Abstract

The 75th anniversary of the founding of the Financial Analysts Journal offers a rare vista of the evolutionary path of financial analysis and its practitioners. That path is by no means random but is shaped by a complex ecosystem in which technological innovation interacts with shifting business conditions and a growing population of financial stakeholders. Using the lens of the Adaptive Markets Hypothesis—the principles of evolutionary biology and ecology applied to the financial system—we can clearly identify eight discrete financial “eras” in which unique combinations of economic need and technological advances gave rise to new products, services, and financial institutions. By understanding the underlying drivers and resulting dynamics of these eras, we can begin to develop a deeper appreciation for the origins of financial innovation and its great promise for our future.

In 1937, a small group of security analysts decided over a luncheon that “the benefit of their discussions could be multiplied by organizing a formal group and holding meetings regularly” (Tatham 1945, p. 3). Thus began the New York Society of Security Analysts, with an initial membership of 20 analysts. The Financial Analysts Journal was launched eight years later, in 1945. Today, CFA Institute has roughly 180,000 investment professionals, of which over 175,000 hold the Chartered Financial Analyst designation. And in 2019, more than 350,000 participants took the CFA Program examination. With 161 local societies globally, CFA Institute is the most widely recognized professional organization in the world for financial analysts, and its flagship publication, the Financial Analysts Journal, reflects the diversity and creativity that such an organization has fostered over three-quarters of a century.

Through seismic historical shifts and spectacular technological developments, the Financial Analysts Journal has continued to advance the theory and practice of financial analysis into a very different world from the one where it originated. It is now a richer and more participatory world—a development made possible in no small part by the journal’s efforts—but it is still a world with the same recognizable functions and objectives that existed in the 1940s.

At one level, this functional constancy makes intuitive sense. We are all human—buyers and sellers, practitioners and academics, regulators and the regulated—and there are fundamental commonalities in what we seek to accomplish. The means may differ over time, in the different kinds of technologies and the different ways and extents to which they are used, but the goals remain very much the same.

However, there is a deeper reason for this constancy amidst the current explosion of financial diversity. The financial system is subject to evolutionary pressures that shape its ability to survive through different economic environments, a phenomenon I have called the “Adaptive Markets Hypothesis” (Lo 2004, 2005, 2012, 2017). According to this hypothesis, the story of financial markets is one of competition, innovation, adaptation, and selection. This is no analogy; the financial system is as much a product of literal human evolution as the opposable thumb and our prefrontal cortex.

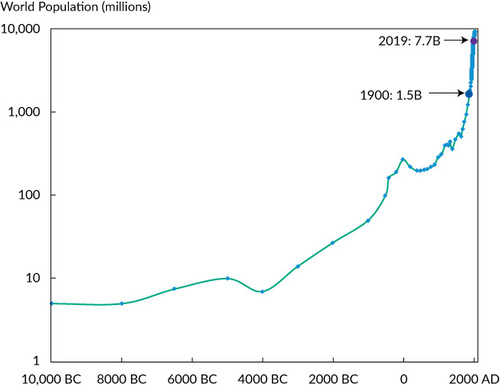

Underlying this narrative of financial market dynamics is the remarkable success of Homo sapiens, as shown in , which documents the growth in our numbers from 10,000 BC to the present. Over the course of the past 12 millennia, humans have reproduced virtually unimpeded and with no natural predators—other than ourselves! Because the vertical axis is scaled logarithmically, the growth rate is simply the slope of the curve, which tells a fascinating story. Based on the changes in slope, we can discern at least four distinct periods of human evolution. The flattest part of the curve, from 10,000 BC to 4000 BC, is the Stone Age. The sharp increase in growth between 4000 BC and 3000 BC signaled the beginning of the Bronze Age, followed by the Iron Age, when those metals became commonplace. This curve continues in a nearly straight line until the 1800s, when another increase in slope occurs. This marks the beginning of the Industrial Age, which spans about a century before the curve steepens once more. This last inflection point, which occurred at the start of the 20th century, is where we are today, a period that some have called the “Digital Age.” In 1900, the world population is estimated to have been approximately 1.5 billion; as of 2019, the corresponding estimate is 7.7 billion. Within a century—a blink of an eye on an evolutionary timescale—we managed to increase our numbers fivefold.

Sources: US Census Bureau’s International Data Base and author’s calculation.

How did Homo sapiens come to dominate its environment so completely, populating virtually every ecological niche on the planet, even including short stays beneath the oceans, at both poles, atop the highest mountains, and in outer space?

The answer, of course, is technology. Technologies of all kinds—agricultural, biomedical, manufacturing, transportation, computational, telecommunications, and so on—are key drivers of our success. Underlying each of these technological advances, however, is a common denominator: financial technology. The reason is simple: Theory can only be put into practice with financing. Here, “financing” refers not just to money but also to the particular terms by which money is provided to stakeholders to foster innovation. It is no coincidence that technological innovation is almost always accompanied by financial innovation. “Necessity is the mother of all invention,” but invention necessarily requires financing.

Nevertheless, as Robert C. Merton—the economist, not the sociologist—observed, individual institutions change much more quickly than the core functions of finance. Merton enumerates six such functions:Footnote1

to provide ways to transfer economic resources through time, across borders, and among industries;

to provide ways of managing risk;

to provide ways of clearing and settling payments to facilitate trade;

to provide a mechanism for the pooling of resources and for the subdividing of ownership in various enterprises;

to provide price information to help coordinate decentralized decision making in various sectors of the economy;

to provide ways of dealing with the incentive problems created when one party to a transaction has information that the other party does not or when one party acts as agent for another.

By focusing on functions rather than institutions, we can develop a deeper understanding of how financial technology co-evolves with other technologies and can even anticipate to some degree how institutions will adapt as the environment changes. This is the theme of this article. On the occasion of the 75th anniversary of the founding of the Financial Analysts Journal, I hope to take readers on a guided tour of the evolution of financial markets across the journal’s lifespan, highlighting the interconnected and dynamic roles that theory, practice, and regulation played along the way.

The Evolution of Technology and Finance

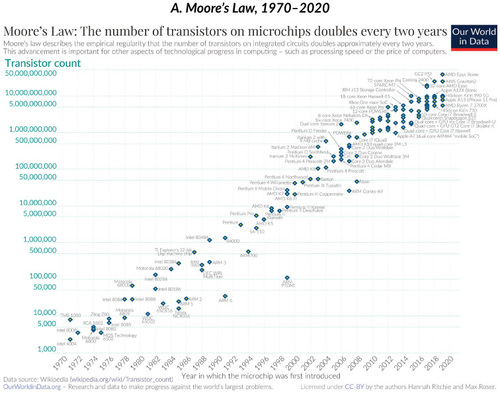

In 1965—three years before he co-founded Intel, now the largest semiconductor chip manufacturer in the world—Gordon Moore published an article in Electronics magazine in which he observed that the number of transistors that could be placed onto a microchip seemed to double every year (Moore 1965). This simple observation, implying not merely constant growth but a constant rate of growth, led Moore to extrapolate an increase in computing potential from 60 transistors per chip in 1965 to 60,000 in 1975. This number seemed absurd at the time, but it was realized, on schedule, a decade later. Later revised by Moore to a doubling every two years, “Moore’s Law” has been a remarkably prescient forecast of the growth of the semiconductor industry over the last 40 years, as Panel A of confirms.

Figure 2. Moore’s Law and Its Financial CounterpartSources: Panel A: Max Roser and Hannah Ritchie, https://ourworldindata.org/uploads/2020/11/Transistor-Count-over-time.png; licensed under CC-BY by the authors Hanna Ritchie and Max Roser. Panel B: Lo (2017, ).

Moore’s Law now influences a broad spectrum of modern life. It affects everything from household appliances to biomedicine to national defense, and its impact is no less evident in the financial industry. As computing has become faster, cheaper, and better at automating a variety of tasks, financial institutions have been able to greatly increase the scale and sophistication of their services. Automated algorithmic trading, online brokerage, mobile banking, crowdfunding, financial robo-advisers, and cryptocurrencies (such as bitcoin) are all consequences of Moore’s Law.

