Abstract

In this article, I analyse challenges to manufacturing-led development in the Global South in the context of digitalisation. I look at three phenomena in particular: (1) the rise of digital services as an alternative to manufacturing in achieving economic development; (2) the impact of digital automation technologies on job creation in the manufacturing sector; (3) manufacturing-led development in the context of digital and global value chains. I make two important arguments. The first argument is that the rise of digital services or digital automation technologies do not require a serious reformulation of manufacturing-led development strategies. The second argument is that the expansion of digital and global value chains are empowering transnational corporations headquartered in the North at the expense of industrialisation in the South. Industrial policy and international politics can play a part in mitigating the challenge underscored by my second argument. At the national level, the establishment of state-owned enterprises is a good alternative to development strategies that rely purely on linking up to transnational corporations. At the international level, we need change within organisations that enforce rules of trade in favour of the North, and we need to support agreements and initiatives established by and for the South.

Introduction

The digital age, in this article, refers to two developments in the realm of digital technology that are ongoing but started at different points in time. The first development is the shift from mechanical and analogue electronic technology to digital electronic technology, starting approximately in the 1970s. Sometimes referred to as the ‘digital revolution’ or the ‘third industrial revolution’, the most obvious manifestation of this shift is the use of digital computers and related advances in information and communication technology (ICT), like the massive expansion of the internet (OECD Citation2017). The second development is more recent, and refers to technologies within more specific domains, such as (in alphabetical order) additive manufacturing, advanced robotics, artificial intelligence, big data analytics, cloud computing, industrial internet-of-things and machine learning (see UNIDO (Citation2019) for a typology of these technologies and how they are used in production). This group of technologies, and the merging of these technologies with one another and with other digital technologies, is sometimes referred to as the ‘fourth industrial revolution’ (Andreoni, Chang, and Labrunie Citation2021; Schwab Citation2016).

This article analyses challenges to manufacturing-led development in the Global South in the context of both the third and the fourth industrial revolutions. I look at three phenomena in particular: (1) the rise of digital services as an alternative to manufacturing in achieving economic development; (2) the impact of digital automation technologies on the job-creating potential of the manufacturing sector; and (3) manufacturing-led development in the context of digital and global value chains (GVCs). These developments may or may not call for a reorientation of how we, as a community of scholars and policy stakeholders, think about industrialisation pathways, manufacturing-led development and industrial policy in the Global South. The aim of this article is to help shape this reorientation.

I make two important arguments in this article. The first argument is that digital technology, in a direct and explicit sense, does not call for a drastic reformulation of manufacturing-led development strategies or industrial policy in the Global South. ‘Direct and explicit’ refers here to the first two phenomena in the above paragraph, asking whether digital services are replacing manufacturing as an engine of productivity growth and trade, and whether digital automation technologies are threatening the manufacturing sector’s potential for job creation. I will show how, in the process of economic development, manufacturing remains the central engine for productivity growth, international trade and employment creation.

The second important argument I make in this article is that digital technology, in an indirect and implicit sense, does pose a challenge to manufacturing-led development in the Global South. It does so by expanding the global reach and power of transnational corporations headquartered in the Global North at the expense of manufacturing firms and workers in the Global South. I will show how the expansion of GVCs has enabled a small number of large transnational corporations – mostly based in the Global North – to appropriate increasing shares of profits over a larger market. This appropriation is fortified by technological dominance, strong protection of intellectual property rights particularly in digital production technologies, low trade barriers, and privileged access to low-cost capital and labour all over the world. I will show especially how digital technology plays into and reinforces this, both through enabling the expansion of GVCs, and because of how asymmetric power relations are rampant in digital industries and value chains.

The following three sections address the three topics of concern to the article in turn, as they relate to industrialisation pathways and manufacturing-led development in the Global South. In the very last section, I discuss implications for industrial policy and international politics.

Are (digital) services a feasible alternative to manufacturing-led development in the Global South?

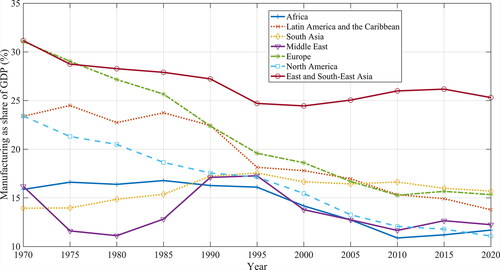

Historically, the process of economic development has been associated with a process of industrialisation, specifically through developing and expanding the manufacturing sector. This is why many of the seminal theories within the field of development economics focus on the importance of manufacturing for the process of economic development (see Hauge and Chang (Citation2019) for a list of economists associated with these seminal theories). But a snapshot of countries’ national accounts around the world reveals that the size of the manufacturing sector is shrinking almost everywhere. This is not only happening in countries that have already built up a competitive manufacturing sector – some level of de-industrialisation seems inevitable for most high-income countries – it is also happening in countries in the Global South with low levels of manufacturing output. In fact, since the 1970s, most regions in the world have seen a decline in the share of manufacturing (see ) and a rise in the share of services in their total economic output. While scholars have highlighted the importance of services for economic development for some time now (see for example Baer and Samuelson (Citation1981) and Bhagwati (Citation1984)), only in recent years has the literature on this started to grow fast, highlighting the increased potential of services to be catalysts for trade, innovation and productivity growth (Baldwin and Forslid Citation2020; Ghani and O’Connell Citation2014; Hallward-Driemeier and Nayyar Citation2017; International Monetary Fund Citation2018; Loungani et al. Citation2017; Miroudot and Cadestin Citation2017; Owusu, Szirmai, and Foster-McGregor Citation2020; WTO Citation2019). In fact, service-oriented development strategies are already showing some promise in countries in the Global South, such as India and Rwanda (as discussed by, for example, Behuria and Goodfellow Citation2019; Ghani and Kharas Citation2010; Hauge and Chang Citation2019; Kleibert and Mann Citation2020). This increased potential for services to contribute to economic development relates to digital technology on several levels. In the following, I will elaborate on how exactly, focusing on the two most important areas: (1) the increased productivity growth and innovation potential of services, especially digital ones; and (2) the increased tradability of services, which is largely due to advances in digital technology.

Figure 1. Manufacturing as a share of gross domestic product (GDP) in world regions, 1970–2020. Source: UNCTAD Statistics Database.

Developments in digital technology, specifically ICT, are making economies of scale more easily achieved in a range of services and making it more profitable to procure some services from specialist providers rather than provide them within a manufacturing firm (Hallward-Driemeier and Nayyar Citation2017; Hauge and Chang Citation2019; Nayyar Citation2013). Many digital service operations now have higher productivity growth potential than manufacturing operations. Think, for example, about software-related services: fixed assets are costly (for example, server farms, cooling systems, secure sites and so on), just as with manufacturing operations, but costs rapidly decrease with scale as the services are sold around the globe in a flash. In fact, the World Trade Organization (WTO) finds that total-factor productivity growth of services within the ICT segment has been higher than that in the manufacturing sector in four of the world’s largest economies during 2005–2015 (WTO Citation2019).Footnote1 Sector data on research and development (R&D) expenditure shows a similar trend: on a global scale, R&D expenditure in services increased from an annual average of 6.7% of total business R&D during 1990‒1995 to 17% during 2005‒2010 (WTO Citation2013).

The spread of the internet, digitalisation and low-cost telecommunications is also making many services more tradable, such as distribution services, financial services, computer services and R&D services (Hauge and Chang Citation2019; WTO Citation2019). The WTO’s flagship report in 2019 on trade in services provides important data on this development, stressing three points: (1) in the period 2005–2018, the growth of world trade in services was higher than the growth of world trade in goods; (2) since the mid-1990s, service-sector employment as a share of global total employment has steadily been increasing; and (3) services make up an increasing share of world exports in terms of value added (WTO Citation2019).Footnote2 This last point is important, especially as it relates to the role of services embedded in manufacturing processes. Using a GVC framework in a sample of 31 advanced economies (mostly economies in the Organisation for Economic Cooperation and Development (OECD)), Miroudot and Cadestin (Citation2017) find that services account for 37% of the value in exports by manufacturing firms. They also find that, across these countries, between 25% and 60% of employment in manufacturing firms is found in service functions such as R&D, engineering, transport, logistics, distribution, marketing, sales, after-sale services, ICT, management, administration and back-office support.

