?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

The COVID-19 crisis has had a significant impact on UK craft breweries. In this paper we explore and assess the impact of COVID-19 on the UK craft beer sector from a locational perspective, targeting entrepreneurial responses from breweries within and across the urban, suburban and rural dimensions. Using a mix of quantitative and qualitative data collected between 2015 and 2022, we identify a marked geographical contextualization in terms of how UK craft breweries adapted and responded to the pandemic crisis, which explains how location shaped and still shape breweries’ strategies in a post-COVID-19 ‘new normal’ world.

1. INTRODUCTION

Craft breweries in the UK are defined by the Society of Independent Brewers (SIBA) as independent businesses that use traditional ingredients and methods in the brewing process and work independently from larger national or multinational brewers (SIBA, Citation2020). Mirroring international trends (Garavaglia & Swinnen, Citation2018), the number of craft breweries in the UK increased significantly in the last two decades, passing from 140 to 2200 between 2000 and 2019 (SIBA, Citation2020). These businesses, which usually produce less than 5000 hectolitres (hl) per year and employ 10 workers or fewer (Cabras & Bamforth, Citation2016), progressively passed from serving a localized niche market of pubs and small wholesalers predominantly located within their spatial proximity to supplying distributors and customers located in the UK and overseas. The SIBA report published in February 2020, while suggesting a slight reduction in beer production volumes, provided a positive outlook for the UK craft beer sector at least for the immediate future (SIBA, Citation2020). This prediction, however, occurred just before the COVID-19 outbreak.

In response to the pandemic crisis, many governments worldwide imposed strict measures, such as movement lockdowns and business closures, to control infection rates. In the UK, the closure of pubs, bars and restaurants shut down a key route to market for craft breweries, forcing them to reconfigure their business models, shifting a substantial proportion of sales to private custom mainly using online websites and marketplaces, and turning to local communities for support. Several recent studies investigated the impact of COVID-19 on small and micro-businesses, in the UK and overseas (Beltiski et al., Citation2022; Brown & Cowling, Citation2021; Galkina & Jack, Citation2022). However, there is still a paucity of research in relation to how businesses reacted based on their location (Welter et al., Citation2019). Being in densely populated urban areas, or in most remote and less served rural and peripheral areas, would affect how many businesses to face and absorb shocks associated with crisis, shaping their level of resilience and capacity of bounce back, or determining their failure (Bailey et al., Citation2021; Cowling et al., Citation2020).

The objective of this paper is to investigate the impact of the COVID-19 pandemic crisis on UK craft breweries by exploring and examining patterns of resilience at urban, suburban and rural levels. In doing so, we analyse a panel dataset of breweries surveyed between 2015 and 2019 to assess the state of the sector before the COVID-19 outbreak, evaluating results with 31 in-depth interviews conducted with a sample of 21 craft breweries between April 2020 and June 2022, and two focus groups with breweries and consumers conducted in July 2021. Our findings demonstrate how opportunities in the moment of crisis emerge from combining solutions and behaviours which can differ across business settings, strategies and networks. Equally, they provide a fresh account of how businesses in the craft beer sector are adapting to the post-COVID ‘new normal’, verifying whether solutions adopted during the pandemic crisis are still in place.

This study aims to make a two-fold contribution. First, it adds to the literature about the impact of COVID-19 on small and medium-sized enterprises (SMEs), which have been affected more severely from the pandemic crisis compared with larger enterprises and companies (Bailey et al., Citation2020; Beltiski et al., Citation2022; McCann et al., Citation2022). We explore how SMEs in the UK craft brewing sector reacted to COVID-19 and how their actions and strategies led them to absorb the shock and reconfigure operations in view of increasing resilience (Dormady et al., Citation2019). In addition, we examine how the interplay across different network layers in the sector made a difference in view of offering supply chain solutions and widening their geographical reach in terms of market channels (Clausen, Citation2020; Greenberg et al., Citation2018).

Second, the study investigates how the crisis affected UK craft breweries by examining their spatial and contextual factors. How locational dimensions can affect entrepreneurs and entrepreneurial phenomenon has been a theme relatively neglected by small business scholars (Brown & Cowling, Citation2021; Welter et al., Citation2019). However, in time of recessions, understanding differences across urban centres and peripheral areas is important to evaluate the effects of contractions and the speed of recovery associated with them (Korsgaard et al., Citation2020; Martin et al., Citation2016), as these differences can create new or exacerbate old spatial inequalities affecting employment, household incomes and welfare (Bailey et al., Citation2021; Martin et al., Citation2016). Focusing on craft breweries, we explore how the COVID-19 crisis triggered different responses from businesses within the sector located across urban, suburban and rural areas of the UK.

2. THEORETICAL BACKGROUND

2.1. Entrepreneurial, community and regional resilience in the face of the pandemic crisis

Resilience refers to the ability of a system to thrive and adapt to changes (Boschma, Citation2015). In entrepreneurship, different domains of resilience frequently coalesce across studies investing how entrepreneurs and business managers address, overcome challenges and survive; or perish in adverse market conditions based on individuals’ attributes such as personality, sense of coherence, self-efficacy, etc. (Doyle Corner et al., Citation2017). The spatial, geographical and regional dimensions are also very important components of entrepreneurial studies. As individual resilience is often affected by the context and social settings in which individuals live, likewise entrepreneurs are bounded to the community in which they operate, with the term ‘community’ identifying a wide texture of individuals, networks and stakeholders which defines the boundaries in which firms operate (Beltiski et al., Citation2022; Miklian & Hoelscher, Citation2022). At a local level, the existence, development and engagement of community resources by community members determines whether a community can thrive in an environment characterized by change, uncertainty, unpredictability and surprise (Magis, Citation2010). Berkes and Ross (Citation2012) emphasize community strength through agency and self-organization, based on people–place connections, values and beliefs, social networks, collaborative governance, economic diversification, infrastructure, and leadership. As such, community resilience, and reflexively the resilience of businesses and entrepreneurs are inextricably bound up with that of the local ecosystems in which these are located (Eachus, Citation2014).

Expanding from unit to groups and more complex social systems, resilient organizations or firms frequently display efficient mechanisms of adaptation, learning and self-regulation in addition to the general ability to persist through disturbances. Frequently, resilient organizations or firms depend solely on their own resources and capabilities (Hillmann & Guenther, Citation2021), but again geography assumes a significant role in shaping the conduct, strategy, attitude, and performance of businesses and entrepreneurs at different levels (Korsgaard et al., Citation2020; Martin et al., Citation2016; Sutton & Arku, Citation2022). Focusing on the regional/subregional scale, Boschma (Citation2015, p. 1) defines regional resilience as the ‘long-term ability of regions to develop new growth paths’, with resilient regions capable of overcoming the trade-off between adaptation and adaptability, as embodied in their industrial (related and unrelated variety), network (loosely coupled) and institutional (loosely coherent) structures. In this sense, regional resilience defines how firms and communities develop long-term adaptability to shocks and how history can stand in the way of true economic renewal, based on how pre-existing industrial, network and institutional structures within regions provide opportunities and/or set limits to the process of diversification (Boschma, Citation2015).

Over time, regional resilience has gained increased attention as a place-sensitive, multilayered and multi-scalar, conflict-ridden and highly contingent process associated with the institutional experience of dealing with crises such as the most recent COVID-19 pandemic (Bailey et al., Citation2021; Gong et al., Citation2020). However, the concept also attracted criticism for the neglect of state and policy at several spatial levels (Hassink, Citation2010), the lack of attention to long-term adaptive capacity (Martin et al., Citation2016; Pike et al., Citation2010), and its strong quantitative approach based on economic growth-oriented indicators that detract from alternative principles of development, such as post-growth or degrowth (Hassink & Gong, Citation2020; McCann et al., Citation2022).

