ABSTRACT

The field of CSR in family firms has experienced remarkable growth recently. Therefore, a literature review on the topic is needed to provide an updated overview of extant research and draw guidelines for future research. Using bibliometric mapping, we conducted a systematic literature review (SLR) on corporate social responsibility (CSR) in family business drawing on the Web of Science (WOS) and Scopus databases. The bibliographic coupling conducted suggests that family involvement, corporate governance, and sustainability are the most frequently studied topics. Furthermore, through our SLR, we systematized the studies into an interpretative framework, identifying the drivers and outcomes of CSR practices, processes, and strategies in family business. The study reveals and organizes the state-of-the-art of CSR research in family business, outlines important theoretical implications and develops a future research agenda.

Introduction

Since the 1950s, corporate social responsibility (CSR) has flourished as a research topic in the management field (Bergamaschi & Randerson, Citation2016; Bowen, Citation1953; Carroll, Citation1999; McWilliams & Siegel, Citation2001; Moura‐Leite & Padgett, Citation2011). Scholars have developed numerous definitions of CSR, mirroring the evolution of social movements pertaining to civil rights and environmental issues (Carroll, Citation2016), and incorporating different nuances regarding the economic, regulatory, voluntarism, and ethical dimensions of CSR. Generally, CSR is related to a company’s activities, processes, and status in connection with its stakeholder obligations (Hsu & Cheng, Citation2012; Wood, Citation1991).

However, the issue at stake in this work is not defining CSR, but rather assessing the research field of CSR in family firms. Indeed some CSR research suggests that it is important to understand how CSR behaviors and strategies might change in different organizational settings (Dahlsrud, Citation2008). One type of organizational setting that is ubiquitous in any world economy is the family firm (Bennedsen et al., Citation2007; De Massis et al., Citation2018a; M. A. Gallo, Citation1995; Poutziouris et al., Citation1997; Poza, Citation1995). Family firms (FFs) and their management are increasingly studied in the management field (De Massis et al., Citation2021; King et al., Citation2021; Lu et al., Citation2013; Sharma, Citation2004), and specifically in the entrepreneurship field (Williams et al., Citation2018). Academics used a variety of definitions to identify family firms (Chua et al., Citation1999), combining family involvement and family essence criteria (Chrisman et al., Citation2012; De Massis et al., Citation2014). One of the most adopted definitions of FF is any firm in which the founder owns a portion of the firm and sits on the board of directors (Chrisman et al., Citation2012; Habbershon et al., Citation2003; Miller et al., Citation2011).

Family business CSR research has focused either on the relationship between family involvement and CSR, or on the impact of CSR on FF performance. For example, Cui et al. (Citation2018) address the relationship between family involvement and CSR, Martínez-Ferrero et al. (Citation2017) examinethe role of family ownership and CSR disclosure, Iyer & Lulseged (Citation2013) investigatethe relationship between family status and CSR, and Gavana et al. (Citation2017a) study the influence of equity and bond issues on sustainability disclosure. Gavana et al. (Citation2018) analyze the impact of CSR reporting on revenues. Before our systematic review, we could not quantify exactly whether family firms are more or less socially responsible than other types of firms. The vast number of papers on CSR in the FF literature analyzed in this work have allowed us to gain a deep understanding of the behavioral and operational aspects of FFs in relation to CSR adoption, and the impact of such adoption on FFs.

Despite calls for a comprehensive study of CSR in FFs, most research has tended to focus on firm characteristics and contextual factors (Campopiano & De Massis, Citation2015), with few studies examining the relationship between FFs and CSR orientation. The latest FF CSR research stream constitutes a promising avenue for further exploration, given the high proportion of such firms in any national economy and that FFs are increasingly interested in (and engaging with) CSR (Le Breton-Miller & Miller, Citation2009; Kuttner et al., Citation2020; De Massis et al., Citation2018a; McGuire et al., Citation2012; Miller et al., Citation2009; Peake et al., Citation2015), especially considering that (i) research on CSR has not yet reached full maturity, and (ii) management scholars, while using different perspectives, have attained inconsistent findings on the drivers and outcomes of CSR strategies and practices. Therefore, despite the research field has experienced a remarkable growth recently, a systematic literature review on the topic is needed to provide an updated overview of extant research and draw guidelines for future scholarship. Two relevant and unanswered research questions emerge when observing the limited understanding of CSR practices in FFs in extant literature:

What are the most recurrent topics in the literature on CSR in FFs?

What are the drivers and outcomes of CSR adoption in FFs?

In addressing these two research questions, we contribute to both the FF and CSR literature streams. Indeed, not only do we illustrate the evolution of the research field at the intersection of FFs and CSR, but also shed light on the factors that motivate FFs to embrace CSR and the outcomes of CSR for FFs. To our best knowledge, no attempts have been made to carry out either a systematic literature review or bibliometric mapping of research at the intersection of CSR and FFs, illuminating the motivations for CSR adoption and the outcomes of CSR practices in FFs.

Research design

To understand the evolution of the topic over time and capture the drivers and outcomes of CSR adoption in FFs, we carried out a systematic literature review (SLR), drawing on the Web of Science (WOS) and Elsevier Scopus databases, corroborated with bibliometric mapping. SLR is considered a necessary tool to systematically evaluate a given body of literature (Ginsberg & Venkatraman, Citation1985). Moreover, as a comprehensive, structured, and analytical means of accurately organizing reviews, SLR is an effective method to identify research gaps in the literature (Klassen et al., Citation1998). Widely adopted in the broad social sciences (Tranfield et al., Citation2003) and in management and entrepreneurship research (Crossan & Apaydin, Citation2010; Parris & Peachey, Citation2013; Pittaway et al., Citation2004), SLR offers a number of benefits, including the ability to construct flexible databases of articles that can be easily updated and interrogated (Pickering & Byrne, Citation2014).

Furthermore, bibliometric mapping is a method that introduces a statistical evaluation of academic connections across publications (Garfield, Citation1955; Platt, Citation1965; Pritchard, Citation1969), providing a clear picture of the most relevant topics under analysis (in our case, CSR in FFs). This method has been commonly adopted in the management literature (Fahimnia et al., Citation2015; Markoulli et al., Citation2017; Zupic & Čater, Citation2015), and the benefits include the ability to provide visualization maps based on the most cited papers, presenting insights for current research concerns and guidelines for upcoming research (Jones & Gatrell, Citation2014).

Data

Data were gathered from the most comprehensive sources of indexed academic work: WOS and Scopus. The former covers works published since 1900 and content from 8,700 journals. In addition, it focuses on a multifaceted set of disciplinary fields in the wider hard sciences, technology, social sciences, arts, and humanities (Archambault et al., Citation2009; Falagas et al., Citation2008). The latter covers works published since 1966, indexing 12,850 journals in fields such as physical sciences, health sciences, life sciences, and of course, social sciences (Archambault et al., Citation2009; Falagas et al., Citation2008). The two databases have been widely adopted in prior academic research (Liñán & Fayolle, Citation2015; Mariani et al., Citation2018; Mariani & Borghi, Citation2019; Zupic & Čater, Citation2015), and are considered the most comprehensive sources of studies in the social sciences (Mongeon & Paul-Hus, Citation2016; Vieira & Gomes, Citation2009). The data for this study were collected in January 2021, with the search limited to articles published until 2020.

To search the databases, we first created a data extraction protocol/sheet (Kraus et al., Citation2020) covering a set of keywords related to CSR and FFs. The objective was to gather the greatest number of relevant articles from both data sets. More specifically, the CSR-related keywords are “corporate social responsibility” and “social responsibility,” while the FF-related keywords are “family business*,” “family firm*,” “family-owned compan*,” “family-owned business*,” “family-owned firm*,” “family owned compan*,” “family owned business*,” “family owned firm*.” Where appropriate and relevant, words were taken in both their singular and plural form using appropriate syntax (for example, an “*” symbol). We then linked the CSR-related keywords with the FF-related keywords, using Boolean operators (for example, we matched “corporate social responsibility” AND “family business,” “social responsibility” AND “family business,” “social responsibility” AND “family-owned firms,” and so forth), and combinations using the plural forms.

To begin, we ran different queries in WOS based on the identified keywords (and their plurals), and all the different combinations of keywords in the “topic” and “title” fields. Only works published up to December 2020 were included in the analysis. The WOS search yielded 345 studies in total. After excluding duplications, proceedings, book chapters, books, and editorial material not published in English, the final results yielded 134 outputs.

We then repeated the same process on Scopus. We ran the same queries, using the different combinations of keywords in the fields related to “articles,” “abstract,” and “keywords.” For consistency, we only took into account works published until December 2020. The search yielded a total 236 works. After the same exclusions, the final results yielded 121 outputs. The overall data gathering process is illustrated in .

Figure 1. Data-gathering process.

