult to adopt iPod OS for networking and advanced graphics, while OS X would not run on a mobile chipset. Another obstacle was posed by the phone carriers, who were powerful actors and had very specific views about value-creation. They viewed handsets as ‘cheap, disposable lures, massively subsidised to snare subscribers and lock them into using the carriers’ proprietary services’ (Vogelstein, Citation2008). At the time, it seemed that Apple encountered significant barriers to enter the mobile phone market.

4.3. Samsung

In 1998 Samsung sought to expand in the US market and focused their strategy on winning over carriers. While Nokia was spearheading phones compatible with the GSM standard, Samsung had gained expertise in making phones compatible with the CDMA standard after the South Korean government funded the construction of a CDMA network. Sprint was the first carrier to build its own CDMA network in the US and Samsung signed a $600 m deal for 1.7 m phones with them (Cain, Citation2020, p. 123). Samsung launched the SCH-3500, which had a ‘unique curvy flip-up earpiece clipping to the display’. Though it sold poorly in Europe and South Korea, Sprint and Samsung’s American executives liked the design, and they signed a deal to buy about 3 m handsets from Samsung. It was popular with consumers and would go on to sell more than 6 m units over the next couple of years. This prompted other American carriers to become more interested in partnering with Samsung (Cain, Citation2020, p. 129).

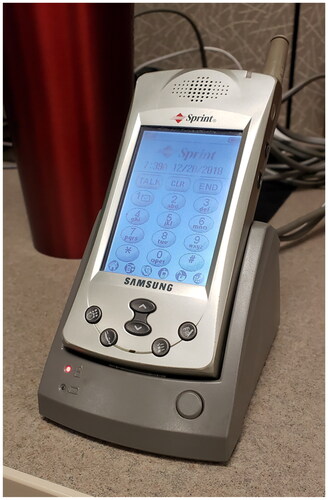

Like Nokia and Apple, Samsung was also aware of the ‘digital convergence’ trend and that the mobile phone will emerge as a central device in the future. In 1999 Samsung launched the world’s first MP3 mobile phone (SPH-M2500) and developed a prototype of a wireless Internet phone (smartphone) which was released two years later as Samsung SPH-i300. There were some home-context advantages that helped Samsung. South Korea was one of the most wired countries in the world; providing the advantage of testing new digital technologies (The Economist, Citation2005). Samsung was also shielded from the shareholder value pressures in the US stock market, as it maintained its stock market listing in South Korea ().

Figure 2. The first Samsung smartphone, Samsung SPH-i300. Source: https://commons.wikimedia.org/wiki/File:SPH-I300.jpg. CC-BY

The conglomerate structure of Samsung as a chaebol meant that it was well prepared for the convergence, as different divisions held expertise and know-how for different parts required for a smartphone. Samsung was a pioneer in hardware components such liquid-crystal displays (LCD) and flash memory chips, which became so important in smartphone devices (The Economist, Citation2011b). When Sony’s CEO Nobuyuki Idei announced in October 2003 that Sony would join Samsung in a joint venture to produce LCD screens, it was a move that would have been unthinkable some years earlier (Cain, Citation2020, p. 141). While Samsung was competing with Nokia on mobile phone handsets, it was also competing with LG-Phillips on LCD screens; with AMD/Intel on flash memory chips; and Samsung itself was a supplier to both Nokia and Apple. The chaebol structure served Samsung well in terms of pooling resources and bailing out the mistakes of unprofitable ventures with profits from their successful businesses (Khanna et al. Citation2011); patient family-controlled governance and weak shareholder pressures (The Economist, Citation2011a). Unlike many of its competitors, which preferred to source components from outside suppliers, Samsung was more vertically integrated, supplying its own needs or buying from closely associated group firms (The Economist, Citation2005). This turned into an immense advantage as digital convergence blurred product categories.

5. The smartphone wars, 2002–2008

5.1. Nokia

Since 2002, Nokia was essentially locked into two networks: the Symbian OS partnership and the Open Mobile Alliance (OMA). While the OMA-Symbian platform was driven by handset manufacturers and phone carriers (Lamberg et al. Citation2021, p. 582) the power was gradually shifting to software firms and app developers. Still, Nokia was technologically ahead of its time. As the former CEO Ollila mentioned in an interview ‘We had exactly the right view of what it was all about…We were about five years ahead’ (Troianovski & Gundberg, Citation2012). Indeed, in 2004 Nokia released the first 3 G smartphone and launched Nokia 7710, which was the first smartphone with a touchscreen (). Those innovative devices were released three years earlier than the Apple iPhone with 2 G capabilities.

Figure 3. The first Nokia with a touchscreen, Nokia 7710. Source: https://commons.wikimedia.org/wiki/File:Nokia_7710.png. CC-BY

Despite Apple’s famed secrecy, Nokia engineers were aware of the iPhone, at least one year before its launch (Vuori & Huy, Citation2016, p. 22). However, the relationships between key actors proved more important than technological innovations. The disruption brought by Apple’s iPhone destabilised the longstanding relationships between Nokia and carriers, as it changed the way carriers perceived mobile phones and the overall business model of the industry. This was a turning point for Nokia’s old networks and undermined the ‘strong ties’ between handset manufacturers and carriers, as it reduced the importance of exclusivity of handsets. Watching the tremendous success of Apple’s iPhone, other carriers were suddenly looking to their partner manufacturers for competitive smartphones. The focus of the manufacturers shifted from building phones to fit the carriers’ specifications towards building phones that appeal directly not only to users, but also to app developers (Vogelstein, Citation2008).

The power relations in the industry were shifting rapidly, as the standardisation of wireless networks was shifting from industry platforms based on carriers to platforms based on software companies (Grøtnes, Citation2009). This meant that carriers lost their power over content and standards and retained only control over delivery (Vogelstein, Citation2008). Instead, the big software firms emerged as key players in setting standards and content, and Google was a new entrant with a very dynamic product (Android) backed up by the network of Open Handset al.liance. To be precise, Android had a unique ‘openness’; it was adequately open for app developers to create their apps, but Google retained a tight grip on the core OS and did not allow handset manufacturers to come up with ‘forked’ versions.