2.2. The COVID-19 outbreak: response in the UK

These considerations assume significance in view of the COVID-19 outbreak in March 2020, which caused significant disruption across the world. Measures adopted by governments such as lockdowns and quarantines, including the closure of essential services such as schools and nurseries, reduced the supply of labour by restricting movements of people and hindering multiple supply chains, leading to shortages of parts and intermediate goods (Beltiski et al., Citation2022; McCann et al., Citation2022). Consumers’ sudden loss of income, increased levels of uncertainty and the introduction of ‘social distancing’ caused severe liquidity shortages for SMEs due to reduction in spending and consumption levels (Bailey et al., Citation2020). As SMEs account for most companies, value added and employment in almost all countries, their prevalence in regions and sectors exacerbated the effects of the crisis even further (Belghitar et al., Citation2022).

In response to the crisis, governments worldwide launched a variety of supporting schemes for businesses with the objective to mitigate the effects of lockdowns on both businesses and workforces (Belghitar et al., Citation2022). Two schemes were launched in the UK: the Coronavirus Job Retention Scheme (CJRS), allowing businesses to furlough their employees with the government paying 80% of monthly salaries up to £2500; and the Bounce Back Loan Scheme (BBLS), a government guarantee loan programme that enabled SMEs to borrow up to 25% of their turnover to a maximum of £50,000 (Belghitar et al., Citation2022). Belghitar et al. (Citation2022) analysed the governments’ mitigation policies on a sample of 42,401 UK SMEs. Their empirical results indicate the combination of CJRS and BBLS as overall successful in supporting SMEs during COVID-19, extending the residual life of targeted businesses between 189 and 194 days, and saving approximately 14,000 jobs in the sample considered. However, their results also suggested ‘overprotection of weak firms and unmatched between industries/areas that are worst hit and those that benefit most’ (p. 958). In particular, the authors criticize the ‘one size fits all’ approach of CJRS and BBLS which did not discriminate support according to industries, economic sectors and geographical areas. By doing so, both schemes might simply have extended the lifetime of firms that would not be able to trade properly otherwise, simply postponing their closures and bankruptcies (p. 957).

Other studies seem to confirm that governments’ interventions worldwide were crucial for keeping economic stability and jobs and save many businesses from closure (Bartik et al., Citation2020), but also that measures adopted had different impacts on different types of firms (Sutton & Arku, Citation2022), and that results varied considerably across SMEs operating in different areas and locations (McCann et al., Citation2022). As in many other crises, SMEs during COVID-19 had likely to adapt and turn threats into opportunities for their business to survive (Branicki et al., Citation2018; Dormady, Citation2019), drawing on mixed networks to combine the benefits of strong ties, such as trusting cooperation and loyal support (Galkina & Jack, Citation2022). While SMEs might be more vulnerable to exogenous shocks, given shorted resources which increase exposure to demand and supply shortages, they might be also be best placed to spot new opportunities and to exploit these compared with larger firms.

According to Cowling et al. (Citation2020), the level of success of SMEs’ responses to crisis remains context specific. Strong and weak network components can increase local system resilience and confer greater confidence and self-motivation to SME owners to take informed action in the face of external threats (Dormady et al., Citation2019), although locational settings would have had an impact in their conducts. For instance, the closure of services and amenities in rural and remote areas in the UK had been a trend of recent years, with many of these transferred to towns and urban areas due to a centralization effort made by successive governments in view of achieving savings and meeting budget constraints. Limited access to higher quality bandwidth for rural residents negatively affected those forced to work, hindering their productivity (Phillipson et al., Citation2020). On average, more older and retired residents live in these areas compared with urban and suburban areas, these residents being significantly more exposed to the virus and therefore more vulnerable and at risk.

The nature of vulnerability and resilience of SMEs, including craft breweries, in the face of crisis can be mainly associated with business’ attributes (e.g., size, age, sector), type of crisis (e.g., political, financial, military), and SMEs’ attitude (e.g., reactive, strategic, instinctive; Miklian & Hoelscher, Citation2022). The COVID-19 outbreak demonstrated the high sensitivity of local economies to global shocks (Bailey et al., Citation2021; Beltiski et al., Citation2022), and how these would undermine businesses and communities within regional and subregional settings. Still, research targeting spatial contextualization within entrepreneurship remains extraordinarily reduced (Welter et al., Citation2019; or see the ‘thin contextualisation’ in entrepreneurship research problem highlighted by Yue & Cowling, Citation2020), and even more limited in relation to specific businesses or economic sector.

2.3. Craft breweries in the UK: a brief overview

Since the early 1970s, the UK craft brewing sector developed and consolidated in three distinctive waves (Cabras & Bamforth, Citation2016; Mason & McNally, Citation1997). The first wave (early 1970s–1990) sought an increase of consumers’ demand for ‘real ales’, traditionally cask conditioned and non-filtered promoted by the Campaign for Real Ale (CAMRA), a movement of beer-lovers which has the effect to attract new firms into the British beer market. The second wave (1990s–2000) saw a change in the pub structure following the Beer Orders Act 1989 that forced the six largest national brewersFootnote1 either to sell or to free most of their pubs from their direct control or ‘tie’. While Parliament sought to break a monopoly, the unintended consequences of such act were the pubcos, newly formed estate companies that acquired large stocks of pubs at cheaper prices to run them as managed businesses, achieving economies of scale by having their beers supplied by a restricted number of breweries (Mason & McNally, Citation1997). The availability of more efficient, affordable and cost-effective brewing equipment attracted more entrepreneurs into the market, although the rise of pubcos reduced opportunities for new breweries to expand their supply network, severely limiting their growth (Cabras & Bamforth, Citation2016). The third wave (2000–10) was characterized by fiscal measures such as the Progressive Beer Duty (PBD; introduced in 2012) which granted a lower tax levy to smaller brewers compared with large ones, cutting the beer duty by up to 50% for any brewer producing less than 5000 hl/year; this relief rate lowered on a sliding scale once a brewer started producing above the threshold (Cabras & Bamforth, Citation2016). The effect of these measures was a sharper increase in the number of craft breweries, further helped by the lower duties applied to beers, with three 1 p duty cuts on beer sales introduced in the Budgets between 2013 and 2016. In 2018, the UK government lowered the threshold for breweries’ tax relief from 5000 to 2100 hl to encourage consolidation and growth in the sector, as lobbied by small but more established brewers, although its impact on very small breweries is still uncertain (Hancock, Citation2020).

3. METHODOLOGY

In developing our study, we combined a range of information from various datasets provided by the Office for National Statistics (ONS) (2019–21) and from the SIBA Annual Membership Surveys conducted yearly in November–December between 2015 and 2019. The SIBA surveys provide a wide range of information including breweries’ location, year of business foundation, beer production (hl), employment (e.g., number of full-/part-time staff), business performance indicators, such as annual turnover, routes to market; and breweries’ support and engagement with community activities, local charities and initiatives.

