?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

We study private shareholder engagements with 2,465 listed firms about environmental, social, and governance (ESG) issues from 2007 to 2020. We examine the extent to which private engagements address financially material ESG issues and contribute to firm performance. We find that material engagements succeed more often than immaterial engagements and that the targets of successful material engagements significantly outperform their peers by 2.5% over the next 14 months. Further, we find that material engagements are more often associated with improvements in profitability and cost ratios than immaterial engagements. Finally, our evidence indicates that a decrease in CO2e emission intensity accompanies environmental engagements.

PL Credits: 2.0:

Introduction

Institutional investors increasingly engage with portfolio companies on environmental, social, and governance (ESG) issues via letters, calls, physical meetings, public statements, or votes on shareholder proposals. For example, through the Climate Action 100+ initiative, investors engage with firms producing more than 80% of the global industrial emissions to encourage them to reduce those emissions and to improve corporate disclosure (Climate Action 100 + Citation2022). The research has pointed out that such shareholder engagements are a plausible mechanism for investors to affect ESG policies relative to other methods, such as capital allocation (Kölbel et al. Citation2020).

For institutional investors, it is important to determine which ESG issues matter for performance and what makes engagement successful. To shed further light on the nature and outcomes of ESG engagement, we study private engagements (e.g., calls, letters, meetings) undertaken by an investor with a long track record of active ownership on ESG issues: Columbia Threadneedle Investments UK International Limited (formerly traded as BMO Global Asset Management EMEA). Columbia Threadneedle provided us with data on their 2007–2020 global ESG engagements that are part of their responsible engagement overlay (reo®) service. They had previously collaborated with Dimson, Karakaş, and Li (Citation2015) in a similar way. With the reo service, the asset manager engages on behalf of a global client base of external investors and itself. We add new insights on ESG engagement topics, characteristics of successful engagements, and the subsequent ESG and financial performance of targeted firms.

Importantly, we are the first to make a distinction between financially material and immaterial private engagements by mapping each engagement in our sample to industry-specific material ESG topics from the Sustainability Accounting Standards Boards (SASB) and MSCI ESG research. We argue that the materiality of ESG engagement topics can be informative about engagement outcomes for a number of reasons. First, although a wide range of issues may shape firms’ ESG policies and practices, studies increasingly find that a subset of (industry-specific) ESG issues is financially material to the firm and its investors (Khan, Serafeim, and Yoon Citation2016; Khan Citation2019; Serafeim and Yoon Citation2022; Matsumura, Prakash, and Vera-Munõz Citation2022). Consequently, we expect that an engagement on financially material ESG issues has different return implications than an immaterial engagement. Second, we learn from studies on shareholder proposals in the United States; these proposals are a form of public engagement, but fewer than half of those filed address financially material ESG topics (Grewal, Serafeim, and Yoon Citation2016; Schopohl Citation2017; Bauer, Derwall, and Tissen Citation2022a). Because private engagement constitutes a more common form of active ownership than filing shareholder proposals, we study how prevalent material private ESG engagements are in our dataset.

A priori, we expect private engagements to address financially material and immaterial issues. On the one hand, many institutional investors seek to maximize risk-adjusted returns, implying an emphasis on the ESG issues that can materially affect the firm’s bottom line. On the other hand, there is growing evidence that institutional investors and their clientele have prosocial preferences for sustainability beyond a financial orientation (Riedl and Smeets Citation2017; Bauer, Ruof, and Smeets Citation2021) that could motivate engagement on ESG topics that are not necessarily financially material.

Based on our comprehensive dataset containing 7,415 engagements with more than 12,000 activities (i.e., contacts between the asset manager and firms), we first study the topics and the frequency of engagements on material ESG issues over time. We find that engagements on environmental and social issues have become more prevalent and have reacted to important market developments. For example, we observe a spike in environmental engagements after countries had adopted the Paris Climate Agreement in 2015 and an increase in social engagements as a response to concerns about labor conditions during the COVID outbreak. Turning to the materiality of engagements, we find that between 75% and 87% of the engagements in our sample address financially material ESG issues according to the SASB and MSCI frameworks, respectively. Governance engagements are most likely to be material, while the materiality of social engagements is lower. For example, based on the MSCI framework, which deems governance material to all sectors, the average materiality rates of E, S, and G engagements are respectively 83%, 71%, and 100%.

Next, we examine whether materiality matters for achieving engagement milestones (i.e., successes) reported by the active owner in our study. We find that 19.9% of engagements connect to a milestone and that material engagements are between 2.3 (MSCI) and 6.4 (SASB) percentage points (pp) more likely to succeed than immaterial engagements. These findings indicate that for active owners, it is easier to convince firms to improve their material ESG disclosures and practices, presumably because they can recognize during the engagement that a topic is financially relevant. Beyond materiality, engagements are more likely to be successful when they are intense (e.g., meetings rather than emails) and when collaborating with other investors.

Another important question is how firms that experience ESG engagements perform subsequently. We first analyze the stock returns of targeted firms after an engagement relative to their peer group in the same MSCI industry, country, and within-industry size quartile. We find that firms that experience successful material engagements significantly outperform peers by 2.5% over the following 14 months (i.e., the median time it takes to reach success). However, when distinguishing between engagement topics, outperformance is only statistically significant for successful material governance engagements. In contrast, firms experiencing material engagements without a recorded milestone outperform peers by 0.19% over the same period, but this outperformance is not statistically significant.

Next, we test whether materiality matters for post-engagement changes in firms’ underlying fundamentals. We find that material engagements are more often significantly associated with profitability and cost ratios than immaterial engagements. Material governance engagements show significant associations with future performance in terms of higher profitability and lower expense ratios. A potential reason for this finding is that improved governance could decrease overinvestment and, therefore, decrease expenses. Compared to governance engagements, post-targeting changes in fundamentals are less pronounced for environmental and social engagements. However, environmental engagements positively relate to capital and R&D expenditures when they are material, which suggests that firms might spend more on innovation to decrease their environmental footprint.

Finally, we study the ESG performance of firms that experience engagements on ESG issues. We find improvements in the MSCI ESG score and the environmental score of target firms. Successful engagements are associated with a 3.8% (3.4%) increase in the target firm’s MSCI ESG (environmental) score in the years after being targeted relative to peers. Furthermore, environmental engagements are associated with a 12.4% decrease in CO2e emission intensity (emissions divided by sales) after engagement. This effect is stronger when the engagement specifically addresses corporate emissions (−24.6%). However, unlike emission intensity, the total level of CO2e emissions does not significantly change during the post-engagement period we study, which could mean that it takes more time for such reductions to be accomplished.

The main takeaway of this paper is that material ESG engagements are associated with improvements in accounting and in stock market performance and are more likely to reach a milestone than immaterial engagements. These results add new insights to the relevant literature on active ownership for investment practitioners. Focusing on the engagement records of specific asset managers, a few studies have analyzed earlier data on the characteristics of engagement targets, determinants of engagements recorded as successful, and the actual post-engagement performance of targeted firms (Dimson, Karakaş, and Li Citation2015; Barko, Cremers, and Luc Renneboog Citation2022). Overall, the empirical evidence so far shows that targeted firms on average experience modest improvements in ESG performance, accounting performance, and stock returns. Improvements might be larger for engagements that investors successfully complete (Barko, Cremers, and Luc Renneboog Citation2022), for targeted firms with weak ESG profiles (Barko, Cremers, and Luc Renneboog Citation2022), and when coordinated with other institutional investors (Dimson, Karakaş, and Li Citation2021). Further, firms may have a lower downside risk after ESG engagement (Hoepner et al. Citation2022).

We add to the literature by using one of the most comprehensive datasets on private ESG engagements studied to date, performed by a large asset manager on behalf of a global base of external investors and itself. We provide a detailed framework for mapping such engagements to the SASB and MSCI materiality standards, which allows for distinguishing between financially material and immaterial engagements. Moreover, we use a stringent empirical design to examine the effects of engagement on the financial and non-financial performance of target firms and contribute to previous work by examining not just changes in ESG scores but also changes in carbon emissions.