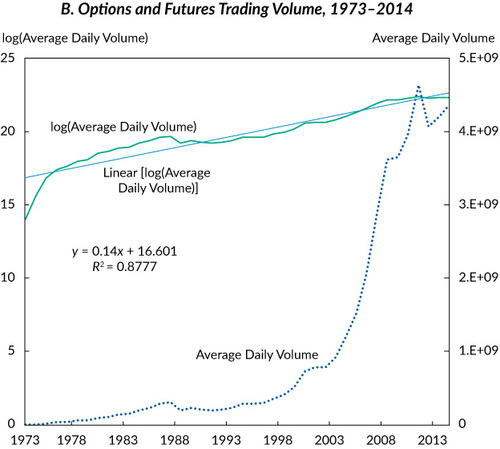

Therefore, it should come as no surprise that there are financial analogues of Moore’s Law, one of which is depicted in Panel B of . This graph of average daily trading volume of exchange-listed options and futures from the Options Clearing Corporation from 1973 to 2014 shows that volume doubles approximately every five years.

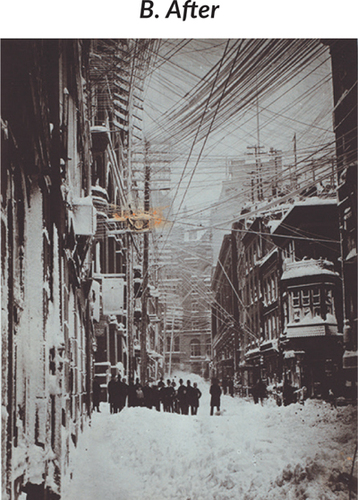

In fact, technological innovation has always been intimately interconnected with financial innovation.Footnote2 New stamping and printing processes, used to prevent clipping, counterfeiting, and other forms of financial fraud, directly led to the modern system of paper banknotes and token coinage. To take another example, New York City’s Wall Street in its earliest days was not far removed from the Dutch coffee shops where the first modern business of financial trading took place, and the light of a candle was used to time the length of an auction. After the invention of the telegraph, however, Wall Street quickly found itself “wired,” and its physical appearance changed in short order (see ), sparking a continent-spanning communications revolution that led to the creation of the modern futures market in the new 19th century city of Chicago. And improvements to the ticker tape machine—symbolic of Wall Street for over a century—made Thomas Edison his early fortune.

Figure 3. Photographs of Wall Street before and after the Invention of the TelegraphSources: Panel A: The Miriam and Ira D. Wallach Division of Art, Prints and Photographs: Picture Collection, The New York Public Library. “Wall Street, N.Y.” New York Public Library Digital Collections. Accessed 7 June 2021. https://digitalcollections.nypl.org/items/510d47e1-06da-a3d9-e040-e00a18064a99. Panel B: Irma and Paul Milstein Division of United States History, Local History and Genealogy, The New York Public Library. “Manhattan: New Street - Wall Street.” New York Public Library Digital Collections. Accessed 7 June 2021. https://digitalcollections.nypl.org/items/510d47dd-4bd9-a3d9-e040-e00a18064a99.

The current financial system has survived world wars, trade wars, shifts in ideology large and small, the collapse of governments, and multiple financial crises. In the process, it has catalyzed the rise of most of the world out of grinding poverty. Its development has been disorderly, the product of trillions of individual decisions in response to ever-changing social, economic, and technological trends. Nevertheless, the financial system has become a highly complex and finely tuned machine for the allocation of finite financial resources. In short, the financial system has evolved into its current central role in much the way we ourselves as a species have evolved biologically over the ages. The six functions of the financial system that Merton described are precisely the ones that facilitated our survival and growth over eons.

However, there is one important difference between financial evolution and its biological counterpart. Thanks to the uniquely human abilities of engaging in abstract thought, high-level communication, and expansive methods of collaboration, our financial institutions and technologies evolve not generation by generation over geological timescales but within a single generation and at the speed of thought. If we can imagine it, with sufficient time and resources, we can almost always make it so. Even the 16th century alchemist’s dream of turning lead into gold is now a reality, albeit a rather impractical one.Footnote3 In fact, on the one hand, the market may immediately adopt an innovation that previously existed only on paper if the financial environment is thought to be ripe for it. On the other hand, an idea may lie fallow for years, if not decades, until the proper mix of demand, technology, and environment allows it to flourish.

Despite its important role, technological invention is far from the only source of evolutionary change in the financial industry. Academia is another important engine of innovation. Advances in research are analogous to mutations in biological systems, a source of evolutionary surprise rather than an intensification of earlier trends. Academics develop and refine new ideas for the pure joy of learning, without necessarily attempting to profit from them. This difference in goals separates them from the practitioner, who may be equally knowledgeable but whose intentions are often far more practical. As a consequence, academic research plays a critical role in driving financial evolution, as underscored by the 75-year history of the Financial Analysts Journal and the specific journal publications cited in this article.

The evolutionary lens also helps explain otherwise difficult-to-interpret trends about the adoption and diffusion of these innovations. For example, rather than an innovation always occurring in a large, dominant market and spreading to smaller ones, at times a useful innovation will occur in a smaller market, where its success as a proof of concept will allow it to expand to larger ones, such as the index future, originally developed in Kansas City, or the exchange-traded fund, first implemented in Toronto. These have exact analogues in population genetics, which describe how a favorable rare mutation can first become fixed in a small isolated population and, from there, proceed to become the most frequent variant in the population as a whole.

In addition, the role of the economic and regulatory environment in shaping financial innovation cannot be overlooked. To take a well-documented example, the switch from a gold-dollar standard and fixed exchange rates in the Bretton Woods international monetary system to a world of independently managed currencies and floating exchange rates in 1971 inspired an enormous wave of financial innovation. In that same period, the emergence of “stagflation” precipitated by oil shortages created the need for risk management tools, such as exchange-traded and OTC derivative securities. Other shifts in the environment are far subtler, such as “May Day” in 1975, when commissions for trades switched from a fixed rate, no matter the size of the trade, to a negotiable commission. A more recent example is decimalization, when in 2001, price movements on all US stocks switched over to decimals from eighths or sixteenths of a dollar. Not only did these changes shift trading terms more favorably toward the retail investor, but they allowed discount brokerages to proliferate and automated trading strategies to become much more than curiosities.

Innovation thus has transformed the financial system in the past 75 years in unforeseen and unforeseeable ways. However, institutional form follows financial function, and the evolutionary process of innovation, competition, and selection in performing Merton’s six functions expedites a convergence in form.

Timetable of Financial Evolution

Expanding on Merton’s insight, I classify financial innovation over time into six practical categories of implementation based on their broad functions: communication, computation, security, commercial use, accessibility, and cost. Communication in this schema is the transmission of financial information, while computation is the transformation of financial information, and security is the protection of that information. Similarly, taking into account a financial innovation’s interaction with the human environment, commercial use is the application of an innovation in a business setting, accessibility is a widening of its potential user base, and cost is a reduction in price.

These categories encompass the specific implementations of these broad functions to incorporate the timelessness of Merton’s functional perspective. For example, take communication speed in trading. In 1920, the highest speeds would involve a seat on an exchange and a physical presence on the trading floor. In 2020, it involved high-frequency trading (HFT) servers competing for microsecond advantages in latency. Similarly, a wire transfer is still a wire transfer, whether it uses a telegraph and a codebook or a fiber-optic line and advanced cryptographic techniques. As with the six functions of finance, it is useful to make a distinction between the timeless implementation of these concepts and their time-bound manifestations.