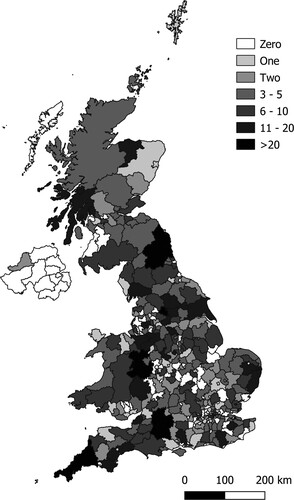

In the 2019 survey, a total of 237 valid responses (no duplications, no missing information for relevant variables) were received, accounting for 60.9% of the total responses, and 31.9% of total SIBA memberships. The number of valid responses in other years were 289 (2018), 327 (2017), 311 (2016) and 222 (2015). By combining the annual datasets, we created an inter-annual panel dataset that covers a period of five years and encompasses information for 722 breweries located in 274 local authorities (LAs). shows the location of breweries and responses obtained by LAs; variables included in the dataset, together with some descriptive statistics, are illustrated in the supplemental data online. Overall, the dataset comprises 1386 observations and is classified as unbalanced, as not all breweries were surveyed in each year.

Figure 1. Location of breweries and responses captured by the dataset (n = 1386).

Using classification provided by Bibby and Shepherd (Citation2004), we define each LA associated with observed breweries as ‘predominantly urban’, ‘suburban’ or ‘predominantly rural’, and we analyse the UK brewing sector before COVID-19 by examining both business characteristics and regional characteristics on breweries’ annual turnover, taken as a proxy for business performance. Annual turnover is defined as a four-levels ordinal variable: < £50,000 (low); £50,001–£250,000 (medium); £250,001–£1 million (high); and > £1 million (very high). Brewery characteristics cover eight independent variables: the size of beer portfolios; volumes of beer sales beyond an approximate 40-mile radius and directed to free trade, respectively; the number of pubs owned or controlled by breweries; the number of local charities and initiatives supported; the amount of investment, beer production levels and breweries’ age. The first four are used as proxies to investigate breweries’ expansion in terms of meeting increasing demand, supply channels and beer sales and their ability to extend their reach beyond the most immediate spatial proximity, the latter frequently seen as a barrier to expansion for many craft breweries due to transaction costs associated with production equipment, transport fleet and marketing costs (Garavaglia & Swinnen, Citation2018). Local charities supported by a brewery are used as proxies to measure breweries’ engagement within the local community (Cabras & Bamforth, Citation2016). Breweries’ age is investigated as younger breweries face more difficulties in terms of settling into the market than older ones (Carroll & Swaminathan, Citation2000). We control for beer production volumes and investment levels to capture breweries’ ability of expanding their capacity and size, for instance by buying new equipment, hiring more staff or investing into training workforce.

Regional characteristics consist of two variables of main interest, namely the median house price; and number of pubs and bars located in a LA; as well as three control variables, namely gross domestic product (GDP) per capita at current market prices, unemployment rate and median population age. The number of pubs and bars within spatial proximity provide breweries with access to both supply channels and consumers which can affect both beer price and consumption levels (Treno et al., 2007); while housing prices are used to capture the costs of setting up/running operations (Gallin, Citation2008), as well as a proxy of rental costs associated with setting up or running a brewery. As GDP per capita reflects the level of economic output, it is used as a robustness check of how the beer sector performs compared with the regional economy (Freeman, Citation2001; Nelson, Citation1997). We assume higher levels of GDP per capita positively linked to higher levels of production and consumption of different goods, including beer (Schmidt et al., Citation2010). Average population age is used as a proxy to capture alcohol consumption at a local level, likely to decline with older ages (Moore et al., Citation2005).

Next, we organized in-depth interviews with 21 independent brewery owners to verify attitudes and approaches to the crisis and related challenges. Interviewed breweries were selected based on attributes such as production levels, employment size and annual turnover. The first round of interviews was conducted between April and May 2020, after the UK government introduced the first measures to control the spread of COVID-19 across the country. Later, in September 2020, six interviewees were approached again to explore and examine how they re-adapted their businesses in face of the crisis. Following in-depth interviews, two focus groups, one with six breweries – three classified as urban, one as ‘town’ and two as rural – and another one with a group of eight consumers (three women and five men aged between 19 and 56 years) were organized on 21 July 2021 – two days after the decision to lift all restrictions made by the UK government. Other five in-depth interviews were conducted between April and June 2022, bringing the total number of interviews to 31.

Interviews and focus groups were audio-recorded; participants were asked to consent to our use of the information at the start of the audio-recording. Each interview lasted between 30 and 45 min, while both focus groups lasted approximately 50 min. Transcripts of the conversations were produced for the data analysis. The main attributes and characteristics of selected breweries are provided in the supplemental data online; any association with specific locations is concealed to preserve confidentiality.

4. DATA ANALYSIS

4.1. Findings from the econometric analysis: the UK craft brewing sector before COVID-19

In the five years preceding the COVID-19 outbreak, the UK craft beer sector presented many of the characteristics identified by Drakopoulou Dodd et al. (Citation2018): a fiscal regime in support of small-scale brewers, favourable licensing laws and alcohol regulations for small breweries, hyper-differentiation of beer portfolios and brands, an historical identity (derived by traditional ales brewed and served in inns, as well as neo-localism; Cabras et al., Citation2020); and a robust networked community of breweries and consumers which facilitated and fostered collaboration and cooperation among brewers (Waehning et al., Citation2022). However, the share of craft beers on the UK market was still marginal, at around 7% (SIBA, Citation2020). Production levels were slowly plateauing, with about seven in 10 craft breweries running less than £500,000 of investment, and with most breweries generating less than £250,000 in terms of annual turnover (Beeson, Citation2018).

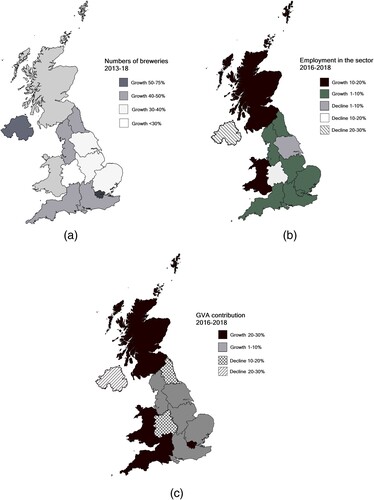

shows trends in the number of breweries, employment and gross value added (GVA) contribution across UK regions. All areas in the country, with the sole exception of the West Midlands, reported growth rates above 40% between 2013 and 2018, with London and Northern Ireland registering an increase above 50% (a). The number of new breweries registered a 64% increase in the same period, although this positive trend has not been uniformed regarding employment and GVA contribution (b and c, respectively). In terms of employment, most regions have seen an increase in the number of workers occupied in the sector, with growth in Scotland and Wales above 20% between 2016 and 2018, although Yorkshire and the Humber, the West Midlands, and particularly Northern Ireland experienced a decline. In terms of sectoral GVA, a direct contribution to regional economies, Scotland, Wales and the South West registered growth rates above 20% within the same period, while the North East, West Midlands and Northern Ireland all registered a decline.

Figure 2. Changes in the number of (a) breweries, (b) employment and (c) gross value added (GVA) sectoral contribution by UK region.

provides Spearman’s rank correlations among variables. Higher levels of annual turnover are positively and significantly associated with larger beer portfolios, sales beyond 40 miles, number of controlled pubs, capital investments and charitable initiatives. These correlations corroborate findings gathered from other studies in relation to craft breweries’ expansion and business trajectory (Cabras et al., Citation2020 Drakopoulou Dodd et al., Citation2018;; Waehning et al., Citation2022). However, breweries’ performance is significantly, negatively correlated with volume of sales directed to free trade and breweries’ age: the first signals diversification in terms of sale channels already occurring in the sector before the pandemic crisis, while the second reflects the challenges for younger businesses to survive in a progressively saturated market (Carroll & Swaminathan, Citation2000). Correlations between breweries’ performance and several regional characteristics confirm assumptions previously made (Freeman, Citation2001; Gallin, Citation2008; Treno et al., Citation2007), with proxies such as housing prices and number of pubs and bars positively associated with correlation with breweries’ growth.