For practitioners, our results show that investors who pursue both financial and ESG goals benefit from making the financial materiality of ESG issues more salient when selecting targets and prioritizing these in dialogues with them. We acknowledge that our paper provides an in-depth analysis of a single active owner, and we remain cautious about inferring causal effects from our sample of ESG engagements. Future research can shed more light on the external validity of our results by studying additional active owners.

Determining the Materiality of ESG Engagements

Not all ESG issues are financially relevant to each firm. For example, water management is important to a beverage company but might not affect the financial performance of a car manufacturer. The literature outside the field of shareholder engagement indicates that material ESG issues can affect performance and returns more than immaterial ESG issues. For example, firms with good ratings on financially material issues outperform firms with poor ratings, while firms that score well on financially immaterial issues do not (Khan, Serafeim, and Yoon Citation2016; Khan Citation2019).

However, studies on ESG-related shareholder proposals in the United States indicate that fewer than half of such proposals address topics that are financially material according to SASB’s Materiality Map™ (Grewal, Serafeim, and Yoon Citation2016; Schopohl Citation2017; Bauer, Derwall, and Tissen Citation2022b). This finding is consistent with a growing body of empirical evidence that investors make investment choices that are partially rooted in social or environmental preferences. For example, Riedl and Smeets (Citation2017) report that investors are willing to forgo financial benefits from holding a socially responsible mutual fund in order to align investments with their social preferences. In the context of shareholder engagement, Bauer, Ruof, and Smeets (Citation2021) report that 68% of a pension fund’s shareholders are willing to expand their engagement on the sustainable development goals, even when they expect lower financial returns from these engagements.

The findings of these previous studies imply that private engagements may not exclusively address financially material topics because of social and environmental preferences. However, it is not the case that financially material engagements are always driven by financial motivation. Social preferences can underlie financially material and immaterial engagements if the addressed issue is relevant to a firm’s social and environmental policies. Oppositely, an investor might engage on a financially immaterial issue for financial reasons when the investor either does not know that the issue is not financially material or has different beliefs on which issues are financially material than existing materiality frameworks.

The question remains as to what extent private ESG engagements are material and whether material engagements have stronger effects on the performance of targeted firms than immaterial engagements. Determining the materiality of an engagement is an essential first step in answering this question. We use the materiality frameworks developed by the SASB and MSCI to identify material ESG topics by industry.

Materiality Frameworks

The SASB is an independent organization that establishes 77 industry-specific standards to guide the disclosures of financially material sustainability information of firms to their investors. They argue that information about how firms manage material ESG factors helps investors understand near-term costs and the probability that the effective management of these factors will pay off in the long term. These long-term improvements can result from improved efficiency, reduced operating expenses, enhanced reputation, greater risk resilience, and an improved competitive advantage (SASB Citation2020b).

The SASB engages in ongoing evidence-based research and consultation with market participants and industry experts to develop its disclosure standards. The results of this process are summarized in the SASB Standards© (2021 Value Reporting Foundation. All Rights Reserved.). These standards address the sustainability information that is reasonably likely to affect a firm’s financial performance in a specific industry, and they cover 26 general issue categories in 5 dimensions: environment, social capital, human capital, business model and innovation, and leadership and governance. The core focus of the SASB is to identify financially material topics through consulting with capital market participants and evidence of financial impact; this process is for us an important reason to map engagement topics with the SASB topics.

In addition, several empirical studies have validated the view that the SASB identifies financially material issues. For example, Serafeim and Yoon (Citation2022) study how the stock market reacts to material and immaterial news about ESG issues at firms by using scores conditioned on the SASB’s material topics by industry. They find that positive ESG news triggers positive reactions from the stock market only if it addresses financially material issues, according to the SASB standards. In contrast, they find no price reaction to immaterial ESG news. Further, Matsumura, Prakash, and Vera-Munõz (Citation2022) find that S&P 500 firms experience a lower cost of equity when they disclose climate risk in 10K forms and more so when that risk is financially material according to the SASB given the industry in which the firm operates. Thus, empirical evidence supports the idea that the SASB provides a valuable framework for identifying material topics.

In addition to the SASB, we use the ESG Industry Materiality Map that MSCI ESG Research developed as a foundation for their firm-level ESG ratings. MSCI’s ESG ratings measure firms’ resilience to long-term financially material ESG risks and is one of the most influential ESG ratings (Berg, Kölbel, and Rigobon Citation2022). Like the SASB, MSCI identifies key material issues per industry by examining which risks can lead to substantial costs and which opportunities firms in an industry could benefit from. They identify these issues using a quantitative model that captures externalized effects, such as carbon intensity, water intensity, and injury rates (MSCI Citation2023).

MSCI ESG Research and the SASB conceptually share a focus on financially material ESG issues, and the ESG Industry Materiality Map helps us understand MSCI’s view on key material ESG topics by industry. Therefore, we augment the mapping of all engagement topics against the SASB’s topics with an additional mapping to topics covered under MSCI’s ESG Industry Materiality Map. By doing so, we expect to obtain the most accurate assessment of the financial materiality of the ESG engagements that we study.

For our research, MSCI’s framework for identifying material topics by industry offers an additional benefit because it underpins their firm-level ESG ratings and sub-ratings. Hence, when we study the relationship between engagements and firms’ subsequent ESG performance, we can study the effect on the specific MSCI ESG sub-rating that is relevant to the engagement.

Mapping Engagements to the Materiality Frameworks

The private engagement data come from Columbia Threadneedle Investments U.K. International Limited (hereafter, CTI) that was formerly traded as BMO Global Asset Management EMEA (BMO EMEA). The data cover from 2007 to 2020 and therefore end before CTI’s acquisition of BMO EMEA. Thus, it contains the engagements belonging to BMO EMEA and their reo service. This service provides its clients with corporate engagements and proxy voting services aligned with their preferences and has a global client base of external investors that represented €303bn in assets under engagement at the end of 2020.Footnote1

The data contain 25,122 activities between the asset manager and a firm and 4,080 milestones from 2007 to 2020. We know the company name, activity date, and a summary of the content for each activity. Moreover, the activity data comprise the topic category (e.g., climate change or human rights), the method used (e.g., phone call or letter), whether there were other investor participants, and the leadership level addressed. Successes at target firms, such as improved disclosures, targets, and policies, we marked as “milestones.” The milestone data comprise the company name, milestone date, milestone contents, and the milestone topic category.

We needed to make two adjustments to the dataset. First, the original data record the activities and milestones separately, and no identifier connects them. We connected activities to milestones ourselves based on our SASB and MSCI mapping process. Second, although the original data contain topic classifications, they were not sufficiently detailed to determine the materiality of activities. We studied the asset managers’ comprehensive activity summary for each activity and manually determined whether it corresponded to a material ESG topic, as identified by the SASB and MSCI.

We performed the following tasks to do so.Footnote2 First, we took an inventory of all ESG topics covered by the materiality framework of the SASB. Because it determines on an industry-by-industry basis which ESG topics are financially material, we could determine which subset of ESG topics was material for a specific firm once we had determined the key SASB industry to which the firm belonged. The SASB uses its own Sustainable Industry Classification System (SICS), and we obtained a SICS® classification from it for each of the firms in our sample.

Next, we manually analyzed the descriptions of all activities in our dataset to determine which of the SASB ESG topics best corresponded to the topic central to the activity. When the description of an activity did not contain sufficient detail, we removed it from our sample. Moreover, if participants discussed multiple topics in an activity, we created an entry for each unique topic.

