?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

The ability of companies to adapt in a short time to adverse situations is related to their resilience. This study aims to assess the resilience of companies listed in the Bucharest Stock Exchange (BSE) during the COVID-19 pandemic through a multistage approach, identifying as a proxy the stock price of their securities compared to the market trend. Testing the behavior of companies during phases of resilience (resistance, recovery, transformation) according to the evolution of the benchmark index of the BSE, and by applying the slope function and factor analysis methods, this paper shows that, in periods of crisis, the behavior of the financial market is different from normal periods.

Introduction

Recent events – the COVID-19 pandemic and global conflicts – have had and continue to have adverse effects on both people and organizations. Being exposed to external disruptions such as the COVID-19 pandemic has required entities in general and public interest entities (including listed entities) in particular to respond quickly to this threat, as the business environment is uncertain and difficult to anticipate (Asadzadeh et al. Citation2022; Duchek, Raetze, and Scheuch Citation2020; Liu et al. Citation2021). The ability of organizations to adapt quickly to adverse situations or changes brings into question organizational resilience. To be considered resilient, organizations need to be able to withstand shocks, remain as strong after shocks, adapt to change and, even more importantly, take advantage of the opportunities that change brings. According to experts (CECCAR Citation2016), “normality” means constant change and adaptation.

These adverse events have led to an understanding of how individuals and organizations can cope with these external perturbations and the ways in which they can recover from adversity (Anwar, Coviello, and Rouziou Citation2021; Williams et al. Citation2017), thus giving appropriate special attention to organizational resilience. Various authors see organizational resilience clearly explained as the way organizations survive in the face of turbulence and their ability to withstand, adapt, maintain or gain long-term competitive advantage (Hillmann Citation2021; Karunarathna et al. Citation2020; Ortiz-de-Mandojana and Bansal Citation2016; Williams et al. Citation2017). The question to be answered is: How can an organisation be considered resilient? To answer this question, the starting point is the 5Rs theory, published in 2011 by the Association of Risk and Insurance Managers of Industry and Commerce of the UK (ARIMIC) (Deloitte-Țițirigă Citation2020). More precisely, the 5Rs refer to: Risk Radar, Resources, Relationships of Organization, Rapid Incident Response and Review and Adaptation of the Organizational Environment. Risk radar involves a constant focus on identifying errors and learning from past mistakes. Resources refer to employees and the value system of the company. Relationships within the organization refer to both internal communication and communication with external partners. Rapid incident response is necessary because, in the event of an adverse situation, organizations should be prepared to respond quickly so that the incident does not escalate into a crisis or even a disaster. A continuous review of the organizational environment that requires changes and improvements, but also immediate adaptation, are fundamental elements in ensuring resilience (Deloitte-Țițirigă Citation2020).

Although the Europe 2020 Strategy set a long-term vision for the EU economy, ensuring that Member States are committed to a sustainable growth path, the economic impact of COVID-19 was threefold, according to the EC Communication on the Annual Strategy for 2020 (European Commission Citation2020) on sustainable growth, directly affecting production, causing supply chain and market disruption, including a financial impact on companies and financial markets. The European Commission’s economic analyses showed that the EU economy contracted by 7.4% in 2020, but was forecast to return to pre-pandemic levels within two years. However, the economic impact of the pandemic varied greatly between Member States. Romania’s economy was found to have one of the smallest economic contractions, at around 4% of GDP in 2020, with growth toward the end of 2020 compared to contractions in the first quarter of 2020 (Ministry of European Investments and Projects Citation2020).

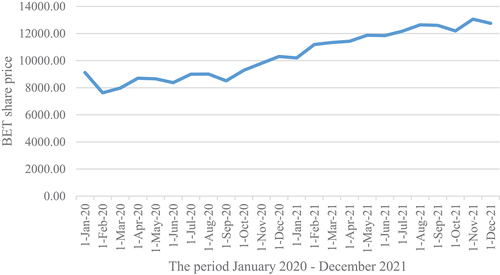

In order to analyze the timing of the recovery and subsequent resilience of companies listed on the regulated financial market in Romania, in this study the focus is on the fourth R, i.e. the response of companies listed on the Bucharest Stock Exchange (BSE) to the risk factor – the COVID-19 pandemic – a response given through the financial market. More specifically, our approach is focused on identifying a profile of the resilient company listed on the Bucharest Stock Exchange by stages of resilience (resistance, recovery, transformation) during the period crossed by the COVID-19 pandemic, a period chosen according to the evolution of the BET index (the benchmark index of the Romanian stock market-BSE), as can be seen in (on the X axis are represented the months: January 2020-December 2021, and on the Y axis is represented the BET index quotation).

Figure 1. Evolution of the BET index in the period January 2020-December 2021.

shows that the BET index, which reflects the evolution of the most traded companies on the Regulated Market of the BSE (maximum 20 companies), registers a drop immediately after the outbreak of the COVID-19 pandemic, recovering within about eight months, and then the shares included in the BET register a new trend, reaching at the end of the period under analysis a price much higher than at the beginning of the period under analysis. The period is limited to 24 months (January 2020 - December 2021), as these were the years most affected by the COVID-19 pandemic, and it was possible to assess resilience across the three phases – resistance, recovery, transform – as the trend of the BET index allowed us to assess resilience across its phases. The choice of the sample was driven by the desire to assess the resilience of listed companies operating in a developing country.

From the literature review, it can be noted that previous studies have focused, on the one hand, on the content of the connotations of organizational resilience and its influencing factors (Chen, Xie, and Liu Citation2021), and on the other hand, on the mechanisms of action, i.e. how businesses remain resilient in a crisis and/or post-crisis period (Neise, Verfurth, and Franz Citation2021). Thus, from the analysis carried out on the studies found in the scientific literature, it is found that no analysis has yet been carried out on the resilience of listed companies on its three phases, which nuances the contribution of our study toward a new approach in the literature.

As mentioned above, our study aims to identify a profile of resilient companies listed on the BSE, where resilience is explained through the lens of the stock exchange quotation of the securities, by comparison with the market evolution, starting from the market model developed by Markowitz (H. Markowitz Citation1959).

The market model describing the return and risk of securities is run on 1,848 observations (month-firm). Specifically, the applied model shows that entities listed on the BVB can be structured into two categories: offensive and defensive, according to the variations of individual securities returns to market returns during the period of the COVID-19 pandemic (24 months).

The analysis over time is performed using the Slope function and shows that the amplitude of the fall for the companies included in the study varies significantly compared to the BET index, with some being more resilient, with a smaller amplitude of fall, and for others the financial market is less generous during the COVID-19 pandemic. Three intervals are created according to the evolution of BET during the analyzed period, and the comparison of the three phases of resilience: resistance, recovery, transformation is made for each individual company. Following the processing carried out, it is noted that some of the companies included in the sample are adapting and returning to the maximum quotation reached before the COVID-19 pandemic, others are characterized by a transformative capacity, following a new trend, but it is also noted that there are companies that have not yet reached this stage, during the period under analysis (January 2020 – December 2021). The period was limited to December 2021, as the stock market price trend was rising at the end of this period and exceeded (on average) the values that stocks had before the COVID-19 pandemic. For the cross-sectional analysis, multivariate data analysis models are used, which highlight the connection between the field of activity of companies listed on the BSE during the COVID-19 pandemic, the average return on securities, the chance of winning, the risk assumed by investors and the type of shares (offensive, defensive), determined by comparison with the evolution of the financial market, and the results show that, during a period of crisis, the behavior of the financial market is different from the behavior identified in periods of normality, and some fields of activity are attractive even in times of crisis.