Countries in the Global North are dominating trade in services, but the share of global trade in services in the Global South is increasing (WTO Citation2019). India is the most prominent example, where export growth of ICT services is closely associated with the increase in economic growth since the 1990s (McMillan, Rodrik, and Sepulveda Citation2017). In fact, India has become the world’s largest exporter of ICT services, with exports in this category reaching $136 billion in 2019 (Statista Citation2021). This increase in exports is not only due to more services being ‘produced’, but also due to increasing productivity of India’s services. According to WTO (Citation2019), productivity growth in India’s ICT services has been higher than all other economic sub-sectors – including manufacturing – every year between 2005 and 2015. Hyderabad, the capital of Telangana, is hailed as the prime example of services-led growth in India, where its ICT cluster has earned the nickname ‘Cyberabad’.

Countries in the Global South that are formulating industrial policy plans need to take into account the increased potential of services to be drivers of productivity growth, innovation and trade. However, for a number of reasons, services have not yet reached the potential of traditional manufacturing as a driver of economic development.

First, throughout the history of capitalism, almost all countries that have transformed their economies from low to high income have done so through a process of developing their manufacturing capabilities (Hauge and Chang Citation2019). Although services have become a more important source of economic growth since the mid-1900s, the correlation between industrialisation and long-term economic growth remains remarkably strong. According to a study of ‘growth miracles’ by the World Bank in 2008, only 13 countries in the world were able to sustain an annual growth rate of 7% or higher since 1950. Only two countries, both with small populations and highly idiosyncratic economic structures – Botswana and OmanFootnote3 – are among the group of 13 that have not grown on the basis of manufacturing-led development (Commission on Growth Citation2008). A more recent study looking at a sample of 63 countries between 1990 and 2011 found that manufacturing output growth stimulates economic growth and productivity growth, particularly in developing countries (Marconi, de Borja Reis, and de Araújo Citation2016). The relationship between growth of the manufacturing sector and sustained economic growth has in fact been documented as robust by many more scholars (see, for example, Andreoni and Chang Citation2016; McMillan and Rodrik Citation2011; Nayyar Citation2013; Szirmai Citation2009; Szirmai and Verspagen Citation2015). This is why the terms ‘industrialised country’ and ‘developed country’ are often used interchangeably.

Second, while services have increased their potential for productivity growth, much of this productivity growth potential comes from the manufacturing sector. The theory of productivity ‘spillovers’ from manufacturing to other sectors of the economy was actually spelled out as early as the 1960s by Nicholas Kaldor, in the third of his three classic growth laws, which today are considered the theoretical foundations of manufacturing as the engine of economic growth (Kaldor Citation1966). For contemporary examples of this law, think about how the world’s most productive service economies rely on top-tier computer technology, transport equipment and, in some instances, mechanised warehouses.

Third, many measurement issues put into question the supposed increase of services as a share of global economic output. For example, Haraguchi, Cheng, and Smeets (Citation2017) argue that the manufacturing sector’s value added and employment contribution to world gross domestic product (GDP) and employment, respectively, has not changed significantly since 1970. They find that the declining share of manufacturing in most of the world’s economies over the past few decades is simply a result of the relocation of manufacturing to a small number of economies, led by China. In other words, China is ‘taking over’ most of the world’s manufacturing production. Additionally, many services that used to be provided in-house in manufacturing firms (for example, delivery, catering, security guards, design, programming, marketing, analytics and so on) are now supplied by independent service companies (Chang Citation2014). This has resulted in the reclassification of many activities from manufacturing to services, without an actual corresponding change in countries’ production structures. More importantly, we should question whether manufacturing-related services, like R&D, industrial design and product testing – all of which require engineering know-how – should even be counted as services (Hauge and O’Sullivan Citation2019), which they currently are in most countries’ industrial classification systems.

Fourth, while services do play a more important part in international trade, services have only marginally increased their tradability in the last few decades. According to World Bank data, world trade in services as a share of total world trade only increased from 20% in 1980 to 24.5% in 2020 (World Development Indicators Citation2021). India, despite experiencing an export boom in services, still has a trade deficit, because its trade surplus in services covered only 53% of its trade deficit in goods in 2020 (World Development Indicators Citation2021).

In summary, the digital age has enabled a wider range of services to be catalysts of trade, productivity growth and innovation. In turn, this change in ‘the source’ of economic development has important implications for industrial policymakers, whose responsibility it is to target those economic activities with the highest potential for long-term productivity growth and economic development. But we need to approach the pro-services discourse with a dose of scepticism: this section presented a range of evidence showing that manufacturing is in most instances the main driver of productivity growth and economic development (see for a summary of key points).

Table 1. The role of services as drivers of trade, innovation and productivity growth: key arguments and counterarguments.

That being said, we should keep in mind that this distinction between the economic development potential of manufacturing and services is not the ultimate issue we should be concerned with. Ultimately, we should be concerned with raising productivity and real incomes in a sustainable way, which, in practice, implies supporting technologies, tasks and capabilities embedded within a variety of sectors and clusters. As Schlogl (Citation2020, 8) correctly highlights, the key issue for industrial policymakers is identifying the quality and value-adding capacity of specific economic activities rather than specific (and at times arbitrarily defined) sectors of the economy.

Are digital automation technologies threatening manufacturing-led development in the Global South?

Another development that questions the efficacy of traditional industrial policy – targeting growth of the manufacturing sector – is the impact of automation technologies on manufacturing jobs. There are growing fears that new automation technologies will start displacing jobs at a faster rate than they have in the past (Brynjolfsson and McAfee Citation2014; Chang, Rynhart, and Huynh Citation2016; Frey and Osborne Citation2017; Schwab Citation2016). Some studies highlight that manufacturing jobs (or job creation in the manufacturing sector) in the Global South are particularly at risk (Frey and Rahbari Citation2016; Hallward-Driemeier and Nayyar Citation2017; Manyika Citation2017; Schlogl and Sumner Citation2020). In the context of this article, this is an important issue to study seeing that job creation within the manufacturing sector has historically been an essential part of industrialisation and economic development (Amsden Citation1989, Citation2001).

Many recent studies on automation’s impact on jobs focus on digital automation technologies, so it is easy to forget that automation technologies have been around for a long time. We have to go all the way back to 1785 to find the first completely automated industrial process: a flour mill developed by Oliver Evans (Andreoni and Anzolin Citation2019). Fears of the job-displacing impact of technology date back almost as far. In the early 1800s, textile workers in Nottingham, Great Britain, established a secret oath-based organisation devoted to destroying machines that they feared would replace them (an organisation that became famously known as the Luddites). Over time, such fears of job losses have been proven mostly unfounded (Autor, Dorn, and Hanson Citation2015; Muro, Maxim, and Whiton Citation2019). Even with respect to restructuring of the labour force, which tends to happen over time regardless of fluctuations in employment levels, changes have been more modest than what many people think. For example, Bessen (Citation2016) found that out of the 270 occupations in the 1950 US census, 232 of them (86%) still exist today; 37 of them disappeared because of either changes in consumer demand or technological obsolescence. Only one occupation disappeared due to automation: elevator operators.