Table 1. Regression results (dependent variable: Annual turnover).

The descriptive analysis confirms our general assumptions and identifies some relevant associations among selected variables. To investigate these relationships further, we develop a range of multilevel regression models in which LAs are treated as the higher level, while breweries are treated as the lower level. Given the nature of the dependent variable (categorial and ordered) in the model, a set of two-level mixed-effects ordered logistic regressions were chosen to estimate the effects of the independent variables on breweries’ annual turnover. The underlying equation is:

where

represents the estimated cumulative logarithmic probability (log odds) of brewery i in LA j of being less than or equal to a specific category k, the latter representing the level of breweries’ annual turnover.

represents the constant term of the regression;

represents the coefficients of independent variables associated with breweries’ characteristics (

); while

represents the coefficients of the LA characteristics (

). The error terms are represented by

and

. Tests for multicollinearity on independent variables (variance inflation factor (VIF) = 1.39) confirm that the assumptions of ordinal logistic regressions in our modelling are met (Akinwande et al., Citation2015).

We develop three regression models by applying a step-by-step procedure, starting with a basic intercept model with no dependent variables (M0). Next, we calculate the intra-cluster correlations (ICC) that provide estimated proportions of the total variance attributed to the two levels, using the following equations:

where

and

represent the residual variance at brewery and LA level, respectively. The ICC analysis indicates that 89% of the variance of breweries’ annual turnover can be attributed to the brewery level, while only 5% can be attributed to the LA level, with the remaining 6% likely linked to a time effect. The time effect is captured in model M1, which indicates annual turnover significantly increasing over time, while brewery attributes are introduced in model M2; both models are in the supplemental data online. Regional characteristics are introduced in model M3, which is the final specification for our regression analysis, first applied to the whole dataset; and then separately to predominantly urban (M3.1), suburban (M3.2) and predominantly rural breweries (M3.3).

Results in confirm a few findings characterizing the business performance of UK breweries in pre-COVID times. First, breweries with higher annual turnover were highly involved in supporting charitable and volunteering initiatives. This finding holds for urban, suburban and rural breweries and corroborate engagement with the local community as a key factor for breweries’ success (Cabras & Bamforth, Citation2016; Drakopoloulou Dodd et al., Citation2018). Supporting these initiatives within local communities allows them to build a loyal customer base as well as to nourish strong ties with local businesses and people (Boden, Citation2012).

Table 2. Correlations.

Second, breweries’ age and larger beer portfolios explain higher annual turnover levels in our model, which shows that younger, less established breweries have fewer chances to achieve higher turnover. It might take several years for a new brewery to get the return on capital invested; as such, younger breweries might have struggled to diversify their portfolio offer in pre-COVID-19 times, failing to capture beer craft beer demand driven mostly by variety-seeking consumers (Shakina & Cabras, Citation2022; Waehning et al., Citation2022).

Third, the model identifies a significant relationship between craft breweries’ business performance and increases in capital investment, and with increases in production volumes. Ongoing investment in upgrading and replacing of the equipment used for brewing is essential not only to maintain the current levels of output but also to expand breweries’ production capacities which helps to achieve a higher annual turnover (Bolwig et al., Citation2019).

The models identify several differences in breweries’ performance related to their location. Levels of annual turnover grow significantly over time for breweries situated in urban and rural areas; while higher housing prices increase the odds of higher turnover for an urban brewery, they decrease the odds if the brewery is rural. Overall, urban or town breweries performed better within more affluent LAs, probably due to higher consumption levels and a willingness to spend for craft beers of potential consumers (Cabras et al., Citation2020). On the contrary, higher housing prices in rural areas, associated with an average older resident population, might have negatively affected demand for craft beers. Unemployment shows different effects on breweries’ turnover in urban and rural zones, which might be explained by differences in population density, consumption and inequality (Young, Citation2013). Rising unemployment in rural areas might lead to out-flow migrations towards urban areas, resulting in decreased beer consumptions at a local level, whereas unemployment in urban areas is usually highly localized and exists spatially within the defined sub-markets (Morrison, Citation2005).

Lastly, better performing urban and town breweries in pre-COVID-19 times were likely to sell a larger proportion of their beers beyond 40 miles from their location, hinting to increasing competition in the UK craft beer sector, with urban and town breweries struggling to grow (Drakopoulou Dodd et al., Citation2018). Due to market saturation, some breweries might have reconsidered their trajectories to develop or even survive well before COVID-19, focusing on sales outside of their immediate spatial proximity and inevitably denting into rural markets. As for rural breweries, the models indicate that their performance depended mostly on the pubs they controlled, used as safe channels to sell their own beer production.

4.2. Findings from in-depth interviews and focus groups: contextualizing the UK craft brewing sector

Information gathered from in-depth interviews and focus groups is investigated by using the framework proposed by Drakopoulou Dodd et al. (Citation2018), which illustrates different entrepreneurial contexts in which craft breweries operates. Their framework comprises four main contexts: institutional, which defines legislative and regulatory boundaries; business, which identifies the main business and commercial characteristics associated with beers’ demand and supplies within their market of reference; spatial, which refers to the locational areas and embedded networks served by craft breweries; and social, which arguably alludes to the historical and traditional roots that reflect many aspects of the collaborative, cooperative and competitive environment characterizing the craft beer sector in the UK and abroad. Given that the spatial context is already embedded in our investigation, with three levels classifying breweries as urban, suburban and rural areas; we focus on the remaining three contexts.

These are analysed across a temporal span comprised in three macro-periods: pre-COVID-19 (information gathered from our econometric analysis and secondary sources between 2015 and 2019); during COVID-19 (2020–21) and after COVID-19 (2022 onwards). summarizes the main outcomes of this exercise. The situation before the COVID-19 outbreak and summarized in the first column has been already discussed and assessed above. In this section we focus on the following two periods considering data gathered from interviews and focus groups.

Table 3. Contextualization of the UK craft brewing sector.

4.3. Craft breweries during COVID-19

Like many other SMEs and micro-enterprises, craft breweries suffered significantly from the COVID-19 outbreak in March 2020 due to severe limitations imposed on hospitality and related sectors. Being cut off from their usual networks and customer interactions, and in some cases from their furloughed staff, affected the capacity of many small breweries to ‘bounce back’ with innovative ideas and to explore alternative solutions. By contrast, larger established brewers with traditionally robust supply chains and property portfolios were better suited to provide a resilient response. During this period, four key findings transpire from our interviews and focus groups.

4.3.1. Location and turnover

Breweries’ growth associated with larger product variety appears to be a strategic business decision not necessarily linked to location. Before 2020, breweries selling their beer further afield through on- and off-trade outlets registered an average higher turnover compared with other breweries. The turbulence and disruption brought by COVID-19 and the consequent lockdowns had a detrimental impact on the hospitality sector, essentially eliminating on-trade as a key route to market for the brewing industry overnight. Opportunities for sales to the pub trade, particularly for brewers seeking to extend their market reach, disappeared indefinitely from one day to the next. This was confirmed in the first round of interviews with comments such as:

Route to market. … Basically, three days before the recommendation against going to pubs was announced, our sales dropped to about zero … the next week we had negative sales, so it was customers returning products because they know they can’t sell them.

