ABSTRACT

The outbreak of the COVID-19 pandemic has imposed numerous constraints, caused enormous disruptions and has been associated with more than 5.8 million deaths worldwide (at the time of writing). It also raised opportunities to imagine a new environment. Accounting academics have been involved in studying and thinking about the questions this poses for research and practice. Accounting scholars have explored the responses to the pandemic crisis and provided important insights about its impact. However, there is relatively little research into how accounting scholarship has contributed collectively to understanding and challenging the effect of the COVID-19 crisis. As accounting scholarship had time to grow, this seems an opportune time to offer a preliminary assessment and an early indication of the emergent themes and challenges. This paper aims to bring together and reconcile insights from an understandably fragmented literature and propose an agenda for future research. The paper provides a conceptual consolidation of published scholarship by establishing connections and identifying key challenges and opportunities. Building on a systematic review of publication patterns across 53 academic journals, the paper analyses the themes explored in the literature as investigated by accounting researchers and identify important gaps. A structured analysis can help identify the role and relevance of accounting scholarship in a way that might not be as clear when examining individual aspects.

1. Introduction

The COVID-19 pandemic has resulted (at the time of writing) in more than 412 million confirmed cases and more than 5.8 million deaths globally (WHO, Citation2020a). It has raised significant concerns about future health crises (Roberts, Citation2021) and economic shocks (Guan et al., Citation2020). The pandemic has also caused a deep social reconfiguration, and all areas of knowledge are called to present their contribution.

Since the outbreak, the scientific progress in understanding COVID-19 has been overwhelming. Data collated and analysed by Nature (Else, Citation2020) and other databases (Dimensions, Citation2021) show an impressive wealth of research produced and published from early 2020 onwards. The focus of this enormous body of literature changed with time. At first, COVID-19 research focused on the spread of the disease, diagnostics, and testing (COVID-Citation19 Primer, Citation2021). Subsequently, there has been growing interest in the broader impacts of the COVID-19 pandemic, with research focusing on mental health, sustainability, and studies in human societies (COVID-Citation19 Primer, Citation2021).

In the meantime, scholars engaged in research aiming to bring together an understandably fragmented literature. Researchers in various fields sought to classify the main contributions published on the topic of COVID-19. These include, among others, public health (Harapan et al., Citation2020), bioengineering (Lella & PJA, Citation2021), psychology (Cachón-Zagalaz et al., Citation2020), education research (Pokhrel & Chhetri, Citation2021), economics (Brodeur et al., Citation2021), corporate governance (Koutoupis et al., Citation2021), and business and management (Piccarozzi et al., Citation2021; Verma & Gustafsson, Citation2020). As accounting continues to gain in importance in so many spheres of social life (Hopwood & Miller, Citation1994), understanding the role and relevance of accounting research in the context of the COVID-19 pandemic is important (Rinaldi et al., Citation2020). However, how accounting scholarship has collectively contributed to making sense of and challenging the COVID-19 crisis is still unclear.

The paper aims to reconcile the publication patterns and propose an agenda for future research in this emerging and important area of accounting scholarship. To achieve its aim, the paper conducts a systematic analysis of accounting-COVID-19 research published in accounting journals between 1st January 2020 and 15th October 2021 to offer a comprehensive framework of past and future accounting functioning on which to build new policies and practices. In total, 135 research articles were identified as covering issues related to themes associated with COVID-19 and contributing to research and practice on how accounting may be implicated in shaping (or be shaped by) the pandemic. To structure the analysis of the insights, the paper consolidates extant published accounting literature, establishing connections and identifying key challenges and opportunities drawing on a series of graphics to represent the accounting-COVID-19 research landscape.

This paper contributes to the literature by being one of the first studies to collectively explore accounting-related studies that address the COVID-19 crises. As accounting on COVID-19 research is in an early stage of development, this paper highlights avenues for future research and provide a conceptual representation of accounting literature in this area. In so doing, the paper extends accounting scholarship by identifying the role and relevance of accounting in response to the COVID-19 crisis in a way that might not be as clear when examining individual aspects. As accounting and accountability research had time to grow, this seems an opportune time to offer a preliminary assessment and outline an early indication of emergent themes and challenges.

The scientific publishing process has been under intense scrutiny for the time lag between the emergence of a phenomenon and published research appearing (Powell, Citation2016; Vosshall, Citation2012). In this instance, the accounting research community has demonstrated the ability to quickly react to a global challenge. The pace with which accounting researchers and journals have produced and disseminated research findings on the COVID-19 pandemic has the potential to enable other scholars to make quicker and better-informed decisions about what alternatives could be attempted to provide meaningful insights in their studies.

The conceptual graphic supports the contextualization and simplification of the field by establishing links and identifying gaps. The critical analysis of the current state of accounting-COVID-19 research provides insights into the roles of accounting in the COVID-19 crisis. The paper also sketches an agenda for future research based on the insights emerging from the analysis in this paper.

The remainder of the paper proceeds as follows. The next section explains the methods used to capture and analyse insights from existing literature. Section 3 provides a conceptual representation of the accounting-COVID-19 research field. Section 4 consolidates the existing accounting literature, establishes connections and identifies key challenges and opportunities. The final section draws conclusions and sketches an agenda for future research based on insights emerging from the analysis in this paper.

2. Research method

An analytical review scheme is required to systematically assess the contribution of a given body of literature (Crossan & Apaydin, Citation2010; Ginsberg & Venkatraman, Citation1985). This section explains the scheme used to capture and analyse insights from studies published in peer-reviewed accounting journals from 1st January 2020 to 15th October 2021.

To determine the broad areas and themes of research published in peer-reviewed accounting journals over the review period first required establishing which journals to include in this study. Given the quality of criteria used in selecting journals for inclusion in its database, it was decided to analyse the research articles published (either included in an issue or online as early cite) in accounting journals within Scopus. Then, we identified highly influential “accounting journals” using the CABS (Citation2021) academic journal guide categories, considering those journals classified as “2”, “3” or “4” from the Academic Journal Guide (AJG). As a result, 53 Scopus-listed AJG journals were identified (Appendix 1). While this choice was made to overcome the risk of subjective specification of the field, academics have expressed their concern about calculating and ranking the quality of research (Guthrie et al., Citation2019; Sangster, Citation2015; Tourish & Willmott, Citation2015), not least in that it ignores or downplays other views and information (Unerman, Citation2020). Accounting scholars have also noted that investigating an emerging field might be useful to broaden the boundaries to include, for example, conference proceedings (Massaro et al., Citation2016). As accounting-COVID-19 is a new topic, few academic articles have been published. Practitioners’ journals, public reports, and books also provide insights to help develop academic scholarship in this area. The exclusion of these outlets and journals allocated scores of less than “2” is another limitation of this work, as is the omission of journals not considered by CABS (Citation2021). Previous research looking at the journey of a nascent body of research argued that less established journals are publishing interesting and insightful research related to accounting (Rinaldi et al., Citation2018), and future research should consider them. Nonetheless, it is commonly accepted that journal rankings represent an important proxy of accounting research publications that exert an important role in “legitimating accounting research across the whole research community” (Thomson, Citation2014, p. 17).

To identify the journal articles from this body of research, structured searches were conducted for all papers with the terms “Covid”, “COVID-19”, “pandemic” and “coronavirus” in their title, keywords (where available) and abstract for the period 1st January 2020 – 15th October 2021. The length of time was important to investigate research from when COVID-19 was characterized as a pandemic (WHO, Citation2020b). The key terms were used concurrently to capture the academic papers that were explicit about their engagement in the COVID-19 pandemic concerns.