However, some scholars argue that this time things will be different, especially because of advances in artificial intelligence. Previously, computer-based automation was limited by the need to be able to programmatically describe/codify every operation that needed to be done (ie step-by-step instructions). This made it difficult for automation to be used in applications that involve abstract thinking or manual adaptability and situational awareness, including both high-skilled jobs (like creative design) and low-skilled manual jobs (like housework) (Autor, Dorn, and Hanson Citation2015). Today, new methods in machine learning, a sub-field of artificial intelligence, are enabling digital systems to independently learn and apply rules to achieve specified outcomes. It is believed that this, combined with the miniaturisation of computers, increased computing power and continuous data collection through the internet-of-things, will allow work in many different industries to be automated in a short time frame (Acemoglu and Restrepo Citation2020).

If we look at forecast studies that predict the impact of automation on employment in the future, the first and most important thing to note is that their estimates vary widely (see for a compilation of key studies). For example, Frey and Osborne (Citation2017) estimate that 47% of workers in the US are at high risk of losing their jobs to automation over the next two decades, whereas Arntz, Gregory, and Zierahn (Citation2016) find that only 9% of workers in the US (and 6–12% of workers in all OECD countries) are at high risk of losing their jobs to automation. The global consultancy firm McKinsey estimates that 60% of all occupations in the world contain at least 30% technically automatable activities – although this study does highlight that automation is more likely to lead to restructuring of the labour force rather than large-scale unemployment (Manyika et al. Citation2017). In developing countries, the World Bank estimates that two-thirds of all jobs are susceptible to automation (World Bank Citation2016), but like the McKinsey study, they caution against equating automatability with unemployment. Chang, Rynhart, and Huynh (Citation2016) find that in the case of the ASEAN-5 countries (Cambodia, Indonesia, the Phillippines, Thailand and Viet Nam), 56% of all jobs are at high risk of automation, 32% of all jobs are at medium risk of automation, and only 12% of all jobs are at low risk of automation. According to the McKinsey study referred to above, manufacturing is in the top three automatable activities, particularly low-skilled manufacturing in the Global South. It is important to emphasise that many of these forecast studies look at automatability of occupations/tasks rather than the impact on unemployment. Extrapolating from automatability to unemployment levels is a big leap. This is why studies like the World Bank (Citation2016) and Manyika et al. (Citation2017) caution against such extrapolation.

Table 2. Estimates of automatability of jobs in key studies.

There is in fact strong support for the hypothesis that aggregate employment levels will not be impacted much in the future by new automation technologies. The first reason for this is the positive impact automation technologies have had and are still having on productivity growth. James Bessen’s work on automation is important in this respect. In a recent paper, he points out that during the first industrial revolution, machines automated over 90% of human work in the textile industry. However, prices in the industry rapidly decreased due to productivity growth, increasing demand for clothes, which in turn increased demand for weavers in factories (Bessen Citation2016). In a recent study of the South African apparel industry, Christian Parschau and I found that most firms that have implemented new automation technologies have increased employment levels, largely due to the positive effect these technologies have had on within-firm productivity growth (Parschau and Hauge Citation2020). While some studies report short-term spikes in unemployment in response to ‘technology shocks’, mid- and long-term effects are generally found to be positive (Kim, Lim, and Park Citation2010; Manyika et al. Citation2011; Mokyr, Vickers, and Ziebarth Citation2015).

The second reason for the strong support behind the hypothesis that aggregate employment levels will not be impacted significantly by new digital automation technologies in the near future is the many barriers that exist to implementing these automation technologies, particularly in labour-intensive industries in the Global South. For example, UNCTAD (Citation2017, 39) states that, ‘Most existing studies overestimate the potential adverse employment and income effects of robots, because they neglect to take into account that what is technically feasible is not always also economically profitable’. The report by UNCTAD identifies many industries where this is the case: ie industries that display automation potential from a technical standpoint but not from an economic standpoint. The report highlights especially the textile industry and the food industry because automation technology cannot compete with the low cost of labour in those industries. A number of additional barriers to implementing automation technologies exist in the Global South, such as a lack of trained maintenance people, a lack of access to capital and an unreliable energy infrastructure (Parschau and Hauge Citation2020).

Regarding this last point, a possible counterargument would be that jobs lost to automation in countries in the Global South would not actually happen in these countries; it would mostly occur because of reshoring. This refers to a process whereby high-income countries ‘withdraw’ previously offshored production because of the availability of new automation technologies in their own countries. However, while evidence shows that reshoring does occur (Tate Citation2014), it is on a small scale (Dachs et al. Citation2019), in fact on a smaller scale than new offshoring activity (Kinkel, Dewanti, and Zimmermann Citation2017).

In summary, while new digital automation technologies have the potential to displace jobs faster than in the past, many of the forecast studies that predict large job losses lose sight of the fact that automatability of occupations/tasks does not equate with rising unemployment, especially because automation technologies have historically created jobs as well as displaced them. A restructuring of the labour force is therefore a more realistic outcome than large-scale unemployment. Additionally, many activities that are technically feasible to automate are not economically feasible to automate, particularly activities in those industries where labour is still cheap. However, it is important to highlight that impacts across countries and industries are and will continue to be widely different. For example, in the US, advances in automation technology and artificial intelligence have undeniably played a role in stagnating labour demand, declining labour share in national income, and rising inequality (Acemoglu and Restrepo Citation2020). Clearly, restructuring the labour force does not come without costs, and will not be smooth unless managed properly. Policy has an important role to play in designing education and training policies that facilitate occupational transitions, manage adjustment costs and more broadly ‘reskill’ the labour force (Bechichi et al. Citation2019) Finally, any prediction – optimistic or pessimistic – about long-term socio-economic change should be read with caution due to the highly uncertain nature of how social and economic change unfolds in the long term. For example, while this section presented evidence that reshoring to the Global North so far is not stealing jobs from the Global South, we cannot exclude the possibility that reshoring will increase as more of the available automation technologies are rolled out for commercial use.

Does the expansion of digital and global value chains help or hinder manufacturing-led development in the Global South?

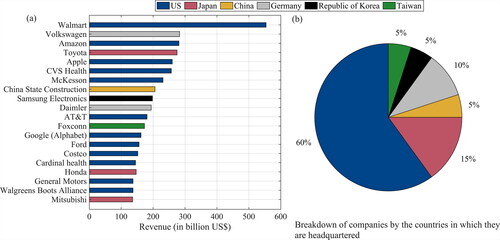

Since the early 1990s, production processes have become increasingly globally fragmented, borderless and interconnected, giving rise to the concept of GVCs. The expansion of GVCs is a result of many factors, including lowered trade barriers and reduced transport costs, but rapid advances in ICT is arguably the most important one. Cheaper and more reliable telecommunications, information management software and increasingly powerful computers have decreased the cost of organising and coordinating complex activities over long distances, both within and between companies (Baldwin Citation2016; OECD Citation2013). Advances in digital technology have also increased the tradability of many production-related services, such as data entry and information processing. Moreover, lead firms are able to outsource more of their production with the help of sophisticated software that can digitally track inputs and outputs in the production process (Raj-Reichert, Zajak, and Helmerich Citation2021; Azmeh and Nadvi Citation2014). The expansion of GVCs is not only aided by digital technology, it is also part and parcel of an expansion in power, in reach and of profits of large digital firms. As can be seen from , seven of the 20 largest companies in the world, excluding energy and finance/insurance companies, are companies that sell digital hardware/software/services or rely almost exclusively on digital platforms to sell their products.

Figure 2. (a) Top 20 revenue-generating companies in 2020, excluding energy and finance/insurance companies. Seven of these companies are digital, in that they sell digital hardware/software/services or rely almost exclusively on digital platforms to sell their products. These are, in order of revenue generation: Amazon, Apple, McKesson, Samsung, AT&T, Foxconn and Google (Alphabet). (b) Breakdown of all companies by countries they are headquartered in. Source: Author’s compilation based on Fortune 500 in 2020.