Looking through the evolutionary lens reveals that different financial environments will benefit different sets of stakeholders. They can be considered analogous to distinct species within the financial ecosystem. For example, an inflationary environment favors debtors, while a deflationary environment favors creditors. High transaction costs will favor large institutional investors and financial intermediaries over retail investors and ordinary consumers. A shift in interest rates relative to stock market performance will shift the position of banking relative to trading. And two groups—academics and regulators—will often respond to a rapidly changing financial environment with innovations of their own.

We can use Merton’s six functions of the financial system, the six corresponding conceptual categories of implementation, and the intellectual history of academic finance to organize the long post–World War II period of financial innovation into a series of eight distinct periods—analogous to the major eras in the timetable of evolutionFootnote4—each with its particular defining characteristics (see ). When the natural history of the financial industry is viewed in a sequential narrative, the functional perspective of finance and how it relates to the Adaptive Markets Hypothesis comes into sharper focus. Also, by recognizing how environmental changes can help or harm a given species, we can use the Adaptive Markets framework to increase our chances of survival in the face of extinction-level events.

Exhibit 1. Timeline of Eight Eras of Financial Evolution from 1944 to 2021 and Key Technology, Financial, and Regulatory Milestones during Those Eras

The first era, dating from the establishment of the Bretton Woods monetary system in 1944, I call the “Classical Financial Era.” The Bretton Woods agreement established the US dollar, backed by gold, as the basis for the global postwar economy, which was dominated by the United States—unlike any other era before or since.

The Classical Financial Era ended with Harry Markowitz’s first definitive paper on modern portfolio theory in 1952. Although it would take time for Markowitz’s ideas to be digested by the financial community, his publication introduced the theoretical basis for portfolio diversification into risk management at a time when the US economy was beginning to diversify from the heavy industry that it used to become a superpower. For this reason, it seems appropriate to characterize this next period as the “Modern Portfolio Theory Era.”

The Modern Portfolio Theory Era ended with William Sharpe’s first paper on the capital asset pricing model, in 1964, although, of course, Jack Treynor’s private work foreshadowed it, and John Lintner and Jan Mossin nearly simultaneously developed it.Footnote5 This new financial model was applied to the first technology boom, which John Brooks called the “Go-Go Years,” but also to the bust that followed. Overall, this era can be called the “Alpha Beta Era.”

The Alpha Beta Era came to an end with the opening of the Chicago Board Options Exchange (Cboe) in 1973 and, in the same year, Fischer Black and Myron Scholes’s (1973) publication of their paper on option pricing, as well as Robert C. Merton’s nearly simultaneous development of the idea (Merton 1973). This tumultuous period can only be named the “Derivatives Era” for the explosive growth of these instruments that followed.

The Derivatives Era ended with a technological development, the advent of the first Bloomberg Terminal at the end of 1982. This phase in financial history was characterized by the adoption of consumer electronics in financial practice, from specialized terminals to home spreadsheets to program trading. The “Automation Era” captures the essence of these years.

The Automation Era ended with another technological milestone, the development of the World Wide Web (WWW) in 1989 by Sir Timothy Berners-Lee, then a young computer scientist working at a CERN research facility outside Geneva. This event coincided with major geopolitical changes that led to the reintegration of the global economy, supplying an apposite name, the “Financial Globalization Era.”

The next dividing line may appear arbitrary, but many computer professionals were worried about the systemic failures that might have taken place because of obsolescent code on the date of 31 December 1999, the infamous “Y2K” problem. It is also a convenient milestone for the establishment of high-frequency trading in the global markets. For this reason, the following period is named the “Algorithmic Trading Era.”

At the end of the Algorithmic Trading Era, the seeds for the next era were planted with the self-publication in 2008 of the bitcoin protocol by the mysterious figure known as “Satoshi Nakamoto” (2008). Still in their infancy, cryptocurrencies and their related technologies form an entirely new evolutionary branch in our financial history that will no doubt create a series of offshoot technologies and financial institutions in the coming years. Therefore, this last period is called the “Digital Assets Era.”

In the remaining sections, I describe each of these eras in more detail from an evolutionary perspective, with particular attention paid to the complementary roles of financial theory and practice and how they interact with technological innovation and the changing environment. To highlight the role of research in these evolutionary dynamics, I draw on the rich fossil record of all past publications of the Financial Analysts Journal in its 75-year history.Footnote6 In keeping with our theme of technology, I use a bit of data science by tabulating the top 20 authors (ranked by number of Financial Analysts Journal articles) and the top 20 words in article titles during each of the eight eras. The results, given in , offer a fascinating glimpse of the changing list of personalities and topics that have graced the pages of this venerable journal over time.Footnote7

Exhibit 2. Top 20 Authors and Words in the Titles of All Articles Published in the Financial Analysts Journal within Each of Eight Distinct Eras from 1945 to 2021

The Era before the Financial Analysts Journal

No financial market can exist without communication. Even the simplest forms of barter and exchange include a transfer of information, often weighted with symbolic meaning. By the modern era, market participants often vied for being the first to acquire information that could move markets—for example, in the apocryphal legend that Nathan Rothschild, the founder of the banking dynasty, made his fortune by learning of the British victory at Waterloo over Napoleon by carrier pigeon and, armed with that information, bought British government bonds on the cheap before news of the victory could reach London. (In fact, Rothschild seems to have learned of the news via fast couriers, although the family did employ a pigeon network as well.)

The speed of communication has a fundamental limit set by the laws of physics: the speed of light. This limit was reached as early as 1838, with the invention of the telegraph by Samuel F. B. Morse, for whom Morse code is named. The telegraph revolutionized the markets, allowing information about commodities in distant regions to reach financial centers nearly instantaneously. In the United States, former frontier settlements became enormous hubs organized around the buying and selling of commodities, none of the hubs bigger than the new city of Chicago, which spawned the modern futures market. Market information could be sent over the wire to the first stock tickers, as could encrypted financial information, such as the first wire transfers, using printed codebooks as an early form of cryptographic security for the transaction.

By current criteria, financial activity in this period moved at a snail’s pace. The financial system’s reliance on a metallic standard was intended to limit activity that might lead to inflationary pressures, creating an environment that broadly favored creditors over debtors. Membership in the financial professions was often limited by social strictures and laws that would seem grotesque today. Despite these restrictions on use and accessibility, the financial system was also prone to systemic crises, the larger ones leading to regulatory innovation, structural changes, and reforms, such as the formation of the Federal Reserve System following the Panic of 1907 and the creation of the Securities and Exchange Commission (SEC), the Federal Deposit Insurance Company, and much of the regulatory framework of the entire financial industry—the Banking (also known as Glass–Steagall) Act of 1933, the Securities Act of 1933, the Securities Exchange Act of 1934, and the Investment Advisers Act of 1940—during and after the Great Depression. But perhaps the greatest innovation in financial analysis to emerge from this primordial period was Benjamin Graham and David Dodd’s (1934) now classic tome Security Analysis, which would dominate the financial world—and the pages of the Financial Analysts Journal—until the Modern Portfolio Theory Era.

1944–1951: Classical Financial Era (Bretton Woods to Markowitz)

The political and economic pressures of World War II transformed the financial landscape into that of the Classical Financial Era. By 1944, it was clear that a postwar order would emerge with the United States as the dominant capitalist power. A blueprint for the financial underpinnings of this new order was put together in July 1944 at Bretton Woods, New Hampshire: a gold-dollar standard designed to finance the reconstruction of the damaged economies of the postwar period. The demobilization of millions of Americans in the armed forces taking place so quickly after the mass unemployment of the Great Depression caused legislators to pursue policies to improve the lives of returning veterans. The GI Bill provided financing for their college education, while the newly founded Veterans Administration insured home mortgages, which catalyzed a postwar wave of homeownership and shifted the residential patterns of Americans from central cities to suburbs for generations.

This business environment set the stage for increased growth in commercial finance focused on the needs of its newly prosperous clients. After almost two decades of the Great Depression and wartime dearth, the US society became strongly consumerist, and this pent-up demand found new outlets. The first modern hedge fund, started by Alfred Winslow Jones in 1949, was the harbinger of new fund types and trading strategies, while the first general-purpose charge card, Diners Club, would become the forerunner to an enormous expansion of consumer credit.

