ABSTRACT

The paper investigates the economic performance of Czech electro-engineering companies in relation to their tier, ownership, size, level of specialization, and host region in order to scrutinize one of the key assumptions about functional upgrading, namely that lead firms and higher tier suppliers capture more value than lower tier suppliers. This issue has fundamental policy implications, as global value chain (GVC)/global production network (GPN) policy recommendations revolve mainly around two paradigms: to ‘plug-in’ into GVC/GPN and to ‘move-up the chain’, meaning to upgrade functionally. The paper contributes to the GVC/GPN literature by scrutinizing the underinvestigated electro-engineering industry, accounting for variegated levels of specialization of particular companies in the industry, combining sectoral and regional perspectives (i.e. the modes of strategic coupling), and providing disaggregated data for individual companies instead of values aggregated by tiers. The results show large variation in the economic performance of individual companies, yet ownership and tier are the key factors driving economic results. Companies operating outside the production networks performed strongly in terms of profitability, while maintaining the same level of wages as other domestic companies in the electro-engineering industry. Thus, the authors conclude that ‘plug-in’ imperative should be carefully considered within specific industrial and regional contexts.

Introduction

In recent decades, innovations in the transport and communication technologies, and liberal reforms in advanced countries triggered significant transformation processes in the global economy (Dicken Citation2014). As international trade becomes cheaper and easier, and as production is dispersed geographically under the paradigm of vertical disintegration of production (Feenstra Citation1998), firms no longer produce an entire product alone. Instead, global production networks (GPNs), defined as organizational platforms through which various firm and non-firm actors in different regional and national economies compete and cooperate (Yeung & Coe Citation2015), have become widespread in recent decades. However, not all global production networks are literally ‘global’. Instead, many networks are embedded in a macro-region and are therefore ‘regional production networks’. Moreover, the recent COVID-19 pandemic is likely to strengthen the trend towards regionalization of production networks even further. Nevertheless, we (the authors of this paper) prefer the term ‘global production networks’ as well as ‘global value chains’ (GVCs), as these are widely used in the literature. Global production networks impart competitiveness and innovation to transnational companies by enabling access to, for example, low-cost production factors, new markets, and specialized knowledge. Engagement in production networks is also important for lower tier companies, as it enables access to new and voluminous markets, offers potential for learning, and provides upgrading opportunities within a chain/network (Coe et al. Citation2004; Blažek Citation2016). However, Werner and Blair’s disarticulation perspectiveFootnote1 unravelled the dark side of engagement of companies and territories in GVCs/GPNs (Bair & Werner Citation2011).

Thus, GVC/GPN framework highlights the strongly variegated role of companies and territories in the global economy and illuminates numerous causal mechanisms leading to uneven development. Overall, the role of a particular company is seen as a function of its position within the network/chain (Johns Citation2006; Shin et al. Citation2009; Citation2017). In this regard, an especially useful tool is the concept of tiers, which refers to the structuring of suppliers into segments according to the predominate nature of their business activities (Thoburn & Takashima Citation1992). Generally, the position of a company in a higher tier in the production network is considered more rewarding, as it implies preoccupation with higher value-adding activities based on specialized assets and innovation (Isaksen & Kalsaas Citation2009; Pavlínek & Ženka Citation2016; Szalavetz Citation2017). Thus, a higher tier grants the supplier an advantageous bargaining position in relation to its key buyers, and makes the company less replaceable. This motivates lower tier suppliers to ‘move-up the chain’. However, the extent to which higher tier suppliers outperform lower tier suppliers in terms of their financial indicators remains an empirical question or even the ‘Achilles’ heel’ of the upgrading literature (Tokatli Citation2013). Moreover, Gereffi (Citation2019) warns against false homogeneity and false heterogeneity in case of upgrading stages and tiers, and suggests the need to further investigate these broad categories. It is this substantial research gap that we intended to address by investigating the relationship between the economic performance of companies and their tier, while testing the significance of other key variables that might also impact the economic results of companies such as their ownership, size, level of specialization and type of host region. For the study on which this paper is based, we selected the important, yet under-researched, electro-engineering industry in Czechia.

This article has two objectives. The first objective is to investigate the relationship between the economic performance of companies, their tier, and number of other key variables that might also affect their economic results, such as their specialization/diversification, ownership, size, and region. The second objective is to investigate the distinctions in the mode of strategic coupling of electro-engineering companies among the 14 self-governing NUTS 3 regions of Czechia.Footnote2

The article is organized as follows. First, we introduce the conceptual framework for our study. At the end of the section, two research questions are presented. Next, we provide a brief outline of the historical development of the Czech electro-engineering industry and of its current structure. In the following section, the data and methodology applied in the research are explained. The empirical section describes the key findings of our study. We conclude by summarizing our main arguments and outlining possible pathways for future research.

Conceptual framework

Theories of global value chains (GVCs) and global production networks (GPNs) represent a comprehensive conceptual framework that can be used to explain the organization of production in the current globalized economy. The GVC approach examines the firm-level governance of vertically structured production systems, and the distribution of power within the chain, with implications for value creation and capture (Gereffi et al. 2005). By contrast, the GPN perspective acknowledges the role of cultural, social, and political environments in which the particular production processes are embedded (Alexander Citation2018) and can be applied when investigating various modes of strategic coupling that drive regional development (MacKinnon Citation2012; Coe & Yeung Citation2015). Still, the two theories have significant overlaps and amplify each other organically (Alexander Citation2018). Therefore, while we acknowledge the distinctive contributions of the two theories, we use the abbreviation GVC/GPN to reflect mutual amplification and growing coherence between them.