The expansion of GVCs has important implications for economic development, as it is enabling countries in the Global South to participate in the global economy on an unprecedented scale. In the years since the 1990s, countries in the Global South have significantly increased their share of global exports (UNCTAD Citation2020), global foreign direct investments (Hauge Citation2020) and global trade in value added (World Bank Citation2020). Given this opportunity for countries in the Global South to participate in global production systems on a larger scale, manufacturing-led development and industrial policy in the Global South in the context of GVCs is drawing more interest (Baldwin Citation2011; Citation2016; Hauge Citation2020; Kaplinsky and Morris Citation2016; Milberg, Jiang, and Gereffi Citation2014; Morris and Staritz Citation2019; Taglioni and Winkler Citation2016; World Bank Citation2020).

The expansion of GVCs has both positive and negative impacts on manufacturing-led development in the Global South. Among the positives are the benefits of integrating into the world economy through increasing trade and inflows of foreign direct investment. This can boost employment, increase foreign exchange and tax revenues, boost infrastructure development, enhance the skills of the local workforce, and support technological transfer and spillovers from foreign firms to the domestic economy (Farole and Winkler Citation2014; OECD Citation2002; Taglioni and Winkler Citation2016; World Bank Citation2020). Another positive development is that, in the age of GVCs, countries can join value chains and supply chains rather than build them from scratch (Baldwin Citation2011, Citation2016; Cattaneo et al. Citation2013; OECD Citation2013). In other words, GVCs are making it relatively easier for countries in the Global South to develop certain industrial capabilities, as these countries now have the opportunity to specialise in particular segments of an industry (stages of production, tasks or business functions) without needing to have all the ‘upstream’ capabilities in place. This means that developing countries can start exporting sophisticated products more quickly at a lower cost. China is a very good example of a country that has reaped the benefits of this opportunity. The country’s success in exporting manufactured goods largely reflects strategic participation in GVCs, relying on a high share of imported inputs in its exports before starting to increase domestic content in exports (OECD Citation2013; World Bank Citation2020).

While the expansion of GVCs is accompanied by opportunities for economic development and industrialisation, the dark side of this expansion, largely ignored in publications by the mainstream international development community (as argued, for example, by Selwyn and Leyden Citation2021; Bair et al. Citation2021), needs to be highlighted. From the perspective of the Global South, the criticism of GVCs – or, in some cases, more subtle ‘warnings’ about GVC participation – has been mounting. This criticism most importantly underscores the oligopoly-driven structure of GVCs and asymmetric power relations within GVCs (Anner Citation2020; Milberg and Winkler Citation2013; Nolan, Zhang, and Liu Citation2007; Pagano Citation2014; Selwyn and Leyden Citation2021; Selwyn Citation2019; Slaughter Citation2010; Starrs Citation2014; Suwandi Citation2019; Wade Citation2019). In essence, large and powerful transnational corporations – mostly headquartered in the Global North – often use their growing dominance and power in the global economy to squeeze and minimise the profits of firms and wages of labour in the Global South. According to Kvangraven (Citation2021), the rise of GVCs in many ways restates the relevance of dependency theory. This is a theory first introduced many decades ago, postulating that poor states are impoverished by the way they are integrated into the world system through a relationship of unequal economic exchange with wealthy states.

As mentioned, the expansion of GVCs has been enabled by advances in digital technology. Referring to also highlighted that many of the largest companies in the world today are companies that sell digital hardware/software or rely almost exclusively on digital platforms to sell their products. We further see from that the headquarters of the world’s largest companies, including the digital ones, are highly concentrated in the US. In fact, only one company on this list is headquartered in a middle- or low-income country: China State Construction. And that’s stretching it, as China is about to graduate into high-income status. This global dominance of transnational corporations based in the Global North (‘lead’ firms, in GVC jargon) has been documented more broadly. Nolan, Zhang, and Liu (Citation2007) show that a handful of firms, mostly based in the Global North, have accounted for 50% or more of the market share in practically every global industry since about 2000. Starrs (Citation2014) show that companies from the US have the leading profit shares among the world’s top 2000 firms in 18 of 25 sectors. Slaughter (Citation2010) points out that the income collected by US-based transnational corporations from their foreign affiliates increased from 17% in 1977 to 49% in 2006, measured as a share of their total worldwide net income.

According to Selwyn (Citation2017, 54), the global manufacturing system has become ‘a structure through which lead firms seek to enhance their global positions and strategies for extended capital accumulation and profit maximisation in relation to supplier firms, would-be competitor firms, and labouring classes’. This dominance of large, transnational and often digital companies extends beyond the traditional metrics of measuring the power of firms in the world economy. For example, Zuboff (Citation2019) outlines the unprecedented opportunities by powerful transnational corporations to predict and control our behaviour due to the vast increase in the amount of data they are able to collect from us. In the context of the Global South, Mann (Citation2018) shows how, as African countries become increasingly digital, data will become a source of power in economic governance. Even data extraction from African countries that is justified on the basis of humanitarian assistance and development, Mann shows, allows transnational corporations to advance their strategy of becoming data custodians of Africa’s economies.

While firms based in the Global North are often the ones that walk away with windfall profits in global manufacturing, they are rarely the ones who make the products. Digital manufacturing industries are no exception. The electronics industry, one of the world’s largest consumer industries, is a good case in point. According to Wade (Citation2019), China accounts for only 3% of global profits in the electronics sector, despite being the world’s largest exporter of electronics. The US, by comparison, accounts for 33% of global profits in the electronics sector, while not exporting nearly as many manufactured electronics goods as China. Why is this? Part of it can be explained by the global control and power that US firms have amassed over the years, as already shown. Among other things, this allows powerful lead firms to push down prices of supplies/inputs to marginal cost, and thus extract the full profits from the sales of the final goods, known as the ‘mark-up effect’ (Milberg Citation2008). Milberg and Winkler (Citation2013) document how the price of manufactured goods imports into the US declined steadily relative to US consumer prices between the 1980s and the 2000s, in some instances by more than 40%.

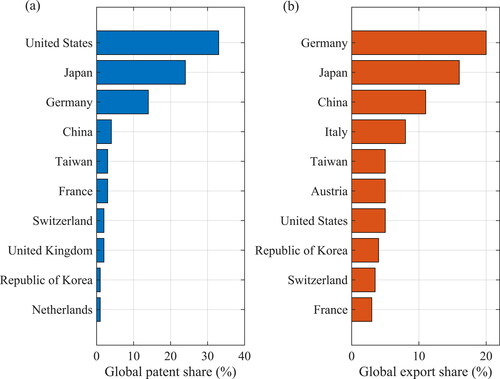

Another explanation for this unequal distribution of value is patent protection. Pagano (Citation2014) and Wade (Citation2019) argue that knowledge monopolies and patent protection concentrated among transnational corporations are driving intense concentration of corporate wealth and power, thereby holding back catch-up by the Global South. This is especially true for digital technologies. As seen from , the discrepancy between patent protection and export activity in advanced digital production technologies in the US is massive: patent protection is ripe, while export activity relatively low. In China, this discrepancy is also massive, but in the other direction: patent protection is low, and export activity is high. This is clearly an unequal distribution of global patents. This injustice is exacerbated by the agreement on Trade-Related Aspects of Intellectual Property Rights (TRIPS) within the WTO (Wade Citation2019), an agreement that prevents the transfer of intellectual property and technology to the Global South.

Figure 3. (a) and (b) depict the world-leading countries in global patents and global exports, respectively, in advanced digital production technologies. Panel (a) refers to the cumulative number of global patent families in the last 20 years. Panel (b) refers to the average export values of capital goods associated with advanced digital production technologies for 2014–2016. Source: UNIDO (Citation2019).

