ABSTRACT

This article draws upon novel survey evidence to examine the possible regional impacts of Brexit as a ‘disruptive process’ to manufacturing operations and logistics in the automotive industry, in the context of the regional resilience literature. The current Brexit (and Covid-19) context, along with the sector’s need to re-orientate towards electrification, provides renewed urgency to reconsider industrial policy in spatial terms. The findings have salience not only in the context of anticipating and reacting to Brexit-induced economic shocks at a regional level, but also over the role of decentralized regional bodies. In this regard, the UK government’s agenda of ‘levelling up’ will be challenging, especially in the context of the place-based shocks likely to arise from Brexit as well as the impact of Covid-19. The article concludes that a more place-based regional industrial policy is required both to anticipate and to respond to shocks and also to reposition the sector in the region going forward.

INTRODUCTION AND CONTEXT

Economic shocks have the potential to disrupt development paths at various spatial scales, suggesting the need for policy approaches at multiple levels. The impact of Brexit and the trajectory of the automotive sector in the West Midlands and East Midlands regions of the UK offer an opportunity to explore some of these issues in depth, given the potential exposure to Brexit in both regions via trade. Brexit, however, is also of particular interest because it can be seen as an ongoing ‘slow burn’ process rather than a single one-off shock. Hence, this article contributes to wider debates around regional resilience, arguing that effective subnational industrial policy is imperative to support economic resilience in regions where a few embedded industries comprise a disproportionate share of employment and value-added (Kitsos et al., Citation2019) and where sectoral and regional resilience come into contrast. The novel micro-level dataset used in this paper allows us to examine these issues at a much more granular level than is typical in the literature. By looking at the specific preparations and experiences of firms, we find that intra-country transport infrastructure, the presence of certain ‘key skills’ within a workforce and individual heterogeneity in the sectors that firms supply are key. Thus, the aggregate exposure of a region and sector to disruption of this form conceals considerable heterogeneity in firm-level differences at a regional level. Policies aimed at enhancing regional resilience therefore need to explicitly acknowledge and be framed in response to individual business experiences and circumstances, rather than solely relying on aggregate indicators (regional or sectoral). This raises implications for place-based industrial policies.

The pre-Covid-19 run-up to Brexit offered an interesting perspective on such issues, enabling detailed investigation of how regional, national and international supply-chain linkages contribute to regional vulnerability and, conversely, resistance (Martin, Citation2011) to disruption. This paper defines a ‘disruptive process’ as an ongoing process that causes episodic or continuous disruption over a period of several years; namely a ‘slow burn’ process (in line with Dawley et al., Citation2010). We distinguish it from a shock by arguing that the latter terminology is most sensibly reserved for a discrete ‘one-off’ event or series of events occurring in a short period. Whilst the ramifications of a discrete shock can be long term, the shock itself is not. In contrast, the ‘disruptive process’ itself – rather than its consequences – lasts for years, causing renewed ongoing periods of additional disruption as the process evolves.

In the case of Brexit, the evolution of just such a process has become clear. The initial vote to leave the European Union (EU) in 2016 ushered in a period of greatly heightened uncertainty, which was punctuated by a series of additional discrete shocks in their own rights as various deadlines came and went (many of which are directly visible in export data, for example). Thus, 2019 saw repeated climaxes in uncertainty as a series of last-minute deadlines to avoid a sudden ‘no deal’ Brexit were pushed back. However, these did not end with the termination of Britain’s formal EU membership in early 2020. The terms of the new relationship only became clear days before the end of the ‘transition period’ when Great Britain (that part of the UK excluding Northern Ireland) left the EU Customs Union and Single Market. Hence, 1 January 2021 saw an additional rupture as this occurred, which was itself followed by the imposition of additional customs controls on imports in 2022. Thus, some six years after the original referendum campaign, the disruptive process remains ongoing, with full controls over imports to the UK yet to be imposed at the time of writing.

Within that context, this research highlighted the extent to which actors within a particular sector planned to deal with an anticipated shock and the wider regional situation that framed it (which differed considerably between the two regions). There is growing evidence that ‘non-core’ regions are more exposed to Brexit (even with the trade deal that has been agreed with the EU) as a result of Brexit’s negative trade-related consequences (Chen et al., Citation2018), with small and medium-sized enterprises (SMEs) facing particular issues (Brown et al., Citation2019). The supply chain mapping and Brexit exposure analysis focus on a dataset of respondents from automotive vehicle manufacturers and parts and components suppliers in the West Midlands and East Midlands regions of the UK, which comprise a total of six NUTS-2 regions. In exploring this, we combine this unique dataset on firm-level exposure and preparations with a mix of official reports and statistics to elucidate the wider consequences and more general lessons for regional resilience. Hence, the paper can be regarded as an inductive piece, ascertaining elements of regional interest and potential avenues for further theoretical and empirical research. presents shares of gross domestic product (GDP) and local labour income exposed to Brexit in the Midlands.

Table 1. Regional shares of gross domestic product (GDP) and local labour income exposed to Brexit.

As can be seen, many of the NUTS-2 areas within the Midlands have heavy potential exposure to Brexit via trade, with only Derbyshire and Nottinghamshire below the UK average of 12.2% (Chen et al., Citation2018). Such estimates have predominantly been based on the aggregate importance of trade linkages and the possibility of trade disruption arising from Brexit (Thissen et al., Citation2020). While the Trade and Cooperation Agreement (TCA) agreed between the UK and EU largely avoids tariffs and quotas (subject to complying with rules of origin), it introduces an array of non-tariff barriers (NTBs) which are relevant here. These include delays, the costs of completing customs declarations, demonstrating compliance with local content requirements, regulatory divergence and so on (Bailey & Rajic, Citation2022). These are critical for regions specializing in manufacturing and specifically for the automotive sector, given the importance of just-in-time supply chains where extra costs and delays are likely to have a major impact.

More broadly, an inability to adjust to economic shocks is a characteristic of many of the UK’s economically weaker regions, with lower levels of economic diversity, skills and connectivity alongside a heavier focus on manufacturing compared to service-oriented economies such as London (Billing et al., Citation2019). Thinking about what role regional institutions can play in building economic resilience by supporting the adaptation of regional industries to continuous changing environments (Kitsos & Bishop, Citation2018; Martin, Citation2011) is critical in this regard. In the sections that follow, the experience of the automotive sector in the East and West Midlands is used to critically assess the relevance of place-based approaches in the context of Brexit disruption. As such, the paper examines the following research questions:

What are the likely regional ramifications from the impacts of trade ‘dis’-integration on automotive supply chains?

What actions do actors in the regional space take to mitigate the impacts of these, and what policy lessons can be drawn for regional resilience?

What are the implications for regional industrial policy to minimize any negative outcomes and ameliorate the likely regional impacts?

Although we position the automotive clusters in the East and West Midlands of the UK during Brexit as a case study, our findings have wider relevance for the interaction of sectoral and regional resilience and implications for industrial policy.