Methods

Our aim is to present a clear picture of the most relevant topics and aspects relating to CSR in FFs and identify the drivers and outcomes of CSR adoption. To provide a systematic review, we used a bibliometric approach and, consistent with Mas-Tur et al. (Citation2020), Mariani (Citation2020), and Rovelli et al. (Citation2021), we implicitly proxied productivity through the number of publications and popularity through the number of citations. Moreover, we moved a step forward and conducted a data analysis using bibliometric mapping (for example, co-citation, co-occurrence, and bibliographic coupling) that utilizes bibliographic data extracted from databases to create structure maps of scientific fields (Zupic & Čater, Citation2015). Bibliographic coupling is a technique that measures the similarity between documents by capturing the number of shared references (Kessler, Citation1963). The references cited in an article help explain the topic. Therefore, articles citing the same references are linked (Perianes-Rodriguez et al., Citation2016). Such analysis has been widely adopted in the literature (Mura et al., Citation2018; Nosella et al., Citation2012; Yan & Ding, Citation2012), as it is considered a beneficial technique to evaluate data through mapping extant research (Boyack & Klavans, Citation2010; Small, Citation1999; Vogel & Güttel, Citation2013). We hence deemed the bibliographic coupling analysis of documents, authors, and journals an appropriate approach to present a clear picture of the evolution of scientific production on the focal topics of CSR in FFs. We employed the VOSviewer package of Van Eck & Waltman (Citation2009) to generate bibliometric maps, widely adopted in the literature (for example, Apriliyanti & Alon, Citation2017; Ferreira, Citation2018). The mapping technique used (VOS) did not involve multidimensional scaling as VOS has been found to be superior to multidimensional scaling to build bibliometric maps (Van Eck et al., Citation2010).

The stages of our data analysis are shown in . After bibliographic coupling, the next step was to merge the 134 outputs from WOS and the 121 from Scopus to obtain a final merged sample of 168 studies after removing 87 duplicated publications. The merged sample was examined in relation to the following criteria: subtopics, variables, constructs, samples, geographic region, theory, and findings.

Figure 2. Data analysis steps.

Subsequently, after evaluating CSR in the FF literature, we organized the selected studies into a framework as shown in .

Figure 3. Conceptual framework.

The framework identifies the drivers, practices, and outcomes of CSR adoption in FFs, drawing on several literature reviews (Campopiano et al., Citation2017; Feliu & Botero, Citation2016; Lumpkin, Citation2011; De Massis et al., Citation2013). We interpret CSR as a set of practices and strategies influenced by certain drivers that produce outcomes in FFs. We define drivers as any FF factor that has an impact on CSR, while outcomes are any impact of CSR on FFs. This framework is useful to create a matrix analysis of CSR drivers and outcomes in FFs.

We next provide a descriptive analysis of our samples (obtained through the SLR queries), and then present the findings of the bibliographic coupling. Last, after identifying the drivers and outcomes of CSR in FFs based on the adopted framework, we present the findings of the selected review studies.

Findings

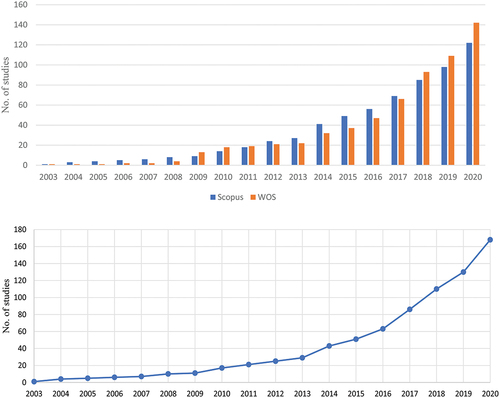

The findings illustrate the scope and variety of research on CSR in FFs. As clearly show, interest in this topic from entrepreneurship and management researchers has increased exponentially over time both within each database (WOS and Scopus) and generally (considering both databases). The studies were carried out in 34 different countries and published in 76 different journals. A wide variety of theories and methods have been adopted. To illustrate the evolution of scientific production on the focal topics, we plotted the cumulative frequency of the published documents. The annual growth of outputs testifies to this evolution: the average annual growth in WOS is 33% and in Scopus 29%.

Figure 4. (a) Cumulative frequency of published documents from WOS vs Scopus databases until 2020. (b) Cumulative frequency of published documents from the merged sample (WOS and Scopus databases) until 2020.

Samples description

The field of CSR in FFs has experienced remarkable growth over the last 10 years, since half the documents in our data set were published between 2010 and 2020, as shown in . One of the main objectives of our research is to provide a clear picture of the current research and the journals that have published the highest number of articles on CSR in FFs.

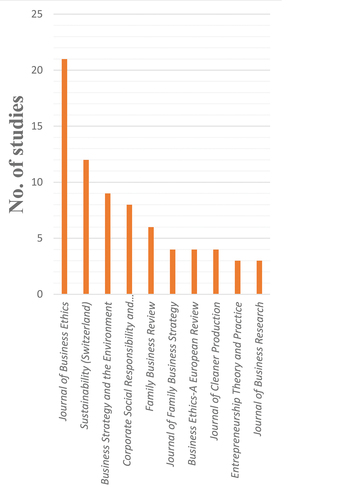

The data set extracted from WOS shows that a total 134 relevant academic studies were published in 59 different journals until 2020. The journals that published the most studies are the Journal of Business Ethics (21 studies), Sustainability (12 studies), and Business Strategy and the Environment (9 studies), as shown in . Among the 305 authors, the most active are: Martínez-Ferrero, J. (with eight articles), Rodríguez-Ariza, L. (with seven articles), García-Sánchez, I.-M. (with six articles), Gottardo, P., Block, J., Wagner, M., Gavana, G., and Moisello, A.M. (with four articles each), and Campopiano, G., Cuadrado-Ballesteros, B., and De Massis, A. (with three articles each).

Figure 5. Top 10 publishing journals from the WOS data set.

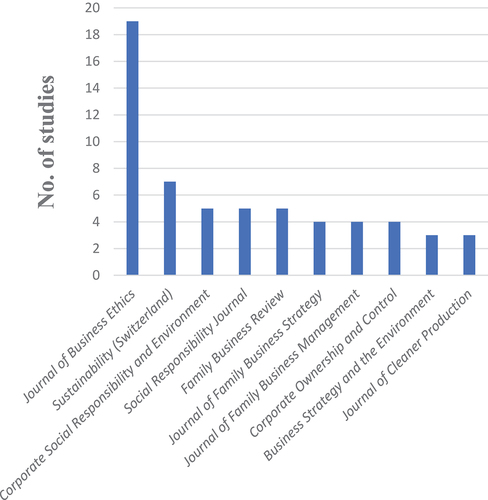

The data set extracted from Scopus shows that a total 121 studies were published in 61 different journals until 2020. Among the articles, 19 studies were published in the Journal of Business Ethics, seven in Sustainability, five in Family Business Review and in Corporate Social Responsibility and Environmental Management, as shown in . Among the 272 authors identified, Martínez-Ferrero J published six articles, while Rodríguez-Ariza L., Lin F., and García-Sánchez I.-M published four articles each, and Campopiano G., García-Meca E., López-González E., Wagner M., and De Massis A. published three articles each.

Figure 6. Top 10 publishing journals from the Scopus data set.

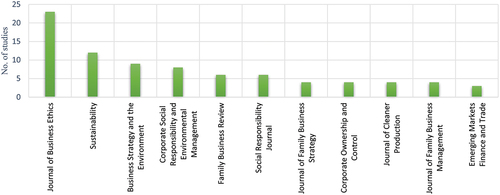

After merging the WOS and Scopus data sets, and deleting the duplicates we came up with a merged sample of 168 studies. Among the 168 selected studies, (23) were published in the Journal of Business Ethics, (12) in Sustainability, (nine) in Business Strategy and the Environment, (eight) in Corporate Social Responsibility and Environmental Management, (six) in Family Business Review and Social Responsibility Journal, (four) were published in each Journal of Family Business Management, Journal of Cleaner Production, Journal of Family Business Strategy, and Corporate Ownership and Control. These journals are illustrated in .

Figure 7. Top 10 publishing journals from the merged (Scopus + WOS) data set.

According to our analysis, the most active authors in the merged data set are: Martínez-Ferrero, J. (with eight articles), Rodríguez-Ariza, L. (with seven articles), and García-Sánchez, I.-M. (with six articles).

Our analysis includes both conceptual and empirical work. Based on bibliographic coupling, in what follows we cluster the studies based on the drivers and outcomes of CSR activities.