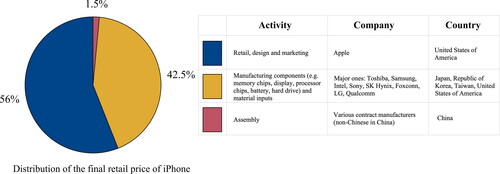

The iPhone is a telling example of the unequal distribution of value in a global digital industry. In have calculated the average distribution of value for iPhones released between 2010 and 2018. The figure is nothing short of shocking. Throughout practically every new iPhone release, Apple has been raking in 56% of the final retail price (on average) without actually producing or assembling any of the components; 1.5% of the final retail price goes to the most labour-intensive part of the production stage – assembly – mostly carried out in China. This value squeeze on labour also explains the dire working conditions in the global electronics industry and most other global manufacturing industries, evidenced by wages below the social reproduction wage, excessive overtime work and damaging health conditions (Anner Citation2020; Chan Citation2013; Mezzadri Citation2016; Selwyn Citation2019; Selwyn and Leyden Citation2021).

Figure 4. Distribution of the final retail price of the iPhone by activity, company and country (see table, on the right side of the figure, corresponding to each colour). It represents the average of the value distribution of three iPhone models in their year of release, between 2010 and 2018 (iPhone 4, iPhone7, iPhone X). Source: Author’s calculation based on Kraemer, Linden, and Dedrick (Citation2011), Dedrick, Linden, and Kraemer (Citation2018) and Jourdan (Citation2018).

In summary, while the expansion of GVCs is accompanied by some opportunities for countries in the Global South to integrate into the world economy in a beneficial manner, it also comes with massive challenges. In this section, I have showed how the expansion of GVCs has enabled a small number of large transnational corporations – mostly based in the Global North – to appropriate increasing shares of profits over a lager market. This appropriation is fortified by technological dominance, strong protection of intellectual property rights, low trade barriers and privileged access to low-cost capital and labour all over the world. I also showed how digital technology plays into and reinforces this, both through enabling the expansion of GVCs, and because of how asymmetric power relations are rampant in digital industries and value chains. This era of dominance by transnational corporations based in the Global North has (1) made it harder for countries in the Global South to break into higher-value-added industries and stages of production in value chains, and (2) reduced the value and profits of many manufacturing activities that already take place in many countries in the Global South, which has detrimental impacts for firms and workers in these countries. This second development is exacerbated by an increasingly competitive environment in global manufacturing between countries in the Global South. In the following section, I will discuss the implications of these developments for industrial policy and international politics, with respect to both the analysis in this section and the analysis carried out in the article as a whole.

What are the implications for industrial policy and international politics?

In this article, I discussed challenges to manufacturing-led development in the Global South in the context of digitalisation. Two important arguments emerge from my analysis. The first argument is that digital technology, in a direct and explicit sense, does not call for a drastic change to manufacturing-led development strategies in the Global South. ‘Direct and explicit’ refers here to the first two questions I explored, asking if digital services are replacing manufacturing as an engine of productivity growth and trade, and asking if digital automation technologies are threatening the manufacturing sector’s potential for job creation. I concluded that in the process of economic development, manufacturing still remains the central engine for productivity growth, international trade and employment creation.

There are, of course, caveats to this argument. It is important that industrial policymakers recognise the increasing potential of digital services to drive productivity growth, trade and economic development. Ultimately, the key issue for industrial policymakers is to identify the quality and value-adding potential of specific economic activities rather than specific sectors of the economy. With respect to automation’s impact on job displacement, it might well be that when digital automation technologies become commercially available more widely and more rapidly, the relationship starts to change: automation technologies could displace more jobs in more manufacturing sub-sectors in the future. Another issue is that the lack of adoption of digital automation technologies in the Global South, and digital technologies at large, has created a digital divide between the Global South and the Global North (see for example Banga and Te Velde Citation2018). Seeing that economic development is a process of technological development, advanced economies’ first-mover advantages in the area of digital technologies and the fourth industrial revolution implies that the technological capability gap between the South and the North can increase.

The second argument emerging from my analysis is that digital technology, in an indirect and implicit sense, does pose a challenge to manufacturing-led development in the Global South. It does so by expanding the global reach and power of transnational corporations headquartered in the Global North at the expense of manufacturing firms and workers in the Global South. I showed how the expansion of GVCs has enabled a small number of large transnational corporations – mostly based in the Global North – to appropriate increasing shares of profits over a larger market. This appropriation is fortified by technological dominance, strong protection of intellectual property rights particularly in digital production technologies, low trade barriers and privileged access to low-cost capital and labour all over the world. I showed especially how digital technology plays into and reinforces this, both through enabling the expansion of GVCs, and because of how asymmetric power relations are rampant in digital industries and value chains.

In this era of GVCs, how can countries in the Global South implement industrial policies to overcome this divide? One strategy is to link up to transnational corporations and lead firms often headquartered in the North, finding niche industrial activities that add value and employment, using this as a springboard for further industrialisation (Baldwin Citation2011; Taglioni and Winkler Citation2016; World Bank Citation2020). I highlighted how China’s industrialisation success has partly relied on such a strategy. However, this strategy runs into problems most of the time because transnational corporations have incentives to prevent developing countries from breaking into higher-value-added industries and stages of production in value chains. As I documented, the profits of GVC-based digital manufacturing activities carried out in developing countries, even in China, are being massively squeezed.

An alternative strategy is the establishment of state-owned enterprises. In their review of the role of the state in GVCs, Horner and Alford (Citation2019) actually highlight state-owned enterprises as a research area that the literature on GVCs has neglected. An important rationale for establishing a state-owned enterprise is that the government has the best ability to take on investment projects that involve high risks for the private sector, but can potentially bring high social returns in the future (Chang, Hauge, and Irfan Citation2016). Historically, issues of national security, economic autonomy from multinational capital, and sufficient control over strategic industries and natural resources have also been key motivations (Nem Singh and Chen Citation2018). In fact, state-owned enterprises are abundant around the world (for a good overview, see Nem Singh and Chen Citation2018), especially in developing countries, where 41 of the top 100 transnational corporations are state-owned (Horner and Alford Citation2019). And one of the world’s fastest growing economies is the heaviest user: In China, 51,000 firms are fully or partially owned by the state (Horner and Alford Citation2019). The importance of state-owned enterprises in the Global South is an indication that there are industrial policy pathways in the era of GVCs that are not confined to carrying out activities on the demands of transnational corporations headquartered in the Global North.

Ultimately, though, we need international cooperation to level the playing field in the global economy. This means that we need to go outside the realm of domestic industrial policy and into the realm of international politics, in particular investigating the practices of international organisations that have power in setting rules of industrial and trade policies. The most important organisation in this respect is the WTO, as nearly all countries in the world have joined this organisation and are therefore subject to rules set by the organisation. The WTO has come under fire for years for protecting the technologies of transnational corporations headquartered in the Global North and for limiting the policy space of countries in the Global South for formulating industrial policies that enable technology transfer and nurture domestic industries (Chang, Hauge, and Irfan Citation2016; Meyer Citation2009; Wade Citation2003; Wade Citation2019; Shadlen Citation2005).

One important part of the system of rules within the WTO is TRIPS, the most comprehensive multilateral agreement on intellectual property to date. In essence, TRIPS ensures that intellectual property (most importantly patents and copyrights) is better protected globally. The idea behind TRIPS is to incentivise more innovation. But the problem with TRIPS is that when innovation is highly skewed globally, it serves to protect the interests of those who are net producers of patentable knowledge (Wade Citation2003, Citation2019). And in the global economy today, the North is a net producer of patentable knowledge, and the South is a net consumer. I showed how this is particularly true for advanced digital production technologies (see ), and how this reinforces a highly unequal distribution of profits in, for example, the global electronics value chain (see ). Clearly, TRIPS limits technology transfer from the Global North to the Global South and generally limits the policy space of countries in the Global South to develop their manufacturing sectors. This is also true for other important agreements within the WTO, which, taken together, prohibit the use of local content requirements on foreign investment and prohibit the use of export subsidies (Chang, Hauge, and Irfan Citation2016) – industrial policy tools that have historically been important for technology transfer and manufacturing-led development.

