ABSTRACT

The Covid-19 pandemic and Brexit have focused attention on the resilience of key sectors and firms. This paper explores the financial resilience of the 50 largest automotive firms in the West Midlands region of the UK in their response to disruption and economic shocks. The findings demonstrate that 22 firms are at high risk due to poor current liquidity ratios, with Coventry and Birmingham emerging as locations most susceptible to firm closures. High-risk firms include key flagship original equipment manufacturers operating at the downstream end of supply chains. If these firms were to fail, there would be a significant destructive impact on both the industry and the local economy. We assert an effective subnational industrial policy is required in order to support economic resilience in regions such as the West Midlands where a few firms account for a disproportionate share of employment and value-added.

JEL:

1. INTRODUCTION

The outbreak of Covid-19 will have long-term repercussions on the global economy. When a shock impacts an entire industry’s production and sales, these sectors must develop resilience qualities, or the capacity to adapt, and these dynamics are referred to as sectoral resilience (Fromhold-Eisebith, Citation2015). Given the difficulties of precisely defining a sector (Bentley et al., Citation2017), we use Fromhold-Eisebith’s (Citation2015) approach, defining a sector as the sum of all companies and other organizations, no matter where they are located, that contribute to the creation of a specific end product (e.g., automotive vehicles – which is the focus of attention here). Although the aftermath of Covid-19 will impact the entire automotive sector, the West Midlands region in the UK is particularly vulnerable. This is because the West Midlands has a high concentration of jobs in manufacturing and a large proportion of these jobs feed into the automotive sector.

Given the interconnected nature of automotive supply chains, temporary factory shutdowns and interruptions to supply chains require policy intervention. Bailey et al. (Citation2022) specify that in order to quantify the full exposure of a region and sector to disruption, one must consider firm-level differences and embedded linkages at a regional level. Thus, policies aimed at enhancing sectoral and regional resilience need to directly acknowledge and be framed in response to individual business positions and circumstances, as opposed to the reliance on aggregate indicators (sectoral or regional). This guides our focus in this paper and we draw our main insights using firm-level data; more precisely we use financial ratios as a proxy of individual firm resilience.

Before the Covid-19 pandemic the UK automotive industry was suffering from Brexit-related issues (de Ruyter et al., Citation2018) and a significant decline in sales from China. The recent global semiconductor shortage has led to episodic temporary shutdowns of automotive firms. The UK automotive industry produced 987,044 vehicles in 2020, which was 29.3% less than in 2019 (SMMT, Citation2021a). The pandemic has cost businesses £11 billion since March 2020–21 (SMMT, Citation2021b). Although Covid-19 can be seen as a shock, Bailey et al. (Citation2022) assert given the aforementioned conditions (i.e., Brexit, declining sales in China, semiconductor shortage) the UK automotive sector is undergoing a ‘disruptive process’. In this article we concur with the notion that the sector is not just facing a shock; instead of a discrete ‘one-off’ event or series, the automotive sector has been facing continuous disruption over a period of multiple years.

Importantly, two key characteristics of firms and industry sectors are of significance for regional economic resilience or recovery and so of interest to policymakers. The first is the direct exposure of a firm’s (or sector’s) performance to the impacts of shocks and disruption. Increased costs or reduced demand that can impact performance and financial viability can lead to downsizing or restructuring and redundancies. A wholesale collapse of a ‘flagship firm’ (Collinson et al., Citation2020) can lead to large-scale unemployment, with damaging knock-on effects to communities, public services and inequality. This was evident in Wolverhampton (West Midlands) in 2018 when Carillion (a British multinational construction and facilities management company) collapsed (Qamar & Collinson, Citation2018). The second characteristic is the degree to which other firms in the region are dependent on a particular firm or sector. De Ruyter et al. (Citation2021) label these firms ‘anchor firms’ as they tend to attract smaller and innovative firms to cluster around them. This is generalizable not only to the West Midlands automotive sector but also to regions that are relatively dependent on certain sectors (e.g., the East Midlands aerospace sector) or firms (e.g., Waterloo’s (Canada) previous dependence on Blackberry). Multiplier effects, related to the volume and range of buyer–supplier linkages, both positive and negative, depend on the degree to which a firm or sector is ‘embedded’ in a local economy. Thus, in times of disruption and shock, policymakers should consider focusing support on sectors and particular firms that are most at risk of failure, and on those that directly or indirectly support other businesses in the local economy.

The Covid-19-induced economic crisis provides a unique opportunity to analyse corporate resilience through a sectoral and regional lens. Given the UK government’s pledge to help large businesses via the Coronavirus Large Business Interruption Loan Scheme (CLBILS) by facilitating access to loans and other kinds of finance, in this study we investigate the financial health of the largest automotive firms in the West Midlands. This is in line with Gittell et al.’s (Citation2006) work as we argue that organizations need a viable business model that allows financial reserves (i.e., slack resources) to be built up, which can be used during times of crises and uncertainty (Linnenluecke, Citation2017). Slack resources can act as shock absorbers. Absorbed slack is resource within an organization that is already tied to the business, whereas unabsorbed slack is resource that is currently uncommitted and readily available for redeployment. Cash resources are the easiest form of resource that can be redeployed. In this paper we focus on unabsorbed financial slack. Specifically, we use financial ratios such as current ratios, credit scores and profit margins to explore the financial resilience of the 50 largest (in terms of revenue) automotive firms in the West Midlands.

Finally, we reflect on the location-embeddedness of firms within the sector and wider impacts that could be triggered by restructuring or collapse of these firms. Although regions are often subject to sudden, major shocks, and activate policies in response (Martin, Citation2012; Martin & Sunley, Citation2015), these responses should be tailored to the extended structures of firms operating in a region. This is particularly critical, as noted by Kitsos and Bishop’s (Citation2018) work on the economic resilience of regions, when a small number of embedded sectors or firms account for a disproportionate share of employment and value-added within the region. As well as contributing to wider debates around sectoral and regional resilience, our policy recommendations are specifically tailored using a holistic place-based approach, which is in line with Bentley et al.’s (Citation2017) recommendations.

2. THE UK AUTOMOTIVE INDUSTRY

During the 1950s the UK was the largest exporter of automotive vehicles and the second largest nation in terms of vehicle production. UK output peaked during the 1960s and early 1970s; however, slow growth in comparison with rival nations (e.g., Japan, France, Germany and Italy) and competition from overseas multinationals eradicated the nation’s position in this sector. The sector experienced higher levels of global sourcing, and a shift to lower wage cost locations (Bailey & De Propris, Citation2014), leading to a ‘long-run’ trade deficit (Coffey & Thornley, Citation2020).

