?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

One of the most complex policy issues that developing countries will face as a result of the employment crisis caused by the Covid crisis is the question of how they can better protect the unemployed. However, the analysis of unemployment insurance (UI) in developing economies with large informal sectors is in its infancy, with few papers providing solid empirical evidence. This paper therefore makes several contributions: first, it applies Chetty’s 2008 landmark work on UI to a transition economy (Chile) and shows that the moral hazard effects expected by policy makers, who designed the system are minimal, while liquidity effects were entirely neglected. Second, it demonstrates that it is not enough merely to quantify effects such as moral hazard, but to understand their causes as unemployment generated by moral hazard or liquidity constraints has different welfare implications and should therefore result in different policies. By means of an RDD, this paper analyses the Chilean UI system using a large sample of administrative data, which allows for an extremely precise analysis of how the system works, thus providing invaluable empirical lessons for other countries.

1. Introduction

All over the world the Covid 19 pandemic and its resulting economic consequences have highlighted social policy shortcomings. One of the most complex issues is the question of how workers who become unemployed can be protected. This is an even more crucial question in developing countries, which rarely have fully fledged welfare states and where the Covid19 pandemic and resulting economic crises have highlighted the need for functioning UI systems even more (Caram & Pupo, Citation2020; Otero, Citation2020). The crisis has undoubtedly accelerated changes in the way we work, for example in the proportion of people who work (at least partially) from home. In addition, the advent of technological progress and the increased use of artificial intelligence will likely exacerbate and accelerate structural changes in labor markets.

The theoretical literature on unemployment insurance (UI) in developed countries has long recognized its role in terms of both its economic and social value. Terms such as consumption smoothing and job matching are used in line with those related to welfare benefits and analysis. According to Chetty and Looney (Citation2006), these potential welfare gains can be particularly significant in less industrialized countries, where many workers live in households that are particularly vulnerable to economic shocks, which can lead to costly expenditure reductions, such as taking children out of full time education. However, in the literature in developing countries, concerns relating to moral hazard have dominated the debate.

There is now a consensus in the policy making literature that some form of two-tiered UI provision in developing countries would be desirable. This should feature (1) a mandatory individual savings account (ISA) and (2) a risk sharing funding mechanism that is redistributive and financed through taxes or collective contributions, which step in when savings accumulated in the ISA run out (Duval & Loungani, Citation2019 and Ribe, Robalino, & Walker, Citation2010). The idea is that such a structure would protect workers who become unemployed without incurring significant moral hazard in transition and developing countries where informal sectors and limited institutional capacity to monitor the behavior of the unemployed make the establishment of traditional risk sharing, redistributive UI systems unfeasible.

In this literature, Chile’s UI system is widely assumed to have achieved a near optimal design (Vodopivec, Citation2013). In fact, several countries have already instituted such two-tiered systems, including Brazil, Colombia, Jordan, and Mauritius. Unfortunately, with the notable exception of BrazilFootnote1 and ChileFootnote2, little empirical research analyses how they work in practice. As Schmieder and von Wachter (Citation2016, p. 577) point out: ‘the analysis of the role of UI in developing economies with large informal sectors is in its infancy’. Studying this subject is particularly important given the ‘sizable interest by many emerging market countries in developing UI systems’. However, previous studies of the Chilean UI, such as Hartley et al. (2011) and Huneeus, Leiva, and Micco (Citation2012), only discuss moral hazard effects without examining whether the behavior of the unemployed may be motivated by a liquidity effect.

Given this context, this paper studies the case of Chile, which has long been considered a pioneer of social insurance policies in Latin America (Madero-Cabib et al., Citation2019) and is widely regarded as a model by other countries in the region and beyond. This research uses longitudinal administrative data from the Chile’s UI system, which allows for a very precise analysis of how the system is functioning. Using a regression discontinuity design (RDD), this paper explores several key research questions: first: has the design of the Chilean UI system indeed minimized moral hazard, and, if so, to what extent? Second, does it provide users with enough benefits to generate a liquidity effect?Footnote3 Third, what are the reasons why the Chilean UI provides such limited benefits to unemployed workers? And finally, is the Chilean UI system regressive in its design?

The paper makes four key contributions: First, it analyses how the Chilean UI system works using a large sample of longitudinal administrative data. Previous studies published on the system used biased datasets as the insurance had not been fully rolled out yet.Footnote4 Second, the RDD used shows minimal moral hazard, while a liquidity effect does exist, although only among first-time users of the system with fixed-term contracts. Third, this paper contributes to development research by showing that it is not enough merely to quantify an effect (as most economists do), but to understand its causes and implications: An extended unemployment period stemming from moral hazard has extremely different welfare implications than one stemming from a liquidity effect and should therefore result in different policy recommendations. Finally, our results emphasize that the Chilean UI system is regressive overall, as it protects workers with higher income levels and stable jobs much more than vulnerable workers, who are much more likely to become unemployed.

This research thus has important implications for other developing countries, which may also be considering the implementation of some form of UI, especially given the impact of the Covid crisis. Although Chile is now no longer considered a developing country, its UI system was designed and implemented in 2001–2004, when it was still very much considered a developing country. The period covered by this paper (2010–2019) shows how Chile’s labor market developed during this transition period to becoming a country that is officially considered ‘developed’. However, its labor market is still characterized by employment patterns that are typical of developing countries, in particular a significant informal sector and very high job turnover rates.Footnote5

This paper proceeds as follows: Section 2 discusses the literature relevant to this paper. Section 3 explains the particularities of the Chilean unemployment insurance system and presents a descriptive analysis of how the system works in practice. Section 4 then presents the analytical model and the data used, Section 5 analyses its results and their implications for moral hazard and liquidity effects. Section 6 discusses the social policy implications of this research for other countries.

2. Theoretical approaches to unemployment insurance

The theoretical literature on UI systems has historically focused on the optimal design of UI (Hopenhayn & Nicolini, Citation1997) by examining the relationship between the contribution requirements to UI systems, the duration of unemployment benefits and job search behavior through stylized models. Recent papers have extended their models to include biased beliefs about employment prospects (see, e.g. Spinnewijn, Citation2015) or by adapting them to include dynamic profiles (see e.g. Kolsrud, Landais, Nilsson, & Spinnewijn, Citation2018; Landais, Citation2015).Footnote6 The goal of these ‘optimal designs’ is twofold: to provide liquidity and avoid adverse incentives when searching for a new job (Fredriksson & Holmlund, Citation2006). However, initially, the main concern in the development literature has always focused on the latter.

