?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

Using a global dataset of over 840,000 equity, bond and syndicated loan investment banking deals, we build the fossil fuel investment brokerage profile of financial centres worldwide between 2000 and 2018. We also study whether city-level fossil fuel divestment commitments and country-level green banking policies impact the profile of fossil fuel financial centres over our study timeframe. We find that several financial centres shift their fossil fuel investment brokerage profiles substantially, including the asset classes in which they are active. However, we do not find any evidence that this is driven by city-level divestment commitments. In contrast, we find that fossil fuel investment banking brokers situated in financial centres exposed to voluntary green banking policies reduce their fossil fuel financing. This is driven by foreign brokers whose behaviour appears to signal an anticipation of forthcoming mandatory green finance policies.

INTRODUCTION

The growth of financial and business services (FABS) and the competition among cities to attract FABS firms is well documented (Daniels, Citation1993; Desmarchelier et al., Citation2013; Wójcik et al., Citation2018). The race for cities to establish themselves as financial centres is resolutely global (Pažitka et al., Citation2021). In a context of globalization, financializaton and rapid technological advancement, investment banks have become a strategic cog of financial centres’ infrastructure by claiming a central role in orchestrating global financial flows (Wójcik et al., Citation2018).

Whereas asset owners and managers have received considerable attention in scholarly debates in sustainable finance, investment banks remain a remarkably under-researched and under-appreciated flywheel in financing climate change as well as climate mitigation and adaptation initiatives. Yet recent research suggests that investment banks are key brokers of misaligned finance as they offer substantial debt and equity capital market services to fossil fuel companies and enterprises responsible for major environmental degradation (Cojoianu et al., Citation2021; Urban & Wójcik, Citation2019). Financial geographers have documented widely the key role of investment banks and bankers in the competitiveness of the financial centres from which they operate. In addition, economic geographers have widely acknowledged that cities and regions play a crucial role in the transition to a low carbon economy and the fight against climate change (Jones, Citation2019; Kythreotis et al., Citation2020; Truffer & Coenen, Citation2012).

However, we know very little about the contribution of financial centres in financing the fossil fuel economy. In addition, the research on the geographical contextuality of emerging institutions such as the fossil fuel divestment campaign is in its infancy, and we know little about the geographical scale it operates at and whether it has any effect in shaping fossil fuel brokerage within and between financial centres. Scientific evidence has established that new financing of fossil fuel infrastructure must come to halt and that 20% of existing fossil power infrastructure must be stranded to achieve net zero by 2050 (Pfeiffer et al., Citation2018) in order to stabilize global warming to below 1.5°C (International Energy Agency (IEA), Citation2021). In this respect, defunding fossil fuel business models is vital. As syndicated bank loans (64%), followed by bonds (26%) and equities (10%), are the primary sources of financing for the oil and gas sector (Cojoianu et al., Citation2021), investment banks hold enormous power and responsibility in limiting the sector’s access to capital.

In this paper we aim to bridge these gaps by assessing the extent to which financial centres and their investment bank-led brokerage activities are fuelling the climate crisis. Based on the work of Wójcik et al. (Citation2019), we use the nationality of parent companies of investment bank subsidiaries and the nationalities of their customers to distinguish between domestic, export, import and platform brokerage activities of investment banks across financial centres. By analysing over 840,000 investment banking multi-assets deals from Dealogic between Q1 2000 and 2018, we build a typology of fossil fuel brokerage centres. This allows us to map the distribution of fossil fuel brokers across financial centres and to test our hypotheses of drivers of fossil fuel brokerage at the city level. In particular, we ground the study in institutional theory (Bathelt & Glückler, Citation2014), where we view the effect of the fossil fuel divestment campaign and that of green banking country policies on different types of fossil fuel investment brokerage as emerging institutions.

The remainder of the paper is structured as follows. We next review the relevant literature on fossil fuel finance and position the paper in brokerage theory and related financial geographical work. Next, we proceed to present the data and methodology used in the econometric analysis. The results and discussions follow. Finally we discuss our contribution to the literature and conclude.

THEORETICAL BACKGROUND AND HYPOTHESES

Proven effective in the anti-Apartheid movement, divestment is no new impact investing strategy (Hunt, Citation2017). Yet the movement in response to the climate emergency, which started in 2008 with the US non-governmental organization (NGO) 350.org, represents the fastest growing divestment campaign to date (Cojoianu et al., Citation2021; Hunt, Citation2017), with over US$14 trillion divested.Footnote1 While initially the movement has focused mostly on divesting from secondary market equities and bonds given the exposure of university endowments to such asset classes, more recently the movement has started to target primary market issuances (such as bond issuance and new loan financing) (Cojoianu et al., Citation2021). In addition to the normative divestment movement, which seeks the stigmatization of oil companies and their investors – the most impactful outcome of divestment campaigns, according to Ansar et al. (Citation2013) – we have also witnessed recently a rise in regulatory developments, which are targeted specifically at investors with regard to their climate impact and financing of fossil fuel and green industries. In addition to unveiling a typology of fossil fuel brokerage at the financial centre level for over 400 cities worldwide, we seek to understand whether the financial centre geographical scale is a level at which we could observe the impact of the divestment movement on fossil fuel financial flows, as well as whether fossil fuel investment brokerage activities. In the following sections we frame our paper within the existing brokerage research as well as institutional theory as applied to the fossil fuel sector city-networks.

Cities as fossil fuel financial brokers

Generally, a broker can be defined as an independent intermediary who acts as an agent to facilitate deals for their clients. In the financial industry, a broker is a regulated professional – individual or firm – who, on behalf of their clients, buys and sells assets without having title to the property and charges a fee for their services. Investment banks, central actors of contemporary capitalism, typically provide brokerage services to their clients.

While Truffer and Coenen (Citation2012) note an increased appetite for sustainable development and environmental innovations in regional studies, our review suggests scholars have paid little attention to the role of cities in the brokerage of fossil fuel-related financial flows. Notwithstanding economic geographers’ recent interest in the sustainability–finance nexus (Liu et al., Citation2018), spatially aware scholarship on the role of bankers as fossil fuel finance brokers and the emerging landscape of different fossil fuel brokerage services across financial centres is still relatively underdeveloped.