Despite the growing number of industries and services studied within the framework represented by GVC/GPN theories, the study of the electro-engineering sector (Afewerki et al. Citation2019; Hansen et al. Citation2021) has been neglected so far (Lema et al. Citation2011; Elola et al. Citation2013; Pimentel & Flores Citation2016), with the exception of a renewables.

A fundamental claim of the GVC/GPN framework is that production networks are organized hierarchically with a tiered supplier structure that is orchestrated by a lead firm (Thoburn & Takashima Citation1992). Generally, suppliers are categorized into tiers based on their competence, capabilities, and the level of sophistication of their production. In addition to lead firms, usually three or four tiers of suppliers are identified in most manufacturing industries. However, we emphasize that the structuring of suppliers into tiers is an abstraction and that there is significant diversity in the production portfolios of companies of the same tier, especially those of the larger suppliers (Gereffi Citation2019). Moreover, the classification of companies into particular tiers is far from straightforward, as the higher tier suppliers often also perform activities typical of lower tier suppliers. Nevertheless, in line with the voluminous literature, we still maintain that tier reflects the character of companies’ production. Therefore, one should anticipate differences in economic performance of companies of particular tiers, as also suggested by the authors of numerous studies of functional upgrading (for a critique, see Ponte & Ewert Citation2009; Tokatli Citation2013; Blažek Citation2016; Gereffi Citation2019).

In addition to tier, companies also differ substantially based on other key characteristics such as ownership (foreign, domestic, mixed), size (small, medium, large), and their focus (specialization) within the electro-engineering industry (Coe et al. Citation2004). For our research, two distinctive contributions of the GPN stream are crucial. First, the theorization of the major causal drivers of GPN evolution, namely cost-capability ratio, market imperative, and financial discipline of companies (Yeung & Coe Citation2015). The notion of optimizing cost-capability ratios explains why certain business activities are outsourced to other companies and why the mix of these activities evolves over time (Yeung & Coe Citation2015). While the focus on cost as a fundamental driver of global production is widespread, cost needs to be intertwined with the capabilities of the firm, thus making cost a relative concept (Yeung & Coe Citation2015). Therefore, we argue that the tier of suppliers reflects, among other things, their specific cost-capability ratios. Market development has been defined by Yeung & Coe (Citation2015) as an iterative process in which both producers and customers shape and create markets. We argue that the nature of market imperative differs substantially according to a number of key characteristics of companies. The third causal driver, financial discipline, has been defined by Yeung & Coe (Citation2015) as the transformative imperative in which financial considerations, such as market valuation and shareholder value paradigm (Milberg Citation2008), drive the strategies of the firm.

The second major contribution of the GPN school is conceptualization of the notion of strategic coupling (Coe et al. Citation2004), which is defined as ‘a mutually dependent and constitutive process involving particular ties, shared interests, and cooperation between two or more groups of economic actors who otherwise might not act in tandem to achieve a common strategic objective’ (Yeung Citation2016, 54). The mode and type of strategic coupling is widely recognized as an important mechanism in shaping the possibilities of the economic upgrading of firms and regions. It is therefore an important driver of uneven development in general (Coe et al. Citation2004). In our view, the modes of strategic coupling can be usefully interlinked with the GPN triad of casual drivers, as defined by Yeung & Coe (Citation2015). For the sake of brevity, we have outlined the relationships between GPN casual drivers, modes of strategic coupling, and other key characteristics of companies in a tabular form (). shows that each mode of strategic coupling can be typified by the specific nature of particular GPN casual drivers. While connecting the modes of strategic coupling and individual GPN casual drivers is relevant in terms of further conceptual development of the GPN framework, it can also serve as inspiration for the design of policies aimed at repositioning regional companies into more favourable mode of strategic coupling. For example, the nature of market capabilities of companies (as conceptualized by the market development casual driver) differs substantially among various modes of strategic coupling, which can be contemplated by both companies and policymakers in their struggle to achieve a more favourable mode of strategic coupling.

Table 1. The relationships between GPN casual drivers, modes of strategic coupling, and other key characteristics of companies (based on Coe & Yeung Citation2015; Yeung & Coe Citation2015)

Consequently, our analysis of the economic performance of electro-engineering companies according to tier and number of other key variables that might also affect their economic results, such as ownership, level of specialization, and region (mode of strategic coupling) represents the backbone of our study. We pose two research questions. First, what relationships exist between the economic performance of companies and (1) their level of involvement in GVCs/GPNs, (2) the level of specialization/diversification of their production portfolio among the various branches of electro-engineering, (3) their participation in other industrial branches, and, in case of companies engaged in GVCs/GPNs, (4) what relationship exists between their economic performance and their position (tier) when the significance of other key variables, such as their ownership, level of specialization, region, and size, is tested? Second, can distinctions in the mode of strategic coupling of electro-engineering companies among the 14 self-governing regions of Czechia be identified?

Brief history of electro-engineering in Czechia and its current structure

The electro-engineering industry specializes in the development, production, and installation of electric power systems (nuclear, coal and gas, wind, water, solar, cogeneration power plants, and transmission/distribution systems) and their components. The global electro-engineering market is highly diversified but is based mainly on the high level of technological competence of the largest firms within the same industry (George et al. Citation2005). Unlike the automotive or the consumer electronics industry, in which the end market consists of voluminous categories of customers, the electro-engineering industry, with the exception of photovoltaics, is characterized by a low-batch nature of production. However, the products themselves encompass a large number of sophisticated subsystems and components. In this respect, the electro-engineering industry resembles the aircraft industry (Heerkens et al. Citation2010; Blažek et al. Citation2021). Electro-engineering is a typical producer-driven, technology-intensive industry, and may have an important impact on regional development by creating jobs for highly qualified labour, attracting significant foreign direct investment (FDI), and integrating numerous supporting industries. In recent decades, the global electro-engineering industry has been strongly influenced by the shift from carbon fuels (oil, gas, coal) to renewables.