Hopenhayn and Nicolini (Citation1997, 2009), for example, argue that unemployment benefits should incorporate a decreasing replacement ratio, together with a future wage tax that increases with the duration of unemployment. Feldstein and Altman (Citation2007) even suggest that individual savings accounts should be established for workers so that they can save for the possibility of unemployment, with the government extending potential loans against future earnings (at a premium) when individual accounts are depleted.Footnote7 These options thus propose to eliminate any social risk sharing associated with traditional unemployment insurance systems to avoid the potential of moral hazard.Footnote8

These arguments are based on research which shows a spike in the hazard rate (i.e. in job search effort) around the time when social benefits run out in countries such as Austria or Germany (Card, Chetty, & Weber, Citation2007; Schmieder, von Wachter, & Bender, Citation2012). However, attributing this spike only to moral hazard ignores the existence of other issues, such as liquidity constraints related to the fact that better unemployment benefits reduce the pressure to accept the first job offer received, which in some cases can explain up to 60% of the increase in unemployment durations (Chetty, Citation2008; Landais, Citation2015; Landais & Spinnewijn, Citation2019). Both the ‘moral hazard effect’ and the ‘liquidity effect’ result in longer non-contribution periods, but their welfare implications differ greatly.

A more recent strand of literature has therefore examined consumption responses to income changes and has highlighted the sensitivity of consumption to liquidity. This literature focuses on the positive welfare effects of unemployment insurance: providing liquidity and limiting the need for precautionary savings (Jappelli & Pistaferri, Citation2010). Gerard and Naritomi (Citation2021) show that Brazilian workers eligible for both unemployment insurance and severance pay increase their consumption at layoff by 35% and suffer a 17% drop after they stop receiving benefits. Similar patterns have been found in the United States (Ganong & Noel, Citation2019) and Sweden (Landais & Spinnewijn, Citation2019).

However, the social policy debate on ISA based systems in transition and developing countries either predates this more recent literature or simply does not consider its arguments on liquidity constraints.Footnote9 Also, this debate emphasizes that labor markets in these countries are different from those in advanced economies, as they are characterized by both higher levels of informal employment and lower levels of institutional capacity, thus generating a higher potential risk of moral hazard.Footnote10 Many experts therefore suggest that self-insurance schemes based on Individual Savings Accounts (ISAs), complemented with some state funding would work best in developing countries, although Blanchard and Tirole (Citation2008) warn that the use of individual savings accounts can also result in excessive job destruction as firms do not have to internalize the cost of layoffs.

Four conclusions can be drawn from the literature on UI in transition and developing countries: first, a theoretical concern about moral hazard outweighs welfare issues, in particular the potentially positive impact of liquidity effects as specified by Chetty (Citation2008). Second, as Schmieder and von Wachter (Citation2016) have pointed out, there is a dearth of empirical literature on how UI systems really function in these countries – as opposed to theoretical discussions of how they could function. In particular, studies analyzing administrative data from UI systems are scarce.Footnote11 Third, to the best of our knowledge, there are no empirical studies of the complementarity between UI systems and the characteristics of the labor markets in which they operate. This means that optimal insurance systems can be designed in theory and then fail to cover the unemployed as the conditions they impose on potential beneficiaries are not compatible with employment conditions in precarious labor markets (Robalino, World Bank, & USA, Citation2014; Sehnbruch, Carranza, & Prieto, Citation2019). Fourth, despite warnings from some authors (e.g. Blanchard & Tirole, Citation2008), a consensus has emerged in the literature that ISAs with some form of additional government support would work best in developing countries. Overall, this literature significantly underestimates the role of UI as a social policy as well as its potential to address liquidity constraints resulting from loss of employment. These shortcomings were highlighted even more by the Covid crisis.

In the case of the Chilean UI, Sehnbruch et al. (Citation2019) chronicle the process of this debate. So far, the existing literature has concluded that the Chilean system provides reasonable protection and limited distortions (Berstein, Citation2010), even though some studies argue that it has not eliminated the issue of moral hazard (Reyes-Hartley, van Ours, & Vodopivec, Citation2011 and Huneeus et al., Citation2012). As discussed above, these papers have not at all considered the implications of liquidity effects, as they continue to attribute all changes in unemployment durations to moral hazard. This paper shows that the study of the Chilean UI system requires a more nuanced approach, particularly regarding the use made of its solidarity component, as well as its effects on job search efforts.

3. Background to the Chilean UI system

The Chilean UI covers all dependent workers between the ages of 18 and 65, who work in the private sector and who have been unemployed for at least 30 days. This means it excludes the self-employed (or informal workers), domestic service workers (who have an individual savings account mechanism) and the public sector.Footnote12

Since its institution in October 2002, all new employment contracts have been contributing to the UI system. The amount each worker contributes to the system depends on their type of contract. Workers with open-ended contracts contribute 0.6% of their taxable income to their own ISA, while employers contribute 1.6% to the same account and 0.8% to the Solidarity Fund, resulting in a total contribution of 3% per worker. Workers with fixed-term contracts, on the other hand, do not contribute to the system at all, but their employers contribute 2.8% of their taxable income to their ISA and 0.2% to the Solidarity Fund, also resulting in a 3% contribution per worker.Footnote13 These contributions are summarized in of the Supplementary Material to this paper.Footnote14

Table 1. Characteristics of employed workers (RAW data – January 2018).

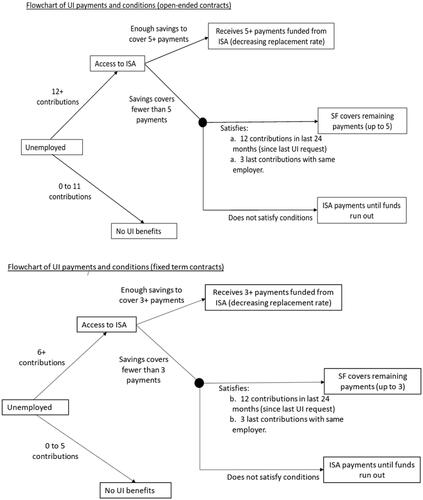

To withdraw money from the UI system, workers who had open-ended contracts must have contributed to the system for at least 12 months if they are to receive savings from their ISA or 12 months over the course of the last 24 months if they wish to claim payments from the Solidarity Fund. In the case of workers with fixed-term contracts, they may receive payments from their ISA if they have contributed for 6 months to the system. If they wish to claim benefits from the Solidarity Fund, however, they too must have contributed for 12 months. Workers only have access to the Solidarity Fund if they lose their job as a result of a redundancy clause, not if they resign voluntarily from employment. illustrates how the UI system works by means of a flow chart for workers with open-ended and fixed-term contracts.