5.2. Apple

Apple’s innovations started with the touchscreen. In 2003 it developed a multi-touch prototype tablet known as Model 035, just as an input device for the Mac (Kahney, Citation2013). It was one of the first ‘capacitive’ displays linked to a projector, which was then shrunk to a 12” MacBook display, a patent which was filed in early 2004 (Kahney, Citation2013). Up until then most touchscreen technology relied on ‘resistive’ displays, which used pressure for input (e.g. pens). But the innovativeness of capacitive displays enabled a much better user experience as they used the conductive touch of a human finger for input.

In 2004 Apple gathered two teams to work on the highly confidential ‘Project Purple’. The P1 team led by Tony Fadell (head of iPod) tried to build an iPhone by adding networking capabilities to an iPod, adapting the software, and adjusting the click-wheel design (Vogelstein, Citation2017). The P2 team led by Jony Ive with Scott Forstall began by shrinking Mac OS X to run on a smaller device with memory, battery, and processing constraints (Vogelstein, Citation2017), but after six months the P1 project was cancelled and folded into P2 (Kahney, Citation2013). As we will discuss later this casts doubt to explanations of Nokia’s failure, because of a ‘disunited organisational design’ with too many teams working on competing projects. Apple was also working in parallel on competing projects, and so did Samsung.

In February 2005 Jobs approached Cingular to make a partnership for a new high-end smartphone (Richtel, Citation2007). Apple offered to sign an exclusive deal to Cingular but wanted to retain control of the device, and even threatened to walk away and become a (competitor) virtual mobile network operator. Cingular were attracted by a growth in data sales (more profitable at the time than selling minutes) and the idea of attracting new customers to their network with a standout device. From the options available in the US market, Apple also preferred Cingular as a partner. Verizon were unwilling to cede control to Apple, T-Mobile was too small, and Sprint’s network used the CDMA technology, while the GSM technology (used by Cingular) was more popular globally (Cohan, Citation2013).

In the same period, Apple failed in a joint venture with Motorola and continued to struggle with the design of the iPhone. The iPhone team tried several different designs including a prototype with a split screen and used the capacitive touchscreen of trackpads to phones. Apple was very innovative in sourcing materials and innovative components to enhance the design and the user friendliness. It found a Taiwanese company called TPK which was producing transparent capacitive touchscreens and asked them to scale up production (Kahney, Citation2013). TPK invested $100 m in this and supplied 80% of the first iPhone’s screens. Apple also switched from using plastic to glass -supposedly after Jobs complained that the plastic display scratched too easily.

As of Autumn 2006, the iPhone was still buggy and dysfunctional from a hardware and software view with dropped calls, battery issues, and crashing apps. This prompted a stressful and frantic push with increased overtime (Vogelstein, Citation2008). Apple and Cingular/AT&T reached an agreement in mid-2006, giving Apple complete control over the device in return for exclusivity on their network and a revenue sharing agreement for device sales and phone contracts (Cohan, Citation2013). Other manufacturers had to follow detailed manuals on how phones should be designed according to the carrier’s specifications (Guglielmo, Citation2013). So, this is another turning point for the industry, since up until that time, carriers were both a source of content for smartphones as well as the provider of the infrastructure. Cingular (AT&T) gave up this control in return for revenue from an increase in mobile data usage and approved the deal without ever having seen an iPhone prototype (Richtel, Citation2007).

Apple turned to Samsung as their supplier, with the specifications for their desired iPhone chip (CPU) and asked Samsung to create one in just five months. Samsung did not know that this was to be used for the iPhone but responded by meeting the ‘impossible’ deadline and shipping the chips two months before the announcement in January 2007. Apple engineers admitted that without Samsung’s expertise and speed in designing the main processor, the iPhone would not have launched on time (Cain, Citation2020). On 9 January 2007 Steve Jobs announced the first iPhone and an intention to capture 1% of the global market for phones (10 m units) by the end of 2008 ().

Figure 4. The first Apple smartphone, the iPhone. Source: https://commons.wikimedia.org/wiki/File:IPhone_First_Generation.jpg. CC-BY.

The phone was clearly targeting the high-end range of the market and was available starting at $499. Tech expert reviewers wrote dithyrambic articles praising the software, the touch interface, web browser, and overall describing it as a ‘breakthrough handheld computer’ (Mossberg & Boehret, Citation2007). Among other things, they emphasised that switching to the iPhone and learning how to use it felt fun and lived up to the hype (Levy, Citation2007).

By November 2007 Apple had already sold 1.4 m iPhones in the US and by the end of the year it had sold 3.4 m iPhones (Vogelstein, Citation2017). For AT&T it was a huge success; 40% of iPhone buyers were new customers to AT&T, and the iPhone had tripled the carrier’s volume of data traffic, while AT&T and Verizon announced that any compatible handsets can be used on their networks and consumers would no longer be limited by exclusivity (Vogelstein, Citation2008). Apple had changed the business model of the industry from one focused on handsets and minutes, to one focused on software apps and data.

5.3. Samsung

In the smartphone arena, Samsung launched the BlackJack smartphone in November 2006 on Cingular (later renamed to Jack after a lawsuit from RIM/Blackberry) and was well reviewed by tech experts (Gade, Citation2006). It was among the first 3 G smartphones offered by Cingular and helped to cement Samsung’s relationship with the carrier (Cain, Citation2020, p. 131). In the meantime, Samsung was already supplying Nokia, Sony, and Apple with memory chips, which were often customised to a company’s specific requirements (The Economist, Citation2005) and gained expertise in an important component.

It is important to stress that Samsung’s innovations helped to deliver the iPhone, for example, the flash memory chips. In 2005 Samsung’s Hwang Chang-Gyu, president of the semiconductor and memory business, travelled to Palo Alto with two fellow executives to show Samsung’s new NAND flash memory to Steve Jobs and Apple (Cain, Citation2020, p. 150). Flash memory was more durable and less power-hungry, and Steve Jobs was persuaded to include it in iPods for which Samsung became the sole supplier of flash memory and later managed to manufacture the iPhone CPU chip in just five months.

