Abstract

The hypothesis of a trade-off between homeownership and welfare state provision, first proposed by Jim Kemeny around 1980, is a foundational claim in the political economy of housing. However, the evidence for this hypothesis is unclear at both macro and micro levels. This paper examines the link between welfare and homeownership at the macro level using new long-run data and a multilevel modelling approach. It shows that the negative cross-sectional correlation between homeownership and public welfare provision observed in the earliest available data disappears and becomes neutral by the 1980s and possibly positive subsequently. Within-country trajectories vary, but are significantly positive in more countries than significantly negative, suggesting that in some contexts welfare and homeownership are complements rather than competitors. The paper posits a dual ratchet effect mechanism in both pension benefits and homeownership capable of producing this inversion, and further suggests that rising public indebtedness and the debt-stabilising effects of welfare states may account for the emergence of complementarity in the pension‒homeownership relationship. The latter supports the hypothesis that some countries have avoided the trade-off by ‘buying time’ on credit markets.

Housing has long been relatively neglected in the comparative welfare states literature and in political economy more generally. Nevertheless, the best-established hypothesis in this terrain is the notion of a long-run trade-off between homeownership and social policy generosity, especially in old-age pensions (Kemeny Citation1981). Castles (Citation1998) termed this homeownership‒pension relationship the ‘really big trade-off’. While scholars took up this hypothesis only sporadically for two decades, recent literature has seen a number of studies of the housing‒social policy link (Ansell Citation2014; Delfani et al. Citation2014; Kohl Citation2018a; Prasad Citation2012; Schwartz Citation2014; Schwartz and Seabrooke Citation2008). Despite initial empirical support, more recent studies have failed to find evidence to support the trade-off hypothesis (e.g. Ansell Citation2014; Kohl Citation2018a). However, a key limitation of this literature is that it confounds cross-sectional and longitudinal dimensions of this hypothesis, which are both theoretically and empirically distinct. The goal of this paper is to test both dimensions of the trade-off hypothesis using the best available data and methods appropriate to the underlying hypotheses.

Kemeny’s primary comparative formulation of the trade-off hypothesis posited a stable negative association between homeownership and social policy, emerging in the early twentieth century or before. One conjecture motivating our research is that previous studies have yielded inconsistent findings because this cross-sectional relationship existed historically, but disappeared over time. Indeed, we show that a homeownership‒pension trade-off existed prior to the 1990s, but has disappeared and even possibly turned positive since. The inversion of the trade-off reflects a process of upwards convergence: a simultaneous increase and decline in variance in both pension generosity and homeownership levels. For most countries, this contradicts the secondary, longitudinal social insurance hypothesis proposed by Castles (Citation1998): the argument that declining welfare provision might incentivise households to pursue homeownership as a form of self-insurance. As we emphasise, however, it is important to recognise the heterogeneity of country trajectories.

This inversion of the trade-off relationship raises the question of why the cross-sectional pattern changed over time (or, equivalently, why within-country longitudinal trajectories vary so widely). Due to the intrinsic limitations of cross-national comparative research in the presence of widely varying patterns, our answers are tentative. First, drawing on the comparative welfare states literature, we posit a dual ratchet effect in both pension and housing systems capable of producing upwards convergence. We provide evidence consistent with this ratchet effect mechanism. Second, we consider the permissive conditions that have enabled some countries (but not others) to achieve an ‘embarrassment of riches’ (both generous pension systems and high homeownership rates). Streeck (Citation2014) has recently argued that a key feature of the post-1970s political economy is the avoidance of seemingly hard trade-offs by ‘buying time’ on credit markets (cf. Krippner Citation2011). We present evidence consistent with this ‘buying time’ view: countries with higher long-run rates of inflation and debt accumulation tended to see greater simultaneous growth in homeownership and pensions.

In addition to changes in the underlying relationship between homeownership and social policy, a second set of reasons for the inconsistent results found in the previous literature is methodological. First, given the difficulty of assembling appropriate long-run datasets, studies have tended to rely on data series beginning in the 1980s. Second, common statistical models are more appropriate for assessing the longitudinal social insurance hypothesis than the original cross-sectional hypothesis, and also assume causal homogeneity across countries. One of the main contributions of this paper is to address these issues. First, we report findings from two datasets: one with the earliest available data for homeownership and pensions (from the interwar period), and another with data from the 1960s through the present, spanning more than 50 years. As we will see, inclusion of pre-1980s data is critical to a test of the cross-sectional trade-off hypothesis. Second, we adopt a multilevel modelling approach that enables us to both distinguish between longitudinal and cross-sectional effects (Bell and Jones Citation2015) and remain attentive to the heterogeneity of within-country trajectories (Western Citation1998).

The paper is structured as follows: after a review of existing literature, we suggest theoretical reasons for the inversion of the trade-off and develop hypotheses about its disappearance. We then present the new long-run data and a methodological discussion of the reasons for inconsistent findings, as well as presenting the motivation for our multilevel modelling approach. The results section first documents the inversion of the trade-off through simple descriptive analyses and then tests whether this shift is robust in multivariate, multilevel regressions. The conclusion summarises the findings and considers implications for the literature on asset-based welfare.

Literature and theory

The hypothesis of a relationship between welfare states and homeownership has a long pedigree in sociology, political science and housing policy scholarship. Writing in the early 1980s, Kemeny (Citation1981) first argued for a systematic trade-off between homeownership rates and a broad range of social policies. At the core of the argument is the observation that homeownership ‘front-loads’ the cost of housing over the lifecycle, because young families need to save for down payments and pay mortgages out of early-career salaries. Kemeny reasoned that this financial burden would tend to depress support for the taxation required to fund redistribution in the form of generous social policies. This account viewed homeownership as the exogenous (and presumably causal) variable: the argument was that in countries with a pre-existing high level of homeownership (especially new world settler societies), welfare state generosity would remain contained (Kemeny Citation2005: 65; Schwartz Citation2012: 42).

An implicit assumption of this argument is that welfare states and homeownership levels reflect highly stable equilibria. In this sense, the original Kemeny trade-off hypothesis is fundamentally cross-sectional. Castles (Citation1998) revised this hypothesis in two ways. First, he argued that the ‘really big trade-off’ was between homeownership and pensions (rather than welfare states as a whole). On this view, homeownership and social insurance are functional substitutes in the provision of old-age livelihoods. Second, he introduced the secondary hypothesis that because of this equivalence, declining public pension provision could incentivise households to seek homeownership as a form of self-insurance. This ‘social insurance’ hypothesis reverses the causality of the relationship, with welfare state spending or benefit levels driving homeownership rates. In contrast to the classic trade-off view, this social insurance hypothesis was mainly longitudinal, rather than cross-sectional: the fundamental claim was that welfare state retrenchment would trigger rising homeownership rates as households sought to self-insure.1

Table A1 in the online appendix provides a list of studies which, broadly speaking, address the trade-off hypothesis. Castles (Citation1998) reported negative and statistically significant correlations between homeownership and a variety of social policy indicators for 20 Organization for Economic Cooperation and Development (OECD) countries between 1960 and 1990. In the first multivariate regression analysis, Conley and Gifford (Citation2006) presented evidence supporting the trade-off hypothesis from a primarily cross-sectional standpoint. In keeping with recent statistical practice, more recent studies have employed fixed effects (and in many cases first-differenced) estimation, making these studies implicitly tests of the social insurance/welfare retrenchment hypothesis, rather than the classic trade-off view. We return to this key methodological point below. Extending the hypothesis to mortgage debt (assumed to be closely related to homeownership), Prasad (Citation2012) also presented supporting evidence.2 However, Ansell (Citation2014) finds that the political and policy effect of homeownership is entirely dependent on housing price increases. Doling and Horsewood (Citation2011) also use within-country longitudinal methods and focus on housing prices, presenting somewhat mixed evidence. Finally, Kohl (Citation2018a) finds a positive rather than negative, but not clearly significant, relationship between homeownership and general state spending.