Historically, there have been several government policies and takeovers to revitalize the sector; however, these attempts have generally been unsuccessful in the long-run (MacNeil & Bailey, Citation2010). For instance, through a series of mergers the British Leyland Motor Corporation, formed in 1968, was arguably disastrous (Donnelly et al., Citation2017), and after many different owners the business collapsed in 2005. Similarly, Rootes was taken over by American giant Chrysler during the late 1960s, and controlled by Peugeot during the late 1970s. Peugeot ceased operations in 2007. This represented the end of mass car production in the West Midlands.

Despite these developments having left UK automotive supply chains fractured (Bailey & De Propris, Citation2014), the sector demonstrated signs of growth from 2010 to 2016. Over £8 billion was injected, including to help the sector respond to the challenge of a carbon-neutral future. Although there were a variety of reasons (high skills base, cooperative working between unions and management, university collaborations, supportive industrial policies) for growth between 2010 and 2016, Bailey & De Propris (Citation2017) assert that a critical reason for success was the UK’s access to the EU Single Market. After the 2016 referendum on UK membership of the EU, Brexit represented a (potential) shock to the automotive sector. Given the ensuing uncertainty concerning a post-Brexit trade deal (with no deal concluded until December 2020), the industry’s health deteriorated. This raised questions concerning the importance of the UK automotive sector and whether automotive investment might go elsewhere.

The automotive sector accounts for over £78.9 billion turnover and £15.3 billion in value-adding activities (SMMT, Citation2021a), employs around 180,300 people directly in automotive manufacturing and over 864,300 across the wider automotive industry (SMMT Citation2021a). It accounts for 13% of total UK exports (worth £42.4 billion). The industry invests £3.75 billion annually in automotive research and development (R&D). Over 30 manufacturers build in excess of 70 vehicle models in the UK, supported by 2400 component providers and some of the world’s most skilled engineers. In 2020, 987,044 cars, 66,116 commercial vehicles and 1.84 million engines were produced in the UK (SMMT, Citation2021a).

The West Midlands has a cluster of organizations (operating at various supply chain positions) and component groups including driveline, chassis and body panel, engine components, interior trim, electrical components and design. Despite a deficiency in skilled labour supply, the region has developed a significant presence in automotive design and engineering, particularly among small and niche firms (Amison & Bailey, Citation2014). Summary statistics show 20 vehicle manufacturing sites, 35 automotive and off-highway original equipment manufacturing (OEM) brands, 26 OEM vehicle R&D centres, eight automotive centres of excellence and four low-carbon centres of excellence (WMREDI, Citation2020). Reflecting the region’s position as a top global location for automotive foreign direct investment (FDI), Qamar et al. (Citation2019a) suggest that foreign-owned multinationals have positioned themselves within the region to exploit the explorative capabilities of domestic firms operating upstream in automotive supply chains. However, these upstream, and often smaller, firms are largely dependent on the success of larger downstream firms. Given the challenges of Brexit, a decline in overseas sales and Covid-19, it is important to understand whether, financially, these downstream firms can weather the storm, let alone compete on a global scale.

Given the number of firms and employees in the region depending on the automotive sector and the resulting proportion of the local economy at risk when sector-specific shocks occur, these are important issues for policymakers with a remit to intervene to support the regional economy. We address the implications of our analysis later but provide an overview of some support measures in the next section.

3. EXAMINING CORPORATE RESILIENCE AND THE IMPACT OF GOVERNMENT FINANCIAL SUPPORT MEASURES

Despite progress in theory and practice concerning firm performance, Markman & Venzin (Citation2014) assert that there has been little development on a robust measure for firm resilience. Within the business and management literature the notion of resilience can be traced to seminal papers by Staw et al. (Citation1981) and Meyer (Citation1982). Both papers used evolutionary theory when outlining propositions about how firms deal and respond to external threats. External shocks and abrupt unexpected events surprise organizations, often leading to disruptions within operations, and with economic consequences which ripple through supply chains (i.e., from raw materials to transportation) across multiple tiers (Linnenluecke, Citation2017). Given the interconnectedness between suppliers and producers (i.e., greater interdependency and complexity among automotive businesses), disruption can lead to further disturbances amongst the supply network and this is referred as the ripple effect (Marcucci et al., Citation2022). Some firms are more successful than others when responding to (or surviving) unexpected abrupt events. The term ‘resilience’ has been widely used in the literature. At organizational level it is about the characteristics which enable firms to respond and recover faster in comparison with others. Resilience is typically observed to be a desirable characteristic. Gittell et al. (Citation2006) drew upon Meyer’s (Citation1982) arguments and advocated that one way that firms can be highly resilient is by developing business models or strategies that allow financial reserves (or slack resources) to be built up. Unabsorbed resources can act as shock absorbers; thus, we argue that firm resilience can be captured by the use of financial ratios (i.e., profit margins, current ratios, liquidity ratios). Collinson and Wilson (Citation2006) link resilience to adaptability, observing that firms with a variety of latent routines, knowledge, capabilities and agency to draw on when needed possess organizational responsiveness and less inertia in the face external change.

During the Covid-19 pandemic, countries across Europe (e.g., Germany, France, Switzerland) were quick to issue government-backed business loans (Makortoff, Citation2020). In April 2020, the UK government declared that they would support large businesses via the Coronavirus Large Business Interruption Loan Scheme (CLBILS).

This scheme supported large businesses with an annual turnover of over £45 million. They could apply for up to 25% of their annual turnover. Initially large organizations could apply for up to £50 million, but this was increased to £200 million. The scheme was open to applications until 31 March 2021. Loans were offered at commercial rates of interest through 27 accredited lenders. The scheme’s aim was to ensure that lenders provided temporary financing to support firms that had bills to pay but were earning little/no revenue. In April 2020 one-quarter of UK businesses had temporarily closed; others closed permanently. Schemes such as CLBILS provide cash flow or liquidity to help firms survive until markets somewhat recovered. The need for these schemes, and the value of them to the economy in terms of helping firms survive and reducing redundancies, varies by sector and firm. This depends on: (1) the degree to which this particular crisis impacts their business; and (2) their level of resilience, including levels of assets, savings or a cash surplus sufficient to survive an economic shock. The Covid-19-induced economic crisis provides a unique opportunity to analyse corporate resilience in a regional context and to assess the role of financial support measures in aiding survival.

4. METHOD AND ANALYSIS

Our approach incorporates measures of the financial resilience of car producers in the face of the economic shock and disruption, to indicate the ‘likelihood’ of collapse. We add to this direct employment as a ‘weighting’ for the scale of the economic and social impact, should a firm collapse.