Historical and case studies-based accounts (Cassis & Wójcik, Citation2018) notwithstanding, most examination of financial activities is either at the national or the enterprise level (Wójcik et al., Citation2019). Wójcik et al. (Citation2018) note that financial centres have become ‘a self-evident preoccupation of financial firms as well as local policy makers’ (p. 2). While large metropolitan areas are often framed as a sustainability challenge (Wheeler, Citation2009), they may actually offer opportunities for bringing together the local political power, financial infrastructure and expertise that is critical in promoting local brokerage of climate aligned financial flows.

Wójcik et al. (Citation2018) define international financial centres (IFCs) as places where there is a high concentration of FABS firms that partake in cross-border transactions. Although technology has leapfrogged the spatial reach of FABS, it has also resulted in the increasing spatial concentration of FABS within an arguably small number of cities (Wójcik et al., Citation2018). Knox-Hayes (Citation2009) stresses that ‘global cities’ now act as command points in the financial service industry. Investment banks, which epitomize these dynamics (Pažitka et al., Citation2021), could be an extremely powerful enabler of the climate transition if they were to align their brokerage activities with it. This is not only because of their processual role in the intermediation capital flows, but also, perhaps more importantly, because of their unique ‘position within global urban-economic networks’ (Sigler et al., Citation2020, p. 1).

The last decade has seen a remarkable surge in scholarship, both theoretical and empirical, on the topic of brokerage (Kwon et al., Citation2020). However, the concept of brokerage finds its roots in sociological work dating back as far as the mid-20th century with the work of Simmel (Citation1950) on third-party influence and, later, Granovetter’s (Citation1973) seminal paper ‘The strength of weak ties’. Burt’s (Citation1992) idea of ‘structural holes’ is particularly interesting when considering the role of investment banks in bringing together issuer of financial securities (demand for capital) and investors (offer for capital) in a climate transition context. Although investment banks may like to think and argue that they are climate agnostic (a neutral intermediary), they are better described by the concept of ‘tertius gaudens’ or ‘third who enjoys’ (see also Stovel & Shaw, Citation2012) because they maintain close dealings with polar opposites on the climate problem–solution continuum. Indeed, it is common practice for an investment bank to broker capital market deals for both coal and renewable energy companies.

Because structuring and executing these deals requires close dealings with issuers, it also yields privileged insights into the financial risks and opportunities associated with their business models. From a geographical standpoint, these information asymmetries are likely to have a particular spatial distribution that reflects the relative closeness between issuers, brokers and market participants.

While the literature on fossil fuel financing brokerage is sparce, there is a more prolific area of energy production networks and the conceptualization of fossil fuels in a world city-network framework. In the following, we discuss a few characteristics of production and city networks of fossil fuels to understand how they are linked with the geography and scope of their financiers.

In the oil and gas sector, the operational control usually falls under the administrative headquarters of the transnational (or state owned) oil and gas company. Loginova et al. (Citation2020) argue that depending on the country, present energy networks are globally interlinked either through energy hubs (e.g., Houston) or national capitals (e.g., Moscow). Energy city networks usually reflect the strategic choices of firms to hold a physical presence across the energy value chain as well as the role of companies as national producers versus global diversified energy companies (Breul & Revilla Diez, Citation2019). The geography of their financiers also varies widely depending on the location of the energy company, the markets it seeks to access as well as the pots of financing it seeks to attract (e.g., local commercial banks versus international investment banks) (Cojoianu et al., Citation2021; Loginova et al., Citation2020). In addition, the literature argues that the credit worthiness of the fossil fuel industry is also highly dependent on their home country’s credit worthiness and sustainability profile (e.g., for semi- or fully state-owned companies) (Cojoianu et al., Citation2021; Hoepner et al., Citation2016).

In this light, the literature further suggests that the evolving relationships between headquarters and subsidiaries of companies, and equally the relationships with the headquarters or subsidiaries of their financiers, have an inherent overlapping spatial scale which can be to some extent explained through firm city networks (Loginova et al., Citation2020; Phelps & Fuller, Citation2000). The empirical work of Wójcik et al. (Citation2019) on cross-border investment banking activity provides a useful lens through which to categorize the brokering role of financial centres (as defined by investment banking firms) because it distinguished between domestic, export, import and platform brokerage activities of financial centres. These definitions relate to the location of investment banks (headquarters (HQs) and subsidiaries) and the relation with their investee companies (their HQ or subsidiaries) through the banks’ lending and underwriting activities. We follow Wójcik et al. in our definition of financial centre brokerage activities that we employ throughout this paper, and which we explain in more depth in the synthesis of the results.

Institutional theory and the spatiality of fossil fuel investment brokerage

This study mainly builds its theoretical framework on institutional theory developed by Scott (Citation1995). The underlying notion of institutional theory is that organizations are framed and rooted by the social and cultural environment in which they operate (Scott & Christensen, Citation1995). The three pillars of the theory are normative, regulative and cognitive. The normative pillar includes the social norms and values that delineate the boundaries of acceptable behaviour in alignment with a set of prescribed goals. The regulative pillar defines acceptable behaviour through the setting of regulations, the monitoring of compliance and the penalizing of non-compliance. Finally, the cognitive pillar encompasses wider belief system(s) built upon a common understanding and shared by individual organizations and persons. Bathelt and Glückler (Citation2014) stress that institutions are spatially and temporally embedded. As a result, institutions not only provide necessary environments for a stabilized social interaction but also define and limit interactions in space (North, Citation1990) and time.

For the purpose of our study, we frame fossil fuel brokerage as an institution whose manifestation can be observed in space and time through patterns of capital flows from global investors, through investment banks, to the fossil fuel industry. Building on the financial geographical work reviewed above, we posit that the institution of fossil fuel brokerage is performed and become stabilized in variegated financial centres, resulting in variegated capital allocation outcomes. Starting from this theoretical proposition, our study seeks to empirically investigate if and how city-level fossil fuel capital allocation outcomes result from spatially variegated green banking finance regulations and fossil fuel divestments while controlling for key financial centre characteristics (detailed in the methods section).