Bibliographic coupling

We then analyzed the most cited papers in the FF CSR literature in both data sets: 134 from WOS and 121 from Scopus. The top 20 most cited articles are illustrated in . The table is organized from the most cited to the least cited papers. The first column shows the ranking of the article in both data sets, columns two-to-five show the data extracted from WOS, and columns six-to-nine the data extracted from Scopus. The work of Dyer & Whetten (Citation2006) is ranked as the most cited paper, with a total of 425 citations in WOS and 473 in Scopus at the time of data retrieval (that is, January 2021). It is worth noting that the order and number of citations of papers differ in each data set.

Table 1. Top 20 most cited studies in WOS and Scopus.

Recurrent topics

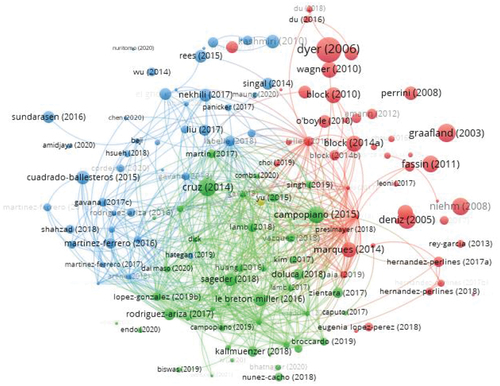

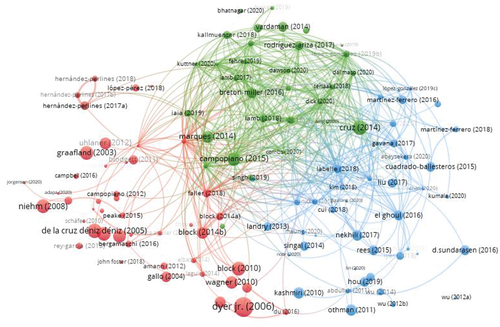

Adopting a bibliographic coupling network analysis using the VOSviewer software, we present the graphical representations () for each database. We followed Van Eck & Waltman (Citation2009) recommendation to create a visualization map, which presents many colored dots, each indicating an article. The size of each dot represents the density of citations, the colors represent the theme of the clusters, and the lines between dots the linkages between articles. The clusters’ themes were identified based on a frequency analysis carried out by the software, and subsequently named by the authors according to the main theme covered by the documents belonging to the same cluster.

Figure 8. Bibliographic coupling network visualization of WOS articles stemming from the analysis.

Figure 9. Bibliographic coupling network visualization of Scopus articles stemming from the analysis.

The bibliographic coupling analysis of the WOS outputs using a network visualization map shows that the literature on CSR in FFs focuses mainly on three themes. Hence, the three colors in the map each refer to a theme. The most frequently occurring theme is family involvement, which includes 46 articles (in red in ). The topic appears in many different studies addressing family ownership, family control, family influence, and FF structure. The corporate governance theme is the second largest group and includes 45 articles (in blue in ). The topic appears in various different studies focusing on the role of independent directors and family mangers. The sustainability theme features in 42 articles (in green in ) and appears in many diverse studies focusing on the sustainability practices in FFs.

The bibliographic coupling analysis of the Scopus outputs using a network visualization map shows that the FF CRS literature focuses mainly on three themes. Hence, the three colors in the map each refer to a theme. The most frequently occurring theme is family involvement in 47 articles (in red in ) addressing family ownership and family control. The theme of corporate governance is the second largest group and includes 40 studies (in blue in ) examining the impact of family members on boards. The sustainability theme features in 31 articles (in green in ).

Interestingly, the themes identified by running the bibliographic coupling analysis across the WOS and Scopus data set are largely consistent. This cross-database comparison, working also as a robustness check for our bibliographic coupling analysis, reveals that family involvement, corporate governance and sustainability are the three topical areas where a critical mass of research has been produced. SEW, ethics/religion, and entrepreneurial orientation are topics often examined in conjunction with one or more of the three major topics indicated (that is, family involvement, corporate governance, and sustainability). Moreover, some studies cover more than one theme: for instance, some on family involvement also appear to examine marginally corporate governance aspects.

The results of the bibliographic coupling analysis from both databases (WOS and Scopus) provide a clear picture in terms of the most active authors, topics, relevant journals, and the most cited documents relevant to CSR in FFs.

Family vs non-family firms

Based on our analysis of the reviewed articles, several studies in the CSR and FF literature have compared the performance of family and nonFFs in relation to their CSR engagement (Campopiano et al., Citation2019; Gavana et al., Citation2017a, Citation2017b, Citation2018; Kim et al., Citation2017; López-Pérez et al., Citation2018; Maung et al., Citation2020; Nekhili et al., Citation2017). Research on the spread of social responsibility in FFs has focused on differences in terms of CSR among family and non-FFs (Bergamaschi & Randerson, Citation2016), addressing FFs with regard to their different CSR approach.

In a recent study, García‐Sánchez et al. (Citation2020) examine an international sample of 956 listed firms and show that FFs show a higher level of CSR performance compared to non-FFs. Abeysekera & Fernando (Citation2020) analyze firms in the US and observe that FFs are more responsible to shareholders than non-FFs in engaging in environmental investments. In the US context, Madden et al. (Citation2020) draw on socioemotional selectivity theory to examine the differences between FFs and non-FFs in engaging with CSR activities, and show that FFs are more likely to invest in CSR than non-FFs. Rubino & Napoli (Citation2020) examine the impact of ownership structure and board of directors on corporate environmental performance (CEP) and find that Italian FFs have better environmental performance compared to non-FFs. Sharma et al. (Citation2020) analyze the linkage between CSR disclosure and firm value in 245 Indian firms, showing that FFs make higher CSR disclosure than non-FFs. Esparza Aguilar & Reyes Fong (Citation2019) suggest that FFs are more engaged with CSR practices than non-FFs. In the US, Dyer & Whetten (Citation2006) compare the degree to which family and non-FFs are socially responsible. The authors build their argument on organizational identity. The findings, based on a sample of 261 family and non-FFs, show that FFs are more socially responsible compared to non-FFs. Furthermore, Kashmiri & Mahajan (Citation2014b) emphasize that FFs are likely to maintain high levels of corporate social performance during recessions compared to non-FFs. Building on institutional theory, Kim et al. (Citation2017) indicate that FFs positively moderate the link between the top management team’s consideration of natural environmental concerns and proactive environmental actions. In contrast, non-FFs show few active environmental actions as their consideration of environmental concerns increases. Campopiano & De Massis (Citation2015) adopt institutional theory and a content analysis to analyze the CSR reports of familyowned and non-familyowned firms. A total of 40 out of 168 articles compare the performance of FF vis-à-vis non-FF in terms of firms’ engagement in CSR. Our analysis shows that 15 out of 40 studies reveal that family firms are more socially responsible than non-FFs. In the following section, we address the drivers of CSR adoption in FFs.

Drivers of CSR adoption in family firms

The findings indicate that firm features, family involvement, corporate governance, ethics and religion, and SEW motivate FFs to engage in CSR practices.

1) Firm Features

Based on our analysis, we identify that firm features, such as firm size (Huang et al., Citation2016) and firm's name (Kashmiri & Mahajan, Citation2010), influence FF engagement in CSR practices.

Regarding firm size, a recent study conducted in Mexico by Esparza Aguilar & Reyes Fong (Citation2019) indicates that CSR engagement is higher for large size FFs. In Italy, a study conducted by Gavana et al. (Citation2017b) indicates that a firm’s visibility in terms of size influences significantly CSR practices, and that the impact is higher for FFs than non-FFs. In Italy, Campopiano & De Massis (Citation2015) argue that the research stream examining the relationship between FF and CSR has focused on firm characteristics and contextual factors. Huang et al. (Citation2016) adopt resource-based and behavioral theories to explore the effect of family influence and the firm’s internal factors in the adoption of green product innovations. Their findings indicate that firm size positively affects the adoption of green product innovations. In the Netherlands, based on small- and medium-sized enterprises, Uhlaner et al. (Citation2012) find that firm size motivates FFs to engage in selected environmental practices. Using the US as their empirical setting, Niehm et al. (Citation2008) show that firm size is significantly correlated with an FFs ability to provide and obtain community support. Graafland et al. (Citation2003) find that firm size positively influences the use of several instruments and tools, such as social reporting. In Morocco, Elbaz & Laguir (Citation2014) develop an argument building on stakeholder, legitimacy, and stewardship theories to address the link between family structure, financial performance, and CSR orientation. Their findings, based on 50 FFs in the food and tourism industries, indicate that family structure positively affects CSR orientation.

As for firm name, Kashmiri & Mahajan (Citation2014a) emphasize that the family name is positively related with product-related trustworthy behavior. In the US, Mullens (Citation2018) shows that the level of entrepreneurial orientation is an important antecedent of social and environmental practices. Building on stakeholder and institution theories to explore the impact of internationalization on corporate philanthropy, Du et al. (Citation2018) analyze Chinese firms, showing that internationalization is positively related to corporate philanthropy. In Italy, Arena & Michelon (Citation2018) emphasize that the family name drives an increase in environmental disclosure.