4.1. Financially, how resilient are regional car manufacturers?

We accessed company information from the Fame Bureau van Dijk database covering approximately 11 million firms within the UK and Ireland (Fame, Citation2020). It includes information concerning finances, shareholders, subsidiaries, Standard Industrial Classification (SIC) codes and industry descriptions. Using this database, we compiled , listing the 50 largest automotive manufacturing firms in the West Midlands region (based upon revenue) at the end of 2019: an ideal moment to capture the financial health of automotive organizations just before the pandemic hit. We only investigated the largest 50 firms (based on revenue) because eligibility for the CLBILS was restricted to firms with a turnover of more than £45 million and we wanted to include eligible and other large (non-eligible) firms. These firms in are ranked (in descending order) on their total revenue. A total of 27 out of the 50 firms have an annual turnover of less than £45 million, indicating ineligibility for the CLBILS, leaving 23 out of the top 50 firms in the West Midlands automotive sector eligible to apply.

Table 1. Largest 50 (revenue) automotive firms in the West Midlands, 2019.

Cash flow is a key measure of resilience in the face of economic shocks, given that firms face a time delay across their supply and demand chains, created by both breaks in component supply and stalled demand. We use the current ratio as a proxy for cash flow as it is used to estimate the liquidity position of an organization. The ratio represents a firm’s ability to convert its assets into cash to cover its short-term liabilities. The current ratio is calculated by dividing current assets by current liabilities. The liquidity ratio in is calculated by current assets less stock divided by current liabilities (Smith, Citation2005).

The methodology we adopt is similar to that of Soroka et al. (Citation2020), who used the QuiScore credit indicator (Fame) to measure firm and regional economic resilience in Cardiff (UK). Our risk parameters are outlined in the final column in . We define a firm as being high risk when its current ratio is below 1.20 (low financial resilience), medium risk (medium levels of financial resilience) if current ratios are between 1.20 and 1.80, and low risk (high levels of financial resilience) if above 1.80. We use the current ratio as a proxy for cash flow and resilience because it represents a firm’s ability to meet its short-term debt obligations. Thus, the current ratio is a resilience indicator because it identifies whether or not a firm has enough financial resources to pay its debts over the next year.

shows 22 firms that we define as high risk. A total of 18 of these high-risk firms are subsidiaries to larger firms. Many high-risk firms display negative profit levels or low profit margins. Together these high-risk firms employ 44,328 people, but only 11 of these high-risk firms are eligible for the CLBILS. Out of these 11, six firms have credit scores below 50; thus, applying for the CLBILS is exceptionally important for these organizations. Critically important, the OEMs (i.e., Jaguar Land Rover (JLR) and Aston Martin) are amongst the high-risk firms. JLR is the largest direct employer (with nearly 33,000 employees) and has a revenue that is over double that of the next largest automotive company in the region (Aston Martin). It supports several tiers of supply chain firms and a wide range of dependent contractors and service firms in the region. If JLR were to shut down, the contagion risks for the West Midlands economy would be severe. Of the 11 high-risk firms that do not qualify for the CLBILS, nine also have negative profit margins. These firms have a total workforce of 1969 individuals, and negative profits coupled with poor current ratios make these jobs vulnerable to redundancies.

Next there are 12 firms classified as medium risk, with a total of 31,856 employees. Of these, eight firms have an annual turnover of more than £45 million, thus qualifying for the CLBILS. Two of the four medium-risk firms that cannot qualify for the CLBILS and have negative profit margins are relatively vulnerable to closures. These two firms employ 426 people. We identify 16 firms that cumulatively employ 4659 people with relatively healthy current ratios. Of these firms, four qualify for the CLBILS. The remaining 12 low-risk firms are not eligible to apply for the CLBILS illustrate relatively healthy and positive profit margins. Yet, Arcelormittal Tailored Blanks Birmingham Ltd, which is one of the firms not eligible for the CLBILS, has an exceptionally weak credit score, thus sourcing alternative funding is certainly required.

With regards to profit margins, 17 firms (including key firms such as JLR and Aston Martin) have negative profit margins. These firms also have negative profits per unit (i.e., per employee). JLR signalled profit warnings at the start of 2019. This is because it incurred £3.1 billion in write-offs due to an adjustment in its carrying value of capitalized investments (Attwood, Citation2019). Additionally, the British giant incurred another £1.5 billion of exceptional charges in 2020. This is because of £952 million in non-cash investment write-offs and £534 million of restructuring charges. The firm recorded a loss of £861 million for 2020/21 compared with a loss of £422 million for 2019/20 (Attwood, Citation2021). Next, six firms are only marginally profitable (below 2%). In contrast, 10 firms not only display healthy (low risk) current ratios but also have profit margins greater than 4%. Of these firms, five have profit margins of more than 10%; these are firms less likely to make redundancies.

also shows whether the firms from the top 50 list belong to parent organizations. A total of 40 firms are subsidiaries controlled by a parent organization. It is not uncommon for investments (e.g., R&D) to be undertaken at a subsidiary level for the benefit of the parent or whole (Rabbiosi & Santangelo, Citation2013). Although not the focus here, given the difficulties relating to parent/subsidiary structures, careful consideration must be placed on the profit and loss of individual subsidiaries that belong to parent corporations. In our study, most of the parent organizations listed in are global organizations headquartered outside the UK, aligning with Qamar et al.’s (Citation2019a) finding that the majority of key firms within the West Midlands automotive industry are of foreign ownership. demonstrates that two parent organizations own and control two subsidiaries each from our list: Faurecia owns SAI Automotive Fradley Ltd and Faurecia Emissions Control Technologies UK Ltd. Although both firms are profitable, the latter is a high-risk firm in terms of its current ratio. Ontario Inc. owns Stadco Ltd and Magna International Holding (UK) Ltd; both firms are identified as high-risk firms using current ratio parameters.

4.2. Where are the high-risk firms located?

provides a breakdown of where (using headquarter postcode areas) the largest 50 automotive firms are located in the West Midlands, alongside risk levels and employment size. With 19 firms, Coventry (also encompassing Warwickshire) has the highest number of automotive firms (including high-risk firms) within the top 50 list. Birmingham has the second highest number of firms. Of these 13, five firms are high-risk firms, positioning Birmingham as a high-risk area. The remaining areas in have one high-risk firm from the top 50. Given that the data relate to headquarter location, not all employees are necessarily working within the region. For instance, for Sumitomo Electric Wiring Systems (Europe) Ltd, in Stoke-on-Trent, total employment relates to the whole of Europe and North Africa. In contrast, the majority of JLR’s and Aston Martin Lagonda Ltd’s employment is within the region. The findings, although not always directly comparable, are pertinent for policymakers in highlighting which subregions within the West Midlands face different risks in the face of disruption in the sector.

Table 2. Risk by location of the ‘top 50’ automotive firms.