Our approach is anchored in the literature on the integration of environmental, social and governance (ESG) considerations into investment processes (Hoepner et al., Citation2019; Scholtens & Sievänen, Citation2013) as well as dedicated literature on the banking sector’s recent adoption of ‘soft indicators’ in their practices – such as the environmental and sustainability profile of their clients’ home country (Hoepner et al., Citation2016; Weber et al., Citation2008, Citation2015). In particular, there is evidence that banks are increasingly aware of the reputational risks associated with being stigmatized by the fossil fuel divestment movement should their name be associated with financing the oil and gas sector (Ansar et al., Citation2013; Cojoianu et al., Citation2021; Le Billon & Kristoffersen, Citation2020). Another common argument for divestment stems from stranded asset implications (Caldecott et al., Citation2014; Hunt, Citation2017). This cognitive change, we argue, could in turn lead to material and positive changes in climate finance considering investment banks facilitate the flow of close to US$10 trillion/year of investors’ money to corporations and governments (Urban, Citation2020; Urban & Wójcik, Citation2019). Using game theory, Kruitwagen et al. (Citation2017) demonstrates how engagement or divestment decisions ultimately depend on the respective environmental risks and effectiveness of investor stewardship and engagement.

Although the normative pillar does not constitute legislation, whether voluntary or mandatory, it defines an institutional setting that confers legitimacy as well as obligations towards social behaviours. There is a general literature on how environmental movements, through their inherent social norms, confer legitimacy on a transition to low-carbon economy (Pacheco et al., Citation2014; Sine & Lee, Citation2009; Vedula et al., Citation2019; York & Lenox, Citation2014). An example in case is the criticism directed at charities and foundations whose endowments invest in activities that are direct contradiction with their objectives. For instance, the National Trust (a heritage conservation organization) in the UK was forced to divest its fossil fuel holdings after being publicly shamed by an investigation conducted by The Guardian newspaper (Taylor, Citation2019). Generally, Cojoianu et al. (Citation2021) found that the fossil fuel divestment campaign negatively affects the level of fundraising for the oil and gas sector. Concurrently, Ansar (Citation2013) argues that divestment can increase the cost of capital of targeted firms. Finally, Hoepner et al. (Citation2019) found that public sector pension funds are more likely than corporate pension funds to sign the principles for responsible investments (PRI), which, they argue, reflects different expectations of acceptable behaviours in the public and private sector.

In Scott’s typology of institutional theory, the regulative pillar spans a wide spectrum of informal and formal mechanisms, from ostracism (informal) to legally binding outcomes (formal). Hoepner et al. (Citation2019) find that in countries where there are historically more mandatory ESG laws, asset owners are less likely to sign up to the PRI. In addition, the authors highlight the fact that in the sphere of responsible investment there is little coercive regulation that would be classified as formal. Generally, it can be argued that the emergence of voluntary responsible investment practices signals the industry’s preference to self-regulate and preclude regulatory intervention from policymakers (Bengtsson, Citation2008; Cox & Schneider, Citation2010; Sandberg et al., Citation2009; Scholtens, Citation2005).

Nonetheless, the introduction of official policy and regulation can be a powerful tool in accelerating the adoption of responsible investment practices by dispelling uncertainties regarding asset owners’ and asset managers’ compliance with their fiduciary duty (Juravle & Lewis, Citation2008; Sandberg, Citation2011, Citation2013). Green finance policies in general and those aimed at the banking industry in particular, although they might only be a disclosure guideline, implicitly approve ESG investing and a shift towards sustainable finance. As illustrated by Sievänen (Citation2014), green finance policies allow early adoption of responsible investment practices, creating and expanding specialized knowledge, joint initiatives and networks.

It is also important to note that social movements, such as the fossil fuel divestment movement, are acting and impacting the oil and gas sector at multiple geographical scales, local, regional and country level, and transnational. Cojoianu et al. (Citation2021) provide evidence with respect to the country level as well as transnational aspect of the divestment movement by showing that cumulative divestment commitments in a country are associated with lower capital flows to domestic oil and gas companies. However, the study also shows that the movement may have an unintended consequence in that it encourages banks to export their financial services to oil and gas companies abroad if their domestic sector is targeted by the divestment movement. The paper then calls for more research, including on subnational and regional effects of the divestment movement. It therefore proposes to test whether the city-level divestment movement does have an effect on, or whether it is disembedded from, the operation of investment banking brokers in the context of their local financial centre.

In the light of the above, we explore how fossil fuel divestment commitments and country-level green banking policies may have shaped fossil fuel brokerage activities for 417 financial centres worldwide.

DATA AND METHODOLOGY

Dependent variables

City fossil fuel investment brokerage activity

We use data on investment banking from a database provided by Dealogic – a financial markets platform collating information on thousands of capital markets transactions from both investment banks and other financial service providers. The data used in this paper span the period from 2000 to 2018 and cover three groups of deals: (1) issuance of equity; (2) issuance of debt, including corporate and government bonds; and (3) syndicated loans. Specifically, a total of 847,259 deals across sectors (32,545 for fossil fuels) are included in the study, of which 117,269 (9247 fossil fuels) belong to the issuance of equity, 541,759 (8447) are debt issuance and 188,231 (14,851) are syndicated loans. Our scope of transactions is limited to those on primary capital markets only, which means that trading, securitization of loans and other secondary transactions are not covered. One of the main reasons is that data available on these activities are of lower quality than the data on investment banking (Wójcik et al., Citation2019). As such, our interpretation of the results will be kept in line with the definition of financial centres as brokers of primary market investment in fossil fuels as well as across industries.