Interestingly, Samsung was offered the opportunity to acquire the Android smartphone OS. Android Inc. was founded in Palo Alto, California in 2003 and the following year Android Inc. led by Andy Rubin offered to sell their new operating system to Samsung. But their offer was declined, Samsung did not believe that such a small start-up could build a new operating system (Cain, Citation2020, p. 209). Instead, Google acquired Android in 2005, and developed its own Google Chrome browser in 2008. Google realised that the mobile phone became a more important Internet gateway and, to ensure prominent placement with users, developed Android into a low-cost, open-source OS for smartphones, which it then provided free of charge to mobile handset manufacturers. Google did not profit directly from Android OS; rather, it profited by making Google search the default for phones running Android. As one tech expert reviewer wrote, ‘Android would be a Trojan horse for Google’s consumer apps, chief among them mobile search’ (Amadeo, Citation2018). As with other ‘free’ services, like price comparison, Google used these products to monetise the users’ data and improve their advertising revenue (Kornelakis and Hublart, Citation2022).

Whilst Samsung refused to buy the Android OS, it joined the Open Handset alliance, which was formed on 5 November 2007. Google was the platform leader, and mobilised several actors in the new network, device manufacturers such as HTC, Motorola and Samsung, wireless carriers such as NTT, Sprint, Deutsche Telekom/T-Mobile, China Mobile, Telecom Italia and Telefónica, and chipset makers such as Qualcomm and Texas Instruments, who became partners to promote Android (Grøtnes, Citation2009).

Samsung was unique in its strategy to develop handsets for a very wide variety of OS platforms. It was making phones using Symbian (up until 2010); Google’s Android (Samsung was a founding member of the OHA); Samsung was developing its own OS (Bada, later folded under Tizen); launched handsets in Microsoft’s Windows Phone (despite Microsoft’s strategic partnership with Nokia); adopted Qualcomm’s BREW OS; and finally took over of Intel’s MeeGo following Nokia’s abandoning of the partnership (later also folded under Tizen) (Vakulenko et al., Citation2011). In other words, Samsung not only tried to build its own in-house OS platform; but also had its foot in the door of every single OS that was up for grabs. This suggests again that there were multiple competing projects with different OS/hardware combinations and casts doubt on the ‘sunk costs’ in embedded technologies explanation of the fall of Nokia. Samsung also had sunk costs in many different projects, included a home-grown OS (Bada/Tizen) but this did not deter the company from launching a successful alternative to iPhone.

6. The endgame 2008–2014

6.1. Nokia

The Symbian-Nokia industry platform began to disintegrate, because of the dual assault from the competing Apple and Google platforms. Some of the key players like Motorola and Psion had already jumped ship from Symbian and were now part of the Android network as an OHA founding member in 2007. Sony-Ericsson moved to OHA in 2008. The same year Nokia acquired the remaining shares of partners in Symbian (West & Wood, Citation2014). In 2010, Samsung cancelled Symbian plans, leaving only Nokia as the licenced handset maker in the Symbian Foundation. Despite the early innovativeness of Symbian OS, it was a clunky platform to develop apps, and app developers had started moving to the more attractive platforms of Apple’s iOS and Google’s Android (Lamberg et al. Citation2021, p. 586).

Nokia was however very much locked into it and tried to launch several ‘iPhone-killers’ running Symbian: the Nokia N95 in 2007; the Nokia 5800 in 2008; Nokia N97 in 2009 and the Nokia N8 in 2010. However, all these devices clearly fell short of the user experience of the iPhone (Vuori & Huy, Citation2016, p. 37). In a belated move to diversify its OS portfolio,Footnote4 in 2010 Nokia launched the E7 Communicator (running Symbian); the N9 (running on MeeGo); and the Lumia 800 (running Windows Phone). Nevertheless, tech expert reviewers launched a salvo of criticism against Nokia products and the dominant discourse was that they had old processors, low quality screens and the availability of apps did not match either the Samsung Galaxy (Android) or the iPhone 4 (iOS) (O’Brien, Citation2011).

The financialisation of the company and exposure to US markets had come back to bite Nokia hard. In the period up until 2008 Nokia’s spending on share buy-backs increased exponentially. Indicatively, in 2005 Nokia spent more money on share repurchases (€4.2bn) than on total R&D expenses (€3.8bn) and Nokia continued to spend a substantial portion of its net sales on share buy-backs: it spent €3.4bn in 2006; €3.9bn in 2007; and €3.1bn in 2008 (Nokia, Citationn.d.). However, this strategy run out of steam in the context of the global financial crisis of 2008/9 when global sales began to fall rapidly, and share repurchases stopped in 2009. In April 2009 Moody’s changed the outlook for Nokia’s credit rating to negative, and in October 2010 Moody’s was the first to downgrade Nokia’s credit rating from A1 to A2 (Moody’s, Citation2009).

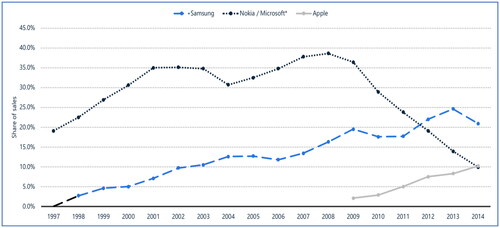

In early 2011 the sense of the crisis was widespread. On 1 February 2011, the media reported that the US rating agency Standard & Poor’s was considering downgrading Nokia’s short and long-term corporate credit ratings, because ‘the Finnish company’s share of the converged mobile device market had slipped from 40% in the fourth quarter of 2009 to 31% in the fourth quarter of 2010’ (Ben-Aaron, Citation2011). The dramatic decline in Nokia’s global market share in just a few years is shown below ().

Figure 5. Market share of mobile phone unit global sales, 1997–2014. Source: Statista.com.