4.3. Snapshot: risk by employment size

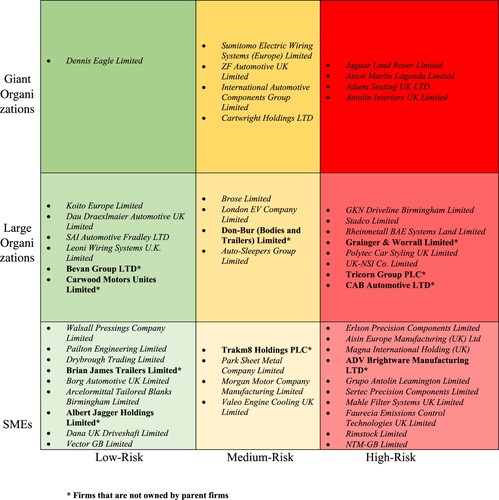

shows the ‘top 50’ automotive firms by revenue in the West Midlands by risk and employment size. Low-, medium- and high-risk firms are categorized using the same current ratio parameters used in . We categorize firm size by the number of employees (small and medium-sized enterprises (SMEs): up to 250 employees, large organizations: over 250 but equal to or less than 750 employees, giant organizations: over 750 employees). There are four giant firms (including Aston Martin Lagonda Ltd and JLR) at high risk, and thus vulnerable to closures (or redundancies). Given the size of these firms and their respective positions in the automotive supply chain, redundancies and closures will have a sizeable impact on the rest of sector. In contrast, there are three giant firms with heathy current ratios. There are six large firms and nine SMEs possessing healthy current ratios, thus deemed as low-risk firms. Given the size of the firms, the giant organizations are shaded darker and represent the negative ‘contagion’ effects on the industry if these firms were to fail. Policymakers should pay particular attention to the giant and large firms that demonstrate medium and high risk. Given that vast majority of high-risk firms have foreign ownership, the government should assist these firms as much as possible to ensure FDI remains in the region.

Figure 1. Vulnerability (risk) versus employment size.

5. DISCUSSION: POLICY AND MANAGEMENT IMPLICATIONS

At the same time as dealing with the Covid-19 crisis, although the UK has secured a free trade deal with the European Union (EU), the automotive sector faced a Brexit trade-related obstacle (i.e., rules of origin). Components from Japan and Turkey used in the UK are not classified as British, and related exports experience higher tariffs. To avoid tariffs petrol and diesel vehicles need to be manufactured with at least 55% local content, whereas electric vehicles and hybrids require 40% local content. Up until 2023, batteries can have as much as 70% foreign content. From 2024 to 2026 batteries can only have up to 50% foreign content and electric vehicles and hybrids 55% foreign content (Trudell & Philip, Citation2020).

More broadly, net zero targets and the longer term shift towards electric vehicles presents a challenge to both firms and policymakers. Over 85% of UK domestic transport CO2 emissions are from vehicles and over 55% are from cars and taxis (Department for Transport, Citation2021). Regulatory pressures will drive a fundamental restructuring of the automotive value chain and supplier networks. This will also have a large-scale impact on the labour market and skills demand, and in turn on the relative attractiveness of different locations for new investment and therefore for policymakers looking to attract investment.

Our analysis shows that 23 out of the top 50 firms have an annual turnover of more than £45 million, and qualify for the CLBILS. It took over a month to allocate 18,595 loans worth £3.1 billion. In June 2020, the UK government announced a £73.5 million package to boost green economic recovery within the automotive sector, yet only three out of the 10 funded projects were located in the West Midlands. The West Midlands is home to over 430 specialist automotive firms, including 36 of the top 50 global suppliers (WMGC, Citation2019). Thus, our findings provide guidance for government agencies to target support more precisely –by sector and region – where it is needed.

One reason for direct government intervention is the need to limit redundancies, retain skills and provide certainty to the automotive sector’s foreign investment (Islam, Citation2020). Firms create additional investment and employment in regions via direct and indirect supply chains, known as multiplier effects. These are often used to estimate the positive impact of inward investment, and less often to assess the negative effects of divestment or firm collapse. Our framework extends this approach by taking a more holistic view of the overall embeddedness of a firm in a region. This follows previous work on embeddedness from evolutionary and institutional perspectives (Plöger, Citation2020) and draws on international business studies approaches where the ratio of local assets, sales and employment to total company assets, sales and employment is widely used as a relative measure of domestic-market embeddedness or home-country dependency (Collinson et al., Citation2020).

From a responsible business perspective, JLR, which is a high-risk firm (based on our analysis), is unusually important for the West Midlands. JLR has a high proportion of global production and employment in this one region. Four of its major plants are in the West Midlands. JLR employs approximately 33,000 people working in a range of business functions (dealerships/retailers, service providers, R&D, direct supply chain jobs) within the West Midlands and the UK. There are other jobs indirectly supported by JLR, so the ‘knock-on’ effect of job loss at JLR would ripple through the regional economy. In 2018, when the firm had a workforce close to 43,000 people, it was reported that 260,000 jobs were supported by JLR (Mullen, Citation2019). This suggests that JLR yields a multiplier of 1.0:6.0, so for any single job created within JLR, six jobs are created within production, dealerships/retailers, R&D and direct supply chain jobs. Although this may seem exceptionally high, Donnelly et al. (Citation2017) assert that automotive industry in the West Midlands is almost entirely dependent on JLR. Disruptions related to Covid-19, alongside longer term disruptive processes relating to the greening of the economy and notably the development of electric vehicles, had a sizeable impact on the industry and local economy. This highlights the need for policymakers to understand broader labour market impacts of disruptions impacting large employers in key sectors.

Uncertainty is a key deterrent to foreign investment: the higher the uncertainty or value that firms ascribe to their ‘net present value calculations’, the less likely they are to invest (Bailey et al., 2017). Analyses have shown that firms with inward FDI are more productive than non-FDI firms (Bailey et al., Citation2019). Productivity and skills issues in the West Midlands are important given the region’s relatively poor performance on skills indicators (Green et al., Citation2018). Preventing firm closures within the British automotive industry is important for productivity within the UK: the industry is one of the most productive sectors in the UK.

The 27 firms in that did not qualify for CLBILS could access the Coronavirus Job Retention Scheme (CJRS). The CJRS was introduced in spring 2020 to stop people being laid off by their employers during lockdown. Initially the UK government paid 80% of wages up to a monthly limit of £2500 of employees who could not work/whose employers could not afford to pay them. In July 2021 employers were required to pay 10% of salaries with the government’s contribution falling to 70%, and in August and September (the CJRS ended on 30 September 2021) employers’ contribution increased to 20% and the government’s contribution fell to 60%. The CJRS contributed to the resilience of the automotive sector by protecting key skills and R&D. It has also been used to deal with shortages of components due to supply chain issues as well as health-related Covid-19 impacts. In June 2021, the furlough take-up rate for the manufacturing sector (more detailed sectoral disaggregation is not available regionally) in the West Midlands was 10% of eligible employments (26,600 employments), which was the highest proportion of any UK region outside London and the North East. At the UK level, in June 2021, 31% of employers in the automotive sector had staff on furlough, representing 16% of eligible employments (23,000 employments).