Czechia is one of the first countries where the electro-engineering industry emerged in the late 19th century. For example, E. Škoda built his first turbine in the year 1904. Already before World War I, the Czech electro-engineering companies were technological leaders, and the demand for electrical equipment increased rapidly after World War I (Kubín Citation2009). After World War II, the communist government, which seized power in 1948, prioritized heavy industries, including electro-engineering, to build the economic base of the ‘socialist camp’ (i.e. the then USSR and its Central and Eastern Europe satellites). Domestic and foreign-owned companies were nationalized and merged into vast conglomerates, and research and development (R&D) activities were centralized (Kubín Citation2009). Intensive construction of nuclear power plants, particularly in socialist countries, opened new opportunities for the Czech electrical companies, especially for Škoda Plzeň.

After the collapse of state socialism in 1989, the industrial tradition of Czechia, its geographical proximity to the core markets, and its relatively cheap but qualified labour played a crucial role in transforming the Czech electro-engineering companies and their engagement in GPNs. The old industrial linkages among companies were broken in the early 1990s, and a critical drop in the production occurred due to the collapse of some its branches, especially production of nuclear power systems (Kubín Citation2009). After profound restructuring, the Czech electro-engineering returned to a growth trajectory in 1994 with the help of large inflows of foreign capital, especially from Germany. For example, Siemens employs more than 7000 people in Czechia (Tramba Citation2021).

To summarize, the electro-engineering industry in Czechia underwent a series of fundamental ruptures (both World Wars, nationalization in 1948, privatization after 1989), and was subject to the significant role of foreign-owned companies, except during the command economy phase. Today, the Czech electro-engineering industry is strongly globalized, with foreign contracts comprising c.70% of the total contract amount (CzechTrade Citationn.d.).

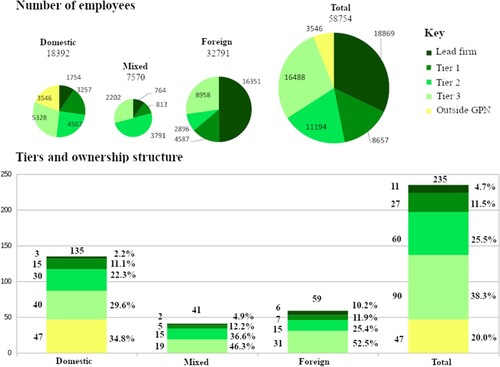

In 2018, the Czech electro-engineering industry consisted of 235 firms, of which 135 were domestic (57.5%), 41 were jointly owned (17.5%), and 59 were foreign-owned (25%).Footnote3 The industry employed c.59,000 (58,754) people, 28% (16,351) of whom were employed by foreign-owned lead firms (). We identified 47 firms (20%), all domestic, which are not to any substantial extent involved in GPNs, but that instead develop and manufacture products according to specification of particular, often one-off, customers. For example, BV Elektronik Ltd. in Eastern Bohemia manufactures several thousand items, such as various transformers or self-induction coils, according to the needs of various customers. Foreign companies and firms with mixed ownership dominate, especially among the lead firms (67%). Surprisingly, a significant number of the first-tier suppliers are small or medium-sized companies. This could be due to two industry-specific reasons: first, the production is heavily automated, especially in photovoltaics (Korsnes Citation2019; Renewable Energy World Citationn.d.); second, small firms that operate as first-tier suppliers are often focused on production of small energy generation units, such as wind farms or cogeneration units. Most foreign-owned third-tier companies are large firms typically engaged in labour-intensive production of specialized armatures or cables. By contrast, domestic third-tier companies tend to be small and medium-sized enterprises (SMEs) mainly focused on the production of components for transmission-distribution-warehousing (TDW) equipment.

Fig. 1. Number of employees and structure of the Czech electro-engineering companies according to ownership and tier in 2018 (based on data accessed from Merk.cz’s online database in July 2020)

Most firms (120, 51%) are involved in the production of transmission-distribution-warehousing (TDW) equipment, and systems for coal or gas power plants (76, 33%). While a slight majority of companies are engaged in at least two electro-engineering branches, 110 firms (47%) are involved only in a single branch. The most frequent combinations found were between nuclear and coal or gas (27 firms), solar and TDW (27), coal or gas and TDW (21), coal and gas, and water (19), and nuclear and water systems (17). In terms of cross-industry business activities, only 56 companies are engaged mainly in electro-engineering, of which 34 produce exclusively for one of the seven investigated electro-engineering branches. A total of 176 electro-engineering firms operate in one, two, or three industries outside electro-engineering, such as in the oil and gas industry (48), metalworks (47), consumer electronics (46), automotive (33), and chemicals (21). For examples of products manufactured by suppliers of particular tiers, see .