On 9 February 2011 the Wall Street Journal reported Nokia’s CEO Stephen Elop famous ‘Burning Platform’ memo, in which the CEO suggested that the ‘battle of devices has now become a war of ecosystems’, and explained that

…ecosystems include not only the hardware and software of the device, but developers, applications, ecommerce, advertising, search, social applications, location-based services, unified communications and many other things (The Wall Street Journal, Citation2011).

On 11 February Nokia CEO Stephen Elop and Microsoft CEO Steve Ballmer jointly announced a major business partnership between the two companies, which would see Nokia adopt Windows Phone as the primary OS for its future smartphones, replacing both Symbian and MeeGo (BBC, Citation2011). In an ironic twist of history, Nokia spent the 2000s to avoid Microsoft’s domination in mobile phone OS (Greene et al. Citation2001), only to turn to them at the end of the decade.

Why didn’t Nokia turn to the Android platform? There are different views on this particular question. Stephen Elop tried to negotiate a deal with Google to run Android, but Google refused to give any advantages over its other partners, and thereby, to give the ability to Nokia engineers to add their innovations to Google’s software (Burrows, Citation2011b). Lamberg et al. (Citation2021), following Burrows, suggest that Elop did not want to turn Nokia into just another company distributing Android. Doz and Wilson (Citation2017, p. 119) offer a slightly different version of the story, they suggest that the mobile carriers did not want Nokia to distribute Android, because they wanted Nokia to break the emerging duopoly between Apple-iOS & Samsung-Android. But whilst avoiding distributing Google’s Android OS, Nokia ended up distributing Microsoft’s Windows Phone OS, which had only a small portion of the mobile OS market (Burrows, Citation2011a). This was a ‘last ditch’ attempt to stem the advancement of Apple-iOS and Samsung-Android industry platforms, by launching a third pole, the Nokia-Windows platform. As it turned out, it was too little too late. Nokia Lumia 800 was the first Windows Phone, but the software offered little push to switch from Android or iOS; it had fewer apps, was not deemed equally user friendly and did not work on Verizon and Sprint.

Despite the alliance with Microsoft, the rating agencies continued their assault on Nokia. On 2 March 2012 Standard & Poor’s further cut Nokia’s long-term corporate credit rating to BBB- from BBB, with a negative outlook ‘reflecting the possibility of a further downgrade’ if the company’s margins remained too weak (Virki & Cox, Citation2012). The Microsoft-Nokia partnership did not appease the markets, and the exposure of Nokia to the US financial markets was continuing to bite. Unlike Samsung, which was not exposed to the US, and Apple was sheltered because of no debt and huge reserves, Nokia had no ‘safe haven’. The rating agencies, as key actors in the US financial system, had already predicted a ‘death spiral’ for Nokia and their discourse was that the new Apple and Android platforms would become dominant.

The death knell was put when the credit rating of Nokia was downgraded to junk status by both Fitch ratings and Standard and Poor’s. The Fitch rating went from A+ in December 2008 down to BB- in July 2012. The Standard and Poor’s press release was reminiscent of an obituary. It suggested that ‘Nokia, once the world’s dominant mobile phone provider, has lost out to Apple Inc. and Google Inc. in the smartphone business’ and that ‘we still expect revenue from Lumia smartphones to grow over time, but not sufficiently to offset a rapid decline in revenue from Symbian-based smartphones over the next few quarters’ (Virki & Cox, Citation2012). In 2013 Nokia announced the sale of its mobile and devices division to Microsoft. In 2014 the acquisition of Nokia’s mobile division was completed, becoming Microsoft Mobile and Nokia exited the industry.

6.2. Apple

In the period 2008–2009 the addition of technological innovations to iPhone products intensified. The iOS 2 was released and supported third-party applications via the App Store. In 2009 all Apple’s rivals, RIM (Blackberry), Nokia, Microsoft, HP/Palm, were setting up their own versions of Apple’s App Store (Jana & Burrows, Citation2009). Next year Apple launched iPhone 4 with several new design features: Retina display, selfie camera, FaceTime, multitasking. In 2011 Apple launched iPhone 4S with SIRI as a new feature. In 2013 Apple launched iPhone 5S with new features: Touch ID (fingerprint unlock), 64-bit processor, redesign of iOS. By 2014 Apple was leading the market towards larger devices and launched iPhone 6 and 6 Plus.

The innovation frenzy went hand in hand with a financial markets rally. From 2007 to 2014 Apple’s share price increased more than 700% and Apple’s shareholders were handsomely rewarded. Apple was totally outside the radar of the credit rating agencies, because as of February 2004 Apple had no long-term debt obligations and huge reserves (Apple, Citationn.d.). This provided a shelter from financial markets and focused on a strategy of ‘retain and reinvest’ drawing money from its profits to fund R&D expenditure.

In the period 2008–2011 Apple did not spend on share buy-backs, but total R&D expenses increased from $535 m in 2005 to $6bn in 2014 (Apple, n.d.). At the end of the 7-year period (that coincided with the smartphone wars) the reward for the shareholders was immense. Apple spent gigantic sums on share buy backs compared to R&D ($34.5bn in 2013 and $57.2bn in 2014). However, in line with financialisation that permeates the US capitalism, these handsome rewards to shareholders were financed through debt, rather than profitability. In April 2014 Apple announced it would seek to tap the debt market as part of its plan to sell out billions to shareholders in dividends and stock buybacks without paying taxes to bring home its massive overseas cash pile.

6.3. Samsung

The home context continued to provide some advantages for Samsung. The South Korean government banned the iPhone from going on sale on the grounds that it failed to support WIPI (Wireless Internet Platform for Interoperability) technology. This protectionist policy helped to minimise Samsung’s competition in the home market and gave them time (Cain, Citation2020, p. 154). In October 2009 Samsung released the Omnia II (running Windows Mobile OS) to compete with the iPhone. It was rushed, poorly reviewed by tech experts, and used a less user-friendly resistive display, and faulty with dropped calls and a slow user-interface (Cain, Citation2020, p. 168). In the period between 2007 and 2009 Samsung made several false starts to launch a phone that would compete with the iPhone, essentially, experimenting with different operating systems, e.g. Jack (Windows), Behold I (Touchwiz), Omnia II (Windows), and Behold II (Android). But it consistently failed to match the quality and user experience of the iPhone. Finally, in 2010, Samsung launched the Galaxy S Series with Google Android in four US carriers (Cain, Citation2020, p. 169).