Finally, we determined that an activity was financially material if the assigned ESG topic of the activity matched the set of ESG topics that the SASB deemed material for the SICS industry to which the firm belonged. This industry-specific mapping is important. For instance, based on the SASB standards, activities on animal welfare are classified as “product design and lifecycle management” for meat, poultry, and dairy producers and as “supply chain management” for food retailers and restaurants. We followed a similar approach to determine the materiality of the activity when using MSCI’s framework.

Still, MSCI differs from the SASB in several ways. One difference is that they cover somewhat different potentially material topics. They may also cover similar topics but label them differently. In addition, MSCI determines the materiality of their ESG topics by industry based on the Global Industry Classification Standard (GICS). Thus, we collected the GICS categorization for each firm in our dataset and matched each activity with one of the ESG topics covered by MSCI. If the assigned ESG topic of the activity matched one of the material topics that MSCI reported for the firm’s GICS industry, we deemed the activity to be material through the lens of MSCI.

Given that we use two materiality frameworks independently, it is conceivable that an activity topic is not always material according to both materiality frameworks. Moreover, the SASB and MSCI topics do not relate one-to-one. For example, when the asset manager engages a car manufacturer on carbon emissions, this activity is part of the “environment” category (product carbon footprint) for MSCI but is part of the “business model and innovation” category (product design and lifecycle management) for the SASB.Footnote3 In our cross-sectional tests of engagement success, we use one materiality indicator for the SASB and one for MSCI. However, when we move to panel data and examine the effects of engagements on target firms over time, we use only one materiality indicator. This indicator equals one when both materiality frameworks agree an engagement is material and zero if not.Footnote4

Based on the mapping process, we create sequences that comprise activities and milestones on the same SASB/MSCI topic targeting the same firm over time. The end of a sequence occurs when the asset manager reaches a milestone. For example, say that the asset manager sent a letter on workforce diversity to a target firm and followed it up with a meeting. Three months later, the target firm published a report on workforce diversity. These two activities (letter and meeting) and the milestone (disclosure) form a sequence. After this milestone, a new sequence starts if the investor targets the same firm with another workforce diversity issue. After the data processing and ensuring that the target firm is covered by MSCI ESG, we end up with 7,415 engagement sequences containing 12,727 activities and 1,476 milestones. Hereafter, we refer to such sequences as engagements.

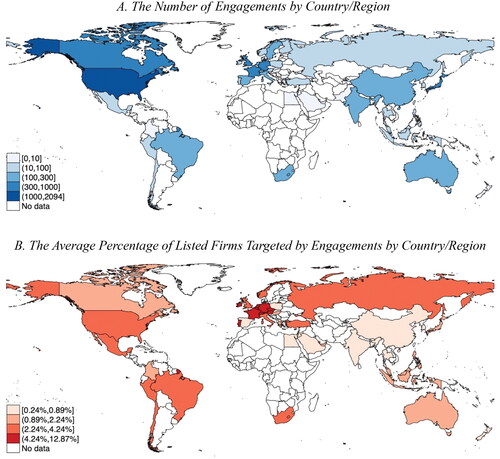

provides a geographic breakdown of engagements to give a first impression of the global nature of our data. Most of the engagements in our sample target European (38.36%), North American (34.40%), and Asian (19.83%) firms, while the remaining engagements cover Oceania, South America, and Africa. The continental breakdown we observe for our investor is similar to the global engagement orientations of two other institutional investors that Barko, Cremers, and Luc Renneboog (Citation2022) and Hoepner et al. (Citation2022) have studied. Clearly, some countries have more listed companies than others, which can affect the frequency of engagement in each country. We therefore also gather data on the number of listed companies by country/region from the World Bank and display the average percentage of listed companies by country/region in . We find that the intensity of engagement is highest in Western Europe.

The Materiality and Success of ESG Engagements

How often do these ESG engagements address material topics? Panel B of Appendix A shows that 74.77% of engagements are material if we evaluate them with the SASB framework. The SASB does not cover traditional governance topics (i.e., board independence, board size, and CEO–chairperson separation) because existing regulations require companies to report on them. Therefore, we deem them material for all industries. Beyond these topics, engagements on environmental issues (70.55%), business model and innovation (67.58%), and social capital (63.76%) are material most often. In contrast, engagements on leadership and governance (53.68%) and human capital (43.31%) are least likely to be material following the SASB standards. These categories, for example, include engagements on business ethics, labor practices, and employee engagement, diversity, and inclusion.

Similar to our findings using the SASB standards, social engagements are least likely to be material (70.53%) when using the MSCI framework (Appendix B). Moreover, environmental engagements are more often material (83.31%) and governance engagements are most often material (100%). MSCI deems the two themes under its governance pillar, corporate governance and corporate behavior, universally relevant and therefore material to all firms (MSCI Citation2023).

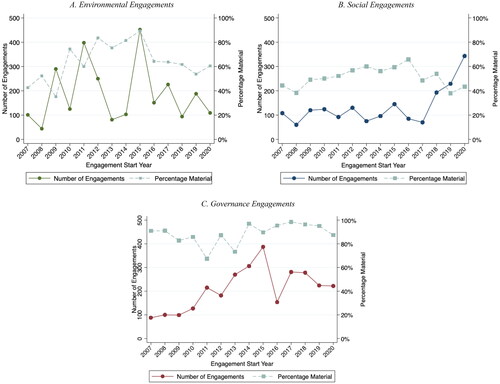

Next, we examine whether there has been a trend in materiality and the focus of engagements. In , we display the number of engagements and the percentage of material engagements by E, S, and G issues over time. There are two important details to consider when examining this figure. First, because the SASB and MSCI can differ in their materiality assessment, we deem an engagement material when it is material following both the SASB standards and the MSCI framework. Therefore, when there is disagreement on materiality between the SASB and MSCI for an engagement, we consider it immaterial. Second, the engagement year is determined by the start of an engagement sequence. Hence, whenever the number of engagements is low in a particular year, it does not naturally follow that the asset manager had less activity in that year because engagements that started in previous years can still be ongoing.

In Panel A, we do not observe a clear trend in the number of environmental engagements. However, there were two spikes in 2011 and 2015. In 2011, the asset manager joined a carbon disclosure project (CDP) campaign and sent letters to firms asking them to disclose their carbon emissions. Another campaign explains the spike in 2015. That campaign involved sending letters of support for the Paris Climate Agreement to firms in carbon-intensive industries. Interestingly, the materiality of environmental engagements increased from about 40% in 2007 to 90% in 2015, after which it decreased by about 20 pp. The high level of materiality in 2015 appears to come from this campaign. After 2015, the proportion of new engagements on carbon emissions went down because others are still ongoing, which explains the lower levels of average materiality of engagements initiated from 2016 onward.

We plot the number of social engagements and their materiality in Panel B. The number of social engagements substantially increased from about 100 new engagements per year between 2007 and 2017 to 200 new engagements between 2018 and 2019 and roughly 350 new engagements in 2020. This finding illustrates that the asset manager responded to the COVID-19 pandemic by engaging more on social issues, such as employee health and safety and labor management. The fact that materiality decreased from more than 60% in 2016 to about 40% in 2020 due to this focus on human capital engagement demonstrates that developing an ESG materiality framework is an ongoing process. Standards do not always reflect the most recent information. However, the SASB writes that they will take the lessons learned from the COVID-19 pandemic into account in their ongoing work related to human capital standards (SASB Citation2020a).

Last, we find that the number of governance engagements increased in the early parts of the sample and peaked in 2015. Several letter campaigns, such as those about voting rights and lobbying behavior, caused this peak. Due to a focus on traditional governance issues, the percentage of material governance engagements hovered between 80% and 100% except for the years 2011 and 2013. Appendix A shows that this dip in materiality was caused by relatively more engagements on business ethics in those two years.

Our findings illustrate that investors’ and firms’ understanding of ESG issues continuously develops. As government policies (e.g., the Paris Climate Agreement) and global predicaments (e.g., the COVID-19 pandemic) evolve, investors, firms, and standards must adapt. We find that the asset manager reacted to such changes by shifting the focus of ESG engagements over time as new issues became relevant.