Table 2. Typology of electrical engineering components used for classification of suppliers into tiers

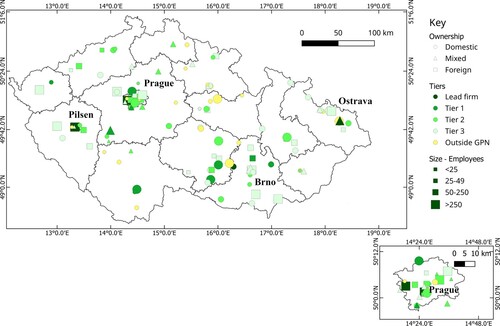

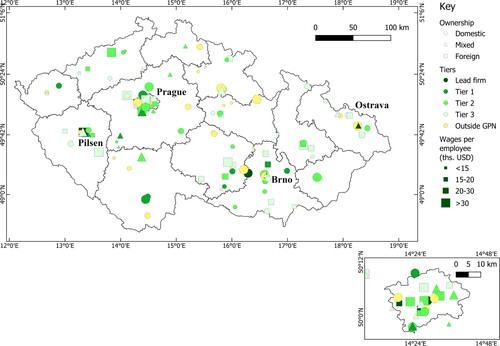

Geographically, even though we found electro-engineering firms in all 14 Czech self-governing NUTS 3 regions, most companies are concentrated in Prague in the Central Bohemian Region, the Pilsen Region, the South Moravian Region (in which the city of Brno is located), and the Moravia-Silesian Region (in which the city of Ostrava is located) ().

Fig. 2. Regional distribution of the Czech electro-engineering companies in 2018 (based on data accessed from Merk.cz’s online database in July 2020)

Data and methodology

The first step of our research was to create a database of Czech electro-engineering companies.Footnote4 Most (140) of the 235 firms/companies were identified from the supplier database of the Czech business development agency CzechInvest and from the Czech Register of Economic Subjects/Entities (ARES), which is maintained by the Czech Ministry of Finance. We selected companies belonging to the Classification of Economic Activities (CZ-NACE) categories 27110 – production of electrical motors, generators, transformers, 27120 – production of electrical distribution and control equipment, and 27320 – production of electrical conductors and cables. Additional companies were identified using the subcontractor listings on the websites of the major electro-engineering companies. Altogether, 235 firms were identified as being involved in the electro-engineering industry. Financial data for 127 of the 235 firms on our list were accessed from Merk.cz’s online database, while the general statistical information for the Czech electro-engineering industry was sourced from the Register of Economic Subjects (RES) online database, accessed July–October 2020 via by the official website of the Czech Statistical Office (ČSÚ).

Next, the companies’ websites were analysed to scrutinize their production portfolios, which often span other industries. Subsequently, the companies were categorized into lead firms and three tiers of suppliers. In line with methodology used by Pavlínek & Janák (Citation2007), the companies were assigned to a particular tier according to the most sophisticated/complex product they produce (for an overview of products and components used for classification of suppliers, see ). We distinguished six main types of power generation firms: nuclear, coal and gas, hydro, wind, solar, and cogeneration. We also distinguished between firms oriented by transmission, distribution, or warehousing. At the same time, we investigated whether a firm was involved in GVCs/GPNs. We acknowledge that it is not straightforward to identify whether or not a company is engaged in a GPN. Despite the relatively high number of companies in our dataset, we investigated companies on a case-by-case basis, using their websites and available annual reports. Fortunately, our examination showed (in line with the observation by Ivarsson & Alvstam Citation2011) that businesses tend to publicize the information about their customers, especially in case of well-known companies such as lead firms or higher-tier suppliers, as such information serves as a valuable reference for new clients. Except for lead firms, a company was considered as involved in global production networks if it mainly supplied components or subsystems to other companies. By contrast, if the business strategy of a given company rested predominantly on developing and manufacturing products according to the specifications of particular, often one-off, customers, it was considered as not involved in GPNs.

While we were able to gather non-financial characteristics for 235 companies, financial information for only 127 companies (54%) was available in the Merk database for the investigated seven-year period (2012–2018) that covered a phase of a relative growth and stability. Consequently, only those companies were included in the analysis of the firms’ economic indicators. To analyse the role of financial discipline (Yeung & Coe Citation2015) in the economic performance of companies, we investigated the companies’ websites, and we examined their annual reports to determine which companies were listed on a stock market (either the Prague Stock Exchange or foreign stock exchanges). Altogether, shares of 21 companies were traded on a stock market.

We used eight indicators to capture the economic performance of electro-engineering companies. Four of the indicators were absolute – turnover, gross profits, value added, and personnel costs, and based on them, we calculated four relative indicators: profit-turnover ratio, personnel cost-turnover ratio, value added per employee, and wages per employee.

Economic performance of electro-engineering firms in Czechia

The most decisive factor influencing the economic performance of companies proved to be ownership. While the domestic companies dominate in numbers, they underperform significantly in absolute economic indicators such as turnover, gross profit, and added value, reflecting their smaller size compared with foreign-owned companies. However, when we investigated relative indicators (i.e. profit-turnover ratio, personnel costs-turnover ratio, value added per employee, and wages per employee), the differences between foreign and mixed companies and domestic companies were not very large ( and ).

Table 3. The key absolute economic performance indicators according to firms’ ownership and position in the global production networks (GPNs) – mean and median values for the period 2012–2018 (thousand USD) (Source: data accessed from Merk.cz’s online database in July 2020)

Table 4. The key relative economic performance indicators according to firms’ ownership and position in the global production networks (GPNs) – mean and median values for the period 2012–2018 (thousand USD) (Source: data accessed from Merk.cz’s online database in July 2020)

While the absolute indicators differed statistically significantly across tier, ownership, and according to size, three of the four relative indicators (added value per employee, wages per employee, and personnel costs-turnover ratio), differed statistically significantly only in relation to tier. Only the fourth relative indicator (personnel costs-turnover ratio) differed both in relation to tier and ownership. Thus, surprisingly, the relationship between ownership and the rest of relative financial indicators proved to be not statistically significant, similarly to the profit-turnover ratio in relation to tier, and to firms’ size in relation to all relative indicators. Correlation analysis with the firms divided into two categories – those involved in GPNs and the rest – revealed that companies outside GPNs had statistically a significantly higher personnel costs-turnover ratio. Firms engaged in GPNs also tended to show statistically significantly higher values of absolute economic indicators (turnover, added value) than uninvolved firms, due to the fact that GPN suppliers are usually larger than companies outside production networks. However, there was no statistically significant difference between these two categories of companies in terms of their gross profits.