All the research products identified through the above processes were downloaded and systematically analysed to identify the key themes of each article. All records were examined manually to make sure the searched parameters were consistent with the content of the papers. The final database included 135 journal articles (Appendix 2). When the selection process was completed, the analysis concerned the full text of the collected papers.

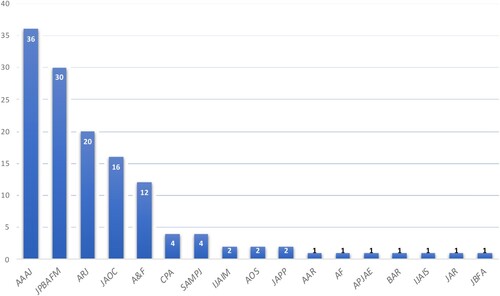

A theme table was prepared for each article which summarized the article’s stated aim, purpose, contribution, research methodology, theoretical framework used (where available), jurisdiction, level of analysis of the article’s inquiry (in terms of individual, organizational or national/international) and main findings. The theme table was prepared through an iterative process and served three important functions. First, the table was directly linked with the research aim, providing a schematic representation of the different types of issues and problems being investigated. Second, the theme table provided a record for all steps taken in the process. Finally, the theme table became the basis for constructing the conceptual graphic of the areas associated with the emergent accounting-COVID-19 literature (Tranfield et al., Citation2003). shows the distribution of accounting-COVID-19 research across journals.

Figure 1. Accounting-COVID-19 publications 1st January 2020-15th October 2021. Key to journal abbreviations: AAAJ – Accounting, Auditing & Accountability Journal; JPBAFM – Journal of Public Budgeting, Accounting and Financial Management; ARJ – Accounting Research Journal; JAOC – Journal of Accounting and Organizational Change; A&F – Accounting and Finance; CPA – Critical Perspectives on Accounting; SAMPJ – Sustainability Accounting, Management and Policy Journal; IJAIM – International Journal of Accounting & Information Management; AOS – Accounting, Organizations and Society; JAPP – Journal of Accounting and Public Policy; AAR – Australian Accounting Review; AF – Accounting Forum; APJAE – Asia-Pacific Journal of Accounting and Economics; BAR – British Accounting Review; IJAIS – International Journal of Accounting Information Systems; JAR – Journal of Accounting Research; JBFA – Journal of Business Finance and Accounting

This filtering methodology is conceptually similar to the method used in Unerman and O'Dwyer (Citation2010). However, it is possible that for some articles, the key focus might not be reflected in the title, keywords, or abstract. Nevertheless, this hypothetical omission should not materially affect the overall picture portrayed by the results of the study, given that the whole population of articles has been analysed.

highlights a concentration of published articles within a small range of journals, namely AAAJ – Accounting, Auditing & Accountability Journal; JPBAFM – Journal of Public Budgeting, Accounting and Financial Management; ARJ – Accounting Research Journal; JAOC – Journal of Accounting and Organizational Change; A&F – Accounting and Finance. It is worth noting, however, that these journals have promoted special issuesFootnote1 exploring themes such as accountability and management practices, remote teaching/learning, and organizational change during the COVID-19 pandemic. Therefore, it should not be surprising to see that these journals accounted for almost 85 per cent of the articles.

However, what should be surprising is the relative absence of accounting-COVID-19 paper in journals that might be expected to publish COVID-19 relevant work (namely: Accounting Review; Journal of Accounting and Economics; Contemporary Accounting Research; Journal of Accounting Research; Accounting Organizations and Society; Review of Accounting Studies; Accounting Forum; Accounting and Business Research; Journal of Accounting and Public Policy; British Accounting Review; European Accounting Review and Management Accounting Research) raising the question as to why. Even though many accounting scholars have explored the responses to the pandemic crisis and provided important preliminary insights about its impact, several issues require further in-depth investigations. Recent research has highlighted that to analyse the considerable breadth and depth of complexity underlying societal problems, accounting scholars should promote interdisciplinary studies, and engage in a range of refined theories and transform accounting data into evidence to influence policy and practice (O'Dwyer & Unerman, Citation2016; O’Dwyer & Unerman, Citation2014; Unerman & Chapman, Citation2014). While the COVID-19 crisis raised awareness about the importance of being prepared and at speed, also reveals several journals that, so far, only managed to publish 1 or 2 papers on COVID-19. This absence point to the challenges still faced by the accounting community to get this massive global issue into print in numbers (of papers published). As the impact of COVID-19 on society will be deep and long-lasting, we may expect that accounting research will continue to emerge as research matures and grows. Alternatively, we should strongly question what should factor in accounting scholarship if not the pressing issues that threaten the very existence of our society (Guthrie et al., Citation2019; Thomson, Citation2014; Unerman, Citation2020).

The analysis also checked on the citations of the papers included in the accounting-COVID-19 literature. Recent research suggests that highly cited articles are important because they point to potential issues that will need to be examined in a future corpus of research (Garanina et al., Citation2021). To conduct the citation check, the paper used citation counts based on Google Scholar data as of 30 January 2022 (Appendix 4 shows the total citation counts for all journal articles included in the analysis). This preliminary assessment reveals two papers that already have 155 and 71 Google Scholar cites, respectively, while 12 papers were cited 30 times or more. Although it is too soon to assume how the literature will develop, the most cited research provides an early indication that organizational functioning and financial resilience of public and private institutions are important research issues.

3. Designing the conceptual graphic

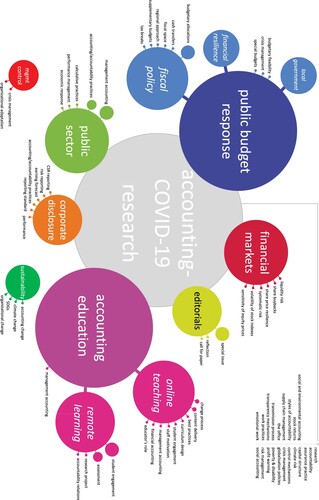

This paper provides a systematic review of accounting-COVID-19 academic research, published in a wide range of journals from 1st January 2020 – 15th October 2021. It classifies and links several research themes that accounting academics and practitioners are engaged in. The graphics presented in this paper offer a schematic illustration of the accounting-COVID-19 field, structured around the themes that they primarily address (). Each article has been categorized to one theme according to its primary purpose, as denoted by the authors in their work. However, these papers were not aimed at providing insights into only one theme but contributed to more than one area of accounting scholarship. This paper classifies each article according to the main area that its insights primarily inform. It also provides, where possible, further sub-classifications to reflect other areas covered.

Figure 2. Representation of Accounting-COVID-19 research themes and sub-themes.

The design of the graphics involved an iterative process that was directed at categorizing the research material to detect how COVID-19 was implicated in accounting functioning. The theme table helped gain a sense of the different types of issues and problems being investigated and discussed in accounting-COVID-19 academic literature, how often these problems were explored, from what perspective, and by which journals. Once the theme table was constructed, the coding process began. This process considered the stated aim, contribution, and purpose of each paper as a preliminary framework for the open coding of the research. The purpose of this first stage of analysis was to allow a preliminary classification of themes to emerge. In the second stage of the analysis, these themes were grouped and considered for specific arguments relating to key areas and sub-areas as described in the papers. In the final stage of the analysis, these patterns were further refined by cycling between the data and the papers. As the concepts were refined through this process, they began to consolidate into a number of overarching dimensions. The data classification of each paper was conducted manually to retain maximum sensitivity to the key themes adopted by the accounting literature addressing the study of the COVID-19 crisis.