Since the Dealogic database does not provide detailed location of bank subsidiaries on a city level, in order to aggregate investment banking activities on such a granular level, we adopt the same approach as Wójcik et al. (Citation2019). In other words, the information on the location of operational HQs are collected from the websites of Bureau van Dijk’s Orbis, Nexis UK, Bloomberg and individual company websites. The process results in a dataset of 18,451 bank subsidiaries and their respective cities, as classified based on the metropolitan statistical area (MSA) code. The dataset covers more than 90% of the total number deals for equity and debt issuances, and 80% for syndicated loans. Therefore, the resulting datasets are expected to be representative of financial centres’ activities.

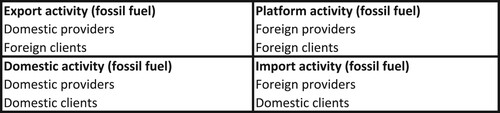

Based on the information on the nationalities of the bank subsidiary, bank parent as well as parent company, transactions are further categorized into four groups: export, import, domestic and platform, which is aligned with the typology in Wójcik et al. (Citation2019). Specifically, the definitions of ‘foreign’ and ‘domestic’ depends on the relationship between the country where the parent company of a bank is located in relation to a financial centre of reference (which is represented by the location of the bank subsidiary involved in a particular transaction). As a result, foreign providers located in a financial centre are understood to be owned by foreign bank parents. Domestic providers, on the other hand, are those banks whose parent are in the same country in which they are headquartered. Foreign clients are defined as those headquartered abroad, and domestic clients are locally headquartered companies to which bank subsidiaries provide either loans or equity/bond underwriting services ().

Figure 1. A typology of the activities of financial centres involved in fossil fuel industry financing based on the nationalities of providers and clients.

Source: Adapted from Wójcik et al. (Citation2019).

For fossil fuel industry classification, we use the Standard Industrial Classification (SIC) and North American Industry Classification System (NAICS) industry classifications of the company provided by Dealogic to categorize whether or not a company belongs to the fossil fuel industry. We focus mostly on the oil and gas and coal industry value chain, and cover equity, bond issuances and loans to the following subsectors: oil and gas extraction, distribution, oil and gas equipment manufacturing, oil and gas well drilling, oil and gas pipeline construction and operation, oil and gas refinery and marketing, and coal mining and fossil fuel (coal, oil and gas) power generation. illustrates the financial centre classification of investment banking activities that finance the fossil fuel industry through new equity and bond issuances, as well as through syndicated bank loans.

The total deal value (US$) of each deal is divided equally among the bank subsidiaries involved in the deal, given that we do not have any information with respect to the actual deal amount by bank. Based on fossil fuel industry classification as well as financial centres’ activities (export, import, domestic and platform), we aggregate the total deal values attributed to bank subsidiaries across three groups of transactions, grouped by the MSA code of each city. Finally, these values are summed up to arrive at five dependent variables on a city level, namely, total fossil fuel investment brokerage activity, export fossil fuel investment brokerage activity, import fossil fuel investment brokerage activity, domestic fossil fuel investment brokerage activity and platform fossil fuel investment brokerage activity.

Explanatory variables

City-level fossil fuel divestment commitment

The source for fossil fuel divestment by country is Divest Invest Initiative.Footnote2 The initiative has started to collect fossil fuel divestment commitments since 2008, with the first such commitment made by 350.org – an NGO. Divest Invest Initiative contains data of divestment commitments as well as the amount of assets committed to the cause of NGOs, private sector firms, governmental institutions and financial institutions. This independent variable is aggregated in US$ million by year and city based on the MSA code of the funds committed to fossil fuel divestment.

Number of country green banking finance policies

The study uses the Green Finance Measures Database (GFMD),Footnote3 an initiative that records sustainable finance policies from over 60 countries, including the European Union. The initiative is a collaboration between the United Nations Environmental Programme (UNEP) and the Green Growth Knowledge Partnership (GGKP). Originally, the database is built from the Inquiry into the Design of Sustainable Financial System, which is comprised of in-depth analysis, global reports as well as the Green Finance Progress Report series for G20 finance ministers. Later, the database is complemented by desk research of policy, regulatory measures and initiatives aimed at facilitating green finance. As of July 2020, there are 428 green finance polices in the database. In addition to being classified by country, the compilation is further categorized by focus area or objective, theme, and asset class. Sustainable finance policy or green finance policy, as the terms are used in this study, include mandatory, voluntary regulations as well as other types of measures without compliance such as consultations, guidelines, strategic roadmaps and the establishment of working groups for the banking sector. The variable is a dummy variable indicating whether any new green finance policy is issued in a country in a given year, from 2000 to 2018. We build two such dummy variables, one for mandatory policies and the other for voluntary policies.

Control variables

presents the control variables and their detailed description. Five out of eight control variables used in this study are taken from the Oxford Economics’ Global Cities database, which has been built to serve a wide range of purposes, from business decision-making, research analysis to urban planning and client consultations. These five control variables are gross valued added (GVA), employment, gross domestic product (GDP), GDP per capita and population. Apart from these variables, the study also controls for the environmental innovative profile of a country (proxied by the number of green patents), fossil fuel subsidy support, feed-in tariff (FiT) for renewable energy, country oil, gas and renewable power production as well as the country-level greenhouse gases (GHG) per capita.

Table 1. Control variables definition and data sources.

Model specification

Our analysis is conducted at the city/financial centre level, with the data organized in a balanced panel between 2000 and 2018. Fixed-effects models can only provide an estimation of within-cluster variation (in our case, within financial centre variation), and cannot estimate the effect of the average variation between financial centres (Schunck & Perales, Citation2017). Random effects models, on the other hand, assume that the within- and between-cluster variations are statistically the same. However, when this is not the case, the results of the random effects model are often meaningless (Bell et al., Citation2019). In order to solve this issue, we estimate a random effects model with features of time-varying covariates expressed as deviations from the individual-specific means, similar to Cojoianu et al. (Citation2020). This allows us to differentiate within- and between-regional effects and rely on the strengths of both random- and fixed-effects models (Bell et al., Citation2019; Schunck & Perales, Citation2017). A between–within estimator used to estimate our econometric models is specified by equation (1):

(1)

(1) where the effect of the independent variable

on

is divided in:

, which represents the average within region variation of

; and

, which explains the remaining between-region average variation. Equation (1) can be rewritten in a mathematical equivalent form, as shown in equations (2) and (3), so that the resulting coefficient on

represents the contextual effect (the average between region effect while keeping

), and

can be still interpreted as the average within region variation of

. The model written in the form of equation (3) is also known as the correlated random-effects model (Wooldridge, Citation2010) or the Mundlak model (Mundlak, Citation1978; Schunck & Perales, Citation2017):

(2)

(2)

(3)

(3) Hence, our paper follows the Mundlak (Citation1978) model (equation 3) and reports both within-region effects (

) and contextual between-region effects

in order to understand the factors that explain the variation in fossil fuel investment brokerage both within and between financial centres. For robustness, we also cluster standard errors at the regional level for all models (Petersen, Citation2009). All regressors in our models are lagged by one year. We use the xthybrid STATA package, which allows us to implement the Mundlak model (Schunck & Perales, Citation2017).