UNDERSTANDING REGIONAL AUTO SUPPLY CHAIN EXPOSURE TO BREXIT

Both Brexit and the recent pandemic are ‘disruptive’ processes in a supply-chain context. Both are systemic, with the former an unusual example of trade ‘dis’-integration in a ‘developed’ economy and the latter a huge but asymmetric global shock. We seek to understand the potential impacts of disruptive processes and firm responses to these when supply chains cross borders numerous times and major strategic decisions are made outside the regions under consideration. In the case of the automotive industry, the production networks of interest are less ‘global’ and more European in nature, being shaped around final assembly (Sturgeon et al., Citation2009) albeit with fine-grained supply chains crisscrossing borders. A major issue within the automotive sector is that some original equipment manufacturers (OEMs) have little knowledge of their suppliers beyond tier one (De Ruyter et al., Citation2018).

It is nevertheless clear that the regions’ manufacturers are deeply embedded in pan-European value chains (Bailey et al., Citation2019) and Brexit will directly impact this by making trade more costly through NTBs, changing the calculus in terms of the cost capability ratio (Yeung & Coe, Citation2015) for both suppliers and those they supply. This will be true for both EU and UK manufacturers in the sector and suggests an obvious catalyst to reconfigure production. The reliance on imported parts and components from the EU is reflected in aggregate figures for automotive manufacturers in the UK, as depicted in .

Table 2. UK imports of parts and components by country.

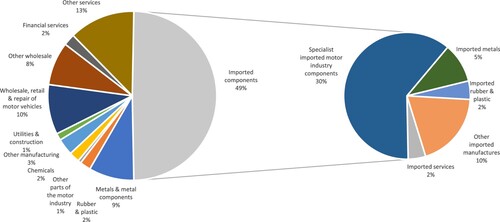

The UK automotive supply chain consists of a wide range of companies, ranging from small specialist firms to large multinationals. Figures from the Interdepartmental Business Register (Office for National Statistics (ONS), Citation2020c) indicate that in 2020 a total of 3480 businesses were directly involved in the manufacture of vehicles or vehicle parts. Similarly, there are over 30 manufacturers of vehicles based in the UK, although many are smaller, specialist manufacturers including of commercial vehicles (Society of Motor Manufacturers and Traders (SMMT), Citation2020). However, this is only part of the picture; many companies that provide inputs for the automotive industry categorize their business in terms of the materials they work with. Many of these suppliers will be upstream, primarily selling to tier-one suppliers rather than vehicle producers themselves. UK tier-one companies import a large proportion of their inputs, including metals, plastics, glass and other subcomponents. Some 80% of imported parts and components are from the EU (SMMT, Citation2020). illustrates the particular importance of imported specialist parts and components.

Figure 1. Wider supply chain for manufacturers in the motor vehicle sector.

Source: Office for National Statistics (ONS) (Citation2020b).

The view that Brexit will impact UK regions differently exacerbating regional inequalities, remains highly relevant, even allowing for the TCA that has been negotiated. The TCA removes tariff barriers on manufacturing providing rules-of-origin rules are complied with. Whilst welcome for the UK’s weaker regions (such as the East and West Midlands) which tend to be more specialized in manufacturing than the UK’s more prosperous regions (Bailey & Rajic, Citation2022), the TCA only ameliorate some of the additional costs faced by manufacturing businesses. This is because NTBs, which include all the non-price and non-quantity restrictions and restraints on trade, are highly significant – in some cases being more important than tariffs. The NTBs associated with the US–EU automobile trade outside of the Single Market typically imply costs increases of some 25% (Berden et al., Citation2009). However, many of the components, inputs and services embodied in the automotive industry come from other non-automotive sectors, and therefore the overall costs increases for the automotive industry also depend on the composition of these inputs. The UK government (HM Government, Citation2018) assumed that under a ‘No Deal’ scenario, then NTB cost increases on goods would range from 6% to 15% of the value of trade, while for an FTA, they range between 5% and 11% of the value of trade. The ‘hard Brexit’ nature of the rather thin EU–UK TCA falls squarely into these ranges, and these are also consistent with the NTB costs increases embedded in Thissen et al. (Citation2020), whose estimates of the impact on regional competitiveness are given in .

Table 3. Brexit regional competitiveness effect in UK transport industries for a selection of regions.

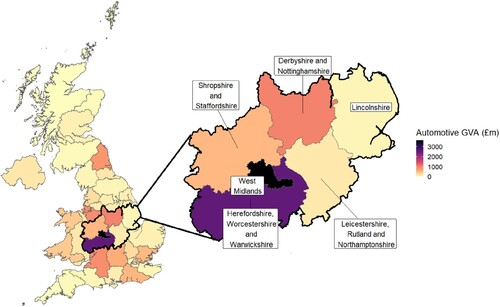

This is concerning given the spatially concentrated nature of the sector, which is apparent in . Indeed, this highlights the extent to which the East and West Midlands dominate automotive manufacture in the UK, with the country’s three top NUTS-2 vehicle manufacturing regions (by gross value added – GVA) all contained therein.Footnote1 In 2018, these were the only three areas whose GVA from motor vehicle manufacture exceeded £1 billion and the East and West Midlands combined accounted for almost half (48.3%) of the UK’s automotive value added (ONS, Citation2021). The rationale for focusing specifically on these regions is further strengthened when one considers the fact that the current policy vogue is increasingly to focus on either the city-region or meso-level regions, into which the Midlands Engine initiative squarely falls (Bentley, Citation2018; ONS, Citation2021).

Figure 2. Automotive gross value added by NUTS-2 region.

Moreover, both regions run a substantial automotive trade surplus, although this hides complexity. The West Midlands’ automotive trade surplus is driven by high-value exports to diverse markets (Her Majesty’s Revenue and Customs (HMRC), Citation2020a). This high-value-added industrial structure relies on imported goods (predominantly from the EU), many of which have no UK alternative suppliers. It is therefore unsurprising that the region is so exposed to Brexit.

The situation in the East Midlands is different. Although it, too, runs a trade surplus in the automotive sector, export values are much smaller at just £3.1 billion versus £13.8 billion for the West Midlands in 2019 (HMRC, Citation2020a). The structure of exports across the two regions is also different: 82.7% of all East Midlands automotive exports go to the EU, highlighting the region’s dependence on this trade partner. Japan is a major source of imports, demonstrating the importance of Toyota (which sources a significant value of parts and components from Japan, although further investment in its Walbrzych plant in Poland could gradually shift some of this to the EU).

In contrast to the detailed work undertaken to understand the exposure to Brexit at the macro-regional level for particular sectors, firm-level evidence on the supply chain and related logistics issues for the sector at the regional scale is more fragmentary. Kerridge (Citation2018) cites a 2015 Institute for Government study that lists lorry movements for most major ports in the UK, with the predominance of Dover and the Eurotunnel being all too evident. Beyond expediting inward traffic through ports, it appears to have been widely assumed by the UK government until the last minute that companies were preparing for the exit of the EU Customs Union and Single Market as part of normal risk management and contingency planning exercises. Linked to this, there is a need to understand the micro-responses of businesses within regions that are highly exposed to ongoing Brexit disruption, which in turn has implications for place-based industrial policies.