Table 1. Hypotheses.

This literature is empirically inconclusive. While early studies showed a negative and statistically significant correlation, more recent papers have failed to find supporting evidence (Ansell Citation2014; Kohl Citation2018a). There are several reasons for this ambiguous evidence. First, although the original hypothesis posits a trade-off emerging in the first half of the twentieth century, studies have tended to rely (largely for reasons of data availability) on post-1980s data. Second, largely for methodological reasons, recent multivariate analyses have tended to implicitly shift from the original hypothesis of a stable, cross-national relationship to the secondary hypothesis (Castles Citation1998; Kemeny Citation2005) that welfare retrenchment beginning in the 1980s incentivised households to pursue homeownership as a form of self-insurance. We emphasise that these hypotheses should be treated as distinct.

A third reason is that no study has systematically investigated the possibility that there was a cross-sectional trade-off, but that this trade-off disappeared due to structural changes in housing and/or welfare regimes (Blackwell and Kohl Citation2018). This possibility is suggested by Castles’ (Citation1998) finding of a declining cross-sectional, bivariate correlation between homeownership and pension spending falling from −0.68 to −0.4 between 1960 and 1990. Indeed, simple descriptive statistics suggest that the cross-sectional association between pensions and homeownership has turned from negative to neutral or even positive (see ). Below, we show that this shift is robust to controlling for other variables and that the change in cross-sectional slopes is statistically significant.

Given these patterns, we consider two descriptive hypotheses about the processes that may be driving this inversion. These hypotheses, as well as further arguments about explanatory mechanisms and permissive conditions, are summarised in . The first is asymmetric convergence driven by declining pension benefits in historically high pension countries. According to this hypothesis, exogenous changes in pension spending and benefits reflecting welfare state retrenchment, particularly in historically low homeownership countries, induced increases in homeownership. In other words, high pension countries historically positioned in the ‘top left’ quadrant of the homeownership‒pension space in and moved towards the centre. Note that this implies a negative within-country relationship between pensions and homeownership, at least in countries with a substantial degree of retrenchment. This process is thus consistent with the Castles secondary social insurance hypothesis, and thus with the conjecture of a within-country trade-off. However, an important implication is that a substantial effect of this kind would moderate or potentially neutralise Kemeny’s primary cross-sectional observation.

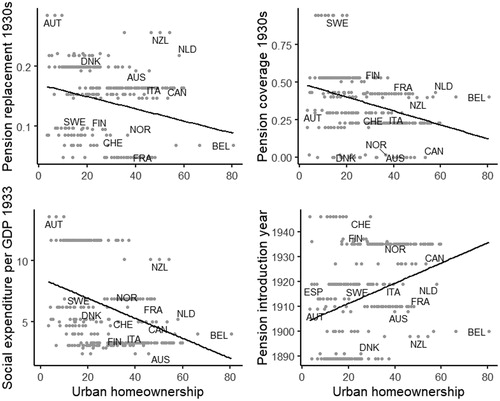

Figure 1. Homeownership‒pension trade-off in major interwar cities.

Sources: see Online Appendix I.

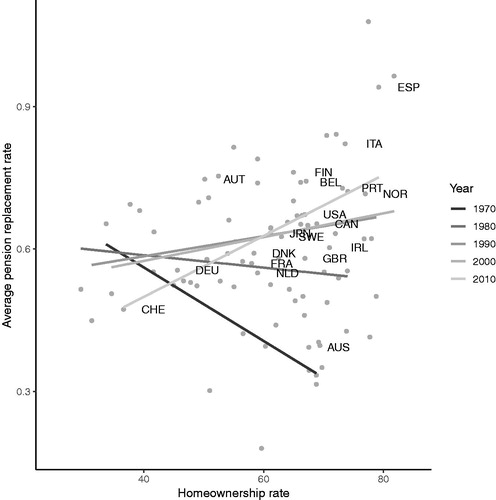

Figure 2. Inversion of the pension‒homeownership trade-off.

The second hypothesis is bi-directional upwards convergence. According to this interpretation, both homeownership and pensions have increased ever time, converging on levels that were considered ‘high’ in relative terms in the 1970s. Upwards convergence implies a declining correlation for reasons contrary to the welfare retrenchment hypothesis: as pension benefits rose among relative laggards (historically high homeownership countries), the cross-sectional correlation declined as these countries moved towards the ‘high spending, high homeownership’ quadrant. On this hypothesis, many countries have experienced a growing ‘embarrassment of riches’ as they achieve both high levels of homeownership and generous pensions. This hypothesis implies a positive within-country relationship between pensions and homeownership in most cases, contradicting Castles’ social insurance hypothesis. We show below that the evidence supports the latter, upwards convergence hypothesis: the within-country relationship is positive in most countries, and significantly positive in more countries than significantly negative.

From the standpoint of the welfare states literature, this is perhaps unsurprising. This is because, despite early concerns about pension retrenchment, there has in fact been little decline in pension spending and benefits in most countries. Pierson (Citation2011: figure 4) shows that pension benefits (measured by replacement rates) rose between the 1970s and 1990 as liberal, social democratic and late-developing Southern European countries ‘caught up’ with the high benefits of conservative regimes. Huber and Stephens (Citation2001) posit a ratchet effect mechanism to account for this pattern: social policies are resistant to downward adjustments because of the political difficulty of reducing benefits.3 describes significant convergence regressions for the replacement rate and pension spending: countries with initially low pension provision had higher average growth rates over the later decades. Thus, upward adjustments tend to accumulate over time and not be offset by corresponding downward pressures.

Table 2. Multilevel models of average pension replacement rate, 1970–2013.

Table 3. Convergence regressions for homeownership (1963‒2010), replacement rates (1975‒2010) and pension spending (1960‒2010).

We address two explanatory questions about this process of upward convergence: first, what are the mechanisms underlying the process; second, what are the permissive conditions that enabled it to take place? Regarding the first question, we extend Huber and Stephens’ analysis of welfare policy ratchet effects to housing, suggesting that a dual ratchet effect in both realms could account for upward convergence. Regarding the second, we draw on a recent body of work arguing that a key feature of the post-1970s political economy is the existence of political efforts to avoid apparently binding trade-offs (Krippner Citation2011; Streeck Citation2014), especially through credit markets. In both cases, we emphasise that our goal is to suggest theoretical mechanisms and conditions capable of producing the patterns we observe in the data. Below we present evidence consistent with these hypotheses, but we emphasise that data limitations inherent in cross-national research on a small group of countries rule out the possibility of definitive tests.

Explanatory mechanisms: a dual ratchet effect

While early theorists treated the trade-off argument almost as an accounting law – more money for tax-financed social policy, less for mortgage payments – on further reflection it is clear that any trade-off is conditional on other factors. For example, given that all households consume housing in some form, the choice between homeownership and renting depends on their relative cost. For a given level of taxation, a shift in housing prices or the price/rent ratio may therefore affect the homeownership rate. There are also numerous influences on welfare state development other than homeownership. Castles and Ferrera (Citation1996) recognised this conditional character of the trade-off argument in their discussion of the apparent Southern European ‘exception’ combining high homeownership and relatively generous social policy.4 They argued that this apparent exception is possible in part due to deficit spending. We return to this point below, showing that this is not an ‘exception’, but a general pattern not limited to Southern Europe.