Figure 1. Flowchart of UI system by type of contract.

The amount and number of payments that a worker can ultimately withdraw from the UI system thus depends on the type of contract held before becoming unemployed and on the amount of savings accumulated in his or her ISA. Replacement rates then begin at 70% of the prior wage, decreasing to 55% and then by 5% each month until reaching a minimum of 30%. If a worker has sufficient savings, the number of withdrawals that can be made is theoretically unlimited, although after the seventh month of unemployment the replacement rate is maintained constant at 30 per cent. In case of high unemployment,Footnote15 each worker can get up to two additional payments with a replacement rate of 30% each.

If the funds accumulated in a worker's individual savings account are insufficient to fund a period of unemployment and the worker was made redundant, s/he has the right to obtain additional benefits from the system's Solidarity Fund for up to five months equal to what a worker would obtain from his/her ISA, and subject to legal minimum and maximum amounts (Sehnbruch et al., Citation2019). The maximum duration for SF benefits is fixed at 5 months (3 for fixed term workers) and does not depend on ISA benefits. SF benefits kick-in if the ISA account has been exhausted before five payments have been made (and only if additional conditions are satisfied), assuring 5 payments in total. In case of high unemployment rates, the SF increases the number of payments from 5 to 7. This means that both workers with fixed-term contracts and open-ended ones can receive two more payments.

Unemployed workers thus only receive payments from the Solidarity Fund if their own savings have been used up. It is this inclusion of a Solidarity Fund that distinguishes the Chilean UI system from other such systems in Latin America and that led to its description as a ‘model’ for other transition and developing countries.

3.1. Data used in this study

This paper uses the longitudinal administrative database of the Chilean UI system, which is managed by the Supervisory Agency of Pensions (Superintendencia de Pensiones). This paper uses an 8% sample of workers from this database, which includes monthly information on each employment relationship. It also includes information on benefit claims between 2002 and 2018.Footnote16

This paper uses the terms ‘unemployment’ and ‘unemployed’ loosely when referring to workers, who stop contributing to this UI system. In fact, the nature of the administrative dataset does not distinguish between workers who are genuinely unemployed while not contributing to the system (i.e. not working and looking for a new job), or those who are inactive, working informally, or working in sectors not covered by the UI system (e.g. domestic service, armed forces, or the public sector). For the purposes of linguistic simplicity, workers not contributing to the UI system are referred to as ‘unemployed’.

To account for the problem of including people, who may not be unemployed, we focus on workers with an unemployment duration of less than 24 months. These are workers who reappear in the data (or stopped working during the last two years) thus minimizing the issue of working outside of the formal non-public job market.Footnote17

The analysis presented in this paper centers on all terminated employment relationships after 2010 as the database is highly biased prior to this date: when the UISA system was implemented in 2002, all newly created employment relationships were automatically affiliated to the system, while workers with an active contract could opt in. This resulted in a database highly biased towards shorter employment relationships. It is not until 2009 that the database matured and stabilized, producing estimates comparable to statistics derived from official employment surveys. In addition, a reform in 2009 changed the requirements for accessing the UI system. Focusing on data after 2010 thus provides a sample of workers representative of the formal labor force, who all shared a common set of rules to access the UI.

3.2. Benefits paid by the UISA

The four main factors that determine benefits received from the UISA are the reason for unemployment, the duration of the previous job and its wage level, and the contractual status the worker had prior to becoming unemployed (open ended or fixed-term contracts). These are therefore the conditions that have to be considered when analyzing the empirical evidence that relates to the functioning of the Chilean unemployment insurance system.Footnote18 shows that 69.8% of the workers contributing to the UI system have open-ended contracts. Their average income is USD 1,243 and the job duration of all workers is very low at only 31 months.

It is this low level of job duration that explains why relatively few workers claim benefits from the insurance. Although the condition that workers must have contributed for a minimum of 6 or 12 months (fixed or open-ended contracts respectively) is not particularly stringent in the comparative context of UI systems (Asenjo & Pignatti, Citation2019), the short duration of employment in Chile means that very few workers are able to comply with this condition before becoming unemployed, especially as the unemployed are more likely to have held precarious jobs to begin with, as shows.

Table 2. Characteristics of employed and unemployed workers (raw data – January 2018).

In the case of terminated employment relationships, 73.6% held fixed-term contracts, average wages were lower at USD 602, and jobs lasted only 8.7 months on average. Unsurprisingly, therefore, workers are likely discouraged from applying to the UI system as many would not qualify for benefits. Of those workers, who do, 60% held open-ended contracts, averaged earnings of USD 612.5 and had accumulated savings during 24.9 months. It is therefore fair to conclude that workers who apply to the UI system for funds self-select. Those workers, who become unemployed and held the most precarious jobs know that they would not be eligible for benefits and therefore rarely bother making a claim.Footnote19

Overall, the share of workers with the right to use the SF among the unemployed of the UISA are quite low as illustrated in . In our sample (2010-2018), we see that 7% of all terminated employment relationships make a request to the UI system. Within those requests, a third satisfy the requirements for using the Solidarity Fund (44% of open-ended and 17% of fixed-term contracts). Among all requests, 16% end up using the Solidarity Fund (16% on average, 24% of open-ended and 5% of fixed-term workers). In other words, despite eligibility rates being low, among those eligible, half of the workers opt for using the Solidarity Fund.Footnote20

shows that the use of the UI is not only low, but highly regressive. On average, requests to the UI as well as the right to use the Solidarity Fund increase with earnings. The same is true for the use of the Solidarity Fund, which is higher among the top three quintiles. Among open-ended contracts in the fifth quintile, 23% of all terminated relationships make a request to the UI, whereas only 5% of workers at the first quintile do so. This gap is even bigger for fixed-term workers at 10% and 1% for the fifth and first quintile respectively, among whom the overall use is much lower. We also see large differences when looking at access to the Solidarity Fund. On average, 27% of requests made by workers with open-ended contracts have the right to use it in the first quintile, versus 44% among the top quintile (13% and 21% among fixed-term workers, respectively). The actual use of the Solidarity Fund shows a more heterogenous pattern, with a higher share of users among the third and fourth deciles for open-ended contracts and a very uniform use (albeit low, at 4–6%) for fixed-term workers. Overall, access and use of the solidarity component are thus highly skewed towards higher earning jobs, leaving the most vulnerable workers with lower incomes and who had fixed-term contracts (and are therefore much likely to become unemployed) wholly unprotected. Evidently, such a system exacerbates labor market inequalities rather than redressing them.