METHODOLOGY

The broad research method of this work is pragmatic and inductive. Survey evidence was solicited on the supply chain implications of Brexit as a disruptive process which were used to inform a coherent theoretical approach, albeit one that is situated within the broader literature on regional resilience. The aim is to use the case study to ascertain potential gaps in our knowledge and elucidate some consequences for the resilience literature. A survey questionnaire was conducted in late 2019 looking to ascertain company planning and the potential supply-chain impact of Brexit on the sector. In terms of survey method, the population of interest (i.e., our sampling frame) was any firm involved in the automotive supply chain. However, this was interpreted broadly to include logistics firms and those selling specialist machinery into the sector. Since we lack population-level data on this set,Footnote2 probabilistic sampling was infeasible. As such, the sampling method was non-probabilistic, being a combination of quota and convenience sampling (within each quota a convenience sample was taken). Respondents were solicited via e-mail and the survey was administered through an online portal. The survey itself was designed principally around closed questions, which were answered through a variety of ‘tick box’-style responses, with a small number of ‘free form’ open-ended questions in order to allow participants to expand on points of particular importance to them.

This evidence should be seen as inductive, informing the wider theoretical framework. Extensive use of inferential statistics would be inappropriate given the absence of a probabilistic sampling frame. In contrast, the considered application of simple descriptive statistics can give useful insights into areas where the wider literature can be built upon, which we have sought to exploit this in the piece. As noted, analysis focuses on a dataset of respondents from automotive vehicle manufacturers and parts and components suppliers (as a subset of transport manufacturers) in the West Midlands and East Midlands regions of the UK, which comprise a total of six NUTS-2 regions.

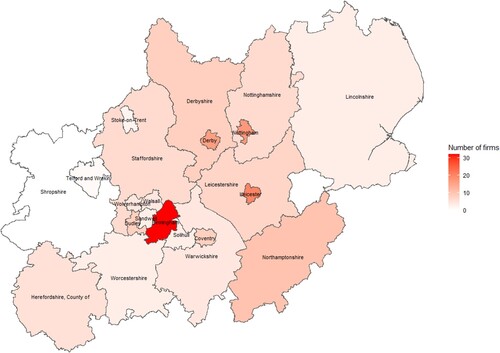

In terms of the profile of automotive respondents, 65 were exclusively involved in automotive manufacture; three were exclusively involved in non-auto road vehicles; 24 were mixed manufacturers; and a further 22 were freight/logistics firms serving the automotive sector. The geographical spread of manufacturers is depicted in . Evident is a preponderance of respondents located in Birmingham, although we note again that the sample is non-probabilistic and the number of firms is only very loosely linked to sectoral output, which is dominated by a small number of large firms.

Figure 3. Number of manufacturing firms by council area.

A breakdown of firm respondents by perceived position in the supply chain and employment size threshold is provided in Tables A1–A4 in the supplemental data online. The survey questionnaire specifically sought to assess which of the rail, automotive and aerospace sectors respondents’ firms operated in (some operated in more than one sector). Although the impact of related variety on regional resilience is potentially ambiguous (Martin & Sunley, Citation2014), in this case diversification across industries is likely to be positive for resilience. The survey also asked which OEMs accounted for a given percentage of turnover; whether they imported and/or exported goods from the EU; what transport routes (e.g., trunk roads) were used and what ports/airports they used for EU trade. In so doing, the questionnaire sought to assess vulnerability, particularly in terms of connectivity and supplier/customer disruptions (Pettit et al., Citation2010). Brexit is an interesting phenomenon in this regard because much supply-chain research has focused on unexpected events (Chowdhury et al., Citation2019; Pettit et al., Citation2019). In contrast, Brexit was a specific, known disruptive process and in spite of uncertainty over the outcome there were clear actions that would mitigate risk. Again, understanding such firm-level responses is important in informing the ramifications for the wider literature.

A range of ‘Brexit exposure’ questions relating to preparedness in terms of customs, value-added tax (VAT), human resources (HR), regulatory compliance, logistics and supply chain management issues were also asked. These attempted to assess the extent to which firms proactively prepared, a recurring theme in the literature around Brexit and resilience throughout the supply chain (Roscoe et al., Citation2020). The survey also provided quite granular data (down to five-digit Standard Industrial Classification (SIC) equivalent) on the specific industrial area that these firms operate in. As such, the questions were deliberately practically focused, which was an inevitable (and desirable) result of our methodological approach.

These themes and specific questions were largely asked based on issues that had been repeatedly raised by trade body and policy reports. For example, the possibility of major disruption on the Dover–Calais route (both via sea and the Channel Tunnel) had been repeatedly raised as a serious risk to just-in-time production (House of Commons, Citation2018). Hence, detailed questions were asked around companies’ choice of transport routes when importing and exporting (including ports of entry/egress as well as the domestic road infrastructure on routes to and from them. Likewise, given the mooted supply-chain disruption (Roscoe et al., Citation2020; Safonovs & Upadhyay, Citation2017) and modest domestically sourced content in the UK’s automotive industry (Howleg et al., Citation2017), a number of questions focused carefully on companies’ awareness of their supply-chain readiness and strategic choices around sourcing (a factor that subsequently grew in importance given the pandemic and subsequent limited supplies of semiconductors).

In the subsequent findings section, we group the survey results into four key areas, which are summarized in .

Table 4. Key themes within the survey.

FINDINGS

We group our findings in terms of four themes: OEM exposure; EU trade exposure; workforce exposure; and Brexit preparedness.

OEM exposure

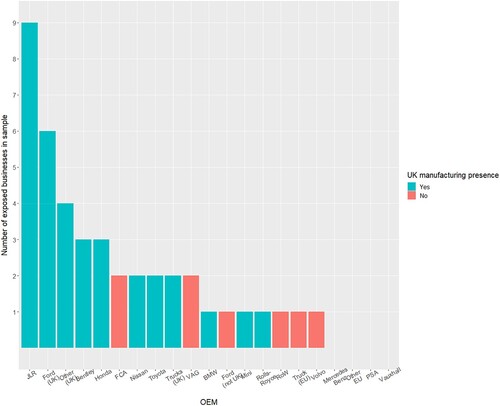

Plant closure potentially poses significant challenges to suppliers. Honda ceased car assembly in the UK in 2001, and Ford at Bridgend has likewise recently terminated petrol engine production. Other plants including in the supply chain in the UK are at risk, with suppliers inevitably exposed to this; notably the case of the GKN Driveline plant in Birmingham which is currently earmarked for closure (Bailey & Rajic, Citation2022). We define ‘exposure’ as having a single OEM account for over 20% of revenue, which is widely accepted in management texts.Footnote3 Evidence of this from our survey is depicted in . This is problematic insofar as suppliers and OEMs enjoy a symbiotic relationship shaped by close cooperation in terms of product development (Sturgeon et al., Citation2009). Unsurprisingly, demonstrates the expected pattern of high exposure to firms with a substantial UK-based manufacturing presence (note that firms can be ‘exposed’ to more than one OEM), and particularly acute exposure to those with local manufacturing plants (namely, Jaguar Land Rover (JLR) and Toyota).

Figure 4. Number of exposed firms (more than 20% of revenue).