Materiality as a Driver of Engagement Success

In this subsection, we ask whether engaging on material topics matters for the success rate. To answer that question, we use engagement milestones that the institutional investor in our study reports. In , we report the percentage of successful engagements by topic and by SASB/MSCI materiality. On average, the engagements in our sample are successful in about 20% of all cases, which is similar to the average ESG engagement success rates reported in Dimson, Karakaş, and Li (Citation2015) and Hoepner et al. (Citation2022).

Do the topics and materiality of ESG engagements determine their success? We find that material engagements are, on average, 6.39 pp more likely to succeed than immaterial engagements when we use the SASB framework to classify engagements by materiality (success rates of 21.52 vs. 15.13%) and 2.34 pp more likely when we use the MSCI framework (19.77 vs. 17.43%). Both differences are statistically significant at the 1% level. An explanation for this finding is that it is easier to convince a firm to disclose information or improve its policies whenever they deem that the issue is financially relevant to its business. Moreover, it is likely that a larger percentage of a firm’s ownership will agree with the need for engagement when a topic is material, which increases the likelihood of success.

Next, we examine whether materiality plays a larger role in success depending on the topic of an engagement. Environmental engagements as a whole have an average success rate of 21.86% that is just above the total sample average. We also see that materiality matters for the success rates of environmental engagements: Material environmental engagements are 5.15 pp more likely (SASB) and 3.77 pp less likely (MSCI) to succeed than immaterial engagements. Although it is surprising that the SASB and MSCI mappings show opposite effects of materiality on the success of environmental engagements, the negative effect of materiality on success derived from MSCI’s framework is not statistically significant.

For social engagements, materiality also matters. We find a positive effect of materiality on the success of social engagements between 3.71 and 5.93 pp. However, social engagements are less likely to succeed than environmental or governance engagements. We argue that there are two reasons. First, there was a significant increase in social engagements during the last three years of the sample. Therefore, those engagements could still have been ongoing at the end of our sample and could have had a milestone after 2020. Second, the business case for social issues is less explored than environmental and governance issues. Therefore, investors might have more heterogeneous views on the importance of social issues. This heterogeneity potentially plays a role in the decision-making of firms being targeted for social issues, which decreases the likelihood of engagement success.

As for the success rates of governance engagements, we first distinguish between traditional governance issues and issues in the SASB’s leadership and governance (L&G) category, such as business ethics. We find that material L&G engagements are 4.92 pp more likely to succeed than immaterial engagements in that category (20.28 vs. 15.36%). Traditional governance engagements are all treated as material in this paper and, on average, are successful in about 21% of all cases. Some of the traditional governance engagements fall under L&G using the SASB standards, and keeping the remaining ones in traditional governance leads to an elevated average success rate of 23.32% for this category.

Overall, there is a consistently positive effect of materiality on the success of private ESG engagements when using the SASB’s framework that ranges from 3.7 to 5.2 pp. However, when using MSCI’s framework, materiality only has a significantly positive effect on the success of social engagements. These results highlight that the SASB and MSCI can differ in their materiality assessments.

Other Drivers of Engagement Success

We have so far explored the success rates by the materiality of the topic, which is the focus of our paper. Because the empirical literature on private engagements is scarce, it is interesting to devote attention to some other potential success factors. Looking at Panel A of , we observe that the success rate decreased over time. While rates in later years are partially lower because some engagements might still be ongoing, another reason is that engagements are increasingly focused on social issues that appear to have a relatively lower likelihood of success.

We can see from Panel B that the target firm’s industry matters for engagement success. Engagements targeting the “extractives and minerals” and “health care” industries are most likely to lead to success, while firms in the “transportation” and “resource transformation” industries are the least responsive. Although, surprisingly, engagements targeting “extractives and minerals” firms succeed more often, the successes often concern disclosure or target setting, which does not necessarily mean a change in ESG performance. We examine whether such a change occurs in subsection “ESG Scores.”

Engagement characteristics are also a relevant determinant of success. In Panel C, we show that engagements with only one activity are unlikely to succeed (1.45%), while the success rate of engagements comprising multiple activities is much higher (44.16%). In addition, the intensity of engagement methods matters for success. We give conferences and seminars an intensity score of 1, emails and letters a score of 2, and meetings and calls with the target company a score of 3. To determine the method’s intensity, we take the average of the intensity scores of all activities in an engagement. We find that engagements with below-median or median intensity (i.e., 2 or lower) are 15.65 percentage points less likely to reach a milestone than engagements with above-median intensity (i.e., higher than 2).

There is another form of intensity, the number of investors, that can matter for success. The asset manager has an average success rate of 14.08% when engaging alone but a success rate of 22.13% when collaborating with other investors or stakeholders.Footnote5 This finding supports earlier work on collaborative engagement (Dimson, Karakaş, and Li Citation2015; Dimson, Karakaş, and Li Citation2021) and reinforces a general industry trend of collaboration.

Another interesting and potentially important success driver is the percentage of ownership of the asset manager and its reo clients in the target firm. The underlying reasoning is that an active owner backed by larger ownership might be able to exert a greater influence on target firms and has larger incentives to engage. However, based on empirical studies to date, it is not evident that this ownership affects the probability of success (Dimson, Karakaş, and Li Citation2015). We obtained a list from the asset manager that details its reo clients by year. Based on ownership data from Factset, we calculated “client ownership” for each firm year using this list. We added the asset manager’s ownership of the target firm to this measure because they also engage on their own assets. On average, client ownership is 0.35%.

In , we report the engagement success and characteristics by quartile of client ownership. We find that there is a positive relationship between client ownership and success. For example, the average success rate for the first quartile of client ownership (i.e., <0.03%) is 13.44%, while the success rate for the fourth quartile (i.e., >1.69%) is 25.07%. However, this difference in success rates can potentially be explained by changes in engagement focus and tactics based on ownership of the target firm.

We observe that the asset manager focuses on different topics that are dependent on ownership. In Panel A, we show that environmental engagements occur more often when ownership is small. Moreover, in Panel B, we observe that engagements are shorter when ownership is small. Based on these two findings, we conclude that the asset manager is more likely to send letters to smaller holdings and that the increased focus on environmental topics for such holdings is driven by the letter campaigns around the CDP and the Paris Climate Agreement.

In Panel C, we observe increased engagement intensity when client ownership is larger. For example, 31.39% of engagements contain multiple activities, and 20.72% of engagements have an above-median method intensity when client ownership is small (Q1). However, these percentages increase to 47.04% and 38.77% when client ownership is large (Q4). Since we previously discussed that intense engagements with multiple activities are most likely to succeed, the positive effect of ownership on success is most likely driven by changes in engagement characteristics rather than increased control over the target firm.

Using a logistic regression, we formally test the effects of materiality, engagement characteristics, and client ownership on success. The dependent variable is Success that equals 1 for engagements that ended with a milestone and 0 for engagements that did not (yet) lead to a milestone. We use materiality and engagement characteristics as the independent variables. Moreover, we obtain data on firm characteristics and monthly stock returns from Factset and ESG scores from MSCI as control variables. In addition, we add year, industry, and country fixed effects to our model.

In , we report the results of the logistic regression. Our results confirm that material engagements are more likely to succeed, provided that an engagement emerges as material under both the SASB’s and MSCI’s materiality frameworks. However, whenever there is a disagreement between the SASB and MSCI, we do not observe a positive effect of materiality on success. For example, at the bottom of , we report the average marginal effects based on the materiality indicators. For the set of immaterial engagements following the MSCI framework (i.e., MaterialMSCI = 0), we do not find that material engagements following the SASB standards are more likely to succeed than immaterial engagements (i.e., the AME of MaterialSASB is −0.021 and insignificant).