The successful launch of the Galaxy S Series suggests that ‘Samsung could wait until after Apple explored the smartphone market, invest later once risk had diminished, and thereby occupy the market through fast execution made possible by the intense inter-unit cooperation’ (Song et al. Citation2016, p. 136). But this waiting time was afforded by patient capital from state-owned banks and weak pressures for profitability. South Korea is characterised by weak external capital markets (Khanna et al. Citation2011), but this also necessitated the company to rely on internally generated cash from one operation to fund the others. Unlike Nokia, Samsung benefitted from its embeddedness in the South Korean capitalism. The weak shareholder pressure and family control allowed Samsung to be sheltered from financialisation pressures and a longer-term horizon to come up with an alternative to iPhone (The Economist, Citation2011b). Indeed, the Lee family had a controlling 46% stake in the umbrella company Everland, and as a strategy it prized market share over profits (The Economist, Citation2011a). While it retained only a home country listing, it returned money to domestic and foreign shareholders though share-buy backs and dividends (The Economist, Citation2005). This was clearly reflected in the positive credit ratings that Samsung enjoyed, while Nokia was battered hard by rating agencies. Fitch ratings for Samsung stood fixed at A+ for the period between 2006 and 2014. Moody’s announcement was glorious, as it praised Samsung justifying its A1 rating on Samsung’s ‘expansion in the smartphone segment, where it increased its global market share to around 30.6% in 1Q 2012 from just 3.7% in 2009’ (Moody’s, Citation2012).

The Samsung Galaxy S II was launched in May 2011 and was very well received by tech expert reviewers. Samsung’s Telecommunications Chief Marketing Officer, Todd Pendleton, was instrumental in leading the advertising war against Apple (Cain, Citation2020, pp. 177–194). In 2012 The Galaxy S III was launched in May 2012 – after the iPhone, this was the only other smartphone to launch globally as a single device with one name. It was available on the four major US carriers. The device was a huge commercial success and helped boost Samsung’s profits. It had 9 m pre-orders and sold 40 m units in the first six months (Cain, Citation2020, pp. 195–196). Samsung was well hooked into the Android industry platform and abandoned Microsoft’s Windows Phone OS.

7. Concluding remarks and future research

The narrative of the competitive dynamics in the smartphone industry provided a combined account of the co-evolution of the industry by looking at the three tech giants: Nokia, Apple and Samsung in their wider institutional contexts. It yielded several interesting insights, which are summarised below. The events involved in this comparative history, and the interpretation put forward, highlight important questions for further research in business history and beyond, that we discuss in the remainder of the article ().

Table 1. Comparative overview of cases.

7.1. First mover advantages, institutional context, and sunk costs

Earlier literature articulated the mechanisms of first mover advantages and how being a technological pioneer can facilitate market success. As Cusumano et al. (Citation1992, p. 53) note the first movers are ‘the first firms to commercialise a new technology’ and they ‘often benefit from superior technology and reputation, which they may sustain through greater experience, or a head start in patenting’. However, being a first (or fast) mover in technological innovation does not necessarily ensure success in the long run, instead, fast followers may copy the best features of pioneers’ products as the example of Apple copying the Graphical User Interface from Xerox (Graham, Citation2008, Citation2017) and offer even more consumer appealing versions. In contrast to works that emphasise the unparalleled innovativeness of Apple’s iPhone (Ali-Yrkkö et al. Citation2013; Van Rooij, Citation2015), we showed that Nokia as a company was working on similarly innovative technologies towards developing smartphone hardware and software since the late 1990s explicitly as new product line to accommodate the digital convergence of mobile phones and other devices. Several of the innovations in the iPhone were already available in various Nokia products, e.g. app store, touchscreens, wireless connectivity, email and browser capabilities, and others.

The critical re-examination of the history of the smartphone wars unveiled that -in fact- Apple was a latecomer in the technological race and experienced several false starts and failures. Yet, it managed to disrupt the industry, not just by offering a more customer appealing device as in the early computer industry (Chandler, Citation1997; Chandler et al. Citation2005), but also by reconfiguring the power relations in the industry.

Hence, the notion of disruption needs to be qualified here, as the conventional conceptualisation of ‘disruptive innovation’ (Christensen et al. Citation2015) is narrowly understood as new entrants targeting the low-end of the market and due to the cost advantages of their business model moving gradually towards the mainstream part of the market. This type of disruption does not cohere with the story of smartphones, because Apple’s product disrupted the industry by explicitly targeting the high-end market. To be precise, Christensen et al. (Citation2015, p. 49) argued that Apple disrupted the market ‘not of other smartphones’ but the market for ‘laptop as the primary access point to the internet’. We find this argument suffering from conceptual stretching, as it is far-fetched to argue that the functionalities of a laptop (e.g. Office applications) are fully substitutable from an iPhone, especially the early one launched in 2007.

Notwithstanding, the new iPhone was indeed disruptive in the sense that it helped to shift consumer demand from conventional handsets to smartphones, whereas Nokia and other manufacturers were still struggling along a pattern of ‘incremental innovation’ (Christensen, Citation1993) in multiple product lines. The case of the iPhone is congruent with conceptions of ‘architectural innovation’ (Henderson & Clark, Citation1990) and the different ways to organise an industry between assemblers and suppliers. As we elaborate in further detail below this had profound effects in the architecture of the industry through what we call a reconfiguration of power relations within ‘industry platforms’ (Gawer & Cusumano, Citation2014).

The home country context and especially national innovation systems (Miozzo & Walsh, Citation2006) mattered, but not decisively. Nokia gained from one of the first international mobile networks in the world and standardisation of GSM across Europe. Samsung also benefitted from its country’s well-established wireless connectivity, government subsidies and protective industrial policy. Apple benefitted from being part of a regional innovation cluster of Silicon Valley (Lazonick et al. Citation2013), and for the development of the iPhone, collaborated with Motorola and US carriers to expand aggressively in the home market. Hence, the home country context in which each company was embedded, although important, again did not appear as either a necessary or sufficient condition for success.