(10N – Urban)

When there was the first announcement from the government about don’t go to pubs. … That was a massive blow to your business. Yes, we lost 95% of our business in two hours on that night.

(2N – Town)

We’ve bought a small brew kit so that we can do more interesting specials and things that don’t take up the capacity that we need in other places … it was always in the plan (but) it may have been brought forward.

(4G – Rural)

Lockdown helped us gain perspective … we had time to reflect and noticed things we were doing wrong before the lockdown and changed those. For example, we invested into a new brewery in 2021 and are still at full capacity. So, yea it gave us perspective.

(10N – Rural)

4.3.2. Support from local communities

The relevance of support from local consumers to keep the breweries alive during the pandemic is rated as a key success factor by breweries in each of the three geographical settings considered. For instance, a prominent requirement to respond to changing market routes was the ability to sell directly to consumers: this greater emphasis on direct sales saw increased importance for both hyper-local trade at a community level and some nationwide sales through online retailing directly to the consumers. However, this factor was crucial regardless of breweries’ location, since routes to markets broke off for everyone and consumers were very limited in their movements due to the lockdown. The research identified a growing desire to support local businesses, although in some cases local support proved a barrier for breweries trying to re-establish routes to market further afield:

I think there’s going to be a lot more support for your local brewery and your local businesses. So, it seems like our you know, our web sales went out like that and they’ve maybe gone down slightly. But they’re staying at a level, we’re getting multiple orders a day still.

(6N – Urban)

More local support was great, but it also meant that we’re now finding it hard to get into the other cities because they’re all supporting their local breweries … it became almost like a tribal warfare of, ‘oh well, you’re not local to me’ or something like that. So, it was a double-edged sword you know.

(FocusG)

One of the things that was massively beneficial for us during lockdown was … social media interactions through any form. … People in our industry no longer want to consume what we produce regularly; they always want to have the next new thing. This pandemic accelerated that because they were sat at home, they were consuming, so they were getting through way more beer at home.

(FocusG)

The funny thing I find that’s really tied into your brewing identity as well. So, we took the exact opposite approach, we curbed the specials, we did a big focus on core and the core seems to be doing way better than the specials.

(FocusG)

4.3.3. Access to financial support at a local level

The level of accessibility to grants and loans for surveyed breweries during to the crisis appears to be heavily associated with location. With the advent of COVID-19, the ability to pivot by making quick changes and investments became a vital business strength. The CJRS and BBLS removed an important fixed cost for them in the short run, although these schemes mostly benefited those who had the expertise required to navigate the administrative burden of securing business support and engaging with larger retailers and wholesalers. Responses from interviews highlight how breweries’ location and spatial position played a crucial role in the accessibility to various grants and funding to pivot in such a volatile time. Breweries located in urban areas and towns appeared to be best placed in terms of capturing such opportunities:

Yes, we were lucky in that we had the website … we’ve qualified for a £1,000 grant; we’re using that £1,000 grant to hire a website developer to improve our website, … it is the most critical and essentially only point of revenue in the business now.

(4N – Urban)

So, we’re going to move or warehousing to another site and we can do that because we can take advantage of some of the funding mechanisms that are available right now … we are going to tidy ourselves up, but we just can’t think about hugely expanding production.

(2F – Town)

4.3.4. Collaborative initiatives

Various types of collaborative initiatives sparkled particularly among breweries located in town areas, offering new and/or additional routes to market to those involved and mitigating the adverse effects of lockdowns. Interviews provided some evidence about breweries ‘joining forces’ and working together to respond to the crisis. With sales moving entirely online, some breweries lacking online presence found support from other breweries having a functioning website and web-shop, who offered the possibility to sell their products as guest although this applied only among breweries located in towns and urban areas. Aside website and online commerce, only one new collaborative venture between two breweries emerged from interviews. The need to look after one’s own business was predominant among our interviewees, as shown by excerpts below:

We’ve got … Brewery round the corner. They don’t have a website. They had some canned stock, so we’ve worked with them to get their stuff onto our website as well, so we’ve sort of become a factor some other breweries too, which has been quite convenient.

(2G – Town)

With a much smaller economy, there is a lot more fighting for sales involved … everyone has respectfully backed down on asking for the assistance of the networks.

(F1 – Urban)

But in terms of networking with other brewers, nothing. There’s been no contacts other than from with our bottling customers.

(F6 – Town)

4.4. Brewing in a post-COVID-19 world

When all restrictions were lifted in January 2022, some breweries hoped for a paced recovery through the years. However, from interviews’ responses gathered between April and June 2022, it appears that many craft breweries were not experiencing the business relief they hoped for. The fiscal incentives provided by government ceased almost immediately, and loans needed to be repaid. A combination of rising inflation and diminishing investments hit the UK brewing industry hard. The Ukraine–Russian conflict, which started in February 2022 and is still ongoing, exacerbated the situation further by significantly increasing brewing costs compared with the previous year, mostly due to increased energy prices (more than 200% in the first half of 2022; Cooney, Citation2022) and CO2 costs (300% more expensive; BBC, Citation2022). Higher fuel prices and difficulties in the supply chain, mainly due to keg shortages, squeezed already tight profit margins for craft breweries, making it almost impossible to run a profitable business.

Surveyed breweries across rural, urban and towns confirmed the importance of local support and enhanced online engagement as two key success factors identified from earlier interviews. Direct sale was now even more crucial for them due to increased profit margins, enabling many to develop closer relationship with customers and to learn from them. In addition, online sales removed publicans as the middleman between craft breweries and customers, increasing profit margins for businesses.

We strengthen our relationships with our customers, just by me delivering directly I got a feel of the background of our customers, so I got a much better feel for the type of our customers e.g., do I deliver to a castle or council estate.

(10G – Urban)

Initially we were planning 30% direct sales and 70% pubs, but we learned from the pandemic to maximise your direct sales because that is where your money is … we started having tab days in the brewery we can get £3.50 for a pint instead of £1 and it gets the relationship with people. So, we can tap into the massive tourism trade.

(11N – Rural)

You showcase your drinks in the pub, but people are drinking at home … I had all the wrong kit because I did supply cask to pubs, if I had waited a bit longer, I would have bought dual purpose vessels and tanks … now I must go out and get a contract bottler. And that is the lessen for me going forward is small pack.

(F10 – Rural)

Trade in terms of cask and pubs has picked up again the bottle shops are where they were for us but cask is still down a lot of the pubs are still buying very tentatively still and buying less.

(F11 – Rural)

Whereas the craft beer world keeps asking ‘what is new?’, I would rather give consistency of what is good rather than to bring something new all the time; but I got to satisfy the demand so if it is successful, it will be added to my core range.

(F10 – Rural)

In 2020 we brewed 100 different beers even though before we were mainly focussing on our core range, but those kept making people coming back. People have the fear of missing out.

(F10 – Urban)

We are keeping up the variety of beers because it allows us to use cheaper ingredients to keep our prices stable for the customers. Since prices for everything are still going up so the variety allows us more flexibility.

(F7 – Urban)

We got an e-commerce manager to come in and keep the customers on board since the pandemic. So, we now have a team who actively generate direct sales. Now direct sale online is something we actively push. We make higher profit margins.