The results of our statistical analysis of the relationships between economic indicators of companies and their tier, ownership, size, financial discipline (proxied by the listing of companies’ shares on a stock market) and level of specialization were as follows. As our data were not normally distributed, we used the non-parametric Kruskal-Wallis test to examine dependencies between categorical variables and absolute and relative economic indicators. provides an overview of the statistically significant relationships (alpha = 0.05) between firms’ basic characteristics (i.e. independent variables) and the economic indicators. Unlike tier, ownership, size, and financial discipline, the level of specialization of a firm did not exhibit any statistically significant difference; therefore, these results are not shown in .

Table 5. The relationships between economic performance indicators and ownership, tier, and size, tested by Kruskal-Wallis tests (N = 127 (Source: data accessed from Merk.cz’s online database in July 2018)

As expected, all four characteristics (tier, ownership, size, and financial discipline) were statistically significant in relation to all absolute indicators of economic performance (turnover, profit, and added value). This reflects the fact that lead firms and higher tier suppliers tend to be large foreign-owned companies, which are usually listed on a stock market. The differences according to tiers (as well as financial discipline) were statistically significant also in relation to added value per employee and wages per employee; higher tier firms reported much better results than lower tier suppliers. However, in case of lead firms, median values of their relative economic indicators differed substantially according to ownership, as foreign-owned lead firms are much more profitable than domestic lead firms and tended to report higher added value (but did not pay higher wages).

Overall, we observed significant differences between mean and median values, which reflect the influence of outliers (both very low and very high individual values) within the investigated categories. For example, while the total profit-turnover ratio and the added value per employee for lead firms and third-tier foreign-owned suppliers had negative means, their median values, which were much less sensitive to outliers, were much more favourable.

Finally, the correlation analysis yielded a positive statistically significant relationship between tier and firm’s size, ownership, and listing on the stock market (Spearman coefficients were .236, .246, and .247 respectively). Thus, large foreign-owned companies tended to hold higher positions in the (GPN) and were often listed on the stock market (). There was no dependency (-.001, p-value = 0.988) between tier and involvement of the company in the other branches of electro-engineering or engagement outside the electro-engineering sector (-.070, p-value = 0.437). The larger firms tend to be active in several branches of electro-engineering (0.214) as well as in other industries (0.219).

Table 6. Correlation analysis of the relationships between the firms’ characteristics and their economic performance for the period 2012–2018 (N = 127)

There was a weak negative relationship (-.241, p-value = 0.06) between tier and level of specialization in electro-engineering industry. Lower-tier firms tended to have more diversified production. This was confirmed by the Kruskal-Wallis test (p-value = 0.001), which yielded statistically significant differences among tiers in relation to the level of specialization. Thus, the third-tier suppliers (81.6% of which are, perhaps counterintuitively, medium and large companies) tended to be less specialized in electro-engineering in comparison with higher tier firms, and they tended to supply other industries outside electro-engineering. However, we did not find any statistically significant relationship between the level of specialization and economic performance of companies. Like the Kruskal-Wallis test, the correlation analysis revealed that employees in the higher tier companies tended to earn higher wages and produce more added value in comparison with those in lower tier firms. In terms of ownership, domestic firms spent significantly more on their staff in relation to their turnover than companies with mixed and foreign ownership.

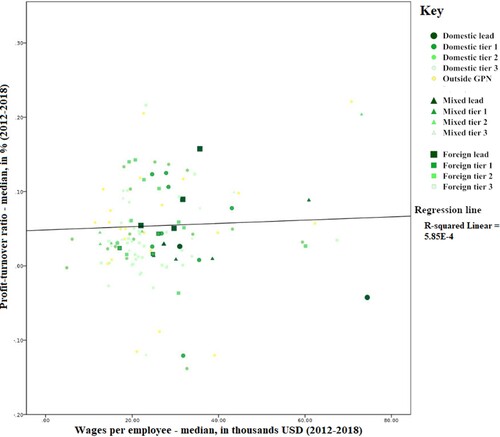

As shown in , added value per employee correlated significantly with profit-turnover ratio (0.420), and wages per employee were related to added value per employee (0.781) (the relationship is also shown in ). However, wages per employee had a negative relationship with personnel costs-turnover ratio (-0.266). This suggests that some companies tend to rely on a large pool of a relatively low-skilled labour. However, there was significant variation among individual companies (also shown in ).

Fig. 5. Relationship between profit-turnover ratio and wages per employee for the period 2012–2018 based on data accessed from Merk.cz’s online database in July 2020)

The correlation analysis revealed that companies that traded on a stock market, and hence operated under the shareholder value paradigm, tend to be larger, foreign-owned and higher tier firms, typified by high added value and lower personnel cost-to-turnover ratio, even though the average wages of their employees were higher. This suggests that companies operating under the shareholder value paradigm (Milberg Citation2008) specialize in capital-intensive production, thus requiring less, but highly qualified and well-paid labour. By contrast, those companies’ profit turnover ratio did not differ significantly from companies operating outside a stock market.