The motivation for the research is that it is important for investors to know how companies behave even in times of crisis, so that the losses they might incur can be mitigated. The contribution of the study to the literature is made, on the one hand, by analyzing the literature focused on resilience and synthesizing the most important aspects revolving around this concept, and on the other hand, by analyzing the resilience of companies listed in the regulated market in Romania (a developing country) by its phases: resilience, recovery, transformation and by business fields. The study is further divided into sections. Section 2 is intended to review the specialized literature, focusing, on the one hand, on the analysis of the theoretical framework that underpins the field of organizational resilience, but also the portfolio theory, and on the other hand, on the analysis of the empirical framework, in order to highlight different models of measuring organizational resilience and the results obtained. In Section 3, the research methodology is developed, and broken down into: the population studied and the sample analyzed, the variables analyzed, the data source and the models proposed for testing. Section 4 deals with the results obtained from the processing carried out and their interpretation, and the final part of the study is devoted to the conclusions.

Literature Review

The concept of resilience is found in different fields, but has the same basic roots and connotations (Mihalciuc et al. Citation2022; Xiaolong, Wang, and Yang Citation2018). In a broad sense, resilience reflects the ability of a system to maintain or quickly return to its desired functional state as a result of a disruption that has occurred (Lozupone et al. Citation2012), to adapt to the new state or change for a new situation (Strigini Citation2012; Walker et al. Citation2004), to rapidly transform systems that limit current or future adaptive capacity (Sara, Newell, and Stults Citation2016), respectively, the adaptability and survivability of systems (McDaniels et al. Citation2008). At the organizational level, other authors (Kiuchi and Shireman Citation1999; Strong Citation2010) have included resilience as a performance indicator in their studies, which takes into account the life cycle of the organization. In our study, we will consider resilience also as a performance indicator, one which is influenced by an exogenous factor – the financial market – and not endogenous.

Assertions and Multidimensionality on Resilience in General and Organizational Resilience in Particular

The topic of resilience is approached differently in the scientific literature. For the first time, the concept of resilience was brought up in the field of physics in the late 1960s. In the mid-1980s, it was addressed in fields such as ecology, psychology, sociology, and in the late 1990s it was introduced in the organizational field (Chen, Xie, and Liu Citation2021). In physics, the study of resilience refers to the ability of a material to return to its original shape after deformation (Petak Citation2002). It is noted that in the engineering sciences, the term is used to explain the ability of a system to cope with change while maintaining its basic function (Walker et al. Citation2004). In other words, in these areas, resilience studies show the robustness of the technical dimension (Frangopol and Soliman Citation2016; Mattsson and Jenelius Citation2015) and the return to baseline from shocks (Barasa, Mbau, and Gilson Citation2018). In disaster situations, resilience is presented as the capacity of human communities to withstand and recover from external shocks or infrastructure disruptions (Blaikie et al. Citation2014). Thus, resilience is also closely related to ecosystem stability (Simmie and Martin Citation2010), knowing the ability of an ecosystem to return to its previous state after being damaged (Seyedmohsen, Barker, and Ramirez-Marquez Citation2016). In the study of ecological environments, Holling (Citation1973) pioneered the introduction of the term resilience, presenting this concept as “a measure of the persistence of systems and their capacity to absorb changes and disturbances” (Holling Citation1973). Psychology researchers explain the term resilience by the adaptive capacity that individuals display when faced with adverse conditions (Kantur and Iseri Say Citation2015).

In terms of organizational resilience, the first studies were conducted by Wildavsky in 1988 (Wildavsky Citation1988). Subsequently, studies have addressed crisis management themes (Manyena Citation2006), focusing on post-disaster resilience research (C. A. Lengnick-Hall and Beck Citation2005; Paton and Johnston Citation2001; Rose Citation2006), and strategic management has introduced the concept of resilience as a way of organizational adaptation to environmental change, to a new external equilibrium and to new circumstances (Hillmann Citation2021; Kantur and İ̇şeri-Say Citation2012; McManus et al. Citation2008). When an organization faces unexpected adversity, its ability to maintain its functions and recover quickly from adversity by mobilizing and procuring the necessary resources is considered vital to organizational resilience (Doern, Williams, and Vorley Citation2019; Hillmann Citation2021; Linnenluecke Citation2017; Williams and Shepherd Citation2016). An organization considered resilient is one that relies on certain resources (Rodríguez-Sánchez et al. Citation2021) that can be harnessed to survive, but also to recover and transform to respond to adversity (Anwar, Coviello, and Rouziou Citation2021; Bonanno et al. Citation2010; Chandler and Hanks Citation1994; Grant Citation1991; Hillmann Citation2021; Sutcliffe and Timothy Citation2003; Williams et al. Citation2017). Resources refer to both human resources in the organization (C. Lengnick-Hall et al. Citation2011; Williams et al. Citation2017), and relational resources generated by communication, coordination, and relationships within the organization (Gittell Citation2008), which support organizational resilience and are essential for an entity to respond to adversity (Anwar, Coviello, and Rouziou Citation2021; Gittell Citation2008; Williams et al. Citation2017).

An important aspect for the recovery of organizations is to improve the efficiency of activities through social coordination and resource allocation through digitization (J. Zhang, Long, and von Schaewen Citation2021). Digital technologies (artificial intelligence, big data, cloud computing, blockchain) are transforming the traditional economy into a digital economy (Vial Citation2021), and digitization is an absolutely necessary mechanism for innovation and sustainable development, as it is also an effective means for organizations to cope with shocks and be characterized by resilience (Velu et al. Citation2019). Thus, organizational resilience can be seen as a set of capabilities that can facilitate a company’s response to unexpected disruptions (Ortiz-de-Mandojana and Bansal Citation2016) and develop responses specific to the situation, ultimately engaging in transformative activities to harness disruptive situations that may threaten the organization’s survival (Zhang et al. Citation2021; Iancu et al. Citation2022; Adžić and Al-Mansour Citation2021).

It follows that organizational resilience can be viewed as a complex of dynamic characteristics from several perspectives, namely: the capability perspective, the process perspective and the outcome perspective (Chen, Xie, and Liu Citation2021; Hillmann Citation2021). The capability perspective is seen through the perceived adaptability of organizations to environmental changes (companies with greater organizational resilience are able to spot warning signs in a crisis in a timely manner). The process perspective takes into account corporate flexibility in coordinating, mobilizing and integrating internal and external resources to withstand crises. The outcome perspective aims at achieving the expected outcome or at least maintaining the existing one (Limnios et al. Citation2014; Y; J. Zhang, Long, and von Schaewen Citation2021). These dynamic characteristics provide a suitable framework for analyzing organizational resilience (Hamel and Välikangas Citation2003).

In today’s turbulent environment, business resilience means overcoming barriers by finding innovative responses to changes (Ates and Bititci Citation2011; Reinmoeller and van Baardwijk Citation2005). When referring to organizational resilience, some authors (Duchek, Raetze, and Scheuch Citation2020; Ma, Xiao, and Yin Citation2018) present the directions in which entities need to have a certain capability, namely: dynamic and flexible capability (predictive capability), survival capability (ability to adapt and cope with any disruptive situations), learning capability (ability to respond to crises). In other words, in the aftermath of shocks, disasters, entities need to find a new state of equilibrium, with certain behaviors related to identity management, reintegration and emotional work (Ishak and Ann Williams Citation2018; Paton and Johnston Citation2001). In a detailed study, Chen et al (Chen, Xie, and Liu Citation2021). outline the key elements of organizational resilience: the environment in which an entity operates is dynamic; resources must be reconfigured and organizational processes reshaped; after recovery, the organization must also pursue growth.