(F10 – Urban)

5. DISCUSSION AND CONCLUSIONS

The above analysis provide comprehensive insights on the UK craft brewery sector before, during and after the COVID-19 crisis. The econometric models identified several factors for successful business performances before the crises, mostly related to larger beer-portfolios, engaging with local communities, and expanding market reach beyond spatial proximity. In terms of location, community engagement, brewing capacity and market reach beyond 40 miles were factors of success in more urban areas, while a larger beer-portfolio seemed a distinctive factor of success for breweries located in more rural areas. In addition, being located in LAs with higher numbers of pubs and bars provided an advantage to more established breweries in comparison with younger ones. Although recent studies identify young start-ups and micro-sized firms operating in sectors such as hospitality and food services as those most affected by COVID-19 (Bailey et al., Citation2020; Cowling et al., Citation2020; Galkina & Jack, Citation2022), this was not the case among craft breweries we analysed.

At the start of the pandemic crisis, support from local consumers remained crucial to keep breweries alive regardless of the three locational settings investigated. This situation, however, seems to have somehow penalized rural breweries, as custom volumes generated from their local customers would not be enough to face the crisis. Rural breweries faced more challenges to attract customers compared with urban and towns breweries, now also keen to support ‘their’ local breweries, confirming the importance for firms to rely on more mixed networks in order to expand their market and business opportunities (e.g., Branicki et al., Citation2018). In terms of resilience, this finding corroborates evidence provided by Brown and Cowling (Citation2021) who indicate higher business risks associated with COVID-19 ‘unequally concentrated in poorer and more peripheral towns and cities, implying that any potential economic recovery will be more difficult to achieve given their already lower starting point pre-crisis’ (p. 328). For rural craft breweries, the pandemic crisis seems to have had a stronger impact due to the reduced custom, limited social capital and fewer networking opportunities related to their spatial dimension.

During COVID-19, Brown and Cowling (Citation2021) identified different levels of business performance in relation to spatial proximity from the London region, with more peripheral regions deemed less resilient and therefore more exposed to the negative effects of the pandemic crisis. We could not identify such levels of regional disparity across craft breweries in the UK, although our findings did highlight some significant variation associated with urbanity and rurality mostly linked with different business strategies. For instance, before COVID-19, expanding beer portfolios was a strategic business decision not necessarily linked to where businesses were located, although implicitly customer base and demand size would have had an impact on the range of beers produced. With the COVID-19 outbreak, some breweries continued expanding their beer portfolios, while other decided to focus just on selected styles. This choice could have been determined by asset endowment: breweries that already had assets such as on-premises bottling and canning machines and an operative web-shop before COVID-19 were able to better absorb the disruption caused in the sector immediately after the first lockdown was lifted. These breweries could operationalize changes in a quicker and more flexible manner than others, corroborating findings provided by other studies in relation to resource efficiency and high levels of agility needed by firms to change direction in response to external conditions (Galkina & Jack, Citation2022; McCann, Citation2004). These aspects would have influenced breweries’ decision about whether expanding beer portfolios or focusing on selected brands; equally, it is reasonable to assume that location and localization of both breweries and breweries’ sales would also matter, particularly in rural areas due to demand volumes at a local level.

Our analysis demonstrates a strong relationship between location and better access to financial support such as grants and loans. Sampled breweries located in urban and towns areas benefited most from loans and grants made readily available by the UK government compared with rural ones. Urban and town breweries would have had more access at a local level to the necessary expertise required to navigate the administrative burden of securing financial support. They may also be involved in more varied networks, providing them with benefits in terms strong ties (Galkina & Jack, Citation2022), trusting cooperation and loyal support (Bosworth & Atterton, Citation2012), more flexible and accessible routes to supply chains and institutional structures – a ‘double-layered’ embeddedness from which SMEs can profit from at a local level (Dormady et al., Citation2019; McCann et al., Citation2022).

Re-adapting to a post-COVID-19 world appears very challenging for craft breweries. At the time of writing, growing levels of inflation and soaring energy costs are significantly reducing their profit margins. Breweries in urban and town areas pivoted the fastest towards other routes to market, for example, small packaging solutions, continuing deliveries and direct sales via online engagement. Those in rural areas appear slower in embracing change and suffered from an increased consumers’ demand for craft beer variety. For all breweries, the necessity to cut costs might probably expand opportunities for joint ventures, but we only found two examples of collaborative initiatives, in contrast with the narrative reporting high levels of collaboration in the craft brewing sector (Drakopoulou Dodd et al., Citation2018; Garavaglia & Swinnen, Citation2018). Findings indicate that a higher, broader interplay across different network layers in the sector benefited urban and town breweries to find supply chain solutions, confirming the importance of widening geographical reach in terms of market channels (Clausen, Citation2020; Greenberg et al., Citation2018).

The current post-COVID-19 UK craft beer sector sees breweries in urban and towns areas more resilient and better placed from a business perspective compared with rural breweries, mainly due to the variety of their networks and the size of their local customer basis. They also benefited more from public financial support, although this is now fading down before the pandemic crisis. The commitment of the UK government towards craft breweries – particularly smaller ones – in terms of rate reliefs, accessible grants and favourable loan schemes will be important to enable many of these businesses to recover and bounce back in a post-COVID-19 world. This statement seems particularly relevant for rural breweries, which represent important employers and training providers (SIBA, Citation2020) in areas where these types of opportunities are frequently reduced.

From our analysis, it appears that COVID-19 has accelerated the rebalancing process in the craft beer market that started well before the crisis. The significant fiscal support provided by successive UK governments to craft breweries and the duty cuts introduced in the 2000s and 2010s may have helped many of them to survive, even those whose business performance was poor and not financially sustainable (Cabras et al., Citation2020). Likewise, the widespread financial aid provided by the UK government during lockdowns helped many breweries to survive, including some already operating in not profitable conditions, confirming fears expressed by Belghitar et al. (Citation2022) that support measures for SMEs may have simply extended the life of already troubled businesses, creating ‘zombie firms’ in the sector which would have long gone without support. The recent spike of closures among craft breweries reported in the media (BBC, Citation2022; Cooney, Citation2022) seems to support this hypothesis.

We acknowledge some limitations in our research study. First, the econometric models are based on a five-year span and therefore constrained in capturing economic trends or craft breweries in the pre-COVID period, although we could not find any consistent information related to a longer period. Second, despite the effort in increasing the level of representativeness of our interview sample, we are aware that the information collected from the 31 in-depth interviews and two focus groups provides a broad but limited overview of the themes and issues addressed in our investigation. Third, our analysis is based on a general urban, suburban (towns) and rural categorization: while these three categories enabled us to capture main trends and behaviours of the breweries we surveyed in our study, they also neglect some notable exceptions (e.g., breweries located in significantly rural LAs could still be based in large conurbations).

While this paper provides a fresh and timely contribution to the economic literature addressing the impact of COVID-19 on UK craft breweries, we hope it can inspire further research on the subject. Given the significant impact the pandemic crisis has had and will have on this as well as other related sectors, more studies are needed to help predict future trends in the beer and brewing industry, and to better understand the potential of craft beers and breweries in terms of local economic development.

Supplemental Material

Download PDF (246.5 KB)ACKNOWLEDGEMENT

The authors thank the three anonymous referees for the useful comments and feedback.

DISCLOSURE STATEMENT

No potential conflict of interest was reported by the authors.

Notes

1. Allied Breweries, Bass Charrington, Courage Imperial, Scottish and Newcastle, Whitbread, and Watneys (Cabras & Bamforth, Citation2016).