While government support packages can reduce costs and improve resilience for firms, unemployment places the financial burden on the taxpayer via the costs of benefits and welfare support. Redundancies and knock-on effects have important implications for policymakers (nationally, regionally and locally) looking to mitigate against the risks of redundancies that will have significant direct and indirect impacts on any one region or promote economic growth and social well-being through employment. Attention has been paid in the Covid-19 crisis to sectoral, occupational and subnational online job-matching initiatives to help redeploy workers suffering job loss to fill openings where they can use their skills, particularly in sectors where demand has risen. Importantly, such job-matching can play a role in ensuring that regions/nations retain valuable skills by helping to balance redundancies in one company with recruitment in another. While previous research on redundancies in the automotive sector (albeit not in the context of a global pandemic-induced crisis) has indicated that strong policy responses, including initiatives to facilitate both skills retention and also reskilling, have helped those made redundant to move into employment in the short and medium terms, in some instances this has been at the expense of reduced job quality and greater employment precarity (Bailey et al., Citation2012).

The policies discussed above are focused primarily on dealing with shocks. To address slower burn disruptive processes, greater emphasis needs to be placed on an ongoing participatory approach with a place-based focus to secure both sectoral and regional resilience (Bailey et al., Citation2022), through limiting the adverse impacts of shocks and longer term disruptive change, promoting recovery and renewal, and providing a skills anticipation function to meet changing sectoral demand. This involves bringing together businesses and actors with relevant sectoral and local knowledge. While ongoing institutional changes, coupled with the acute nature of recent shocks, have been a barrier to a longer term policy approach, they underscore how essential such dialogue and collaborative working is in the context of the co-evolution of firms and industries in the region. This approach has been relatively successful in the Staffordshire ceramics industry (Fai et al., Citation2022).

Returning to our analytical focus on financial resilience, in the face of disruption (e.g., Brexit, Covid-19) and from a longer term strategic perspective, one of the ways in which firms can develop firm resilience is to develop ‘agile’ capabilities. The literature concerning the West Midlands (Qamar & Hall, Citation2018; Qamar et al. Citation2018, Citation2019a, Citation2019b) notes that downstream (OEMs and first-tier suppliers) firms predominantly adopt a lean strategy and upstream (third-, fourth- and fifth-tier suppliers) firms an agile strategy. Although this may work within a stable market, disruption may require a more agile approach across all tiers of the automotive supply chain. Also, re-segmenting supply chains (Safonovs & Upadhyay, Citation2017) could also be one of the ways in order to enhance the resilience of supply chains. Yet, these options may worsen the cost–capability ratio (Bailey et al., Citation2022). Our data reveal that a large proportion of automotive firms are not financially healthy enough to be implementing change. This is a key reason why tailored policies and support packages are crucial for some of the embedded automotive manufacturers in the region.

6. WHAT DOES THIS MEAN FOR POLICYMAKERS?

The issues discussed in this article relate to ongoing debates in the literature on sectoral resilience and regional resilience and the role of firm dynamics therein. The basic idea of resilience is how an entity or system reacts to and recovers from an adverse disruption (Martin et al., Citation2016). Although Martin (Citation2012) distinguished between four dimensions of resilience – resistance, recovery, reorientation and renewal – in subsequent contributions the multifaceted nature and complexity of resilience has been emphasized more by scholars. Martin and Sunley (Citation2015) conceptualized regional resilience as comprising four sequential (and recursive) steps: first, the vulnerability of a region’s firms, industries, workers and institutions to shocks; second, the resistance of those firms, industries, workers and institutions to the impact of shocks; third, the ability or otherwise of the region’s firms, industries, workers and institutions to undergo the adjustments and adaptations necessary to resume core functions and performances; and fourth, the degree and nature of recoverability from the shock.

It is important here to consider the cross-over relationships between automotive, aerospace and other manufacturing activity in the region. Firm dynamics are intrinsically related to sectoral and regional resilience because processes of adaptation and structural reorientation work at the level of firms (Duschl, Citation2016). From an evolutionary perspective, co-dependency between firms, clusters and regional economies can underpin virtuous cycles of growth and vicious cycles of decline. The complexities of firm-level interactions within (and across) sectors and the development of multi-scale patterns of relational geographies of production shape regional resilience (Bentley et al., Citation2017). The combined shocks of Covid-19 and Brexit on the West Midlands automotive sector, and the renewed urgency of the transition to net zero, have the potential to de-lock the sector from its former evolutionary path, contributing either to decline (with implications for gross value added (GVA) and jobs) or to resurgence.

From a policy perspective this highlights the need for a holistic approach to sectoral and regional policy in the longer term, as well as the importance of interventions (such as the financial assistance measures available to firms from the UK government during the Covid-19 pandemic) to enable firms to weather acute changes in the short term. It also underscores the need for a sophisticated understanding of local and regional industrial structures. In the context of US manufacturing, Clark (Citation2014) points to the role of regional intermediaries in building collective agency and cooperation to address supply chains, innovation, and labour market and skills issues. These three issues are in turn interrelated, with the production, and importantly the retention, of human capital emerging as a key linking factor across these domains (Clark & Bailey, Citation2018). As in the Great Lakes automotive sector (Rutherford & Holmes, Citation2014), the West Midlands automotive sector has accumulated strengths and advantages in R&D and specialized skills, and for these to be retained and used to realize future growth opportunities (Bailey & de Propris, Citation2014), it is important the sector in the region follows a high-skill high-wage trajectory.

There are important lessons from the demise of Australian auto manufacturers, as local industry production fell from 500,000 in the 1970s and over 400,000 in 2004 to 175,000 by 2009. Subsequently the Ford Australia engine and vehicle plants closed in 2016 and the Holden and Toyota Australia factories closed in late 2017. Initial estimates that 40,000–50,000 jobs would disappear within three years prompted a series of interventions aimed at reskilling and re-employment of workers and stimulating other kinds of economic growth in affected regions. The lessons from this experience include the need for more precise, early interventions to support labour to transition into new areas, and proactive policies to create jobs in other emergent industry sectors in advance of plant closures (Irving et al., Citation2022). In the UK it is important that initiatives such as the Talent Retention Solutions online platform, originally developed to support redeployment, recruitment and skills retention across manufacturing and engineering, continue to evolve to support the talent management and skills development needs of individuals and companies through a single point of access to a sector-specific pool of talent, vacancies and development opportunities. More strategically, it is important to monitor the supply of skills at degree and technician levels and the evolving demand for skills (including requirements for a mix of science, technology, engineering and mathematics (STEM) and other skills) over the short and medium terms. The impacts of other developments, notably post-Brexit immigration policy, which have exacerbated labour and skills deficits in the sector, also need to be taken into account.