Huber and Stephens (Citation2001, cf. Pierson Citation2011) argue that because of the political costs of withdrawing benefits, social policies are resistant to downwards adjustments. We suggest that homeownership is subject to similar effects: homeownership is politically popular and constraints on home purchase politically costly. For example, homeownership subsidies (such as mortgage interest tax deductions) are the largest part of the ‘hidden welfare state’ (Howard Citation1997), which is resistant to retrenchment (Pollard Citation2011). Moreover, with almost all countries turning into ‘property-owning democracies’, centre-right and centre-left parties compete to represent home-owning constituencies (Schelkle Citation2012). A study of housing policies in party manifestos in 19 OECD countries since 1945 shows that support for homeownership increased across parties through the 1990s (Kohl Citation2018b). The dual ratchet effect mechanism implies that other factors bundled into the implicit ‘ceteris paribus’ claim underpinning the trade-off hypothesis have tended to push both variables up without triggering declines in the other. The political unpopularity of decreases in either public pensions or homeownership means that causal forces pushing in this direction are weaker than those driving increases.

Thus, in keeping with Kemeny’s original hypothesis, we suggest that in the early stage of welfare state formation, high homeownership rates were an effective political barrier to the taxes required to finance social policy expansion. However, because homeownership is not the only influence on welfare state development – after all, housing figures little in the broader literature on welfare state formation (Esping-Andersen Citation1990; Huber and Stephens Citation2001) – over time, these countries did develop and then expand welfare states. The ratchet effect implies that these increases in social policy generosity did not cause substantial declines in homeownership, because of the inherent downwards rigidity of the latter.

Conversely, in the first half of the twentieth century, political demand for public pension policies was strongest (and opposition to taxation weakest) in low homeownership countries. Subsequent to this welfare state expansion, many of these countries saw increases in homeownership rates. This occurred in part because political elites in these countries saw promoting homeownership as consistent with their goals of establishing robust welfare states. Promoting homeownership, as has been widely observed, is also social policy (Prasad Citation2012; Schelkle Citation2012). In the Nordic countries, for example, long-standing policies favour ownership in housing cooperatives, consistent with the social democratic orientation of these welfare regimes (Stamsø and Tranøy Citation2019). Similarly, Southern European countries have engaged in a variety of policies to promote homeownership, while also developing generous (albeit segmented) welfare states (Castles and Ferrera Citation1996). According to the classic trade-off view, these increases in homeownership rates should have depressed support for the welfare state, especially pensions. However, the social policy ratchet effect implies that whatever the impact on the political preferences of marginal homeowners, rising homeownership has little aggregate effect on social policy.

Permissive conditions: ‘buying time’

The homeownership‒pension ratchet effect provides a theoretically consistent analysis of the mechanism producing an inversion of the trade-off. However, it does not account for the structural conditions which make it possible for countries to sustain an ‘embarrassment of riches’ (i.e. a combination of a high homeownership rate and generous pensions). That is, if the trade-off first observed by Kemeny was a binding constraint in the early twentieth century, why has it not been more recently?

A recent strand of literature suggests that the post-1970s political economy is characterised by policies that avoid allocative trade-offs by ‘buying time’ on credit markets. Streeck (Citation2014) argues that, in the face of declining state revenue, governments resorted first to inflation (in the 1970s), then public debt (in the 1980s and 1990s) and then private debt (in the 2000s) in order to avoid cuts to public spending. Similarly, Krippner (Citation2011) argues that the post-1970s expansion of credit in the US emerged as the unintended consequences of a turn towards credit markets to make tough choices about allocating capital. In this vein, we suggest that the trade-off lost its ‘bite’ because political elites have avoided passing the costs of social policy directly on to homeowners. The upshot of the ‘buying time’ argument is that countries can avoid the trade-off because private and public debt (as well as inflation) defer the costs of homeownership, pensions, or both. The buying time hypothesis thus implies that countries that experienced higher long-run inflation and/or growth in public and private debt saw greater joint growth in homeownership and pension generosity.

Several channels enable households and governments to defer costs and thus escape the trade-off logic. Inflation can shift the mortgage burden from borrowers to creditors (in some contexts) and create ‘money illusion’ giving a temporary boost to spending (Streeck Citation2014). Developments in mortgage markets, in particularly the lengthening maturities of mortgages (e.g. the increasing availability of long-term mortgages) allowing households to extend the repayment process (Van Gunten and Navot Citation2018) can make debt burdens more manageable under some conditions.5 Although mortgage market development has not always favoured rising homeownership (Kohl Citation2018a), the 1960s and 1970s (the period of late welfare expansion and rising homeownership) seem to be the main time when it did. Larger and longer mortgages permit higher loan-to-value ratios, thereby lessening the down-payment constraint. Both exogenous factors thus began to disable the ‘front-loading’ micro-mechanism behind the trade-off by making homeownership more accessible and by stretching its costs over time.

Public debt, in turn, works in a similar way on the pension side of the trade-off by shifting the possibilities of what governments can simultaneously afford. This is most obvious in countries with pay-as-you-go pension plans and where pensions are closely tied to the overall tax-financed budgets, such as in Scandinavian countries. But even in countries where contributory pensions have their own budget, increasing life expectancy makes general budget supplements necessary. Moreover, the pension costs of government employees – which make up more than 15% of OECD countries’ labour force and between 17% (in France and Germany) and 27% (Austria) of pension expenditure (Ponds et al. Citation2011) – have been steadily rising as an often implicit liability. As tax income failed to keep pace with rising social spending since the 1980s (possibly due to conservative tax revolt) (Streeck Citation2014), only large increases in public debt could impede a pension retrenchment.

A key factor in the availability of credit for pensions and homeownership is the so-called global savings glut. Since the 1970s, the international deregulation of financial markets, growth in private pension fund assets due to the privatisation of pensions and rising life expectancy led to an abundance rather than a scarcity of capital (von Weizsäcker Citation2016). This is visible in the generally declining trend of global interest rates, the importance of asset management firms and the rising ratios of most financial indicators to underlying economic activity (Yi and Zhang Citation2017). This capital supply hypothesis complements the buying time hypothesis and implies that countries with a greater capital supply (as reflected in the savings rate) are more likely able to afford both high pensions and homeownership levels.6 To the extent that the widespread availability of capital allows countries to fund pensions and homeownership, we expect these countries to exhibit a weaker trade-off, or indeed a complementarity.

In addition to these political economy-based hypotheses, we also consider two simple explanations for the disappearance and apparent inversion of the trade-off. First, rising levels of homeownership and pension generosity may simply reflect an increase in aggregate national income. According to this hypothesis, rising incomes weaken the trade-off because households have more ability to pay both taxes and mortgages. This income growth hypothesis thus states: countries that experienced faster growth incomes experienced a stronger positive association between homeownership and pensions. Second, increasing life expectancy could cause mechanical increases in homeownership (as population ageing implies that homeowners account for a greater share of the population) and pension spending. This life expectancy hypothesis implies that countries that saw greater increases in life expectancy (i.e. longer retirement duration) saw greater positive associations between homeownership and pensions.