The war effort also brought about enormous advances in computation. The first programmable digital computer, ENIAC, created in 1945 for the needs of war, performed the numerical calculations necessary in weapons development and in the hybrid field of operations research. The invention in 1947 of a new type of electronic component, the transistor, by three scientists at Bell Labs in New Jersey, opened up new possibilities for the miniaturization of these room-sized devices. In 1948, Claude Shannon, also working at Bell Labs, published the basic concepts of information theory, which was to revolutionize communications (Shannon 1948).

Similarly, the young science of economics was given a boost by two important events: the publication of Paul A. Samuelson’s (1947) Foundations of Economic Analysis and, just one year later, the publication of Samuelson’s principles-based textbook, Economics, which became the best-selling economics textbook for decades and is currently in its 19th edition (Samuelson 1948).

The Financial Analysts Journal was launched in this intellectual milieu. From , we see that the focus of articles during this era was on the financial outlook for various industries—utilities, railroads—and general investment and security analysis. Benjamin Graham is among the top 20 authors in this time period, with five articles to his credit. Based on the most frequently used words appearing in Financial Analysts Journal titles during this era, the origins of value investing and security analysis and the canonization of Graham and Dodd become self-evident.

1952–1963: The Modern Portfolio Theory Era (Markowitz to CAPM)

Under these conditions, it is no coincidence that the Classical Financial Era is also the precursor to a golden age of academic finance. With a background in operations research and frustrated with the lack of treatment of risk in the financial models of the time, Harry Markowitz (1952) developed the mean–variance theory of portfolio selection. He incorporated the trade-off between risk and return into a systematic analysis for the first time and almost incidentally set into motion the development of a new academic field and a multi-trillion-dollar industry.

This body of work gave rise to the Modern Portfolio Theory Era, a development that we now take for granted as an obvious intellectual advance. In the heyday of Graham and Dodd’s (1934) Security Analysis, however, the thought of abandoning the company-specific analysis of financial ratios, earnings multiples, and discounted cash flows in favor of return expectations, standard deviations, and covariances must have been considered absurd by most finance professionals. Even decades later, Benjamin Graham’s most famous disciple, Warren Buffett, famously quipped that, rather than not putting all his eggs in one basket, as modern portfolio theory recommends, he preferred to do just that and then watch that basket very carefully.

Of course, such a strategy is highly effective if you happen to have Buffett’s considerable basket-watching skills. Markowitz offered an alternative that required a different set of skills, one more easily acquired than Buffett’s stock-picking ability. Markowitz’s alternative quietly marked the beginning of two important trends that would continue for decades: the democratization of finance and the revenge of the nerds. We shall return to both in the following eras.

During the Modern Portfolio Theory Era, the United States had an expanding and confident economy marked by short recessions and stable prices. Americans, believing (rather inaccurately) that these years were a high point of American prosperity and stability, would later become nostalgic for this period. Below the surface, however, this seeming stability concealed a subterranean current of technological innovation and sometimes even technological panic. It was the first decade when every household had to have a television set, which prefigured our age of ubiquitous screen technology. The first integrated circuit was invented in this decade, as was the first metal-oxide-semiconductor field-effect transistor, the basis for the modern computer chip. It was the decade when the United States first realized that it might fall technologically behind its competitors, after the Soviet Union successfully launched Sputnik 1, the first artificial Earth satellite, in 1957.

It was also the decade when the first mass-produced electronic computer went to market, the IBM 650. It was becoming clear that the electronic computer, far from being a niche product for a select group of scientists, engineers, and military professionals, was a general-purpose technology, one that could be applied to any field that generated a large amount of data, including financial markets. With this greater computing power, it became possible to apply statistical methods to financial data in greater depth and with greater rigor, in addition to performing humbler tasks, such as calculating values for bonds and mortgages that were unlisted in standard financial tables.

The Financial Analysts Journal during this time continued to focus on industry outlooks and security analysis, with eight articles from Graham in this era, including his highly influential 1952 contribution, “Toward a Science of Security Analysis” (Graham 1952). For the first time, however, “economic” and “economy” appear in the list of top 20 title words, perhaps reflecting the growing impact of economics on business analysis, thanks to Samuelson’s (1948) best-selling textbook from the previous era.

1964–1972: The Alpha Beta Era (CAPM to Cboe)

The popular memory of the 1960s is one of a politically tumultuous and, at times, violent era, but it was also the time of the first long technology stock bull market, the “Go-Go Years,” and not coincidentally, also the time of the first tech stock bust.

Underlying the technology stock boom was the realization that there was something new in the technological world, as Gordon Moore presciently observed in 1965. In this intellectual environment, four financial researchers proposed the tenets of the capital asset pricing model (CAPM) almost simultaneously: William Sharpe (1964), John Lintner (1965), Jan Mossin (1966), and Jack Treynor (1961, 1962). These four individuals with varying backgrounds—three Americans and one Norwegian, three born in the 1930s and one in the 1910s, three academics and one practitioner—converged on the same fundamental concepts of a quantifiable trade-off between risk and reward, where risk is measured by the correlation of an asset’s return with the return of the market portfolio.

The CAPM was the final brick in the theoretical foundation of passive investing that began with Markowitz and his development of modern portfolio theory. The CAPM gave investors a framework that distinguished unique investment skill, alpha, from commoditized risk premium, beta. In doing so, the CAPM catalyzed the development of an array of financial innovations, including index products and benchmarking, portable-alpha and hedging strategies, performance attribution, risk budgeting, and many more. But most important of all, the CAPM framework and lexicon provided a systematic method through which institutional portfolio managers could discharge their fiduciary duties, thereby unleashing trillions of dollars of investable assets for those seeking prudent investment opportunities. It is only fitting that the Alpha Beta Era is bookended by Sharpe’s (1964) academic publication on the CAPM at its start and his very first Financial Analysts Journal publication, the practitioner version titled “Risk, Market Sensitivity and Diversification” (Sharpe 1972), at its end.

Ironically, at the same time that the seeds of passive investing were being planted and watered, the age of the “gunslinger” portfolio manager had arrived. The finance profession elevated a new generation of managers and analysts—such as the charismatic financier Gerry Tsai of Fidelity and, subsequently, the Manhattan Fund—who entered it during a period of financial euphoria and propelled the popularity of retail mutual funds to a new level, only to see the market falter and plunge by the end of the decade. It was an extinction-level event among hedge funds, since those that failed to hedge, a forgotten skill, failed entirely. While the market was increasingly accessible, transaction costs were still high, making it difficult for the retail investor to diversify.

Moore’s Law, first announced in 1965, was originally a statement about computing power, but the same discoveries in electronics that created a revolution in computing also made possible a less heralded revolution in financial communications. The Alpha Beta Era saw the emergence of electronic clearinghouse operations between banks; the opening of Instinet, the first off-exchange trading system; and the opening of NASDAQ, the first electronic exchange, although initially it only served as an electronic quotation system for the “pink sheets” of the OTC market.

At the same time, analyses of return data making use of new computing technologies showed that professional managers often had worse performance than simple strategies and portfolios. By current standards, this quantity of Big Data was absurdly small, but computing power, and thus the ability to crunch these numbers, was increasing at an exponential rate. In this informationally richer environment, Paul Samuelson (1965) and Eugene Fama (1970) first formulated the radical idea that asset prices reflect all available information—what is now called the Efficient Markets Hypothesis. Further empirical work testing the CAPM and its application to measure the alphas of mutual fund managers added more weight to the academic conviction that active management did not justify its fees, setting the stage for the passive-investment revolt in the subsequent era.