In this article we considered a wide range of interactions between various actors engaged in the technological transition: competitors, phone carriers, suppliers, tech experts, and rating agencies. Further research might look at the role played by national and transnational regulators in shaping and constructing the new markets. This is an important area of further research in business history as evidenced by recent works exploring the role of regulators in competition policy and the interplay between business strategy, monopolies and antitrust regulation (Kornelakis and Hublart, Citation2022) (Rollings & Warlouzet, Citation2020). A related area of further research might also consider the role patent rights protection since the extent to which Samsung’s success can be attributed to an imitation of Apple’s innovations, remains an open question. Indeed, Apple believed that Samsung copied the design of the iPhone with the Galaxy S model. Tim Cook had been wary of damaging Apple’s relationship with Samsung, which was a key supplier, and therefore part of the Apple’s industry platform. But Steve Jobs subsequently decided to go ahead with lawsuits against Samsung for allegedly copying the design of both the iPhone and the iPad, initially demanding $2.5bn in damages (Cain, Citation2020, p. 169). Hence, further historical research could also examine the degree to which Samsung’s success indeed was based on infringing patents, by looking especially at the legal archives and contributing to the literature linking business history and the policy context regulating patents and innovations.

Many scholars have underlined the role of sunk costs in embedded technologies, something that incumbents struggle with (Shapiro & Varian, Citation1999), as the switching costs represent substantial transaction costs. This article suggested that all three players had sunk costs in their own home-grown technologies and this condition did not appear as either necessary or sufficient to explain success or failure. Nokia was clearly well invested into Symbian, a platform that had become clunky and largely dysfunctional – despite being innovative in the early years. But equally, Samsung had sunk costs in Symbian and Bada (later Tizen), which was its home-grown OS system. Apple was also trying to develop a smartphone OS by tweaking its own iPod OS or MacOS. Further research could also consider the role of sunk costs and path dependence, whereby new platforms emerge alongside old platforms, following patterns of ‘symbiosis’ (Khanagha et al. Citation2022) with the dominant platform, and/or partial competition with it during a technological transition.

7.2. Industry platforms, power relations, and platform leadership

In our comparative perspective, we proposed that what mattered in the technological transition to smartphones was the reconfiguration of industry platforms and power relations within networks (Dobbin, Citation2005), rather than technological innovativeness or sunk costs per se. The analysis threw light on the power shifts within the ‘industry platforms’ (Gawer & Cusumano, Citation2014) in which key actors were members. The transition to smartphones signified a move from an old to a ‘new economy’ business model (Lazonick, Citation2010) and a power shift from carriers and handset manufacturers towards software companies and app developers. In the old business model the power rested with carriers, who intermediated the triangular relationship between carriers, consumers and handset manufacturers. Apple disrupted the architecture of the industry, and in the newly formed ‘industry platforms’ the power rested on software firms, which increasingly intermediated the more complex pentagonal relationship between software firms, users, app developers, phone carriers and handset manufacturers. Apple became a platform leader. Samsung, on the other hand, appears to have followed a process similar to Cisco’s ‘mutualism’ being part of the new and old platform at the same time (Khanagha et al. Citation2022). Samsung was not a platform leader itself; the home-grown Bada/Tizen never really took off. But it allied itself with Google, who was clearly the leader in the Android industry platform. In a delicate acrobatic strategy, Samsung was simultaneously a part of the old industry platform (Symbian) and the new industry platform (Android), thus, hedging its bets.

Nokia was the platform leader of the Symbian platform, but the platform was disintegrating, with exiting members, few apps and decreasing app developers (West & Wood, Citation2014). It failed to successfully remobilise in the face of the new industry platforms and lost the opportunity to jump onto the bandwagon of the Android platform. Further research should therefore examine other industries undergoing structural change and power shifts, including new alliances and multi-stakeholder relationships. This is important because it should give us an insight of the interdependence between changing business models (Lazonick, Citation2010) and shifting power relations between stakeholders.

7.3. Financialisation, shareholder value, and the innovation-finance nexus

The article also highlighted how the financialisation of a company (Dore, Citation2008; Lazonick, Citation2010) may include the seeds of its own destruction, because of the limited time horizons that the mantra of shareholder-value allows. Nokia had become too dependent on the US financial system, which afforded the company very short-term horizons and spent substantial resources in share buy-backs to appease shareholders.

While Nokia was losing customers due to the launch of iPhone; this loss of market triggered a self-fulfilling prophecy through beliefs and expectations of the fall of Nokia. At the same time, the rating agencies’ expectations and beliefs played a ‘performative’ role (Ansari & Garud, Citation2009) in constituting markets and conditioning the success of products. The downgrading of Nokia’s creditworthiness constrained even further the potential to raise capital and catch up with Apple’s innovations. Essentially, the financial markets gave Nokia only a couple of years to come up with an Apple-competing smartphone. By the end of 2009, Nokia had run out of time, its share price was on a downward spiral, and the rating agencies evaluated Nokia’s creditworthiness to ‘junk’ status. Interestingly the discourse of the rating agencies was to a lesser extent based on solid accounting or financial information, and to a larger extent on the outlook of the industry platform and the innovative potential of future products.

By contrast, Samsung had access to the patient capital afforded by Korean capitalism and was sheltered from the immense pressures of US financial markets. It was not listed in the NYSE, but only in the home stock market. The Korean government delayed the entry of iPhone in the home market and patient capital came from state-owned Korean banks. The chaebol structure and ownership afforded the company with a home country advantage. It provided Samsung with the valuable resources to draw together expertise, funding (Khanna et al. Citation2011) and know-how from different units (Song et al. Citation2016), and managed to come up with an iPhone killer, despite much experimentation and false starts. Similarly, Apple was shielded from financial markets because of its huge cash reserves and no debt. The rating agencies did not even evaluate its creditworthiness until 2014. The share buy-backs policy kept shareholders happy, whilst it could fund innovation via the profits from sales in a ‘retain and reinvest’ (Lazonick et al. Citation2013) fashion.

