Abstract

Few recent geographic studies have focused on how market dynamics might explain macroregional shifts in industrial production. This article examines the pivoting of semiconductor manufacturing toward East Asia during the 2010s, drawing upon proprietary data sets and interviews with leading semiconductor firms. Building on the existing conceptions of user-producer collaborations in economic geography, I conceptualize the relevance of market dynamics for explaining industrial-geographic change. In particular, I specify how customer intimacy in intermediate markets and demand responsiveness in end markets, as two critical dimensions of market dynamics, create strong demand for new chip-making capacity, and how spatial and relational proximity can strengthen interfirm collaboration and customer intimacy in semiconductor production networks. Empirically, market dynamics prompting massive growth in East Asian chip-making capacity are manifested in new product transition and chip demand from global lead firms in the information and communications technology sector and their manufacturing partners mostly located in East Asia. Demand responsiveness to new lead firms and end markets within East Asia has also induced chip design and new capacity to be colocated in the region. Customer intimacy between chip design firms and their foundry providers has led to massive growth of outsourced wafer fabrication in East Asia. Complementing supply-side explanations, such as state support and technological leveraging, this article’s core findings on demand-led market dynamics in explaining geographic shifts in semiconductor manufacturing contribute not only to the studies of global production networks in high-tech industries but also to the renewed interest among geographers in market dynamics and their consequences for uneven development.

Geographers’ interest in semiconductors was strong during the 1980s and the 1990s, but this body of work focused primarily on the domestic restructuring of the semiconductor industry in the US (e.g., Scott Citation1988; Angel Citation1994; Óhuallacháin Citation1997). Evolving from the earlier trends toward internationalization and the rise of Japan as a serious contender to American leadership, the global semiconductor industry has undergone significant geographic shifts since the 2000s. The global center of gravity for integrated circuits (IC) manufacturing or fabrication, known as chip making in this article, has shifted much further toward East Asia beyond Japan. By the late 2010s, East Asia accounted for over 80 percent of worldwide IC fabrication capacity, up from 60 percent in 2000 (almost half in Japan, then the world’s largest producer). In 2018, Taiwan and South Korea became the two largest producers, together accounting for 45 percent of world capacity. Chip-making capacity in China and Singapore was respectively larger than the US and Europe. The cutting-edge fabs or wafer fabrication facilities of leading chipmakers in Taiwan (TSMC) and South Korea (Samsung) are now more advanced than the home fabs of Intel, the long-time industry and technology leader.

This geographic pivot toward East Asia in global semiconductor manufacturing has taken place at the same time when chip demand by customers (i.e., device manufacturers) in the information and communications technology (ICT) sector has also become much more concentrated in East Asia (see more in Yeung Citation2022). The market dynamics of chip making are largely driven by the application-specific demand of these ICT customers in personal computers (PCs), data storage (servers), and wireless devices (e.g., smartphones and tablets), and their need for demand responsiveness in highly competitive end markets worldwide. These two broad trends in semiconductor manufacturing and market dynamics are clearly interrelated. They have enormous implications for academic research and public policy (e.g., 2020/2021 US sanctions on China’s chipmakers and their suppliers and customers).

How then can we account for this pivoting of chip-making capacity toward East Asia, particularly during the 2010s? Unlike other end-product industries, such as automotive, apparel, and consumer electronics, much of this new capacity growth in East Asia came from the heavy investment of leading domestic semiconductor firms, rather than the international relocation of American or European semiconductor firms. In this sense, the term geographic shift does not entail the actual locational shifts in chip-making fabs (e.g., from the US to East Asia) but reflects the changing relative shares of different macroregions in global semiconductor manufacturing. I argue that it is insufficient to explain this very high concentration of semiconductor manufacturing within several East Asian economies on the basis of only supply-side factors unique to the macroregion (e.g., strong developmental state policy and technological upgrading in national economies).

This renewed global competition in semiconductors has accentuated the importance of demand-led market dynamics as a possible explanatory driver for the massive chip-making capacity growth in East Asia. Changing market dynamics have created new demand for specific kinds of chips requiring new cutting-edge fabs and/or capacity growth that subsequently take place within East Asia. These market dynamics are driven by product transitions in computers (to notebook PCs and data centers) and wireless communications (to smartphones and tablets) and technological transition in digital chip design led by fabless semiconductor firms (i.e., without their own fabs).

This article examines how these upstream fabless firms and downstream device manufacturers serve as the key customers of East Asian chipmakers, and in turn influence their geography of fab location and capacity growth. The global semiconductor industry, however, is rather complex, and any major geographic shift is unlikely caused by a singular driver or independent variable such as state support, modularization in production, and chip-making ecosystems. While focusing on market dynamics as a demand-led explanation—albeit relatively underdeveloped in the existing literature—this article will engage briefly with these supply-side explanations where appropriate and clarify how demand-led explanation might complement them.

In economic geography, some recent work on supply-side explanations has examined the coconstitutive role of the state, industrial policy, and the global linkages of domestic lead firms in East Asia’s semiconductor industry (Yeung Citation2016, Citation2022; Hsu Citation2017; Grimes and Du Citation2021). Even though the US remains as the leader in designing microprocessors and programmable chips (termed logic chips) used in ICT devices and digital platforms, the fabrication of most logic and memory chips is now taking place in cutting-edge fabs located throughout East Asia, particularly those in Taiwan and South Korea. Still, few geographers have examined how changing market dynamics might account for these geographic (re)configurations of semiconductor global production networks (GPNs).

In the much larger body of literature on the semiconductor industry in development studies and innovation studies, the explanatory focus is commonly premised on the strong role of the state, technological leveraging, and/or national innovation systems (e.g., Dibiaggio, Nasiriyar, and Nesta Citation2014; Hwang and Choung Citation2014; Ernst Citation2016; Lee and Malerba Citation2017; Shin Citation2017; Fuller Citation2019). Much of the earlier work on East Asia has also analyzed the latecomer catching up by domestic semiconductor firms during the 1980s and the 1990s (e.g., Mathews and Cho Citation2000; Chu Citation2013; Yap and Rasiah Citation2017; Lee Citation2019). A few exceptions have focused on industrial users in shaping technological innovation in semiconductors (Ernst Citation2005; Fontana and Malerba Citation2010; Adams, Fontana, and Malerba Citation2013; Park Citation2019). Others have deployed the evolutionary perspectives of Nelson and Winter (Citation1982) and Langlois and Robertson (Citation1995) to examine the changing industrial structure, production processes, and technological shifts in the semiconductor industry (e.g., Linden and Somaya Citation2003; Dibiaggio Citation2007; Glimstedt, Bratt, and Karlsson Citation2010; Nepelski and De Prato Citation2018). Overall, this large literature has not systematically examined market dynamics and their causal role in shaping the geography of global semiconductor production.

Meanwhile, economic geographers have long recognized the importance of the customer in producer-user interfaces in collaborative knowledge development (Gertler Citation1995, Citation2003; Grabher, Ibert, and Flohr Citation2008) and, more recently, the changing market imperative in GPNs (Yeung and Coe Citation2015; Horner and Murphy Citation2018; Dodge Citation2020). Building on this work, the article is theoretically grounded in the recent literature on GPNs in economic geography and global value chains in the wider social sciences (Coe and Yeung Citation2019; Ponte, Gereffi, and Raj-Reichert Citation2019; Kano, Tsang, and Yeung Citation2020; Coe Citation2021). I argue that the semiconductor industry has specific attributes that accentuate the causal relevance of the market imperative in Coe and Yeung’s (Citation2015) GPN 2.0 theory. The pivoting of chip-making capacity toward East Asia by the late 2010s can be explained by two analytical pathways of market dynamics as a causal mechanism. The first causal pathway for capacity growth refers to the massive demand for East Asia–made chips by intermediate customers—global lead firms and their outsourced manufacturing partners assembling final devices/products in computer and data storage and wireless communications. In 2018, these two top market applications alone accounted for two-thirds of the entire semiconductor industry’s historic peak revenue of $485 billion. The second explanatory pathway is premised on the rise of East Asia as the home region of not only the final assembly of ICT devices but more importantly also new global lead firms in PCs and smartphones, and rapidly growing end markets for these products. Since the 2000s, much final assembly of ICT devices has been taking place in East Asian economies such as China (Sun and Grimes Citation2017; Xing Citation2021; Yeung Citation2022). By the late 2010s, East Asia also became one of the most significant end markets for these ICT devices, accentuating the role of home market dynamics in driving chip-making capacity growth within the macroregion.