Like the Kruskal-Wallis tests, the correlation analysis revealed a statistically significant relationship between tier and absolute indicators (turnover, gross profit, and added value), where higher tier firms, which usually were large and foreign-owned, showed higher values than lower tier suppliers (correlation between size and foreign ownership 0.375, p-value = 0.006). The analysis also yielded a strong positive relationship between a firm’s size and absolute profits (0.468, p-value = 0.00), and size and added value (0.869, p-value = 0.00). Additionally, the analysis revealed that the higher the number of electro-engineering branches a particular firm supplied, the higher the number of industries outside electro-engineering it also served (0.263) (). The examination of individual branches of electro-engineering (e.g. nuclear, coal, gas) revealed only a few statistically significant dependencies between economic performance indicators and explanatory variables. We assume that the inconclusive results of our analysis of particular branches of electro-engineering could be due to the relatively small number of companies in particular branches.

Our examination of the modes of strategic coupling of electro-engineering companies according to Czech regions followed the examination conducted by Coe & Yeung (Citation2015). They posit that modes of strategic coupling differ in two key dimensions: the level of autonomy or external dependency of companies, and the nature of regional assets (distinctive or generic). Accordingly, we investigated not only the differences between regions in terms of the economic performance of nested companies, but also the differences in their ownership (reflecting the level of external dependency) and tier. In line with Coe & Yeung (Citation2015), we assume that higher tier suppliers use distinctive assets, while lower tier suppliers rely on generic assets. We did not find many significant differences between the regions in their mode of strategic coupling, with the exception of the Central Moravian Region (which includes Prague) and the South Moravian Region, both of which command a distinctive manufacturing tradition and specialized regional assets (). Moreover, the current mode of strategic coupling of electro-engineering firms in Czech regions does not fit neatly into the ideal modes of strategic coupling. Instead, their characteristics position them somewhere between assembly platforms of the structural mode of strategic coupling (typified by generic regional assets and external dependency) and international partnership of the functional mode of strategic coupling (typified by distinctive regional assets and some regional autonomy (Coe & Yeung Citation2015)). This may represent a window of opportunity for electro-engineering companies in Czech regions to move gradually towards a more favourable mode of strategic coupling (i.e. to the functional mode), provided the strategic effort of companies is supported by public institutions to enhance the assets of respective regions (Breul et al. Citation2019).

Conclusions

In this paper we have aimed to contribute to the GVC/GPN literature, based on our study of the economic performance of electro-engineering companies in relation to their respective tiers, in which we also investigated the significance of other key variables such as ownership, size, level of specialization, and host region. To date, the predominant assumption in the upgrading literature is that higher tier suppliers perform better than lower tier suppliers, with subsequent policy imperatives to ‘move up the chain’ and thus to couple with GPNs in a more favourable mode. The main empirical findings can be summarized as follows.

First, companies that were not integrated into the production networks to any significant extent (all of them were small domestic firms) tended to allocate a higher share of their turnover to personnel costs. They generally reported a higher profit-turnover ratio than all other categories of companies, except foreign-owned lead firms. This finding suggests that in certain cases companies might more favourably operate outside the production networks. Consequently, the ‘plug-in’ imperative should be carefully considered within the specific industrial and regional context.

Second, our analysis of the characteristics of companies (tier, ownership, specialization, and size) that could affect their economic performance revealed that two major factors drove the economic performance of companies – tier and ownership. In particular, foreign firms outperformed domestic companies on both relative and absolute economic indicators.

The analysis of the economic performance of companies according to tier revealed that higher tier firms tended to report higher added value per employee and higher wages compared with lower tier suppliers. However, the analysis according to tier did not yield any statistically significant differences in profit-turnover ratio. Even though profit maximization is often regarded as the raison d'être for the existence of companies, these results suggest a need to investigate a broader spectrum of economic indicators beyond profit, such as those covering value creation and value capture (Coe & Yeung Citation2015).

We also found that companies operating under the financial discipline of the shareholder value paradigm (Milberg Citation2008; Yeung & Coe Citation2015) tended to rely on less, but highly qualified and well-paid labour, which reflected their specialization in capital-intensive and high value-added production. However, their profit turnover ratio did not differ significantly from companies operating outside a stock market.

While our analysis of the role of companies’ size revealed a significant relationship on all absolute indicators, none of relative indicators proved to be significantly related to size. Thus, in the case of Czech electro-engineering companies, ownership and tier proved to be the key drivers of their economic performance. These results are broadly in accordance with the findings of Pavlínek & Ženka (Citation2016) relating to the Czech automotive industry, the most studied Czech industry within the GPN framework. However, in contrast to the automotive industry, where the economic performance of companies tends to improve neatly towards the top of GPN pyramid, our research of the electro-engineering industry revealed a more complicated pattern ( and ). While in the automotive industry the vast majority of assemblers and first-tier suppliers are foreign-owned, domestic firms in the electro-engineering industry enjoy a better position.

Next, we investigated the mode of strategic coupling of electro-engineering companies typified by their level of external dependency and by generic or distinctive nature of their assets. Our study did not reveal any substantial differences among the 14 Czech regions. The prevailing mode of strategic coupling can be characterized as between assembly platforms (structural mode) and international partnership (functional mode) which suggests a possibility to reposition Czech electro-engineering companies towards the functional mode by a concerted effort of companies and both regional and national-level policies (Breul et al. Citation2019).

In our effort to make a conceptual contribution to GVC/GPN theory, we combined the modes of strategic coupling with three main GPN casual drivers (Yeung & Coe Citation2015) and specified the envisaged prevailing features of companies operating in regions in all three modes of strategic coupling. Thus, in we have outlined the relationships between modes of strategic coupling, GPN causal drivers, and the key characteristics of companies, such as ownership, tier, level of specialization, and size. Nevertheless, we were able to operationalize directly only one of GPN causal drivers (financial discipline). Thus, we believe that operationalization of remaining two causal drivers represents an important research challenge not only within GVC/GPN studies but also in comprehending the key mechanisms of uneven development in general.

