?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

In this article we develop semiparametric regression techniques for fitting partially linear additive models. The methods are for a general Hilbert-space-valued response. They use a powerful technique of additive regression in profiling out the additive nonparametric components of the models, which necessarily involves additive regression of the nonadditive effects of covariates. We show that the estimators of the parametric components are -consistent and asymptotically Gaussian under weak conditions. We also prove that the estimators of the nonparametric components, which are random elements taking values in a space of Hilbert-space-valued maps, achieve the univariate rate of convergence regardless of the dimension of covariates. We present some numerical evidence for the success of the proposed method and discuss real data applications. Supplementary materials for this article are available online.

1 Introduction

We study useful semiparametric regression techniques that can be used for analyzing a finite or infinite dimensional response variable. The response variable takes values in a general separable Hilbert space. The model consists of a parametric and a nonparametric part. The parametric part is linear in a covariate (predictor) vector, say for

, and the nonparametric part is to model the effect of another covariate vector, say

for

. To avoid the curse of dimensionality in estimating the nonparametric part, it is assumed that the nonparametric effect is additive in Z, that is, it adds the unknown nonparametric effects of the individual covariates Zk. We consider two scenarios for X. One is that both Xj and Zk are real-valued, and the other that Xj take values in the Hilbert space where the response variable takes values while Zk are real-valued. The new techniques are important extensions of the partially linear additive regression for scalar responses coupled with scalar covariates studied by Yu, Mammen, and Park (Citation2011). In this article, we develop powerful techniques of estimating the models and provide sound theory that supports the methodology.

Our framework of Hilbert-space-valued (henceforth, Hilbertian) responses can be specialized to various data types. Its coverage is broad enough to include random variables, random vectors, random functions, random densities, compositional random vectors, infinite sequence random vectors, and compositional random functions, etc. All these types are commonly encountered in today’s data environments. The present work also provides a base toward semiparametric regression for other response spaces, such as Riemannian manifolds and Lie groups, along the way paved by Lin, Müller, and Park (Citation2022). The latter work pioneered a link connecting additive regression for manifold-valued responses to Hilbertian additive regression (Jeon and Park Citation2020) via Riemannian logarithmic map. Despite its importance, semiparametric regression with Hilbertian responses remains unexplored. To the best of our knowledge, this is the first attempt to study a semiparametric regression model for general Hilbertian responses.

We prove that our estimators of the parametric effects of Xj are -consistent in case Xj are real-valued. We also derive the joint asymptotic distribution of the parametric estimators. For Hilbertian Xj, we show that the corresponding parametric estimators are still

-consistent if the Hilbert space where Xj take values is of finite-dimension, while they achieve a slightly slower rate if the Hilbert space is of infinite-dimension. Furthermore, we show that our methodology of estimating the nonparametric effect of the covariate Z is free from the curse of dimensionality, that is, affords a univariate rate of convergence regardless of the dimension of Z. This is in contrast with the partially linear modeling approach that does not have additivity structure in the nonparametric part. The latter suffers from the dimensionality problem. Not only the nonparametric part, our approach also improves the estimation of the parametric part. Indeed, we demonstrate, theoretically and numerically, that using additivity structure in the nonparametric part leads to efficiency gain in the estimation of the parametric part. It turns out that the gain is larger if

are farther from being additive.

The present work is not considered a direct extension of Yu, Mammen, and Park (Citation2011). Dealing with a general Hilbert space, instead of the conventional , as the space of the values of the response variable, needs a number of innovations in developing relevant methodology and theory. In case Xj takes values in

, the theory requires to assess the stochastic magnitude of terms of the form

for some

, which is a known function of

, and for some stochastic (random) map

, which is a random element taking values in the space of Hilbertian maps

for a Hilbert space

and a compact subset S of

. The usual way of analyzing such a

-weighted average is to consider a large set

to which

belongs with a high probability, and then derive the maximal stochastic size of

over

using an entropy bound for the set

. The set

embodies Hilbertian maps

. In case

is finite-dimensional as Euclidean spaces, the entropy of

is finite although the dimension of

may be infinite, particularly when

is a class of nonparametric maps g. In case

is infinite-dimensional, however, the entropy of

is infinite so that it is not feasible to apply the empirical process theory directly to the

-weighted average. To resolve this difficulty we take the Hilbertian norm of the

-weighted average, and convert its maximal stochastic size to that of a

-weighted average where

is a stochastic map from S to

. The conversion with the associated calculation of the sizes of various stochastic terms is one of the challenges we tackle in this article. For Hilbertian Xj taking values in

, however, a similar idea leads to dealing with

, where

is an

-valued function of

and

is a stochastic map from

to

. It turns out that the class embodying the latter stochastic map with a high probability does not necessarily have a finite entropy. Thus, the case of Hilbertian Xj needs a different treatment, which is another difficulty we resolve in this work.