Methodologically, this article draws on comprehensive material collected through custom data acquisition and original interviews. In 2016 and 2019, I acquired, at considerable cost, proprietary data sets on semiconductors and other top ten global lead firms in PCs, mobile handsets, and consumer electronics from IHS Markit, a leading industry information provider. The semiconductor data sets are highly detailed, such as custom fab-level data on chip-making locations, key customers, and product categories (e.g., logic, memory, and foundry). Complementing these data sets are my twenty personal interviews conducted in 2017 and 2018 with senior executives from fifteen leading semiconductor firms, as part of a large-scale study of electronics GPNs in East Asia (see Yeung Citation2022). These fifteen firms range from integrated device manufacturing (IDM) firms with their own fabs (e.g., Samsung, Micron, STMicroelectronics, and NXP) to fabless chip design firms (e.g., Qualcomm, Nvidia, MediaTek, and AMD) supported by top providers of outsourced foundry production (Samsung foundry and UMC) and outsourced assembly, packaging, and testing services (ASE). Sixteen interviewees were at the rank of (senior) vice presidents or higher. All face-to-face interviews lasted one to two hours and were recorded and transcribed according to strict research protocols. Due to confidentiality consent, I will anonymize the names of firms and individuals when quoting directly from them.

The article has three main sections before conclusion. The next section sets up the analytical framework by conceptualizing market dynamics in the GPNs of different industries, drawing upon earlier work on customers and markets in economic geography and innovation studies. The second section specifies different customers and key dimensions of market dynamics in the semiconductor industry that inform my empirical analysis. The penultimate empirical section describes the global shift in semiconductor manufacturing toward East Asia during the 2010s and analyzes the specificities of market dynamics that explain this geographic shift.

Conceptualizing Market Dynamics in GPNs

Since the early 2000s, geographers have developed a distinct theoretical approach to analyze uneven development—the GPN perspective (Henderson et al. Citation2002; Coe et al. Citation2004; Yeung Citation2009, Citation2021a; Coe Citation2021). This GPN 1.0 approach has built upon and extended further the earlier work on global value chains (Ponte, Gereffi, and Raj-Reichert Citation2019; Kano, Tsang, and Yeung Citation2020). Recently, Coe and Yeung’s (Citation2015) GPN 2.0 theory has taken a new conceptual step by theorizing the organizational dynamics of GPNs and applying them to explaining uneven geographic outcomes. As reviewed in Coe and Yeung (Citation2019) and Yeung (Citation2021b), the deployment of this GPN 2.0 theory in geographic studies remains quite scattered and diffuse. This article’s focus on market dynamics in the global semiconductor industry offers a potential conceptual advancement in this GPN literature. The peculiarities of semiconductors and the broader industry point to the likely conceptual relevance of some causal drivers in the GPN 2.0 theory such as the market imperative, financial discipline, and the wider risk environment. Focusing on semiconductor manufacturing as a much more capital- and technology-intensive industry, this article further theorizes the complex relationships between market dynamics and geographically dispersed production networks.

In GPN 2.0 theory, “market imperative” has been conceptualized as “a complex and negotiated outcome of the producer-customer interface through which both producers and customers are actively involved in market creation” (Coe and Yeung Citation2015, 95; original italics). This iterative process of market making represents one of the causal dynamics determining the different organizational outcomes of GPNs. Producers and customers can be defined by their respective roles in these networks, ranging from merchandisers, manufacturers, and suppliers to distributors, intermediaries, and final consumers or end markets. The geographic configurations of production networks are shaped by competitive market pressures influencing lead firms, suppliers of intermediate goods, and final producers of finished goods and services.

But what constitutes market dynamics and how do they drive production networks in relation to the diverse roles of customers and producers worldwide? In advanced economies, customer-centric innovation in intermediate markets and demand responsiveness in end markets are two key dimensions of market dynamics in GPNs. Termed customer intimacy in this article, this concept of mutually dependent relationships between customers and producers in intermediate markets has been quite well developed in economic geography. In his pioneering work, Gertler (Citation1995, Citation2003) argued that closeness between collaborating parties, defined as being there in both spatial and organizational-cultural proximity, was critical in the successful development and adoption of advanced process technologies between producers of industrial machinery in Germany and their customers (users) in Canada. This conception of being there has also fostered critical understandings of tacit knowledge and relational proximity in relational economic geography (Bathelt and Glückler Citation2003; Yeung Citation2005, Citation2021a; Murphy Citation2012).

Further economic geography work on technology users has theorized the central importance of customers in innovation and knowledge production. Grabher, Ibert, and Flohr (Citation2008) and Grabher and Ibert (Citation2018) argue that innovative firms increasingly harness user knowledge such that organizational distinctions between producers and customers are blurred as their relational proximity increases. To them, customer intimacy premised on greater relational proximity in knowledge production networks has evolved into an emerging class of user-producer relationship known as codevelopment. Users well embedded in innovative networks characterized by knowledge cocreation are termed Schumpeterian customers who exhibit the greatest intimacy with producers in these knowledge ecologies.

Drawing on the above literature, I define customer intimacy as codependency between users as customers and producers as suppliers through their highly collaborative interfirm relationships in demand fulfillment, codevelopment of technologies, and strategic-organizational alignments that can be engendered through both spatial and relational proximity. In diverse GPNs comprising spatially dispersed value activities, customer intimacy is not just driven by spatial proximity between users and producers in localized clusters—a long-standing observation in economic geography and innovation studies. Customer intimacy can also be strengthened by high relational proximity through close customer-producer collaboration across different localities via what Bathelt, Malmberg, and Maskell (Citation2004) term global pipelines (Ascani et al. Citation2020; Balland, Boschma, and Frenken Citation2020).

In practice, intimacy is necessarily two way because it refers to two sides of the same interfirm relationship. In this sense, customer intimacy is also supplier intimacy because a customer needs to know much about its supplier’s capability, commitment, and reliability in order to trust its support and services. In such mutual and trusting relationships, a supplier is often known as a strategic partner to the customer. For brevity, this article uses the term customer intimacy throughout. The term is also commonly mentioned by my interviewees from leading semiconductor firms.

In the Global South, market dynamics may play out quite differently. The role of customer intimacy framed within the above technological and production relationships between customers and suppliers in intermediate markets is less relevant vis-à-vis the need for demand responsiveness in end markets for finished goods. This concept of demand-led corporate responses was first identified in Feenstra and Hamilton’s (Citation2006) work on how business groups in South Korea and Taiwan responded differently to market demand from big buyers (large retailers and distributors) in the US and how their differential demand responsiveness led to divergent development trajectories in home economies (see also Hamilton and Kao Citation2018). More recent work has reconceptualized these emerging and shifting end markets critical to the geographic expansion of local and regional production networks in the Global South (Kaplinsky and Farooki Citation2011; Horner and Nadvi Citation2018).

In , I conceptualize the above two key dimensions of market dynamics in GPNs across different industries and economies: (1) customer intimacy in industrial markets for intermediate goods and (2) demand responsiveness in end markets for final goods. The customer for different types of producer firms in GPNs is defined in relation to their value activity and the market(s) for their products or services. Such value activity in a production network is broken down into upstream activity in design and research and development (R&D), production of critical inputs and modules, and the final assembly of end products. In Coe and Yeung’s (Citation2015) GPN 2.0 theory, a transnational corporation may internalize all of these value activities within its intrafirm production network, but most lead firms tend to outsource some of these activities, such as certain parts and components and/or final assembly, to specialized suppliers or platform/technology leaders and outsourced manufacturers.

Table 1 Market Dynamics and Customer Relationships in GPNs

Clearly, the customer may be a different entity to different firms even in the same production network. First, the relationship between a design and R&D firm and producers of industrial goods in intermediate markets is likely to be greater in customer intimacy due to the knowledge-intensive nature of its value activity mostly located in high-tech industrial clusters. As conceptualized in Gertler (Citation1995, Citation2003) and Grabher, Ibert, and Flohr (Citation2008), this high-value design work is closely linked to the implementation of new technologies and/or the cocreation or design-in of new products and services by industrial users. Spatial proximity through colocation of activities can strengthen interfirm collaboration and customer intimacy between producers and users of these industrial goods and services.