Table 3. Use of the UI by income quintile (% of all terminated employment relationships).

3.3. Additional benefits from the solidarity fund – the size of our treatment

Before discussing our empirical framework, this section presents an overview of the applied treatment – having a right to claim the Solidarity Fund – and its impact on the overall formal labour force. As discussed before, ‘having a claim to the Solidarity Fund’ means that you satisfy the eligibility criteria discussed above, but also that the worker does not have enough savings to receive a minimum number of payments from the individual savings accounts. As such, the Solidarity Fund only complements individual savings.Footnote21 As shows for our final sample, a third of UI claimants have a claim to the Solidarity Fund and only 16% end up using it (24% for open ended contracts, 5.4% for fixed-term contracts). In other words, one third of our sample falls within the treatment group, with roughly half of that group actually benefiting from the Solidarity Fund.

Table 4. Use of the SF among UI claimants.

Those who do take up the Solidarity Fund benefit from additional payments, such that they can secure 3 or 5 payments, depending on the type of contract. shows the total number of payments for each of these groups. Workers who had open ended contracts and make a claim to the UI but had no claim to the Solidarity Fund receive on average 3 payments (2.3 for those with a claim but that do not use it). As expected, those who do accept the Solidarity Fund receive 5 payments. Fixed-term workers, on the other hand, receive around 1.3 payments on average, while those that use the Solidarity Fund receive 2.8.Footnote22

Table 5. Average number of payments among UI claimants.

The additional benefit of accessing the Solidarity Fund is around 2 additional payments. As they are the last payments, they have the lowest replacement rate (40 and 35% for the last two payments). In other words, a worker who had an open-ended contract and makes a claim to the UI system receives, on average, three payments for a total of 1.7 times their average wage. In addition, if that worker accessed the Solidarity Fund they would get two additional payments amounting to 0.75 of their average wage, or an 45% increase of what they would receive if there were no Solidarity Fund. A similar calculation for a fixed-term worker (receiving one additional payment through the SF) would represent an 85% increase. We see that the impact of payments from the Solidarity Fund can be substantial for the average worker. However, it is a very small percentage of workers who does – around a third of the unemployed could access it, but only a sixth does. As it stands, our treatment is a small one if the whole formal labour force is considered, which is why these findings should be treated as lower bounds of the effect of actually benefiting from the Solidarity Fund.

4. Methodology and empirical framework

To quantify the effect of having the right to use the Solidarity Fund, we propose a sharp regression discontinuity design. This design exploits the fact that workers need at least 12 contributions in the last 24 months for them to have the right to request benefits from the Solidarity Fund. Using this cut-off, we compare workers’ rights below and above this threshold to estimate the effect of having the right to access the Solidarity Fund. Under certain assumptions, the difference between these two groups will equal the effect of having the right to use the Solidarity Fund (Imbens & Lemieux, Citation2008; Lee & Lemieux, Citation2010).

We first examine the relevant discontinuities visually, and then proceed to estimate a standard regression discontinuity using the following model:

Where is the unemployment duration in months,

is an indicator variable equal to one if the worker has the right to use the Solidarity Fund, and

is a function of the running variable

in this case the number of contributions in the last 24 months for the previous employment, and the eligibility rule

whether the worker has 12 or more contributions (i.e.

). For estimation,

is modelled as a linear function with different slopes on both sides of the slope. Bandwidth for estimation is set at 4 months. Different bandwidths and a fourth-degree polynomial were tested in the Supplementary Material: Appendix, with results showing no important differences.

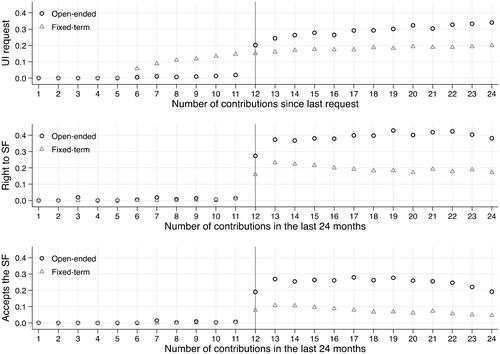

In this context, the treatment is having the right to use the Solidarity Fund. Treated workers are the unemployed workers who have made at least 12 contributions in the last 24 months, and thus have the right to use the Solidarity Fund, while untreated workers are the unemployed workers with 11 or fewer contributions in the same period, and who do not have the right to use the Solidarity Fund. Our RDD analysis uses the same data set for all estimations. We look at all terminated relationships between January 2010 and January 2018. We can see how this assignment rule works in . The first graph shows the share of unemployed workers who make an UISA request relative to the number of contributions since their last request. In the case of fixed-term workers, requests can only be made after making six contributions to the UISA, while open-ended contract workers must contribute for at least 12 months before being able to claim benefits. Between 15 and 20% of unemployed fixed-term workers claim benefits from the UISA, while the figure increases to between 20 and 35% of the unemployed among open-ended contracts.

Figure 2. Take-up rates of the UISA and the solidarity fund (SF). Note: Panel 1 includes the share of all terminated relationships that made a UI request as function of the number of contributions since the last request (i.e. the rule to access the UI). Panel 2 and 3 focus on the use of the solidarity fund, and therefore show shares of workers that made a request, as a function of the number of contributions in the last 24 months (i.e. the rule to access the SF). Panel 2 includes the share of workers with the right to use the SF and panel 3 the share of workers that accepts the SF. Contributions in the last 24 months do not necessarily have to have been continuous.

illustrates the rule that determines access the Solidarity Fund: Workers have the right to request the Solidarity Fund after 12 contributions, which is exactly the cut-off we see in . The first panel in the figure shows the number of UI requests made by workers whose employment relationships are terminated. The second panel illustrates how many of them theoretically have the right to payments from the Solidarity Fund, while the third panel shows how many of them actually apply for and receive funding from the Solidarity Fund.

5. Results

This section discusses the effect of having the right to use the Solidarity Fund, by type of contract as well as for the total sample. It starts by showing our results graphically and then proceeds to show the regression tables. Graphs include the corresponding 95% confidence interval at every point of the running variable. Lastly, to study the relative importance of the moral hazard and liquidity effects, it proceeds to repeat the analysis for each quintile of the earnings distribution. summarizes all results in regression form.

below analyses our sample: all terminated employment relationships that contributed to the UI system between 2010 and 2018. In addition to presenting the main results, the analysis makes a distinction between established workers and first-time entrants. The latter are defined as first-time contributors to the system and (if they make a request) first-time users of the UI system. This does not necessarily mean that this refers to a worker’s first job. As the UI only includes formal wage-earners from the private sector, entrants could include former public workers, self-employed or domestic service workers, informal workers or even former employers.