The logistic regressions also confirm that engagements with multiple activities and above-median method intensity are more likely to succeed. After controlling for whether an engagement contains one or more activities by using the “Multiple Activities” indicator, the likelihood of success decreases as the number of activities in an engagement increases. This result can partially be explained by our data setup in which we mark a milestone as the end of an engagement. We record several shorter engagements whenever the asset manager reaches several milestones on the same topic. However, when they do not reach a milestone, the engagement does not end, and we record the time between the first and last activity on that topic.

Last, we do not find an effect of client ownership on the probability of success, all else being equal. Therefore, the positive effect of ownership on success in is because the asset manager has more intense engagements with firms in which they represent a larger shareholding. The mere percentage of ownership in the target firm, irrespective of engagement characteristics, does not play a role.

We can conclude that investors who aim to maximize their success rate should be materiality salient when engaging with the target firm. The success rate increases further when there are multiple and intense activities, such as calls or meetings. Even though these activities increase the cost of engagement, collaboration allows investors to share costs and also increases the probability of reaching success. In Online Appendix 1, we provide formal support for the idea that collaboration with other investors increases the probability of success.Footnote6

What Is the Effect of Engagements on Target Firms?

A key goal of shareholder engagement on ESG issues is to achieve change or to have an “impact” on the target firm in terms of its ESG policies, practices, and performance. Depending on the scope of the active owner and the nature of the ESG topic, the engagement may also have the aim of ultimately improving the target firm’s financial returns. The successes of private engagements that we have discussed up to this point were based on milestones that our institutional investor reported whenever the target firm acted to the investors’ satisfaction. They leave unanswered how significantly and in what ways firms change their ESG behavior, fundamentals, and performance after engagement. In this section, therefore, we ask: How do firms perform after being targeted?

Our goal in this section is twofold. First, because we address engagements on topics deemed material to investors, we are particularly interested in firms’ financial performance measures after an engagement. We study stock market performance and test whether target firms outperform peer firms in the months following engagement. Moreover, we examine whether engagements are related to changes in accounting ratios in the years after being targeted. Our next objective is to examine whether ESG engagements can improve the ESG scores of target firms along with their CO2e emissions relative to peers. Because ESG scores are based not just on performance but also on policies and targets, examining them is an added validation of our earlier examination of milestones. Moreover, we study post-engagement changes in carbon emissions to determine the real effects of engagements on target firms. We obtain the data on firm characteristics and monthly stock returns from Factset, ESG scores from MSCI, and carbon emission data from Refinitiv.

Before we can perform our tests, we need to find a comparable set of peer firms because firms in different industries and countries are exposed to different ESG issues and regulations. Therefore, we match every target firm to a set of non-targeted peer firms in the same MSCI subindustry and country. Moreover, since size greatly influences performance, we ensure that peer firms are in the same quartile of the within-industry market size the year before the engagement. If we cannot find such peers, then we match on the less granular MSCI sector instead of the subindustry, which occurs for about 25% of the target firms.Footnote7 Further, in case there are more than 10 peer firms for a target firm, we keep those with the closest market size to the target firm.

In all tests, we average the characteristics of peer firms by year to create a pseudo-firm. Subsequently, each time we compare target firms to peer firms, “peer firm” refers to this pseudo-firm. We report the average differences between target firms and peer firms in the year before the engagement in Online Appendix 2.Footnote8 When looking at accounting measures, it becomes clear that target firms are larger than peer firms within their quartile for industry market size.Footnote9 However, we do not find a consistent pattern of over or underperformance compared to peers in the performance and valuation metrics.

Because we map all engagements to MSCI topics, we can directly link each engagement to one of the scores for 30 key issues (see Appendix B). We find that target firms do not have a higher or lower MSCIKI score than peer firms. Although this result seems surprising, firms with higher ESG scores are potentially more receptive to engagements that, in turn, increase the probability of successful engagements that can lead to spillover effects within the industry. Therefore, the asset manager occasionally engages with industry leaders instead of laggards. Besides considering ESG scores, we also evaluate the level of corporate CO2e emissions and their intensity (emissions-to-sales). We find that target firms emit 31.3% more tonnes of CO2e and have a 29.4% higher CO2e intensity than peer firms in the year before engagement.

Stock Market Performance

In this subsection, we test whether target firms outperform peer firms in the months after an engagement. Following Dimson, Karakaş, and Li (Citation2015) and Barko, Cremers, and Luc Renneboog (Citation2022), we use monthly returns because most engagements are not publicly known and, therefore, will take time to be reflected in stock prices. We deduct the average return of a peer firm from the average return of the target firm for each month that then equals the monthly abnormal return.

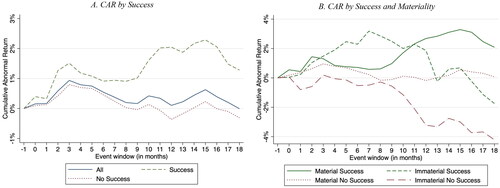

In , we accumulate these abnormal returns from the month before engagement to 18 months after. Panel A shows that the engagements ending with success are associated with positive cumulative abnormal returns (CARs) in the months after the engagement. For example, 14 months after the start of a successful engagement, which is the median time it takes to reach a milestone, the CAR equals 2.17%. Next, we distinguish between material and immaterial engagements. Panel B shows that materiality matters for CARs following engagement. For example, after a successful material engagement, the average firm experiences a CAR of 3.10% over a 14-month window. In contrast, successful immaterial engagements are associated with a 0.60% CAR.

To study the statistical significance of these CARs, we calculate the average CAR of all target firms in the periods [0], [0,6], and [0,14] and test whether they are significantly different from zero. We use the 14-month interval because this is the median time between the first activity and the milestone of successful engagements.Footnote10 We report our results in and separate the CARs by the success and materiality of each engagement. In addition, we show the differences in CARs between successful/unsuccessful and material/immaterial engagements and whether these differences are statistically significant.

In the first three columns of , we report on all engagements (column 1) and those that are successful/unsuccessful (columns 2 and 3). The average CAR across all ESG engagements is positive for all event windows (respectively, 0.10%, 0.44%, and 0.34%) but statistically not significant. However, columns 2 and 3 indicate that the average CAR across ESG engagements depends on whether the engagements were successful or not. The CAR of successful ESG engagements is positive for periods [0] and [0,6], and it becomes significantly positive (1.87%) over the 14-month period after the first activity. However, the CAR for period [0,14] is not significant at the 5% level (p = 0.054).

In columns 4 through 9 of , we shed light on whether materiality matters for the average CAR across ESG engagements. Several important observations emerge from this table. First, we find that over the 14-month window, the average return following immaterial engagements is negative (−2.16%, column 5) and below that following material ESG engagements (0.70%, column 4). This negative return is primarily driven by significantly negative returns on immaterial engagements that are successful (−2.79%, column 9). Second, column 6 shows that successful material engagements are associated with a positive and significant CAR of 2.54% over the 14 months after the engagement. Hence, to the extent that engagements are successfully completed, engaging on material ESG issues is associated with positive CARs.

In , we also divide ESG engagements into E, S, and G categories. On the environmental front (E), we find that target firms significantly outperform their peers six months after an engagement by 1.69% (column 1), but the significance disappears over the 14-month window. Of the E engagements, mainly material engagements are associated with this positive six-month outperformance (1.74%, column 4). Given that most E engagements have not (yet) been successfully completed, one could infer that the positive six-month performance following E engagements does not require the engagement to be successfully completed. Columns 3 (no successful completion) and 8 (material, no successful completion) indeed show positive six-month abnormal returns for E engagements. On the social front, we do not find significant CARs for any event window. Last, for governance (G) issues, we find substantial outperformance by target firms following G engagements. For example, successful G engagements are associated with a significant CAR of 3.02% in the window [0,14]. Notably, the CAR is only statistically positive for successful material governance engagements when distinguished by materiality.