Second, the key customers to these producers of critical inputs may vary from lead firms in original equipment manufacturing (OEM) to their outsourced manufacturers. Due to the critical nature of these essential inputs, such as core ingredients, components, and modules, network relationships between specialized suppliers and their key customers in final assembly are likely to be strategic and interdependent. In this strategic partnership, defined in Yeung and Coe (Citation2015, 49; my emphasis) as “the collaboration, coevolution, and joint development of a lead firm and its strategic partner(s) or key suppliers in the same global production network,” final producers often rely on strong supplier ecosystems/intimacy to sustain their strategic partnership with specialized suppliers.

Third, the assembly of finished goods for customers in end markets worldwide tends to take place in low-cost locations in the Global South. Market dynamics in these end markets are typically manifested through high demand responsiveness from producers, that is, OEM lead firms or their outsourced manufacturers responding to new competition and product fluctuations.

Specifying Market Dynamics in Semiconductor Production Networks

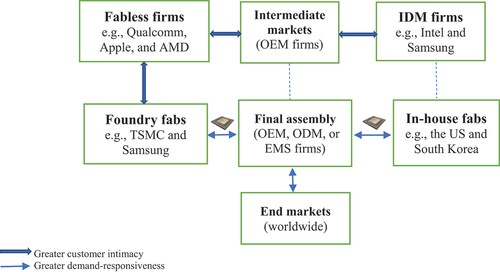

differentiates key firm actors and their value activity in semiconductor production networks. To simplify it, I have excluded specialized suppliers of software, equipment, and materials necessary for semiconductor manufacturing. In general, lead firms in semiconductor production networks are those holding and controlling the intellectual property rights, patents, and design blueprints of integrated circuits. There are two main types of semiconductor lead firms differentiated in relation to their extent of vertical integration (i.e., with or without their own fabs). IDM firms are those engaging in both the design and fabrication of semiconductors, whereas fabless firms specialize in chip design and outsource wafer fabrication to their manufacturing partners known as foundry providers. These two types of lead firms are directly involved in device design and product definition—often in close collaboration with their industrial customers such as OEM lead firms producing final goods for end markets ().

Table 2 Key Firm Actors and Value Activity in Semiconductor Production Networks

So how do market dynamics shape semiconductor production networks? In theory, we start with new or changing demand in end products/markets for chip applications. New product applications may entail demand for different kinds of semiconductor chips (e.g., application-specific logic chips and high-density memory chips). This can be seen in the almost monopolistic dominance of Intel and its microprocessor (logic) chips in tandem with the rise of PCs during the 1980s that subsequently reduced the market significance of mainframes and minicomputers (Dedrick and Kraemer Citation1998; Campbell-Kelly and Garcia-Swartz Citation2015; Yeung Citation2022).

New end markets may entail greater demand for technologically advanced chips that are smaller, energy efficient, and more powerful in computation. The rise of the digital platform economy since the 2010s (Kenney and Zysman Citation2020) and the widespread reach of smartphones represent two such new end markets that create an incessant demand for new generation logic and memory chips capable of delivering high-performance data processing and storage. As IDM and fabless lead firms cater to these new products and changing end markets through their innovative chip design and applications, they work closely with key OEM lead firm customers to deliver chips with the right application specifications and performance. Such interfirm relationships are often mutually dependent and relatively enduring in nature.

specifies these market dynamics in the different segments of semiconductor production networks. To begin, OEM customer-chip producer relationships in the semiconductor intermediate market are characterized as greater in customer intimacy that applies to both IDM and fabless firms. Here, customer intimacy operates through close interfirm relations (relational proximity) evident in the strategic desire for design-ins of IDM/fabless chips with the key products of OEM lead firms for end markets (e.g., PCs and smartphones). This entails strong customer orientation in IDM or fabless firms’ chip design and product functionality to achieve a design-in fit with their OEM customers’ product roadmaps. As evident in Dibiaggio (Citation2007) and Adams, Fontana, and Malerba (Citation2013), industrial users, such as OEM lead firms and their key suppliers of electronics modules or systems, are highly critical in the innovation capacity of chipmakers and their production networks.

Figure 1. Market dynamics in semiconductor production networks.

EMS = electronics manufacturing services; IDM = integrated device manufacturing; ODM = original design manufacturing; OEM = original equipment manufacturing.

Source: Interviews with IDM and fabless firms, foundry providers, OEM, and ODM firms.

In fabless-foundry chip making in , customer intimacy is expressed in mutual commitment through advance order from top fabless customers and guaranteed supply adequacy by their foundry providers. For foundry firms to invest heavily in new fabs and capacity, they need assurance of future demand for their new cutting-edge process technologies, that is, committed orders from top fabless customers for high-volume production using these process nodes. Equally, top fabless firms must secure their supply adequacy from foundry providers to fulfill chip demand from their OEM lead firm customers (frequent launches of new end products).

As evident in the next empirical section, strong fabless-foundry relationship is critical to the competitive success of fabless firms in new application markets for logic chips in smartphones, notebook PCs, and servers during the 2010s. In earlier studies (Ernst Citation2005; Dibiaggio Citation2007; Fontana and Malerba Citation2010; Epicoco Citation2013), fabless firms were driven by a strong desire to ensure the market dominance of their application-specific chips through a high level of involvement with key OEM customers early in their chip design and product development process. Ernst (Citation2005) thus argues strongly that customer intimacy in chip design and production has exposed the limits of modularity as an industrial-organizational platform, in contrast to the popularity of modular production in ICT end products (Sturgeon Citation2002; Gereffi, Humphrey, and Sturgeon Citation2005).

In the most advanced semiconductor manufacturing, the very high share of several top fabless firms in intermediate markets for logic chips is predicated on their greater intimacy with trusted foundry providers who are committed to expanding fab capacity and preferential allocation, and coevolve with their fabless customers through intense technological interactions in chip design and implementation of custom chip-making processes. Rapidly changing chip design and fabrication technologies have created much product uncertainty and knowledge complexity that cannot be easily reduced through codification and modularization.

To serve the highly complex technical demand of their top fabless customers and to achieve rapid ramp-up in risk production and subsequently high yield in mass production, top foundry providers need to master the necessary know-how of fabricating highly miniaturized and sophisticated logic chips in their most advanced fabs. As explained by the senior vice president of top five semiconductor firm #10, this capital- and knowledge-intensive wafer fabrication can take over one thousand steps and two or more months to complete, making it very hard to master mass production at the cutting-edge technology or process nodes (seven nanometers in 2018, five nanometers in 2020, and three nanometers by mid-2022).

Further downstream in , OEM lead firms themselves are subject to immense competitive pressures in end markets worldwide that accentuate the need for high demand responsiveness and technological innovation in their final products. These new products (e.g., notebook PCs, tablets, and smartphones) are powered by ever-more advanced chips with higher computing capability (logic chips) and much larger storage capacity (memory chips). To OEM lead firm customers, the fabrication of cutting-edge chips by their chip suppliers’ in-house fabs (IDM firms in memory chips) or foundry fabs (for fabless firms in logic chips) must be closely calibrated and managed in relation to the final assembly sites of these ICT devices because chip supply can be a serious choke point in their supply chains (e.g., the 2021 global chip shortages for carmakers and ICT producers).

Through these interfirm production networks, the intense drive for high demand responsiveness in end markets (e.g., frequent new product launches and localization of product configurations) feeds back recursively from OEM customers to their top chip suppliers and their in-house or foundry fabs, creating new demand pressures for fab capacity expansion and (re)allocation to ensure supply adequacy, consistent yield, and timely delivery. Over time, these market pressures on chipmakers to enhance demand responsiveness lead to new rounds of capital investment in fabs and/or capacity expansion by leading IDM firms (logic and memory chips) and foundry firms (logic chips).

Preempting my empirical analysis, the causal mechanism of market dynamics shaping the pivoting of global semiconductor capacity toward East Asia during the 2010s operates through two pathways: (1) the extension of East Asia’s existing leadership in chip making and (2) the rise of very significant new OEM customers and end markets in East Asia. First, the much greater chip demand by lead firms for applications in their ICT devices has benefited existing IDM firms and foundry providers in East Asia that had already attained market leadership by the late 2000s (). This demand-responsive market dynamic has incentivized chipmakers in East Asia to invest in new fabs and/or capacity expansion, accounting for much of the world’s semiconductor manufacturing capacity growth during the 2010s.