2) Family Involvement

The relationship between family involvement and CSR is well researched in the FF literature. Building on stewardship and SEW theories, Marques et al. (Citation2014) address the heterogeneity of 12 Spanish FFs and their engagement in CSR practices. The findings reveal that a high level of family involvement is a driver of high CSR engagement. Building on agency and SEW theories, Labelle et al. (Citation2018) examine the relationship between family control and corporate social performance (CSP) in FFs and non-FFs, suggesting that when the family’s control increases, CSP also increases. Based on 146 publications, Faller & zu Knyphausen-Aufseß (Citation2018) emphasize that the level of equity ownership concentration influences a firm’s CSR commitment. J. H. Block & Wagner (Citation2014a), building on organizational identity and family identity theories, study 286 FFs and show that family ownership is negatively correlated with community-oriented CSR performance, but positively correlated with diversity, employee, environment, and product-oriented dimensions of CSR.

In Germany, Fehre & Weber (Citation2019) build on SEW theory to examine the relationship between family ownership and CSR activities, indicating that FFs ownership positively effects CSR activities. Ye and Li (Citation2021) investigate the impact of family involvement on internal and external CSR for 2,114 Chinese listed firms and show that family involvement is positively correlated to external CSR. In India, Cordeiro et al. (Citation2018) build on neo-institutional theory to analyze the impact of ownership type on CSR, and reveal that multinational ownership, family control and management can be considered as driving factors to CSR. In the US, Cordeiro et al. (Citation2020) draw on resource dependency, SEW and secondary agency theories to examine the impact of ownership structure and board gender diversity on CEP, revealing a positive relationship between ownership structure and CEP. Britzelmaier et al. (Citation2015) address the motivations for CSR in small FFs. Their findings, based on five FFs in southwest Germany, indicate that owner families have a strong influence on the CSR approach. Building on SEW theory, Bansal et al. (Citation2018) examine an international sample of 1,072 firms, indicating that family involvement in ownership increases the likelihood of CSR disclosure. In the US, building on regulatory focus theory and based on 71 public FFs, Lamb et al. (Citation2017) show that the higher the percentage of family owners’ equity, the higher the diversity-oriented CSR concerns. Building on stewardship, SEW, and agency theories, Lamb and Butler (Citation2018) study firms in the US and reveal that the greater the percentage of familyowned equity, the higher the increase in CSR strengths. Building on agency theory and examining an international sample of firms, Martínez-Ferrero et al. (Citation2016) suggest that family ownership positively affects the promotion of socially responsible practices.

3) Corporate Governance

Some studies in our data set examine corporate governance aspects and issues, such as the involvement of family members on boards as CEOs, and how this affects their decision to engage in CSR practices. In Japan, Endo (Citation2020) builds on stakeholder theory to examine the impact of board size on CEP and shows that the relationship is positive. In Europe, Meier & Schier (Citation2020) draw on stakeholder theory to examine the impact of different types of CEOs and their impact of internal and external CSR, thus revealing that family CEOs are positively related to both internal and external CSR practices. In an international study conducted by López-González et al. (Citation2019), the authors build on SEW theory and find that CSR engagement is greater when family members are present in the management team and family directors are on the board of directors. Building on behavioral agency theory, Cui et al. (Citation2018) examine 177 US FFs and find that a family CEO enhances the influence of family ownership on the firm’s CSR performance. Building on stakeholder and agency theories, Cuadrado-Ballesteros et al. (Citation2015) analyze an international sample and reveal that the higher the proportion of independent directors, the higher the level of CSR reporting disclosure.

In France, Laguir & Elbaz (Citation2014) indicate that FFs managed by competent external CEOs show better social performance than those managed by family CEOs. In Italy, building on institutional and agency theories, Gavana et al. (Citation2017a) show that a family CEO improves CSR disclosure. Drawing on SEW theory, J. Block & Wagner (Citation2014b) analyze 399 FFs and find that the presence of a family founder as CEO is associated with fewer CSR concerns. Building on stakeholder, legitimacy, and agency theories, Rudyanto & Siregar (Citation2018) examine 123 Indonesian FFs and find that the board of commissioner efficiency positively affects the quality of sustainability reports. Building on stakeholder, legitimacy, and SEW theories, Gavana et al. (Citation2016) examine 230 firms and reveal that family CEOs have a significant positive effect, specifically on environment and labor disclosure. Dick et al. (Citation2020) build on stakeholder theory to examine the impact of founder-controlled family firms and managerial overconfidence on CSR of 343 medium-sized Polish FFs: they reveal that overconfident executives show higher CSR performance.

The presence of women directors is examined by Sundarasen et al. (Citation2016) analyzing 450 nonexecutive directors and independent nonexecutive directors, revealing a positive relationship between female representation on the board and CSR engagement. In Italy, Campopiano et al. (Citation2019), draw on self-construal theory to examine the impact of presence of female directors on CSR practices, thus showing that female directors are positively related to CSR activities. In the US, Cordeiro et al. (Citation2020) indicate that board diversity influences positively CEP.

4) Socioemotional Wealth

Many recent studies illustrating the ways that FFs differ from other firms in making decisions focus on the role of SEW, defined as the “non-financial aspects of the firms that meet the family’s affective needs” (Gómez-Mejía et al., Citation2007, p. 106). Management and entrepreneurship scholars are paying increasing attention to SEW as a developing perspective in the FF literature. Lamb & Butler (Citation2018) emphasize that FFs are particularly interested in SEW as conducive to adopting CSR practices. Labelle et al. (Citation2018) argue that FFs make CSR investments to balance SEW preservation and financial performance. Yu et al. (Citation2015) evaluate the CSR performance of family and non-FFs in Taiwan. In the US, building on SEW and organizational identity theories, J. H. Block & Wagner (Citation2014a) examine 286 firms and reveal that FFs care about their SEW, which in turn leads to a high relevance of CSR. Moreover, Kallmuenzer et al. (Citation2018) analyze 152 Austrian firms and show that SEW enhances CSR activities for FFs in the rural tourism industry. Vazquez (Citation2018) systematically analyzes 31 articles and indicates that SEW is considered one of the characteristics allowing FFs to adopt CSR practices.

5) Ethics and Religion

Scholars have investigated the impact of ethical behavior on CSR practices. In Belgium, Fassin et al. (Citation2011) examine 226 small FFs and show that managers understand the interrelationships and interdependencies of business ethics concepts. Building on stewardship theory, Déniz & Suárez (Citation2005) illustrate that CSR practices are based on ethical and cultural factors. Among 112 Spanish CEOs, Schäfer & Goldschmidt (Citation2010) examine the motives for CSR engagement in large German FFs. Their findings indicate that the ethical motive dimension is a significant predictor of the overall success of CSR engagement. Based on 10 semi-structured interviews, Perrini & Minoja (Citation2008) indicate that the beliefs and value systems of entrepreneurs play an important role in determining a sustainable corporate strategy. In their multicountry study, including the UK, US, Thailand, and Malaysia, Feliu & Botero (Citation2016) reveal that one of the motivations of philanthropy in the family business is moral. The authors identify several philanthropic practices, such as planned donations, multiple levels of charitable trusts, and public community foundations. Chou et al. (Citation2016) reveal that Buddhism has led to several external and internal stakeholder CSR initiatives. Bhatnagar et al. (Citation2019) based on 14 case studies of Indian Hindu business families, indicate that spiritual beliefs and values are a driving factor for philanthropic practices.

Having presented the findings from the literature, we identify the drivers of CSR adoption in FFs as firm features, family involvement, corporate governance, ethics and religion, and SEW, as shown in .

Figure 10. Drivers of CSR in FFs.

In the following section, we provide an analysis of the outcomes of CSR adoption in FFs.

Outcomes of CSR adoption in family firms

The findings of our analysis – based on a triangulation of bibliometric methods and in-depth reading of the articles – indicate that financial performance, reputation, innovation, and sustainability are the most recurrent outcomes of CSR adoption in FFs.

1) Firm Performance

Four studies investigate the impact of CSR on firms’ value. For instance, Noor et al. (Citation2020) build on stakeholder theory to analyze the relationship between CSR and firm value and show that the relationship is positive. Nirmala et al. (Citation2020) examine the impact of CSR on Indonesian firms’ values, detecting a positive association. Nekhili et al. (Citation2017) examine the moderating role of family involvement on the relationship between CSR and firm market value, finding a positive relationship between CSR disclosure and FF market-based financial performance. In Korea, Choi et al. (Citation2019) draw on stakeholder theory to examine the impact of CSR on firm value, and detect a positive relation between CSR and firm’s value measured by Tobin’s Q.