Underneath these technologically driven innovations was a slower trend, dating back to the wave of postwar homeownership but now vastly accelerated thanks to the Housing and Urban Development Act of 1968. The Government National Mortgage Association, known as Ginnie Mae, which guaranteed many federally issued residential mortgages, developed a new financial process, securitization, aggregating a pool of mortgages into a new type of financial instrument, the mortgage-backed security. For decades, this financial innovation would allow lenders to provide loans to prospective homebuyers at a lower cost by providing a market for the risk. The process of securitization would eventually be applied to other assets, such as credit card receivables, auto loans, student loans, and music royalties.

In this era, the Financial Analysts Journal debuted three articles in 1971 by a 32-year-old practitioner who had launched his consulting practice, called Associates in Finance, only two years earlier. His first article in the journal was titled “Implications of the Random Walk Hypothesis for Portfolio Management,” while his second and third were Parts I and II of “Toward a Fully Automated Stock Exchange” (see the cover illustration in Panel B of ).Footnote8 These contributions presaged the central role that academic finance and technology were to play in the next decades, particularly the ideas of market efficiency and the growing importance of artificial intelligence and algorithmic trading. This young financial analyst was named Fischer Black.

Figure 4. Illustrations for Volume 27 of the Financial Analysts JournalSource: CFA Institute.

This same volume of the Financial Analysts Journal also included Walter Bagehot’s (1971) article “The Only Game in Town,” a landmark contribution on the role of the market maker in providing liquidity in exchange for the bid–offer spread. This penetrating analysis—by an author adopting the name of a long-departed financial writer of the Victorian Era as a pseudonym—was the acorn that sprouted into the mighty oak of the market microstructure literature, one of the earliest examples of a practitioner and Financial Analysts Journal author having a substantial impact on academic finance rather than the other way around. In fact, this article was cited by both of the academic publications often considered to be the theoretical cornerstones of microstructure theory: Glosten and Milgrom (1985) and Kyle (1985). It was subsequently revealed that Walter Bagehot was, in fact, Jack Treynor, and his article was republished in 1995 in the Financial Analysts Journal’s special 50th anniversary issue under Treynor’s own name (Treynor 1995).

During the Alpha Beta Era, several new words appeared in the Financial Analysts Journal’s list of top 20 title words, as can be seen in : “portfolio,” “accounting,” and “policy.” As a testament to the durable impact of academic finance on practice, “portfolio” appears in the top 20 list for all future eras as well. Meanwhile, the growing importance of accounting and policy to financial analysis is consistent with the introduction of government-sponsored enterprises and their impact on mortgage markets, in particular, and fixed-income markets, more generally.

1973–1981: The Derivatives Era (Cboe to Bloomberg Terminal)

In addition to the aforementioned banner articles, the year 1971 saw the suspension of convertibility of the dollar into gold and the formation of a floating-currency exchange rate regime to replace the fixed exchange rates of the Bretton Woods monetary system. This monetary crisis was a foreseeable one. As the world’s economies regained their former strength, imbalances in the system made the United States’ central role increasingly untenable. The United States left this system at a time of increasing inflation and increasing debt. Over the next several years, it would be struck by a shock in the price of meat, leading to price ceilings set by the president, and by two oil shocks, causing local shortages in gasoline and escalating energy prices, while the price of gold, now disconnected from the dollar, reached a record high. Standard macroeconomic policy did not gain any traction. These were the years of stagflation—a combination of low growth, high unemployment, high interest rates, and high inflation.

This economic environment of risk and uncertainty was the ideal setting for the growth in financial derivatives to better manage these challenges. For this reason, this period is named the “Derivatives Era.” There is a recurring pattern of development between necessity and technology in this era, most famously between the founding of the Cboe in 1973; Black, Scholes, and Merton devising the option pricing formula that bears their name in that same year;Footnote9 and the release in 1975 of the Texas Instruments SR-52, the first programmable handheld calculator capable of handling the logarithmic and exponential functions of the Black–Scholes/Merton formula.Footnote10

This turning point not only sparked a blossoming of the derivatives markets, but it also cemented the connection between academia and the financial industry—started by Markowitz and fueled by Sharpe and his CAPM co-creators years before—by giving practitioners a formal and systematic framework for understanding the behavior of increasingly complex financial instruments. Finance professionals began to think of their field as a form of engineering rather than deal making, part of a longer sociological trend in which the broader economic sciences would take their primary inspiration from physics and mathematics (see Lo and Mueller 2010).

Meanwhile, the change to floating exchange rates was a perfect environment for the creation of entirely new categories of derivatives. Although currency futures and forward contracts were developed in anticipation of the abandonment of fixed exchange rates, they became actively traded only afterward. These were followed by currency swaps, developed in order to avoid capital controls, and then interest rate swaps. Salomon Brothers brokered the first such deal in 1981, between IBM and the World Bank, with IBM swapping its Swiss francs and German marks for the World Bank’s US dollars. These derivatives would grow exponentially in popularity.

Nevertheless, other markets were in the doldrums. Brokerages had urged the SEC for years to increase the rate of commissions in response to a long-term decline in retail investors. On May Day, 1975, however, the SEC abolished fixed rates entirely, signaling a new wave of financial competition and innovation centered on the drop in trading cost, resulting in the growth of index and mutual funds as well as electronic and automated trading technologies. The First Index Investment Trust, later to become the Vanguard 500 Index Fund, implementing John C. Bogle’s at-cost philosophy, was incorporated on 31 December 1975.

Thus began the decades-long trend toward passive investment strategies and products, built on the firm academic foundations of the two previous eras. This trend was hastened by attractive equity returns, declining trading costs, and technological advances in trade execution, order processing, and telecommunications, such as the Designated Order Turnaround (DOT) routing system at the New York Stock Exchange and the realization of NASDAQ into a fully electronic financial exchange. Moore’s Law continued to accelerate the infrastructure of the financial system, and even consumers with no direct connection to the financial markets experienced this acceleration firsthand through the birth of direct deposit for their paychecks.

This era also included a key milestone for the co-evolution of technology and finance theory: the founding of Barr Rosenberg Associates, or BARRA, in 1974 by its eponymous University of California, Berkeley, finance professor. A consulting firm that eventually became a technology company, BARRA provided the entire financial industry with the tools to implement the theories of Markowitz, Sharpe, and others, becoming a pioneer in translating finance theory into practice. The legacy of Rosenberg still stands to this day through Morgan Stanley Capital International (MSCI), which acquired BARRA in 2004 and now offers a greatly expanded set of portfolio construction tools under the MSCI/BARRA brand.

With the arrival of BARRA, the practical infrastructure needed to accelerate the trend from active to passive investment was now complete. The elitism of unique investment opportunities was beginning to give way to the democratization of finance. Access to the old-boys network began losing ground to those with knowledge of computer networks. Graduates of Harvard and Yale began losing ground to the graduates of Caltech and MIT. Meanwhile, the cult of the star portfolio manager was giving way to the science and engineering practice of portfolio management and the rise of the Wall Street quant.

This was the revenge of the nerds, the trend first initiated by Markowitz in 1952, whose thesis adviser, Milton Friedman, jokingly threatened to withhold Markowitz’s PhD in economics because his dissertation was not “economics.” Markowitz (1991, p. 476) acknowledged that “at the time I defended my dissertation, portfolio theory was not part of economics. But now it is.” In the same vein, alpha, beta, and the Black–Scholes/Merton formula were not part of financial analysis at the birth of the Financial Analysts Journal. But now they are.

During the Derivatives Era, the word “risk” made its first appearance in the top 20 Financial Analysts Journal title words list, right on cue in this financially tumultuous period, and it has remained in the top 20 ever since. Given the double-digit levels of inflation during this era, it is no surprise that “inflation” also joined the top 20, but it has not appeared on the top 20 lists of subsequent eras.