In economic policy at the West Midlands scale, automotive is recognized as a sectoral strength, and in the local industrial strategy (West Midlands Combined Authority, Citation2019) was seen as a key ingredient in major new market opportunities around the future of mobility, building on cutting-edge R&D (including university-based STEM assets and in-house teams in automotive firms) and the development of electric vehicles. The Manufacturing Technology Centre (MTC) and Warwick Manufacturing Group (WMG) are examples of triple helix innovation, functioning in hybrid forms translating university-based R&D into applied innovation and supporting upskilling amongst local SMEs. Funded as part of the national High Value Manufacturing Catapult network, they attract substantial commercial income from industry. Locally embedded catapults provide some of the inspiration for the new Innovation Accelerators initiative, which involves a £100 million investment from Innovate UK shared across the Birmingham, Glasgow and Manchester city-regions. The aim is to catalyse longer term growth in emerging industry clusters through stimulating applied and translational R&D.

Amongst the practical lessons for policymakers at national and regional levels, it seems important to find ways to accelerate the allocation of subsidies and interventions but also improve the precision with which different interventions are targeted at firms with different challenges. The four dimensions of resilience, referred to above, encompass ‘reactive’ and ‘proactive’ policy interventions. Reactive interventions to reduce insolvencies which lead to unemployment and increase the burden on taxpayers, including emergency subsidies should be quickly deployed to firms that most need it. This includes support for the newly unemployed, such as redeployment and reskilling.

Similarly, proactive strategies to improve innovation and competitiveness and the ability of firms to adapt to new regulatory hurdles, net zero transition, Brexit and Covid-19 supply chain constraints, in the case of the automotive industry, should be linked to wider policy goals including improving local productivity, growing FDI, and attracting more public R&D funding to support product and process innovation and central government investment into the region. This is support for ‘re-orientation’, in the Martin et al. (Citation2016) sense, and requires consistent, long-term policies which can ultimately help firms transition into new markets and business models.

Application of reactive and proactive policies appropriately will enhance firm-level resilience, in turn supporting resilience in the regional economy. This micro–macro connection is dependent on the precision with which the ‘right’ firms are targeted for support. Our study highlights how interventions must be proportionate to the wider importance of a firm and/or sector to the regional economy. This requires a sophisticated understanding of the relative differences between firms and their related local networks, in terms of their size and direct and indirect contributions to regional employment, productivity and GDP amongst other aggregate outcome measures. Embeddedness, as a measure of local value-chain (or supplier–buyer) connectedness, but also as an indicator of where a firm’s employees work, live and spend, is an important framing for evaluating the targets, scope and scale of interventions. This conclusion aligns with Bailey et al. (Citation2022) and builds on Kitsos and Bishop (Citation2018).

For reactive policy interventions, this approach would guide an assessment of the impact of specific shocks on specific groups of firms and include the wider negative impacts on employment and local communities. By targeting support on the most vulnerable and most embedded firms to reduce insolvency rates, the intervention would have maximum regional impact to leverage limited amounts of public funding. Similarly, for proactive policy interventions, focusing on firms with the greatest growth potential and the high levels of current or future embeddedness could significantly improve the effectiveness of government policy interventions.

To do this effectively, requires a combination of detailed knowledge of the geography of regional economic growth with intelligence about the evolving performance and financial resilience of local firms. It follows that there could be geographically focused interventions, from more generous targeted capital allowances for plant and machinery to address problems of under-investment and new allowances to encourage investment in human capital and diffusion of new technologies (additional to R&D tax credits) to aid regional growth. At a micro level sandboxes and sandpits can be useful self-contained environments to share knowledge and develop new ideas and technologies, allow experimentation and build proof of concept.

Arguably, both speed and accuracy would be improved with greater devolution of budgets and decision-making and the development of enhanced capabilities for region-specific analysis. In this regard this study supports others which have recommended greater devolved funding and decision-making power to regional authorities to enable faster local responses. Bailey and Berkeley (Citation2014) also focused on the West Midlands example and highlight the importance of regional taskforces with ready resources and some degree of local decision-making power as key to the maintenance of a ‘permanent capacity’ to deal with transitions, as well as shocks. Empowered, local agility should be complemented by improved regional analysis and intelligence capabilities, focused on understanding the specific vulnerabilities as well as areas of future growth potential for each local economy. As part of this a more in-depth understanding of local firm demography, including sector specialization, embeddedness and key fiscal, market or regulatory ‘tipping points’ is required.

At the simplest level this would improve the allocation of reactive subsidies, like CLBILS, or proactive local business support programmes, so that the most vulnerable and perhaps most embedded firms are supported. The UK automotive sector has historically proven to possess the ability and capacity to recover from disruption and economic shocks. Yet, sectoral resilience does not necessarily equate to only the action of individual firms (Bentley et al., Citation2017). Instead sectoral resilience will need to include the complexities, dynamics and interaction of multiple factors (e.g., firms, firm interactions, local government, education/skills, innovations, etc.) which were discussed in this section. Cumulatively, these factors can help to shape regional resilience. Thus, policy interventions and initiatives will only work they are aligned and matched with the dynamics and complexities of a region holistically (Bentley et al., Citation2017).

7. CONCLUSIONS

Our results identify that a large proportion of the largest 50 automotive firms (by revenue) in the West Midlands are facing severe cash flow issues (indicating low levels of financial resilience and high levels of vulnerability), to the degree that some business closures may be inevitable. We use the current ratio as a proxy to cash flow because it is commonly used to evaluate whether an organization has enough resources to meet its short-term obligations.

Our findings reveal if some of the high-risk firms were to close, Coventry and Birmingham would be the hardest hit subregions within the West Midlands. Out of the largest 50 automotive firms, these subregions are home to 32 firms, of which 15 are considered to be at high risk. Our analysis shows that the largest 50 automotive manufacturing firms by revenue in the West Midlands employ a total of 80,843 individuals and of these, 44,328, 31,856 and 4659 people are employed in organizations of high, medium and low risk, respectively. Regional sector-specific (e.g., aerospace industry) analyses of this type can be used by policymakers to specifically target where government packages will be most useful in terms of cushioning the impacts of Covid-19.

Understanding financial resilience of large organizations, and the nature of their supply chains, is of fundamental importance in all regional economies. This underpins the principle of proportionality in guiding interventions at regional level. Specific firms and particular regions are far more vulnerable than others. Hence, national and regional policymakers may need to adapt support mechanisms appropriately to help some organizations survive in the short/medium terms in the context of major shocks alongside longer term disruptive processes. Importantly, the analyses presented in this paper are of broader relevance for sectoral and regional resilience. This includes other regions or city-regions internationally that face similar vulnerabilities – either in relation to automotive (i.e., Detroit (United States), Wolfsburg (Germany), Ulsan (South Korea)) or other key sectors with strong local/regional embeddedness. We provide a contribution to this discussion by outlining a novel approach (financial vulnerability and regional embeddedness) and some of the metrics that regional studies scholars can use when examining firms within a particular region.