The predominance of JLR is further underscored by this analysis and reiterates the importance of this vehicle manufacturer to the continued viability of the automotive manufacturing sector in the UK and particularly within the West Midlands. Indeed, such is the degree of value-added by JLR in the West Midlands that it should be considered as a ‘strategic asset’ for the UK; this is considered further below on policy implications. The spatial element of value creation and capture (Henderson et al., Citation2002) is critically important, yet often underappreciated by national policymakers (Bailey et al., Citation2019). We can see this demonstrated in practice: whilst it is clear that a significant proportion of total automotive value-added is captured by OEMs, a significant portion of this is captured by design and engineering activities. On a technical level, this should not be surprising: compensation of employees is usually the largest component of value-added. Since engineers and designers are typically highly paid in comparison with those elsewhere in the business, the region(s) in which they are located therefore by definition capture a large proportion of total value-added. The same applies to head office locations since executive salaries dwarf those of the average employee.

As a result, regions such as the East Midlands that predominantly specialize in the final assembly of mass market products typically capture a much smaller proportion of total value-added than those that include significant research and development (R&D) spending (notably including the West Midlands). Since these processes are inherently symbiotic (one cannot mass manufacture a product that has not been designed and the value of said design is only realized when a product is actually produced), there are difficulties inherent in ascribing value-added (and especially profits) to a particular location. Indeed, these practical difficulties reinforce the multi-scalar nature of the processes underlying the creation and capture of value. Indeed, as explicitly pointed out by Coe et al. (Citation2004, p. 470), ‘regional development is shaped […] by a variety of extra-local institutions’. In the context of Brexit, this is critical: regionally specific institutions have no power to shape the outcome of Brexit – they lack agency. Instead, agency lies entirely with national and supra-national actors. This matters precisely because policies pursued by those extra-regional actors will interact with regional institutions (and global production networks associated with them) in order to shape regional outcomes.

Of course, automotive firms have significant prior investments in the UK (and hence sunk costs) that will likely see them having to continue to hold substantive manufacturing operations in the country (in the short-term at least). Nevertheless, given the NTBs now in place, parts of the sector remain at risk. This reiterates the need for both supply chain diversification and support for domestic operations (a theme taken up in the policy section below). This particularly applies to JLR given the value of its R&D and design operations in the UK. Next, we turn to examine the nature of importing and exporting to other EU states in order to ascertain the nature of Brexit ‘exposure’. Following this, we then offer an analysis of the nature of job exposure for the sector.

EU trade exposure

The EU is the UK’s largest trading partner, and this is even more pertinent for the transport manufacturing sector, with supply chains deeply entwined with those in EU countries (especially Germany). In terms of manufacturers studied, a large majority (82.6%) of firms surveyed import from the EU. In contrast, only 14.1% stated that they did not (a further 3.3% did not answer the question). This trading intensity did not differ much between the East and West Midlands – 89.5% of firms in the former and 85.3% of firms in the latter import from the EU. Almost all (89.6%) of the larger manufacturers imported from the EU, whilst 90.9% of medium-sized firms imported from the EU. In contrast, ‘only’ 68.4% of small manufacturers did so. The findings were very similar for exporters (87.5% of larger manufacturers, 85.7% of medium ones but only half of smaller ones). Likewise there were only modest differences between regions (84.2% of firms in the East Midlands and 79.5% in the West Midlands respectively export to the EU). In terms of the mode of transport used to import and export products or components, of those manufacturers who gave a response, approximately half (55.8%) imported components via rail. This figure was lower for freight/logistics firms involved in the automotive and road vehicle manufacturing sectors (at 45%). This propensity was greater for manufacturers in the East Midlands (64.7%) than the West Midlands (50.8%). presents the disaggregation of the manufacturers that imported and manufacturers that exported considering the size of firms by employee numbers.

Table 5. Import and export transport mode by firm size.

In considering the mode of transport used to move freight to and from the EU to the UK, only freight shipped by air is likely to be unaffected by Brexit. For all firms and particularly for SMEs, heavy dependence on the Channel Tunnel rail link is a particular concern as its combination of speed and cost is unlikely to be replicable via any other source. These firms are likely to be highly vulnerable to Brexit disruption. In contrast to the prevailing media narrative, product shipped by sea is somewhat less vulnerable in many cases,Footnote4 being more cost sensitive (and commensurately less time sensitive). In contrast to expectations, only a minority of firms import through the Dover sea port (31.6%), although the figure for firms that import by sea at all is higher (45.3%). Few firms use Dover exclusively, although it is used more heavily by larger firms. Crucially, however, a large majority of firms of all sizes use some combination of Dover and the Channel Tunnel and as by far the shortest sea crossing it is crucial. There were no significant differences between the two regions.

As such, the analysis suggests that for companies in the sample, the continental rail link is more important for just-in-time components than the Dover–Calais ferry service. What is likely to occur even with the UK–EU trade deal, however, is rerouting of freight traffic through alternative ports in the event of customs delays. In this sense, Felixstowe/Harwich (depending on whether Ro-Ro or Lo-Lo traffic is required) and Southampton are likely to prove key ports, with the A14 and A34/M3 trunk roads likely to provide several ‘pinch points’. Similarly, the analysis strongly suggests that issues might also arise on freight rail links.

Workforce exposure

Unsurprisingly, the survey results are suggestive of high dependency on EU workers. This has implications for both regional and sectoral resilience, implying a reduction in the ability to recover from a shock due to supply-side (skills) constraints, noting that risk is borne unequally by different market participants. Questions on the workforce composition revealed a high dependency on EU workers across the considered transport sectors. Insofar as the expertise of EU workers boosted these firms’ capabilities, there are clear risks arising from Brexit. Linear interpolation of size categoriesFootnote5 indicates that, on average, 30.6% of the total automotive manufacturing workforce in our survey was from EU member states. However, this varied substantially by firm size and location, ranging from 25.2% for the very largest firms (500 or more employees); 38.9% for large firms (251–500); 13.1% for medium firms (51–250), and just 8% for small firms (fewer than 50 employees). Likewise, firms in the West Midlands appear more dependent on EU labour than those in the East Midlands with an estimated 36.2% of their workforce from the EU in the former compared to just 27.5% in the latter. Evident from some firms within the sample was an extremely high reliance on EU workers, with several respondents indicating that a majority of their employees were from the EU-27, suggesting a problem of skill mismatches in terms of industry needs and that supplied by the domestic labour market. This over-representation of EU workers may be considered as an indicator of Brexit exposure. The sector appeared to be highly dependent on the EU not only in terms of trade and competitiveness but also in terms of high-skilled labour. It reveals the fragility of the business model pursued by firms in the sector. This fragility was reinforced by the lack of stable long-term business relationships of smaller UK suppliers enjoyed by some of their counterparts elsewhere (e.g., in the German Mittelstand).