Overall, our study documented a widely acknowledged fact, yet one that is often disregarded in the policy arena, namely that there is profound variation in the economic performance of companies with the same features (e.g. tier, ownership, region) (). While such differences are hardly surprising, we wish to underscore that the scale of the variation is such that it requires careful consideration in policy design. Thus, seemingly obvious and straightforward policy implications (such as to ‘move up the chain’) may be highly relevant in some cases but can be unjustified or even counterproductive in other cases and settings. The need for sensitivity in public policies for industrial and regional contexts has been recently emphasized by a study of the Czech aerospace industry (Blažek et al. Citation2021), which revealed that lead firms and higher tier suppliers tended to reach a higher level of value capture, yet not a higher level of profitability. Importantly, that study revealed that companies remaining outside the production networks performed strongly in terms of profitability, while maintaining the same level of wages as other domestic companies in the Czech aerospace industry. This supports the argument about the harsh profit squeeze on GVC/GPN suppliers by their powerful customers (Isaksen & Kalsaas Citation2009).

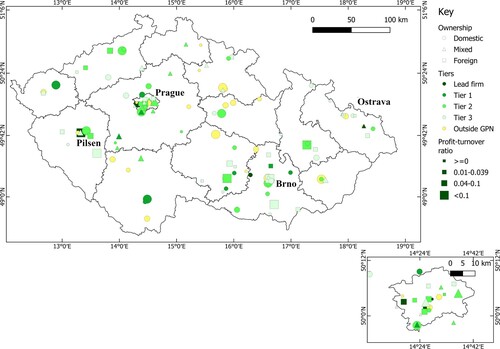

Fig. 3. Regional distribution of firms’ profit-turnover ratio, median values for the period 2012–2018 (in %) (based on data accessed from Merk.cz’s online database in July 2020)

Fig. 4. Regional distribution of firms’ wages per employee, median values for the period 2012–2018 (thousand USD) (based on data accessed from Merk.cz’s online database in July 2020)

The analysis in our study was limited to a mere seven-year long snapshot of the economic performance of companies and, therefore, did not allow us to capture the evolutionary (repositioning) dynamics of the investigated companies and the resulting changes in their economic performance. Nevertheless, our results concur with those reported in a recent study by Szalavetz (Citation2017), who shows that companies that succeeded in functional upgrading frequently did not improve their economic performance. Thus, it might well be the case, as argued by Sako & Zylberberg (Citation2019, 699), that ‘investments in upgrading are simply the price of sustained admission to a GVC’. Overall, our study was limited to one industry in a single country, and, thus, research of key drivers of economic performance of companies across much wider spectrum of industries and regions would help to enhance our understanding of global production and its effects on regions as well as to design sound policy implications.

Acknowledgements

The authors wish to thank the editors and both referees for encouraging and insightful feedback on an earlier version of this paper.

Notes

1 The disarticulation perspective represents an approach sensitive to processes of accumulation, disinvestment, and dispossession that produce and reproduce uneven development (for more information see Werner & Bair Citation2019).

2 The NUTS classification (from the French La Nomenclature des Unités Territoriales Statistiques) is a fundamental tool for providing statistical information to the European Union. In Czechia, NUTS 3 refers to regions (i.e. to 14 higher territorial self-governing units).

3 All statistics relating to the studied companies/firms were accessed from Merk.cz’s online database in July 2020.

4 In this paper, the terms ‘company’ and ‘firm’ are treated as synonymous.

References

- Afewerki, S., Karlsen, A. & MacKinnon, D. 2019. Configuring floating production networks: A case study of a new offshore wind technology across two oil and gas economies. Norsk Geografisk Tidsskrift–Norwegian Journal of Geography 73(1), 4–15.

- Alexander, R. 2018. Sustainability in global production networks – Introducing the notion of extended supplier networks. Competition & Change 22(3), 255–273.

- Bair, J. & Werner, M. 2011. Commodity chains and the uneven geographies of global capitalism: A disarticulations perspective. Environment and Planning A 43(5), 988–997.

- Blažek, J. 2016. Towards a typology of repositioning strategies of GVC/GPN suppliers: The case of functional upgrading and downgrading. Journal of Economic Geography 16(4), 849–869.

- Blažek, J., Bělohradský, A. & Holická, Z. 2021. The role of tier, ownership and size of companies in value creation and capture. European Planning Studies 29(11), 2101–2020.

- Breul, M., Revilla Diez, J. & Sambodo, M.T. 2019. Filtering strategic coupling: Territorial intermediaries in oil and gas global production networks in Southeast Asia. Journal of Economic Geography 19(4), 829–851.

- Coe, N.M & Yeung, H.W.-C. 2015. Global Production Networks: Theorizing Economic Development in an Interconnected World. Oxford: Oxford University Press.

- Coe, N.M., Hess, M., Yeung, H.W.-C., Dicken, P. & Henderson, J. 2004. ‘Globalizing’ regional development: A global production networks perspective. Transactions of the Institute of British Geographers 29, 468–484.

- CzechTrade. n.d. Electronics in the Czech Republic. https://www.czechtradeoffices.com/d/.www.czechtradeoffices.com/sector%20publications/Electronics-2018.pdf (accessed 15 November 2022).

- Dicken, P. 2014. Global Shift: Mapping the Changing Contours of the World Economy. 7th ed. New York: Guilford Publications.