ACKNOWLEDGEMENTS

This article builds upon on a policy briefing by Qamar and Collinson (Citation2020).

DISCLOSURE STATEMENT

No potential conflict of interest was reported by the authors

REFERENCES

- Amison, P., & Bailey, D. (2014). Phoenix industries and open innovation? The Midlands advanced automotive manufacturing and engineering industry. Cambridge Journal of Regions, Economy and Society, 7(3), 397–411. https://doi.org/10.1093/cjres/rsu007

- Attwood, J. (2019). Jaguar Land Rover posts £3.4 billion loss in final quarter of 2018. Autocar. https://www.autocar.co.uk/car-news/industry/jaguar-land-rover-posts-%C2%A334-billion-loss-final-quarter-2018

- Attwood, J. (2021). Jaguar Land Rover begins recovery from £861m loss in 2020. Autocar. https://www.autocar.co.uk/car-news/industry-news-dealership%2C-sales-and-marketing/jaguar-land-rover-begins-recovery-%C2%A3861m-loss

- Bailey, D., & Berkeley, N. (2014). Regional responses to recession: The role of the West Midlands Regional Taskforce. Regional Studies, 48(11), 1797–1812. https://doi.org/10.1080/00343404.2014.893056

- Bailey, D., Chapain, C., & de Ruyter, A. (2012). Employment outcomes and plant closure in a post-industrial city: An analysis of the labour market status of MG Rover workers three years on. Urban Studies, 49(7), 1595–1612. https://doi.org/10.1177/0042098011415438

- Bailey, D., & De Propris, L. (2014). Manufacturing reshoring and its limits: The UK automotive case. Cambridge Journal of Regions, Economy and Society, 7(3), 379–395. https://doi.org/10.1093/cjres/rsu019

- Bailey, D., & De Propris, L. (2017). Brexit and the UK automotive industry. National Institute Economic Review, 242(1), R51–R59. https://doi.org/10.1177/002795011724200114

- Bailey, D., de Ruyter, A., Hearne, D., & Ortega-Argilés, R. (2022). Shocks, resilience and regional industry policy: Brexit and the automotive sector in two Midlands regions. Regional Studies, 1–15. https://doi.org/10.1080/00343404.2022.2071421

- Bailey, D., Driffield, N., & Kispeter, E. (2019). Brexit, foreign investment and employment: Some implications for industrial policy? Contemporary Social Science, 14(2), 174–188. https://doi.org/10.1080/21582041.2019.1566563

- Bentley, G., Bailey, D., & Braithwaite, D. (2017). Resilience, adaptation and survival in industry sectors: Remaking and remodelling of the automotive sector. In N. Williams, & T. Vorley (Eds.), Creating resilient economies: Entrepreneurship, growth and development in uncertain times (pp. 55–69). Edward Elgar.

- Clark, J. (2014). Manufacturing by design: The rise of regional intermediaries and the re-emergence of collective action. Cambridge Journal of Regions, Economy and Society, 7(3), 433–448. https://doi.org/10.1093/cjres/rsu017

- Clark, J., & Bailey, D. (2018). Labour, work and regional resilience. Regional Studies, 52(6), 741–744. https://doi.org/10.1080/00343404.2018.1448621

- Coffey, D., & Thornley, C. (2020). Britain’s Car industry: Policies, positioning, and perspectives. In New frontiers of the automobile industry (pp. 137–161). Palgrave Macmillan.

- Collinson, S. C., Narula, R., & Rugman, A. M. (2020). International business, 8th edition. FT Pearson/Prentice Hall, Harlow.

- Collinson, S. C., & Wilson, D. C. (2006). Inertia in Japanese organizations: Knowledge management routines and failure to innovate. Organization Studies, 27(9), 1359–1387. https://doi.org/10.1177/0170840606067248

- De Ruyter, A., Hearne, D., & Henry, I. (2021). The resilience of advanced manufacturing supply chains across the Midlands. Midlands Engine. https://www.midlandsengine.org/wp-content/uploads/Manufacturing.pdf

- De Ruyter, A., Sukhwinder, S., Shishank, S., Li, D., Bailey, D., Hearne, D., Guy, J., & Ali, S. (2018). Brexit and the UK automotive industry: Understanding the impact, centre for Brexit studies. Birmingham City University.

- Department for Transport. (2021). Green Paper on a New Road Vehicle CO2 Emissions Regulatory Framework for the United Kingdom (July 2021). UK Government Publishing Service. https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/1007466/green-paper-on-a-new-road-vehicle-CO2-emissions-regulatory-framework-for-the-United-Kingdom-web-version.pdf

- Donnelly, T., Begley, J., & Collis, C. (2017). The west midlands automotive industry: The road downhill. Business History, 59(1), 56–74. https://doi.org/10.1080/00076791.2016.1235559

- Duschl, M. (2016). Firm dynamics and regional resilience: An empirical evolutionary perspective. Industrial and Corporate Change, 25(5), 867–883. https://doi.org/10.1093/icc/dtw031

- Fai, F., Tomlinson, P. R., & Branston, J. R. (2022). Actors, knowledge and path transformations in a declining cluster. European Urban and Regional Studies. https://doi.org/10.1177/09697764221105765

- Fame. (2020). The definitive source of information on companies in the UK and Ireland. https://www.bvdinfo.com/en-gb/our-products/data/national/fame

- Fromhold-Eisebith, M. (2015). Sectoral resilience: Conceptualizing industry-specific spatial patterns of interactive crisis adjustment. European Planning Studies, 23(9), 1675–1694. https://doi.org/10.1080/09654313.2015.1047329

- Gittell, J. H., Cameron, K., Lim, S., & Rivas, V. (2006). Relationships, layoffs, and organizational resilience: Airline industry responses to September 11. The Journal of Applied Behavioral Science, 42(3), 300–329. https://doi.org/10.1177/0021886306286466

- Green, A., Sissons, P., Qamar, A., & Broughton, K. (2018). Raising productivity in low-wage sectors and reducing poverty. Joseph Rowntree Foundation.