SYNTHESIS OF THE RESULTS

Descriptive results

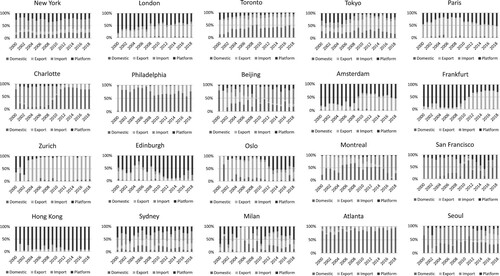

Tables A1 and A2 in the supplemental data online present basic descriptive statistics and the correlation matrix of our variables. First, we seek to unveil the top 20 financial centres in the world that have brokered new fossil fuel finance deals through new equity issuances, bonds and syndicated loans over the period 2000–18, and to further understand how this relates to their ranking as investment brokers across industries. We find, perhaps unsurprisingly, that New York and London dominate with global shares of fossil fuel investment brokerage of 20.2% and 9.7%, respectively, followed by Toronto (8.8%), Tokyo (7.3%) and Paris (7.3%). The financial centres that disproportionately finance fossil fuels compared with their overall brokerage activities across sectors are Oslo, Montreal, Toronto and Atlanta, while cities such as Frankfurt and Tokyo are less prominent in fossil fuel brokerage activities given their prominent roles as global financial centres ().

Table 2. Top 20 financial centres involved in financing the fossil fuel industry, 2000–18 (based on total deal value).

Next, we show the type of fossil fuel investment brokerage types in which financial centres engage. New York seems to show a relatively balanced split between the four types of brokerage activities, with a tilt towards facilitating the financing of the US fossil fuels sectors through domestic and import investment brokerage activities. London, on the other hand, is almost exclusively focused on financing fossil fuels abroad, through export and platform activities. Cities that have transitioned notably from one type of activity to the other include Charlotte (from import activities to domestic activities after the financial crisis), Beijing (which has steadily increased its import fossil fuel brokerage activities and almost phased out the export of fossil fuel financial services), Frankfurt (transitioned from a platform to the export of financial services to fossil fuels), Edinburgh (phased out its export of finance to fossil fuels for the benefit of platform activities), Oslo (became primarily a platform financial centre for fossil fuel investment from an export type centre), Montreal (transitioning to fossil fuel capital imports from a domestic and export financial centre), San Francisco (which after the financial crisis diminished its capital import activities to become a domestic financial centre for fossil fuels) and Seoul (which emerges as an export fossil fuel financial centre in Asia).

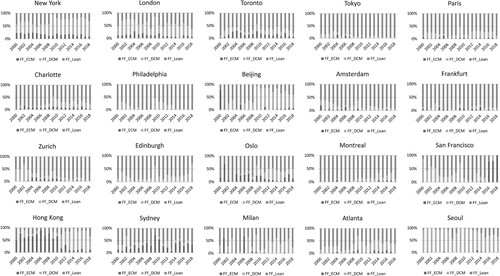

The majority of financial centres have a stable distribution of the asset classes through which they finance fossil fuels, but examples show significant shifts among these, particularly in San Francisco (which has significant deal activity in public equity markets recently, having transitioned from investment brokerage focused primarily on loans), Edinburgh (which is increasing its share of fossil fuel bond issuance facilitation), Beijing (which transitions from private syndication of loans to public markets through bonds) and Hong Kong (transitioning from equity to bond issuance) ( and ).

Figure 2. Top 20 financial centres by fossil fuel investment brokerage type, 2000–18.

Figure 3. Top 20 financial centres financing fossil fuels by asset class, 2000–18.

Note: FF, fossil fuel; ECM, equity capital markets; and DCM, debt capital markets or bonds.

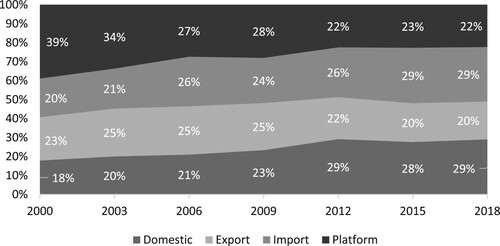

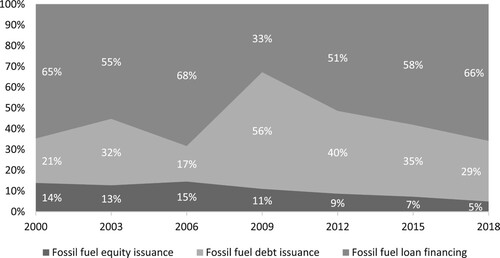

At a global level, shows that the fossil fuel investment brokerage types that dominate by deal value are domestic and import financing activities (each with 29%), followed by platform activities (22%) and export of fossil fuel finance. The asset classes through which the financing occurs are mostly loans (66% as of 2018), followed by bonds (29%) and only 5% equities ().

Figure 4. Global fossil fuel investment brokerage, 2000–18.

Figure 5. Global financing of fossil fuels at the financial centre level by asset class, 2000–18.

Statistical results

In and (models 1–10), we run the statistical models for each investment brokerage type with mandatory and voluntary green policies.