In management studies, resilience is approached from two perspectives, namely from a static and a dynamic point of view (Pan and Zhang Citation2020). The static view sees resilience as representing a firm’s ability to recover from disruptions, while the dynamic view sees resilience as an entity’s ability to cope with threats as well as opportunities from external environments (J. Zhang and Liangqun Citation2021). Resilience is therefore about stability, but also about flexibility (DesJardine, Bansal, and Yang Citation2019). Stability refers to an organization’s ability to maintain a stable flow of its processes and maintain its organizational attributes, and flexibility refers to an organization’s ability to innovate and adapt to changes (J. Zhang and Liangqun Citation2021).

The literature review on organizational resilience helps substantiate the research objectives and formulate hypotheses that will be tested econometrically in the empirical research part.

Organizational Resilience – Determinants and Assessment Criteria

A number of studies have focused on identifying factors influencing organizational resilience and assessing the effects of these factors on this phenomenon (Liu et al. Citation2021; McManus et al. Citation2008; Vakilzadeh and Haase Citation2020). Liu et al. (Liu et al. Citation2021) present factors influencing organizational resilience grouped into three levels: general, medium and deep. The level distribution of organizational resilience influencing factors is shown in .

Table 1. Separation by levels of factors influencing organizational resilience.

Considering the three levels presented in , organizational resilience can be seen as the ability of an organization to learn from certain adverse situations, by using organizational relationships, by optimizing structure and leadership levels, but also by reconfiguring resources in crisis situations so that the entity can withstand shocks, recover, but also transform itself following a crisis, by appealing to cognitive and emotional capacities. Training and continuous learning are key to improving organizational viability, supporting increased organizational resilience (Chabot Citation2008), where as higher learning capacity is beneficial to increase the speed of organizational recovery after a crisis (Mithani, Gopalakrishnan, and Santoro Citation2021). Organizational learning is, in unfavorable situations, both an input and an output of organizational resilience (Vogus and Sutcliffe Citation2007). Positive interpersonal relationships in the workplace also lead to improved individual, organizational and community outcomes and are a precondition for organizational resilience, playing an important role in explaining it, so that organizations can easily overcome difficulties and resume operations (Cameron and Dutton Citation2003; Dutton and Ragins Citation2017; Gittell Citation2008). From the perspective of organizational communication, considered an important factor in shaping organizational resilience, resilience depends on the ability of affected stakeholders to communicate and organize during times of rapid change or disruption, as well as the ability to respond to crises and adapt to find new solutions (Chewning, Lai, and Doerfel Citation2013; Duchek, Raetze, and Scheuch Citation2020; Gomes et al. Citation2014; C. Lengnick-Hall et al. Citation2011). An organizational culture open to innovation is an important factor in organizational resilience (Samuel, Munene, and Ahiauzu Citation2013), and balancing organizational structure can lead to what we call organizational resilience (Andersson et al. Citation2019). An organization with a stable structure, recovery plans, an adequate configuration of staff, funding reserves, and technology, and a viable business model will have a greater ability to respond to crises facing the organization (Andrew and Hawkins Citation2013; Gittell Citation2008). In order to have quick and effective feedback in the face of unexpected events that entities may face, a good cognitive capacity is required, represented by a clear sense of vision and purpose, a strong sense of value, and professional knowledge (Sajko, Boone, and Buyl Citation2021; Williams et al. Citation2017). Positive emotional skills include optimism and hope to identify opportunities to reduce losses and achieve some stability in crisis situations (Williams et al. Citation2017). Other authors (Jüttner and Maklan Citation2011; J. Zhang and Liangqun Citation2021) talk about four directions that organizations need to consider in order to minimize the impact of adverse events that may occur during their lifetime, namely: flexibility, speed of reaction, access to timely information and optimal relations with business partners. Other research shows that the basis of organizational resilience is both individual resilience and inter-functional coordination (Anwar, Coviello, and Rouziou Citation2021).

In addition to the factors listed, leadership is considered a key factor in building resilient organizations (Teixeira and Werther Citation2013), but resource availability is also necessary to overcome disruptions (Barasa, Mbau, and Gilson Citation2018; McManus, Erica Seville, and Vargo Citation2007; Pal, Torstensson, and Mattila Citation2014). Resource depletion is what will severely limit organizations’ ability to recover from shocks (Liu et al. Citation2021).

Exploring the factors influencing organizational resilience can help organizations better understand how to cope with crisis and orient themselves to deal with shocks (Liu et al. Citation2021). Among the strategies used by organizations to prepare for crises or disasters are those aimed at going through scenario exercises (pseudo-crisis situations) (Barasa, Mbau, and Gilson Citation2018). In other words, organizational resilience refers to risk awareness (Andersson et al. Citation2019), survival, and recovery from unexpected events and chaotic changes (Chen, Xie, and Liu Citation2021). Presented in summary, the three closely related dimensions that characterize organizational resilience are resilience, recovery, and transformation (Sincorá et al. Citation2018).

The multidimensional structure of organizational resilience is supported by numerous authors, who have developed various measurement criteria (Chen, Xie, and Liu Citation2021; McManus et al. Citation2008; Umoh, Amah, and Wokocha Citation2014; Vargo and Stephenson Citation2010; Wicker, Filo, and Cuskelly Citation2013). Some researchers have considered that organizational resilience includes the capacity to plan, adapt, and learn (Jones Citation2015; McManus et al. Citation2008; Prayag et al. Citation2018; Şengül, Marşan, and Gün Citation2019; Umoh, Amah, and Wokocha Citation2014), while other approaches consider organizational resilience as a construct composed of four dimensions, namely: robustness, resilience, appropriateness, and speed (Vogus and Sutcliffe Citation2007; Wicker, Filo, and Cuskelly Citation2013).

Burnard et al. conduct a study of three UK organizations and examine how entities act before and after a disruption to support the building and development of organizational resilience and conclude that responses vary from one situation to another, identifying two dimensions that determine configurations of organizational resilience, namely: Preparedness and Adaptation. The final results of the research demonstrate that there are four types of organizational configurations and these are: process-based organizations, resource-based organizations, organizations operating under high risk conditions and resilience-focused organizations (Burnard, Bhamra, and Tsinopoulos Citation2018). In a study (Oprea et al. Citation2020) which analyses the economic resilience of regions in seven Eastern European countries during the 2008 crisis (Bulgaria, Hungary, Croatia, Czech Republic, Romania, Slovakia and Slovenia), it is shown that Bulgaria and Slovenia were the most resilient, while Croatia, the Czech Republic, Hungary, Romania and Slovakia performed negatively. However, in terms of recovery and transformation, Bulgaria, Romania and Slovakia performed better than the other Eastern countries. Among the determinants of organizational resilience that were considered in the study (Oprea et al. Citation2020) and had a significant influence were: the size of the manufacturing sector, services and public administration, entrepreneurship, and the human capital represented by tertiary education.

Arranged in a four-item scale, the elements that give content to organizational resilience, through which it could be measured, are listed as follows: the ability of the organisation to cope with changes caused by external crises, the ability to easily adapt operations to external crises, the ability to provide a rapid response to the negative effects generated by external crises on the business, and the ability of the organization to maintain a high level of situational awareness at all times (Parker and Ameen Citation2018). Briefly presented, the dimensions of organizational resilience are oriented toward: capital resilience, strategic resilience, cultural resilience, relationship resilience and learning resilience (Chen, Xie, and Liu Citation2021).

Of the five dimensions, this study focuses on measuring organizational resilience based on the image of companies in the financial market during times of crisis. More specifically, the study aims to identify a profile of a resilient company listed on the stock exchange, resilience explained through the stock exchange quotation of securities, in comparison with the evolution of the market during the period of the COVID-19 pandemic. In this context, different views on financial market returns and risk are presented below, which will substantiate the research hypotheses formulated.