7.4. The comparative method and causality in business history

Finally, the article raised methodological questions about further historical research and especially the examination of causality in the case studies of success and failure in business. Studying success or failure in isolation is legitimate and has led to important insights. Contributions focusing on primary sources involve extensive and difficult efforts of analysis that clarify facts and allow to develop important interpretations. For example, without the secondary sources focusing on Nokia (e.g. Aspara et al. Citation2023; Doz & Wilson, Citation2017; Häikiö, Citation2002; Lamberg et al. Citation2021) it would not have been possible to develop this perspective article. Moreover, research focusing on single firms has shaped profoundly the way we think about capitalism and its evolution as well as success (Chandler, Citation1976) and failure (Christensen, Citation1993).

But the single-case approach also raises important methodological challenges, as highlighted by this study. We proposed that one way to respond to these challenges is by studying simultaneously firms that succeed and fail, and this helps discriminate between modes of causation and identifying which mechanisms are necessary or sufficient (George & Bennett, Citation2005; Mahoney, Citation2000; Ragin, Citation1987). This suggests a need to move away from deterministic forms of causation towards an approach that incorporates configurational causation, i.e. constitutive of a combination of factors, and conjunctural causation (George & Bennett, Citation2005), i.e. factors that are mutually reinforcing in the Weberian sense. The article provides a call for more contextualised comparisons of success and failure in business history that move the field towards greater generalisability and beyond idiosyncratic and company-specific explanations.

The methodological approach followed in this article was to take a broad perspective of the new emerging industry and consider the co-evolution of the strategies of key players in a dynamic environment, by applying Mill’s comparative method of difference (Ragin, Citation1987). Further research could consider other negative or ‘failed’ cases in the same industry. For example, Palm and RIM/Blackberry appear as equally puzzling cases of failure. Palm led the digital convergence with the PDAs; and RIM was on the vanguard with its innovative Blackberry phone, but both were wiped out from the smartphone market. Examining these cases in comparative perspective is important, because to understand failure we also need to understand success and vice versa. Admittedly, calls for integrating comparisons in business history are not something new (Chandler, Citation1976). But further research in business history could also move forward by tapping on novel methodologies such as fuzzy set Qualitative Comparative Analysis (Fiss, Citation2011; Ragin, Citation2000) to examine the configurations of causes in a more structured and systematic manner for medium-N numbers of cases.

A final contribution of this article is to examine the cases in their wider societal and economic and institutional setting. Our explanations focused on key contextual factors: the reconfiguration of industry platforms and the degree of shelter from financialisation pressures. These complement existing explanations of earlier literature, which focused on internal factors, such as Nokia’s disunited organisational design, matrix organisation inefficiencies, skills losses, internal conflict, and poor leadership (Doz & Wilson, Citation2017; Lamberg et al. Citation2021; Vuori & Huy, Citation2016). Naturally, whether a factor is necessary to an outcome in a case is a separate issue from ‘how much it contributed to the magnitude of the outcome’ (George & Bennett, Citation2005, p. 27) and hence this is also an avenue for further research. This reaffirms the power of thick historical organisational narratives (Popp & Fellman, Citation2017; Rowlinson et al. Citation2014) based on rich primary sources that help discriminate between the relative importance of competing explanations.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Notes on contributors

Andreas Kornelakis

Andreas Kornelakis is a Reader (Associate Professor) in Comparative Management at King’s Business School, King’s College London. He holds a PhD from the LSE and his expertise covers comparative management, political economy and institutional analysis. He has published in journals such as: British Journal of Industrial Relations, Business History, and Journal of Common Market Studies.

Dimitra Petrakaki

Dimitra Petrakaki is Professor of Technology and Organization at the University of Sussex Business School and Co-Investigator of the ESRC-funded Digital Futures at Work Research Centre. Her work focuses on the implications of the introduction of digital technology for the organization of work. She has published in journals such as Harvard Business Review, Organization and Information Systems Journal.

Notes

1 For a detailed consideration of earlier explanations, including from works in the Finnish language, see the Table offered by Lamberg et al. (Citation2021, p. 604).

2 We would like to thank one of the anonymous reviewers for this suggestion, with which we agree, and helped us to spell out our argument more explicitly.

3 We would like to thank one of the anonymous reviewers for bringing this and other works to our attention.

4 For a thorough perspective on the different Operating Systems (OS) that Nokia experimented with see the comprehensive table offered by Lamberg et al. (Citation2021, p. 583).

References

- Alcacer, J., Khanna, T., & Snively, C. (2014). The rise and fall of Nokia. Harvard Business School Cases, 9, 714–428.

- Ali-Yrkkö, J., & Hermans, R. (2002). Nokia in the Finnish innovation system. ETLA Discussion Paper, 811.

- Ali-Yrkkö, J., Kalm, M., Pajarinen, M., Rouvinen, P., Seppälä, T., & Tahvanainen, A.-J. (2013). Microsoft acquires Nokia: Implications for the two companies and Finland. ETLA Brief, 16, 1–6.

- Amadeo, R. (2018, July 21). Google’s iron grip on Android: Controlling open source by any means necessary. Ars Technica. https://arstechnica.com/gadgets/2018/07/googles-iron-grip-on-android-controlling-open-source-by-any-means-necessary/3/

- Ansari, S., & Garud, R. (2009). Inter-generational transitions in socio-technical systems: The case of mobile communications. Research Policy, 38(2), 382–392. https://doi.org/10.1016/j.respol.2008.11.009

- Apple. (n.d.). Annual Reports. 1996–2014.

- Argyres, N., Mahoney, J. T., & Nickerson, J. (2019). Strategic responses to shocks: Comparative adjustment costs, transaction costs, and opportunity costs. Strategic Management Journal, 40(3), 357–376. https://doi.org/10.1002/smj.2984

- Aspara, J., Lamberg, J.-A., Sihvonen, A., & Tikkanen, H. (2023). Chance, strategy and change: The structure of contingency in the evolution of the Nokia Corporation, 1986–2015. Academy of Management Discoveries, 9(4), 469–496. https://doi.org/10.5465/amd.2019.0067

- BBC. (2011, February 11). Nokia and Microsoft form partnership. BBC News.