Second, several top OEM lead firms in smartphones, PCs, and other consumer electronics have emerged from new and expanding end markets in East Asia and, in particular, China since the 2010s. This far greater significance of East Asia as both the home region of lead firms and a large and growing end market has not only reinforced the above demand-responsive dynamic for expanding preexisting chip-making capacity in the region but also accentuated the significance of spatial proximity for top American fabless firms to develop greater customer intimacy with East Asian lead firms by being there in the region. Setting up their R&D centers in East Asia, these fabless firms can achieve greater design-ins of their application-specific logic chips with the key products of East Asian lead firms for end markets worldwide. In a recursive way, the geographic copresence of American fabless firms in East Asia have further strengthened their intimate and mutually dependent relationship with top foundry providers in Taiwan, South Korea, and China, prompting the latter’s further investment in fab capacity throughout much of the 2010s.

How might this causal mechanism of demand-led market dynamics driving chip-making capacity growth in East Asia be reconciled with several supply-side explanations, such as state support, technological innovation, and financial market preferences,that collectively constitute the sufficient condition for explaining the geographic shifts in global chip making? While these new market dynamics serve as a necessary condition for such geographic shifts, the very substantial capital investment in new fabs and capacity growth in anticipation of new demand and market applications would likely require the concomitant supportive industrial policies by the respective governments in East Asia (Mathews and Cho Citation2000; Chu Citation2013; Yeung Citation2016; Yap and Rasiah Citation2017; Fuller Citation2019; Grimes and Du Citation2021).

Technological breakthroughs and organizational innovation in chip production and capital market preferences are also important in allowing East Asian foundry providers to catch up through technological leveraging to meet the technologically demanding challenge of making logic chips for new ICT end products. The separation of chip design and wafer fabrication was made possible during the 1990s by the use of computer-aided design technology and electronic design automation software from the US to codify knowledge of device characteristics in computer models and to provide digital interfaces between the design and fabrication of integrated circuits. Described by Langlois (Citation2003, 373) as “perhaps the most significant organizational development of the 1990s” in the semiconductor industry, this tightly coupled interfirm model of fabless-foundry production networks has shaken up the entire industry previously dominated by IDM firms and captive producers in the US.

In Brown and Linden’s (Citation2011) capital market explanation, the unprecedented window of opportunity for East Asian foundry firms owes much to the extremely high cost of building new fabs that have deterred shareholder-minded American IDM firms since the late 1990s. Prompted by American venture capital’s preference for investing in high-value and potentially high-return chip design work, more fabless firms have emerged in Silicon Valley and outsourced wafer fabrication to foundry providers located throughout East Asian economies (Kenney Citation2011; Nenni and McLellan Citation2019). In this geographic fragmentation of design and production, the international outsourcing of chip making to East Asian foundry fabs might seem similar to the earlier trend in the final assembly of ICT end products through which production modularization has enabled the massive East Asian presence of contract manufacturers from North America and Taiwan (Sturgeon Citation2002; Sun and Grimes Citation2017; Xing Citation2021). In practice and as evident below, there are intricate technological-organizational differences that mitigate the significance of modularity in chip making. The next section will identify major geographic and organizational shifts in the 2010s and explain them in relation to market dynamics and its two causal pathways.

Chips and Fabs: Explaining Global Shifts in Semiconductor Manufacturing during the 2010s

The 1980s and the 1990s witnessed major upheavals and restructuring of the global semiconductor industry (Angel Citation1994; Mazurek Citation1999; Mathews and Cho Citation2000; Brown and Linden Citation2011; Yeung Citation2022). As Japanese and, later, South Korean IDM firms became top memory producers and American IDM firms remained dominant in microprocessors, two major changes to the industry started to take place—the fabless revolution in logic chip design and the rise of pureplay foundry providers dedicated to serving external customers in logic chips (). These technological and production network shifts would have profound impact on the industry’s subsequent development and the changing geography of production in the next three decades.

By the early 2000s, however, this impact was still limited in scale and geographic reach. In 2000, the total revenue of all fabless firms reached $16.7 billion. But the global semiconductor market was already thirteen times larger at $221 billion, led by Intel’s $30 billion revenue or 14 percent share (IHS Markit data set). There were only a handful of pureplay foundry providers (e.g., TSMC and UMC in Taiwan) whose trailing-edge fabs at 150–180 nanometers were still behind top IDM firms in process technologies (e.g., 130 nanometers in Intel, Micron, Texas Instruments, and STMicroelectronics). The total revenue of all pureplay foundry providers was a meager $10.2 billion or one-third of the market leader Intel. In brief, the industry prior to the 2000s was dominated by top IDM firms and their in-house fabs in the US, Europe (Germany, France, and Italy), Japan, and South Korea.

Since the early 2000s, the world market for semiconductors has changed profoundly, and East Asia has emerged as the dominant macroregion for manufacturing logic and memory chips. Worldwide revenue doubled in size from $240 billion in 2005 to $485 billion in 2018 (down slightly to $466 billion in 2020 but forecasted by the World Semiconductor Trade Statistics to reach $551 billion in 2021 and $573 billion in 2022). And yet in this industry with over four thousand firms, market concentration has grown further, with the top ten firms’ share increasing from 48 percent in 2005 to 60 percent in 2018. Leading semiconductor firms from the US, South Korea, and Taiwan dominated the industry’s top ten largest firms by revenue in 2018, eclipsing top European and Japanese firms that were significant up to the mid-2000s. Throughout the 2005–20 period, three firms were top leaders in their respective segments—Intel in microprocessors, Samsung in memory devices, and TSMC in foundry (mostly logic chips) due to their class-leading technology and continuous investment in in-house R&D and wafer fabs.

Meanwhile, three fabless firms in logic chips—Broadcom, Qualcomm, and Nvidia—moved dramatically from outside the top ten list in 2005 to within the top six by revenue in 2018 (and 2020). In , the rise of these top fabless firms in relation to new market applications in mobile and wireless ICT devices has created an enormous demand-responsive condition and intermediate market opportunity for the concomitant growth of their manufacturing partners—foundry providers primarily in East Asia. The revenue of TSMC, by far the largest market leader in foundry for logic chips, grew massively from only $5.1 billion in 2000 (Intel was $30 billion) to $31 billion in 2018 and $46 billion in 2020 (Intel still led with $73 billion), due to the massive demand for dedicated logic chip making from its key fabless customers (all top seven) and strong policy support from home institutions in Taiwan (Chu Citation2013; Hwang and Choung Citation2014; Hsu Citation2017; Yap and Rasiah Citation2017).

By the late 2010s, the global semiconductor market became codominated by both IDM firms and fabless firms from the US and East Asia, together with top foundry partners mostly based in East Asia (). Their main products are in memory, logic, and microprocessor chips that drive ICT devices (e.g., smartphones, personal computers, tablets, and servers) and other industrial applications (e.g., automotive and machinery). maps such changing geography of chip-making capacity during the 2000–18 period, based on the fab-by-fab aggregation of microdata on over three hundred fabs worldwide. During this period, the total number of IDM and foundry fabs remained fairly stable—325 fabs in 2000, increasing to 344 in 2010, and consolidating to 296 in 2018. However, the total capacity of these fabs worldwide increased very significantly, doubling between 2000 and 2010 and increasing further by 32 percent to reach almost seventeen million wafers per month in 2018. This growth rate matches fairly well the semiconductor market’s revenue growth during the same period—from $221 billion in 2000 to its historic peak at $485 billion in 2018.

Table 3 Geography of World Semiconductor Manufacturing by Fab Location, Product Applications, and Capacity, 2000–18 (Foreign Owned in Parentheses)

Geographically, substantial growth in new fabs and capacity has taken place in East Asia since the 2000s. While the two East Asian tigers of South Korea and Taiwan already had some capacity in 2000, they were still far behind Japan, the US, and, for Taiwan, even Europe. Fab capacity in China and Singapore was marginal. By 2018, Taiwan became the world’s largest producer of semiconductors at 4 million wafers per month, followed by South Korea (3.6 million), Japan (3.0 million), and China (2.2 million). Even the city-state of Singapore’s capacity of 1.04 million was slightly larger than Europe’s entire output of 1.02 million. The US fell to fifth place, with 1.8 million wafers per month from its 44 fabs. During the 2010s, there was a substantial consolidation of fabs in Japan, from 131 in 2010 to 87 in 2018. The US also witnessed the closure of almost a quarter of its fabs and a slight decline in total fab capacity. In terms of product applications, Taiwan and China were by far the largest foundry producers (mostly in logic chips), whereas South Korea and Japan led in memory chip making, with Singapore and Taiwan trailing behind. In both logic and memory chips, the US and Europe experienced declining fab numbers and capacity throughout the 2010s.