To conclude, we find that target firms significantly outperform their peers after material ESG engagements. In untabulated findings, which are available on request, we find that the results in this subsection are similar when we use buy-and-hold returns instead of cumulative returns.

Accounting Performance

To examine whether there are other effects on financial performance besides stock market performance, we use a difference-in-differences model to examine whether material engagements are associated with changes in accounting performance. In brief, we compare the pre-targeting performance of a targeted firm (often dubbed the “treated” firm in a difference-in-differences model) with the performance observed post-targeting. Because target firms’ performance over time may change due to characteristics that are unrelated to the engagements they experience, the pre- and post-engagement performances of targeted firms are evaluated relative to the performance of non-targeted peers (i.e., the control group). These peers share key characteristics with the target firms in the year before targeting.

However, two complications arise when analyzing performance after engagement. First, firms can be targeted multiple times within our sample period that makes it difficult to connect changes in performance to specific engagements. We, therefore, only examine each firm’s first engagement with multiple activities to account for this difficulty. We do not count engagements with only one activity as a firm’s first engagement because they are very unlikely to be successful (1.45 vs. 44.16%, Panel C of ). Moreover, we take the first E, S, or G engagement with multiple activities when examining ESG engagements by topic. This approach ensures that target firms have never been treated by an intensive engagement in the pre-target period. Second, the treatment (being targeted) can happen at any time within the sample period. Hence, there is no fixed treatment date, unlike a classic difference-in-differences setup. Instead, we use our sample of peer firms to solve this timing issue by examining what happens to the accounting performance of peers after a firm is targeted. Thus, each target–peer pair has the same pre-target and after-target periods. This method results in the following empirical specification:

(1)

(1)

where Performanceijt is the accounting performance measure i for firm j in year t. Specifically, we study ROE (net income/total shareholder equity), ROIC (net income/total invested capital), opex/assets, log(sales), capex/sales, and R&D/sales. When a firm changes after an engagement, this change could lead to higher costs following new investments. In contrast, improved governance could lead to cost-cutting. We capture the effect of engagements on costs and investments by examining operational, capital, and research and development expenses. Moreover, improvements in ESG performance could lead to an improved reputation and a subsequent increase in sales. Subsequently, these two effects influence the firm’s profitability; we capture them with the ROE and ROIC. Afterjt is an indicator equal to one after the target year and zero before or in the target year. For peer firms, we use the target year of the paired target firm. Moreover, Targetj is an indicator equal to 1 for target firms and 0 for peer firms. Last, Materialj is an indicator equal to 1 for firms targeted by a material engagement following both the SASB standards and MSCI framework, and 0 if not. Hence, Targetj × Afterjt captures the treatment effect, and Materialj × Targetj × Afterjt captures the additional effect of materiality on the treatment.

To account for changes in firm characteristics over time, we add a set of lagged control variables (Xij,t−1): MSCI ESG score, log(size), Tobin’s Q, sales growth, ROE, leverage, dividends per share, capex/sales, client ownership, institutional ownership, inside ownership, and an institutional blockholder indicator. Further, we add firm and time fixed effects (ΛF,T) and only keep the five years before and after an engagement in the panel. Hence, we examine the within-firm changes in accounting performance up to five years after an engagement.

Based on related literature reviewed earlier, we could expect that firms exhibit improved fundamentals after an engagement on material issues but not after immaterial issues. Because research is still undecided on the channels through which ESG issues can affect fundamentals of firm in specific industries, we explore several measures of profitability, costs, sales, and expenditures that are common in related studies on active ownership.

We report the results in .Footnote11 For ease of interpretation, we report only the estimated marginal effects of being treated separately by the materiality indicator. When all ESG engagements are analyzed together, the estimated targeting effects lack statistical significance regardless of the dependent variable and whether engagements are material or not. There is some decline in operating expenses relative to assets (−2.24%, p = 0.063) and in R&D expense over sales (−11.99%, p = 0.076) after material ESG engagements, but the estimates are not significant at the 5% level.

Because we expect that changes in performance after targeting may vary by engagement topic, we also report in on the effects of targeting based on the subsamples of governance, social, and environmental engagements. We find that material G engagements are followed by significantly higher profitability ratios (14.58% and 10.55% higher ROE and ROIC, respectively) and lower operating expenses (4.22% lower opex/assets). In addition, material and immaterial G engagements are associated with lower R&D expenses over sales after targeting. An explanation for these results based on agency theory is that improved governance could decrease overinvestment and therefore decrease expenses.

Along the social spectrum, we find modest evidence that the materiality of the topic raised at the target matters to post-engagement performance. Engagements on material S issues are associated with a lower R&D/sales (−22.77%) after targeting.Footnote12 A reason could be that firms experience increased labor costs after material S engagements and compensate for this by investing less in R&D. We find that targets of material S engagements increase their opex/assets by 2.70% after engagement, but this effect is not statistically significant.

Looking at environmental engagements, we find that targets experience more capital spending (+14.29%) and higher R&D expenses relative to sales (+13.88%) after they have been targeted for a material environmental issue. Although profitability ratios do not significantly improve following material environmental engagements, finding higher CAPEX/sales and higher R&D/sales in comparison to peers could mean that firms targeted for environmental engagements invest more in innovations that decrease the environmental footprint of their operations.

Overall, these results indicate that material governance engagements and to some extent material environmental and social engagement are associated with changes in certain fundamentals of targeted firms. Furthermore, except for a decrease in R&D expenses after governance engagements, immaterial engagements do not exhibit significant post-targeting effects on any of the accounting variables we study.

ESG Performance

Our final empirical analysis examines whether engagements are associated with changes in a firm’s ESG performance. We use the same difference-in-differences model as in the previous section but replace the dependent variables with measures of ESG performance. These measures are the MSCI ESG score and key issue (sub)scores, the level of CO2e emissions, and CO2e emission intensity.

ESG Scores

Before we discuss the results of the difference-in-differences model, we examine the average ESG scores of target and peer firms over time. In Online Appendix 4, we define the target year as year t and plot average ESG scores from the five years before the engagement to five years after the engagement. The results indicate that the trends in ESG scores in the five years before the engagement are reasonably similar between target and peer firms. Moreover, we see an increase in the average MSCI ESG and MSCI environmental scores after the engagement that indicates positive targeting effects.

We empirically confirm these targeting effects in using EquationEquation (2)(2)

(2) :

(2)

(2)

After an engagement, we find a significant within-firm increase of 0.188 in the MSCI ESG score (column 1). Given the average score of 4.994 in the period before engagement, that increase corresponds to a 3.76% increase relative to peers. Similarly, for environmental engagements, we find a significant 3.44% increase (column 4). We also find a positive effect on the category-specific environmental score (column 8), but it is not statistically significant (p = 0.096). Furthermore, we do not find significant effects of engagements on the governance and social scores.

Although the estimated targeting effects on ESG scores seem small, our results are conservative. We use firm fixed effects, and the MSCI ESG scores have limited within-firm variation.Footnote13 Moreover, we do not estimate an aggregate engagement effect because we only examine the first intensive E, S, and G engagements with each target firm. Therefore, our results could be interpreted as lower bound estimates of the effects of engagements on the ESG performance of target firms.

Moreover, because studies have found that ESG ratings diverge (e.g., Gibson Brandon, Krueger, and Schmidt Citation2021; Berg, Kölbel, and Rigobon Citation2022), we check the robustness of our results by examining Refinitiv ESG as an alternative source of firm-level ESG data. In Online Appendix 5, we show that there are significant and positive improvements after engagement in the Refinitiv ESG, governance, and environmental (ENV) scores. Moreover, the magnitude of these effects is similar to the effect on MSCI’s ESG scores. For example, the Refinitiv ENV score improves by 2.71% in the years after engagement relative to peers.