Moreover, whilst the context is Brexit, the problem is generalizable: a variety of shocks can lead to a sudden reduction in the flow of skilled labour,Footnote6 particularly when this comes from outside the region or country in question. There are clear policy ramifications in terms of skills upgrading and facilitating and incentivising retraining, as discussed later. The West Midlands is much more acutely affected than the East given that it accounts for 33.3% of total employment in Great Britain’s automotive industry (ONS, Citation2019) in spite of accounting for less than 8.9% of the UK’s population (ONS, Citation2020a). This is in part due to the presence of JLR, which employs some 25,000 people and undertakes significant R&D and value-added activities within the region. In contrast, the East Midlands accounts for 7.2% of the UK’s population (ONS, Citation2020a), but only 5.0% of automotive employment (ONS, Citation2019). Unlike the West Midlands, the automotive industry in the East Midlands focuses primarily on final assembly (particularly Toyota) of lower cost vehicles.

Brexit preparedness

The survey results further highlight questions about the disparity in Brexit readiness levels amongst OEMs and suppliers in the automotive sector. At one end of the spectrum were companies with no or minimal understanding of readiness to Brexit, whilst on the other are companies that have thought through and may even be prepared to mitigate the impact of Brexit. For example, at least one supplier had chosen to invest in expanding production in the EU rather than the UK so as to serve OEMs located in the EU (a production relocation decision).

Worryingly, only 51% of manufacturing firmsFootnote7 that we surveyed (at the end of 2019) had fully prepared for the impact of Brexit on their suppliers, and there were no significant differences between larger and smaller manufacturers.Footnote8 The overwhelming majority of firms (89%) had increased inventory levels. While these stocks were then run down during the Covid-19 pandemic, and there was a later stockpiling effort in the run up to the end of 2020. Of more significant concern was the fact that only 34% had completed detailed and accurate activities around commodity code and product classification. Similarly, only 21% of respondents felt that their organization was wholly prepared with the necessary skills to complete new customs requirements related to trade with the EU. A majority felt that they were at medium risk (63%), with the remainder of firms highly exposed on this front. While more businesses are likely to have prepared since then, uncertainty over the terms of the trade deal right up until the end of 2020 hampered business preparations. For all of these metrics, differences between the two regions were very small and not statistically significant.

In response to the potential impacts of Brexit, conventional approaches to supporting supply chains have been to emphasize increased supply-chain (as opposed to regional) resilience and ease to adapt to a new environment. One aspect of this is to reduce the impact of the so-called ‘bullwhip effect’ – that is, the distortion of demand information when traveling upstream in the supply chain, which can generate severe inefficiencies within the whole supply chain (Costantino et al., Citation2013). Re-segmenting supply chains (Safonovs & Upadhyay, Citation2017) could also be possible responses to enhance supply chain resilience. Since both of these worsen the cost–capability ratio (Yeung & Coe, Citation2015), it is probable that supplier re-evaluation will occur, as firms look to optimize existing supply chains and deal with the supplier impact brought about by Brexit.

However, no business responses take place in a spatial vacuum: there are likely to be wider ramifications for regional infrastructure from business re-evaluations of supply-chain logistics. A key point here is that the actions undertaken by the sector to boost sectoral resilience (Fromhold-Eisebith, Citation2015; Bentley et al., 2017)Footnote9 could in turn have a negative regional impact. Such actions might include, inter alia: market reorientation; value chain reorientation; corporate reorganization; the relocation of production, and so on). In this regard there is a disconnect between sectoral and regional resilience. Some of the responses described above could entail changes in the route of transport or mode of transport – or both, depending on the situation facing any business. Small-scale niche producers, such as Aston Martin in the West Midlands, for example, have stated that they would look to airfreight in parts and components in order to overcome any disruptions at ports and the Eurotunnel (Perez, Citation2019) in the short term.

For landlocked regions, these concerns take on particular saliency as disruptions arising elsewhere (notably the south-east of England) could have cumulatively negative knock-on effects as firms operating in the Midlands have to contend with congested transport routes that pass around (typically via the M25) heavily populated areas such as London. For businesses and regional planners then, connectivity (both in the physical and digital sense) is critical; and any Brexit disruption might well incur a cost in terms of the need to upgrade infrastructure, be it in terms of broadband coverage, or major east–west road links. There are, in turn, implications for regional governance arrangements in terms of ensuring that current governance structures enable sufficient place leadership to ensure a rapid, coordinated response to ongoing regional shocks.

In the discussion that follows, policy measures to underpin the sector and thereby promote regional resilience are detailed.

REGIONAL INDUSTRIAL POLICY BEYOND BREXIT: PROMOTING REGIONAL RESILIENCE

Regional industrial policy necessarily needs to interact with these impacts, whilst accounting for national and supranational decision-making. Indeed, this has broader applicability beyond that of Brexit with key salience for the broader research agenda around regional resilience in the face of disruption. Whilst regional resilience has traditionally been conceived of in terms of economic shocks (Fingleton et al., Citation2012), arguably another contribution relates to ‘disruption’ of existing networks. Disruption, as a concept, encompasses an extremely broad array of events and processes. Where a ‘shock’ is clearly identifiable, often representing a break in a time series or a specific event, ‘disruption’ can also refer to an ongoing ‘slow burn’ process whose nature and impact evolves over time. This might be true of various forms of ‘structural change’, or alterations in the political system. Brexit is best conceived of as a process rather than an event. It represents a change in a relationship, but the nature of this is likely to change over time and dealing with it will require regional and industrial adaptation to a continuously changing environment requiring a strong capacity to adapt and create new development paths. Moreover, unlike a typical recessionary shock, its existence (or potential existence) has been clearly signposted for some years in advance and likely to go on for some time.

Thus, whilst 1 January 2021 might have represented a ‘shock’ in the conventional sense, some of the impacts of Brexit had already been felt (such as in a significant fall in investment and loss of economic activity; Dhingra & Sampson, Citation2022) and further impacts will be felt over time. Changes of government and policy in the UK and the EU are likely to ensure that whatever is agreed is far from permanent. Yet notions of ‘resilience’ (Martin, Citation2011; Bailey & Turok, Citation2016) are useful in framing discussion around regional disruptions. However, the level of regional resilience to disruption varies according to the nature of the shock at hand and industrial make-up of the region. The economic structure of the West Midlands in particular renders its ‘resistance’ to Brexit unusually low. It is vulnerable to the shock of Brexit precisely due to the preponderance of manufacturing industries which trade with the EU, and particularly the automotive industry, with a high dependency on EU trade.

There is an implied need for ‘reorientation’, which, as identified in the literature, is inherently related to regional resistance (Martin, Citation2011) (addressing the first two themes in the findings above). This implies that a medium-term aim of regional policymakers should be encouraging industrial diversity and technological and skills diversification (addressing the third theme), cognisant of the benefits of agglomeration (Frenken et al., Citation2007; McCann & Ortega-Argilés, Citation2015) although the ‘devolution offer’ outlined in the recent Levelling Up White Paper (Secretary of State for Levelling Up, Housing and Communities, Citation2022) falls short of being able to develop such a regional industrial policy, with a centralist instinct firmly in place in UK government (Wincott, Citation2022). Addressing skills gaps after Brexit will be vital in facilitating this as part of a wider regional industrial policy in order to attract (and foster) businesses that make use of those new skills.