To summarise, we argue that the existence of a trade-off between homeownership and pension spending is conditional on a number of different factors. Among these is the extent to which households are actually pinched by social security taxes that (at the margin) prevent them from achieving homeownership. In many cases, the rate of increase in taxes has lagged that of pension benefits and expenditure, while debt increases have also accompanied welfare state expansion. We return to these issues in the discussion section below.

Data and methods

As we argued above, the literature to date has produced inconsistent evidence of a homeownership‒pension trade-off. Data limitations are a first reason. Most previous research on the welfare state‒homeownership trade-off uses OECD social spending data or some narrower spending component, particularly pension spending. These data in panel form are conveniently available only from 1980, which partially explains the sample period used in many previous studies. The (recent) historical period used in previous studies is important because, as we show, the trade-off had largely disappeared by the 1980s. Since we seek to explore both the primary long-run, cross-sectional trade-off argument and the secondary longitudinal hypothesis, we seek to use the longest possible panel and a variety of social policy indicators.

We do so in several ways. First, we primarily use a direct policy (as opposed to spending) indicator, the average pension replacement rate computed from the Comparative Welfare Entitlements Dataset (Scruggs and Allan Citation2006), which is available from 1970. There are two main reasons to consider policy as well as spending indicators of social policy. First, replacement rates are a direct measure of the benefits actually received by households, while social spending data reflect demographic patterns (such as population ageing) and other structural needs (Esping-Andersen Citation1990; Scruggs and Allan Citation2006) as well as welfare policies. Second, as far as we are aware, no previous trade-off studies have used policy rather than spending indicators. Thus, one of our main contributions is to test the trade-off hypothesis using direct policy indicators for the first time.

Second, we also construct a panel of pension spending as a percentage of GDP going back to 1960 using data provided by the OECD (Citation1985). While there are well-known issues of comparability (Kangas and Palme Citation2013), we apply a statistical adjustment to reconcile pre- and post-1980 data.7 We also gathered national homeownership rates going back to the 1950s, interpolating the country trend where necessary (Kohl Citation2017: 20–21). The panel includes controls taken from the Penn World Tables, World Bank and Comparative Political Data Set (Armingeon et al. Citation2018; Feenstra et al. Citation2015). We adopt the same set of controls as Ansell (Citation2014), with the addition of life expectancy.8

Third, we also collected cross-sectional data for the interwar years in the form of urban homeownership rates (by city) for most of the OECD countries (see sources in Online Appendix I), as well as social spending and policy data from the International Labour Organization (ILO)9 and the Social Insurance Entitlements Dataset (SIED) database for the 1930s (SIED Citation2015). As far as we know, these are the earliest available relevant data.

A second reason for inconsistent findings is methodological. While the earliest studies (Castles Citation1998; Kemeny Citation1981) focused on cross-sectional correlations, more recent and sophisticated studies (Ansell Citation2014; Kohl Citation2018a; Prasad Citation2012) employ fixed effects estimation and other common methodological practices (Beck and Katz Citation1995). There are two problems with this approach in this context. First, a country fixed effects approach does not test the classic trade-off argument, namely a stable negative cross-sectional correlation. If this hypothesis is true, we should not expect fixed effects estimation to confirm it.

Second, attention to statistical issues such as omitted variable bias should not distract from simple descriptive patterns clearly visible in the data. Our preliminary descriptive analysis showed clear evidence of heterogeneity in both cross-sectional and within-country associations. Given this descriptive pattern, we focus on identifying the country-specific trajectories that result in the inversion of the cross-sectional association from negative to positive. To do so, we employ multilevel estimation with country-varying coefficients that capture within-country paths as well as time-varying slopes that capture the changing cross-sectional pattern. Allowing for country- and decade-specific slopes allows for heterogeneity in the underlying processes generating cross-national associations (Western Citation1998).

A key issue in such models is the potential correlation of group-level coefficients (in this context, varying country intercepts) with predictor variables. However, this issue can be addressed by including the country-specific mean of each independent variable as an additional predictor (Bafumi and Gelman Citation2006; Bell and Jones Citation2015). Simulations show that this method performs at least as well as fixed effects estimation. In this paper, we follow Bell and Jones (Citation2015) in additionally expressing each predictor as a difference from this country mean. This has the advantage of allowing an interpretation of the difference and country-mean terms as the within-country and between-country effects, respectively.

Whereas commonly reported fixed effects estimates assume causal homogeneity, providing one parameter estimate that pools data across countries, our multilevel analysis provides evidence of substantial heterogeneity in within-country parameters. Ideally, one might take the next step and formally account for this heterogeneity using country-level predictors of these slopes. Unfortunately, the number of cases (around 20) in comparative OECD country-level data is simply too limited to allow for formal test of this kind. Thus, we examine this variation descriptively, presenting evidence consistent with the ‘buying time’ hypothesis, but do not claim to provide a definitive test.

The trade-off in the long run: descriptive findings

Given that modern welfare states emerged between the late nineteenth century and the immediate post-war period, the ideal time period for identifying any trade-off is roughly the first half of the twentieth century. Before 1950, most countries did not report national homeownership rates. We therefore collected urban homeownership rates in countries’ major cities for benchmark years between 1910 and 1950 and took the average of available data. To measure welfare state provision at this time, we use the ILO’s data on social expenditure as a percentage of GDP reported for 1933, the pension coverage and the replacement rate in the 1930s (from SIED), and the year of introduction of a country’s pension system (Schmitt et al. Citation2015). These measures capture different aspects of welfare provision and do not always correlate highly between each other. They are, however, negatively correlated with the averages of cities’ homeownership rates (expectedly positive in the case of the timing of pension introduction) at below 0.001 significance (see ). While cities tend to display certain national profiles, they also display considerable within-country variance, which is of course not accounted for by the national welfare variable.

Castles (Citation1998) also presented a version of the trade-off argument suggesting that extensive rural farm ownership rather than urban homeownership rates which pre-empted the need for a generous public pension system. We therefore examined the association between the percentage of family-owned farms in 1928 (or, alternatively, 1898) with the four welfare variables used above, using Vanhanen’s (Citation2007) family farm share, ILO social expenditure and the pension entitlement data, respectively. There is a significant negative correlation between countries’ farm ownership share and its pension coverage rate as well as a positive one with the pension reform introduction years, while the correlations with either the replacement rate or the ILO social expenditure measure are insignificant. Thus, the evidence does not strongly support the rural ownership hypothesis in early data. There is, however, moderate to strong evidence of a trade-off between urban homeownership and social policy in the interwar period.

Moving forward to the 1970s, illustrates the relationship between homeownership and pension generosity, measured by average replacement rates, with independent cross-sectional slopes. The figure shows that the negative cross-sectional association observed by Kemeny holds in the 1970s, but as early as the 1980s this slope turned neutral and then positive in subsequent decades. We see similar patterns in scatterplots (see Figure A1 in the online appendix) using the synthetic pension generosity index proposed by Scruggs and Allan (Citation2006). Data on pension spending also suggest a trade-off in the 1960s and 1970s which has become neutral in more recent decades, though (in contrast to policy measures), there is little evidence that the trade-off became a complementarity in the most recent data.