Corporate Emissions

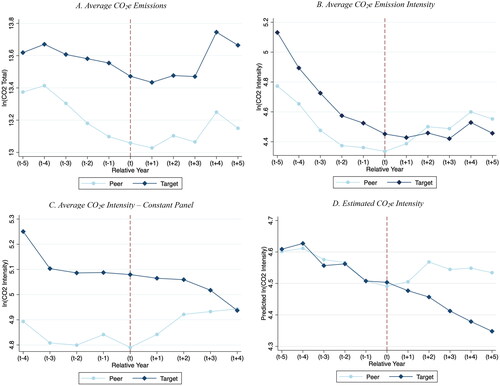

After finding that environmental engagements are associated with improvements in the MSCI and Refinitiv environmental scores, we examine whether we also find an effect on scope 1 and scope 2 corporate emissions. We plot the average level of CO2e emissions and their intensity (i.e., CO2e emissions divided by last year’s sales) over time in . In Panels A and B, we see that target and peer firms have similar decreasing trends in the years before engagement. This decreasing trend might seem surprising but can be explained by the increase in Refinitiv’s availability of emission data. In earlier years of our sample, Refinitiv mainly covered large firms, while emission data on smaller firms was added over time.

To illustrate, we plot the average CO2e intensity for a strongly balanced panel of firms for the four years before and after engagement in Panel C.Footnote14 We observe that the strong negative trend in emission intensity disappears when coverage is constant. Moreover, when we plot the estimation results of the difference-in-differences model in which we control for time-varying firm characteristics and time trends (Panel D), we see similar emission intensities for target and peer firms before engagement. However, after an engagement, the emission intensity of target firms decreases relative to peer firms.

In , we show the regression results for our emission measures. Columns 1 to 3 indicate that environmental engagements are not significantly associated with a change in total scope 1 or scope 2 CO2e emissions. However, we find a significant 0.12 decrease in the log of the CO2e intensity of target firms (column 4) that corresponds to a 12.41% reduction. Moreover, we divide scope 1 and scope 2 intensities into columns 5 and 6 and find that the effect shown in column 4 is mainly driven by a lower scope 1 emission intensity.Footnote15 Hence, environmental engagements are associated with a decrease in the intensity of scope 1 emissions (column 5, p = 0.057) rather than a firm’s scope 2 emissions (column 6, p = 0.657).

Our detailed engagement classification allows us to look at environmental engagements that specifically address corporate emissions. In , we show the results of regressions in which we only include engagements that we mapped to the MSCI categories “carbon emissions,” “product carbon footprint,” and “toxic emissions and waste.” We find no effect on the level of emissions but a significantly negative effect on emission intensity. These negative effects are stronger than the effect when considering all environmental engagements (). Our results indicate a 24.61% decrease in total CO2e intensity, a 30.47% decrease in scope 1 intensity, and a 25.73% decrease in scope 2 intensity for target firms relative to peers.

As a validation check, we also examine the effect of governance and social engagements on CO2e emission intensity. Although we would not expect an effect of social engagements on a firm’s environmental performance, it is plausible that governance can improve environmental performance. For example, Dyck et al. (Citation2023) found that board renewal improved environmental performance. We find that firms targeted by governance engagements lower their CO2e emission intensity significantly compared to peer firms (Online Appendix 6, column 2), but the effect is less strong than the effect of environmental engagements (−7.36 vs. −12.41%). As expected, we find no change in the emissions of firms targeted by social engagements. Overall, we can conclude that environmental and governance engagements are followed by a decreased emission intensity but no change in total emissions.

Discussion and Conclusion

We study a unique database of 7,415 private shareholder engagements on ESG issues with 2,465 publicly listed firms worldwide from 2007 to 2020. We provide new insights into private engagement characteristics and evaluate target firms’ financial and ESG performance after the engagements. Importantly, we investigate the extent to which private engagements address financially material ESG issues and how materiality matters for the financial performance of firms following the engagement. Using the materiality frameworks of the SASB and MSCI, we determine which engagements address ESG issues that are material given the industry in which the target firm operates. We find that more than 74% of the private engagements address material topics, suggesting that materiality matters to the choice to engage. We also find that target firms recognize which issues are material since material engagements are more likely to succeed.

An important question we answer in this paper is how firms perform after engagements on material ESG issues. We find that firms with successful material engagements significantly outperform peers by 2.5% over the 14 months after those engagements. In terms of economic significance, some of the magnitudes of the post-engagement stock returns we find are modest, while they are more significant for material engagements and for specific ESG subtopics. On the whole, we agree with the observation of Dimson, Karakaş, and Li (Citation2015) that ESG engagement returns, on average, lie somewhere in between the large effects found for traditional activism by hedge funds and the smaller effects found by earlier studies on the traditional activism by institutional investors (e.g., filing shareholder proposals at U.S. firms).

Regarding accounting performance, we find that material engagements are more often significantly associated with profitability and cost ratios compared to immaterial engagements. Material governance engagements most consistently show significant associations with future performance in terms of higher profitability and lower expense ratios. Furthermore, environmental engagements positively relate to capital and R&D expenditures when they are material.

Next to financial performance, our evidence indicates that engagements are, on average, accompanied by an improved ESG performance of target firms. Importantly, environmental engagements are associated with a decrease in CO2e intensity and an increase in the MSCI environmental score. However, we do not observe a significant decrease in the total level of CO2e emissions. Since current research shows that institutional investors might choose to decarbonize their portfolios by underweighting high-carbon firms rather than engaging with them (Atta-Darkua et al. Citation2022), future research could further study whether firms’ emissions deteriorate over the long run following engagements.

Several implications arise from the results of our paper. First, the results indicate that materiality matters for the post-targeting stock market and accounting performance of target firms. Hence, investors who engage on ESG issues that align with their financial goals are more likely to accomplish their objectives by focusing on material ESG issues. Second, our finding that material engagements are more likely to succeed indicates that investors who strive for engagement success should address material topics, regardless of whether they pursue financial or other goals with their engagements. At the very least, our findings illustrate that investors benefit from making materiality salient when engaging on ESG issues.

Third, we recommend that investors use materiality frameworks, such as SASB or MSCI, to collect structural data on their engagement efforts. Investors differentiate between financially material and stakeholder-material sustainability. Financially material sustainability encompasses the effects of the economy, environment, and its people (stakeholders) on the corporation, while stakeholder materiality involves the effect of the corporation on its stakeholders. It is important to note that ESG issues can be both shareholder and stakeholder material (i.e., double material). In this paper, we do not determine the extent to which private ESG engagements are material from a stakeholder perspective. The Global Reporting Initiative (GRI) is currently developing sector-level, stakeholder-materiality standards that investors and academics can use to examine the double materiality of shareholder engagement in future reporting and research.

We conclude this paper with a few cautionary notes and recommendations for future research. First, although academics and practitioners increasingly deem engagement as a plausible mechanism for shareholders to generate a positive societal impact, we are cautious not to interpret our results as evidence that the engagements causally affect firm behavior. Because we cannot observe the entire universe of private engagements by other stakeholders, identifying which ones affect firm behavior is challenging. Moreover, given ESG data limitations, we mostly study larger firms while the potential to influence smaller ones through engagement is arguably greater. Hence, our study provides a solid indication but not a definitive account of the overall effect of engagements on target firms.

Second, many investors aim to improve firms’ ESG performance via engagement, but our study may not capture long-term improvements in ESG performance. Many ESG policies that firms adopt today materialize slowly. For example, after an engagement on carbon emissions, a target firm might set long-term targets to reduce emissions. However, only time will tell whether the firm can reach the targets. Because we study ESG scores and emissions in the five years after an engagement, we cannot make claims about the long-term effects of engagement.

Finally, our paper does not take a stance on whether frameworks for assessing the financial materiality of ESG issues, such as those of the SASB and MSCI, should be prioritized over other materiality frameworks in engagement decisions. For example, given the scope of our paper, we do not address the extent to which engagements guided by financial materiality steer firms toward achieving the UN sustainable development goals or climate targets laid out by climate science. How well different materiality frameworks help investors in contributing to such goals is an interesting question that we leave for future research.