In this era, Fischer Black and Jack Treynor—no strangers to the Financial Analysts Journal—joined the list of top 20 authors for the first time, as did Barr Rosenberg and future Nobel Laureate William Sharpe. The many Financial Analysts Journal publications by top academics, alongside such profoundly insightful practitioner articles as Treynor’s “The Only Game in Town” (Bagehot 1971) and Black’s (1975) “Fact and Fantasy in the Use of Options,” transformed the journal’s reputation among finance academics from an industry trade magazine to a highly respected research forum for those academics interested in the practice of finance. As a result, in this era and beyond, finance academics began publishing some of their best work in the Financial Analysts Journal. The list includes Rosenberg and Guy’s (1976a, 1976b) articles on estimating linear multifactor models; Jensen and Meckling’s (1978) foray into the political economy of the theory of the firm; Modigliani and Cohn’s (1979) argument that the stock market was significantly undervalued because it did not properly account for inflation; Reinganum’s (1981) empirical documentation of the small-firm premium; and Rubinstein and Leland’s (1981) recipe for constructing portfolio insurance. The Financial Analysts Journal had arrived.

1982–1988: The Automation Era (Bloomberg Terminal to WWW)

The next several years saw the US economy return to a period marked by the absence of macroeconomic shocks and an environment of low inflation and low unemployment. Internationally, Japan was going through a long boom and was viewed by many Americans as the United States’ primary economic competitor, while the Soviet Union remained its primary military competitor. The personal computer became a common household item, and the home spreadsheet program one of its most popular forms of software, while the US stock market began another long bull run. Therefore, almost inescapably, this period must be named the “Automation Era.”

In this newly wired environment, necessity drove mathematicians and computer scientists to develop new cryptographic security concepts to cope with the possible violation of trust in an increasingly networked world while new cryptographic systems were implemented to protect everyday transactions from interference.Footnote11 The first major financial hack took place against the First National Bank of Chicago in 1988; it was an attempted electronic transfer of $70 million from United Airlines and Merrill Lynch to banks in Austria and was considered at the time an exotic form of embezzlement.

At the same time, the financial exchanges continued to modernize, with the NYSE installing its SuperDOT electronic order-routing system and NASDAQ its Small Order Execution System (SOES), and in December 1982, the first Bloomberg Terminal (with its color-coded “chiclet” keyboard) debuted. New types of trading took advantage of these new electronic interconnections. For example, the pairs trading strategy developed at Morgan Stanley and then at D.E. Shaw used statistical analysis to identify pairs of correlated stocks for automated trading systems to buy and sell.Footnote12 Other forms of statistical arbitrage quickly followed, and the term “SOES bandits” became both a despised moniker used by unsuspecting institutional investors and a badge of honor among those with the technological savvy to profit from their ability to exploit this system.

This newly interconnected financial environment may have contributed to the wholly unexpected Black Monday stock market crash of 19 October 1987. Others cast blame on portfolio insurance, particularly on strategies implemented by Leland O’Brien Rubinstein Associates, as first outlined in the Financial Analysts Journal article by Rubinstein and Leland (1981). While its causes are still unknown, the Black Monday crash introduced the important financial innovation of the “circuit breaker” trading curb, now mandatory on US financial exchanges, which halts trades should prices fall below a set threshold, to reduce volatility and prevent panic sell-offs.

In the Automation Era, three important new additions appeared in the Financial Analysts Journal’s top 20 title words for the first time: “bond,” “pension,” and “index.” The journal’s history until this point was dominated by topics related to equities, understandable given its roots in the New York Society of Security Analysts. However, the increasing sophistication of fixed-income markets and investors—including pension funds—motivated an equally sophisticated financial analysis. In the jargon of ecology, pension funds are a “keystone species,” a group of stakeholders that are central to the health and robustness of an ecosystem, without which the functioning of that system would be radically impaired. In a pair of articles, mathematician-cum-bond-guru Martin Leibowitz (1986a, 1986b)—a top 20 Financial Analysts Journal author across five eras—introduced the notion of a dedicated bond portfolio for pension plans, forever changing the way institutional investors manage interest rate risk in their massive portfolios.

Indexing also came of age during the Automation Era, hence the term’s popularity in Financial Analysts Journal titles, but the rise of the index fund is also related to the innovation of stock index futures in this period. It is difficult to imagine financial life without S&P 500 Index futures, especially from the perspective of risk management. Figlewski and Kon (1982) first described the benefits and applications of this important contract in the journal prior to the creation of futures contracts in April 1982, when the Chicago Mercantile Exchange first launched its S&P 500 futures contract. There is little debate that pension funds contributed significantly to the popularity of this contract and other financial futures.

Finally, during this era, we see the seeds of algorithmic trading being planted through articles by Burns (1982) on electronic trading in futures markets and Hill and Jones (1988) on what was then called “program trading,” as well as from academics, such as Amihud and Mendelson (1982), who were pioneers of the empirical market microstructure literature.

1989–1999: The Financial Globalization Era (WWW to HFT)

With the benefit of hindsight, the most important financial innovation during the Automation Era was taking place outside the financial world entirely, at CERN, the European Organization for Nuclear Research, located outside Geneva. A young physicist employed by the world’s largest particle accelerator was creating a software platform to share data and coordinate experimental design efforts among fellow physicists hailing from multiple universities around the world. In 1989, this platform—known as the World Wide Web—was launched by Timothy Berners-Lee, ushering in the Financial Globalization Era.

At the time, the fall of the Berlin Wall and the later dissolution of the Soviet Union seemed to overshadow any mere technological innovation. The United States became the world’s first hyperpower, while the diminished geopolitical tensions allowed Germany to reunify and the European Union to form. However, Moore’s Law continued to operate, making computing and communication devices cheaper and more powerful with every passing year. Cellphones became common in the United States, and the first smartphone, combining the power of the computer with the function of a telephone, was invented—becoming popular first in Japan.

The internet and the World Wide Web were becoming commonplace in US households, but their economic potential would not be realized until the development of cryptographically secure transactions for payment over the internet, to keep financial transactions safe and to prevent fraudulent transactions from taking place. Although RSA Security was founded in the previous era (1982) by the three MIT computer scientists who developed this technology—Ron Rivest, Adi Shamir, and Leonard Adleman (1978)—it was in the mid-1990s that the company’s encryption technology became the de facto standard of the computer industry and, by extension, the standard of most companies that conducted business through computers.

This single innovation brings into sharp focus the deep interdependencies between technology and the financial system. By ensuring the security and privacy of data transmission, RSA established trust in all online transactions, and trust is at the very core of finance and commerce. It is no exaggeration to say that RSA encryption facilitated not just the entire e-commerce industry but also the spectacular globalization of the financial industry, which depends on encrypted telecommunications.

Almost immediately following this innovation came what is known as the dot-com boom. An enormous wave of speculative investment funded prospective internet retailers, technology and telecommunications companies, and providers of other internet services, including entirely new categories of enterprise, such as the search engine and the internet auction.

The dot-com boom helped fund the rise of mass accessibility and the further democratization of finance, including the online brokerage and the online payment processor, the cornerstones of current fintech. It specifically made itself felt on NASDAQ, whose composite index rose fourfold from 1995 to its peak in 2000. But other financial innovations were being made at this time, including the development of the modern credit derivative and the credit default swap and the creation of the first exchange-traded funds.

An important factor behind these innovations was the low–interest rate environment leading up to this era. In contrast to the stagflation of the Derivatives Era, during which the US federal funds rate reached an all-time peak of 22% in December 1980, interest rates declined precipitously—to below 3% by December 1992 (). If return on investment is viewed as the foodstuff of the financial ecosystem, a low-yield environment is tantamount to widespread famine, with all its attendant implications for investor behavior, including a “reach for yield” by such financial species as pension funds, insurance companies, and other large institutional fixed-income investors.Footnote13 In this milieu of heightened competition, financial intermediaries created and expanded for these yield-starved financial institutions a smorgasbord of higher-yielding investments—such as junk bonds, collateralized debt obligations, and mortgage-backed securities—and a host of exotic hedge fund strategies—such as statistical arbitrage, convertible bond arbitrage, and emerging market debt. Because higher yields are linked to higher risk, however, reaching for yield inevitably implies the prospect of greater financial losses. It is no coincidence that this era was associated with financial crisis and contagion.