The area of the circles for each theme (and sub-theme) was determined proportionally to the frequency of coverage. As a result, the more papers covered a specific theme (or sub-theme), the broader the area of the circle. The graphics also show in smaller circles other sub-themes that each paper covers but less thoroughly than the main theme it covers.

The conceptual graphic () presented five main themes, and 48 sub-themes that were respectively linked to a further 70 sub-sub-themes. The bigger circles offer thematic representations of the most frequent themes which align the COVID-19 crisis to accounting research published from 1st January 2020 to 15th October 2021. The analysis identifies five broad topic areas: public budget response, accounting education, public sector, financial markets, and corporate disclosure. These five areas alone accounted for almost 60 per cent of the literature and were regarded as the main themes. Note that where the sub-theme is placed outside the main themes, this is intentional and illustrates the article's specific focus. Though the procedure adopted to classify journals was as objective and rigorous as possible, it may still suffer from some subjective bias in that it was conducted by a single researcher. The graphics, therefore, are designed as a learning device to aid the organization of a fragmented literature about the COVID-19 crisis via reconciling and integrating individual journal articles into a coherent architecture.

4. Evaluating the contribution of accounting-covid-19 research

This section discusses the contribution of the literature through a comprehensive critical analysis of the identified journal articles. Given the amount of research included in the systematic analysis, the following sections reconcile the key insights produced by the body of literature classified to the main themes that emerged from the analysis (Appendix 3).

4.1. Public budget response

This literature covers the budgetary and fiscal measures used in response to the pandemic, and the political, economic, and social factors that influenced the design of these responses. It includes 26 articles that provide insights into the magnitude and approaches of fiscal responses across jurisdictions. The papers in this theme highlight the policy tools used by different countries at national, state, and local levels and raise concerns about the long-term resilience of fiscal systems.

A number of these studies set out and discussed the extent of the economic impact of the coronavirus pandemic and the expansion in government spending. Budgetary allocations and monetary policy measures have been shown to construct certainties in a context characterized by ambiguities (Argento et al., Citation2020). The budget responses followed different patterns attributed to a range of factors.

Distinct social, economic, and political contexts in various jurisdictions led to different ways of implementing extraordinary budgetary allocations related to the pandemic. For example, some countries adopted a centralist approach by making incremental and sequential budgetary decisions (Nemec & Špaček, Citation2020). Other countries confronted the pandemic through its diversity, with provinces that made wise strategic decisions capable of assisting provinces that made tactical mistakes (Cho & Kurpierz, Citation2020). The nature of the approach also varied in terms of the level of cooperation, with countries gathering different stakeholders together and creating a single emergency budget via a more comprehensive engagement process (Vakulenko et al., Citation2020). Contrary to the austerity measures adopted to confront the financial and economic crisis, more robust investment policies were implemented to tackle the harmful effects of the spreading of the COVID-19 virus (Cepiku et al., Citation2021; Raudla & Douglas, Citation2020). Forms of “people-focused” budgetary measures, alternative to the neoliberal approach to social welfare and inequality, have proven essential during the initial phases of the pandemic and contributed to addressing inequality (Andrew et al., Citation2021).

However, the conditions created by prior neoliberal policies have sometimes limited the budgetary responses by restricting the government's ability to perform expansionary policies (Andrew et al., Citation2020).

The timeliness of action also contributed to the handling of the COVID-19 pandemic. Where National Parliaments approved substantial supplementary budgets in a timely manner, proactive actions to combat the pandemic were taken, thus increasing the effectiveness of the response and, in turn, the approval rating for the administration (Kim, Citation2020). Where, instead, the magnitude of the pandemic was underestimated, the development of responses to crisis management followed a more reactive path and affected the financial, social, and political stability negatively (de Villiers et al., Citation2020; Ejiogu et al., Citation2020; Upadhaya et al., Citation2020).

Flexibility in rulemaking, resource mobilization and administrative execution played an important role in the effectiveness of budgetary responses. For example, simplified public procurement procedures and quick acquirement and operationalization by all levels of the government of key resources and supplies allowed some governments to address different emergency needs and provide the necessary fiscal interventions and mitigation (Wu & Lin, Citation2020). Among the challenges faced in formulating the response to the pandemic is the fiscal space available to the government. In contexts characterized by pre-existing difficult economic conditions, the revenue shocks and high borrowing environment without adequate fiscal assistance from the central government, prevented spending their way out of the pandemic (Jose et al., Citation2021). The response to the crisis also reflects the power struggle between influential interest groups that promote their interests (Ashfaq & Bashir, Citation2021). Pressure from social groups aimed to either change strict public policy measures (such as lockdowns and quarantines) or to divert public resources towards their institutions, led to an increased burden on public health.

The debate around the budgeting responses to COVID -19 pandemic is frequently linked to the view that these processes need to become more strategic (Anessi-Pessina et al., Citation2020). To tackle the challenges posed by the pandemic, governmental budgeting is required to support policy decision-making (through new formats and classifications) and public accountability (through more active forms of engagement). Governments used a wide range of accounting and accountability tools to respond to the COVID-19 pandemic and mitigate its impact on the economy and society. For example, the “Special budget” offered greater flexibility over the traditional annual budget because governments could maneuver in a space not subject to balanced-budget requirements and debt limits (Liao et al., Citation2021). In response to the centralization that characterizes the budgetary process, “participatory budgets” proved to be an effective means to enable citizens to direct the use of public funds and become more involved in budgetary processes at the local level (Cho, Jérôme, et al., Citation2021).

The long-term macroeconomic implications of the global pandemic (such as the impact on gross domestic products, level of government debt and rate of employment) and the limited effect of some social interventions (such as cash transfer programs) have raised several concerns about the financial resiliency of both regional and national governments for the supportive actions carried out on their initiative. From this perspective, national or federal financial frameworks based on grants have been developed to assist individual local authorities or less developed regions through the central government (Ahrens & Ferry, Citation2020; Klimanov et al., Citation2021).

The response to the COVID-19 pandemic also revealed broader accountability trends. Public authorities adopted various accountability styles, each influenced by how they sought to justify their conduct to the general public (Andreaus et al., Citation2021). One example includes “allocative and external accountability mechanisms” aimed at increasing the traceability of taxpayers’ money through legally binding monthly reports about the specific COVID-19 expenditures (Seiwald & Polzer, Citation2020). However, when developing and implementing different governmental accounting and accountability modes, some tensions can emerge. As a result, forms of accounting characterized by reporting speed and international comparability were favored over others because they increased the credibility of governments (Heald & Hodges, Citation2020).

Collectively this body of literature shows a diversity of budgetary responses aimed at alleviating the effect of the pandemic. At the same time, this research exposes important tensions. The analysis unveils a variety of factors driving the nature and effects of budgetary responses that include, among others: the social, economic, and political contexts; the speed of response of the authorities; the level of cooperation between central authorities, local authorities and the citizenry; the flexibility of the budgetary packages; the fiscal bandwidth of the states; the influence of public groups; and, of course, the pandemic caseload. However, some studies claimed that several measures are accompanied by effects that will impact negatively on poverty, inequality, environmental factors and, more broadly, on the global sustainability agenda (Ahrens & Ferry, Citation2020; Argento et al., Citation2020; Elkhashen et al., Citation2021; Heald & Hodges, Citation2020). Therefore, more research is needed to increase our understanding of the short, medium, and long-term impact and implications of the fragmented budgetary responses to the pandemic, their relationships, and interdependencies. Accounting scholarship has focussed on budgets, budgeting, and stimulus packages, with a depth of insight being generated in each of these domains.