Table 3. Divestment commitments and green finance policy drivers (mandatory and voluntary) of city fossil fuel investment brokerage activity types, 2001–18.

Table 4. Divestment commitments and green finance policy drivers (mandatory and voluntary) of city fossil fuel investment brokerage activity types, 2001–18.

Unlike Cojoianu et al. (Citation2021), who document a relationship between country-level divestment commitments and within-country reductions of oil and gas fundraising between 2000 and 2015, when we zoom in at the financial centre level, we do not find a significant relationship between city-level divestment commitments (related to fossil fuels including oil and gas, coal and extractives) and the within-financial centre variation of fossil fuel brokerage activities.

The introduction of voluntary green finance policies seems to reduce within-financial centre variation of total fossil fuel brokerage activities, especially related to the import of financial services (model 8). In addition, we find that voluntary green finance policies reduce platform brokerage activities relating to the fossil fuel industry (model 10). On the other hand, the introduction of mandatory green finance policies does not seem to counteract the financing of fossil fuels either, apart from a lower level of fossil fuel in the import brokerage activities between-financial centre variation (model 7). We also find that financial centres in countries that increase their fossil fuel subsidies are also increasing their brokerage activities in fossil fuels, particularly in domestic and import of financial services activities, and not in export and platform activities. However, countries with historically high average of state fossil fuel support rely less on their financial centres to broker capital for fossil fuels.

We further investigate these dynamics at the financial asset class level (, models 11–16). We unveil that the introduction of mandatory and voluntary sustainable finance policies produces mixed results, especially in terms of syndicated loan instruments (models 15 and 16). Voluntary green finance policies seem to reduce fossil fuel brokerage activities both within and between financial centres. On the other hand, in financial centres where mandatory green finance policies are issued, fossil fuel financing activities through syndicated loans increase over time, while compared with financial centres where no mandatory sustainable finance policy is issued, those centres have a significantly lower level of fossil fuel financing activities.

Table 5. Divestment commitments and green finance policy drivers (mandatory and voluntary) of city fossil fuel investment brokerage activity by asset class, 2001–18.

DISCUSSION AND CONCLUSIONS

Our paper has unveiled the fossil fuel investment brokerage profile of financial centres worldwide between 2000 and 2018 by using a global dataset of over 840,000 equity, bond and syndicated loan investment banking deals. Our financial centre typology and ranking relies on the nationality of parent companies of banks and their clients, and distinguishes between domestic, export, import and platform fossil fuel investment activities, similar to Wójcik et al. (Citation2019). We also study whether financial centre fossil fuel divestment commitments and country-level green banking policies impact this profile over our study time period. We find that several financial centres shift their fossil fuel investment brokerage profiles substantially, including the asset classes in which they are active, and that divestment commitments fail to restrain fossil fuel investment. We do find, however, a negative effect of the introduction of new country-level voluntary green finance policies on financial centre fossil fuel financing, particularly through the import activities of fossil fuel brokers through fossil fuel loans. Finally, we highlight the importance of bonds and syndicated loans to global fossil fuel financing and conclude that a substantial impact on climate change mitigation can be made if bankers from five key cities (New York, London, Toronto, Tokyo and Paris) decide to defund fossil fuels.

Our study thus contributes to the literature in several ways. First, we provide evidence on the spatial scale of institutional change by showing that the fossil fuel investment brokerage activities at the financial centre level are disembedded from city-level divestment commitments. We also build upon brokerage theory and show how a new typology of financial centres can help us understand the heterogeneity of fossil fuel investment brokerage activities. In this respect, the regulatory institutional environment, proxied by voluntary green finance policies, seems to be salient only for import brokerage activities (domestic clients and foreign financial brokers), which suggest perhaps a divergence in how foreign versus domestic financiers interpret the emergence of green policy. We interpret this finding in the light of the work of Hoepner et al. (Citation2019), which shows that country-specific regulation explains the emergence of sustainable investment practices as investors anticipate potentially more stringent regulation by taking voluntary action. This shows that fossil fuel financial centres that rely on foreign investors are more likely to reduce their exposure to fossil fuels pre-emptively in anticipation of more binding green finance policies. In contrast to the work of Knox-Hayes (Citation2009), who looks at the within-financial centre practices and networks in cities where carbon finance financial products emerge, we do not find that the emergence of the divestment movement spills over yet into investment banking services provision.

Our findings also have wide-ranging implications for divestment campaigners, whose aggregate country-level prominence is more salient (Cojoianu et al., Citation2021) than their prominence and visibility within individual financial centres that finance the fossil fuel industry both domestically and internationally. Hence, divestment campaigners may be more successful in focusing their activities on monitoring new financing of fossil fuels by their target banks, wherever these investments may be in the world. The reason for this is that the climate impact of 1 tonne CO2e emitted in New York has the same impact on the world’s climate as 1 tonne CO2e emitted in London, Beijing or any location around the world. Divestment campaigners are also advised to focus on bond investors who ultimately finance a great chunk of fossil bond issuance, as well as the investment banks themselves.

In addition, our paper informs the emerging research on the governance of financial centres, as initiatives such as the United Nations Financial Centres for Sustainability have emerged which are seeking to influence financial centre-specific actors and push them to invest sustainably. Last but not least, policymakers who know about the typology of their financial centres may be better able to tailor green finance policies towards curbing new fossil fuel financing, both domestically and internationally.

Supplemental Material

Download PDF (149.9 KB)ACKNOWLEDGEMENTS

We are also grateful to Tom Harrison of the Sainsbury Family Charitable Trusts and DivestInvest Initiative (https://www.divestinvest.org/) for sharing data for the purposes of this project. Authors are listed alphabetically. All remaining errors are our own.

DISCLOSURE STATEMENT

No potential conflict of interest was reported by the authors.

Additional information

Funding

Notes

1. See https://gofossilfree.org/divestment/commitments/. Divestment commitments as of 25 November 2020.

REFERENCES

- Ansar, A., Caldecott, B., & Tibury, J. (2013). Stranded assets and the fossil fuel divestment campaign: What does divestment mean for the valuation of fossil fuel assets? Smith School of Enterprise and the Environment, University of Oxford.