However, the recovery from Brexit as a disruptive event will depend on more than just the ability of the region to reorient (or pivot) towards growth sectors. It will, in large part, depend upon actions at the state level since regional policymakers lack agency in this domain. Whilst there is widespread agreement that Brexit is likely to be economically damaging (Chen et al., Citation2018; Dhingra et al., Citation2017; Los et al., Citation2017; Thissen et al., Citation2020), it is nevertheless clear that the impact, including the sector-level impact (Lawless & Morgenroth, Citation2019), will depend crucially on the evolution of the future relationship between the UK and EU, and in particular the nature of the trade relationship with the EU. The UK–EU Free Trade Agreement provides a starting point for this in avoiding tariffs and quotas (subject to complying with Rules of Origin rules) but imposes many non-tariff costs on the auto sector.

In addition, a point to note from our analysis of sectoral resilience is that the trajectory of a sector has an impact on regions (Bentley, Citation2018). In line with Fromhold-Eisebith (Citation2015, p. 1690):

the interplay of sectoral and regional resilience can further be investigated by analyzing how interregional differences in resilience may be attributed to the sector composition of regions. … These insights pave the way for more adequate policies supporting the resilient capacities of regions through those of industrial sectors, and vice versa.

Regional renewal post-Brexit could be facilitated by a regional industrial policy combined with comprehensive action at the regional level on skill retention and training/retraining in local firms (Billing et al., Citation2019; Billing et al., Citation2020) (addressing the third theme). The latter is seen as especially pertinent in the context of the shift to electrification in the auto industry and the need for a ‘Just Transition’. In addition, removing major transport bottlenecks via enhancements to infrastructure will play a crucial role in facilitating regional recovery from disruption (addressing the second and fourth themes). At the sectoral and macro levels, the specific policy proposals that follow this research are that the UK Government should consider a range of actions (Oh, Citation2014). These might include short-time working support – building on the government’s Covid-19 furlough scheme and building it into a part-time support scheme akin to the German Kurzarbeit scheme tailored to local firms’ needs (addressing the first theme). Financial support could be provided through loan guarantees and even taking equity stakes in manufacturers. For example, the French government has provided loan guarantees to Renault during the Coronavirus pandemic. While the UK government looked at providing support via ‘Project Birch’, little financial support for manufacturing has been forthcoming beyond the government’s furlough scheme to keep workers on. The UK government could also consider regional investment support schemes – this could be in the form of an extended or broader Regional Growth Fund with preference given to companies which also committed to the use of domestic suppliers.

While some policy options open to support existing manufacturing will depend on the central government, there are some policy actions which local government, local enterprise partnerships (LEPs), Combined Authorities and the Midlands Engine could consider in order to deal with Brexit-induced economic disruption. These could potentially include helping firms deal with the extra NTBs introduced by Brexit – such as customs declarations and documenting rules of origin requirements (addressing the fourth theme). This could involve training of staff as well as ensuring easy access to support, especially for smaller firms which have struggled with such requirements. In addition, training support could be made available to help companies retrain and reskill workers – not only to fill skills gaps but also to help firms reorientate towards the production of components for electric vehicles and to diversify into other areas (such as the green energy supply chain); this will anyway be critical with the advent of Industry 4.0 (De Propris & Bailey, Citation2020) (the first three themes).

Given ongoing disruption, regional policy makers could offer a loan fund for firms in the supply chain. This was used in the case of the Rover Task Force and also in the wake of the Global Financial Crisis (GFC) (Bailey & Berkeley, Citation2014) to support the sector at the regional level. This could link with offering diversification support for firms in the industry regionally (the first and second themes). This was significant and important in both the MG Rover collapse (Bailey & MacNeill, Citation2008) and in the wake of the GFC and helped re-orientate the regional economy into faster growing areas. Today it could foster a shift into electrification and green technologies as well as related software areas (artificial intelligence (AI), robotics, data analysis, etc.) Linked to this, the region could make the case for establishing special enterprise zones with strong connectivity and a range of tax incentives. These could support the growth of key new technologies in the region (e.g., building batteries at scale in ‘gigafactories’) so as to anchor car assembly. This in turn may require infrastructure improvements which could also help firms overcome logistic challenges post Brexit (the first and second themes).

These points are especially relevant as the UK–EU trade deal will require batteries in electric cars to be assembled in the UK or EU from the end of 2026 to avoid tariffs, and the UK lags behind in this regard (Bailey & Rajic, Citation2022). Pulling together such approaches could be done through a regionally based ‘task force’ approach. Taskforces were set up around Rover and LDV and at the region level in the wake of the GFC. This could be reactivated under the remit of the Combined Authority or Midlands Engine partnership, with a clear remit and resources and working in partnership with local firms.

CONCLUSIONS

This paper has investigated the impact of trade dis-integration on the automotive sector in the East and West Midlands of the UK as a long-run slow burn process and considers the ramifications for industrial policy and resilience arising therefrom. These are illuminating case studies given their vulnerabilities to Brexit disruption due to the intricate nature of their trading relationships with the EU. Detailed survey data has brought out four major themes: OEM dependent exposure; EU trade exposure; workforce exposure; and Brexit preparedness. Across all four we find significant subnational ramifications from Brexit trade disruption, with Brexit seen as having a ‘slow burn’ disruptive impact. For example, trade disruption poses existential risks to delicate just-in-time supply chains. Since industries are spatially concentrated – and the automotive sector is a prime example of this phenomenon – the regional impact of trade disruption is significant in both the short and longer term. In this regard, the actions taken by firms to mitigate Brexit risks and maintain sectoral resilience impact regionally, with a consequence for regional resilience.

While there are no ‘quick fix’ industrial policy solutions to these issues, the analysis presented here points to the need for an appropriate regional industrial policy to anticipate and mitigate some of these impacts with a focus on regional resilience and sustainability of the regional industrial ecosystem. Whilst this needs coordinating with national-level policies, it could take a range of approaches in limiting the impact of disruption (resistance), promoting recovery and enabling opportunities for renewal and reorientation through a partnership approach between regional bodies and business. Particular attention needs to be paid to the development of skills in the region and the changing demands of an evolving sector (particularly with disruption linked to automation, digitalization and globalization far beyond the EU).

Indeed, this links industrial policy debates with notions of resilience by Martin (Citation2011) in positing a wider agenda around both regional reorientation – to enable a focus on growth industries at a time of disruption – and recovery from a potentially transformative disruption to trade. As regards the latter, we find that agency is a key concept, noting that the highly centralized administrative governance arrangements within England are inimical to coherent regional policymaking at the micro and meso-scales. A significant danger arises for policy making with the effective abolition of the government’s industrial strategy. We thus suggest that genuine devolution of both financial resources and, crucially, power is necessary (but perhaps not sufficient) to deal with the consequences of ongoing disruptive events adequately.

Supplemental Material

Download PDF (92.8 KB)DISCLOSURE STATEMENT

No potential conflict of interest was reported by the authors.

Additional information

Funding

Notes

1. These were the West Midlands metropolitan area; the region of Herefordshire, Worcestershire and Warwickshire in the West Midlands; and the region of Derbyshire and Nottinghamshire in the East Midlands.

2. There are several reasons for this. There is evidence that firms misclassify themselves (De Ruyter et al., Citation2021). Moreover, classification involves a firm’s primary activity, but many firms derive a significant portion of their revenues from ancillary activities. Finally, many firms which are (correctly) classified in non-automotive sectors are part of the automotive supply chain (e.g. metal fabrication, plastics and rubber etc.).