- Irving, J., Beer, A., Weller, S., & Barnes, T. (2022). Plant closures in Australia’s automotive industry: Continuity and change. Regional Studies, Regional Science, 9(1), 5–22. https://doi.org/10.1080/21681376.2021.2016071

- Islam, F. (2020). Brexit: Blow to UK car industry in search for EU deal. BBC News. https://www.bbc.co.uk/news/business-54345882

- Kitsos, A., & Bishop, P. (2018). Economic resilience in Great Britain: The crisis impact and its determining factors for local authority districts. The Annals of Regional Science, 60(2), 329–347. https://doi.org/10.1007/s00168-016-0797-y

- Linnenluecke, M. K. (2017). Resilience in business and management research: A review of influential publications and a research agenda. International Journal of Management Reviews, 19(1), 4–30. https://doi.org/10.1111/ijmr.12076

- MacNeill, S., & Bailey, D. (2010). Changing policies for the automotive industry in an ‘old’ industrial region: An open innovation model for the UK West Midlands? International Journal of Automotive Technology and Management, 10(2–3), 128–144. https://doi.org/10.1504/IJATM.2010.032620

- Makortoff, K. (2020). Why the UK fell behind European peers on emergency funding. The Guardian. https://www.theguardian.com/business/2020/may/18/why-the-uk-fell-behind-european-peers-on-emergency-funding

- Marcucci, G., Mazzuto, G., Bevilacqua, M., Ciarapica, F. E., & Urciuoli, L. (2022). Conceptual model for breaking ripple effect and cycles within supply chain resilience. Supply Chain Forum, 23(3), 252–271. https://doi.org/10.1080/16258312.2022.2031275

- Markman, G. M., & Venzin, M. (2014). Resilience: Lessons from banks that have braved the economic crisis – And from those that have not. International Business Review, 23(6), 1096–1107. https://doi.org/10.1016/j.ibusrev.2014.06.013

- Martin, R. L. (2012). Regional economic resilience, hysteresis and recessionary shocks. Journal of Economic Geography, 12(1), 1–32. https://doi.org/10.1093/jeg/lbr019

- Martin, R. L., & Sunley, P. J. (2015). On the notion of regional economic resilience: Conceptualization and explanation. Journal of Economic Geography, 15(1), 1–42. https://doi.org/10.1093/jeg/lbu015

- Martin, R., Sunley, P., Gardiner, B., & Tyler, P. (2016). How regions react to recessions: Resilience and the role of economic structure. Regional Studies, 50(4), 561–585. https://doi.org/10.1080/00343404.2015.1136410

- Meyer, A. D. (1982). Adapting to environmental jolts. Administrative Science Quarterly, 27(4), 515–537. https://doi.org/10.2307/2392528

- Mullen, E. (2019). This is how many jobs depend on Jaguar Land Rover. Coventry Telegraph. https://www.coventrytelegraph.net/news/coventry-news/jaguar-land-rover-jobs-15947089

- Plöger, P. (2020). Employers stuck in place? Knowledge sector recruitment between regional embeddedness and internationalization. Regional Studies, 54(12), 1737–1747. doi: 10.1080/00343404.2020.1765231

- Qamar, A., & Collinson, S. (2018). Carillion’s Collapse: Consequences (City-REDI Policy Briefing Series). https://blog.bham.ac.uk/cityredi/wp-content/uploads/sites/15/2018/03/Carillion-Policy-Brief-B-Final.pdf

- Qamar, A. & Collinson, S. C. (2020). The West Midlands’ automotive industry in the aftermath of COVID-19: Survival of the fittest? (WM-REDI/City-REDI, Policy Briefing Paper Series). University of Birmingham. https://blog.bham.ac.uk/cityredi/wp-content/uploads/sites/15/2020/06/WM-Policy-Brief-The-West-Midlands-Automotive-Industry-in-the-Aftermath-of-COVID-19-c.pdf

- Qamar, A., Gardner, E. C., Buckley, T., & Zhao, K. (2019a). Home-owned versus foreign-owned firms in the UK automotive industry: Exploring the microfoundations of ambidextrous production and supply chain positioning. International Business Review, 30(1), 101657. https://doi.org/10.1016/j.ibusrev.2019.101657

- Qamar, A., & Hall, M. (2018). Can lean and agile organisations within the UK automotive supply chain be distinguished based upon contextual factors? Supply Chain Management, 23(3), 239–254. https://doi.org/10.1108/SCM-05-2017-0185

- Qamar, A., Hall, M. A., Chicksand, D., & Collinson, S. (2019b). Quality and flexibility performance trade-offs between lean and agile manufacturing firms in the automotive industry. Production Planning & Control, 31(9), 723–738. https://doi.org/10.1080/09537287.2019.1681534

- Qamar, A., Hall, M. A., & Collinson, S. (2018). Lean versus agile production: Flexibility trade-offs within the automotive supply chain. International Journal of Production Research, 56(11), 3974–3993. https://doi.org/10.1080/00207543.2018.1463109

- Rabbiosi, L., & Santangelo, G. D. (2013). Parent company benefits from reverse knowledge transfer: The role of the liability of newness in MNEs. Journal of World Business, 48(1), 160–170. https://doi.org/10.1016/j.jwb.2012.06.016

- Rutherford, T. D., & Holmes, J. (2014). Manufacturing resiliency: Economic restructuring and automotive manufacturing in the great lakes region. Cambridge Journal of Regions, Economy and Society, 7(3), 359–378. https://doi.org/10.1093/cjres/rsu014

- Safonovs, R., & Upadhyay, A. (2017). Is your Brexit supply chain resilient enough? The British footwear manufacturers’ perspective. Strategic Direction, 33(11), 34–36. http://doi.org/10.1108/SD-02-2017-0018

- Smith, J. A. (2005). Empirical study of a venture capital relationship. Accounting, Auditing & Accountability Journal, 18(6), 756–783. https://doi.org/10.1108/09513570510627702

- SMMT. (2021a). SMMT motor industry facts 2021. SMMT. https://www.smmt.co.uk/wp-content/uploads/sites/2/SMMT-Motor-Industry-Facts-August-2021-1.pdf

- SMMT. (2021b). UK car production rises on anniversary of pandemic-driven factory shuttering. SMMT. https://www.smmt.co.uk/2021/04/uk-car-production-rises-on-anniversary-of-pandemic-driven-factory-shuttering/

- Soroka, A., Bristow, G., Naim, M., & Purvis, L. (2020). Measuring regional business resilience. Regional Studies, 54(6), 838–850. https://doi.org/10.1080/00343404.2019.1652893

- Staw, B. M., Sandelands, L. E., & Dutton, J. E. (1981). Threat rigidity effects in organizational behavior: A multilevel analysis. Administrative Science Quarterly, 6(4), 501–524. https://doi.org/10.2307/2392337

- Trudell, C., & Philip, S. V. (2020). Brexit deal is too little, too late for U.K.’s car industry. Bloomberg. https://www.bloomberg.com/news/articles/2020-12-29/Brexit-deal-may-be-too-little-too-late-for-u-k-s-car-industry

- West Midlands Combined Authority. (2019). West Midlands Local Industrial Strategy. HM Government.

- West Midlands Growth Company. (2019). Welcome to the West Midlands: Automotive. https://investwm.co.uk/wp-content/uploads/2019/10/Automotive.pdf

- WMREDI. (2020). State of the region 2020: Full report. West Midlands Combined City, Birmingham.