Views on Financial Market Returns and Risk

Investment management, as a branch of the financial industry, has become increasingly important during the 20th century, both in theory and in practice. Numerous studies have focused on optimizing financial decisions and maximizing returns on investors’ securities investments (Marinciuc Citation2020). A major challenge faced by equity owners is the choice of investment, as it is not easy to identify investments with high returns and minimal risk (Ofikwu Citation2019). In other words, every investment comes with a certain level of risk and the return is not always what is expected. For any investment, the investor expects to make a profit, but achieving this depends on market conditions and the actions of other market players.

Financial markets are a complex system, their behavior is sometimes difficult to understand, but investments in financial assets are often made in the capital market (Garas and Argyrakis Citation2007; Setyantho and Hadi Wibowo Citation2019). Investments in various securities have a significant weighting in developed countries, and in recent decades have also gained momentum in emerging countries, as rapid development in the economic sector has made people think about their future needs (Komang and Made Citation2020). The decision to invest in securities refers to portfolio management. The portfolio theory provides a foundation for choosing the optimal combination (risk-return) of securities investments (Anuwoje Ida and Victor Citation2019). A rational investor will choose an investment that will usually provide maximum returns with minimum risk (Hasanah, Irdiana, and Lukiana Citation2019). The purpose of investing in securities is clearly to achieve a certain result, but investors must also carefully calculate the risk to which they may be exposed (Komang and Made Citation2020; Yunita Citation2018).

Among portfolio optimization techniques, Modern Portfolio Theory (MPT) is one of the most influential economic theories concerning financial investments, first introduced by Harry Markowitz (winner of the 1990 Nobel Prize in Economics) in his 1952 article published in The Journal of Finance as “Portfolio Selection” and in his 1959 book “Portfolio Selection – Efficient Diversification of Investments” (H. Markowitz Citation1959). The foundation of this theory was later extended by the American economist, William Sharpe, co-recipient of the 1990 Nobel Prize, who developed the Modern Portfolio Theory through the theory of financial asset pricing – the Capital Asset Pricing Model (CAPM) (Sharpe Citation1963). Thus, Markowitz laid the foundations of Modern Portfolio Theory (MPT) by which he created a framework for configuring investment portfolios based on maximizing expected returns and simultaneously minimizing investment risk (H. M. H. M. Markowitz Citation1999). The advantage of Markowitz’s model is that it allows investors to choose portfolios based on the risk-return combination. William Sharpe’s development of Modern Portfolio Theory, through the Capital Asset Pricing Model (CAPM), addresses minimizing risk and maximizing return simultaneously in a portfolio, but through diversification and appropriate capital allocation, based on Markowitz’s rigorous mathematical framework for portfolio selection under uncertainty.

The field of financial investment has evolved over time, especially in terms of the concepts and financial instruments available to investors (Mangram Citation2013), but, regardless of the area, investors have faced the conflicting objective between minimizing risk and maximizing returns, and there has always been a compromise between risk and return (Ivanova and Dospatliev Citation2017; Mangram Citation2013; Trichilli, Boujelbène Abbes, and Masmoudi Citation2020). The market model intuited by Markowitz and developed by Sharpe is an empirical formulation that specifies that the return of a security is due, on the one hand, to market returns and, on the other hand, to the specific characteristics of those securities (Lee, Cheng, and Chong Citation2016).

Developing Research Hypotheses on the Influence of the Financial Market on Organizational Resilience in Crisis Situations

In empirical studies, corporate resilience is seen as a phenomenon that enables organizations to resist, recover and grow, turning threats into opportunities (Williams et al. Citation2017). Clearly, in order to overcome certain obstacles, the management of organizations must also use tools that stimulate innovation while maintaining competitive advantage. This includes corporate social responsibility practices, and as an indicator of organizational resilience we propose the ability to manage change (Ates and Bititci Citation2011). Moreover, to support organizational resilience, the management of entities must design and implement appropriate crisis and continuity management policies (Herbane Citation2013). Not only do appropriate management policies support the resilience of companies, but also the availability of resources is important (Barney Citation2001). Companies should also act by adopting pandemic context-specific management, opting for strategic planning, which translates into the need for resilience and recovery, thus enabling a business to be able to thrive during a crisis through a successful integration of crisis management and strategic planning, as well as more sustainable development models adopted.

Many studies make valuable contributions to the understanding of resilience in business, showing how resilience interacts with supply chains, with the assessment that sustainability in the supply chain will be increasingly difficult to achieve due to the uncertainty created by disruptive events such as natural phenomena, economic and political crises, terrorist attacks, pandemics or possible wars (Bui et al. Citation2021; Shekarian and Mellat Parast Citation2021). Thus, organizations can face high levels of risk because unintentional events occur with quite high severity (Dubey et al. Citation2021; Fattahi, Govindan, and Keyvanshokooh Citation2017; Ivanov et al. Citation2016; Jennifer, Dunn, and Craighead Citation2011).

On a different note, a 2021 study by Chen and his collaborators on organizational resilience shows that certain organizational behaviors can help companies cope with crises. The authors make reference to, rather, emotional aspects. They find that a relaxed organizational environment is more conducive to good organizational performance, and a resilient organizational culture is conducive to shaping a sense of community among organizational members (Chen, Xie, and Liu Citation2021).

Other authors (Kiuchi and Shireman Citation1999; Strong Citation2010) have included organizational resilience as a performance indicator in their studies, which takes into account the life cycle of the organization. In our study, we will consider resilience also as a performance indicator, but one that is influenced by the financial market, specifically an exogenous rather than an endogenous factor. The following are important results that researchers have reached in terms of market models.

As is well known, Markowitz, cited above, laid the foundations of Modern Portfolio Theory (MPT). The Markowitz model is a mathematical model for portfolio optimization by selecting securities for which a maximum return is expected but for which a certain level of risk is accepted. Markowitz argued that a portfolio of securities should be viewed through the prism of statistics in which the probability distribution of its rate of return is evaluated in terms of its expected value and standard deviation. Since the ultimate selection of a portfolio involves the assessment and management of risk as measured by standard deviation, it is clear that Markowitz’s portfolio selection process represents the birth of modern risk management, whereby risk is quantified and controlled (Alexander Citation2009).

Numerous indices have been proposed to measure the performance of a portfolio, such as the Sharpe index (Sharpe Citation1963) which focuses on total risk (standard deviation) and the Treynor index which considers that market fluctuations play a major role in influencing stock returns (Darmitha and Bagus Anom Purbawangsa Citation2016; Suresh and Harshitha Citation2017). Portfolio optimization is the goal that investors pursue in determining investment strategies, hoping to maximize returns and minimize the risk associated with a portfolio (Ivanova and Dospatliev Citation2017). The optimal portfolio cannot be identified as it is influenced by the risk and return preferences of each investor (Keating and Shadwick Citation2002; Limnios et al. Citation2014; Renata, Ogryczak, and Grazia Speranza Citation2014).

presents the sources of the variables of interest to which reference will be made below, the period analyzed in the various studies, the models applied and the results obtained. All these will substantiate the hypotheses formulated in our study.

Table 2. Authors, period analyzed, models and results for variables of interest.

From the summary presented above, it can be concluded that the research gap is due to the fact that in previous research there are no analyses of resilience by its phases and by companies’ business areas at the same time. Based on this finding, it was considered useful to carry out an assessment of resilience in times of crisis by business lines of companies in emerging economies, as a benchmark for investors’ decision making when seeking to finance certain businesses. As can be seen from the synthesis of the studies consulted, it appears that, in general, the studies carried out do not analyze resilience by stage of resilience and by sector of activity, as can be seen from the results presented in . Therefore, the added knowledge provided by this study is found even in the assessment of resilience by stages carried out and attached to the areas of activity of the companies included in the sample in a period of crisis and in an emerging economy such as that of Romania.

Based on the results identified in the literature (as summarized in ), the following research hypotheses are proposed for testing and validation in this study:

Hypothesis 1(H1):

During the period of the COVID-19 pandemic, the return on securities of BSE-listed companies does not depend significantly on the return of the financial market, as measured by the BET index.