A potential next stage in the evolution of this body of work would be to explore these aspects in concert, as constituting an ecology of COVID-19 responses. The holistic nature of COVID-19 impact provides an opportunity for research that explores the extent to which accounting and accountability practices can support organizations in understanding the relationships and interdependencies between the diversity of budgetary responses. The strong momentum amongst central and local authorities in developing initiatives supporting the Sustainable Development Goals (SDGs) would be a focal point for the contributions accounting researchers could make to remedy this shortcoming (Bebbington & Unerman, Citation2020).

4.2. Accounting education

The outbreak of the COVID-19 pandemic has caused massive disruptions in higher education. When teaching shifted from face-to-face to online, accounting educators and accounting students were severely impacted. This theme comprises 22 articles that illuminate a wide range of experiences with coping with the COVID-19 crisis. The literature looks at accounting teaching and learning practices, providing practical thinking, critical self-reflection, and design tips to tackle the challenges that emerged due to the pandemic. It also raises important concerns about the personal and professional struggle of teaching staff and students.

A group of articles within this theme critically discuss the transition and change of teaching and assessment methods. Among the most visible and immediate measures public authorities took to help prevent the spread of the virus were lockdowns and stringent restrictions on indoor gatherings. While universities swiftly moved classroom-based teaching online, accounting academics had to pivot their delivery methods and pedagogy to adapt to the new educational environment.

The move to online teaching required quick and simultaneous major changes. These included finding new ways to interact with students and deliver content and provide assessments. Research in this area highlights different approaches and identifies several outcomes from coping, with a crisis continuum from positive to negative. Aspects discussed by this literature include, among others, the role of technology, modes of online delivery, students and staff motivation, the processes of redesigning assessments and the curriculum, and staff/student engagement.

The suspension of face-to-face teaching set off operational and emotional turmoil. On the one hand, it widened the expectation–performance gap between students, educators and universities as to what could be reasonably implemented to support student learning, support educators and provide a continued sense of community (Osborne & Hogarth, Citation2020). The expectations portrayed by universities to students on what to expect from staff were not mirrored by the reality of resources and support given to educators. Nevertheless, in a fluid context such as that brought about by the impact of COVID-19, it was difficult to imagine what a realistic expectation might have looked like. Given the rapidity of the switch to online learning, most of the changes were driven by the teaching staff’s intuition and past experiences. Establishing boundaries at the outset through expectation setting was therefore difficult.

On the other hand, the workspace integrated life and family in most cases. This had an impact on the approach to teaching. However, the inevitable lack of complete understanding of the details of what that impact could potentially mean led experienced educators to confront feelings of resistance to change (Ackermann, Citation2020).

Remaining motivated was an important driver for accounting academics adapting to the changing work environment. Academic staff faced greater strain during the pandemic, in converting a traditional delivery model into an online format and maintaining a connection to their colleagues (Beatson et al., Citation2021). Some researchers found that engaging with a community of practice was highly beneficial. These communities can be discipline-specific or university-specific, geographically defined or broad-based. They work by enabling informal collaborative learning and sharing of ideas, planting the seeds of a community of practice. During the pandemic, these communities not only provided online educational skills; they also fostered a sense of togetherness and a safe environment to share concerns and challenges on both a professional and personal level (Sadiq, Citation2020).

The move to online education required accounting educators to take proactive steps towards online assessments. Interactive teaching and testing environments were found particularly effective to improve student engagement and experience. Interactivity and authenticity of the learning experience proved to be very positive elements during COVID-19 for both staff and students. Pasion et al. (Citation2020) show that students’ motivation to learn in an online environment correlates with the perceptions of physical proximity and social presence. Fostering social interactions via online channels increased proactive involvement and supported students’ mental wellbeing (Perera et al., Citation2021). For example, Dyki et al. (Citation2020) explain the case of a student-created video assignment introduced in an accounting subject to promote employability skills, such as coordination and collaboration. The students’ feedback indicated that the assignment was less stressful than a live presentation while being among the most authentic assignments they had undertaken. In a similar vein, Halabi (Citation2021) describes the production and administration of a podcast assessment that substituted the final examination in an MBA accounting course. Observing and documenting accounting “in-action” benefited the students pedagogically because it provided strong links between learning, assessment, and real-world experience (Bowyer, Citation2020).

Strategies that seem to have worked well include the use of synchronous and asynchronous channels to facilitate and provide support to students in online learning (Ali et al., Citation2020). For example, making weekly announcements (via email or through the online platform), providing timely feedback (to online discussion posts or about their performance) and giving students ownership and control of their learning experience led to increased motivation. On the other hand, cloze questions, transaction analysis questions with pre-defined selection options (presented with drop-down menus), and written questions with a structured answer template (in the form of a table) contributed to improved engagement (Morgan & Chen, Citation2021). In addition to promoting interaction, authenticity can also significantly reduce the risk of academic misconduct in the assessment process. This is particularly relevant during the pandemic where universities worldwide quickly pivoted to unsupervised open-book assessments. For example, drawing on real settings and content situations can deter contract cheating or student collaboration (Wong & Zhang, Citation2020).

To cope with the challenges of the pandemic, some authors reflect on the pedagogical changes required by the unexpected transition to a different educational environment, suggesting the use of a “digital mindset” (Stewart & Khan, Citation2021). The online educational space required a significant reconsideration of teaching and assessment practices. Adaptive accounting teaching and learning solutions need not just the ability to set up and use technology, but also ways of thinking and acting that enable teachers and students to benefit from the new opportunities. However, the transition to online teaching and assessments requires rethinking the pedagogical approaches and transforming the role of the subject-matter expert (Othman, Citation2020). Accounting educators, it is argued, need to be flexible to adapt, explore, learn and discover new skills and competencies. For example, during the pandemic, the roles of content facilitator (i.e. making sure content is timely and readily available), co-learner (i.e. trying to sort out problems when things did not work) and advisor (i.e. offering extra guidance and help to students) became more dominant than that of the traditional resource provider.

Facilitating cognitive growth in student knowledge when abruptly transitioning to online learning may also require the redesign of the course curricula. Focusing on the restructuring of an undergraduate accounting program curricula, Ng and Harrison (Citation2020) identify practices that were successful in facilitating the development of transferable skills in the online teaching environment. Their study discusses how self-reflection journals and weekly study plans, for example, enabled students to address issues related to the self-management of their learning and kept high levels of student engagement. On the other hand, teaching with cases online holds new challenges. Specifically, the quality of class interaction (relating to both technical and psychological concerns) and the reduced time spent on interactive practices are regarded as the main limiting factors (Gómez García & Alba Cabañas, Citation2021).