Thus, descriptive exploration of the available data provides support for the trade-off hypothesis, in its original cross-sectional formulation, in observations between the 1930s and 1970s. However, high-quality recent data clearly show a moderation (for spending measures) or inversion (for policy measures) of this relationship, such that by the 1980s or 1990s the relationship between homeownership and pension generosity is neutral or even positive. This is important for studies that attempt to test the trade-off hypothesis in a multivariate setting using annual datasets, which typically include only post-1980s data. Given that the cross-sectional relationship manifestly turned positive after the 1980s, there is little sense in testing the hypothesis of a uniform negative relationship. That is, we must take seriously this descriptive evidence of parameter heterogeneity. Moreover, an empirical corollary of the inversion plotted in is that the within-country relationship between homeownership and pensions is on average positive, rather than negative. This can be clearly seen in a scatterplot (not shown) of the data summarised in , but fitting a country-specific (rather than decade-specific) slope. With a couple of exceptions, homeownership and pension replacement rates have risen in tandem since the 1960s. This can be attributed in large part to common trending: in most countries, the long-term trajectory of both variables is upwards. However, given the wide range of trajectories, we turn to multilevel modelling below to examine the range of longitudinal relationships.

Multivariate analysis

The standard approach to our time-series, cross-sectional data is to estimate linear panel models with country fixed effects to account for unobserved heterogeneity. Such an analysis is inconclusive (see Table A2 in the online appendix). Simple ordinary least squares (OLS) panel models show a positive and statistically significant effect between homeownership and pension (apparently contradicting the trade-off hypothesis), but this effect is negative but statistically insignificant (for pension spending) in a fixed effects model, and positive and insignificant in lagged dependent variable estimates and models with time fixed effects. For replacement rates, the association is positive and insignificant in all models. Clustering standard errors at the country level, as is standard practice, also emphasises the substantial uncertainty of these estimates.10

One could conclude from this analysis that there is no robust relationship between homeownership and pensions, or that the data are simply insufficient to provide any definitive answer. We think such a conclusion is premature for one basic reason: fixed effects estimates ignore the parameter heterogeneity readily apparent in . Multilevel models provide a natural approach to modelling such heterogeneity (Western Citation1998). We estimate multilevel models of both pension replacement rates and spending, with separate random-slope models for decade and country. As discussed above, our estimation approach follows the proposal of Bell and Jones (Citation2015). For reasons of parsimony, we report here results from analyses of pension replacement rates, and discuss differences with pension spending where relevant. These models allow us to compute decade- and country-specific slopes, summarising the heterogeneity in both cross-sectional and within-country relationships.11

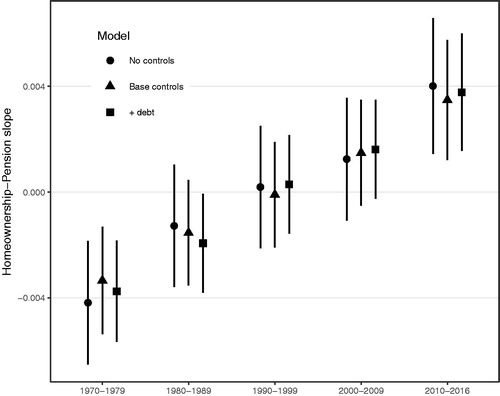

As shown in , in models with random decade and country slopes, the average cross-sectional (between-country) relationship between homeownership and pension replacement rate is indistinguishable from zero. This result is comparable to the OLS results just discussed. However, this average conceals the shifting cross-sectional relationship depicted in . shows the changing cross-sectional relationship between homeownership and pension replacement rates via the random decade slopes taken from three models. In addition to the ‘base controls’ model (column 1 in ) and an extended model including public and private debt, we also report random slopes from a bivariate model as a baseline. Note that debt data are not available for some countries. These models support the hypothesis of a negative cross-sectional relationship in the earliest data; this relationship was insignificant by the 1980s and turned positive in the latest available data (though it should be noted that a full decade since 2010 is not yet available). This pattern is robust to the variables included in our full model and to controls for debt. Similar results are shown by an OLS regression (with year, but not country fixed effects to capture the cross-sectional relationship) which interacts homeownership with a dummy variable for each decade.

Figure 3. Random decade slopes from multilevel estimates.

A similar analysis (see Table A4 and Figure A2 in the online appendix) of our long series on pension spending (1960–2013) instead of replacement rates yields similar conclusions, with a few provisos. The average cross-sectional relationship between homeownership and pension spending is essentially null. However, this average again conceals substantial variation; multilevel estimates imply that the relationship was negative and mostly statistically significant12 through the 1980s, turning neutral thereafter. However, it is less clear that the relationship between pension spending and homeownership has turned positive. This conclusion is supported by multilevel estimates but not by the simple descriptive data, which support a negative-to-null shift, but not a positive coefficient in more recent years. Thus, results for pension spending strongly support the disappearance of the trade-off, but not necessarily a shift towards complementarity.

We turn now to accounting for the logical corollary of this cross-sectional inversion: the longitudinal country trajectories that produced it. The upwards convergence hypothesis implies that some countries have moved towards the top-right quadrant of . This in turn implies that these countries experienced increases in both variables (above the average trend), entailing a positive slope in the country-specific varying slope models. shows that, in models allowing for decade-varying slopes as just discussed, the average within-country (longitudinal) relationship between homeownership and pension replacement rates is positive (and strongly statistically significant). However, this interpretation is undermined for models that allow for country-specific slopes: accounting for the variability of country trajectories, the average relationship is much closer to zero. The conclusion here is similar to the results from fixed effects models: the relationship appears positive but imprecisely estimated.

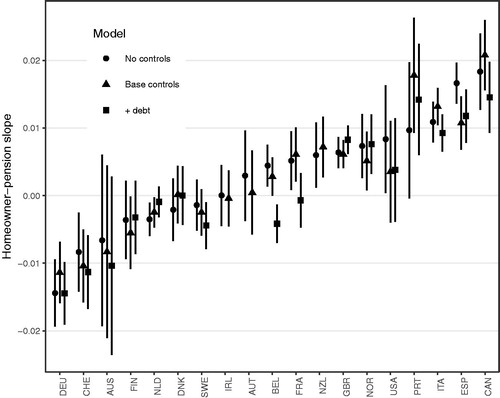

As before, however, we are most interested in the variability of within-country coefficients, rather than the average relationship. shows the country-specific slopes for models of average pension replacement rates. As before, we report results from three different models (including those summarised in columns 3 and 4 in ). Country trajectories display a wide variability centred on zero, with more countries displaying a positive than a negative association with homeownership. Taking the base control model as a benchmark, nine countries experienced homeownership‒pension complementarity, three experienced a trade-off, and five experienced no discernible correlation.

Figure 4. Random country slopes from multilevel estimates.

Focusing on our ‘base’ model, countries that experienced significant, positive, above-trend growth of both homeownership and pension replacement rates fall into two primary groups: predominantly Catholic countries in South-Western Europe (Spain, Italy, Portugal and to a lesser extent France and Belgium), the UK and some Commonwealth countries (including Canada and New Zealand, both not Australia) and, more ambiguously, the US. In addition, Norway falls into this category as a clear outlier relative to the rest of Scandinavia. Meanwhile, only three countries saw an inverse relationship between homeownership and replacement rates (consistent with the ‘welfare retrenchment’ hypothesis): Germany, Switzerland and the Netherlands. Results for pension spending reported in the appendix yield similar results, with a few exceptions.13

On balance these results support the upwards convergence hypothesis rather than welfare retrenchment-induced asymmetric convergence. Countries that have shifted towards the high-homeownership, high-pension quadrant generally saw substantial increases in pension replacement rates between the 1970s and 1990s, and moderate to no retrenchment thereafter. Germany, Switzerland and the Netherlands all had above-average replacement rates in the mid-1970s and saw fairly substantial declines by the 2000s. As suggests, these are the only three countries where a negative and statistically significant negative relationship (predicted by the social insurance hypothesis) appears. In contrast, countries like Spain, France and the UK had average or below-average replacement rates in the mid-1970s, substantial increases through the 1990s and limited if any retrenchment thereafter. Spain in particular stands out as the only country, as of 2000, with an average replacement rate in excess of 90% (a level only briefly reached in European history by Sweden in the early 1980s). These countries also experienced higher than average growth in homeownership rates.