As shows, entrants with open-ended contracts earn higher incomes than established workers, are slightly older and the duration of their contribution to the system is only four months shorter on average. This suggests that entrants with open-ended contracts include workers with previous employment experience, who only became part of the UI system when they changed jobs. On the other hand, entrants with fixed-term contracts are younger, have significantly shorter job durations, and have lower incomes, more in line with what one would expect from first-time jobs.

Table 6. Descriptive statistics of all terminated employment relationships, 2010–2018.

5.1. Average effect of having the right to use the solidarity fund

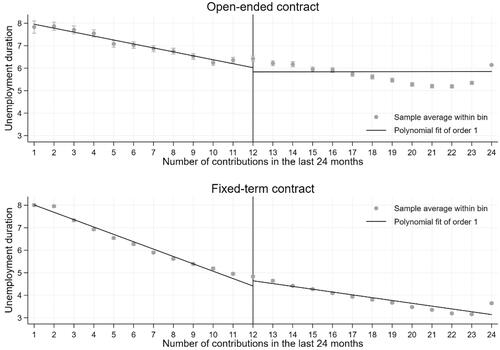

shows the duration of unemployment versus the running variable, namely the number of contributions in the last 24 months for all terminated employment relationships. The first panel shows how workers who had open-ended contracts use the UI system, while the second panel illustrates how workers who had fixed-term contracts use it. The results show small to no effects among the sample, as shown graphically in as well as in , which shows a small difference, of 0.13 months (4 days) for fixed-term workers and 0.18 months (5.4 days) for open-ended workers. Effects, although statistically significant, are small in terms of their economic significance.

Figure 3. Duration of unemployment by number of contributions in the last 24 months.

Figure 4. Duration of unemployment by number of contributions in the last 24 months (entrants only).

Table 7. Effect of having a claim to the solidarity fund.

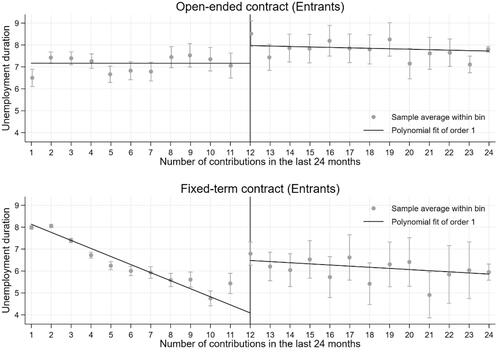

These estimates suggest that the aggregate effect of having the right to use the Solidarity Fund on unemployment duration is negligible. However, an important question is whether this conclusion holds for all workers in the system, or whether there are exceptions to this rule. To this end, first-time entrants to the UISA system are examined, i.e. workers who appear in our database for the first time, as defined above. And as discussed above, entrants with open-ended contracts have slightly better jobs than non-entrants, whereas the opposite is true for fixed-term contracts.

As shows, when looking at entrants, larger differences in how entrants and non-entrants use the UISA can be observed. shows that these effects are equivalent to 1.7 months (51 days) for open-ended contracts, and of 1.4 months (42 days) for fixed-term contracts. The average effect for entrants is of 1.6 months, or 48 days. First-time entrants show a significantly higher effect of having the right to use the Solidarity Fund, but as shows, these effects diminish importantly once the following employment relationships are considered.

These findings show that despite being qualitatively very different, entrants with both types of contracts have a quantitatively similar effect sizes. These effects likely represent different processes. Given that entrants with fixed-term contracts have worse jobs than non-entrants, these estimates may be driven by a liquidity effect. On the other hand, as open-ended entrants have better jobs than non-entrants, their effect may be driven by moral hazard. Using wages as a proxy of net assets, and therefore of liquidity constraints, this hypothesis is tested in the following section.

5.2. Heterogeneous effects: effects by average wage quintile

Following Chetty (Citation2008), the degree of liquidity constraint can be measured using net household assets, as households with no (or negative) net assets will have little liquidity to respond to unemployment shocks. Unfortunately, the Chilean UI database includes no information on savings, wealth, or debt. To provide a measure of the extent of the liquidity constrains of each worker, this paper follows Centeno and Novo (Citation2009) and splits the sample into income quintiles for each type of contract. This idea follows from the evidence that wages are the main driver of differences between poor and rich households and a good proxy of net assets (Ziliak, Citation2003).

Indeed, incipient studies show how wealth in Chile is highly concentrated at the top of the distribution, with the bottom 60% holding almost no wealth at all (Sanroman & Santos, Citation2017). By comparing workers in the lower and higher earnings quintiles, households with different wealth levels are compared. Households with limited (or no) wealth are expected to experience both a liquidity and a moral hazard effect, while high wealthier households should only experience the latter (Chetty, Citation2008; Chetty & Looney, Citation2006). If moral hazard effects are homogeneous across the wage distribution, then lower quintiles having a higher effect would indicate the presence of a liquidity effect.

extends the descriptive statistics of and by splitting the sample into wage quintiles and entrance category. Average wages for the highest quintile are roughly 10 times larger than for the first quintile. The fifth quintile is also comprised by older workers, by a higher share of men and a higher share of workers. The fact that entrants with open-ended contracts have better jobs than non-entrants holds across all quintiles. On the other hand, fixed-term entrants have lower incomes and overall worse quality jobs than non-entrants across all quintiles.

Table 8. Descriptive statistics by entrant status, type of contract, and by quintile.

A heterogeneous use of the UI system is also evident. As mentioned before, on average, higher earnings quintiles make more requests and are more likely to have the right to use the Solidarity Fund, while its actual use (conditional on making a request) is relatively uniform across the distribution. Among open-ended contracts, this result is driven by the non-entrant subsample. Among entrants who held open-ended contracts, the right to use the Solidarity Fund decreases for higher earnings quintiles while its use is higher for the first four quintiles (i.e. the lowest 80% of earners). Although a progressive structure is evident within this group, this is not the case among open-ended entrants, who held better jobs than their non-entrant counterpart. This further illustrates the regressive nature of the system.

estimates the effect of having the right to use the Solidarity Fund separately across three earning groups. It looks at the separate effect for the first quintile (bottom 20%), quintiles 2, 3 and 4 (middle 60%), and quintile 5 (top 20%). The general results hold. Effects for entrants are much larger than effects for the complete sample. The effects for entrants are furthermore driven by the extremes of the distribution.

Table 9. Effect of having the right to use the solidarity fund by average income quintile.