This enormous growth in global semiconductor manufacturing capacity and its pivot toward East Asia during the 2010s has been driven by the tremendous growth in intermediate market demand for logic and memory chips in several major product applications in ICT devices (PCs and smartphones), data center servers, and consumer electronics (e.g., TVs). provides a firm-level perspective to the above macro-observations. In 2018, logic chips accounted for the vast majority of fab outputs by all top five foundry providers, led by Taiwan’s TSMC. Contributing to Taiwan’s dominant role in foundry (), TSMC is ranked top in fabricating logic chips for smartphones, PCs, and industrial electronics, allocating some 54 percent of its 2018 fab capacity to making smartphone logic chips designed by Apple (24 percent share of TSMC’s total revenue in 2019), HiSilicon (15 percent), Qualcomm (6 percent), and MediaTek (4.3 percent). Geographically, TSMC’s enormous fab capacity of 2.3 million wafers per month is heavily concentrated in its 8 fabs in Taiwan. While the US remains the dominant center of logic chip design (i.e., fabless firms mostly based in Silicon Valley) and microprocessor design and manufacturing (i.e., Intel in ), East Asian foundry providers are dominant in logic chip manufacturing.

Table 4 World’s Top Semiconductor Manufacturers by Fab Capacity, Main Applications, Fab Locations, and Markets, 2010 and 2018

In memory devices—the largest chip application with $165 billion revenue or 34 percent of the world market in 2018 (), the geography of chip manufacturing and fab locations is still based on the IDM-model of vertically integrated production networks highly concentrated in East Asia. As evident in , this market is controlled by four very large IDM firms—Samsung, SK Hynix, Micron, and Toshiba/Kioxia. Having emerged as the market leader in the late 1990s (Mathews and Cho Citation2000; Yeung Citation2016; Shin Citation2017), Samsung alone accounted for 40 percent of the memory market in 2018, the equivalent of the next two combined—SK Hynix (22 percent) and Micron (18 percent). Samsung and SK Hynix’s memory fabs are mostly located in South Korea, whereas all of Toshiba/Kioxia’s five fabs are in Japan (). In comparison, American IDM Micron’s seven fabs are more diversified geographically, but its four fabs in Singapore, Taiwan, and Japan account for 80 percent of its total capacity.

To sum up my analysis so far, several supply-side factors might help explain the initial rise of Japan in semiconductor manufacturing by the mid-1980s and the further shift of capacity growth toward East Asia (beyond Japan) by 2000, with the emergence of South Korea and Taiwan as significant players (Tiger chips in Mathews and Cho Citation2000). Coupled with firm-specific initiatives (e.g., Samsung and TSMC in Yeung Citation2016), favorable support from home governments and domestic capital markets in East Asia might provide sufficient initial conditions for their entry into chip making through investing in domestic capacity (Chu Citation2013; Yap and Rasiah Citation2017; Fuller Citation2019).

But once these East Asian economies and their national firms had gained a strong foothold in memory (South Korea as top producer in 2000) and foundry (Taiwan as top but a still small producer in 2000), their massive capacity growth in the 2000s and the 2010s—from 60 percent of world’s capacity in 2000 (half from Japan) to more than 80 percent in 2018 in —has as much to do with new market dynamics analyzed in greater detail in Yeung (Citation2022): (1) the massive growth in ICT devices since the 2000s, such as peak shipments of PCs in 2011 and smartphones in 2018, and the geographic concentration of their final assembly in East Asian locations; and (2) their enormous demand for memory chips and application-specific logic chips (processors).

In memory chips, the shift to East Asia had taken root since Japan’s challenge to the US in the mid-1980s and consolidated further with the rise of South Korea by 2000 (as top producer in ). Still, between 2000 and 2018, memory fab capacity in South Korea, Japan, Taiwan, and China (none in 2000) grew by almost five times: reflecting their demand responsiveness to the final assembly of ICT devices in East Asia such as notebook PCs primarily assembled in China and smartphones in China, Vietnam, and India (Grimes and Sun Citation2016; Gao et al. Citation2017; Yang Citation2017; Xing Citation2021; Yeung Citation2022).

In logic chips, fabless firms—mostly from the US with some exceptions (e.g., Taiwan’s MediaTek and China’s HiSilicon) and supplying to ICT devices—grew their share in worldwide semiconductor revenue from 7.6 percent in 2000 to 18.9 percent in 2010 and 32.8 percent in 2020! Their high growth in revenue and demand drove much foundry capacity growth between 2000 and 2018 in Taiwan (six times), China (from little in 2000 to very significant in 2018), and Singapore (small in 2000 and significant in 2018). Without incorporating these new demand-led market dynamics since 2000, particularly during the 2010s, it would be hard to understand why East Asia has become so dominant in semiconductor manufacturing by the late 2010s on the basis of only supply-side explanations. After all, who would all the chip-making capacity growth in Taiwan, South Korea, China, and Singapore serve?

The massive building of new fabs or capacity expansion in East Asian locations during the 2010s cannot be adequately explained by favorable state policies and strong support from localized ecosystems. These East Asian–specific conditions would be insufficient if there were no corresponding demand for memory and logic chips utilizing this new capacity in East Asia. Since the mid-2010s, building new fabs with the most advanced process technologies in logic and memory chip making has been exponentially expensive—$2 billion for twenty-eight nanometers, $15 billion for ten nanometers, and over $25 billion for three nanometers. Top semiconductor firms in East Asia would not have incurred massive capital expenditure in the 2010s to build new fabs without anticipating future demand and/or attaining strong commitment of orders from their top customers, for example, Apple’s iPhone chips exclusively utilizing TSMC’s latest process nodes in dedicated fabs since 2016 and OEM lead firms in PCs and servers as key customers for memory chips from Samsung and SK Hynix.

In 2000, the capital expenditure (capex) of Taiwan’s TSMC ($2.5 billion) and UMC ($2.6 billion) was still lower than or similar to leading IDM firms from the US (Intel—top with $6.7 billion, Texas Instruments at $2.8 billion, and Motorola at $2.4 billion), Europe (STMicroelectronics at $3.3 billion), and Japan ($1.6–1.8 billion each from NEC, Hitachi, and Fujitsu). By 2010, the capex of top two—Samsung ($9.7 billion) and TSMC ($6.1 billion)—was already larger than Intel ($5.2 billion). Most nonmemory IDM firms in the US, Europe, and Japan invested far less than top foundry firms. Since the late 2010s (2018–2021), these Big Three have remained by far the largest spenders—Samsung’s $28 billion in 2020 and 2021, TSMC’s $17 billion in 2020 and $30 billion in 2021, and Intel’s $14 billion in 2020 and $20 billion in 2021, followed by SK Hynix and SMIC. From only a 31 percent share of total capex in 2000, the top ten spenders in 2020 accounted for over 86 percent, with eight of them based in East Asia.

In short, while market dynamics are neither a sufficient condition in its own right nor an East Asian–specific phenomenon or explanation (though the Asia Pacific including China has become the largest macroregional market for semiconductors, PCs, and smartphones since the mid-2010s), it has become an indispensable condition in any robust explanation of why East Asia’s role in chip making has become so much more dominant by the late 2010s. This is not to say supply-side explanations, such as domestic state support and innovation systems in these East Asian economies, are not relevant. Nor are firm-specific initiatives unnecessary for understanding why they invest heavily in new fabs and process technologies. But without accounting for the demand-led market dynamics driving these firm-specific strategies within their GPNs, we will not be able to explain why further capacity growth in Taiwan and South Korea occurred in the 2010s when their respective developmental states had already become weaker and less interventionist, and their leading domestic semiconductor firms had depended less on state support and much more on their strategic coupling with GPNs (see Hamilton-Hart and Yeung Citation2021).

I now examine further empirically how market dynamics drive chip-making capacity growth through (1) the need for demand responsiveness by OEM lead firms and (2) the role of customer intimacy through geographic copresence. As conceptualized in , higher demand in end markets for certain final products is translated into larger assembly and shipment units by OEM lead firms and, correspondingly, greater production of chips by their key semiconductor suppliers. Demand responsiveness has contributed to greater chip-making capacity in East Asia during the 2010s in two ways (see also Yeung Citation2022). First, as end markets worldwide underwent new product or technology transition toward smartphones and tablets (wireless) and notebook PCs and data centers (computer and data storage), OEM lead firms worked with new chip suppliers at the cutting-edge of technology by switching from earlier IDM suppliers, such as Intel, Texas Instruments, and Motorola (Freescale/NXP) and their fabs in the US, to emerging fabless firms in Silicon Valley for application-specific logic chips.