It is important to understand that it is not ‘employees’ of the WTO who maintain the framework of rules within the WTO. The WTO is composed of member states, and member states vote on rules. In the most powerful sovereign states, like the US, large corporations have immense lobbying power. It is often these large corporations (their owners/shareholders and managers, to be more precise) who benefit from strong protection of intellectual property rights, privileged access to low-cost labour, and extended market access and power. Therefore, pressure to change the set of rules within the WTO is not enough; we also need to put pressure on the US and the EU to implement anti-trust legislation and to decrease the lobbying power of corporations in the political arena.

Given that the most powerful international organisations and the most influential trade agreements have in practice been established by and for countries in the Global North, a different strategy could be for countries in the Global South to offer alternatives. Some notable alternatives are in fact emerging. For example, on the trade front, the Regional Comprehensive Economic Partnership (RCEP) signed by Asia-Pacific nations in 2020 has become the largest trade bloc in history. It is not entirely made up of countries that would be considered part of the Global South, but it certainly does not reflect the WTO’s core–periphery structure. The African Continental Free Trade Area (ACfTA) is another massive trade area, recently created by 54 of the 55 African Union nations. It is the largest free trade area in the world in terms of the number of participating countries since the establishment of the WTO.Footnote4 These trade agreements may not be a magic bullet for all countries that take part in them, but generally, regional and bilateral trade agreements between countries of similar income levels are more beneficial for the countries that take part in them compared to the framework set by the WTO.

Acknowledgements

I would like to thank a number of people who have provided useful feedback on the article and who have helped improve the quality of the article. They include, in alphabetical order, Neeraja Bhamidipati, Carlos Lopez-Gomez, Nicolai Schulz, and Daman Kaur Sethi. I also thank three anonymous reviewers, participants at a workshop organised for this special issue, and the guest editor of the special issue, Jewellord Nem Singh, for providing detailed feedback throughout the review process, which raised the quality of the article. The editorial team at Third World Quarterly also deserves thanks for responding to all queries in a timely manner and for handling the review process in a professional way. Daman Kaur Sethi provided excellent and timely research assistance on the article.

Disclosure statement

There is no conflict of interest to report.

Additional information

Notes on contributors

Jostein Hauge

Jostein Hauge is a political economist and Assistant Professor in development studies at the University of Cambridge. He is also Fellow of the Royal Society of Arts and Associate Fellow of the Higher Education Academy. His recent research has been published in African Affairs, Development Policy Review, Geoforum, Third World Quarterly and World Economy. He also advises on policy issues for governments and international organisations, and has co-authored reports and essays for the UN Economic Commission for Africa, the UN Industrial Development Organization, the World Economic Forum, and the UK Department for Business, Energy, and Industrial Strategy. More information about his research is available at his personal website: www.josteinhauge.com

Notes

1 These four economies are Germany, India, the US and the UK.

2 Data on services trade in WTO (Citation2019) is based on a new experimental data set that includes ‘GATS mode 3’: commercial presence in another country (ie the supply of services through foreign affiliates). It is beyond the scope of this article to critically assess the accuracy of this new data set, but the reader should be alerted to the fact that estimates on services trade from WTO (Citation2019) are much higher than, for example, those of the World Development Indicators (2021).

3 Botswana has amassed its wealth from precious stones (diamonds), while Oman has done so through oil.

4 In this paragraph, I focus on international trade. However, other important initiatives outside the realm of trade have been established that could challenge the hegemony of the Global North in international politics. Two notable ones are the New Development Bank (NDB), established by the BRICS (Brazil, Russia, India, China and South Africa), and the Asian Infrastructure Investment Bank (AIIB), spearheaded by China. While not nearly at the point of being an alternative source of development finance compared to the World Bank and the International Monetary Fund, they are important initiatives that deserve further study.

Bibliography

- Acemoglu, D., and P. Restrepo. 2020. “The Wrong Kind of AI? Artificial Intelligence and the Future of Labour Demand.” Cambridge Journal of Regions, Economy and Society 13 (1): 25–35. doi:10.1093/cjres/rsz022.

- Amsden, A. 1989. Asia’s Next Giant: South Korea and Late Industrialization. Oxford: Oxford University Press.

- Amsden, A. H. 2001. The Rise of "the Rest": Challenges to the West from Late-Industrializing Economies. Oxford: Oxford University Press.

- Andreoni, A., and G. Anzolin. 2019. “A Revolution in the Making? Challenges and Opportunities of Digital Production Technologies for Developing Countries.” Inclusive and Sustainable Industrial Development Working Paper Series 7/2019.

- Andreoni, A., and H. J. Chang. 2016. “Industrial Policy and the Future of Manufacturing.” Economia e Politica Industriale 43 (4): 491–502. doi:10.1007/s40812-016-0057-2.

- Andreoni, A., H. J. Chang, and M. Labrunie. 2021. “Natura Non Facit Saltus: Challenges and Opportunities for Digital Industrialisation across Developing Countries.” The European Journal of Development Research 33 (2): 330–370. doi:10.1057/s41287-020-00355-z.

- Anner, M. 2020. “Squeezing Workers’ Rights in Global Supply Chains: Purchasing Practices in the Bangladesh Garment Export Sector in Comparative Perspective.” Review of International Political Economy 27 (2): 320–347. doi:10.1080/09692290.2019.1625426.

- Autor, D. H., D. Dorn, and G. H. Hanson. 2015. “Untangling Trade and Technology: Evidence from Local Labour Markets.” The Economic Journal 125 (584): 621–646. doi:10.1111/ecoj.12245.

- Arntz, M., T. Gregory, and U. Zierahn. 2016. “The Risk of Automation for Jobs in OECD Countries.” OECD Social, Employment and Migration Working Papers, No. 189.

- Azmeh, S., and K. Nadvi. 2014. “Asian Firms and the Restructuring of Global Value Chains.” International Business Review 23 (4): 708–717. doi:10.1016/j.ibusrev.2014.03.007.

- Baer, W., and L. Samuelson. 1981. “Toward a Service-Oriented Growth Strategy.” World Development 9 (6): 499–514. doi:10.1016/0305-750X(81)90001-2.

- Bair, J., M. Mahutga, M. Werner, and L. Campling. 2021. “Capitalist Crisis in the “Age of Global Value Chains”.” Environment and Planning A: Economy and Space 53 (6): 1253–1272. doi:10.1177/0308518X211006718.

- Baldwin, R. 2016. The Great Convergence. Cambridge, MA: Harvard University Press.

- Baldwin, R. 2011. Trade and Industrialisation after Globalisation’s 2nd Unbundling: How Building and Joining a Supply Chain Are Different and Why It Matters (No. w17716). National Bureau of Economic Research.

- Baldwin, R. E., and R. Forslid. 2020. Globotics and Development. National Bureau of Economic Research.

- Banga, K., and D. W. Te Velde. 2018. Digitalisation and the Future of Manufacturing in Africa. London: Overseas Development Institute.

- Bechichi, N., S. Jamet, G. Kenedi, R. Grundke, and M. Squicciarini. 2019. “Occupational Mobility, Skills and Training Needs.” OECD Science, Technology and Innovation Policy Papers, No. 70, OECD Publishing, Paris.

- Behuria, P., and T. Goodfellow. 2019. “Leapfrogging Manufacturing? Rwanda’s Attempt to Build a Services-Led ‘Developmental State’.” The European Journal of Development Research 31 (3): 581–603. doi:10.1057/s41287-018-0169-9.

- Bessen, J. E. 2016. “How Computer Automation Affects Occupations: Technology, Jobs, and Skills.” Boston University School of Law, Law and Economics Research Paper, 15–49.

- Bhagwati, J. N. 1984. “Splintering and Disembodiment of Services and Developing Nations.” The World Economy 7 (2): 133–144. doi:10.1111/j.1467-9701.1984.tb00265.x.