Overall, this body of literature shows a diversity of practical reflections and design tips taken by accounting educators to cope with the pandemic’s effect on online teaching and learning. Although the virtual learning environment brings the benefits of accessibility and flexibility, this research shows that it does not completely replace the complexity of human connection, authenticity and informal spontaneity found in face-to-face learning (Powell & McGuigan, Citation2020; Spraakman, Citation2020; Sum et al., Citation2021). This literature also finds that transition cycles to new forms of teaching and learning can be looped. Thus, transitions should not be conceptualized as a start with a definite ending. Rather, new processes of transition can emerge if circumstances change. Finally, the experience of going through the COVID-19 pandemic affected people on a deep, personal level. Accounting academics are no exception. Increasing individual frustration and mental exhaustion created by the new forms of social interaction (and lack of), coupled with a sudden shift of working practices (for example, the sudden transition to a distance learning/teaching environment) led to the problematisation of key accounting conceptual underpinnings. For example, by reflecting on a personal teaching experience during the pandemic, Mai (Citation2020) provides insights into the situational nature of the notion of performance as created by a process of social and natural interaction. The key insight is that some factors of this process are conscious and controllable while others are hidden and unconscious. These conceptual contributions have important implications for the construction of performance measurement systems and the indicators to be considered in performance assessment exercises (for example, mental and physical health as part of long-term performance measurement).

This literature also raises important concerns. For example, the level of students’ digital literacy is not homogeneous, which means that some students may take a longer time to be confident with online assessments and that the assessment environment has the potential to increase their stress. It also sheds light on the personal and psychological factors that impact students’ meaningful engagement in students’ learning. Lack of appropriate technological equipment, connectivity issues, home environment and family responsibilities are among the main issues that affect the learning environment (Ali et al., Citation2020)

Social distancing requirements also affected learning due to the lack of in-class interactions. As a result, students encountered several sense-making issues involving concepts, applications, and judgements. However, the extent of the challenge experienced by students varied depending on their approach to studying. More independent and motivated students were more likely to make sense of the conceptual issues they were confronted with. On the other hand, more passive students took longer to adapt to the changing learning environment, particularly where study programs are unstructured (for example, in capstone research projects) (Ramachandra & Wells, Citation2020).

The next stage in the development of this body of literature could deepen our understanding of how the combined online-contact teaching support students manage their learning. The COVID-19 pandemic has led to fundamental changes in accounting education. The transition to hybrid teaching and learning provides an opportunity for a whole research agenda to assess the governance models of hybrid forms of teaching and learning. The shift to online assessment also requires deeper analysis. New research could deepen the discussion on grading systems and students’ learning process. On a more conceptual level, recording lectures and workshops may be perceived as a surveillance technology (i.e. quality control) that undermines morale (Bisbe & Sivabalan, Citation2017). More research could shed light on the implications of the learning experience being constructed outside the classroom (Sangster et al., Citation2020).

4.3. Public sector

This literature covers the various approaches governments and public services took to understand and respond to the emergencies related to the pandemic. This body of research includes 13 articles that provide insights into the roles of calculation, representation, and classification systems in the framing and operationalizing of policy actions aimed at supporting organizations and society.

Research within this theme provides insights into the potential of measurement and reporting systems to assist public authorities in responding to the COVID-19 pandemic. For example, drawing on the case of several cities involved in a large project on circular economy (Parisi & Bekier, Citation2022) illustrates how a set of central and local KPIs contributed to the definition of COVID-19 as an accounting subject, thus making it calculable and manageable by the cities in the project. The findings provide important insights into two properties of accounting technologies. By playing both an “adjudicating” (classifying, enumerating, and comparing performance) and “territorialising” role (rendering those attributes visible by making them calculable, thus constituting the space in which they operate), KPIs influenced the perception of the pandemic, allowing the cities involved in the project to respond to the COVID-19 pandemic crisis. In a similar vein, Huber et al. (Citation2021) find that accounting played an important role in hospitals’ management in the early stages of the pandemic. In hospitals, the aim was to organize as many COVID-19-ready beds as possible and avoid triaging care for infected patients. During the first months of the pandemic, the hospitals used non-financial indicators – i.e. the number of beds – to problematize their care infrastructure. In making the COVID-19 crisis actionable and plannable, accounting transformed an uncertain situation into plannable action. Authorities also used those indicators to prepare funding decisions, inform the public and facilitate the coordination of hospital capacity. The findings point to the “facilitating” and “enabling” roles of accounting information for problematizing the care infrastructure and offering healthcare professionals a platform to engage with the crisis.

A key part of governments’ response to COVID-19 was the procurement of materials and tools for health professionals in hospitals and care homes. Sian and Smyth (Citation2022) analysed the UK Government’s accountability processes in the context of public procurement practices. By exploring the role of legal and auditing mechanisms, and controls in the appropriation of public monies during the early phases of the pandemic, the study shows how an account in the context of public services is given, challenged, and amended. Transparency was regarded as a key control mechanism within the emergency process to ensure accountability for procurement decisions and the increased use of the emergency powers. The findings point to the dynamic nature of accountability and unveil that where competitive processes are missing, timely and complete documentation and disclosure are important means of assuring public accountability.

Accounting research has also emphasized the role of measurements and measurement systems in building trust. The approach taken by authorities to contain and respond to the COVID-19 pandemic required constraints on individual freedoms that required buy-in and cooperation from the public. One way to achieve that is through effective communication strategies adopted by political leaders. de Villiers and Molinari (Citation2022) focus on the New Zealand Government’s non-pharmaceutical intervention to control the spread of the virus. The ultimate objective of New Zealand’s Government was to reduce the incidence to zero and keep it there (Robert, Citation2020). The study shows how accounting and accountability practices contributed to the successful non-pharmaceutical interventions by being transparent and using reliable data, ensuring open-data access, and considering multiple stakeholders’ interests and opinions. Drawing on the case of the UK Government (Broadbent, Citation2020) shows how the use of non-financial performance measures (i.e. tests, hospitalizations, reproduction number, deaths) and the communication of these measures was institutionalized to illustrate the outcomes of actions that had been adopted and seek the cooperation of the public. The findings indicate how forms of accountability depend on the recourse to performance measurement. It also exposes important tensions because measurement is always potentially problematic. Particularly so in the context of COVID-19, where there is no clear understanding of mechanisms that link action and outcomes. Along similar lines, Lapsley (Citation2020) critically analyses the challenges faced by the UK Government during the outbreak of the COVID-19 pandemic, focusing on risk management practices. While the overall approach followed different stages (namely, identification, measurement, evaluation, mitigation, and monitoring), the paper finds that its handling was erratic, suggesting that a more systematic approach would have enabled the UK to respond more promptly and effectively. The paper highlights that accounting is not a neutral technology. Rather, calculations and classifications have enabled a specific form of risk management to emerge as a defensive shield to preserve and maintain the state’s reputation.

Another stream of research within this theme looked at accounting as a technology of governance. Facing the impact of the pandemic required public authorities to mobilize activities and agendas through a variety of schemes. Drawing on the case of the Australian Government, Nikidehaghani and Cortese (Citation2021) show that accounting practices and discourse have enabled the implementation of governmental strategies designed to support jobs in a market significantly affected by the pandemic. Accounting information was central in giving visibility to the problems of government. Specifically, the calculations and quantification of the health impacts and the presentation of the economic consequences of COVID-19 rationalized the need for intervention and facilitated the formulation of solutions to problems of government. However, accounting doesn’t only need things to count; it also needs a context to count them. Drawing on the analysis of a local government’s program to feed the vulnerable, Sargiacomo et al. (Citation2021) highlight the key role of classification, calculation, and representation technologies in governing the response to the pandemic. Before the pandemic, the local government provided its assistance based on existing classifications of people in need (for example, social lists of the elderly, the disabled, the poor and food insecure) to coordinate its important work. This study shows that the classification of space and society is crucial during a crisis. More specifically, due to the pandemic, the local government had to extend its previous knowledge, which required new maps and purpose-built social lists (such as the infected who must not be allowed to leave their houses), whilst also tracking the people who would prefer to be uncounted (such as illegal immigrants and undocumented workers).