Hypothesis 2(H2):

Companies listed on the BSE show an uneven behaviour on the three phases of resilience (resistance, recovery, transformation) during the period crossed by the COVID-19 pandemic, compared to the evolution of the BET.

Hypothesis 3(H3):

A profile of BSE-listed companies by industry during the COVID-19 pandemic can be identified, based on the average stock return, the chance of earnings, the risk attached to the shares and their type (offensive/defensive) compared to the BET index.

Research Methodology: Population, Sample, Variables, Data Source, Data Analysis Methods

In this study, we start from the market model (H. Markowitz Citation1959; Sharpe Citation1963) which describes the return and risk of securities and compares, for a number of 1,848 observations, the average rate of return of individual securities, the chance of gain and the risk assumed by investors for the companies included in the sample during the period crossed by the COVID-19 pandemic (January 2020-December 2021), with the same sizes of the BET index portfolio. The BET index of BSE is calculated based on a portfolio of the 19 most traded shares (in 2021) and expresses the overall stock market trend. The analysis carried out is both cross-sectional in space and longitudinal in time. In both cases, cause-effect analysis is included.

Testing the research hypotheses proposed in the study involves the use of a statistical approach (Jaba Citation2002), which involves: identifying the population, selecting the sample, choosing the variables, establishing the data analysis methods and proposing the econometric models to be analyzed, collecting and processing the data, and obtaining the research results and interpreting them in the final part of the study.

Study Population and Sample Analysed

The population analyzed in this study is represented by all companies listed on the Bucharest Stock Exchange – BSE. Among them, entities listed in the Main Market and applying International Financial Reporting Standards (IFRS) were selected. The importance of the quality and relevance of the information subject to corporate reporting also imposes certain increased requirements for sustainability information, due to investors’ awareness of the financial risks specific to the current period, generated by environmental, social and governance factors (ESG factors). Corporate sustainability reporting enhances corporate reputation, leads to increased trust of customers and other stakeholders, and improves governance and attractiveness to investors (Directive 2014/95/EU (EUR-Lex Citation2014)). A new Corporate Sustainability Reporting Directive (CSRD No 2022/2464 (EUR-Lex Citation2022)) will require large and listed EU companies, as well as large third country companies with substantial business in the EU or securities listed on EU regulated markets to report on sustainability issues in accordance with the detailed set of disclosure standards developed by the European Financial Reporting Advisory Group (EFRAG). Sustainability reporting is a tool to promote and support European and national green transition policies by redirecting capital flows toward sustainable investments and by properly managing financial risks arising from climate change, natural disasters, environmental degradation and social issues. The stakes of moving companies toward such reporting will, of course, also lead to increased resilience, by developing resilient value chains, building stronger commercial and public relationships and providing responsible products and services in a changing and transforming market. Of the 81 companies listed on the main segment at the end of the 2021 financial year, 4 companies were excluded, 3 companies were listed during 2021 and 1 company was suspended during this period. Thus, the sample analyzed comprises 77 listed firms, for which the closing share prices were collected at the end of each month of the financial years 2020 and 2021, the period crossed by the COVID-19 pandemic. Considering the 24 months and 77 listed firms, the number of month-firm observations was 1,848. To these, a number of 24 observations were added for the BET index portfolio quotation from the end of each month in the financial years 2020 and 2021. The reference for establishing the analysis interval (January 2020 - December 2021) was the evolution of the BET index, which allowed us to assess the resilience of the companies listed in the Romanian Regulated Market on its three phases, the BET index having a trend that by the end of the period analyzed has far exceeded the quotation at the time of the outbreak of the pandemic. We believe that the choice of the BET index is a relevant reference, given that the entities included in BET are chosen according to their liquidity, the quality of their reporting and their transparency in communicating with investors. The choice of the sample was driven by the desire to assess the resilience of companies listed by business object and operating in a developing country.

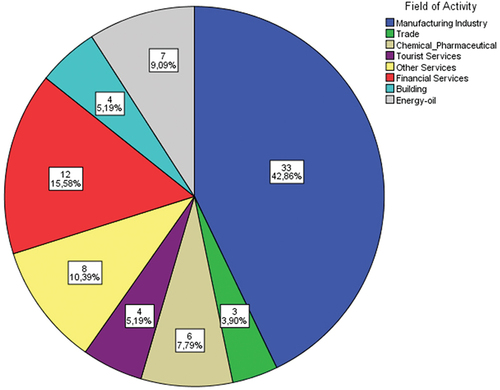

According to the activity, the sample analyzed includes 33 companies operating in the manufacturing industry, 12 entities in the financial services sector, 8 companies in the other services sector, 7 companies in the energy-oil sector, 6 companies in the chemical-pharmaceutical sector, 4 companies each in the tourism and construction services sector and 3 companies in the trade sector. The graph in shows the distribution of the sampled companies according to the field of activity.

Figure 2. Distribution of the sample analysed by field of activity.

The choice of the sample is justified by the desire to assess resilience in a crisis period in an emerging economy for firms applying International Financial Reporting Standards (IFRS), which allows comparisons to be made with the results of other studies conducted on samples of firms in other countries applying the same accounting standards. The reference for establishing the analysis interval (January 2020 - December 2021) was, as mentioned above, the evolution of the BET index, which allowed us to assess the resilience of companies listed in the Romanian Regulated Market in its three phases (resistance, recovery, transformation), the BET index having a trend, which by the end of the period analyzed, has far exceeded the quotation at the time of the outbreak of the pandemic. However, we believe that the small sample is a limitation of our research, which could be overcome in future research by including other companies listed in financial markets in other developing countries and beyond.

Variables Analysed, Data Source and Models Proposed for Testing

The return on a security is an important variable for financial investors when deciding whether to buy or sell shares. But the return on a security should not only be measured by comparisons over time, but also over space, by taking into account the return on the financial market. Empirical studies have shown that there is a linear relationship between the return on a security and the return on the financial market. The best-known model is the market model intuited by Markowitz (H. Markowitz Citation1959) and further developed by Sharpe (Sharpe Citation1963), but also by other authors (Chaweewanchon and Chaysiri Citation2022; Fisher and Hall Citation1969; Komang and Made Citation2020; Partono et al. Citation2017; Setyantho and Hadi Wibowo Citation2019; Trichilli, Boujelbène Abbes, and Masmoudi Citation2020), The best-known model is the market model intuited by Markowitz and further developed by Sharpe (Jaba Citation2008), but also by other authors (Chaweewanchon and Chaysiri Citation2022; Fisher and Hall Citation1969; Komang and Made Citation2020; Partono et al. Citation2017; Setyantho and Hadi Wibowo Citation2019; Trichilli, Boujelbène Abbes, and Masmoudi Citation2020), which justifies that the individual return of a security depends, on the one hand, on the market return and, on the other hand, on security-specific characteristics. To measure the return of the financial market, the return of the general index of the BSE, namely the BET index, which expresses the overall trend of the Romanian stock market, is taken into account.

To define the variables, the monthly closing prices of the shares of the sampled entities on the one hand, and the monthly closing price of the BET index portfolio, on the other hand, were used. At the end of the 2021 financial year, the BET index was calculated on the basis of a portfolio of the 19 most traded shares. Given the market model described above, based on individual shares prices, the individual rate of return of each security and the rate of return of the BET index portfolio were determined according to EquationEquation (1)(1)

(1) , which were then log-transformed to make them compatible with the traditional normality assumption in statistics (Berdot Citation2003), according to EquationEquation (2)

(2)

(2) , but without taking into account the receipt of dividends.

Where:

RRa,t - the rate of return on the share at time t;

Pa,t – share price at time t;

Pa,t-1 - share price at time t-1;

RRLa,t – log-transformed rate of return on the share.