In turn, the wafer fabrication orders from these rapidly growing fabless firms to their trusted foundry providers, mostly based in East Asia, increased dramatically and created the necessary demand precondition for massive new investment and growth in foundry capacity for logic chip making during the 2010s (). Meanwhile, OEM lead firms increased chip orders substantially from existing IDM suppliers in memory chips, adding further demand for capacity growth among leading memory IDM firms in East Asia. Second, the emergence of Asia as a high-growth end market for these new ICT devices provided a strong incentive for IDM and foundry chipmakers to locate and/or invest in new chip production capacity within East Asia and to increase their responsiveness to chip demand from OEM customers and their assembly operations located mostly in East and South Asia.

illustrates the world markets for three major ICT end products, and their top OEM lead firms and locations of final assembly during the 2010s. Overall, the mobile handsets market experienced exponential growth from 320 million units in 2010 to peak at 1.4 billion units in 2018, whereas the PC market declined by 23 percent (but increased to 303 million in 2020 and likely 357 million in 2021), and the TV market remained quite stable in shipment units. Market concentration was very high among the top six in mobile handsets (74 percent) and PCs (82 percent). In terms of revenue, mobile handsets became by far the largest end-product segment in the entire ICT sector, with some $443 billion in total market revenue in 2018. These findings point clearly to the high significance of mobile handsets and smartphones in particular as the key intermediate market for top semiconductor firms in logic and memory chips. In 2018, some $200 billion or 41 percent of the total $485 billion worth of semiconductors were directly consumed by OEM lead firms in mobile handsets ($126 billion by the top six alone) and PCs and servers ($55 billion by the top three). The remaining $285 billion semiconductors were acquired either through major electronics distributors or directly by other end users in different industries.

Table 5 World Markets in Mobile Handsets, Personal Computers, and Televisions by Top-Six OEM Firms, Worldwide Shipment, and Final Assembly, 2010 and 2018 (Shipment and Assembly in Millions of Units)

By the late 2010s, the Asia Pacific region (East Asia in particular) became much more than the overwhelming center for the final assembly of ICT products. The region also emerged as a major end market for these products. In mobile handsets, the market significance of China and Asia has become far greater since the mid-2010s, accounting for 50–60 percent of the global market for new purchases and replacement. China has also become a major and steady market for notebook PCs (almost as large as Western Europe) and TVs (the largest market). Together with Japan and the Asia Pacific, China has formed a formidable market bloc since the mid-2010s, rivaling North America in PC and tablet shipment and doubling North America and trebling Western Europe in TV shipment.

The need for demand responsiveness in both end markets (final assembly by OEM lead firms) and intermediate markets (logic and memory chips in end products) provides a necessary condition for explaining the pivoting of chip-making capacity to East Asia during the 2010s. In 2018, the Asia Pacific region (without Japan) accounted for $344 billion or 71 percent of the entire semiconductor market, followed by the Americas ($57 billion); Europe, the Middle East, and Africa ($49 billion); and Japan ($35 billion). In the Asia Pacific, three main categories of ICT end products were the key customers for semiconductors: wireless communications ($133 billion), computer and data storage ($131 billion), and consumer electronics ($32 billion).

Meanwhile, customer intimacy in chip design and foundry fabrication () has become a necessary condition for the timely supply of chips to OEM lead firms and their final assembly operations throughout East Asia. In chip design, customer intimacy with OEM lead firms matters for both IDM and fabless firms because their proprietary chip devices need to be designed in with the product and technology roadmaps of their OEM customers (). Revisiting the earlier conceptualization of being there, intense knowledge exchanges and cocreation often take place in situ between chip designers/engineers and their customers’ product development teams (Ernst Citation2005; Brown and Linden Citation2011; Nenni and McLellan Citation2019). In wafer fabrication, customer intimacy is also necessary between fabless firms and their foundry providers in East Asia. While fabless firms need to secure demand for their logic chips through design-in and roadmap alignment with their OEM customers, their chip supply can only be fulfilled if they have strong foundry support and guaranteed capacity allocation. In turn, trusted foundry providers can reciprocate this customer intimacy through investment in new fabs, capacity, and process innovation and customization.

This customer intimacy between fabless chip design firms and their OEM customers and foundry providers has shaped the geography of semiconductor production networks. provides some data on the world’s leading fabless firms. All of them are highly specialized and market leaders in logic chips (i.e., processor, graphics, and connectivity chips) used in smartphones, PCs, and other applications (e.g., artificial intelligence and servers). The US dominates in this group of leading fabless firms and only two (MediaTek and HiSilicon) are from East Asia. In chip design, my interviews with four top fabless firms in indicate their strong preference to be close to or even on site with their end customers’ R&D and manufacturing locations. Since most of the top six OEM firms in smartphones, PCs, and consumer electronics (e.g., TVs) in that require logic chips in their final products originate from East Asia (except Apple, Hewlett-Packard, and Dell from the US), Silicon Valley-based fabless firms have located large teams of design and R&D personnel in their offices throughout East Asia.

Table 6 World’s Top-Seven Fabless Lead Firms in Semiconductors by Main Applications and Products, Markets, and Key Foundry Providers, 2010 and 2018

As explained by the vice president of the top fifteen American Fabless-#5, “If you look at our competitors right now, nowadays they are obvious in Asia. A lot of competitors are actually Taiwan companies, like FocalTech and Novatek [both fabless]. Their response time is much faster compared to us as a US-based company. So, it’s very important for us to have R&D centers in Asia as well, especially if you want to do business with China-based [OEM] customers.” To the senior vice president of East Asian Foundry-#11 and the vice president of East Asian Foundry-#14, this need for greater customer intimacy between American fabless firms and their OEM customers in East Asia has created a strong incentive for these fabless firms to have their logic chips fabricated by the most advanced fabs located in East Asia. As noted in , all top six fabless firms source their logic chips from leading fabs in Taiwan (TSMC and UMC), South Korea (Samsung foundry), and Singapore (GlobalFoundries). Coupled with the huge pressure from demand responsiveness in end markets, greater intimacy between fabless firms and their OEM customers has led to massive growth in demand for logic chips and the corresponding demand for new foundry capacity in these East Asian locations.

In the most advanced logic chips (e.g., those by Apple, HiSilicon, and Qualcomm for smartphones), customer intimacy is particularly important because of high complexity in their fabrication and many unknown errors, high tacit know-how or secret sauce in chip making (much learning-by-doing), and difficulty in capacity allocation based on demand forecast and advance order (at least three to four months earlier). During chip design and wafer fabrication, many design changes and intense communications take place between fabless firms and their OEM customers and between fabless firms and their foundry providers. The designated foundry is often involved at the very beginning of new chip development through its shared device libraries and intellectual property rights (e.g., firm-specific process technologies). These intimate interactions and tacit knowledge accumulation make it very difficult to modularize chip production.

As indicated in , this customer intimacy results in a great deal of demand stability and path dependency in foundry choice (Interviews with top five Fabless-#2 and #3). Two foundry technology leaders from East Asia—TSMC and Samsung foundry—have accumulated substantial chip-making learnings and proprietary advantage from serving top fabless customers, who are both demanding and sophisticated in their chip designs, and from managing their complex requirements through different in-house fab-specific process recipes. They can offer stronger manufacturing and highly process-dependent design support for existing and new fabless customers. This intimate and mutual dependency between top fabless firms and their main foundry providers in has led to the further geographic shift of cutting-edge logic chip making during the 2010s from a few foundry providers in the US (e.g., GlobalFoundries and IBM Microelectronics) to Taiwan and South Korea.

Conclusion

This empirical article has shown that the interconnected worlds of semiconductor GPNs during the 2010s shifted further toward East Asia, with the dominant presence of South Korean and Japanese IDM firms in memory chips and foundry providers from Taiwan, South Korea, and China in fabricating logic chips. The foundry model of organizing semiconductor production networks has also supported the consolidation of chip design in logic and other semiconductor devices among leading fabless firms located mostly in Silicon Valley and elsewhere in East Asia (Brown and Linden Citation2011; Nenni and McLellan Citation2019; Yeung Citation2022).