- Brynjolfsson, E., and A. McAfee. 2014. The Second Machine Age: Work, Progress, and Prosperity in a Time of Brilliant Technologies. New York: WW Norton & Company.

- Cattaneo, O., G. Gereffi, S. Miroudot, and D. Taglioni. 2013. Joining, Upgrading and Being Competitive in Global Value Chains: A Strategic Framework. Washington D.C.: World Bank Publications.

- Chan, J. 2013. “A Suicide Survivor: The Life of a Chinese Worker.” New Technology, Work and Employment 28 (2): 84–99. doi:10.1111/ntwe.12007.

- Chang, H. J. 2014. Economics: The User’s Guide. London: Pelican Books.

- Chang, H. J., J. Hauge, and M. Irfan. 2016. Transformative Industrial Policy for Africa. Addis Ababa, Ethiopia: Economic Commission for Africa.

- Chang, J. H., G. Rynhart, and P. Huynh. 2016. ASEAN in Transformation: How Technology Is Changing Jobs and Enterprises. Geneva: International Labour Organisation.

- Commission on Growth. 2008. The Growth Report: Strategies for Sustained Growth and Inclusive Development. Washington D.C.: World Bank Publications.

- Dachs, B., S. Kinkel, A. Jäger, and I. Palčič. 2019. “Backshoring of Production Activities in European Manufacturing.” Journal of Purchasing and Supply Management 25 (3): 100531. doi:10.1016/j.pursup.2019.02.003.

- Dedrick, J., G. Linden, and K. L. Kraemer. 2018. “We Estimate China Only Makes $8.46 from and iPhone – and That’s Why Trump’s Trade War Is Futile.” The Conversation, 6 July 2018.

- Farole, T. and D. Winkler, eds., 2014. Making Foreign Direct Investment Work for Sub-Saharan Africa: local Spillovers and Competitiveness in Global Value Chains. Washington D.C.: World Bank Publications.

- Frey, C. B., and M. A. Osborne. 2017. “The Future of Employment: How Susceptible Are Jobs to Computerisation?” Technological Forecasting and Social Change 114: 254–280. doi:10.1016/j.techfore.2016.08.019.

- Frey, C. B., and E. Rahbari. “Do Labor-Saving Technologies Spell the Death of Jobs in the Developing World?” Prepared for the 2016 Brookings Blum Roundtable, 2016.

- Ghani, E., and H. Kharas. 2010. “An Overview.” In The Service Revolution in South Asia, edited by E. Ghani. 9–36. Oxford: Oxford University Press.

- Ghani, E., and S. D. O’Connell. 2014. Can Services Be a Growth Escalator in Low-Income Countries? Washington D.C.: World Bank Publications.

- Hallward-Driemeier, M., and G. Nayyar. 2017. Trouble in the Making?: The Future of Manufacturing-Led Development. Washington D.C.: World Bank Publications.

- Haraguchi, N., C. F. C. Cheng, and E. Smeets. 2017. “The Importance of Manufacturing in Economic Development: Has This Changed?” World Development 93: 293–315. doi:10.1016/j.worlddev.2016.12.013.

- Hauge, J. 2020. “Industrial Policy in the Era of Global Value Chains: Towards a Developmentalist Framework Drawing on the Industrialisation Experiences of South Korea and Taiwan.” The World Economy 43 (8): 2070–2092. doi:10.1111/twec.12922.

- Hauge, J., and H. J. Chang. 2019. “The Role of Manufacturing versus Services in Economic Development.” In Transforming Industrial Policy for the Digital Age, edited by P. Bianchi, C. R. Duran, and S. Labory. 12–36. Cheltenham: Edward Elgar Publishing.

- Hauge, J., and E. O’Sullivan. 2019. Inside the Black Box of Manufacturing: Conceptualising and Counting Manufacturing in the Economy. Cambridge: Cambridge University Engineering Department.

- Horner, R., and M. Alford. 2019. “The Roles of the State in Global Value Chains.” In Handbook on Global Value Chains, edited by Stefano Ponte, Gary Gereffi, and Gale Raj-Reichert. 555–569. Cheltenham: Edward Elgar Publishing.

- International Monetary Fund. 2018. World Economic Outlook, April 2018: Cyclical Upswing, Structural Change. Washington, DC: International Monetary Fund.

- Jourdan, A. 2018. “Designed in California, Made in China: How the iPhone Skews U.S. trade Deficit.” Reuters, 21 March.

- Kaldor, N. 1966. Causes of the Slow Rate of Economic Growth of the United Kingdom: An Inaugural Lecture. Cambridge: Cambridge University Press.

- Kaplinsky, R., and M. Morris. 2016. “Thinning and Thickening: Productive Sector Policies in the Era of Global Value Chains.” The European Journal of Development Research 28 (4): 625–645. doi:10.1057/ejdr.2015.29.

- Kim, S., H. Lim, and D. Park. 2010. “Productivity and Employment in a Developing Country: Some Evidence from Korea.” World Development 38 (4): 514–522. doi:10.1016/j.worlddev.2009.11.008.

- Kinkel, S., R. T. Dewanti, and P. Zimmermann. 2017. “Measuring Reshoring Trends in the EU and the US.” MAKERS Report, 4. http://www.makers-rise.org/wp-content/uploads/2018/02D

- Kleibert, J. M., and L. Mann. 2020. “Capturing Value Amidst Constant Global Restructuring? Information-Technology-Enabled Services in India, the Philippines and Kenya.” The European Journal of Development Research 32 (4): 1057–1079. doi:10.1057/s41287-020-00256-1.

- Kraemer, K. L., G. Linden, and J. Dedrick. 2011. “Capturing Value in Global Networks: Apple’s iPad and iPhone.” Research Supported by Grants from the Alfred P. Sloan Foundation and the US National Science Foundation (CISE/IIS).

- Kvangraven, I. H. 2021. “Beyond the Stereotype: Restating the Relevance of the Dependency Research Programme.” Development and Change 52 (1): 76–112. doi:10.1111/dech.12593.

- Loungani, M. P., M. S. Mishra, M. C. Papageorgiou, and K. Wang. 2017. World Trade in Services: Evidence from a New Dataset. Washington D.C.: International Monetary Fund.

- Mann, L. 2018. “Left to Other Peoples’ Devices? A Political Economy Perspective on the Big Data Revolution in Development.” Development and Change 49 (1): 3–36. doi:10.1111/dech.12347.

- Manyika, J. 2017. “A Future That Works: AI, Automation, Employment, and Productivity.” McKinsey Global Institute Research, Tech. Rep, 60.

- Manyika, J., D. Hunt, S. Nyquist, J. Remes, V. Malhotra, L. Medonca, B. Auguste, and S. Test. 2011. “Growth and Renewal in the United States: Retooling America’s Economic Engine.” Journal of Applied Corporate Finance 23 (1): 8–19. doi:10.1111/j.1745-6622.2011.00310.x.

- Manyika, J., S. Lund, M. Chui, J. Bughin, J. Woetzel, P. Batra, R. Ko, and S. Sanghvi. 2017. Jobs Lost, Jobs Gained: Workforce Transitions in a Time of Automation. McKinsey Global Institute.

- Marconi, N., C. F. de Borja Reis, and E. C. de Araújo. 2016. “Manufacturing and Economic Development: The Actuality of Kaldor’s First and Second Laws.” Structural Change and Economic Dynamics 37: 75–89. doi:10.1016/j.strueco.2015.12.002.

- McMillan, M. S., and D. Rodrik. 2011. Globalization, Structural Change and Productivity Growth. National Bureau of Economic Research.

- McMillan, M., D. Rodrik, and C. Sepulveda. 2017. Structural Change, Fundamentals, and Growth: A Framework and Case Studies. Washington D.C.: World Bank Publications..

- Meyer, J. 2009. “Policy Space: What, for What, and Where?” Development Policy Review 27 (4): 373–395.