Five studies examine the impact of CSR on firm performance. In Poland, Randolph et al. (Citation2019) investigate the impact of family objectives and community objectives on firm performance and show a significantly positive relationship. In Mexico, Hernández-Perlines & Ibarra Cisneros (Citation2017) analyze 140 small FFs and find that entrepreneurial orientation plays a positive moderator role on the effect of social responsibility on FFs performance. Drawing on stakeholder theory and examining 174 Spanish FFs, Hernández-Perlines & Rung-Hoch (Citation2017) address the relationship between entrepreneurial orientation and firm performance, revealing that entrepreneurial orientation is a good predictor of the success of FFs, and positively influences their performance.

Ten studies examine the impact of CSR on firms’ financial performance. Drawing on stewardship and SEW theories to study the impact of sustainability on both financial and nonfinancial factors, López-Pérez et al. (Citation2018) examine SMEs context located in Spain and show that sustainability positively effects firms’ corporate reputation, brand image, and financial value. In a study carried out in Taiwan, S. Wu et al. (Citation2012a) examine 192 firms, showing that CSR has a positive relationship with financial performance and earnings quality. Singal (Citation2014), based on 580 firms and drawing on slack resources and instrumental theories, reveals that a FF’s investment in CSR generates positive effects on its future financial performance; Niehm et al. (Citation2008) find that commitment to the community significantly explains perceived family business performance, while community support explains financial performance in FFs. Building on legitimacy, stakeholder, and SEW theories, Gavana et al. (Citation2018) find that CSR reporting has a significant effect on revenues when a firm is characterized by consumer proximity. Drawing on social identity theory, Kashmiri & Mahajan (Citation2014a) examine 107 FFs and find that family name is related to higher stock returns and more ethical product-related behavior. C. Wu et al. (Citation2012b) study 125 firms in the high-tech industry and reveal that the relationship between CSP and the cost of capital is negative in FFs. Building on stakeholder and SEW theories, Shahzad et al. (Citation2018) study 190 FFs in Pakistan and reveal that the effect of CSR performance on investment efficiency is high in FFs.

2) Reputation

Family members recognize that their reputation and image are closely identified with the firm’s, as it often carries their name (Dyer & Whetten, Citation2006). Building on stakeholder theory, Uhlaner et al. (Citation2004) find that FFs have a sense of responsibility for workers and the local community: long-term relations and family values increase reputation. In the US, Dyer & Whetten (Citation2006) analyze 202 non-family and 59 FFs and find that FFs tend to be more socially responsible than non-FFs due to family concern about image and reputation, as well as the desire to protect family assets. Building on stakeholder theory, Cruz et al. (Citation2014) emphasize that FFs are socially responsible toward external stakeholders to maintain their firm’s reputation and image. Sageder et al. (Citation2018) adopt a systematic review of FF image and reputation, and one of the studies they reviewed (Fernando & Almeida, Citation2012), finds that CSR initiatives enhance a firm’s reputation as a responsible employer, fostering performance and business opportunities. Moreover, building on stewardship theory, Déniz & Suárez (Citation2005) analyze 112 Spanish FFs and find that CSR practices improve firm image.

3) Innovation

Wagner (Citation2010), in a study conducted in the US, analyzes 3,697 large FFs and finds a link between innovation with high social benefits and CSP. Interestingly, innovation is rarely measured as a dependent variable (except for Wagner, Citation2010): rather, it seems only to appear as a control variable in most of the studies measuring performance. For instance, Kashmiri and Mahajan (Citation2014b) find that FFs outperform non-FFs during recessions because they keep high levels of new product introductions and advertising intensity (however, performance is not measured in terms of innovation).

4) Sustainability

Building on behavioral theory, Foster (Citation2018) observes the impact of philanthropy on firm performance in the UK, US, Thailand, and Malaysia. The results, based on seven case studies, show that social responsibility helps long-term sustainability, especially in a modern business environment. In the US, Niehm et al. (Citation2008) show that CSR dimensions contribute to FF sustainability in small rural communities.

In sum, financial performance, lower cost of capital, reputation, innovation, and sustainability are the outcomes of CSR adoption in FFs, as shown in .

Figure 11. Outcomes of CSR adoption in FFs.

We present the results of the SLR analysis in a comprehensive framework in . The findings illustrate that firm features, family involvement, corporate governance, ethics and religion, and SEW are drivers of CSR practices in FFs, while the outcomes are financial performance, reputation, innovation, and sustainability.

Figure 12. SLR outcomes based on adopted framework.

In the following section, we provide a discussion of the matrix analysis of the variables, theories, methods, and empirical settings adopted for each CSR driver and outcome in FFs.

Discussion

This paper is motivated by the significance of FFs in the global economy and their growth (De Massis et al., Citation2018a). As the following section will show, the number of studies addressing CSR in FFs has increased over time, albeit lacking a comprehensive SLR. In the next section, we provide a discussion of the most relevant and frequently researched topics and aspects of CSR in FFs. Then, we discuss the constructs adopted for drivers v outcomes, and summarize these in .

Table 2. Matrix analysis of the drivers of CSR adoption in FFs.

Table 3. Matrix analysis of the outcomes of CSR adoption in FFs.

FF CSR topics and aspects

The findings of the bibliographic coupling analysis indicate that family involvement, sustainability, corporate governance, SEW, religion and ethics, and entrepreneurial orientation are the most studied topics and aspects in the CSR in FF literature. Some studies compare family and non-FFs with regard to their CSR practices. The most dominant topic in the FF CSR literature is family involvement, measured through family ownership structure (J. Block & Wagner, Citation2014b, Citation2014b; Cordeiro et al., Citation2020; Du et al., Citation2018; Faller & zu Knyphausen-Aufseß, Citation2018; Rees & Rodionova, Citation2015), family involvement in the board (Gavana et al., Citation2016; Lamb & Butler, Citation2018; López-González et al., Citation2019), family control (Labelle et al., Citation2018), and used to examine the impact of CSR on financial performance (Elbaz & Laguir, Citation2014; Liu et al., Citation2017; López-Pérez et al., Citation2018). Some articles measure the impact of family involvement on a specific aspect of CSR, such as CSR concerns (J. Block & Wagner, Citation2014b; Lamb et al., Citation2017), sustainability reports (Gavana et al., Citation2016), CSR disclosure (Cuadrado-Ballesteros et al., Citation2015), CSR community relations (J. H. Block & Wagner, Citation2014a), CSR performance (Labelle et al., Citation2018), and the impact of family ownership and control on the adoption of green products (Huang et al., Citation2016).

The second dominant topic is corporate governance addressed through identifying the impact of family members on the board or as CEOs in making decisions to engage in CSR practices (Bansal et al., Citation2018; Laguir & Elbaz, Citation2014; López-Pérez et al., Citation2018), gender of directors (Campopiano et al., Citation2019; Cordeiro et al., Citation2020; Peake et al., Citation2017), the CEO’s political participation (Du et al., Citation2018), and independent directors (Cuadrado-Ballesteros et al., Citation2015). Some of the studies examine the impact of corporate governance on sustainability reports (Martínez-Ferrero et al., Citation2017), CSR disclosure (Bansal et al., Citation2018), and CSR internal and external factors (Meier & Schier, Citation2020; Rodríguez‐Ariza et al., Citation2017).

Sustainability is another topic that emerged from the literature review, identified and measured through CSR practices (Iyer & Lulseged, Citation2013; Niehm et al., Citation2008), sustainability disclosure (Gavana et al., Citation2017a), sustainability reports (Rudyanto & Siregar, Citation2018), and sustainability certifications (Richards et al., Citation2017).

Ethics and religion are examined in the literature by measuring the product-related ethical behavior of FFs (Kashmiri & Mahajan, Citation2014a). the effect of core Buddhism values (Chou et al., Citation2016), and spiritual beliefs and values (Bhatnagar et al., Citation2019).

Socioemotional wealth is another topic addressed. Vazquez (Citation2018) indicates that three key features in FFs increase ethical behavior, one of which is SEW measured through majority ownership and family control (Yu et al., Citation2015).

Entrepreneurial orientation is the last topic discussed and measured in three dimensions: innovation, proactivity, and risk-taking (Hernández-Perlines & Ibarra Cisneros, Citation2017).

Constructs adopted as drivers

Our findings indicate that firm features, family involvement, corporate governance, ethics and religion, and SEW are the key drivers of CSR in FFs. The findings are summarized in providing a matrix that analyzes the variables, theories, methods, and empirical settings of the drivers of CSR adoption in FFs.

1) Firm Features

Level of entrepreneurial orientation. Drawing on stewardship, agency, and stakeholder theories, Mullens (Citation2018) investigates the relationship between entrepreneurial orientation and investments in sustainability initiatives in the US.