REFERENCES

- Akinwande, R., Dikko, H., & Samson, A. (2015). Variance inflation factor: As a condition for the inclusion of suppressor variable(s) in regression analysis. Open Journal of Statistics, 5(7|7), 754–767. https://doi.org/10.4236/ojs.2015.57075

- Bailey, D., Clark, J., Colombelli, A., Corradini, C., De Propris, L., Derudder, B., Fratesi, U., Fritsch, M., Harrison, J., Hatfield, M., Kemeny, T., Kogler, D. F., Lagendijk, A., Lawton, P., Ortega-Argilés, R., Iglesias Otero, C., & Usai, U. (2020). Regions in a time of pandemic. Regional Studies, 54(9), 1163–1174. https://doi.org/10.1080/00343404.2020.1798611

- Bailey, D., Crescenzi, R., Roller, E., Anguelovski, I., Datta, A., & Harrison, J. (2021). Regions in COVID-19 recovery. Regional Studies, 55(12), 1955–1965. https://doi.org/10.1080/00343404.2021.2003768

- Bartik, A. W., Bertrand, M., Cullen, Z. B., Glaeser, E. L., Luca, M., & Stanton, C. T. (2020). How are small businesses adjusting to COVID-19? Early evidence from a survey (Working Paper No. 26989). National Bureau of Economic Research (NBER). http://www.nber.orgpapersw26989

- BBC. (2022). Brewgooder boss warns of £7 a pint as costs soar. https://www.bbc.co.uk/news/uk-scotland-scotland-business-63379044.

- Beeson, J. (2018). Overcrowded beer market could lead to more craft brewery buyouts. The Morning Advertiser, August 29. https://www.morningadvertiser.co.uk/Article/2018/08/29/Are-more-craft-beer-buyouts-on-the-horizon

- Belghitar, Y., Moro, A., & Radić, N. (2022). When the rainy day is the worst hurricane ever: the effects of governmental policies on SMEs during COVID-19. Small Business Economics, 58(6), 943–961. https://doi.org/10.1007/s11187-021-00510-8

- Beltiski, M., Guenther, C., & Kritikos, A. (2022). Economic effects of the COVID-19 pandemic on entrepreneurship and small businesses. Small Business Economics, 58(2), 593–609. https://doi.org/10.1007/s11187-021-00544-y

- Berkes, F., & Ross, H. (2012). Community resilience: toward an integrated approach. Society & Natural Resources, 26(1), 5–20. https://doi.org/10.1080/08941920.2012.736605

- Bibby, P., & Shepherd, J. (2004). Developing a new classification of urban and rural areas for policy purposes – The methodology (Report). Department for Environment, Food and Rural Affairs, Countryside Agency. http://www.econsultation.net/ru/method_paper_final.pdf

- Boden, M. (2012). Achieving sustainability in the craft brewing industry. University of Nebraska. https://core.ac.uk/download/pdf/17269541.pdf

- Bolwig, S., Mark, M. S., Happel, M. K., & Brekke, A. (2019). Beyond animal feed? The valorisation of brewers’ spent grain. In A. By Klitkou, A. M. Fevolden, & M. Capasso (Eds.), From waste to value valorisation pathways for organic waste streams in circular bioeconomies. Routledge.

- Boschma, R. (2015). Towards an evolutionary perspective on regional resilience. Regional Studies, 49(5), 733–751. https://doi.org/10.1080/00343404.2014.959481

- Bosworth, G., & Atterton, J. (2012). Entrepreneurial in-migration and neo-endogenous rural development. Rural Sociology, 77(2), 254–279. https://doi.org/10.1111/j.1549-0831.2012.00079.x

- Branicki, L. J., Sullivan-Taylor, B., & Livschitz, S. R. (2018). How entrepreneurial resilience generates resilient SMEs. International Journal of Entrepreneurial Behavior & Research, 24(7), 1244–1263. https://doi.org/10.1108/IJEBR-11-2016-0396

- Brown, R., & Cowling, M. (2021). The geographical impact of the COVID-19 crisis on precautionary savings, firm survival and jobs: Evidence from the UK’s 100 largest towns and cities. International Small Business Journal: Researching Entrepreneurship, 39(4), 319–329. https://doi.org/10.1177/0266242621989326

- Cabras, I., & Bamforth, C. W. (2016). From reviving tradition to fostering innovation and changing marketing: The evolution of microbrewing in the UK and US, 1980–2012. Business History, 58(5), 625–646. https://doi.org/10.1080/00076791.2015.1027692

- Cabras, I., Lorusso, M., & Waehning, N. (2020). Measuring the economic contribution of beer festivals on local economies: The case of York, UK. International Journal of Tourism Research, 22(6), 739–750. https://doi.org/10.1002/jtr.2369

- Carroll, G., & Swaminathan, A. (2000). Why the microbrewery movement? Organizational dynamics of resource partitioning in the U.S. brewing industry. American Journal of Sociology, 106(3), 715–762. https://doi.org/10.1086/318962

- Clausen, T. H. (2020). Entrepreneurial thinking and action in opportunity development: A conceptual process model. International Small Business Journal: Researching Entrepreneurship, 38(1), 21–40. https://doi.org/10.1177/0266242619872883

- Cooney, C. (2022). More than 70% of pubs do not expect to survive winter as energy costs soar. The Guardian, August 23. https://www.theguardian.com/business/2022/aug/23/pubs-winter-energy-costs-soar

- Doyle Corner, P., Singh, S., & Pavlovich, K. (2017). Entrepreneurial resilience and venture failure. International Small Business Journal: Researching Entrepreneurship, 35(6), 687–708. https://doi.org/10.1177/0266242616685604

- Cowling, M., Brown, R., & Rocha, A. (2020). Did you save some cash for a rainy COVID-19 day? The crisis and SMEs. International Small Business Journal: Researching Entrepreneurship, 38(7), 593–604. https://doi.org/10.1177/0266242620945102

- Cowling, M., & Yue, W. (2021). The COVID-19 lockdown in the UK and subjective well-being: Have the self-employed suffered more due to hours and income reductions? International Small Business Journal: Researching Entrepreneurship, 39(2). doi: 10.1177/02662426209867

- Drakopoulou Dodd, S., Wilson, J., & Mac an Bhaird, C. (2018). Habitus emerging: The development of hybrid logics and collaborative business models in the Irish craft beer sector. International Small Business Journal: Researching Entrepreneurship, 36(6), 637–661. https://doi.org/10.1177/0266242617751597

- Dorling, D. (2020). Want to understand the COVID map? Look at where we live and how we work. The Guardian, November 29. https://www.theguardian.com/commentisfree/2020/nov/29/want-to-understand-the-covid-map-look-at-where-we-live-and-how-we-work

- Dormady, N., Roa-Henriquez, A., & Rose, A. (2019). Economic resilience of the firm: A production theory approach. International Journal of Production Economics, 208, 446–460. https://doi.org/10.1016/j.ijpe.2018.07.017

- Eachus, P. (2014). Community resilience: Is it greater than the Sum of the parts of individual resilience? Procedia Economics and Finance, 18, 345–351. https://doi.org/10.1016/S2212-5671(14)00949-6

- Freeman, D. G. (2001). Beer and the business cycle. Applied Economics Letters, 8(1), 51–54. https://doi.org/10.1080/135048501750041295

- Galkina, T., & Jack, S. (2022). The synergy of causation and effectuation in the process of entrepreneurial networking: implications for opportunity development. International Small Business Journal: Researching Entrepreneurship, 40(5), 564–591. https://doi.org/10.1177/02662426211045290

- Gallin, J. (2008). The long-run relationship between house prices and rents. Real Estate Economics, 36(4), 635–658. https://doi.org/10.1111/j.1540-6229.2008.00225.x

- Garavaglia, G., & Swinnen, J. (2018). Economic perspectives on craft beer: A revolution in the global beer industry. Palgrave Macmillan.