- Bathelt, H., & Glückler, J. (2014). Institutional change in economic geography. Progress in Human Geography, 38, 340–363. https://doi.org/10.1177/0309132513507823

- Bell, A., Fairbrother, M., & Jones, K. (2019). Fixed and random effects models: Making an informed choice. Quality & Quantity, 53(2), 1051–1074. https://doi.org/10.1007/s11135-018-0802-x

- Bengtsson, E. (2008). Socially responsible investing in Scandinavia – A comparative analysis. Sustainable Development, 16(3), 155–168. https://doi.org/10.1002/sd.360

- Breul, M., & Revilla Diez, J. (2019). ‘One thing leads to another’, but where? – Gateway cities and the geography of production linkages. Growth and Change. doi:10.1111/grow.12347

- Burt, R. (1992). Structural holes. Harvard University Press.

- Caldecott, B., Tilbury, J., & Carey, C. (2014). Stranded assets and scenarios (Discussion Paper, January). https://www.smithschool.ox.ac.uk/research/sustainable-finance/publications/Stranded-Assets-and-Scenarios-Discussion-Paper.pdf

- Cassis, Y., & Wójcik, D. (2018). International financial centres after the global financial crisis and Brexit. Oxford University Press.

- Cojoianu, T., Ascui, F., Clark, G., Hoepner, A., & Wójcik, D. (2021). Does the fossil fuel divestment movement impact new oil and gas fundraising? Journal of Economic Geography, 21(1), 141–164. https://doi.org/10.1093/jeg/lbaa027

- Cojoianu, T., Clark, G., Hoepner, A., Pažitka, V., & Wójcik, D. (2020). Fin vs. tech: Are trust and knowledge creation key ingredients in fintech start-up emergence and financing? Small Business Economics, 1–17. doi:10.1007/s11187-020-00367-3

- Cox, P., & Schneider, M. (2010). Is corporate social performance a criterion in the overseas investment strategy of US pension plans? An empirical examination. Business & Society, 49(2), 252–289. https://doi.org/10.1177/0007650308315491

- Daniels, P. (1993). Service industries in the world economy. Blackwell.

- Desmarchelier, B., Djellal, F., & Gallouj, F. (2013). Knowledge intensive business services and long term growth. Structural Change and Economic Dynamics, 25, 188–205, https://doi.org/10.1016/j.strueco.2012.07.003

- Granovetter, M. (1973). The strength of weak ties. American Journal of Sociology, 78, 1360–1380. https://doi.org/10.1086/225469

- Hoepner, A., Majoch, A., & Zhou, X. (2019). Does an asset owner’s institutional setting influence its decision to sign the principles for responsible investment? Journal of Business Ethics, 1–26. doi:10.1007/s10551-019-04191-y

- Hoepner, A., Oikonomou, I., Scholtens, B., & Schröder, M. (2016). The effects of corporate and country sustainability characteristics on the cost of debt: An international investigation. Journal of Business Finance & Accounting, 43(1–2), 158–190. https://doi.org/10.1111/jbfa.12183

- Hunt, C. W. (2017). A comparative analysis of the anti-Apartheid and fossil fuel divestment campaigns. Journal of Sustainable Finance and Investment, 7, 64–81. https://doi.org/10.1080/20430795.2016.1202641

- International Energy Agency (IEA). (2021). Net zero by 2050. IEA. https://www.iea.org/reports/net-zero-by-2050

- Jones, S. (2019). City governments measuring their response to climate change. Regional Studies, 53(1), 146–155. https://doi.org/10.1080/00343404.2018.1463517

- Juravle, C., & Lewis, A. (2008). Identifying impediments to SRI in Europe: A review of the practitioner and academic literature. Business Ethics: A European Review, 17(3), 285–310. https://doi.org/10.1111/j.1467-8608.2008.00536.x

- Knox-Hayes, J. (2009). The developing carbon financial service industry: Expertise, adaptation and complementarity in London and New York. Journal of Economic Geography, 9(6), 749–777. https://doi.org/10.1093/jeg/lbp004

- Kruitwagen, L., Madani, K., Caldecott, B., & Workman, M. H. W. (2017). Game theory and corporate governance: Conditions for effective stewardship of companies exposed to climate change risks. Journal of Sustainable Finance & Investment, 7(1), 14–36, doi:10.1080/20430795.2016.1188537

- Kwon, S., Rondi, E., Levin, D., De Massis, A., & Brass, D. (2020). Network brokerage: An integrative review and future research agenda. Journal of Management, 46(6), 1092–1120. https://doi.org/10.1177/0149206320914694

- Kythreotis, A., Jonas, A., & Howarth, C. (2020). Locating climate adaptation in urban and regional studies. Regional Studies, 54(4), 576–588. https://doi.org/10.1080/00343404.2019.1678744

- Le Billon, P., & Kristoffersen, B. (2020). Just cuts for fossil fuels? Supply-side carbon constraints and energy transition. Environment and Planning A: Economy and Space, 52(6), 1072–1092. https://doi.org/10.1177/0308518X18816702

- Liu, J., Hull, V., Godfray, H., Tilman, D., Gleick, P., Hoff, H., Pahl-Wostl, C., Xu, Z., Chung, M. G., Sun, J., & Li, S. (2018). Nexus approaches to global sustainable development. Nature Sustainability, 1(9), 466–476. https://doi.org/10.1038/s41893-018-0135-8

- Loginova, J., Sigler, T., Martinus, K., & Tonts, M. (2020). Spatial differentiation of variegated capitalisms: A comparative analysis of Russian and Australian oil and gas corporate city networks. Economic Geography, 96(5), 422–448. https://doi.org/10.1080/00130095.2020.1833713

- Mundlak, Y. (1978). On the pooling of time series and cross section data. Econometrica: Journal of the Econometric Society, 46, 69–85. https://doi.org/10.2307/1913646

- North, D. (1990). Institutions, institutional change and economic performance. Cambridge University Press.