Above, we proposed that a dual ratchet effect mechanism could account for this upward convergence. According to this hypothesis, both pension generosity and homeownership are resistant to downward adjustments; thus, upward shifts tend to accumulate over time, leading to an overall upwards drift. In order to assess this dual ratchet effect hypothesis, we follow convergence analysis in growth economics (Young et al. Citation2008) and regress average annual growth rates in homeownership, pension spending and pension replacement rates on their respective initial (log) values of these variables (measured in 1963, 1960 and 1971, respectively). This so-called beta-convergence method is typically used to account for catch-up processes which are implied by convergence hypotheses. Consistent with the dual ratchet effect hypothesis, we report negative and statistically significant associations between initial values and later growth rates (see ). In other words, countries with higher initial homeownership and pension generosity experienced less subsequent growth, and vice versa. The standard deviation of OECD homeownership rates (or sigma convergence) also falls over time. Thus, the evidence is generally consistent with the ratchet effect mechanism.

The inversion of the cross-sectional relationship between homeownership and pension generosity occurred because countries in Catholic South-Western Europe, the UK and the Commonwealth, and a few others were able to defy the ‘really big trade-off’, providing households with both relatively generous public pensions and the widespread availability of homeownership. The question is therefore how these countries were able to escape the trade-off, and more generally why some countries show a negative association and others a positive one.

We suggested above that public and private debt provide a means of escaping the trade-off bind, because public borrowing disables the tax mechanism at the heart of the hypothesis. For this reason, we add debt measures as predictors in our models in and and . Public debt has a significant, positive within-country association with pension replacement rates and spending, though there is no evidence of a between-country relationship. In other words, growing debt likely accounts for part of the growth in pensions in the post-1970s period, although historically speaking more generous welfare states have not been higher-debt states. Mortgage debt has a negative relationship with pension replacement rates but a positive (though not fully robust) relationship with pension spending. We defer closer study of this anomalous relationship for further research.14

Controlling for debt measures also seems to moderate the trade-off relationship somewhat; in general, country-specific coefficients in models including debt are smaller, though somewhat marginally so. This relatively limited moderating effect may reflect limitations of our modelling approach given the extremely long-run character of the processes involved. In the following discussion section, we return to the role of debt, with some suggestions for further research.

Country trajectories: buying time?

shows that countries followed a wide variety of trajectories through the homeownership‒pension space, with more countries exhibiting an apparent complementarity than a trade-off. Empirically, we would ideally like to account for this variation in country-specific slopes. However, it is critical to recognise the limitations of cross-national data: ultimately, we have fewer than 20 coefficients to be explained. Thus, we focus on establishing which hypotheses are consistent with the data, recognising the difficulty of providing definitive evidence.

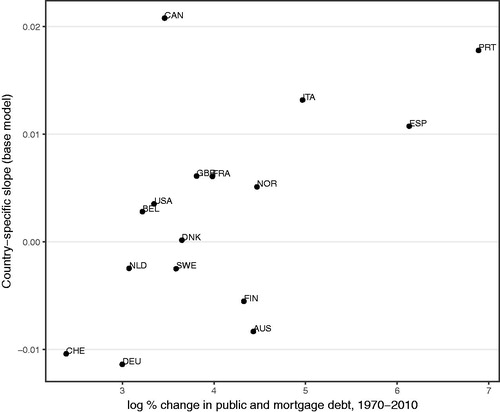

The buying time hypothesis introduced above implies that countries experiencing greater long-term increases in inflation and debt (both public and private) are more likely to see an ‘embarrassment of riches’ (both high pensions and homeownership). The associated variables – inflation, mortgage debt and public debt – are included in our models. However, the buying time hypothesis does not imply that these variables have an immediate impact (or even an impact with a short lag). Rather, the hypothesis suggests a very long-run relationship between changes in inflation and debt and the country-specific relations between homeownership and pensions. While we have already seen that debt has a modest mediating effect on this relationship (see ), these models do not capture the influence of long-run trends and changes. Such effects are much more difficult to model.

In order to assess these long-term relationships more informally, we plot long-run changes (c. 1960/1970 through to c. 2015) in public and private debt, inflation and other variables against the within-country slopes reported in . A series of these plots is provided in Figure A3 in the online appendix. In the appendix figures, there is some indication of a linear association between debt measures and inflation and country slopes. This association becomes clearer in , which combines public and private debt; as this figure shows, countries experiencing greater debt growth since 1970 show a stronger positive within-country association between homeownership and pensions.15 The fact that this relationship emerges more strongly after pooling public and private debt suggests that these forms of credit may be substitutes: in some countries debt growth occurs in the public sector, in others among private actors. For example, Germany saw a large long-run increase in public debt but a relatively small increase in private debt. Conversely, Sweden saw a comparatively small increase in mortgage debt but a larger increase in public debt. Pooling these forms of debt produces the strong linear association with country slopes depicted in , which supports the buying time hypothesis.

Figure 5. Long-run changes and random country slopes.

In addition, Figure A3 in the online appendix shows a fairly strong linear association in long-run inflation with country slopes, also suggested by the buying time hypothesis. This relationship is clearest for the Southern European countries, which also stand out in . For both debt and inflation, however, France, Norway and the United Kingdom are also consistent with this pattern. In contrast, the pattern for national savings is unexpectedly negative, inconsistent with the capital supply hypothesis. This reflects the fact that most countries have seen negative growth in savings relative to income over the past several decades. In this sense, this relationship is a mirror image of the debt findings just discussed. It does suggest, however, that the domestic capital supply is not the driving factor in the inversion of the trade-off. Finally, Figure A3 in the online appendix does not suggest any linear association between country slopes and long-run changes in national income or life expectancy. While admittedly descriptive, this analysis thus supports the buying time hypothesis over any alternative we have considered.

It is instructive to consider this evidence in light of the observations of Castles and Ferrera (Citation1996). Drawing on data from the 1980s and early 1990s, they noted that four countries had both higher than average pensions and homeownership: Greece, Italy, France and the United Kingdom (Spain was a marginal case). Examination of and shows that this claim turns out to have been prescient: not only the Southern Europe ‘exceptions’ but also the UK, US, several Commonwealth countries and France have been moving towards the top-right corner of homeownership‒pension space. These trajectories correlate highly with the combined increase in public and private debt in these countries. Thus, the pattern observed by Castles and Ferrera does not appear at all exceptional, but rather to represent one end of the new homeownership‒pension continuum. While we cannot provide definitive evidence that debt is the key driver of this shift, this relationship stands in need of further research.

Conclusion

The central claim of this paper is that the homeownership‒welfare trade-off once was, but is no more. It belonged to a particular historical period of hard constraints, but has faded and even turned into an ‘embarrassment of riches’ in many countries since the 1980s. This is particularly visible in direct pension policy measures, such as replacement rates, rather than broad expenditure variables. The most extensive long-run data available and multiple methodologies support this claim.