- Elola, A., Parrilli, M.D. & Rabellotti, R. 2013. The resilience of clusters in the context of increasing globalization: The Basque wind energy value chain. European Planning Studies 21(7), 989–1006.

- Feenstra, R. 1998. Integration of trade and disintegration of production in the global economy. Journal of Economic Perspectives 12(4), 31–50.

- George, K., Joll, C. & Lynk, E.L. 2005. Industrial Organization: Competition, Growth and Structural Change. 4th ed. Abingdon: Routledge.

- Gereffi, G. 2019. Economic upgrading in global value chains. Ponte, S., Gereffi, G. & Raj-Reichert G. (eds.) Handbook on Global Value Chains, 240–254. Cheltenham: Edward Elgar.

- Hansen, U.E., Nygaard, I. & Maso, M.D. 2021. The dark side of the sun: Solar e-waste and environmental upgrading in the off-grid solar PV value chain. Industry and Innovation 28(1), 58–78.

- Heerkens, H., Bruijn, E. & Steenhuis, H. 2010. Common factors in the withdrawal of European aircraft manufacturers from the regional aircraft market. Technology Analysis & Strategic Management 22, 65–80.

- Isaksen, A. & Kalsaas, B.T. 2009. Suppliers and strategies for upgrading in global production networks: The case of a supplier to the global automotive industry in a high-cost location. European Planning Studies 17(4), 569–585.

- Ivarsson, I. & Alvstam, G. 2011. Upgrading in global value-chains: A case study of technology-learning among IKEA-suppliers in China and Southeast Asia. Journal of Economic Geography 11(4), 731–752.

- Johns, J. 2006. Video games production networks: Value capture, power relations and embeddedness. Journal of Economic Geography 6, 151–180.

- Korsnes, M. 2019. Wind and Solar Energy Transition in China. New York: Routledge.

- Kubín, M. 2009. Proměny České energetiky: historie, osobnosti, vědecko-technický rozvoj. Prague: Český svaz zaměstnavatelů v energetice.

- Lema, R., Berger, A., Schmitz, H. & Song, H. 2011. Competition and cooperation between Europe and China in the wind power sector. IDS Working Paper 377. Brighton: Institute of Development Studies.

- MacKinnon, D. 2012. Beyond strategic coupling: Reassessing the firm-region nexus in global production networks. Journal of Economic Geography 12(1), 227–245.

- Milberg, W. 2008. Shifting sources and uses of profits: Sustaining US financialization with global value chains. Economy and Society 37(3), 420–451.

- Pavlínek, P. & Janák, L. 2007. Regional restructuring of the Škoda auto supplier network in the Czech Republic. European Urban and Regional Studies 14(2), 133–155.

- Pavlínek, P. & Ženka, J. 2016. Value creation and value capture in the automotive industry: Empirical evidence from Czechia. Environment and Planning A 48(5), 937–959.

- Pimentel, R. & Flores, R. 2016. Global Value Chains as a Regional Integration Tool: The Case of Renewables Industry in South America. Technical Report. https://www.researchgate.net/publication/312489189_global_value_chains_as_a_regional_integration_tool_the_case_of_the_renewables_industry_in_south_america (accessed 15 November 2022).

- Ponte, S. & Ewert, J. 2009. Which way is ‘up’ in upgrading? trajectories of change in the value chain for South African Wine. World Development 37(10), 1637–1650.

- Renewable Energy World. n.d. What Traits Define the Best Solar Companies and How to Use These to Find Local Solar Providers? https://www.renewableenergyworld.com/2018/02/08/what-traits-define-the-best-solar-companies-and-how-to-use-these-to-find-local-solar-providers/ (accessed 15 November 2022).

- Sako, M. & Zylberberg, E. 2019. Supplier strategy in global value chains: Shaping governance and profiting from upgrading. Socio-Economic Review 17(3), 687–707.

- Shin, N., Kraemer, K.L. & Dedrick, J. 2009. R&D, value chain location and firm performance in the global electronics industry. Industry and Innovation 16(3), 315–330.

- Shin, N., Kraemer, K.L. & Dedrick, J. 2017. R&D and firm performance in the semiconductor industry. Industry and Innovation 24(3), 280–297.

- Szalavetz, A. 2017. Upgrading and value capture in global value chains in Hungary: More complex than what the smile curve suggests. Szent-Ivanyi, B. (ed.) Foreign Direct Investment in Central and Eastern Europe: Post-Crisis Perspectives, 127–150. Basingstoke: Palgrave.

- Thoburn, J.T. & Takashima, M. 1992. Industrial Subcontracting in UK and Japan. London: Avebury.

- Tokatli, N. 2013. Toward a better understanding of the apparel industry: A critique of the upgrading literature. Journal of Economic Geography 13(6), 993–1011.

- Tramba, D. 2021. Tržby Siemensu v Česku loni klesly o skoro 20 procent, ale ne jen vinou koronaviru. https://ekonomickydenik.cz/trzby-siemensu-v-cesku-loni-klesly-o-skoro-20-procent-ale-ne-jen-vinou-koronaviru/ (accessed 16 November 2022).

- Werner, M. & Bair, J. 2019. Global value chains and uneven development: A disarticulations perspective. Ponte, S., Gereffi, G. & Raj-Reichert, G. (eds.) Handbook on Global Value Chains, 183–198. Cheltenham: Edward Elgar.

- Yeung, H.W.-C. & Coe, N.M. 2015. Toward a dynamic theory of global production networks. Economic Geography 91, 29–58.

- Yeung, H.W.-C. 2016. Strategic Coupling: East Asian Industrial Transformation in the New Global Economy History. Ithaca: Cornell University Press.