- Gong, H., Hassink, R., Tan, J., & Huang, D. (2020). Regional resilience in times of a pandemic crisis: The case of COVID-19 in China. Tijdschrift Voor Economische en Sociale Geografie, 111(3), 497–512. https://doi.org/10.1111/tesg.12447

- Greenberg, Z., Farja, Y., & Gimmon, E. (2018). Embeddedness and growth of small businesses in rural regions. Journal of Rural Studies, 62, 174–182. https://doi.org/10.1016/j.jrurstud.2018.07.016

- Hancock, E. (2020). UK government to change duty rules for craft breweries (Press Release). The Drink Business, July 22. https://www.thedrinksbusiness.com/2020/07/uk-government-to-change-tax-rules-for-craft-breweries/

- Hassink, R. (2010). Locked in decline? On the role of regional lock-ins in old industrial areas. In R. Boschma, & R. Martin (Eds.), The handbook of evolutionary economic geography. Edward Elgar.

- Hassink, R., & Gong, H. (2020). Regional resilience. In A. Kobayashi (Ed.), International encyclopedia of human geography. Elsevier.

- Hillmann, J., & Guenther, E. (2021). Organizational resilience: A valuable construct for management research? International Journal of Management Reviews, 23(1), 7–44. https://doi.org/10.1111/ijmr.12239

- Korsgaard, S., Hunt, R. A., & Townsend, D. M. (2020). COVID-19 and the importance of space in entrepreneurship research and policy. International Small Business Journal: Researching Entrepreneurship, 38(8), 697–710. https://doi.org/10.1177/0266242620963942

- Magis, K. (2010). Community resilience: An indicator of social sustainability. Society & Natural Resources, 23(5), 401–416. https://doi.org/10.1080/08941920903305674

- Martin, R., Pike, A., & Tyler, P. (2016). Spatially rebalancing the UK economy: Towards a new policy model? Regional Studies, 50(2), 342–357. https://doi.org/10.1080/00343404.2015.1118450

- Martin, R., Sunley, P., Gardiner, B., & Tyler, P. (2016). How regions react to recessions: Resilience and the role of economic structure. Regional Studies, 50(4), 561–585. https://doi.org/10.1080/00343404.2015.1136410

- Mason, C. M., & McNally, K. N. (1997). Market change, distribution, and new firm formation and growth: The case of real-ale breweries in the UK. Environment and Planning A: Economy and Space, 29(3), 405–417. https://doi.org/10.1068/a290405

- McCann, J. (2004). Organizational effectiveness: changing concepts for changing environments. Human Resource Planning, 27(1), 42–51.

- McCann, P., Ortega-Argilés, R., & Yuan, P. (2022). The COVID-19 shock in European regions. Regional Studies, 56(7), 1142–1160. https://doi.org/10.1080/00343404.2021.1983164

- Miklian, J., & Hoelscher, K. (2022). SMEs and exogenous shocks: A conceptual literature review and forward research agenda. International Small Business Journal: Researching Entrepreneurship, 40(2), 178–204. https://doi.org/10.1177/02662426211050796

- Moore, A. A., Gould, R., Reuben, D. B., Greendale, G., Carter, K., Zhou, K., & Karlamangla, A. (2005). Longitudinal patterns and predictors of alcohol consumption in the United States. American Journal of Public Health, 95(3), 458–464. https://doi.org/10.2105/AJPH.2003.019471

- Morrison, P. S. (2005). Unemployment and urban labour markets. Urban Studies, 42(12), 2261–2288. https://doi.org/10.1080/00420980500332031

- Nelson, J. P. (1997). Economic and demographic factors in U.S. alcohol demand: A growth-accounting analysis. Empirical Economics, 22(1), 83–102. https://doi.org/10.1007/BF01188171

- Office for National Statistics (ONS). (2019). The economies of ales. https://www.ons.gov.uk/businessindustryandtrade/business/activitysizeandlocation/datasets/publichousesandbarsbylocalauthority

- Office for National Statistics (ONS). (2020). Population estimates. https://www.ons.gov.uk/peoplepopulationandcommunity/populationandmigration/populationestimates/datasets/populationestimatesforukenglandandwalesscotlandandnorthernireland

- Office for National Statistics (ONS). (2021). Housing prices indexes at local authority level. https://www.ons.gov.uk/peoplepopulationandcommunity/populationandmigration/populationestimates/datasets/populationestimatesforukenglandandwalesscotlandandnorthernireland

- Phillipson, J., Gorton, M., Turner, R., Shucksmith, M., Aitken-McDermott, K., Areal, F., Cowie, P., Hubbard, C., Maioli, S., McAreavey, R., Souza-Monteiro, D., Newbery, R., Panzone, L., Rowe, F., & Shortall, S. (2020). The COVID-19 pandemic and Its implications for rural economies. Sustainability, 12(10), 3973. https://doi.org/10.3390/su12103973

- Pike, A., Dawley, S., & Tomaney, J. (2010). Resilience, adaptation, and adaptability. Cambridge Journal of Regions, Economy and Society, 3(1), 59–70. https://doi.org/10.1093/cjres/rsq001

- Schmidt, A. L., Mäkelä, P., Rehm, J., et al. (2010). Alcohol: equity and social determinants. In E. Blas, & A. Kurup (Eds.), Equity, social determinants and public health programmes. World Health Organisation (WHO).

- Shakina, E., & Cabras, I. (2022). How do beer prices vary across different pubs? An empirical study. International Journal of Contemporary Hospitality Management, 34(5), 1984–2003. https://doi.org/10.1108/IJCHM-08-2021-0981

- Society of Independent Brewers (SIBA). (2016–20). British beer: A report on the annual members survey of the society of independent brewers. SIBA.

- Sutton, J., & Arku, G. (2022). Regional economic resilience: towards a system approach. Regional Studies. Regional Science, 9(1), 497–512. doi: 10.1080/21681376.2022.2092418

- Treno, A. J., Johnson, F. W., Remer, L. G., et al. (2007). The impact of outlet densities on alcohol-related crashes: a spatial panel approach. Accident Analysis & Prevention, 39(5), 894–901. https://doi.org/10.1016/j.aap.2006.12.011

- Waehning, N., Cui, C. C., Cabras, I., & Bian, X. (2022). How consumers’ need for variety and social consumption influences festival patronage and spending. Event Management, doi:10.3727/152599522X16419948391087

- Welter, F., Baker, T., & Wirsching, K. (2019). Three waves and counting: the rising tide of contextualization in entrepreneurship research. Small Business Economics, 52(2), 319–330. https://doi.org/10.1007/s11187-018-0094-5

- Young, A. (2013). Inequality, the urban–rural gap, and migration. The Quarterly Journal of Economics, 128(4), 1727–1785. doi:10.1093/qje/qjt025

- Yue, W., & Cowling, M. (2020) The Covid-19 lockdown in the United Kingdom and subjective well-being: Have the self-employed suffered more due to hours and income reductions? International Small Business Journal: Researching Entrepreneurship, 39(2), 93–108. https://doi.org/10.1177/0266242620986763