Classification schemes supported the pandemic response strategies of public authorities in other ways. Ahmad, Connolly, & Demirag (Citation2021) studied the UK Government’s COVID-19 testing policies to govern the pandemic in the UK. The analysis shows the central role of COVID-19 testing as a technology for inscription and classification. The study illustrates that COVID-19 testing was deployed as “inscriptions” (i.e. assumed number of positive cases) for the UK Government’s performance communication. COVID-19 tests can be conceptualized as science-based classifications that contributed to rendering COVID-19 visible and acted as a dividing practice. As a result, the daily numbers of positive cases and their geographical representation with colour-coded maps played a crucial role in differentiating individuals and spaces, marking the boundaries between the healthy and the sick. The research illuminates how the inscriptive and classificatory roles of accounting construct the risk categories which eventually guide government response to the pandemic.

In a similar vein, Ahrens and Ferry (Citation2021) show that the UK Government underpinned its response with calculations and classifications. Formally conceived to communicate with the public about the social and economic impact of the COVID-19 crisis, accounting data gradually changed into a normalizing role that produced new notions of “case”, “risk”, “danger” and “crisis”, and gave rise to an ideal norm of conduct for the UK population.

Other approaches used accounting to support the public authorities’ strategy to address the COVID-19 emergency. For example, Antonelli et al. (Citation2022) investigate how accounting figures were instrumental in implementing biopolitical measures. Ranging from simple routines (such as washing hands) to remaining at home, these measures were aimed at influencing the behavior of populations. The findings show that the perceived neutrality attributed to numerical accounts of infection and mortality rates, and the geographical representations of the spreading of the virus contributed to shaping people’s perception of reality in a way that was congruent with the government’s ends.

The role and relevance of accounting research in addressing societal concerns are well known (Hopwood & Miller, Citation1994). The COVID-19 pandemic is, of course, a public health emergency, but it is also much more. Collectively, the findings of this area of research have important social and institutional implications. They show how accounting and accountability practices allow a deeper understanding of the needs of the various segments of the population, and act as technologies of government in times of crisis. They also raise important concerns. For instance, measurement and reporting systems are incomplete (Bui et al., Citation2022) and partial in scope (Mitchell et al., Citation2021). They are, therefore, unlikely to capture the full complexity of situational reality. Further research is therefore needed to meet this challenge.

Additionally, the articles included in this theme highlight that accounting is not a neutral technology. Processes of quantification and rationalization can contribute to constructing realities (Berger & Thomas, Citation1966) consistent with the ends of specific pressure groups. With an increasing number of countries facing the resurgence of COVID-19 infections (WHO, Citation2020a), understanding the impact of different strategies implemented in the early phases can provide important insights about effective long-term responses.

The current global vaccination campaign and hopefully a cure in the coming times will help contain the crisis and imagine the future of accounting in the public sector. The next stage in the evolution of this body of research could consider how the public sector can operate and how accounting can be implicated at different levels in the reorganization of life. Although the global pandemic is a health crisis, its effects on how governments and public services respond to society's emerging needs may be long lasting and even transformative. This leads to the importance of broadening the focus of accounting scholarship to comprise the wide range of processes, practices and expertise that enable coordination between policy formulation and resource allocation for future challenging societal problems.

4.4. Financial market

This literature includes research exploring the pandemic's impact on the financial markets and how accounting is implicated in assessing and calculating this impact. This body of research includes nine articles that provide insights into financial risk, equity resilience, and the corporate information environment bore broadly.

The outbreak of the COVID-19 pandemic brought an increase in global financial risk. A group of papers in this area explores how risk spread among stock markets during the COVID-19 pandemic. For instance, Yu et al. (Citation2021) analyse the systemic risk spillover effect between countries during COVID-19. The findings show that the core senders of risk during the early stages of the pandemic were those countries whose economies were most seriously affected. On the other hand, the study finds that the risk spillover effects are remarkably dynamic. In fact, countries capable of undertaking pandemic prevention measures with success turned from being senders to being net receivers of systemic risk contagion. Other studies focus on specific risks, such as liquidity risk (De Vito & Gómez, Citation2020), and offer important suggestions on how to mitigate the risk of cash crunch.

An important focus of this theme is share price resilience. This research advances and discusses measures to assess the extent to which equities are sensitive to any crisis that leads to a short-term fall in macroeconomic activity. Dechow et al. (Citation2021), for example, demonstrate that an implied equity duration measure is effective in measuring the sensitivity of equity securities to unexpected macroeconomic shocks that heavily impact short-term cash flows. They show that organizations with the most expected future cash flows concentrated in the short term, suffer the greatest loss in stock value. In a similar vein, Cui et al. (Citation2021) show that conditional conservatism (i.e. the immediate recognition of expected economic losses while the recognition of economic income is deferred until expected gains are verifiable) supported equity resilience by helping firms implement better risk management practices via timely risk revelations.

Perhaps unsurprisingly, organizations based in countries where the COVID-19 impact is greater, experienced a deeper decline in market value (Chatjuthamard et al., Citation2021). However, the negative impact of COVID-19 on market value is less pronounced for firms with better sustainability performance (Bose et al., Citation2021). These results, however, are not universally supported. Demers et al. (Citation2021) look at the factors that immunize stocks during the COVID-19 crisis. The study shows that ESG performance is not a share price resilience factor during the COVID-19 pandemic. For a sample of US firms, the study demonstrates that accounting-based measures of a firm's liquidity and leverage, financial performance, supply chain management, and internally developed intangible assets offer downside risk protection in times of crisis. This research has important implications for accounting and sustainability research because the view that ESG performance is a share price resilience factor becomes contested. Further research is therefore required to provide evidence of the effectiveness (or the lack of) and feasibility of the ESG approach.

The COVID-19 outbreak complicates the corporate information environment too. The fear of the pandemic hits market sentiment and significantly distorts the price discovery process in the stock market (Xu et al., Citation2021). Specifically, it reduces the stock returns and weakens investors’ processing ability of firm-specific news during the pandemic by slowing the incorporation of new information into the stock price. Social media are regarded as influential platforms for capturing public sentiments (Haroon & Rizvi, Citation2020). During the early stages of the pandemic, social media users shared their impressions and feeling about the reality they were experiencing, thus providing a subjective representation of it. To establish the extent of social media impact on the financial market, Lazzini et al. (Citation2022) analyse the relationship between the sentiment created through social media and the reality of the stock market. By developing a volume-sentiment analysis, the paper finds a strong positive correlation between the trend of conversations on Twitter and the value of the financial market performance in the first phase of the COVID-19 pandemic.

The next stage in developing this body of work could be to consider the emerging issues arising from the uncertainties of market conditions. The level of uncertainty and risk arising from the pandemic has significantly impacted the useful life and residual value of companies’ assets requiring actions for management to take. Hence the importance for accounting scholarship to investigate the rationales and the broader material implications of a range of operations such as restructuring plans, insurance claims, material judgements, and impairment decisions. Accounting research should be playing a central role in supporting the delivery of novel, evidence-based solutions to conceptual, strategic, and operational COVID19-related challenges.