3. For example, see https://www.eulerhermes.com/en_US/resources-and-insights/economic-insights/avoid-high-customer-concentration.html; and https://www.msn.com/en-sg/money/news/what-you-need-to-know-about-customer-concentration-risk/ar-BBVmlNk/.

5. Specifically, the survey asked which size category firms fell into, thus meaning that although we know whether firms are small, medium or large, we do not know the exact number of employees in each firm. Thus, linear interpolation is between size categories. Although simple, this captures most information and has the benefit of being easily interpretable and replicable.

6. Changes in visa requirements, currency movements, post-recession hysteresis, policy decisions that change the pipeline of skilled labour, etc.

7. Specifically, 91.3% of firms gave a valid answer to the question, and of these, 51.2% had fully prepared for the impact of Brexit on their suppliers.

8. There is some weak evidence that small firms (with fewer than 50 employees) are somewhat less prepared than larger ones, but the differences are not statistically significant.

9. This can be seen as part of the ‘industrial ecosystem’ dimension of resilience (Kitsos et al., Citation2019) – our point here is that sectoral resilience plays out with spatial implications, and hence impacts on regional resilience.

REFERENCES

- Bailey, D., & Berkeley, N. (2014). Regional responses to recession: The role of the West Midlands regional taskforce. Regional Studies, 48(11), 1797–1812. https://doi.org/10.1080/00343404.2014.893056

- Bailey, D., Driffield, N., & Kispeter, E. (2019). Brexit, foreign investment and employment: Some implications for industrial policy? Contemporary Social Science, 14(2), 174–188. https://doi.org/10.1080/21582041.2019.1566563

- Bailey, D., & MacNeill, S. (2008). The Rover Task Force: A case study in proactive and reactive policy intervention? Regional Science Policy & Practice, 1(1), 109–124. https://doi.org/10.1111/j.1757-7802.2008.00007.x

- Bailey, D., & Rajic, I. (2022). Manufacturing after Brexit (UK in a Changing Europe Research Report). https://ukandeu.ac.uk/research-papers/manufacturing-after-brexit/

- Bailey, D., & Tomlinson, P. (2021). Industrial strategy: Building back badly. UK in a Changing Europe. https://ukandeu.ac.uk/industrial-strategy-building-back-badly/

- Bailey, D., & Turok, I. (2016). Editorial: Resilience revisited. Regional Studies, 50(4), 557–560. doi:10.1080/00343404.2016.1146478

- Bentley, G. (2018). Territory, policy and governance at meso-scale: The Midlands engine. In F. Fai (Ed.), Place-based perspectives on the UK industrial strategy (pp. 22–33). University of Bath.

- Berden, K. G., Francois, J., Thelle, M., Wymenga, P., & Tamminen, S. (2009). Non-tariff measures in EU-US trade and investment – An economic analysis (OJ 2007/S 180-21949). ECORYS Nederland BV. https://www.gtap.agecon.purdue.edu/resources/download/5177.pdf

- Billing, C., McCann, P., & Ortega-Argilés, R. (2019). Interregional inequalities and UK sub-national governance responses to Brexit. Regional Studies, 53(5), 741–760. https://doi.org/10.1080/00343404.2018.1554246

- Billing, C., McCann, P., Ortega-Argilés, R., & Sevinc, D. (2020). UK analysts’ and policy-makers’ perspectives on Brexit: Challenges, priorities and opportunities for subnational areas. Regional Studies, 55(9), 1571–1582. https://doi.org/10.1080/00343404.2020.1826039.

- Brown, R., Liñares-Zegarra, J., & Wilson, J. O. S. (2019). The (potential) impact of Brexit on UK SMEs: Regional evidence and public policy implications, Regional Studies, 53(5), 761–770. doi:10.1080/00343404.2019.1597267

- Chen, W., Los, B., McCann, P., Ortega-Argilés, R., Thissen, M., & van Oort, F. (2018). The continental divide? Economic exposure to Brexit in regions and countries on both sides of The Channel. Papers in Regional Science, 97(1), 25–54. https://doi.org/10.1111/pirs.12334

- Chowdhury, M. M. H., Quaddus, M., & Agarwal, R. (2019). Supply chain resilience for performance: Role of relational practices and network complexities. Supply Chain Management, 24(5), 659–676. https://doi.org/10.1108/SCM-09-2018-0332

- Coe, N. M., Hess, M., Yeung, H. W.-c., Dicken, P., & Henderson, J. (2004). ‘Globalizing’ regional development: A global production networks perspective. Transactions of the Institute of British Geographers, 29(4), 468–484. https://doi.org/10.1111/j.0020-2754.2004.00142.x

- Costantino, F., Di Gravio, G., Shaban, A., & Tronci, M. (2013). Exploring the bullwhip effect and inventory stability in a seasonal supply chain. International Journal of Engineering Business Management, 5, 23. https://doi.org/10.5772/56833

- Dawley, S., Pike, A., & Tomaney, J. (2010). Towards the resilient region? Local Economy, 25(8), 650–667. https://doi.org/10.1080/02690942.2010.533424

- De Propris, L., & Bailey, D. (2020). Industry 4.0 and regional transformations. Routledge. https://doi.org/10.4324/9780429057984

- De Ruyter, A., Hearne, D., & Henry, I. (2021). The resilience of advanced manufacturing supply chains across the Midlands. https://www.midlandsengine.org/wp-content/uploads/Manufacturing.pdf

- De Ruyter, A., Salh, S., Shishank, S., Li, D., Bailey, D., Hearne, D., … Ali, S. (2018). Brexit and the UK automotive industry: Understanding the impact. https://bcuassets.blob.core.windows.net/docs/report-for-opentext–deliverable-b-final-131880562823173347.pdf

- Dhingra, S., Huang, H., Ottaviano, G., Paulo Pessoa, J., Sampson, T., & Van Reenen, J. (2017). The costs and benefits of leaving the EU: Trade effects. Economic Policy, 32(92), 651–705. https://doi.org/10.1093/epolic/eix015

- Dhingra, S., & Sampson, T. (2022). Expecting Brexit (Discussion Paper No. DP16970). Centre for Economic Policy Research (CEPR). https://ssrn.com/abstract=4026876; https://doi.org/10.2139/ssrn.4023854

- Fingleton, B., Garretsen, H., & Martin, R. (2012). Recessionary shocks and regional employment: Evidence on the resilience of U.K. regions. Journal of Regional Science, 52(1), 109–133. https://doi.org/10.1111/j.1467-9787.2011.00755.x

- Frenken, K., Van Oort, F., & Verburg, T. (2007). Related variety, unrelated variety and regional economic growth. Regional Studies, 41(5), 685–697. https://doi.org/10.1080/00343400601120296

- Fromhold-Eisebith, M. (2015). Sectoral resilience: Conceptualizing industry-specific spatial patterns of interactive crisis adjustment, European Planning Studies, 23(9), 1675–1694. doi:10.1080/09654313.2015.1047329

- Henderson, J., Dicken, P., Hess, M., Coe, N., & Yeung, H. W.-c. (2002). Global production networks and the analysis of economic development. Review of International Political Economy, 9(3), 436–464. https://doi.org/10.1080/09692290210150842

- Her Majesty’s Revenue and Customs (HMRC). (2020a). Regional trade statistics. https://www.uktradeinfo.com/Statistics/RTS/Pages/default.aspx

- Her Majesty’s Revenue and Customs (HMRC). (2020b). UK overseas trade statistics: Interactive tables. https://www.uktradeinfo.com/trade-data/rts-custom-table/

- HM Government. (2018). EU exit: Long-term economic analysis (Cm9742). Her Majesty's Stationary Office (HMSO). https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/760484/28_November_EU_Exit_-_Long-term_economic_analysis__1_.pdf

- House of Commons. (2018). The impact of Brexit on the automotive sector. Fifth report of the Business, Energy and Industrial Strategy Committee Session 2017–19. London.