Firm size. Esparza Aguilar and Reyes Fong (Citation2019) draw on stakeholder theory to analyze the impact of gender, size, and university education on CSR in Mexico. Gavana et al. (Citation2017b) build on institutional and signaling theories, addressing earnings management and CSR disclosure in Italy. Graafland et al. (Citation2003) analyze the relationship between CSR and strategy in FFs in the Netherlands. Uhlaner et al. (Citation2012) build on planned behavior theory and investigate the relationship between firm size and environmental management practices in the Netherlands. Niehm et al. (Citation2008) draw on enlightened self-interest and social capital theories and examine the relationship between total number of employees and CSR dimensions in the US.

Firm name. Kashmiri & Mahajan (Citation2014a) draw on social identity theory and analyze the relationship between family name presence and product-related ethical behavior in the US. Zeng (Citation2020) draws on SEW theory to assess the impact of CSR activities in Canada.

FF structure. Campopiano and De Massis (Citation2015) address the relationship between FFs vs non-FFs and CSR reporting in Italy, building on institutional theory.

Internationalization. Building on stakeholder and institutional theories, Du et al. (Citation2018) investigate the relationship between internationalization and corporate philanthropy in China.

In sum, firm features have been examined through identifying their influence on CSR adoption. Some studies use both qualitative and quantitative methods across various countries. The arguments on this topic mostly draw on stakeholder, institutional, and stewardship theories.

2) Ethics and Religion

Business ethics. Fassin et al. (Citation2011) investigate the awareness of small-business owners and managers regarding CSR and business ethics in Belgium, building on stakeholder theory. Schäfer & Goldschmidt (Citation2010) examine the motives of CSR engagement for FFs in Germany, building on institutional theory. Déniz & Suárez (Citation2005) examine FF orientation and four CSR approaches in Spain, drawing on stewardship theory.

Philanthropy. Foster (Citation2018) observes philanthropy motivation in the UK, US, Thailand, and Malaysia. Feliu & Botero (Citation2016) adopt a systematic review of the FF philanthropy literature. Bhatnagar et al. (Citation2019) show that spirituality represents an antecedent of philanthropic practices in India.

Religion. Chou et al. (Citation2016) examine the core values of Buddhism and CSR in Thailand. Perrini & Minoja (Citation2008) address corporate strategy and CSR in Italy, building on institutional theory and qualitative analysis.

In sum, the impact of religion and ethics has been examined through FF moral motivations to adopt CSR predominantly through qualitative methods across various countries. The arguments on this topic mostly draw on stakeholder, institutional, and stewardship theories.

3) Family Involvement

Family ownership. Fehre and Weber (Citation2019) draw on SEW theory to investigate the impact of family ownership on CSR in Germany. Ye and Li (Citation2021) build on stakeholder theory to examine the relationship between family ownership and CSR in China. Venturelli et al., Citation2021) adopt SEW theory to assess the relationship between family ownership and CSR in Italy. Cordeiro et al. (Citation2020) draw on resource dependency, SEW and agency theories to examine the relationship between ownership structure and board gender diversity and CEP. Dawson et al. (Citation2020) adopt signaling theory to examine the impact of family involvement in management and generational stage on CSR in Italy. J. H. Block and Wagner (Citation2014a) examine family ownership and CSR in the US, building on SEW and organizational identity theories. Lamb & Butler (Citation2018) examine the relation between family owners and CSR concerns and strength in the US, drawing on stewardship, SEW, and agency theories. Marques et al. (Citation2014) draw on SEW and stewardship theories to address the relationship between family involvement and CSR in Spain. Martínez-Ferrero et al. (Citation2016) explore the relationship between managerial discretion and CSR practices based on agency theory. Bansal et al. (Citation2018) draw on agency and SEW theories to examine the relationship between family control and CSP.

In sum, family involvement has been measured through identifying the impact of family involvement in ownership or control on CSR practices relying on qualitative and quantitative methods across a number of countries. The arguments on this topic mostly draw on agency and SEW theories.

4) Corporate Governance

Rubino & Napoli (Citation2020) build on agency theory to examine the relationship between board independence and environmentally responsible practices in Italy. In Japan, Endo (Citation2020) builds on stakeholder theory to examine the impact of board compensation and corporate environment. Dick et al. (Citation2020) draw on stakeholder theory to analysis the impact of founder-controlled family firms and managerial overconfidence on CSR in Poland. Bansal et al. (Citation2018) draw on agency and SEW theories to examine the relationship between family control and CSP.

Gender of directors. Campopiano et al. (Citation2019) build on self-construal theory to analyze the influence of family women on the board on CSR in Italy. Cordeiro et al. (Citation2020) draw on resource dependency, SEW and agency theories to examine the relationship between gender diversity and CEP in the US. Based on an international sample and social role theory, Rodríguez‐Ariza et al. (Citation2017) identify the relationship between the role of females on boards and CSR.

External CEO. Laguir & Elbaz (Citation2014) examine the impact of external CEOs on CSR in France, drawing on stakeholder, legitimacy, and stewardship theories. Cuadrado-Ballesteros et al. (Citation2015) examine the relationship between family ownership and CSR disclosure, building on stakeholder and agency theories.

Family CEO. López-González et al. (Citation2019) analyze the relationship between FFs and CSR performance building on SEW. J. Block and Wagner (Citation2014b) examine the relationship between family CEO and CSR concerns in the US, building on SEW theory. Lamb & Butler (Citation2018) examine the relationship between family CEO and CSR strength and concerns in the US, building on stewardship, SEW, and agency theories. Gavana et al. (Citation2017a) examine the effect of equity and bond issues on sustainability disclosure in Italy, drawing on institutional, agency, and SEW theories. Cui et al. (Citation2018) address the relation between family involvement and CSR performance in the US, building on behavioral agency theory.

In sum, corporate governance factors have been examined by identifying the impact of family members on boards or CEOs on adopting CSR practices, measured through quantitative methods in various countries. The arguments on this topic mostly draw on agency, stakeholder, and SEW theories.

5) SEW

Yu et al. (Citation2015) examine SEW by measuring majority ownership and CSR performance in Taiwan, building on agency and SEW theories in a quantitative analysis. J. H. Block and Wagner (Citation2014a) examine family ownership and CSR in the US, building on SEW and organizational identity theories. Vazquez (Citation2018) draws on a systematic approach to analyze the differences between FFs and non-FFs regarding business ethics. Lamb and Butler (Citation2018) examine the relationship between family CEOs and CSR strength and concerns in the US, building on stewardship, SEW, and agency theories. Labelle et al. (Citation2018) examine the CSP adoption in FFs in multicountry, building on agency and SEW theories.

In sum, SEW factors have been examined through identifying the impact of family ownership or control in FFs measured through qualitative and quantitative studies in various countries. The arguments on this topic mostly draw on agency and SEW theories. Izzo and Ciaburri (Citation2018) examine the relationship between the role of SEW and CSR engagement and practices in FFs in Italy.

Constructs adopted as outcomes

Our findings indicate that the outcomes of CSR adoption in FFs are financial performance (including cost of capital), reputation, innovation, and sustainability, as summarized in providing a matrix that analyzes the outcomes and variables, theories, methods, and empirical settings adopted for each CSR outcome in FFs.

1) Firm Performance

As far as financial performance is concerned, several studies are worth mentioning. Nirmala et al. (Citation2020) examine the impact of CSR disclosure on firms’ value in Indonesia. In Korea, Choi et al. (Citation2019) draw on stakeholder theory to examine the relationship between CSR and firm value. Noor et al. (Citation2020) build on stakeholder theory to examine the impact of CSR on a firm’s value in Brazil, Russia, India, and China. López-Pérez et al. (Citation2018) build on stewardship and SEW to examine the relationship between CSR and both financial and nonfinancial (that is, image and reputation) performance in Spain. S. Wu et al. (Citation2012a) examine the impact of cost of capital and earnings quality on CSR awards in Taiwan. S. W. Wu et al. (Citation2014) and C. Wu et al. (Citation2012b) examine the impact of CSP on the cost of capital in Taiwan. Elbaz and Laguir (Citation2014) draw on stakeholder, legitimacy, and stewardship to analyze the relationship between CSR and financial performance in Morocco. Gavana et al. (Citation2018) draw on legitimacy, stakeholder, and SEW theories to analyze the impact of CSR reporting of a firm’s revenue in Italy.

In Poland, Randolph et al. (Citation2019) build on goal systems to investigate the impact of family objectives and community objectives on firm performance measured by means of comparing firms’ performance (firm’s strategic orientation, relative profitability, investments, and competitive position) with performance in the industry in which the firm operates. Drawing on stakeholder theory, Hernández-Perlines & Rung-Hoch (Citation2017) examine the impact of CSR on FF performance measured by average annual sales growth, average growth of the market share, average profit growth, and average growth of the return on capital in Mexico. Niehm et al. (Citation2008) draw on enlightened self-interest and social capital theories to analyze the impact of community support on a firm’s performance measured by reported gross annual income in the US.