Theoretically, we propose three complementary hypotheses to account for this inversion. First, we distinguish between asymmetric and upwards convergence hypotheses regarding the country trajectories driving change in the cross-sectional pattern. We have shown that the evidence supports the latter: simultaneous increase in both homeownership and pensions in most countries. Second, we suggest a mechanism capable of producing this upward convergence: dual ratchet effects operating through the political resilience of pensions and politics of hidden welfare in homeownership. Finally, we note that trade-offs of whatever sort ‒ between military spending and education, welfare and homeownership or equity and efficiency ‒ are supported by particular historical conditions and constellations which produce real or only perceived scarcity and exclusive alternatives. Once the historical background conditions change, the contingent trade-offs can disappear and even turn into complementary relationships. In keeping with this view, drawing on the ‘buying time’ argument of Streeck (Citation2014), we suggest that the ‘embarrassment of riches’ emerging in high-pension home-owning societies has been made possible by reliance on credit markets. In other words, changes in credit markets were the background conditions that ‘disarmed’ the trade-off. These changes, which set in beginning in the 1980s and varied substantially across countries, helped to offset the scarcity generating the trade-off. Our evidence is consistent with this ‘buying time’ hypothesis, insofar as higher levels of inflation and public and private indebtedness are associated with stronger complementarity between homeownership and pensions.

We conclude by noting the implications of our findings for the literature on asset-based welfare (Doling and Ronald Citation2010). According to this idea, states have shifted from active provision of social policy benefits to more passive efforts to promote homeownership and housing prices as a means of sustaining old-age livelihoods. Empirically, this view suggests that traditional welfare is becoming more and more obsolete in light of the generally increasing homeownership trends. However, our results suggest that, in the long-run perspective and given necessary background conditions, there is little evidence of a shift in this direction. Rather, there is some evidence of a tendency for high-homeownership countries to also become high-welfare provision countries, and vice versa. Whether this trend is sustainable is another question. The implication of the ‘buying time’ view is that the costs of homeownership and pensions have been postponed, not avoided altogether. In the even longer run, if the trade-off logic is ultimately correct, we expect some reversal of this ‘embarrassment of riches’.

Supplemental Material

Download PDF (190.3 KB)Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Notes on contributors

Tod Van Gunten

Tod Van Gunten is Lecturer in Economic Sociology at the University of Edinburgh. His research interests include the comparative economic and political sociology of finance. He has written articles in Socio-Economic Review, Sociological Science and Social Science Research. [[email protected]]

Sebastian Kohl

Sebastian Kohl is senior researcher at the Max Planck Institute for the Study of Societies, Cologne. His research centres on the comparative political economy of housing. He is the author of Homeownership, Renting and Society: Historical and Comparative Perspectives (Routledge, 2017) and articles in Socio-Economic Review and Politics and Society. [[email protected]]

Notes

1 However, Conley and Gifford (Citation2006) apply this logic in a largely cross-sectional empirical context.

2 However, Kohl (Citation2018a; cf. Van Gunten and Navot 2018) shows that the link between mortgage debt levels and homeownership is much weaker than often assumed. Stamsø and Tranøy (Citation2019) and Anderson and Kurzer (Citation2019) in this issue also show that the welfare‒debt trade-off is not easily supported by Scandinavian countries or the Netherlands.

3 In addition to the political forces underpinning the ratchet effect, there may be more mechanical drivers, such as the maturation of pension schemes and the incremental nature of many reforms. We are indebted to an anonymous reviewer for this point.

4 This pattern is also likely consistent with former socialist countries; we do not examine these countries here due to the many complications introduced.

5 During the recent housing boom, there is more evidence that these features contributed to rising housing prices, exacerbating the debt burdens of homeowners.

6 We thank an anonymous reviewer for suggesting this hypothesis, as well as the income and life expectancy hypotheses introduced below.

7 We matched the old (OECD Citation1985) and the new (OECD Citation2018) pension expenditure per GDP series by linking the older ‘pension’ with the newer ‘old age’ category. We took ‘public and mandatory’ expenditure for the newer series, excluding ‘private voluntary’ spending. The two series show a discontinuity in levels in 1980. We corrected for this by using the overlapping years to estimate the post-1980 series using the pre-1980 data, and then predict values consistent with post-1980 series.

8 We exclude capital account openness from our models because inclusion restricts the sample period, and because Ansell (Citation2014) does not report significant relationships with pension spending or replacement rates.

9 Taken from Dryzek and Goodin (Citation1986).

10 Although space precludes a full discussion, we doubt that the assumptions of these models are appropriate to slow-moving, slow-adjusting variables such as homeownership and pension benefits ratios.

11 We do not simultaneously estimate random slopes for both country and decade to avoid over-fitting. Attempting to fit random slopes by year results in convergence problems (because only 20 observations are available per year), requiring aggregation to the decade level.

12 In some decades, either the bivariate or base model coefficient is only significant at a 0.1 threshold. However, controlling for debt, the 95% confidence interval excludes zero in the 1960s and 1970s.

13 Pension spending results suggest that Ireland, Austria, Denmark, Luxembourg and Greece – all of which show no discernible relationship in the replacement rate analysis – experienced a trade-off. At the other end, Iceland (not included in the replacement rate analysis), Finland and Sweden show evidence of complementarity in terms of pension spending. Finland is an anomalous case insofar as replacement rate data (tentatively) suggest a trade-off, whereas pension spending data suggest complementarity. The United States is extremely unusual in that controlling for the variables in our base model inverts the sign (negative in the bivariate model, positive after controls). US pension spending was highly stable over this period, so this instability may reflect the lack of a clear relationship.

14 The negative relationship between pensions and mortgage debt suggests the possibility of a trade-off between mortgage debt (in addition to or rather than homeownership) and social policy (Prasad Citation2012). However, we strongly suspect that such an analysis requires treating policy as the causal variable (as Prasad does), requiring an analytical framework that does beyond the scope of this paper.

15 After analysing the relationship between country slopes and public and private debt separately, we decided to pool both forms of debt in . This results in a better fit, suggesting that different forms of debt may be substitutes.

Related Research Data

References

- Anderson, Karen, and Paulette Kurzer (2019). ‘The Politics of Mortgage Credit Expansion in the Small CMEs’, West European Politics. doi:10.1080/01402382.2019.1596421

- Ansell, Ben W. (2014). ‘The Political Economy of Ownership: Housing Markets and the Welfare State’, American Political Science Review, 108:2, 383–402.

- Armingeon, Klaus, Virginia Wenger, Fiona Wiedemeier, Christian Isler, Laura Knöpfel, David Weisstanner, and Sarah Engler (2018). Comparative Political Data Set 1960–2016. Bern: Institute of Political Science, University of Bern.

- Bafumi, Joseph, and Andrew Gelman (2006). Fitting Multilevel Models When Predictors and Group Effects Correlate. Available at SSRN: https://ssrn.com/abstract=1010095.

- Beck, Nathaniel, and Jonathan N. Katz (1995). ‘What To Do (and Not To Do) with Time-Series Cross-Section Data’, American Political Science Review, 89:3, 634–47.

- Bell, Andrew, and Kelvyn Jones (2015). ‘Explaining Fixed Effects: Random Effects Modeling of Time-Series Cross-Sectional and Panel Data’, Political Science Research and Methods, 3:1, 133–53.