Supplemental Material

Download PDF (846.9 KB)Acknowledgments

We obtained financial support from Columbia Threadneedle Investments UK International Limited for hiring the research assistants, who are affiliated with Maastricht University. Maastricht University licenses the SASB Standards.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Notes on contributors

Rob Bauer

Rob Bauer is a professor of finance at School of Business and Economics, Maastricht University, Maastricht, Netherlands.

Jeroen Derwall

Jeroen Derwall is an assistant professor of finance at School of Business and Economics, Maastricht University, Maastricht, Netherlands, and associate professor of finance at School of Economics, Utrecht University, Utrecht, Netherlands.

Colin Tissen

Colin Tissen was a PhD candidate of finance at School of Business and Economics, Maastricht University, Maastricht, Netherlands until September 2022. He is currently Advisor Responsible Investments at PGGM, Zeist, Netherlands.

Notes

1 As of March, 31, 2022, the reo service has €1,007bn of assets under engagement.

2 Considering the amount of manual data processing, we hired two research assistants.

3 For the automobile sector, SASB writes that “Fuel Economy Use-Phase Emissions” is a material disclosure topic. This topic belongs to “Product Design and Lifecycle Management,” which is a subtopic of “Business Model & Innovation.”

4 We only include one materiality indicator in our time-series analyses to not overcomplicate them. For example, we want to avoid a quadruple interaction in our difference-in-difference analyses (i.e., TargetESG × AfterESG × MaterialSASB × MaterialMSCI). Moreover, in our examination of engagement success, we find that materiality only significantly affects success when both materiality frameworks agree on materiality.

5 The asset manager did not consistently collect data on whether an engagement was done individually or with other investors in earlier years of the sample, which is why the number of observations for “Alone” and “Collaborative” do not add up to the total number of engagements. Moreover, there are two instances where the method of the engagement was unknown.

6 We did not include the measure of participant intensity in our main model because the asset manager did not consistently record the information on whether they engaged alone or with other investors. The inclusion of the measure decreases our sample size by about one-third.

7 We match based on the MSCI sectors and subindustries instead of the more common SIC classifications because MSCI ESG measures different ESG issues depending on the firm’s industry. Hence, to accurately examine the effect of engagement on the ESG performance of target firms compared to peer firms, they must operate in the same MSCI industry.

8 We formally test the determinants of being targeted using a logistic regression in Appendix B.

9 We could use within-industry market size deciles instead of quartiles to control for this, but because we also match on MSCI subindustry and country, this would lead to an insufficient number of matches.

10 Our results are very similar when using [0,12] instead.

11 An assumption of difference-in-difference models is that treatment and control firms show similar trends in the outcome variable before the treatment that would have continued if there were no engagement. In untabulated results, we check this “common-trends” assumption and find that it reasonably holds.

12 Material social engagements are also associated with higher ROE and lower CAPEX/sales, but these effects are only significant at the 10% level.

13 For example, the average within-firm standard deviation for the MSCI ESG score is 1.15 compared to a between-firm standard deviation of 2.17.

14 We use four instead of five years because moving to this strongly balanced panel already decreases the sample by two-thirds, and there are even fewer firms with emission data for 10 years around the engagement.

15 There are more observations for total CO2e emissions than scope 1 and scope 2 CO2e emissions. This difference indicates that some firms only report their total level of emissions to Refinitiv and do not separate their emissions into scope 1 or scope 2.

References

- Atta-Darkua, Vaska, Simon Glossner, Philip Krueger, and Pedro Matos. 2022. “Decarbonizing Institutional Investor Portfolios.” Working Paper.

- Barko, Tamas, Martijn Cremers, and L. Luc Renneboog. 2022. “Shareholder Engagement on Environmental, Social, and Governance Performance.” Journal of Business Ethics 180 (2): 777–812. doi:10.1007/s10551-021-04850-z.

- Bauer, Rob, Jeroen Derwall, and Colin Tissen. 2022a. “Corporate Directors Learn From Environmental Shareholder Engagements.” Working Paper.

- Bauer, Rob, Jeroen Derwall, and Colin Tissen. 2022b. “Legal Origins and Institutional Investors’ Support for Corporate Social Responsibility.” Working Paper.

- Bauer, Rob, Tobias Ruof, and Paul Smeets. 2021. “Get Real! Individuals Prefer More Sustainable Investments.” The Review of Financial Studies 34 (8): 3976–4043. doi:10.1093/rfs/hhab037.

- Berg, Florian, Julian F. Kölbel, and Roberto Rigobon. 2022. “Aggregate Confusion: The Divergence of ESG Ratings.” Review of Finance 26 (6): 1315–1344. doi:10.1093/rof/rfac033.

- Climate Action 100+. 2022. Initiative Snapshot. Accessed May 6, 2022. https://www.climateaction100.org

- Dimson, Elroy, Oğuzhan Karakaş, and Xi Li. 2015. “Active Ownership.” Review of Financial Studies 28 (12): 3225–3268. doi:10.1093/rfs/hhv044.

- Dimson, Elroy, Oğuzhan Karakaş, and Xi Li. 2021. “Coordinated Engagements.” Working Paper.

- Dyck, Alexander, Karl V. Lins, Lukas Roth, Mitch Towner, and Hannes F. Wagner. 2023. “Renewable Governance: Good for the Environment?” Journal of Accounting Research 61 (1): 279–327. doi:10.1111/1475-679X.12462.

- Gibson Brandon, Rajna, Philip Krueger, and Peter Steffen Schmidt. 2021. “ESG Rating Disagreement and Stock Returns.” Financial Analysts Journal 77 (4): 104–127. doi:10.1080/0015198X.2021.1963186.

- Grewal, Jody, George Serafeim, and Aaron Yoon. 2016. “Shareholder Activism on Sustainability Issues.” Working paper.

- Hoepner, Andreas G. F., Ioannis Oikonomou, Zacharias Sautner, Laura T. Starks, and Xiao Y. Zhou. 2022. “ESG Shareholder Engagement and Downside Risk.” Working Paper.

- Khan, Mozzafar. 2019. “Corporate Governance, ESG, and Stock Returns around the World.” Financial Analysts Journal 75 (4): 103–123. doi:10.1080/0015198X.2019.1654299.

- Khan, Mozzafar, George Serafeim, and Aaron Yoon. 2016. “Corporate Sustainability: First Evidence on Materiality.” The Accounting Review 91 (6): 1697–1724. doi:10.2308/accr-51383.

- Kölbel, Julian F., Florian Heeb, Falko Paetzold, and Timo Busch. 2020. “Can Sustainable Investing save the World? Reviewing the Mechanisms of Investor Impact.” Organization & Environment 33 (4): 554–574. doi:10.1177/1086026620919202.

- Matsumura, Ella Mae, Rachna Prakash, and Sandra C. Vera-Munõz. 2022. “Climate-Risk Materiality and Firm Risk.” Review of Accounting Studies 1–42. doi:10.1007/s11142-022-09718-9.

- MSCI. 2023. “MSCI ESG Ratings Methodology.” https://www.msci.com/documents/1296102/34424357/MSCI+ESG+Ratings+Methodology+%28002%29.pdf

- Riedl, Arno, and Paul Smeets. 2017. “Why Do Investors Hold Socially Responsible Mutual Funds?” The Journal of Finance 72 (6): 2505–2550. doi:10.1111/jofi.12547.

- SASB. 2020a. “We’re Learning the Lessons of the Pandemic Alongside Markets.” https://www.sasb.org/blog/were-learning-the-lessons-of-the-pandemic-alongside-markets/

- SASB. 2020b. “WSJ Editorial Misrepresents SASB.” https://www.sasb.org/blog/wsj-editorial-misrepresents-sasb/