In sum, performance (both financial and nonfinancial) has been examined through identifying the impact of CSR practices on firm performance and analyzed through quantitative methods in various countries. The arguments on this topic draw mainly on agency, stakeholder, and legitimacy theories.

2) Reputation

Dyer & Whetten (Citation2006) examine family ownership and CSP in the US. Uhlaner et al. (Citation2004) examine FF characteristics and CSR in Dutch firms, building on stakeholder theory. Cruz et al. (Citation2014) examine family control and social practices in Europe, building on stakeholder theory. Déniz & Suárez (Citation2005) address FF orientation and four approaches of CSR in Spain, drawing on stewardship theory.

3) Sustainability and Innovation

Wagner (Citation2010) examines the impact of CSP on innovation in the US, drawing on stewardship theory. Niehm et al. (Citation2008) examine the impact of community support to sustain FFs in the US, building on enlightened self-interest and social capital theories. Drawing on behavioral theory, Foster (Citation2018) observes the effect of philanthropy on firm long-term sustainability in the UK, US, Thailand, and Malaysia.

Theories adopted

Based on the inspection and reading of each work, and beyond the bibliometric mapping, the most adopted theoretical lenses in the literature on CSR in FFs are agency theory (Labelle et al., Citation2018; Rubino & Napoli, Citation2020), stakeholder theory (Dick et al., Citation2020; Hernández-Perlines & Rung-Hoch, Citation2017; Maggioni & Santangelo, Citation2017), stewardship theory (Lamb & Butler, Citation2018; Marques et al., Citation2014), legitimacy theory (Gavana et al., Citation2018), social identity theory (Kashmiri & Mahajan, Citation2010), and institutional theory (Amann et al., Citation2012; Kim et al., Citation2017). The theory most adopted to explain family business behavior and strategic actions is stakeholder theory, suggesting that firms can obtain benefits from being socially responsible toward their stakeholders (Aguilera & Jackson, Citation2003; Freeman & Reed, Citation1983). Agency theory argues that these firms will pursue their own interests at the expense of other stakeholders, since they own and manage the firm, and determine its strategies. The other main view is stewardship theory, which states that these firms will act in accordance with the interests of all stakeholders. In other words, agency and stakeholder theories provide some insights into understanding the mechanisms of FF CSR conduct, albeit ambiguous. Interesting to note is the different ways the theoretical lenses are adopted in the studies.

Methods adopted

As for the methodological approaches, out of the total 168 studies, 101 (60%) adopt a quantitative approach, 55 (32%) qualitative. The former is mostly adopted to examine the relationships between different variables based on questionnaires, the latter often focused on interviews (Fassin et al., Citation2011; Peake et al., Citation2015), questionnaires (Zhou, Citation2014), the case study approach (Iaia et al., Citation2019), and surveys (Britzelmaier et al., Citation2015). Among the quantitative articles, 46% adopt a cross-sectional approach (Chou et al., Citation2016; Kashmiri & Mahajan, Citation2014a), and seven percent adopt a longitudinal approach (Boissin et al., Citation2007; Kuttner et al., Citation2020).

In terms of level of analysis, eight percent adopt an institutional level (Faller & zu Knyphausen-Aufseß, Citation2018; Peake et al., Citation2015), 82% adopt a firm level (Du et al., Citation2018; Kashmiri & Mahajan, Citation2010) and five percent adopt an individual level (Kallmuenzer et al. Citation2018; Randolph et al., Citation2019).

Empirical settings

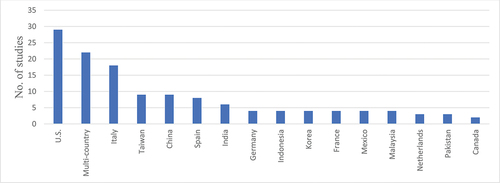

The literature on CSR in FFs focuses both on developed and emerging countries, as shown in . The empirical setting in 29 studies is the US (Cordeiro et al., Citation2020; Cui et al., Citation2018; Liu et al., Citation2017), 22 studies focused on multicountry contexts (Bansal et al., Citation2018; García‐Sánchez et al., Citation2020; Martínez-Ferrero et al., Citation2017), 18 are based in Italy (Gavana et al., Citation2017a, Citation2017b; Venturelli et al., Citation2021), nine in Taiwan (Huang et al., Citation2016), and China (Zhou, Citation2014), eight in Spain (Hernández-Perlines & Rung-Hoch, Citation2017)) and six in India (Bhatnagar et al., Citation2019; Cordeiro et al., Citation2018), four are based in Germany (Britzelmaier et al., Citation2015), Indonesia (Nirmala et al., Citation2020), Korea (Choi et al., Citation2019), Malaysia (Othman et al., Citation2011), and in France (Laguir & Elbaz, Citation2014; Nekhili et al., Citation2017), three are based in the Netherlands (Graafland et al., Citation2003), and Pakistan (Shahzad et al., Citation2018).

Figure 13. The empirical setting of reviewed studies.

The CSR behavior of FFs seems to differ across emerging and developed countries. In developed countries, CSR is typically aimed at addressing environmental, economic, and governance issues (Doluca et al., Citation2018; Fehre & Weber, Citation2019). Moreover, there is more emphasis on business ethics rather than religion (Déniz & Suárez, Citation2005; Schäfer & Goldschmidt, Citation2010). Since within most developing countries there is preoccupation on basic livelihood, it is more frequent for businesses to engage primarily in CSR that concentrates on a few areas: environment, safety, and human rights (Caputo et al., Citation2017; Lamb & Butler, Citation2018), economic performance and environmental preservation (Gavana et al., Citation2017b), community, employees, product quality management (López-Cózar Navarro et al., Citation2017), and environmental human rights, employees, and consumer protection (Rodríguez‐Ariza et al., Citation2017).

In contrast, the CSR behavior of FFs in emerging countries is more related to community and religious orientations. Accordingly, the leading motive for FFs engaging in CSR activities is normative in nature, that is belief or religious reasons (Chou et al., Citation2016; Singh & Mittal, Citation2019). Moreover, it seems that several firms in emerging countries pay attention to philanthropy (Abdelhalim & Eldin, Citation2019; Du et al., Citation2016, Citation2018; Ye & Li, Citation2021) rather than legal or ethical dimensions of CSR. This is driven largely by the desire to feel like they are part of the communities in which they operate, which is often critical to the overall identity of the firms and their employees in these countries.

Conceptualizations and measures of CSR

While our SLR has focused on CSR in family firms, we should acknowledge that CSR is an umbrella concept that entails multiple heterogeneous sub-concepts and constructs including CSR disclosure (Nekhili et al., Citation2017), environmental disclosure (Arena & Michelon, Citation2018), sustainability (Kallmuenzer et al., Citation2018), sustainability reporting (Hsueh, Citation2018), environmental performance (Endo, Citation2020), gender diversity (Peake et al., Citation2017), philanthropy (Du, Citation2015), business ethics (Fassin et al., Citation2011). Overall, the CSR conceptualization adopted in each study reflects the specific nuance of CSR that the author/s aim to illustrate, describe, and capture. The empirical setting seems to influence the conceptualization of CSR: for instance, in developed countries the concept of CSR is related to business stakeholders (for example, customers, suppliers) and entails a focus on reporting (Campopiano & De Massis, Citation2015), while in emerging countries it relates more to philanthropy, spirituality and religion (Bhatnagar et al., Citation2019). Furthermore, CSR has been conceptualized as internal when it involves stakeholders within the firm such as employees, and external when it involves stakeholders external to the firm such as customers, suppliers, governmental bodies, and so forth. Several recent studies look at both internal and external CSR (Meier & Schier, Citation2020).

As far as the measures of CSR are concerned, we note that the methods used to measure CSR are varied. The majority of studies measure CSR by using content analysis (Campopiano & De Massis, Citation2015), while other studies have adopted surveys (Graafland, Citation2020), reputation indices (Rodriguez-Ariza et al., Citation2016), and single case studies (Boissin et al., Citation2007). Moreover, some studies measure CSR based on scores or ratings of CSR dimensions within specific databases such as the Kinder, Lydenberg and Domini (KLD) Research & Analytics database (Kashmiri & Mahajan, Citation2014a, Citation2014b), while other studies measure it through surveys that capture both the internal (employee-related) and external (customers-, suppliers-, and local community-related) dimensions of CSR (Lindgreen et al., Citation2009). Interestingly, while in developed countries it is more likely that established databases are leveraged (Kashmiri & Mahajan, Citation2014a, Citation2014b), this is not the case in emerging countries where typically ad hoc surveys are conducted to build data sets.