Source: FRED® Graphs ©Federal Reserve Bank of St. Louis. Effective Federal Funds Rate [FF], retrieved from FRED 8 May 2021. All rights reserved. All FRED® Graphs appear courtesy of Federal Reserve Bank of St. Louis. https://fred.stlouisfed.org/.

![Figure 5. Effective Federal Funds Rate, 1 July 1954–6 May 2021Source: FRED® Graphs ©Federal Reserve Bank of St. Louis. Effective Federal Funds Rate [FF], retrieved from FRED 8 May 2021. All rights reserved. All FRED® Graphs appear courtesy of Federal Reserve Bank of St. Louis. https://fred.stlouisfed.org/.](/cms/asset/64e94c4d-09e2-475b-a49a-8b7b4b92e66b/ufaj_a_1929030_f0005_c.jpg)

The Japanese asset bubble popped in the early 1990s, leading to decades of stagnation in Japan. The Asian financial crisis of 1997 transmitted itself across nations as different as South Korea and Indonesia. Finally, the Russian financial crisis of 1998 caused Russia to devalue the ruble and default on its debt, almost incidentally bringing down Long-Term Capital Management, whose central connection to many US financial firms led to fears that it would precipitate a chain reaction of failure in the US financial system. Is there any better illustration of the “butterfly effect” and the complex interconnections of the global financial system than the default of a sovereign debt issue (held by relatively few investors) triggering a major global financial crisis four weeks later?Footnote14 Despite these events, substantial new regulatory proposals were dismissed. In fact, it was during this era that the famous firewall between commercial and investment banking—put in place by the Glass–Steagall Act six decades earlier—was deliberately and systematically dismantled.

During the Financial Globalization Era, the most frequently used word in the titles of Financial Analysts Journal articles was “risk,” almost as if the authors sensed they were heading into challenging financial waters. For the first time in the journal’s history, “international” entered the top 20 list, underscoring the fact that the previous Automation Era led inexorably to a more globally connected financial world. Hedging international exposures was the concern at the start of the Financial Globalization Era, as illustrated by the hedging strategies of Black (1989), Kritzman (1989), and many others. But attention eventually turned toward constructing a globally optimal portfolio, as in the highly cited paper of Black and Litterman (1992), and the empirical properties of globally diversified portfolios, as documented by Capaul, Rowley, and Sharpe (1993), Odier and Solnik (1993), and Sinquefield (1996). The US financial industry had finally awakened to the rest of the world.

2000–2009: The Algorithmic Trading Era (HFT to Bitcoin)

The dot-com boom, peaking in March 2000, failed to last. Ready to feed on its downturn, however, was high-frequency trading (HFT), a form of algorithmic trading that places, revises, and cancels buy and sell orders at ultra-fast speeds to generate profits. At the turn of the millennium, this speed could still be measured in seconds—fast but not exceptionally so. However, the frequency of trading rose exponentially in less than a decade to microsecond levels—a pace of innovation so quick that HFT practitioners discovered that their results (and sometimes their systems infrastructure) would become obsolete in a matter of months (Loveless 2013). High-frequency trading became rapid enough that traders were actually running up against the speed of light and other pesky laws of physics as a practical limitation of their algorithms, causing HFT firms to vie for coveted locations for their computers—specific shelves on the metal racks of giant server farms—that were closest in physical proximity to the servers of major stock exchanges. Thanks to Moore’s Law and RSA encryption algorithms, HFT became a significant percentage of the daily trading volume on most electronic exchanges.

But another change in the financial ecosystem facilitated the rise of high-frequency traders: “decimalization,” the SEC-mandated shift of all US stock market price movements from fractions of a dollar (eighths and, for larger trades, sixteenths) to cents on 9 April 2001. On the surface, such a shift seemed a long time coming. After all, denominating heavily traded assets such as the equities of Fortune 500 companies in increments of $0.125 and $0.0625 during the age of programmable calculators, computers, and automated trading systems seems completely incongruous. The fact that this practice originated in the 1600s in Spain—because traders once used gold doubloons that could be easily cut in half, quarters, and eighths—added even more motivation to modernize the system. The final push came from institutional investors, such as pension fund managers, which argued that bid–offer spreads were artificially inflated because of the use of fractional dollars and that decimalization would result in lower trading costs for all market participants. However, as with many well-intentioned proposals, there were unintended consequences.

Bagehot/Treynor (1971/1995) recognized that the existence of the bid–offer spread was meant to compensate designated market makers or “specialists,” individuals charged with the responsibility of “maintaining fair and orderly markets” by quoting bid and offer prices at which they were willing to transact at any time with any counterparty that sought to buy or sell. This responsibility makes the market a market; specialists provide the liquidity to maintain it. In doing so, however, specialists are often trading against parties that possess more information about the asset than they do, hence the existence of a bid–offer spread to compensate the specialist for having an informational disadvantage (known as “adverse selection” in the market microstructure literature).

What would be the implications if spreads were allowed to move more freely, a penny at a time instead of at 12.5¢ intervals? The immediate consequences were as expected: Spreads declined—in some cases, to just a penny—benefiting retail and institutional investors as trading costs also fell. However, the decline in spreads reduced the profitability of specialists, causing a mass exodus of these designated market makers.Footnote15 In the wake of their departure, hedge funds, proprietary trading desks, and HFT shops stepped in, providing the liquidity that specialists had previously offered. As Merton (1993) taught, the need for liquidity services did not change in response to a seemingly minor regulatory shift from eighths to decimals, but the institutions providing that liquidity changed dramatically.

However, unlike the designated market makers of the NYSE and NASDAQ, these new liquidity providers were not under any exchange-mandated obligations to provide liquidity regardless of market conditions. By dynamically deploying capital only when it suited them while getting up from the poker table when the odds were against them, these sophisticated algorithmic traders were able to generate remarkably consistent profits. A rare glimpse of this consistency was afforded by the 2014 initial public offering of the HFT firm Virtu Financial. Its S-1 filing disclosed that between 1 January 2009 and 28 February 2014, a period of 1,278 consecutive trading days, it experienced only 1 losing day.Footnote16

The “fair-weather friend” nature of liquidity provision during this era was made painfully clear during the “Quant Meltdown” of August 2007, when a large statistical arbitrage portfolio was apparently liquidated abruptly, causing losses in that entire strategy class for many hedge fund portfolios.Footnote17 In the midst of heavy trading, liquidity dried up much more quickly than expected, presumably because the new liquidity providers, such as high-frequency traders, experienced losses at the start of the liquidation process and decided not to participate during this rout.

Since decimalization began, institutional investors have observed and complained about the fact that, although spreads are indeed lower, the size of the trades that can be transacted at these lower spreads has also declined and the sensitivity of spreads to changes in market conditions and imbalances between supply and demand is much higher. This episode illustrates the subtle, complex, and dynamic nature of adaptive markets and how new species quickly emerge to occupy ecological niches relinquished by less adaptive competitors.

But the main story of the Algorithmic Trading Era was, of course, the dot-com bust followed by the tragedy of the 11 September 2001 attacks and their military sequels. In response, the Federal Open Market Committee lowered the federal funds rate from 6.5% at the peak of the boom to only 1.0% three years later. At the same time, US politicians told US consumers to spend to prevent an economic downturn and actively promoted the “ownership society” in which homeownership played a significant part. House prices were appreciating, and bipartisan policies were implemented to extend more credit to potential homeowners, while mortgage originators expanded their business. Financial innovations such as adjustable-rate and teaser-rate mortgages, automated mortgage approvals, and NINJA (“no income, no job, no assets”) loans expedited this process. In this environment, more homeowners began to use homeownership as a speculative asset. Meanwhile, these mortgages were packaged into a newly popular form of asset-backed security known as the “collateralized debt obligation,” which pooled the mortgages and divided them into tranches based on the probability of default. Some of these tranches were insured against default through credit default swaps.