4.5. Corporate disclosure

The high levels of uncertainty caused by the outbreak of the COVID-19 pandemic have increased the stakeholders’ demand for information. The six papers in this theme critically analyse the relationship between COVID-19, accountability practices and disclosure strategies.

The impact of the pandemic has highlighted the relationships between social, environmental, and economic dimensions of life, and raised the need for high-quality information for stakeholders. At the same time, organizations are facing several conflicting priorities as the pandemic has worsened operating risks due to uncertainties or unexpected events. To address this challenge, organizations are required to report on their efforts to assess and manage the emerging risks. Addressing stakeholders’ new and evolving information needs might impact the relative importance of different stakeholder groups. Crovini et al. (Citation2022) argue that in times of uncertainty, organizations need to address stakeholders’ emergent and changing information needs, requiring disclosures at a higher frequency than annual reporting. The paper suggests that involving stakeholders in the risk recognition process and disclosing ad-hoc information via multiple channels in a timely manner can facilitate the assessment of and accountability for the material risks connected to the pandemic.

Christ and Burritt (Citation2021) also reflect on how the COVID-19 pandemic affects corporate accountability practices. Focusing on accounting for, and reporting on, modern slavery risk, the paper notes that the measures taken to limit the spread of the virus broke supply chains. At the same time, border and business closures have led to increasing numbers of vulnerable workers. As modern slavery is associated with vulnerability and exploitation, the space for modern slavery will likely increase. In turn, the travel restriction, the lack of physical access to suppliers and the financial and staff constraints affects the collection of data about modern slavery, which, in turn, influences reporting and accountability practices. To overcome these important challenges, operational risk assessment, traceability infrastructures, scenario planning and material communication with stakeholders are regarded as crucial in the management of and accountability for modern slavery risk.

Another stream of this literature explores the disclosure strategies and the decisions of preparers. For instance, Elmarzouky et al. (Citation2021) investigate the opportunistic disclosure timing behavior. They argue that by voluntarily disclosing more performance associated with COVID-19 information, organizations provide investors with a positive assessment of the abilities of the management to cope with difficult situations. Thus, mitigating systematic risk and the adverse effect on the stakeholder’s perceptions. The findings suggest that the association between the level of performance disclosure in the annual reports and COVID-19 information depends on characters of corporate governance (such as board size, board independence and the number of women on the board). However, corporate disclosure decisions can also depend on the business environment. Humphreys and Trotman (Citation2021) note that during the pandemic, the business environment has changed dramatically. As a result, the context in which managers, accountants and auditors make their professional assessment and how stakeholder groups interact need to be recognized. Capital-market pressure and incentives to obtain support during challenging times can significantly shape corporate disclosure practices. For example, Chen et al. (Citation2021) find that non-state organizations, with high managerial ownership, under financial distress are more prone to hide pre-existing firm-specific bad news under COVID-19-induced uncertainty. Importantly, these disclosure strategies influence the market reaction in a favorable direction.

Collectively, the research in this theme contributes to the understanding of accounting and accountability practices in the context of the COVID-19 crisis. The analysis unveils how the pandemic's ongoing uncertainties and emergent risks give rise to dynamic forms of accountability towards a broad range of stakeholders. It also highlights the interconnections and interdependencies between social, environmental, and economic actions and consequences. This means that accounting needs to provide knowledge for and help organizations discharge accountability duties about systems and not simply areas (Adams & Abhayawansa, Citation2021). This literature sheds light on important challenges too. For example, in the rush to secure resources, organizations starting to respond to new accountability demands might adopt opportunistic disclosure behavior or tacitly lend support to unethical practices in their workforces or suppliers (Christ & Burritt, Citation2021). At the same time, there is concern that organizations might deprioritise expensive social and environmentally sustainable policies and initiatives (Adams & Abhayawansa, Citation2021; Cho, Senn, et al., Citation2021). Yet, socially and environmentally responsible businesses are less exposed to systematic risks (Bose et al., Citation2021). Given the challenges organizations face due to the pandemic, accounting research must further develop to provide new knowledge and support organizations in developing new policies and practices towards a healthier, more resilient, more equitable, and environmentally sounder society.

As the COVID-19 pandemic continues to be the cause of significant challenges to corporate disclosure, the next stage in progressing this body of research should provide innovative insights into how organizations prepare and communicate material information to their stakeholders in response to the emergent accountability demands. Future scholarship could explore the reporting approaches in times of uncertainty, shedding light on the extent to which organizations have changed their styles of accountability (Ahrens, Citation1996). Corporate reporting is continuing to evolve, accounting research and accounting scholars are well placed to increase our understanding how this evolution is meeting the accountability challenges created by the pandemic.

The next section draws the conclusions and suggests several research areas and opportunities that warrant academic investigation.

5. Conclusions and a research agenda for future research

The paper aimed to reconcile the publication patterns and propose an agenda for future research in the emerging and important area of accounting-COVID-19 literature. To achieve its aim the paper conducted a systematic analysis of the research published in accounting journals between 1st January 2020 and 15th October 2021. The paper established connections and identified key challenges and opportunities for accounting scholars to provide innovative, theoretically sound, evidence-based solutions to COVID19-related challenges.

As can be seen from the analysis in this paper, there are a wide variety of insights across several areas of accounting research. The findings show that the focus of the literature was placed on five main topic areas: public budget response; accounting education; financial markets; the public sector; and corporate disclosure (that accounted for almost 60 per cent of the literature being investigated) with limited, but growing attention devoted to areas such as “sustainability” and “management accounting”. At a methodological level, most research approaches drew on documental analysis and provided viewpoints, commentaries or autoethnographies. Given the complexities related to gaining access to social actors and venues, a large number of studies relying on such research approaches could have been anticipated. However, if we want to understand the extent to which accounting has contributed to confronting the challenges of the COVID-19 crisis, further research has the potential to investigate the complex interrelationships and interdependencies between accounting and society during and after the COVID-19 crisis.

This study contributes to accounting research in two ways. First, this paper extends accounting literature by being one of the first studies to propose a research agenda and provide a conceptual representation of the literature in this area. The paper reconciled insights from a fragmented body of research and identified the role and relevance of accounting in response to the COVID-19 crisis in a way that might not be as clear when examining individual aspects. Second, this study offered a preliminary assessment and outlined an early indication of emergent themes and challenges. Given that accounting research had time to grow, there is considerable scope for novel approaches that provide a deeper empirical and theoretical understanding of the impact and prospects emerging from the COVID-19 crisis. In conclusion, the structured approach of this paper has provided an overarching logic for creating a new understanding of the accounting-COVID-19 literature and has helped identify opportunities for future scholarship.

The COVID -19 pandemic is a major global crisis that has worsened pre-existing social, economic, ethical, and governance problems while giving rise to big new challenges for accounting and accountability studies. Firstly, tackling the pandemic and bringing it under control involved emergency budgetary spending, procurement, and appointments. It also involved intensified collection and sharing of potentially sensitive personal data. Planning, financing, cooperation, and impact of public interventions in both the COVID-19 response and recovery need to be scrutinized. The role of accounting and accountability in the scrutiny of government information on risks, preventive containment and relief measures, the availability and use of public resources should be of great concern in future research (UNEP, Citation2020). Secondly, despite the challenges of the COVID-19 pandemic, many organizations have found ways to remain functional through new processes and ways of operating. However, little is known about how accounting and accountability are implicated in the reorganization of life. The COVID-19 crisis has triggered a wide array of individual, organizational, and institutional responses. Understanding how these responses occurred and the role of accounting and accountability can inform policies and strategies for future reactions to challenging societal problems. Finally, building a more resilient society will need to go hand in hand with a renewed pledge to action on sustainability. Strategies for accountability in such situations need to work at multiple sites and levels simultaneously. This implies a shift from the local, which has been the focus of accounting and accountability work in the past decade, to include other levels and arenas.