To explain these substantial geographic shifts in semiconductor manufacturing during the 2010s, I have expanded on the market imperative concept in Coe and Yeung’s (Citation2015) recent theory of GPNs. Conceptually, I have specified the two main dimensions of market dynamics—customer intimacy in intermediate markets (e.g., semiconductors) and demand responsiveness in end markets (e.g., ICT final products), building on earlier economic geography work on innovation (Gertler Citation1995, Citation2003; Grabher, Ibert, and Flohr Citation2008; Ascani et al. Citation2020; Yeung Citation2021a) and markets in GPNs (Yang Citation2014; Horner and Nadvi Citation2018; Dodge Citation2020).

In conceptual and empirical terms, this article has demonstrated the necessity of market dynamics, as a demand-led explanation, in accounting for the dominance of East Asia in global chip making by the late 2010s. These market dynamics are manifested in huge intermediate market demand for logic and memory chips from OEM lead firms to serve their end markets and the overwhelming role of China as the key site for the final assembly of major ICT products. In this intermediate market for logic, memory, and microprocessor chips, some two-thirds of all semiconductor devices are integrated into printed circuit boards and/or electronics modules assembled with other components into final ICT products in factories throughout China and other Asian locations (Grimes and Sun Citation2016; Gao et al. Citation2017; Yang Citation2017; Xing Citation2021; Yeung Citation2022).

This article’s elucidations of customer intimacy in GPNs have two implications for economic geography. First, while the concept of customer intimacy is linked to relational proximity (Bathelt and Glückler Citation2003; Yeung Citation2005; Murphy Citation2012) and its kin concepts, such relational governance (Gereffi, Humphrey, and Sturgeon Citation2005) and relational capital (Parker, Cox, and Thompson Citation2014), utilizing the concept, requires a more precise specification of different firm roles in production networks because the concept refers to ongoing processes of mutual dependency between producers and their customers. In my empirical analysis, intimacy is constituted through processes of design-ins and mutual alignments of product and technology roadmaps between semiconductor firms and their OEM lead firm customers, and processes of dedicated chip technologies and capacity allocation between foundry providers and their fabless customers. The concept is thus aligned with and extends further the work of Grabher, Ibert, and Flohr (Citation2008) and Grabher and Ibert (Citation2018) on the cocreation of innovation and products.

Second, the explanatory link between high chip-making capacity in East Asia (dependent variable) and market dynamics (independent variable) is predicated on both spatial and relational proximity. My interview material has illustrated the firm-level specificities in customer intimacy and relational proximity that constitute the demand-responsive relationships between chip design and OEM customers and wafer fabs in their bid to serve end customers better. Being there, as originally conceived in Gertler’s (Citation1995, Citation2003) work, can be achieved through geographic copresence within the same macroregion (i.e., East Asia). This finding on the importance of both spatial and relational proximity in semiconductor manufacturing supports Boschma’s (Citation2005) and Balland, Boschma, and Frenken’s (Citation2020) arguments for different forms of proximities in understanding innovation, and Bathelt, Malmberg, and Maskell’s (Citation2004) notion of global pipelines connecting external customers to localized clusters. Future research in economic geography, regional studies, and industry/innovation studies can benefit from this renewed analytical focus on market dynamics as a necessary explanation for major industrial transformations and geographic shifts.

Acknowledgments

I am most grateful to Jim Murphy for handling this article’s editorial review and his patience and encouragement throughout three rounds of revisions. The detailed and constructive comments from four anonymous reviewers on different drafts of this article were very useful in sharpening its analytical focus and explanatory robustness. All errors and shortcomings are my own.

Correction Statement

This article has been corrected with minor changes. These changes do not impact the academic content of the article.

Additional information

Funding

References

- Adams, P., Fontana, R., and Malerba, F. 2013. The magnitude of innovation by demand in a sectoral system: The role of industrial users in semiconductors. Research Policy 42 (1): 1–14. doi:https://doi.org/10.1016/j.respol.2012.05.011.

- Angel, D. P. 1994. Restructuring for innovation: The remaking of the U.S. semiconductor industry. New York: Guilford.

- Ascani, A., Bettarelli, L., Resmini, L., and Balland, P.-A. 2020. Global networks, local specialisation and regional patterns of innovation. Research Policy 49 (8): 104031. doi:https://doi.org/10.1016/j.respol.2020.104031.

- Balland, P.-A., Boschma, R., and Frenken, K. 2020. Proximity, innovation and networks: A concise review and some next steps. Papers in Evolutionary Economic Geography 2019. Utrecht University: Utrecht, the Netherlands.

- Bathelt, H., and Glückler, J. 2003. Toward a relational economic geography. Journal of Economic Geography 3 (2): 117–44. doi:https://doi.org/10.1093/jeg/3.2.117.

- Bathelt, H., Malmberg, A., and Maskell, P. 2004. Clusters and knowledge: Local buzz, global pipelines and the process of knowledge creation. Progress in Human Geography 28 (1): 31–56. doi:https://doi.org/10.1191/0309132504ph469oa.

- Boschma, R. A. 2005. Proximity and innovation: A critical assessment. Regional Studies 39 (1): 61–74. doi:https://doi.org/10.1080/0034340052000320887.

- Brown, C., and Linden, G. 2011. Chips and change: How crisis reshapes the semiconductor industry. Cambridge, MA: MIT Press.

- Campbell-Kelly, M., and Garcia-Swartz, D. 2015. From mainframes to smartphones: A history of the international computer industry. Cambridge, MA: Harvard University Press.

- Chu, M.-C. M. 2013. The East Asian computer chip war. London: Routledge.

- Coe, N. M. 2021. Advanced introduction to global production networks. Cheltenham, UK: Edward Elgar.

- Coe, N., Hess, M., Yeung, H. W.-c., Dicken, P., and Henderson, J. 2004. ‘Globalizing’ regional development: A global production networks perspective. Transactions of the Institute of British Geographers 29 (4): 468–84. doi:https://doi.org/10.1111/j.0020-2754.2004.00142.x.

- Coe, N. M., and Yeung, H. W.-c. 2015. Global production networks: Theorizing economic development in an interconnected world. Oxford: Oxford University Press.

- Coe, N. M. 2019. Global production networks: Mapping recent conceptual developments. Journal of Economic Geography 19 (4): 775–801. doi:https://doi.org/10.1093/jeg/lbz018.

- Dedrick, J., and Kraemer, K. 1998. Asia’s computer challenge: Threat or opportunity for the United States and the world? New York: Oxford University Press.

- Dibiaggio, L. 2007. Design complexity, vertical disintegration and knowledge organization in the semiconductor industry. Industrial and Corporate Change 16 (2): 239–67. doi:https://doi.org/10.1093/icc/dtm006.

- Dibiaggio, L., Nasiriyar, M., and Nesta, L. 2014. Substitutability and complementarity of technological knowledge and the inventive performance of semiconductor companies. Research Policy 43 (9): 1582–93. doi:https://doi.org/10.1016/j.respol.2014.04.001.

- Dodge, A. 2020. The Singaporean natural gas hub: Reassembling global production networks and markets in Asia. Journal of Economic Geography 2 (5): 1241–62. doi:https://doi.org/10.1093/jeg/lbaa011.

- Epicoco, M. 2013. Knowledge patterns and sources of leadership: Mapping the semiconductor miniaturization trajectory. Research Policy 42 (1): 180–95. doi:https://doi.org/10.1016/j.respol.2012.06.009.

- Ernst, D. 2005. Limits to modularity: Reflections on recent developments in chip design. Industry and Innovation 12 (3): 303–35. doi:https://doi.org/10.1080/13662710500195918.

- Ernst, D. 2016. China’s bold strategy for semiconductors—Zero-sum game or catalyst for cooperation? East–West Center working papers: Innovation and economic growth series 9. Honolulu, HI: East-West Center.

- Feenstra, R. C., and Hamilton, G. G. 2006. Emergent economies, divergent paths: Economic organization and international trade in South Korea and Taiwan. Cambridge: Cambridge University Press.

- Fontana, R., and Malerba, F. 2010. Demand as a source of entry and the survival of new semiconductor firms. Industrial and Corporate Change 19 (5): 1629–54. doi:https://doi.org/10.1093/icc/dtq045.

- Fuller, D. B. 2019. Growth, upgrading, and limited catch-up in China’s semiconductor industry. Policy, regulation and innovation in China’s electricity and telecom industries, ed. L. Brandt and T. G. Rawski, 262–303. Cambridge: Cambridge University Press.