After determining the logarithmic rates of return on shares, the market model, applied for each firm (77 subjects), is a linear regression model, plotted in EquationEquation (3)(3)

(3) :

Where:

RRLCompt – is the log rate of return of each individual company at time t;

RRLBETt – is the logarithmic rate of return of the BET index portfolio at time t;

α, β – regression model parameters;

εi is the error component, ε ~ N(0, 1).

Data were collected manually for the 1848 observations (stock exchange quotation – company) and 24 observations for the BET index on the BSE website, and data analysis was performed using SPSS 23.0 software. To carry out the processing, some variables were used as such, some were discretized, and others were extracted from the processing. The identified variables and their description are presented in .

Table 3. List of identified variables and their description.

The variables – The average rate of return on each company’s shares, The chance of a win, and The risk associated with each company’s shares – are indicators of descriptive statistics and are the result of statistical processing. The Average Rate of Return is the Mean of the individual rates of return of each company, the Chance of Win is the Median, and the Risk associated with the securities of each company is the Standard Deviation. To process the data, the variables – the rate of return on individual securities, the chance of a win, and the assumed risk – were discretized by creating ranges: low, and high.

In order to determine the average return of the shares, the chance of winning, and the risk associated with the shares, descriptive statistics indicators are used: mean, median and standard deviation, and in order to identify the type of action – offensive or defensive – the linear regression model is used, which shows the influence of the return of the BET index portfolio on the return of the shares of companies listed on the BSE (77 linear regression models were determined); the regression coefficient β is the one that shows the type of action (>1 - offensive, <1-defensive) compared to the evolution of the market. To test and validate the research hypotheses, we use linear regression models, Multiple Correspondence Factor Analysis (MCFA) as a multivariate data analysis method (Pintilescu Citation2007), and the Slope function for grouping companies on the three phases of resilience: resilience, recovery, transformation (Oprea et al. Citation2020).

Results and Discussions

The choice of Markowitz’s model for investment portfolio confirmation is justified by the fact that his market model implies portfolio optimization by selecting securities for which a maximum return is expected but for which a certain level of risk is accepted. Given the fact that in times of crisis, the risk hanging over companies is implicit, our study aimed to show whether Markowitz’s modern risk management whereby risk (risk) is acknowledged and controlled is still a means of valuation for portfolio optimization in the financial market. After testing the influence of the financial market return on the return of securities of companies listed on the BVB during the pandemic period, by applying Markowitz’s model, the behavior of companies (uniform/uneven) is tested, according to the evolution of the BET index during the same period, by applying the Slope function (to determine the slope associated with the stock exchange quotations for each company and for each delimited period – resistance, recovery, transformation – with the slope of the BET index for the same periods) and multivariate data analysis methods (to identify the associations between variables).

Since for the testing of the stated research hypotheses, variables resulting from statistical processing are needed, they are determined first. Thus, starting from the monthly closing price of shares of companies listed on the BSE and the BET index portfolio in the period January 2020-December 2021, the logarithmically transformed rates of return on shares are determined for each entity, including BET, and on this basis, descriptive statistics indicators are determined, which will be used further as variables included in the applied models. Specifically, the average rate of return, the median return, and the standard deviation of the share are determined for each sampled entity, respectively for the portfolio of shares included in BET. The average return indicates the return that investors could still obtain in the future by holding a given share or portfolio of shares in BET, the median return of the share or portfolio of shares included in BET shows the distribution of the return of the securities and is called the chance of winning, and the standard deviation is the indicator that measures the risk of a share or portfolio of shares included in BET.

The average rate of return of the BET index portfolio, the chance of winning and the risk of investing in this portfolio are determined by descriptive statistics indicators and the results are presented in .

Table 4. Indicators of descriptive statistics on the BET index.

From , it can be seen that the average monthly return of the BET index portfolio (RRS_BET) during the period under analysis (January 2020-December 2020) is 1.19%, which means that the BSE, during the COVID-19 pandemic, had an average return of only 1.19%. The median portfolio return of the BET index (CW_BET) is 1.07% during the period under review. Since the median is positive, by holding this portfolio over the period analyzed, there was a higher chance of making gains (51.07%) than losses (48.93%). The standard deviation (R_BET) of 6.11% indicates the risk taken by investors by holding this portfolio of shares over the period analyzed.

Next, for each sampled entity the indicators determined above were calculated: mean, median and standard deviation of the share. In addition, by applying the market model that reproduces the influence of the return of the BET index portfolio on the return of shares of BSE-listed companies (77 linear regression models were applied), the type of share was determined – offensive or defensive – the regression coefficient β being the one that directed the classification of each company’s share in one of the two categories (>1-offensive, <1-defensive) with respect to the market trend measured by the BET index portfolio. The data are summarized in .

Table 5. The mean, median and standard deviation of shares for the sampled entities.

From , it can be seen that, in addition to the calculations determined using statistical software, the quantitative variables for each company were transformed into categorical variables by comparing them with the same indicators determined for the portfolio of shares of the BET index. The associated ratings for the rate of return and the chance of winning were: low and high, and for the assumed risk: low and high.

For testing Hypothesis 1: During the period of the COVID-19 pandemic, the return on securities of companies listed on the BSE does not depend significantly on the return of the financial market, as measured by the BET index, the linear regression model is used, as shown in equation (4).

Where:

RRS_COMPi is the rate of return on equity for firm i, with i = 1,…,77;

RRS_BET is the financial market rate of return measured by BET for the period January 2020 to December 2021;

β0, β1 are the parameters of the regression models;

εi is the error component, ε ~ N(0, 1).

For the interpretation of the processing, an extract of the results obtained is presented in .

Table 6. Regression model parameter estimates.

After the statistical processing carried out, it can be seen that the R2 Determination Ratio of approximately 6% shows that in this proportion (very low), the average rate of return of the shares of the companies included in the sample is explained by the rate of return of the BET shares. It follows from this that Markowitz’s model, although statistically significant, is more applicable in periods characterized by normality and less so in periods of crisis. The results obtained are similar to other studies, which show that financial market behavior in crisis periods is different from periods considered “normal” (Bulut, Marangoz, and Daştan Citation2023; Garas and Argyrakis Citation2007). Specifically, Garas and Argyrakis (Garas and Argyrakis Citation2007) analyze the holdings of three different portfolios traded on the Athens Stock Exchange (ASE) for the period 1987–2004 and find that in the case of the Greek stock market, all stocks are (on average) affected in the same way by the price movements of other stocks, and in times of crisis (such as the 1999–2001 crisis), the correlation between stocks is increasingly strong and the market moves as a whole. However, an assessment of the financial market by sector shows that the market is affected differently in certain periods and by sector. Coming closer, in 2023, Bulut et al. (Bulut, Marangoz, and Daştan Citation2023) do a study of US stock market volatility for the period 2019–2022 (pre-Covid 19 and Covid-19) and find that the pandemic has contributed to financial market volatility in general, but not with the same risks for all industries. Therefore, in light of the above findings, economic results can also be intuited at the level of the sample analyzed, in the sense that there is an influence of financial market returns as measured by a benchmark on company stock returns. However, we must bear in mind that the analysis is carried out on companies operating in a developing country (such as Romania), and for the guidance of investors, but also for decision makers interested in certain economic sectors, our study adds to the knowledge by highlighting which sectors are more resilient and which have been more affected by the pandemic crisis (as will be shown below).