When looking at entrants with open-ended contracts, the top 20% increases their noncontribution period in 3.4 months, compared with an increase of 3 months for the bottom 20%. On the other hand, entrants with fixed-term contracts show effects at the bottom of the distribution that are much larger than effects at the top: 2.7.3 additional months versus 2.3 months. Results therefore suggest the presence of a liquidity effect only among entrants with fixed-term contracts.Footnote23

This result supports the idea that the liquidity effect is relatively more important for fixed-term workers. Given a relatively higher wealth stock, workers in the fifth quintile are expected to experience very little liquidity constraints, and therefore their effect is (at least to a great extent) driven by a moral hazard effect. Adapting Chetty (Citation2008), the difference between this effect and the effect for the bottom 20% can be interpreted as being driven by a liquidity effect. The fact that it is the most precarious jobs that have the strongest effect points to the fact that the liquidity effect trumps the moral hazard effect in that group.

When looking at open-ended contracts, the opposite result holds. Entrants have better jobs than the average open-ended worker, and among entrants the strongest effect appears to be among workers with the highest wages. As the largest effect is at the top of the distribution, the moral hazard effect appears to matter more than (or at least as much as) the liquidity effect in this group.

6. Conclusions

As Schmieder and von Wachter (Citation2016: 577) have highlighted, there is a lack of analysis of UI systems in developing countries. This paper attempts to fill this gap by analysing how the Chilean UI works, and whether the theoretical assumptions which underly its design (e.g. moral hazard risks) play out in practice. It highlights the need for further analysis as most of the theoretical literature that recommends ISA based UI systems is not based on empirical evidence. As the current Covid crisis is likely to prompt many developing economies to implement UI systems, it is even more important to understand how existing UI systems in such countries work.

This paper highlights first of all that the moral hazard observed among users of Chile’s UI system is minimal. This contradicts findings from previous studies (Huneeus et al., Citation2012; Reyes-Hartley et al., Citation2011). In fact, the data has to be disaggregated at a very granular level to find minimal evidence of moral hazard among first-time users of the system.

Second, to explore the relative importance of the liquidity and moral hazard effects in these results, this paper examines them by wage quintile, which was not done by previous studies. The low coverage of the system means that it provides very little liquidity to unemployed workers in general. These results show that average effects are driven by the first and fifth quintile, with little to no changes in the middle 60% of the wage distribution. However, the effect size changes by type of contract, and are more pronounced among low-income wage earners with fixed-term contracts. These results point towards a higher relative importance of the liquidity effect for fixed-term workers whose employment conditions are generally the most precarious.

Third, this paper makes the more general point that while the design of the UI system fulfilled its purpose of avoiding moral hazard, this result comes at the cost of providing such minimal benefits that the unemployed are discouraged from claiming benefits. In addition, these minimal benefits mean that potential positive liquidity effects from the insurance system are stunted from the outset.

Finally, it must be highlighted that the Chilean UI system exacerbates prevailing inequalities in the labor market. First, the likelihood of workers with precarious jobs becoming unemployed is much higher than for workers with better conditions. Second, when workers with precarious jobs become unemployed, they are then less protected by the UI system. Finally, the Solidarity Fund embedded in the system, which was originally supposed to redistribute funds towards lower income workers, does exactly the opposite. While most UI systems are not progressive in that benefits are related to previous salary levels and contribution histories, they are not as regressive as the Chilean system.

In addition, the Chilean UI does not include any provisions for redistribution linked to the situation of individual workers. Unlike UI systems in developed countries, which pay higher replacement rates depending on wage levels, age, number of children or dependents and whether a worker is the main earner in the family (Schmieder et al., Citation2012), the Chilean system includes no such mechanism.

This paper contributes to the existing literature in several ways; first, it shows that a theoretical concern about moral hazard and optimal insurance design in the theoretical literature developed in a context of industrialized countries with formal labor markets may play out very differently in transition and developing countries. Second, the liquidity analysis undertaken in this paper shows that this aspect must be considered from the outset when designing insurance systems. Third, this paper contributes to the empirical literature on how UI systems function in transition and developing countries, and therefore hopes to inform theoretical discussions, which at the moment are rarely driven by empirical results. In particular, the paper’s use of administrative data allows for a much more nuanced analysis. Further research, however, is also required to study the effects of UI on the reemployment wages of workers in Chile.

Overall, this paper leads to the conclusion that optimal UI systems can be designed that look good in theory but then fail to cover the unemployed as the conditions they impose on potential beneficiaries are not compatible with employment conditions in precarious labor markets (Robalino et al., Citation2014; Sehnbruch et al., Citation2019). As a result, they may fall into the category of ‘exclusionary social policies’ that Altman and Castiglioni (Citation2020) have identified in Latin American countries, which are ‘segmented and dualistic’. The consensus that can be distilled from the existing literature, which recommends UI systems for transition and developing countries based on ISAs combined with a solidarity component, ends up significantly curtailing the role of UI as a social protection mechanism as well as its potential to address liquidity constraints and inequalities resulting from loss of employment.

Finally, and considering this UI system from a broader perspective, it is essential to highlight how difficult it is for policy makers to design adequate social protection mechanisms when the underlying labor market is as precarious as the Chilean one. This is a salient point given that the data presented in this paper only considers the formal sector, which in developing countries is widely considered as being the non-precarious segment of the labor force. In fact, the UI system shows how high levels of job rotation, a high proportion of fixed-term contracts, frequent non-contribution periods and low wages combine to generate multiple and often simultaneous deprivations for formal workers, who are then not protected by social security structures (e.g. pension systems, which also rely on contributions to individual savings accounts). Policy attention should urgently focus on which policies would contribute to improving these employment conditions if they are to serve as a foundation for social protection systems. This is the key lesson that the Chilean UI system holds for other developing countries.

Correction Statement

This article has been republished with minor changes. These changes do not impact the academic content of the article.

Supplemental Material

Download PDF (1.5 MB)Acknowledgements

The authors would like to thank Francisco Ferreira, Pablo Guzman, Camille Landais and two anonymous reviewers for their comments on earlier versions of this paper.

Disclosure statement

No potential conflict of interest was reported by the autor(s).

Data availability statement

The 3, 5, and 8% samples of the longitudinal administrative database of the Chilean unemployment insurance system can be directly downloaded through the website of the Chilean Supervisory Agency of Pensions (Superintendencia de Pensiones) in www.spensiones.cl. All code is available on request.