- Pacheco, D., York, J., & Hargrave, T. (2014). The coevolution of industries, social movements, and institutions: Wind power in the United States. Organization Science, 25(6), 1609–1632. https://doi.org/10.1287/orsc.2014.0918

- Pažitka, V., Urban, M., & Wójcik, D. (2021). Connectivity and growth: Financial centres in investment banking networks. Environment and Planning A, 53(6). doi:10.1177/0308518X211026318

- Petersen, M. (2009). Estimating standard errors in finance panel data sets: Comparing approaches. Review of Financial Studies, 22(1), 435–480. https://doi.org/10.1093/rfs/hhn053

- Pfeiffer, A., Hepburn, C., Vogt-Schilb, A., & Caldecott, B. (2018). Committed emissions from existing and planned power plants and asset stranding required to meet the Paris agreement. Environmental Research Letters, 13(5), 054019. https://doi.org/10.1088/1748-9326/aabc5f

- Phelps, N., & Fuller, C. (2000). Multinationals, intracorporate competition, and regional development. Economic Geography, 76(3), 224. https://doi.org/10.2307/144291

- Sandberg, J. (2011). Socially responsible investment and fiduciary duty: Putting the freshfields report into perspective. Journal of Business Ethics, 101(1), 143–162. https://doi.org/10.1007/s10551-010-0714-8

- Sandberg, J. (2013). (Re-) interpreting fiduciary duty to justify socially responsible investment for pension funds? Corporate Governance: An International Review, 21(5), 436–446. https://doi.org/10.1111/corg.12028

- Sandberg, J., Juravle, C., Hedesström, T., & Hamilton, I. (2009). The heterogeneity of socially responsible investment. Journal of Business Ethics, 87(4), 519-533. doi:10.1007/s10551-008-9956-0.

- Scholtens, B. (2005). Style and performance of Dutch socially responsible investment funds. The Journal of Investing, 14(1), 63–72. https://doi.org/10.3905/joi.2005.479390

- Scholtens, B., & Sievänen, R. (2013). Drivers of socially responsible investing: A case study of four Nordic countries. Journal of Business Ethics, 115(3), 605–616. https://doi.org/10.1007/s10551-012-1410-7

- Schunck, R., & Perales, F. (2017). Within- and between-cluster effects in generalized linear mixed models: A discussion of approaches and the xthybrid command. The Stata Journal: Promoting Communications on Statistics and Stata, 17(1), 89–115. https://doi.org/10.1177/1536867X1701700106

- Scott, W., & Christensen, S. (1995). The institutional construction of organizations: International and longitudinal studies. Sage.

- Scott, W. R. (1995). Institutions and organizations: Foundations for organizational science. SAGE. doi:10.3917/mana.172.0136.

- Sievänen, R. (2014). Practicalities bottleneck to pension fund responsible investment? Business Ethics: A European Review, 23(3), 309–326. https://doi.org/10.1111/beer.12048

- Sigler, T., Neal, Z., & Martinus, K. (2020). The brokerage roles of city-regions in global corporate networks. Regional Studies. https://doi.org/10.1080/00343404.2021.1950914

- Simmel, G. (1950). The sociology of Georg Simmel. Glencoe.

- Sine, W., & Lee, B. (2009). Tilting at windmills? The environmental movement and the emergence of the US wind energy sector. Administrative Science Quarterly, 54(1), 123–155. https://doi.org/10.2189/asqu.2009.54.1.123

- Stovel, K., & Shaw, L. (2012). Brokerage. Annual Review of Sociology, 38(1), 139–158. https://doi.org/10.1146/annurev-soc-081309-150054

- Taylor, M. (2019, July 4). National Trust to divest portfolio from fossil fuels. The Guardian. https://www.theguardian.com/environment/2019/jul/04/national-trust-to-divest-portfolio-from-fossil-fuels

- Truffer, B., & Coenen, L. (2012). Environmental innovation and sustainability transitions in regional studies. Regional Studies, 46(1), 1–21. https://doi.org/10.1080/00343404.2012.646164

- Urban, M. (2020, July 27). The FinReg Blog. https://sites.law.duke.edu/thefinregblog/2020/07/27/a-call-for-sustainable-investment-banking/

- Urban, M., & Wójcik, D. (2019). Dirty banking: Probing the gap in sustainable finance. Sustainability, 11(6), 1745. https://doi.org/10.3390/su11061745

- Vedula, S., York, J., & Corbett, A. (2019). Through the looking-glass: The impact of regional institutional logics and knowledge pool characteristics on opportunity recognition and market entry. Journal of Management Studies, 56(7), 1414–1451. https://doi.org/10.1111/joms.12400

- Weber, O., Fenchel, M., & Scholz, R. (2008). Empirical analysis of the integration of environmental risks into the credit risk management process of European banks. Business Strategy and the Environment, 17(3), 149–159. https://doi.org/10.1002/bse.507

- Weber, O., Hoque, A., & Ayub Islam, M. (2015). Incorporating environmental criteria into credit risk management in Bangladeshi banks. Journal of Sustainable Finance & Investment, 5(1–2), 1–15. https://doi.org/10.1080/20430795.2015.1008736

- Wheeler, S. (2009). Regions, megaregions, and sustainability. Regional Studies, 43(6), 863–876. https://doi.org/10.1080/00343400701861344

- Wooldridge, J. (2010). Econometric analysis of cross section and panel data. MIT Press.

- Wójcik, D., Knight, E., O’Neill, P., & Pažitka, V. (2018). Economic geography of investment banking since 2008: The geography of shrinkage and shift. Economic Geography, 94(4), 376–399. https://doi.org/10.1080/00130095.2018.1448264

- Wójcik, D., Pažitka, V., Knight, E., & O’Neill, P. (2019). Investment banking centres since the global financial crisis: New typology, ranking and trends. Environment and Planning A: Economy and Space, 51(3), 687–704. doi:10.1177/0308518X18797702

- York, J., & Lenox, M. (2014). Exploring the sociocultural determinants of de novo versus de alio entry in emerging industries. Strategic Management Journal, 35(13), 1930–1951. doi:10.1002/smj.2187