For testing Hypothesis 2: Companies listed on the BSE show uneven behavior on the three phases of resilience (resistance, recovery, transformation) during the period crossed by the COVID-19 pandemic, compared to the evolution of the BET, resorting to the division of the period under study (24 months) into three periods according to the evolution of the BET index. The analysis shows that the index that reflects the evolution of the most traded companies in the Regulated Market of the Romanian Stock Exchange (between 10 and 20) – BET – records a decrease immediately after the outbreak of the COVID-19 pandemic in Romania, as mentioned in the introductory part. Specifically, the amplitude of the fall was not very large (the slope is 0.18), and as the period in which the decrease in the price of the shares included in BET takes place is only two months, only in two months there is a decrease in the price of the shares included in BET. The recovery takes place in an interval of eight months (the slope is 0.0144), and subsequently, the shares included in the BET register a new trend, reaching at the end of the period analyzed a price higher by 40% than at the beginning of the period under analysis, as shown in above, as well as the data in .

Table 7. Assessment of the resilience of BSE-listed companies compared to the BET index.

Starting from the amplitude of the fall, rise, and transformation of the BET index, the slope associated with the stock market quotations for each company and for each delimited period (resistance, recovery, transformation) is determined and compared with the slope of the BET index for the same periods (1 - indicates resilience through resistance, recovery or transformation; 0 - indicates no resilience on all three phases). The results are presented in .

Based on the data presented in and using the multivariate analysis method – Multiple Correspondence Factor Analysis – we identify the associations between the fields of activity in which the sampled companies operate and their resilience in the three phases: resilience, recovery, and transformation. The associations can be seen in .

Figure 3. Association of RRes, RRec, RTrans and activity field by BET.

From , it can be seen that entities operating in the manufacturing, chemical-pharmaceutical industries, and building in the sample analyzed are more resilient to the fall compared to the BET over the period analyzed but recover more slowly than companies that are included in the BET. In contrast, entities in the financial services sector recover more quickly than companies that follow the trend of the financial market and are the sector that is also experiencing a faster transformation. For companies operating in the other sectors (trade, energy-oil, tourism and other services) no relevant association can be made with the resilience phases (resilience, recovery, transformation). From the previous analysis, it was inferred that the sampled entities do not behave uniformly during the COVID-19 pandemic period when compared to the BET index, as found by other authors in studies covering other crisis periods (Fisher and Hall Citation1969; Garas and Argyrakis Citation2007; Hasan et al. Citation2011; Lestari and Sudiyono Citation2020; Setyantho and Hadi Wibowo Citation2019; Ţilică Citation2022), so a statistical approach is used in the following to analyze and compare some characteristics of the companies’ shares with the BET portfolio. However, the lesson to be learned from the research, which may also be a suggestion to investors (given the uncertainty we are going through – a new crisis may emerge), is that they should combine portfolios, when making their investment decision, from manufacturing with financial services, or from chemicals and pharmaceuticals with financial services, or from real estate with financial services. We believe that this is also the added knowledge we bring through the research we have conducted: we have not found in the literature a clear association between listed entities’ actions and resilience phases to characterize companies’ behavior in times of crisis.

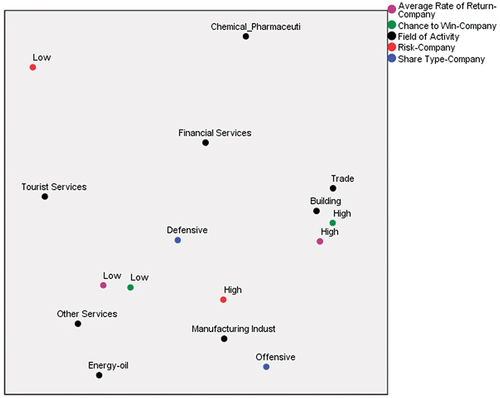

Specifically, for testing Hypothesis 3: A profile of BSE-listed companies by industry during the COVID-19 pandemic can be identified, based on average shares returns, the chance of winning, the risk attached to the shares, and their type (offensive/defensive) compared to the BET index, also using multivariate data analysis methods, namely Multiple Correspondence Factor Analysis (MCFA). The variables: average shares return, the chance of winning, the risk attached to the shares, and the type of shares (offensive/defensive) were presented and explained in and the calculations were presented in . shows the association between the companies’ business scope, average shares price return, the chance of winning, the risk attached to shares, and their type (offensive/defensive) during the COVID-19 pandemic period (January 2020-December 2021) compared to the same indicators for the BET index portfolio.

Figure 4. Association of ARR_COMP, CW_COMP, FA, R_COMP and ST_COMP.

Following the processing carried out and presented in , it can be found that the investments in the securities of the entities that operate in the fields the manufacturing and energy-oil industry in the analyzed sample is characterized by a high associated risk, but are offensive compared to BET, during the period crossed by the pandemic, with similar results to other studies carried out (Fisher and Hall Citation1969; Garas and Argyrakis Citation2007; Lestari and Sudiyono Citation2020; Setyantho and Hadi Wibowo Citation2019). However, between the two areas of activity – manufacturing and energy-oil – an investor in manufacturing is also more likely to achieve a high return associated with equities in a downturn (in addition to owning an offensive stock position relative to BET) compared to an investor in the securities of energy-oil entities, where equity returns are rather low, during the COVID-19 pandemic, as shown in . The shares of the entities in the fields of trade and construction were characterized by high profitability and a chance of winning, but they are rather defensive in relation to BET, and those in the field of other services showed low average profitability and chances of winning, in high risky conditions, which also confirms the results of other studies carried out in other periods of crisis (Bulut, Marangoz, and Daştan Citation2023; Hasan et al. Citation2011). The shares of the entities active in the chemical-pharmaceutical field are, however, characterized by a low risk during the pandemic period for the entities included in the sample, which is also justified by the pandemic period, and the investment in the securities of entities in the field of tourism has a lower risk, but also a low chance of winning and profitability. As other authors have found, in times of crisis, the behavior of the financial market is different from periods considered “normal” (Garas and Argyrakis Citation2007). The mentioned authors analyzed three different portfolios traded on the Athens Stock Exchange (ASE) for the period 1987–2004, including the crisis of 1999–2001, and found that the market was affected differently in different economic sectors, so as suggested by the results presented in our study. Also, a detailed analysis of the effects of the COVID-19 pandemic on the functioning of financial markets and how they differ from standard crises, such as economic crises, is provided in a recent study (Shahzad, Bouri, et al. Citation2021) that looks at the performance of US stock market sectors and finds that the topology of sectors did not collapse into a unified market during the pandemic. However, our study is conducted on companies operating in a developing country and highlights that financial market volatility poses different risks by industry and by resilience stage, as noted by other authors in other studies (Shahzad, Bouri, et al. Citation2021). In their study, the mentioned authors examine the asymmetric volatility spillover among Chinese stock market sectors during the COVID-19 pandemic and provide evidence of the asymmetric impact of good and bad volatilities varying during COVID-19. Exactly, bad volatility spillover shocks dominate good volatility spillover shocks. Fisher, in his study (Fisher and Hall Citation1969) of 88 companies included in the list of the 500 largest industrial firms, also shows that the pharmaceutical sector is characterized by very low risk premiums but the highest risk-adjusted rates of return on equity. While prior to the COVID-19 pandemic, some authors (Lestari and Sudiyono Citation2020), who considered the variables: risk-return associated with equities, suggested that investors could combine portfolios of stocks in the real estate sector with the financial sector or the infrastructure sector with the consumer sector, our study suggests investors based on this research to combine portfolios of manufacturing with financial services or chemical-pharmaceutical with financial services or real estate with financial services. Based on the European Commission’s analysis which generally predicted a recovery of the EU economies within two years of the COVID-19 pandemic, our approach focused on identifying a profile of a resilient or non-resilient company listed on the Bucharest Stock Exchange by resilience stage (resilience, recovery, transformation) during the period of the COVID-19 pandemic, a period also chosen according to the evolution of the BET index. From the analysis of the studies carried out, it could be noticed that previous researches have focused more on the content of the organizational resilience connotations, the factors influencing it and less on the assessment of the resilience of listed companies by its phases, which nuances the contribution of our study toward a new approach within the literature. Therefore, even though many studies have been conducted on this topic, the results of our research can still be used as a reference for potential investors to choose or invest in stocks that represent the optimal type of portfolio and in times of crisis, other than economic crisis and in a developing country. The results of the study are also useful for public officials in targeting recovery and resilience plans to priority areas of activity. However, our study also has limitations due to the small sample, but these open the door for future research on larger samples including companies listed in different world markets and affected by different crises (war, pandemic, economic barriers, etc.).