- Ben-Aaron, D. (2011, March 30). Nokia rating cut for first time by S&P on smartphone share. Bloomberg.

- Burrows, P. (2011a, February 21). Mobile wars! Bloomberg BusinessWeek.

- Burrows, P. (2011b, June 6). Elop’s fable. Bloomberg BusinessWeek.

- Burton, J. (1991, October 7). Mobile sector is Nordic flagship. Financial Times.

- Cain, G. (2020). Samsung rising: Inside the secretive company conquering tech. Virgin Books.

- Castells, M., & Himanen, P. (2002). The information society and the welfare state: The Finnish model. Oxford University Press.

- Chandler, A. (1976). Institutional integration: An approach to comparative studies of the history of large-scale business enterprise. Revue Économique, 27(2), 177–199. https://doi.org/10.2307/3500540

- Chandler, A.Jr. (1997). The United States: Engines of economic growth in the capital-intensive and knowledge-intensive industries. In A. D. Chandler, F. Amatori, & T. Hikino (Eds.), Big business and the wealth of nations (pp. 63–101). Cambridge University Press.

- Chandler, A., Hikino, T., & Von Nordenflycht, A. (2005). Inventing the electronic century: The epic story of the consumer electronics and computer industries. Harvard University Press.

- Christensen, C. M. (1993). The rigid disk drive industry: A history of commercial and technological turbulence. Business History Review, 67(4), 531–588. https://doi.org/10.2307/3116804

- Christensen, C. M., Raynor, M., & McDonald, R. (2015). What is disruptive innovation? Harvard Business Review, 93(12), 44–53.

- Cohan, P. (2013, September 10). Project Vogue: Inside Apple’s iPhone deal with ATT. Forbes.

- Cusumano, M. A., Mylonadis, Y., & Rosenbloom, R. S. (1992). Strategic maneuvering and mass-market dynamics: The triumph of VHS over beta. Business History Review, 66(1), 51–94. https://doi.org/10.2307/3117053

- Dahl, F. (1993, May 24). Finnish firms to tap markets for new capital. Reuters.

- Dobbin, F. (2005). Comparative and historical approaches to economic sociology. In N. J. Smelser & R. Swedberg (Eds.), The handbook of economic sociology (pp. 26–47). Princeton University Press; Russel Sage Foundation.

- Dore, R. (2008). Financialization of the global economy. Industrial and Corporate Change, 17(6), 1097–1112. https://doi.org/10.1093/icc/dtn041

- Dore, R., Lazonick, W., & O’Sullivan, M. (1999). Varieties of capitalism in the twentieth century. Oxford Review of Economic Policy, 15(4), 102–120. https://doi.org/10.1093/oxrep/15.4.102

- Doz, Y., & Kosonen, M. (2008). The dynamics of strategic agility: Nokia’s rollercoaster experience. California Management Review, 50(3), 95–118. https://doi.org/10.2307/41166447

- Doz, Y., & Wilson, K. (2017). Ringtone: Exploring the rise and fall of Nokia in mobile phones. Oxford University Press.

- Fellman, S., Iversen, M. J., Sjögren, H., & Thue, L. (Eds.). (2008). Creating Nordic capitalism: The development of a competitive periphery. Bloomsbury.

- Fiss, P. C. (2011). Building better causal theories: A fuzzy set approach to typologies in organization research. Academy of Management Journal, 54(2), 393–420. https://doi.org/10.5465/amj.2011.60263120

- Fox, J. (2000, May 1). Nokia’s secret code. Fortune.

- Froud, J., Johal, S., Leaver, A., Williams, K., & School, M. B. (2012). Apple business model financialization across the Pacific. CRESC Working Paper Series, 111.

- Gade, L. (2006, November 26). Samsung BlackJack. Mobile Tech Review. https://www.mobiletechreview.com/phones/Samsung_BlackJack.htm

- Gawer, A., & Cusumano, M. A. (2014). Industry platforms and ecosystem innovation. Journal of Product Innovation Management, 31(3), 417–433. https://doi.org/10.1111/jpim.12105

- George, A., & Bennett, A. (2005). Case studies and theory development in the social sciences. MIT Press.

- Giachetti, C., & Marchi, G. (2010). Evolution of firms’ product strategy over the life cycle of technology-based industries: A case study of the global mobile phone industry, 1980-2009. Business History, 52(7), 1123–1150. https://doi.org/10.1080/00076791.2010.523464

- Gospel, H., Pendleton, A., & Vitols, S. (Eds.). (2014). Financialization, new investment funds, and labour: An international comparison. Oxford University Press.

- Graham, M. B. W. (2008). Technology and innovation. In G. Jones & J. Zeitlin (Eds.), The Oxford handbook of business history (pp. 348–373). Oxford University Press.

- Graham, M. B. W. (2017). When the corporation almost displaced the entrepreneur: Rethinking the political economy of research and development. Enterprise & Society, 18(2), 245–281. https://doi.org/10.1017/eso.2017.5

- Greene, J., Baker, S., & Burrows, P. (2001, December 3). Ganging up to compete with Microsoft. Business Week.

- Grøtnes, E. (2009). Standardization as open innovation: Two cases from the mobile industry. Information Technology & People, 22(4), 367–381. https://doi.org/10.1108/09593840911002469

- Guglielmo, C. (2013, January 21). Life after the iPhone: How AT&T’s bet on Apple mobilized the company. Forbes.

- Häikiö, M. (2002). Nokia: The inside story. FT Prentice Hall.

- Hall, P. (2006). Systematic process analysis: When and how to use it. European Management Review, 3(1), 24–31. https://doi.org/10.1057/palgrave.emr.1500050

- Hall, P., & Soskice, D. (2001). An introduction to varieties of capitalism. In P. Hall & D. Soskice (Eds.), Varieties of capitalism: The institutional foundations of comparative advantage (pp. 1–68). Oxford University Press.