Accounting and accountability scholarship are facing the opportunity to critically engage with novel and emerging phenomena at an early stage. To do so, accounting researchers need to promote interdisciplinary work and embrace tailored theorization, pursuing societal relevance and avoiding the trap of contributing to a conversation within the academic bubble (O'Dwyer & Unerman, Citation2016; O’Dwyer & Unerman, Citation2014; Unerman & Chapman, Citation2014). Given that the COVID-19 pandemic is a matter of global public, business and government concern and impact, accounting researchers need to engage more with the policy and practice audience. “As society provides us with resources and consent to undertake our research, the eventual (and often indirect) provision of evidence for knowledge exchange that in some way enhances society could be regarded as an ultimate purpose and justification of much of the research undertaken in accounting, finance, and other disciplines” (Unerman, Citation2020, p. 1).

While this paper focused on identifying the themes most addressed in accounting-COVID-19 research, some articles in this area address concerns that are revelatory of a future body of literature. I realize that addressing this in any depth is way beyond this paper’s scope and length. However, there are matters related to the pandemic that I think are particularly important. For example, Parker (Citation2020) discusses the examination of space issues in accounting research. Focusing on analysing historical office trends and emerging practices, Parker (Citation2020) critically examines the change strategies induced by COVID-19. The paper finds that the pandemic has prompted a transition to remote-working, shaping the re-engineering of working routines and protocols and the re-configuration of the working space. Parker (Citation2020) analysis helps surface insights related to contemporary organizational functioning, which extend beyond the time of the pandemic and the potential for the examination of time/space issues in accounting research (Picard et al., Citation2020a, Citation2020b). Potential research questions in this area may focus on the dialectics of connectivity and dysconnectivity, the future of work in organizations and the reverberation of time/space issues for the accounting profession.

The extent of the above big accounting and accountability challenges further indicates the need for quality research to address several pressing concerns posed by the pandemic. Without being prescriptive, some research themes to encourage our collective reflection on the impacts of the coronavirus crisis are proposed.

Sustainability accounting research has investigated the social and environmental implications of the pandemic, providing critical insights into sustainability reporting and performance management practices (Adams & Abhayawansa, Citation2021; Bose et al., Citation2021; Bui & de Villiers, Citation2021; Cho, Senn, et al., Citation2021; Hörisch, Citation2021; Schaltegger, Citation2020). It is possible that a certain type of research takes more time to be developed, but at the time of this study there does not seem to be much research on sustainability accounting and COVID-19. Academic investigations could contribute to developing a deeper understanding of the roles accounting can play in furthering organizational-level management and operational contributions to the response to the COVID-19 crisis and the reorganization of life (see Tregidga & Laine, Citation2021 for an important perspective). Lodhia et al. (Citation2021) provide an extensive discussion on the implications of the pandemic for the practice of, and research into, accounting for non-financial matters. In this context, the Accounting Auditing and Accountability Journal special issue on advancing research into accounting and the UN Sustainable Development Goals in 2020 (Bebbington & Unerman, Citation2020) supports this ambition. Sustainability accounting researchers are well suited to address questions such as:

- How does sustainability accounting come to be influential during the COVID-19 pandemic?

- How do forms of accounting for sustainability accounting emerge and develop in the context of the COVID-19 crisis, and how do the institutional environments influence these practices?

- How is accounting involved in the resolution of conflicts when contested values are at play?

A research area that may benefit from focus in the context of the COVID-19 crisis, is governance. Accounting scholars have provided valuable insights into how accounting contributed to the governance challenges related to COVID-19 (Ahmad et al., Citation2022;Andreaus et al., Citation2021; Bui et al., Citation2022; de Villiers & Molinari, Citation2022; Kells, Citation2020). However, several mechanisms driving institutional and organizational phenomena occur at the micro-level. This would represent an area of research aimed at answering questions such as:

- How is accounting involved in the interplay between individuals, processes and structures that superintend organizational responses to the COVID-19 pandemic?

- What role does accounting play in the aggregation and emergence of the collective construction of a COVID-19 emergency?

- How can accounting be involved in forms of sustainability governance?

Another example proposed as an area of existing research that might be stimulated by a refocus on the COVID-19 crisis, is that of risk (Carnegie et al., Citation2022;Crovini et al., Citation2022;De Vito & Gómez, Citation2020; Huang & Ye, Citation2021; Tingey-Holyoak & Pisaniello, Citation2020; Velayutham et al., Citation2021; (Yu et al., Citation2021). In this context, accounting scholars need to critically re-examine the processes through which social/societal/natural risks are created (or subsided) and become financially material. Accounting researchers are well suited to address questions such as:

- How can performance measurement systems be redesigned to account for sudden shocks?

- How can accounting and biophysical data be linked to assist short- and long-term decision-making and future-oriented risk planning and management?

- What strategies have been (or can be) adopted to expand reporting practices, and how do they influence different institutional settings during (or after) the COVID-19 emergency?

Accounting scholars have provided insights into performance planning, management, control and disclosure related to the COVID-19 crisis in a variety of empirical and jurisdictional contexts (Broadbent, Citation2020; Huber et al., Citation2021; Kober & Thambar, Citation2022; Lapsley, Citation2020; Mai, Citation2020; Padovani & Iacuzzi, Citation2021; Parisi & Bekier, Citation2022; Passetti et al., Citation2021; Sian & Smyth, Citation2022). The experience of going through the COVID-19 pandemic affected people on a deep, personal level. Increasing individual frustration and mental exhaustion created by the new forms of social interaction (and lack of) coupled with a sudden shift of working practices led to the problematisation of the concept of performance. Future research could critically examine the role of management accounting and management accountants in understanding the measurability of the impact of COVID-19 and the following reorganization of life. This would represent an area of research aimed at answering questions such as:

- Where and how do management accountants fit into the understanding and challenge of the COVID-19 crisis?

- What mechanisms link action and outcomes in the context of COVID-19 where there is no clear causality?

- How can performance measurement systems be designed to consider temporal, conscious, and unconscious factors that characterize the situational nature of performance?

Finally, academic investigations could contribute to developing a deeper understanding of how and why accounting becomes associated with different areas. Comparative studies, for instance, may offer valuable opportunities to increase the understanding of the framings and structures that generate both spatial and temporal differences among the approaches taken to respond to the COVID-19 crisis. Comparative research is well suited to address questions such as:

How do organizations deal with, and account for, scarcity and rivalry in non-financial capitals during the COVID-19 crisis?

How do space and time operate in the context of organizational response to the COVID-19 crisis?

How to develop and use performance-management frameworks, with a particular focus on indicators of impact/outcome?

Future research could add to these contributions by developing in-depth theoretical knowledge. Given the considerable breadth and depth of complexity underlying the role of accounting in the context of the COVID-19 pandemic, future development of accounting research would benefit from a greater theorized engagement that could include:

developing new theoretical models to provide novel understandings of organizational transitions;

developing decision-making frameworks aimed at assisting organizations and institutions in the context of sudden shocks;

critiquing existing ideas aimed at promoting the development of newer and sounder practices.