Conclusions

As we know, organizational resilience is about the ability of companies to adapt quickly to adverse situations, but also about their ability to seize the opportunities that any change brings, so that risk can be turned into advantage. The COVID-19 pandemic was sudden and required a rapid response from organizations in all sectors. Of the 5Rs that show how an organization can remain successful, the focus in this study is on the response of companies listed on the Bucharest Stock Exchange (BSE) to the risk factor – the COVID-19 pandemic – a response given through the financial market. The overall aim of the study was to identify a profile of resilient companies listed on the BSE, during the COVID-19 pandemic, resilience explained in terms of the stock market quotation of the securities, compared to the market trend, measured by the evolution of the BET index. The general finding was that during a crisis period, market behavior is different from the behavior identified in normal periods. More specifically, our approach aimed to identify the profile of the resilient company by resilience stages – resilience, recovery, transformation – during the period of the COVID-19 pandemic, taking into account the domain in which it operates. The choice of the sample is justified by the fact that we wanted to assess resilience in a crisis period in an emerging economy for firms applying International Financial Reporting Standards (IFRS), which allowed us to make comparisons with the results of other studies conducted on samples comprising firms in other countries applying the same accounting standards. The reference for establishing the analysis interval (January 2020 - December 2021) was, as mentioned above, the evolution of the BET index, which allowed us to assess the resilience of companies listed in the Romanian Regulated Market over its three phases. The market model initiated by Markowitz, applied to companies listed in the regulated market of the BSE, revealed that the return on securities of companies listed on the BSE did not depend significantly on the return of the financial market, as measured by the BET index, during the period of the COVID-19 pandemic. So, the results show that in times of crisis, the market return has less impact on the return of the companies’ securities. Specifically, the sampled companies were divided into two categories, according to the variation of individual securities returns to market returns over the period of the COVID-19 pandemic (24 months): offensive and defensive. Thus, the shares of entities operating in the manufacturing, energy-oil, and other services sectors were classified as offensive during the period analyzed, while the securities of companies operating in the trade, construction, financial services, and tourism sectors were classified as defensive. The Slope function analysis over time shows that the magnitude of the fall shows significant variations for the entities included in the study compared to the BET index, with some being more resilient, with a smaller magnitude of the fall, and for others, the financial market being less generous during the COVID-19 pandemic. The processing shows that entities operating in the manufacturing and chemical-pharmaceutical industries in the sample are more resistant to the downturn compared to BET over the period analyzed, but recover more slowly than companies that are included in the BET portfolio. In contrast, entities in the financial services sector recover more quickly than companies that follow the trend of the financial market, which is also an area of activity that is undergoing more rapid transformation. The cross-sectional analysis carried out using multivariate data analysis models, revealed the link between the business area of companies listed on the BSE during the COVID-19 pandemic, the average return on securities, the chance of winning, the risk assumed by investors and the type of shares (offensive, defensive), as determined by comparison with the financial market trend. The results showed that investments in the securities of entities operating in the manufacturing and energy-oil sectors in the sample analyzed were characterized by high associated risk but were offensive relative to the BET during the pandemic period. However, between the two sectors – manufacturing and energy-oil – an investor in the manufacturing sector is also more likely to have a high associated return on equity in a crisis period (in addition to holding an offensive stock position relative to BET) than an investor in the securities of energy-oil entities, where the return on equity is rather low during the COVID-19 pandemic. Consequently, the lesson to be learned from the research, which may also be a suggestion to investors (given the uncertainty we are going through – a new crisis may occur), is that they should combine portfolios, when making the investment decision, from manufacturing with financial services or from chemical-pharmaceutical with financial services or from real estate with financial services. We believe that this is also the added knowledge we bring through our research: we did not find in the literature a clear association between the shares of listed entities and the phases of resilience to characterize the behavior of companies in times of crisis and in emerging economies.

Therefore, the research results can be used as a reference for potential investors to choose or invest in stocks that represent the optimal type of portfolio in times of crisis and in emerging economies given the resilience stages.

The study has practical implications in terms of guiding investors to invest funds in a diversified way, as external risk factors have proven to be completely unpredictable, which demonstrates once again that in economics one cannot make predictions, only forecasts. As the sampled entities are public interest entities, the social implications of the study are obvious. The contribution of our study toward a new approach in the literature is justified by the fact that from the review of studies found in the scientific literature, it is found that no analysis of the resilience of listed companies by the three phases of resilience and by business areas has yet been conducted for companies operating in emerging economies. Therefore, the added knowledge provided by this study is found in the very assessment of resilience through the phasing carried out and attached to the areas of activity of the companies included in the sample in a period of crisis and in an emerging economy such as Romania.

The research undertaken also has limitations, given the limited sample of companies listed in the regulated market in Romania. Subsequently, it is intended to expand the sample by including companies listed in other emerging countries in Europe and beyond.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Maria Grosu

Maria Grosu is Associate Professor, PhD, and a member the Department of Accounting, Business Information Systems and Statistics of the Faculty of Economics and Business Administration of Alexandru Ioan Cuza University of Iasi, Romania. She teaches: Financial Accounting; IFRS Accounting; Financial Audit Approach. Her main areas of interest are the application of IFRS in accounting, the enhancement of financial and non-financial reporting, quality in financial auditing, corporate governance principles, and sustainable reporting.

Camelia Cătălina Mihalciuc

Camelia Cătălina Mihalciuc is Associate Professor, PhD, and a member the Department of Accounting, Auditing and Finance of the Faculty of Economics, Administration and Business of Stefan cel Mare University of Suceava, Romania. She teaches: Financial Accounting; Management Accounting; Accounting and Managerial Control. Her main areas of interest are related to management accounting, the enhancement of financial and non-financial reporting, managerial control, and sustainable reporting.

Liviu George Maha

Liviu-George Maha is Full Professor, PhD Habil., specialized in International Economics and Business, member of the Department of Economics and International Relations, Faculty of Economics and Business Administration, Alexandru Ioan Cuza University of Iasi, Romania. His research interests include economic resilience, international trade, European economy, international labour migration, foreign direct investments, project management etc. He teaches: Economics; Policies, Institutions and Regulations in International Trade; European Business Environment; International Project Management etc.

Ciprian Apostol

Ciprian Apostol is Associate Professor, PhD, and a member the Department of Accounting, Business Information Systems and Statistics of the Faculty of Economics and Business Administration of Alexandru Ioan Cuza University of Iasi, Romania. He teaches: Financial Accounting; Financial-Accounting Management of the Company, Advanced Economic; Financial Analysis; Company Valuation; Economic Diagnosis; Performance and Risk in Business. His main areas of interest are represented by advanced economic and financial analysis, company valuation, the enhancement of financial and non-financial reporting, and performance and risk in business.

References

- Adžić, Slobodan, and Jarrah Al-Mansour. 2021. “The Negative Impact of COVID-19 on Firms: Insights from Serbia.” Eastern European Economics 59 (5): 472–86. https://doi.org/10.1080/00128775.2021.1953387.

- Alexander, Gordon J. 2009. “From Markowitz to Modern Risk Management.” European Journal of Finance 15 (5–6): 451–61. https://doi.org/10.1080/13518470902853566.