- Blackwell, Timothy, and Sebastian Kohl (2018). ‘Historicising Housing Typologies: Beyond Welfare States and Varieties of Capitalism’, Housing Studies. doi:10.1080/02673037.2018.1487037

- Castles, F.G. (1998). ‘The Really Big Trade-off: Home Ownership and the Welfare State in the New World and the Old’, Acta Politica, 33:1, 5–19.

- Castles, F.G., and M. Ferrera (1996). ‘Home Ownership and the Welfare State: Is Southern Europe Different?’, European Society and Politics, 1:2, 163–85.

- Conley, Dalton, and Brian Gifford (2006). ‘Home Ownership, Social Insurance, and the Welfare State’, Sociological Forum, 21:1, 55–82.

- Delfani, Neda, Johan De Deken, and Caroline Dewilde (2014). ‘Home-ownership and Pensions: Negative Correlation, but no Trade-off’, Housing Studies, 29:5, 657–76.

- Doling, John, and Nick Horsewood (2011). ‘Home Ownership and Pensions: Causality and the Really Big Trade-off’, Housing, Theory and Society, 28:2, 166–82.

- Doling, John, and Richard Ronald (2010). ‘Home Ownership and Asset-based Welfare’, Journal of Housing and the Built Environment, 25, 165–73.

- Dryzek, John, and Robert E. Goodin (1986). ‘Risk-sharing and Social Justice: The Motivational Foundations of the Post-war Welfare State’, British Journal of Political Science, 16:1, 1–34.

- Esping-Andersen, Gøsta (1990). The Three Worlds of Welfare Capitalism. Cambridge: Polity Press.

- Feenstra, Robert C., Robert Inklaar, and Marcel P. Timmer (2015). ‘The Next Generation of the Penn World Table’, American Economic Review, 105:10, 3150–82.

- Howard, C. (1997). The Hidden Welfare State: Tax Expenditures and Social Policy in the United States. Princeton: Princeton University Press.

- Huber, Evelyne, and John D. Stephens (2001). Development and Crisis of the Welfare State: Parties and Policies in Global Markets. Chicago: University of Chicago Press.

- Kangas, Olli, and Joakim Palme (2013). ‘Social Rights, Structural Needs and Social Expenditure: A Comparative Study of 18 OECD Countries 1960–2000’, in Jochen Clasen and Nico A. Siegel (eds.), Investigating Welfare State Change: The ‘Dependent Variable Problem’ in Comparative Analysis. Cheltenham: Edward Elgar, 106–29.

- Kemeny, Jim (1981). The Myth of Home Ownership: Private Versus Public Choices in Housing Tenure. London: Routledge.

- Kemeny, Jim (2005). ‘‘The Really Big Trade-Off' between Home Ownership and Welfare: Castles' Evaluation of the 1980 Thesis, and a Reformulation 25 Years on’, Housing, Theory and Society, 22:2, 595–872.

- Kohl, Sebastian (2017). Homeownership, Renting and Society: Historical and Comparative Perspectives. London: Routledge.

- Kohl, Sebastian (2018a). ‘More Mortgages, More Homes? The Effect of Housing Financialization on Homeownership in Historical Perspective’, Politics & Society, 46:2, 177–203.

- Kohl, Sebastian (2018b). ‘The Political Economy of Homeownership: A Comparative Analysis of Homeownership Ideology through Party Manifestos’, Socio-Economic Review. doi:10.1093/ser/mwy030

- Krippner, Greta R. (2011). Capitalizing on Crisis: The Political Origins of the Rise of Finance. Cambridge, MA: Harvard University Press.

- OECD (1985). Social Expenditure 1960–1990: Problems of Growth and Control. Paris: OECD.

- OECD (2018). Social Expenditure Database (SOCX). Available at https://www.oecd.org/social/expenditure.htm.

- Pierson, Paul (2011). The Welfare State over the Very Long Run. edited by ZeS-Arbeitspapier.

- Pollard, Julie (2011). ‘L'action publique par les niches fiscales - l'exemple du secteur du logement’, in Philippe Bezes and Alexandre Siné (eds.), Gouverner (par) les finances publiques. Paris: Sciences Po Les Presses.

- Ponds, Eduard, Clara Severinson, and Juan Yermo (2011). ‘Funding in Public Sector Pension Plans-International Evidence’. National Bureau of Economic Research.

- Prasad, Monica (2012). The Land of Too Much: American Abundance and the Paradox of Poverty. Cambridge, MA: Harvard University Press.

- Schelkle, Waltraud (2012). ‘A Crisis of What? Mortgage Credit Markets and the Social Policy of Promoting Homeownership in the United States and in Europe’, Politics & Society, 40:1, 59–80.

- Schmitt, Carina, Hanna Lierse, Herbert Obinger, and Laura Seelkopf (2015). ‘The Global Emergence of Social Protection: Explaining Social Security Legislation 1820–2013’, Politics & Society, 43:4, 503–24.

- Schwartz, Herman (2012). ‘Housing, the Welfare State, and the Global Financial Crisis: What is the Connection?’, Politics & Society, 40:1, 35–58.

- Schwartz, Herman (2014). ‘Is There a Really Big Trade-Off? Housing, Welfare and Pensions Reconsidered from a Balance Sheet Perspective’. Available at http://www.people.virginia.edu/∼hms2f/trade-off.pdf.

- Schwartz, Herman M., and Leonard Seabrooke (2008). ‘Varieties of Residential Capitalism in the International Political Economy: Old Welfare States and the New Politics of Housing’, Comparative European Politics, 6:3, 237–61.

- Scruggs, Lyle, and James Allan (2006). ‘Welfare-state Decommodification in 18 OECD Countries: A Replication and Revision’, Journal of European Social Policy, 16:1, 55–72.

- SIED (2015). Social Insurance Entitlements Dataset. Stockholm: Swedish Institute for Social Research, Stockholm University.

- Stamsø, Mary-Ann, and Bent Sofus Tranøy (2019). ‘Equality as a Driver of Inequality? Housing Markets as a Threat to the Scandinavian Welfare State’, West European Politics. doi:10.1080/01402382.2019.1612161

- Streeck, Wolfgang (2014). Buying Time: The Delayed Crisis of Democratic Capitalism. London: Verso Books.

- Van Gunten, Tod, and Edo Navot (2018). ‘Varieties of Indebtedness: Financialization and Mortgage Market Institutions in Europe’, Social Science Research, 70, 90–106.

- Vanhanen, Tatu (2007). Index of Power Resources (IPR) 2007 [Dataset]. Finnish Social Science Data Archive. Retrieved from http://urn.fi/urn:nbn:fi:fsd:T-FSD2420.

- von Weizsäcker, Carl Christian (2016). ‘Das Ende der Kapitalknappheit und sein Verhältnis zur Keyneschen Theorie’. List Forum für Wirtschafts-und Finanzpolitik.

- Western, Bruce (1998). ‘Causal Heterogeneity in Comparative Research: A Bayesian Hierarchical Modelling Approach’, American Journal of Political Science, 42:4, 1233–59.

- Yi, Kei-Mu, and Jing Zhang (2017). ‘Understanding Global Trends in Long-run Real Interest Rates’, Economic Perspectives, 41:2, 2–20.

- Young, Andrew T., Matthew J. Higgins, and Daniel Levy (2008). ‘Sigma Convergence Versus Beta Convergence: Evidence from US County‐Level Data’, Journal of Money, Credit and Banking, 40:5, 1083–93.