- Gao, B., Dunford, M., Norcliffe, G., and Liu, Z. 2017. Capturing gains by relocating global production networks: The rise of Chongqing’s notebook computer industry, 2008–2014. Eurasian Geography and Economics 58 (2): 231–57. doi:https://doi.org/10.1080/15387216.2017.1326312.

- Gereffi, G., Humphrey, J., and Sturgeon, T. 2005. The governance of global value chains. Review of International Political Economy 12 (1): 78–104. doi:https://doi.org/10.1080/09692290500049805.

- Gertler, M. S. 1995. ‘Being there’: Proximity, organization, and culture in the development and adoption of advanced manufacturing technologies. Economic Geography 71 (1): 1–26. doi:https://doi.org/10.2307/144433.

- Gertler, M. S. 2003. Tacit knowledge and the economic geography of context, or the undefinable tacitness of being (there). Journal of Economic Geography 3 (1): 75–99. doi:https://doi.org/10.1093/jeg/3.1.75.

- Glimstedt, H., Bratt, D., and Karlsson, M. P. 2010. The decision to make or buy a critical technology: Semiconductors at Ericsson, 1980–2010. Industrial and Corporate Change 19 (2): 431–64. doi:https://doi.org/10.1093/icc/dtq011.

- Grabher, G., and Ibert, O. 2018. Schumpeterian customers? How active users co-create innovations. The new Oxford handbook of economic geography, ed. G. L. Clark, M. P. Feldman, M. S. Gertler, and D. Wójcik, 286–304. Oxford: Oxford University Press.

- Grabher, G., Ibert, O., and Flohr, S. 2008. The neglected king: The customer in the new knowledge ecology of innovation. Economic Geography 84 (3): 253–80. doi:https://doi.org/10.1111/j.1944-8287.2008.tb00365.x.

- Grimes, S., and Du, D. 2021. China’s emerging role in the global semiconductor value chain. Telecommunications Policy. doi:https://doi.org/10.1016/j.telpol.2020.101959.

- Grimes, S., and Sun, Y. 2016. China’s evolving role in Apple’s global value chain. Area Development and Policy 1 (1): 94–112. doi:https://doi.org/10.1080/23792949.2016.1149434.

- Hamilton-Hart, N., and Yeung, H. W.-c. 2021. Special forum on ‘institutions under pressure: The international political economy of states and firms in East Asia. Review of International Political Economy 28 (1): 11–151. doi:https://doi.org/10.1080/09692290.2019.1702571.

- Hamilton, G. G., and Kao, C.-S. 2018. Making money: How Taiwanese industrialists embraced the global economy. Stanford, CA: Stanford University Press.

- Henderson, J., Dicken, P., Hess, M., Coe, N., and Yeung, H. W.-c. 2002. Global production networks and the analysis of economic development. Review of International Political Economy 9 (3): 436–64. doi:https://doi.org/10.1080/09692290210150842.

- Horner, R., and Murphy, J. 2018. South-North and South-South production networks: Diverging socio-spatial practices of Indian pharmaceutical firms. Global Networks 18 (2): 326–51. doi:https://doi.org/10.1111/glob.12159.

- Horner, R., and Nadvi, K. 2018. Global value chains and the rise of the Global South: Unpacking twenty-first century polycentric trade. Global Networks 18 (2): 207–37. doi:https://doi.org/10.1111/glob.12180.

- Hsu, J. Y. 2017. State transformation and the evolution of economic nationalism in the East Asian developmental state: The Taiwanese semiconductor industry as case study. Transactions of the Institute of British Geographers 42 (2): 166–78. doi:https://doi.org/10.1111/tran.12165.

- Hwang, H.-R., and Choung, J.-Y. 2014. The co-evolution of technology and institutions in the catch-up process: The case of the semiconductor industry in Korea and Taiwan. Journal of Development Studies 50 (9): 1240–60. doi:https://doi.org/10.1080/00220388.2014.895817.

- Kano, L., Tsang, E. W. K., and Yeung, H. W.-c. 2020. Global value chains: A review of a multidisciplinary literature. Journal of International Business Studies 51 (4): 577–622. doi:https://doi.org/10.1057/s41267-020-00304-2.

- Kaplinsky, R., and Farooki, M. 2011. What are the implications for global value chains when the market shifts from the North to the South? International Journal of Technological Learning, Innovation and Development 4 (1–3): 13–38. doi:https://doi.org/10.1504/IJTLID.2011.041898.

- Kenney, M. 2011. How venture capital became a component of the US national system of innovation. Industrial and Corporate Change 20 (6): 1677–723. doi:https://doi.org/10.1093/icc/dtr061.

- Kenney, M., and Zysman, J. 2020. The platform economy: Restructuring the space of capitalist accumulation. Cambridge Journal of Regions, Economy and Space 13 (1): 55–76. doi:https://doi.org/10.1093/cjres/rsaa001.

- Langlois, R. N. 2003. The vanishing hand: The changing dynamics of industrial capitalism. Industrial and Corporate Change 12 (2): 351–85. doi:https://doi.org/10.1093/icc/12.2.351.

- Langlois, R. N., and Robertson, P. L. 1995. Firms, markets and economic change: A dynamic theory of business institutions. London: Routledge.

- Lee, K. 2019. The art of economic catch-up: Barriers, detours and leapfrogging in innovation systems. Cambridge: Cambridge University Press.

- Lee, K., and Malerba, F. 2017. Catch-up cycles and changes in industrial leadership: Windows of opportunity and responses of firms and countries in the evolution of sectoral systems. Research Policy 46 (2): 338–51. doi:https://doi.org/10.1016/j.respol.2016.09.006.

- Linden, G., and Somaya, D. 2003. System‐on‐a‐chip integration in the semiconductor industry: Industry structure and firm strategies. Industrial and Corporate Change 12 (3): 545–76. doi:https://doi.org/10.1093/icc/12.3.545.

- Mathews, J. A., and Cho, D.-S. 2000. Tiger technology: The creation of a semiconductor industry in East Asia. Cambridge: Cambridge University Press.

- Mazurek, J. 1999. Making microchips: Policy, globalization and economic restructuring in the semiconductor industry. Cambridge, MA: MIT Press.

- Murphy, J. T. 2012. Global production networks, relational proximity, and the sociospatial dynamics of market internationalization in Bolivia’s wood products sector. Annals of the Association of American Geographers 102 (1): 208–33. doi:https://doi.org/10.1080/00045608.2011.596384.

- Nelson, R. R., and Winter, S. G. 1982. An evolutionary theory of economic change. Cambridge, MA: Harvard University Press.

- Nenni, D., and McLellan, P. 2019. Fabless: The transformation of the semiconductor industry. Danville, CA: SemiWiki.com.

- Nepelski, D., and De Prato, G. 2018. The structure and evolution of ICT global innovation network. Industry and Innovation 25 (10): 940–65. doi:https://doi.org/10.1080/13662716.2017.1343129.

- Óhuallacháin, B. 1997. Restructuring the American semiconductor industry: Vertical integration of design houses and wafer fabricators. Annals of the Association of American Geographers 87 (2): 217–37. doi:https://doi.org/10.1111/0004-5608.872051.

- Park, C. 2019. Customers’ migration paths decided by relative advantage: Longitudinal and comparative case study of successive generations of logic semiconductor technology. Technology Analysis and Strategic Management 31 (9): 1063–80. doi:https://doi.org/10.1080/09537325.2019.1584285.

- Parker, R., Cox, S., and Thompson, P. 2014. How technological change affects power relations in global markets: Remote developers in the console and mobile games industry. Environment and Planning A 46 (1): 168–85. doi:https://doi.org/10.1068/a45663.

- Ponte, S., Gereffi, G., and Raj-Reichert, G., eds. 2019. Handbook on global value chains. Cheltenham, UK: Edward Elgar.

- Scott, A. J. 1988. New industrial spaces: Flexible production, organisation and regional development in North America and Western Europe. London: Pion.

- Shin, J.-S. 2017. Dynamic catch-up strategy, capability expansion and changing windows of opportunity in the memory industry. Research Policy 46 (2): 404–16. doi:https://doi.org/10.1016/j.respol.2016.09.009.

- Sturgeon, T. J. 2002. Modular production networks: A new American model of industrial organization. Industrial and Corporate Change 11 (3): 451–96. doi:https://doi.org/10.1093/icc/11.3.451.