Additional information

Funding

Notes

1 Brazil’s UI system is similar to the two-tiered system described by Duval and Loungani (Citation2019) although it consists of two separate institutions that are not integrated into a single system: The ISA mechanism in Brazil consists of the Fundo de Garantia do Tempo de Serviço (FGTS) and the risk sharing UI system is the separate Fondo de Amparo al Trabajador (FAT). For an analysis of these systems, see Hijzen (Citation2011), who uses panel survey data and Gerard and Naritomi (Citation2021).

2 Reyes Hartley et al., Citation2011 and Huneeus et al., Citation2012 analyse the Chilean UI with administrative data from before 2010 when the system was still being rolled out and had not yet fully matured; while Nagler (Citation2015) uses survey data. Only Sehnbruch et al. (Citation2019) use recent administrative data from a period when the UI system had already matured.

3 See for example Huneeus et al., Citation2012; Vodopivec, Citation2013. Notable exceptions are Hijzen, Citation2011; and Gerard & Naritomi, Citation2021.

4 After its implementation, only new contracts became part of the UI system. This means that data from the early years are biased as they include more workers with temporary or short-term contracts. As Sehnbruch et al. (Citation2019) show, the UI system matured after 2009.

5 The OECD’s Development Assistance Committee (DAC) establishes a list of developing countries that are eligible for receiving Official Development Aid from Institutions such as the United Nations, the World Bank and national development funds. Chile (along with the Seychelles and Uruguay) “graduated” from this list in 2018.

6 For an excellent overview of this literature, see Schmieder and von Wachter (Citation2016).

7 See, for example, van Ours and Vodopivec (Citation2006) on Jordan.

8 See also Orszag and Snower (Citation2002).

9 Note that these findings are replicated by Card et al. (Citation2007) for Austria and Basten et al. (Citation2016) for Norway.

10 See Feldstein and Altman (Citation2007); Ferrer and Riddell (Citation2011); Vodopivec (2013); Duval and Loungani, (Citation2019).

11 Exceptions to this rule are Sehnbruch et al. (Citation2019) and Gerard and Naritomi (Citation2021).

12 According to official data from Chile’s National Institute of Statistics, in 2018, 27.8% of workers in Chile are informal workers (mostly self-employed or “cuenta propia”), 10.9% are employers or formally self-employed, 2% are formal domestic service employees and 10.5% work in the public sector.

13 Note that that there are no rules in Chile in terms of which workers can be offered a fixed-term versus an open-ended contract. Fixed-term contracts are simply limited in that they can only be renewed twice.

14 See also Sehnbruch et al. (Citation2019) for more precise information on how the Chilean UI works.

15 Specifically, an unemployment rate one percentage point above the 4-year average.

16 Raw data from 6 different files were merged and harmonised: these included contribution histories, benefit claims, UI payments, and UI rejections. The final result is a dataset that includes monthly contributions for each worker, with information on whether they made a benefit claim after their employment ended, how many payments they received and from which source. For our analysis, we focus on the last month of employment, so we work with one observation per employment relationship.

17 To further reinforce the idea that this paper focuses on workers, who are searching for formal employment, Table A.15 in the Supplementary Material: Appendix replicates these results for unemployment durations of at most 12, 6, and 3 months. This disaggregation leads to the same conclusions.

18 A more detailed description of how the Chilean UI works (including its linkages to the services of municipal employment services and vocational training) can be found in Sehnbruch et al. (Citation2019).

19 See Sehnbruch et al., Citation2019 for a more detailed discussion.

20 The take up of the UI system is very low. Unfortunately, there is no reliable explanation for this. The Chilean Ministry of Labor undertook a survey of users to examine this issue, but its response rates were so low that its results were never published. Experts assume that the low take-up results from a lack of information about how to use the system combined with a reluctance on the part of users to comply with job search conditions attached to benefit payments from the Solidarity Fund.

21 Note that to receive benefits from the Solidarity Fund, a worker must have contributed to the UI system for at least 12 months. This means that the first payment will only ever be partially funded by the Solidarity Fund if at all.

22 The average number of payments is just below three payments, as before the 2009 reform fixed-term workers had the right to access only two payments from the solidarity fund.

23 These findings are further examined in Table A.16 in the Supplementary Material: Appendix, where the results are disaggregated by income deciles. This table reinforces the idea that differences in effects among fixed-term entrants are indeed found among the extremes of the distributions.

References

- Altman, D., & Castiglioni, R. (2020). Determinants of equitable social policy in Latin America (1990–2013). Journal of Social Policy, 49(4), 763–784. doi:10.1017/S0047279419000734

- Asenjo, A., & Pignatti, C. (2019). Unemployment insurance schemes around the world: Evidence and policy options (No. 49; Working Paper). Geneva: ILO Research Department.

- Basten, C., Fagereng, A., & Telle, K. (2016). Saving and portfolio allocation before and after job loss. Journal of Money, Credit and Banking, 48(2–3), 293–324. doi:10.1111/jmcb.12301

- Berstein, S. (2010). Seguro de Cesantía en Chile (1st ed.). Santiago: Chilean Pension Supervising Authority.

- Blanchard, O. J., & Tirole, J. (2008). The joint design of unemployment insurance and employment protection: A first pass. Journal of the European Economic Association, 6(1), 45–77. doi:10.1162/JEEA.2008.6.1.45

- Caram, B., & Pupo, F. (2020). Governo vai complementar renda de parte de trabalhadores que tiverem salário reduzido – 19/03/2020 – Mercado – Folha. Folha de S. Paulo. https://www1.folha.uol.com.br/mercado/2020/03/governo-vai-complementar-renda-de-parte-de-trabalhadores-que-tiver-salario-reduzido.shtml.

- Card, D., Chetty, R., & Weber, A. (2007). The spike at benefit exhaustion: Leaving the unemployment system or starting a new job? American Economic Review, 97(2), 113–118. doi:10.1257/aer.97.2.113

- Centeno, M., & Novo, Á. A. (2009). Reemployment wages and UI liquidity effect: a regression discontinuity approach. Portuguese Economic Journal, 8(1), 45–52. doi:10.1007/s10258-009-0038-8

- Chetty, R. (2008). Moral hazard versus liquidity and optimal unemployment insurance. Journal of Political Economy, 116(2), 173–234. doi:10.1086/588585

- Chetty, R., & Looney, A. (2006). Consumption smoothing and the welfare consequences of social insurance in developing economies. Journal of Public Economics, 90(12), 2351–2356. doi:10.1016/j.jpubeco.2006.07.002

- Duval, R., & Loungani, P. (2019). Designing labor market institutions in emerging and developing economies : Evidence and policy options. IMF Staff Discussion Notes No. 2019/004.