Our proposals are related to Jeon and Park (Citation2020), which developed a smooth backfitting technique for additive regression with Hilbertian responses. The latter, however, is for additive models without parametric component X, and for additive regression of additive effect, that is, for estimating the “assumed” additive effect of Z. It does not cover cases where the additivity model assumption is violated in additive regression. In contrast, our work is for models with linear effect of X in addition to the additive nonparametric effect of the covariate vector Z. Dealing with the additional linear effect necessarily involves additive regression of nonadditive effects. In this respect, our theory for additive regression is more general than the one in Jeon and Park (Citation2020). Moreover, our modeling approach allows for discrete type covariates (ordinal or nominal), which arise in a variety of statistical problems.

In the case of a functional response, say for a domain

, which is a special case of Hilbetian response, one might think of applying a technique for scalar responses, such as the one in Yu, Mammen, and Park (Citation2011), in a pointwise manner to Y(t) for each

and combine the pointwise results

, to construct

. However, this naive approach is problematic since the resulting

is not guaranteed to take values in the space where

comes from. This is particularly the case when

has constraints, for example,

and

, like a random density. Similarly, for a compositional response

with

and

, component-wise regression with Yj for each j does not give simplex-valued

as a whole. Our approach does not have these drawbacks when specialized to functional and compositional data since it applies directly to the observations of functional

and of compositional vector Y, respectively, as data objects.

A few past works on semiparametric regression for real-valued responses include the estimation of partially linear models without additivity structure in the nonparametric part (Bhattacharya and Zhao Citation1997; Liang Citation2006), and of partially linear additive models (Opsomer and Ruppert Citation1999; Liang et al. Citation2008; Yu, Mammen, and Park Citation2011; Lee, Han, and Park Citation2018). Among the latter four studying partially linear additive models, Opsomer and Ruppert (Citation1999) and Liang et al. (Citation2008) employed the ordinary backfitting technique (Buja, Hastie, and Tibshirani Citation1989) to estimate the additive nonparametric part, while Yu, Mammen, and Park (Citation2011) and Lee, Han, and Park (Citation2018) used the smooth backfitting technique (Mammen, Linton, and Nielsen Citation1999). The smooth backfitting method has been proved to be successful in various structured nonparametric models under weak conditions (Yu, Park, and Mammen Citation2008; Linton, Sperlich, and van Keilegom Citation2008; Lee, Mammen, and Park Citation2010, Citation2012; Zhang, Park, and Wang Citation2013; Bissantz et al. Citation2016; Han and Park Citation2018; Han, Müller, and Park Citation2020). On the contrary, the ordinary backfitting is known to work under stronger conditions on covariates (Opsomer and Ruppert Citation1997).

2 Additive Regression

Our approach to the semiparametric regression requires the estimation of “best” approximations of for W being a general Hilbertian random element, or a real-valued random variable in the respective spaces of “additive” maps. This section is devoted to characterizing the best approximations and their estimation. We assume that Z is supported on

.

2.1 Projection on Additive Function Space

We consider a general separable Hilbert space, denoted by . Euclidean spaces, L2 spaces, Bayes-Hilbert spaces and simplices are special cases of

. Here and below, we denote

-valued maps, random elements taking values in

and their values in

, by bold-faced symbols. Note that we also use bold-faced symbols to denote random vectors and their realizations. Let

be the zero vector in

the inner product of

and

the associated norm. We denote by

and

the operations of vector addition and of scalar multiplication in

, respectively. Let

denote the subtraction operation defined by

.

We let denote the space of additive maps

such that

and

for some

. For a random element W taking values in

with

, let

denote the projection of the mean regression map

onto

. That is,

(2.1)

(2.1) where f is the joint density of Z. For the definition of the conditional expectation for Hilbertian W, we refer to Bosq (Citation2000). The minimizer

with

satisfies

(2.2)

(2.2)

for each

and for all zj with

. Here and below,

for a d-vector z is

, and fj and fjk are the densities of Zj and (Zj, Zk), respectively. The integrals in (2.2) are special cases of the so called “Bochner integral” (Jeon and Park Citation2020), the latter being for Banach-space-valued maps. From (2.2), we see that the additive map

is characterized as the solution of the following system of Hilbertian integral equations:

(2.3)

(2.3)

We note that (2.3) does not define a component tuple , but only the sum of its entries,

. Obviously, if

satisfies (2.3), then

also satisfies (2.3) for any constant

. We also note that

is different from the regression map

unless

belongs to

. Thus, the problem of estimating

, which we present in Section 2.2, is different from that of estimating

under the assumption

, the latter having been studied by Jeon and Park (Citation2020).

2.2 Estimation of Additive Projection

We now discuss the estimation of . The basic idea is to replace the marginal regression maps

and the densities fj and fjk in (2.3) by the corresponding kernel estimators and then to solve the resulting system of equations. We note that our method requires the estimation of

for real-valued Xj and of

for Hilbertian

, as well. Below, we describe the method for W taking values in a general Hilbert space, since specialization to the case of random variables is immediate from the general treatment.