- Mezzadri, A. 2016. “Class, Gender and the Sweatshop: On the Nexus between Labour Commodification and Exploitation.” Third World Quarterly 37 (10): 1877–1900. doi:10.1080/01436597.2016.1180239.

- Milberg, W. 2008. “Shifting Sources and Uses of Profits: Sustaining US Financialization with Global Value Chains.” Economy and Society 37 (3): 420–451. doi:10.1080/03085140802172706.

- Milberg, W., and D. Winkler. 2013. Outsourcing Economics: Global Value Chains in Capitalist Development. Cambridge: Cambridge University Press.

- Milberg, W., X. Jiang, and G. Gereffi. 2014. “Industrial Policy in the Era of Vertically Specialized Industrialization.” In Transforming Economies: Making Industrial Policy Work for Growth, Jobs and Development, edited by Jose M. Salazar-Xirinachs, Irmgard Nubler and Richard Kozul-Wright. 151–178. Geneva: International Labour Organisation and the UN Conference on Trade and Development.

- Miroudot, S., and C. Cadestin. 2017. “Services in Global Value Chains.” OECD Trade Policy Papers No. 197.

- Mokyr, J., C. Vickers, and N. L. Ziebarth. 2015. “The History of Technological Anxiety and the Future of Economic Growth: Is This Time Different?” Journal of Economic Perspectives 29 (3): 31–50. doi:10.1257/jep.29.3.31.

- Morris, M., and C. Staritz. 2019. “Industrialization Paths and Industrial Policy for Developing Countries in Global Value Chains.” In Handbook on Global Value Chains, edited by Stefano Ponte, Gary Gereffi, and Gale Raj-Reichert. 506–520. Cheltenham: Edward Elgar Publishing.

- Muro, M., R. Maxim, and J. Whiton. 2019. Automation and Artificial Intelligence: How Machines Are Affecting People and Places. Washington D.C.: Brookings Institution.

- Nayyar, D. 2013. Catch up: Developing Countries in the World Economy. Oxford: Oxford University Press.

- Nem Singh, J., and G. C. Chen. 2018. “State-Owned Enterprises and the Political Economy of State–State Relations in the Developing World.” Third World Quarterly 39 (6): 1077–1097. doi:10.1080/01436597.2017.1333888.

- Nolan, P., J. Zhang, and C. Liu. 2007. “The Global Business Revolution, the Cascade Effect, and the Challenge for Firms from Developing Countries.” Cambridge Journal of Economics 32 (1): 29–47. doi:10.1093/cje/bem016.

- OECD. 2002. Foreign Direct Investment for Development: Maximising Benefits, Minimising Costs. Paris: Organisation for Economic Cooperation and Development.

- OECD. 2013. Interconnected Economies: Benefitting from Global Value Chains. Paris: Organisation for Economic Cooperation and Development.

- OECD. 2017. The Next Production Revolution: Implications for Governments and Businesses. Paris: Organisation for Economic Cooperation and Development.

- Owusu, S., A. Szirmai, and N. Foster-McGregor. 2020. The Rise of the Service Sector in the Global Economy (No. 2020-056). United Nations University-Maastricht Economic and Social Research Institute on Innovation and Technology (MERIT).

- Pagano, U. 2014. “The Crisis of Intellectual Monopoly Capitalism.” Cambridge Journal of Economics 38 (6): 1409–1429. doi:10.1093/cje/beu025.

- Parschau, C., and J. Hauge. 2020. “Is Automation Stealing Manufacturing Jobs? Evidence from South Africa’s Apparel Industry.” Geoforum 115: 120–131. doi:10.1016/j.geoforum.2020.07.002.

- Raj-Reichert, G., S. Zajak, and N. Helmerich. 2021. “Introduction to Special Issue on Digitalization, Labour and Global Production.” Competition & Change 25 (2): 133–141. doi:10.1177/1024529420914478.

- Schlogl, L. 2020. “Leapfrogging into the Unknown: The Future of Structural Change in the Developing World.” WIDER Working Paper 2020/25.

- Schlogl, L., and A. Sumner. 2020. Disrupted Development and the Future of Inequality in the Age of Automation. London: Palgrave Macmillan.

- Schwab, K. 2016. The Fourth Industrial Revolution. Davos: World Economic Forum.

- Selwyn, B. 2017. The Struggle for Development. Cambridge: Polity Press.

- Selwyn, B. 2019. “Poverty Chains and Global Capitalism.” Competition & Change 23 (1): 71–97. doi:10.1177/1024529418809067.

- Selwyn, B., and D. Leyden. 2021. “Oligopoly-Driven Development: The Word Bank’s Trading for Development in the Age of Global Value Chains in Perspective.” Competition & Change, 102452942199535. doi:10.1177/1024529421995351.

- Shadlen, K. C. 2005. “Exchanging Development for Market Access? Deep Integration and Industrial Policy under Multilateral and Regional-Bilateral Trade Agreements.” Review of International Political Economy 12 (5): 750–775. doi:10.1080/09692290500339685.

- Slaughter, M. J. 2010. How U.S. Multinational Companies Strengthen the U.S. Economy. Washington, DC: Business Roundtable and the United States Council Foundation.

- Starrs, S. 2014. “The Chimera of Global Convergence.” New Left Review 87 (1): 81–96.

- Statista. 2021. “Statista Business Data Platform." https://www.statista.com/

- Suwandi, I. 2019. Value Chains: The New Economic Imperialism. New York: Monthly Review Press.

- Szirmai, A. 2009. “Industrialisation as an Engine of Growth in Developing Countries.” UNU-MERIT Working Paper Series 2009-010.

- Szirmai, A., and B. Verspagen. 2015. “Manufacturing and Economic Growth in Developing Countries, 1950–2005.” Structural Change and Economic Dynamics 34: 46–59. doi:10.1016/j.strueco.2015.06.002.

- Taglioni, D., and D. Winkler. 2016. Making Global Value Chains Work for Development. Washington, DC: The World Bank.

- Tate, W. L. 2014. “Offshoring and Reshoring: US Insights and Research Challenges.” Journal of Purchasing and Supply Management 20 (1): 66–68. doi:10.1016/j.pursup.2014.01.007.

- UNCTAD. 2017. Trade and Development Report 2017: Beyond Austerity: Towards a Global New Deal. Geneva: United Nations Conference for Trade and Development.

- UNCTAD. 2020. World Investment Report 2020: International Production beyond the Pandemic. Geneva: United Nations Conference for Trade and Development.

- UNIDO. 2019. Industrial Development Report 2020: Industrializing in the Digital Age. Vienna: United Nations Industrial Development Organisation.

- Wade, R. H. 2003. “What Strategies Are Viable for Developing Countries Today? The World Trade Organization and the Shrinking of ‘Development Space’.” Review of International Political Economy 10 (4): 621–644. doi:10.1080/09692290310001601902.

- Wade, R. H. 2019. “Catch-up and Constraints in the Twentieth and Twenty-First Centuries.” In How Nations Learn: Technological Learning, Industrial Policy, and Catch-Up, edited by Arkebe Oqubay, Kenichi Ohno. 15. Oxford: Oxford University Press.

- World Bank. 2016. World Development Report 2016: Digital Dividends. Washington, DC: World Bank Publications.

- World Bank. 2020. World Development Report 2020: Trading for Development in the Age of Global Value Chains. Washington, DC: World Bank Publications.

- World Development Indicators. 2021. “World Development Indicators Online Database.” https://databank.worldbank.org/source/world-development-indicators

- WTO. 2013. World Trade Report 2013: Factors Shaping the Future of World Trade. Geneva: World Trade Organisation.

- WTO. 2019. World Trade Report 2019: The Future of Services Trade. Geneva: World Trade Organisation.

- Zuboff, S. 2019. The Age of Surveillance Capitalism: The Fight for a Human Future at the New Frontier of Power. London: Profile Books.