- Feldstein, M., & Altman, D. (2007). Unemployment insurance savings accounts. Tax Policy and the Economy, 21, 35–63. doi:10.1086/tpe.21.20061914

- Ferrer, A. M., & Riddell, W. C. (2011). Unemployment insurance savings accounts in Latin America: Overview and assessment. In Reforming severance pay (No. 5577; Discussion Paper Series). Washington, DC: The World Bank.

- Fredriksson, P., & Holmlund, B. (2006). Optimal unemployment insurance design: Time limits, monitoring, or workfare? International Tax and Public Finance, 13(5), 565–585. doi:10.1007/s10797-006-6249-3

- Ganong, P., & Noel, P. (2019). Consumer spending during unemployment: Positive and normative implications. American Economic Review, 109(7), 2383–2424. doi:10.1257/aer.20170537

- Gerard, F., & Naritomi, J. (2021). Job displacement insurance and (the lack of) consumption-smoothing. American Economic Review, 111(3), 899–942. doi:10.1257/aer.20190388

- Hijzen, A. (2011). The labour market effects of unemployment compensation in Brazil. OECD Social, Employment and Migration Working Papers, 119, 1–38.

- Hopenhayn, H. A., & Nicolini, J. P. (1997). Optimal unemployment insurance. Journal of Political Economy, 105(2), 412–438. doi:10.1086/262078

- Hopenhayn, H. A., & Nicolini, J. P. (2009). Optimal Unemployment Insurance and Employment History. Review of Economic Studies, 76(3), 1049–1070. doi:10.1111/j.1467-937X.2009.00555.x

- Huneeus, C., Leiva, S., & Micco, A. (2012). Unemployment insurance and search effort in Chile (No. IDB-WP-313; Working Paper). Retrieved from SSRN: https://ssrn.com/abstract=2149060

- Imbens, G. W., & Lemieux, T. (2008). Regression discontinuity designs: A guide to practice. Journal of Econometrics, 142(2), 615–635. doi:10.1016/j.jeconom.2007.05.001

- Jappelli, T., & Pistaferri, L. (2010). The consumption response to income changes. Annual Review of Economics, 2(1), 479–506. doi:10.1146/annurev.economics.050708.142933

- Kolsrud, J., Landais, C., Nilsson, P., & Spinnewijn, J. (2018). The optimal timing of unemployment benefits: Theory and evidence from Sweden. American Economic Review, 108(4–5), 985–1033. doi:10.1257/aer.20160816

- Landais, C. (2015). Assessing the welfare effects of unemployment benefits using the regression kink design. American Economic Journal, 7(4), 243–278. doi:10.1257/pol.20130248

- Landais, C., & Spinnewijn, J. (2019). The value of unemployment insurance (No. DP13624; Discussion Paper). London: CEPR Working Paper.

- Lee, D. S., & Lemieux, T. (2010). Regression discontinuity designs in economics. Journal of Economic Literature, 48(2), 281–355. doi:10.1257/jel.48.2.281

- Madero-Cabib, I., Biehl, A., Sehnbruch, K., Calvo, E., & Bertranou, F. (2019). Pension regimes built on precarious foundations: Lessons from a longitudinal study of pension contributions and employment trajectories in Chile. Research on Aging, 41(10), 961–987.

- Nagler, P. (2015). The impact of unemployment insurance savings accounts on subsequent employment quality (UNU-MERIT Working Paper Series, 026). Maastricht: UNU-MERIT.

- Orszag, J. M., & Snower, D. J. (2002). Incapacity benefits and employment policy. Labour Economics, 9(5), 631–641. doi:10.1016/S0927-5371(02)00050-7

- Otero, C. (2020). Políticas laborales en tiempos de pandemia: por qué hay que garantizar el 75% del ingreso de los trabajadores y cómo hacerlo – CIPER Chile. CIPER. https://ciperchile.cl/2020/03/26/politicas-laborales-en-tiempos-de-pandemia-por-que-hay-que-garantizar-el-75-del-ingreso-de-los-trabajadores-y-como-hacerlo/.

- Reyes-Hartley, G., van Ours, J. C., & Vodopivec, M. (2011). Incentive effects of unemployment insurance savings accounts: Evidence from Chile. Labour Economics, 18(6), 798–809. doi:10.1016/j.labeco.2011.06.011

- Ribe, H., Robalino, D. A., & Walker, I. (2010). Achieving effective social protection for all in Latin America and the Caribbean: From right to reality (English) | The World Bank. http://documents.worldbank.org/curated/en/777751468300697044/Achieving-effective-social-protection-for-all-in-Latin-America-and-the-Caribbean-from-right-to-reality.

- Robalino, D, World Bank, USA (2014). Designing unemployment benefits in developing countries. IZA World of Labor. https://wol.iza.org/uploads/articles/15/pdfs/designing-unemployment-benefits-in-developing-countries.pdf

- Sanroman, G., & Santos, G. (2017). The joint distribution of income and wealth in Uruguay. Department of Economics Universidad de La Republica - Documentos de Trabajo, 717 (pp. 1–38).

- Schmieder, J. F., & von Wachter, T. (2016). The effects of unemployment insurance benefits: New evidence and interpretation. Annual Review of Economics, 8(1), 547–581. doi:10.1146/annurev-economics-080614-115758

- Schmieder, J. F., von Wachter, T., & Bender, S. (2012). The effects of extended unemployment insurance over the business cycle: Evidence from regression discontinuity estimates over 20 years. The Quarterly Journal of Economics, 127(2), 701–752. doi:10.1093/qje/qjs010

- Sehnbruch, K., Carranza, R., & Prieto, J. (2019). The political economy of unemployment insurance based on individual savings accounts: Lessons from Chile. Development and Change, 50(4), 948–975. doi:10.1111/dech.12457

- Spinnewijn, J. (2015). Unemployed but optimistic: Optimal insurance design with biased beliefs. Journal of the European Economic Association, 13(1), 130–167. doi:10.1111/jeea.12099

- van Ours, J. C., & Vodopivec, M. (2006). How shortening the potential duration of unemployment benefits affects the duration of unemployment: Evidence from a natural experiment. Journal of Labor Economics, 24(2), 351–378. doi:10.1086/499976

- Vodopivec, M. (2013). Introducing unemployment insurance to developing countries. IZA Journal of Labor Policy, 2(1), 1–23. doi:10.1186/2193-9004-2-1

- Ziliak, J. P. (2003). Income transfers and assets of the poor. Review of Economics and Statistics, 85(1), 63–76. doi:10.1162/003465303762687712