- Howleg, M., Davies, P., & Wood, M. (2017). Growing the automotive supply chain: Local vehicle content analysis. https://www.automotivecouncil.co.uk/wp-content/uploads/sites/13/2017/06/Automotive-Council-UK-local-sourcing-content-research-2017-Final-1.pdf

- Kerridge, M. (2018). The impact of Brexit on the transport industry’. Logistics and Transport, 40(4), 35–42. https://doi.org/10.26411/83-1734-2015-4-40-5-18

- Kitsos, A., & Bishop, P. (2018). Economic resilience in Great Britain: The crisis impact and its determining factors for local authority districts. The Annals of Regional Science, 60(2), 329–347. https://doi.org/10.1007/s00168-016-0797-y

- Kitsos, A., Carrascal-Incera, A., & Ortega-Argilés, R. (2019). The Role of embeddedness on regional economic resilience: Evidence from the UK. Sustainability, 11(14). https://doi.org/10.3390/su11143800

- Lawless, M., & Morgenroth, E. L. W. (2019). The product and sector level impact of a hard Brexit across the EU. Contemporary Social Science, 189–207. https://doi.org/10.1080/21582041.2018.1558276

- Los, B., McCann, P., Springford, J., & Thissen, M. (2017). The mismatch between local voting and the local economic consequences of Brexit. Regional Studies, 51(5), 786–799. https://doi.org/10.1080/00343404.2017.1287350

- Martin, R. (2011). Regional economic resilience, hysteresis and recessionary shocks. Journal of Economic Geography, 12(1), 1–32. https://doi.org/10.1093/jeg/lbr019

- Martin, R., & Sunley, P. (2014). On the notion of regional economic resilience: Conceptualization and explanation. Journal of Economic Geography, 15(1), 1–42. https://doi.org/10.1093/jeg/lbu015

- McCann, P., & Ortega-Argilés, R. (2015). Smart specialization, regional growth and applications to European Union cohesion policy. Regional Studies, 49(8), 1291–1302. https://doi.org/10.1080/00343404.2013.799769

- Office for National Statistics (ONS). (2019). Business register and employment survey. https://www.nomisweb.co.uk/query/construct/summary.asp?mode=construct&version=0&dataset=189

- Office for National Statistics (ONS). (2020a). Estimates of the population for the UK, England and Wales, Scotland and Northern Ireland. https://www.ons.gov.uk/peoplepopulationandcommunity/populationandmigration/populationestimates/datasets/populationestimatesforukenglandandwalesscotlandandnorthernireland

- Office for National Statistics (ONS). (2020b). Input–output supply and use tables. https://www.ons.gov.uk/economy/nationalaccounts/supplyandusetables/datasets/inputoutputsupplyandusetables

- Office for National Statistics (ONS). (2020c). UK business: activity, size and location. https://www.ons.gov.uk/businessindustryandtrade/business/activitysizeandlocation/datasets/ukbusinessactivitysizeandlocation

- Office for National Statistics (ONS). (2021). Regional gross domestic product all NUTS level regions. ONS. https://www.ons.gov.uk/economy/grossvalueaddedgva/datasets/nominalandrealregionalgrossvalueaddedbalancedbyindustry

- Oh, S. (2014). Shifting gears: Industrial policy and automotive industry after the 2008 financial crisis. Business and Politics, 16(4), 641–665. doi:10.1515/bap-2014-0015

- Perez, I. G. (2019). Aston Martin board approves air freight in Brexit planning. Bloomberg. https://www.bloomberg.com/news/articles/2019-01-07/aston-martin-board-approves-air-freight-in-Brexit-planning

- Pettit, T. J., Croxton, K. L., & Fiksel, J. (2019). The evolution of resilience in supply chain management: A retrospective on ensuring supply chain resilience. Journal of Business Logistics, 40(1), 56–65. https://doi.org/10.1111/jbl.12202

- Pettit, T. J., Fiksel, J., & Croxton, K. L. (2010). Ensuring supply chain resilience: Development of a conceptual framework. Journal of Business Logistics, 31(1), 1–21. https://doi.org/10.1002/j.2158-1592.2010.tb00125.x

- Roscoe, S., Skipworth, H., Aktas, E., & Habib, F. (2020). Managing supply chain uncertainty arising from geopolitical disruptions: Evidence from the pharmaceutical industry and Brexit. International Journal of Operations & Production Management, 40(9), 1499–1529. https://doi.org/10.1108/IJOPM-10-2019-0668

- Safonovs, R., & Upadhyay, A. (2017). Is your Brexit supply chain resilient enough? The British footwear manufacturers’ perspective. Strategic Direction, 33(11), 34–36. https://doi.org/10.1108/SD-02-2017-0018

- Secretary of State for Levelling Up, Housing and Communities. (2022). Levelling up the United Kingdom. Her Majesty's Stationary Office (HMSO). https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/1052708/Levelling_up_the_UK_white_paper.pdf

- Society of Motor Manufacturers and Traders (SMMT). (2020). SMMT motor industry facts 2020. https://www.smmt.co.uk/wp-content/uploads/sites/2/SMMT-Motor-Industry-Facts-Oct-2020.pdf

- Sturgeon, T. J., Memedovic, O., Biesebroeck, J. V., & Gereffi, G. (2009). Globalisation of the automotive industry: Main features and trends. International Journal of Technological Learning, Innovation and Development, 2(1–2), 7–24. https://doi.org/10.1504/IJTLID.2009.021954

- Thissen, M., van Oort, F., McCann, P., Ortega-Argilés, R., & Husby, T. (2020). The implications of Brexit for UK and EU regional competitiveness. Economic Geography, 397–421. https://doi.org/10.1080/00130095.2020.1820862

- Wincott, D. (2022). The Anglo-British state, Welsh devolution, and the Covid-19 pandemic in England and Wales: Territorial riddles, mysterious boundaries, and enigmatic identities. In V. Molinari & P.-A. Beylier (Eds.), COVID-19 in Europe and North America: Policy responses and multi-level governance (pp. 211–234), De Gruyter Oldenbourg, https://doi.org/10.1515/9783110745085-010

- Yeung, H. W.-c., & Coe, N. M. (2015). Toward a dynamic theory of global production networks. Economic Geography, 91(1), 29–58. https://doi.org/10.1111/ecge.12063