Conclusions, contributions and future research

Corporate social responsibility in FFs is increasingly gaining the attention of management and entrepreneurship scholars, as the impressive growth in the number of studies on this topic clearly shows. However, the main objective of this review was to identify the topics and aspects of CSR in FFs, and the drivers and outcomes of CSR adoption in FFs. The bibliometric mapping identifies three major topical areas – namely family involvement, corporate governance, and sustainability. SEW, ethics/religion, and entrepreneurial orientation are minor topics often examined in conjunction with one or more of the three major topics. The findings of the SLR analysis reveal that firm features, family involvement, corporate governance, ethics and religion, and SEW are the key drivers of CSR. Conversely, the most recurring outcomes of FF CSR are financial performance, reputation, innovation, and sustainability. However, and interestingly, while there seems to be more consistency across the findings of papers investigating the drivers of CSR, research findings related to the outcomes display mixed evidence. This certainly provides an opportunity for further research, for instance, by means of meta-analyses.

Contributions

This work contributes to advance both the FF and CSR literature. First, we assessed the research field at the intersection of FFs and CSR by offering an updated overview of extant literature. This contributes to address recent calls for more research on CSR in family firms (Kuttner et al., Citation2020) and organize the growing body of research analyzing the role of CSR in FFs (Kuttner et al., Citation2020; De Massis et al., Citation2018a; Peake et al., Citation2015). Second, our findings suggest that there are three established topical areas that are informing developments in the research field at the intersection of FFs and CSR: family involvement (Dyer & Whetten, Citation2006), corporate governance (Campopiano et al., Citation2019), and sustainability (Niehm et al., Citation2008). Moreover, SEW, ethics/religion, and entrepreneurial orientation are further topics often examined in conjunction with one or more of the three major topics indicated (that is, family involvement, corporate governance, and sustainability). Interestingly, several studies cover more than one theme: for instance, some studies on family involvement also appear to examine marginally corporate governance aspects. This suggests that researchers are already working across topical areas which perhaps allows them to gain a more holistic view of what they are researching. Third and last, we have contributed to draw some guidelines for future scholarship (reported in the limitations and research section below), by developing a research agenda that will likely inform the future evolution of this research area in the next decade.

Practical implications

From a practical viewpoint, conducting a systematic literature review to map out the literature at the intersection of FFs and CSR could be potentially interesting for policymakers and practitioners. First, given the high proportion of FFs in any national economy (Le Breton-Miller & Miller, Citation2009; De Massis et al., Citation2018a) and the increasing trend of FFs engaging with CSR (Fehre & Weber, Citation2019), both policymakers and practitioners might derive insights from our work to document themselves on the challenges, issues, benefits, and opportunities for FF willing to engage with CSR. This might support opportunities’ evaluations and cost/benefit analysis before even embracing CSR practices. Second, as CSR is also becoming a trending topic in the rhetoric of policymakers and practitioners, we encourage them to engage with some recent studies (Fehre & Weber, Citation2019) that have critically pointed out that firms’ attention to CSR might be dependent on a number of factors including firm heterogeneity, as well as resources (Huang et al., Citation2016; Singal, Citation2014). Third, by indicating that there are a multitude of antecedents and drivers of CSR across different contexts, the knowledge generated by this SLR might assist policymakers and practitioners in identifying the most relevant reasons why CSR practices could or should be adopted differently in different contexts. Fourth, as there are mixed and inconsistent findings regarding the effect of CSR on firm performance (both financial and nonfinancial), practitioners interested in embracing CSR to enhance their firms’ performance might need to focus on those studies describing firms that operate in a similar national context and industry. Indeed, there does not seem to be any “one size fits all” type of CSR strategy leading consistently to enhanced performance. However, most studies suggest that embracing CSR practices yields reputational gains: therefore, firms could engage with CSR to enhance their reputation. Fifth and last, as CSR behaviors of FFs are different across developed vs emerging countries (Singh & Mittal, Citation2019; Ye & Li, Citation2021), policymakers in emerging countries will need to emphasize community- and religious-related outcomes if they want to persuade FFs to engage more with CSR practices.

Limitations and research agenda

This work has some limitations that could be addressed in future studies. First, our analysis is based on the systematization and bibliographic coupling of extant literature. We encourage scholars to adopt other advanced data science, text-mining, and machine learning tools such as topic modeling to discover the hidden semantic structure of the documents used in our literature review. Second, other sources such as Google Scholar might have been leveraged to derive additional scientific outputs that are neither indexed in Scopus nor in WOS. Third, while the VOSviewer package is certainly a good tool to generate bibliometric maps, there are additional tools to visualize bibliometric maps such as Bibexcel and the Sci2 Tool.

That said, based on our review, we provide a rich agenda for future research by outlining some promising research questions. summarizes this future research agenda based on the knowledge gaps in the field, and while not exhaustive, identifies particularly interesting research questions at the intersection of CSR and family business that deserve attention in the near future. We then briefly discuss some of the key methodological and empirical challenges associated with such research.

Table 4. Selected opportunities for future research on CSR in FFs based on the SLR.

First, our SLR highlights some important knowledge gaps in relation to the social responsibility strategies and practices of FFs. Second, we see a need to better understand the implication of the demographics of FF members on the CSR behavior and performance of their firms. Here, we even encourage future scholars to draw on the psychological foundations of management in family firms (Humphrey et al., Citation2021; Picone et al., Citation2021) to understand how the heuristics, biases, values, emotions, experiences, and memories of different family and non-family actors within the FF may affect CSR strategies and behaviors. Third, although ownership criteria have been the most adopted in the empirical literature to distinguish FFs from their non-family counterparts (De Massis et al., Citation2012), our knowledge of the impact of ownership factors, including not only the extent, but also the type and dispersion of ownership, on CSR strategies and behavior is still limited. Thus, a number of unaddressed questions on the effects of ownership factors remain. Fourth, most literature on CSR in FFs has overlooked the impact and variegated role of CSR investments, leaving a number of questions open. Fifth, most family business research focuses on CSR economic outcomes, thus leaving a gap in our understanding of outcomes of a different nature (for example, economic, noneconomic) and at different levels (for example, individual, firm, family). Sixth, the role of the context and/or industrial sector has been overlooked in prior research on CSR and FFs, despite its potential importance (De Massis et al., Citation2018b). Thus, we see a need for future research that more closely examines the effects of contextual factors on CSR drivers, processes, and outcomes. Seventh and finally, a number of other important unaddressed questions for future research on CSR in the context of FFs emerge, for instance, in relation to topics such as CSR as an enabler of innovation objectives, the impact of SEW dimensions and interactions thereof, the effect of different leadership styles on the adoption of CSR practices, and the use of a microfoundational lens (De Massis & Foss, Citation2018) to better understand CSR practices and dynamics in FFs.

Of course, advancing research on CSR in FFs entails methodological and empirical challenges. In fact, to address some of the unanswered questions presented above, scholars will need to broaden the range of methods currently adopted by relying more on, for instance, qualitative research methods that may be particularly useful to capture aspects related to how processes unfold and/or how practices are adopted, as well as multilevel quantitative research designs. Experimental approaches may also be particularly promising for understanding the cognitive aspects that lead to CSR behavior. Moreover, pursuing the research agenda will also likely affect the data sets that scholars adopt. We encourage future scholars to develop data sets that trace, ideally over time, how organizations, families, and/or individuals have built sustainable competitive advantages through CSR strategies and activities, making decisions and acting in a particular FF context. Thus, moving the FF CSR field forward also has the potential to influence the methods and data sets that scholars adopt.

Disclosure statement

No potential conflict of interest was reported by the authors.

References

- Abdelhalim, K., & Eldin, A. G. (2019). Can CSR help achieve sustainable development? Applying a new assessment model to CSR cases from Egypt. International Journal of Sociology and Social Policy, 39(9/10), 773–795. https://doi.org/10.1108/IJSSP-06-2019-0120

- Abeysekera, A. P., & Fernando, C. S. (2020). Corporate social responsibility versus corporate shareholder responsibility: A family firm perspective. Journal of Corporate Finance, 61, 101370. https://doi.org/10.1016/j.jcorpfin.2018.05.003

- Aguilera, R. V., & Jackson, G. (2003). The cross-national diversity of corporate governance: Dimensions and determinants. Academy of Management Review, 28(3), 447–465. https://doi.org/10.5465/amr.2003.10196772

- Amann, B., Jaussaud, J., & Martinez, I. (2012). Corporate social responsibility in Japan: Family and non-family business differences and determinants. Asian Business & Management, 11(3), 329–345. https://doi.org/10.1057/abm.2012.6

- Apriliyanti, I. D., & Alon, I. (2017). Bibliometric analysis of absorptive capacity. International Business Review, 26(5), 896–907. https://doi.org/10.1016/j.ibusrev.2017.02.007