In the meantime, the global economy had begun to shift. The entry of the People’s Republic of China into the World Trade Organization in 2001 marked the beginning of the largest economic expansion in human history. Chinese manufactured goods became staple items in global commerce, while the Chinese population solidly entered the global middle class, some of its members entering into the ranks of the ultra-rich. In the United States, the technology companies that survived the dot-com bust began to consolidate, as many of their functions expanded to fill the role of natural monopolies. A new form of communication, social media, began to displace the role of older sources of information, while the ease of copying digital media displaced traditional recorded media, such as music.

The story of the downturn in the US housing market, and the financial chain reaction that led to the global financial crisis, has been told and retold, so there is little need to do so again here. By most accounts, the global financial system very nearly collapsed in 2008, as two major US investment banks failed and others were poised to follow. For our adaptive narrative, however, these events had at least three important consequences. The first was the realization that there was no single financial innovation or regulatory failure that was responsible for the crisis. It was a system-wide crisis, with system-wide causes. In fact, Khandani, Lo, and Merton (2013) showed that the combined effect of rising home prices, declining interest rates, and near-frictionless refinancing opportunities—none of which by itself is considered dysfunctional or deleterious—can create an unintentional synchronization of homeowner leverage leading to a “ratchet” effect, because homes are indivisible and their owner-occupants cannot raise equity to reduce their leverage when home prices fall. A simulation of this refinancing ratchet effect in the US housing market yields potential losses of $1.7 trillion from June 2006 to December 2008, which is comparable in order of magnitude to the actual losses during this period.

The second consequence of the financial crisis of 2008 was that, as with any ecological system experiencing major disruption, there would be new winners and losers in its aftermath, when an “adaptive radiation” of species often occurs in newly unoccupied ecological niches.Footnote18 In the case of the financial crisis, this adaptive radiation involved two closely related trends: the continuing consolidation of financial institutions within each financial subsector into more capital-efficient behemoths (e.g., mutual fund complexes, investment and commercial banks, hedge funds, and private equity funds) and the emergence of smaller, more nimble financial technologies, or “fintech,” to compete with these behemoths. The same innovative energy that gave rise to e-commerce, search engines, and social media now turned its focus to reinventing the financial system in its own disruptive image. New payment systems, lending institutions, brokerages, and asset management services were launched, not from Wall Street but from Silicon Valley. One of the most unlikely and most innovative of these new businesses was cryptocurrencies.

Many people distrusted the measures taken to preserve the global financial system, which they saw as rewarding the malefactors who caused it. One of these people may have been an anonymous computer scientist using the name “Satoshi Nakamoto.” This person’s invention, bitcoin, used cryptographically secure principles to create a distributed system of electronic transactions that did not rely on a central authority or trust of any kind to transfer digital assets. It is believed that “Nakamoto” was influenced by hard money theorists who favored the historically unfounded stability of a metallic currency standard, since the ultimate supply of bitcoin, although the result of a digital process, is inherently limited and progressively more difficult to generate. This new wave of cutting-edge technologists effectively wanted a return to the gold standard but on their terms.

The third consequence of the financial crisis of 2008 was to refocus attention on financial ethics, the importance of corporate governance, and the broader environmental, social, and governance (ESG) investment trend that will become even more mainstream in the next era. None of these issues were new to the financial industry, but they gathered considerably more urgency thanks to the financial excesses and malfeasance of this era, topped off in December 2008 with the unraveling of the $50 billion Bernie Madoff Ponzi scheme.

All of these developments were reflected in the concerns of Financial Analysts Journal authors and, in some cases, anticipated by them. At the start of the Algorithmic Trading Era, several articles were published on the risk/reward characteristics of hedge fund strategies—including day trading, statistical arbitrage, commodity futures, and HFT—and how they differed from more traditional investments.Footnote19 The title of Leibowitz’s (2005) contribution to this literature, “Alpha Hunters and Beta Grazers,” provides a pithy summary of the ecological dynamics involved in the financial industry during this era.

The growing importance of credit markets and the unique risks they contain were reflected in two articles by Stephen Kealhofer (2003a, 2003b), the co-founder of the eponymous KMV, a leading credit risk analytics company acquired by Moody’s Corporation in 2002. Meanwhile, the rapid development of structured finance, including the alphabet soup of mortgage-related financial instruments, was covered by Frank Fabozzi (2005), near the peak of the US residential real estate market.

Finally, in the aftermath of the 2008 crisis, the Financial Analysts Journal played an important role in sifting through the wreckage, with articles on regulatory and policy reforms by Markowitz (2009), Reinganum (2009), Statman (2009), and Roll (2011).

With respect to ethics, the journal has published numerous articles on the topic over the years, and CFA Institute has long required charterholders to adhere to its Code of Ethics and Standards of Professional Conduct.Footnote20 In fact, on the first page of the very first issue of the first volume of the Financial Analysts Journal in 1945 (called the Analysts Journal at the time), its editorial board wrote that the journal should include “consideration of ethics and standards in the profession of security analysis.” However, the 2008 crisis highlighted an important new ethical concern to the profession—the overreliance on quantitative methods and models, encouraged by the false precision that these tools exhibit. This concern was well expressed by McAlmond’s (2008, p. 10) letter to the editor, titled “Too Much Emphasis on Quantitative Methods Instead of Ethics?”:

In my most recent [Financial Analysts Journal issue], I find not one article on ethics. The articles are full of probability graphs; they cover relative earnings forecasts, buy-side versus sell-side arguments, and the benefits of short extensions. But what of the benefits of making the best ethical decisions and keeping our clients’ trust? And how can we understand these issues? Our business is more than a hard science. The most important quality we bring to our clients is not our ability to calculate numbers or create graphs.

The most recent credit crisis is full of ethical dimensions that could be discussed. Was it ethical to push people into buying homes that they could not afford? Was it ethical to package these products that did not live up to their credit ratings? Was it ethical to sell these packages to investors, foreign banks, and others? Analysis of the ethical issues of our products and services can be just as important as, if not more important than, the mathematical analysis.

I hope to see many more articles in [the Financial Analysts Journal] that discuss the ethical dimensions of investment products and services.

2010 to 2021: The Digital Assets Era (Bitcoin to Coinbase)

Following the financial crisis, the United States led the long recovery among the advanced economies through financial sector reforms, bailouts of systemically important institutions, and the largest overhaul of the financial regulatory system since the 1930s, culminating in the Dodd–Frank Wall Street Reform and Consumer Protection Act of 2010. This piece of legislation called for a number of new regulations—some of which have yet to be implemented—but one of the signature components was the establishment of the Office of Financial Research (OFR), perhaps the first time the federal government has so explicitly acknowledged the importance of financial research and data collection since Alexander Hamilton’s establishment of the Treasury Department (in which the OFR resides).

This era also saw expansive monetary policy, including several rounds of quantitative easing that seemed extraordinarily aggressive at the time but turned out to be only the dress rehearsal for the multi-trillion-dollar US stimulus amidst the COVID-19 pandemic in 2020–2021. The overhang of accumulated debt, however, exerted a drag on the US economy, while greater fiscal stimulus was politically constrained. Other nations had poorer outcomes, especially those on the periphery of the eurozone, the unified currency area established by the European Union in 1999. Despite fears of inflation, deflationary pressures dominated the recovery. With lower yields and lower amounts of leverage available to hedge funds, their returns suffered, hastening the already sizable flow of capital from actively managed financial products and services to passive index products and causing even greater consolidation across all categories of financial institutions.

Nevertheless, Moore’s Law continued to operate, although signs began to appear that it was finally slowing down. After a significant delay, smartphones became popular and then nearly ubiquitous in the United States. Another technology boom began, centered on applications for these phones. Many previously overlooked services were transformed through these “apps,” such as taxi and ridesharing services and short-term rentals, while banking, trading, and financial advisory apps were quickly developed. These allowed financial services to become portable, accessible, and available at low cost to a much broader population of potential clients.