Suppose that we have n observations, , with

. We estimate the marginal regression map

for

by

(2.4)

(2.4) where

is a kernel estimator of fj. We also estimate fjk by

. Here and throughout the article,

is a normalized kernel function defined by

where h > 0 is the bandwidth,

and

is the baseline kernel function. This type of normalized kernels have been used in the literature (Yu, Park, and Mammen Citation2008; Lee, Mammen, and Park Citation2010, Citation2012; Jeon and Park Citation2020). It has the property that

for all

, which gives

and

for all

. Plugging these estimators into (2.3) gives the following estimated system of Hilbertian integral equations:

(2.5)

(2.5)

In the supplement S.7, we will show that the system of Equationequations (2.5)(2.5)

(2.5) has a unique solution, which we denote by

. Just like that the system of equations at (2.3) determines only

, the EquationEquation (2.5)

(2.5)

(2.5) by itself defines only

, not individual components

. The solution

does not have a closed form, but can be computed by iteration starting with an initial tuple

. We may simply take

, for example. In the rth (

) cycle of the iteration, we update

by

(2.6)

(2.6)

In the supplement S.7, we will show that converges to

as

, see Proposition S.1. In the iteration, we can evaluate the Bochner integrals in (2.6) by the conventional Lebesgue integrals, provided that

are linear in

, that is,

for some real-valued functions

. This is because the marginal

are also linear in

so that all the subsequent updates

for

are linear in

. For a linear form

with real-valued weight functions

, it holds that

where the integral on the left side is in Bochner sense while the one on the right hand side is a Lebesgue integral.

The regression map is not assumed to be additive and thus estimating the additive map

is considered additive regression of nonadditive effect, which is different from additive regression of additive effect, developed by Mammen, Linton, and Nielsen (Citation1999) and Jeon and Park (Citation2020). The very core of the matter in the present case regarding additive regression is that, when we write

with

as an error term,

. Instead, by the definition of

, we have

for all

. This implies that, for all

and for all

with

,

. This gives

(2.7)

(2.7)

We show that the latter is enough for the theory of , see the supplement S.7 for details.

3 Hilbertian PLAM with Scalar Covariates

We introduce a partially linear additive model for a -valued response Y and covariate vectors

and

taking values in

and

, respectively, and present a way of estimating the model. We allow the entries of X to be discrete (nominal or ordinal) while assuming that all entries of Z are of continuous type supported on

. We assume that

for all

.

3.1 The Model

The Hilbertian partially linear additive model (HPLAM) is given by

(3.1)

(3.1)

where are unknown constants in

,

are unknown component maps with

satisfying the constraints

(3.2)

(3.2) and

is a Hilbertian error term such that

and

. Below, we give a proposition that establishes the identifiability of

and

in the model (3.1). Let

denote the distribution of a random vector or element U. We make the following weak assumption.

(A0) The has a density with respect to the product measure

, which is bounded away from zero on the support of

. The marginal distribution

has a density f with respect to the Lebesgue measure such that

for all

, and the support of

is not contained in a hyperplane in

.

Proposition 3.1.

Let for

be Hilbertian constants and

for

be Hilbertian maps with

and

. Assume the condition (A0). Then,

(3.3)

(3.3) implies

and

a.s. for all

and

.

A proof of Proposition 3.1 is given in the supplement S.1. With (3.2), we have , so that by plugging the expression into (3.1) we may rewrite the model (3.1) as

where

and

.

3.2 Estimation of Parametric Components

Here, we discuss the estimation of using the profiling technique (Severini and Wong Citation1992) in conjunction with the estimation of additive projections presented in Section 2.2. Let

and put

. Note that

does not involve

. Then, under the model specification (3.1),

(3.4)

(3.4) where

. Here and below,

for

and

. Considering

for each

, which solves the system of Equationequations (2.3)

(2.3)

(2.3) with

and noting that

, we get

According to the arguments leading to Corollary S.1 in the supplement S.7, is linear in W in the sense that

and

for all Hilbertian variables

and Hilbertian constant c. Also, it holds that

for all Hilbertian constants

and random variables Wj. Thus,

. Furthermore, we also get

and likewise

. This gives

(3.5)

(3.5)

We estimate by minimizing an empirical version of the objective functional at (3.5). Define

where

for

and

, respectively, are the solutions of (2.5) for

and

. Put

. Then,

. We propose to estimate

by

(3.6)

(3.6)

We present an explicit form of defined at (3.6). The Gâteaux derivative of the objective functional in (3.6) at

to an arbitrary direction

equals

Equating the above derivative with zero for all gives

From this we get that, whenever the p × p matrix is invertible,

(3.7)

(3.7) where

for

and

, and

for a p × p real matrix

and

. With

defined at (3.7) we estimate

in the model (3.1) by

where

and

. In Section 7.1, we will show that

is invertible with probability tending to one and that

is

-consistent and

converges to a mean zero Gaussian random element taking values in

.

3.3 Estimation of Nonparametric Components

We estimate in the model (3.1) by

, which solves the system of equations at (2.5) with

. From the linearity of

in

(Corollary S.1 in the supplement S.7), it holds that

, where

. To estimate the individual component maps

satisfying the constraints

, we put the following constraints on

:

(3.8)

(3.8) where the integrals are in Bochner sense. Then, the constraints (3.8) identify the individual

uniquely such that

.

To see how the constraints identify a unique set of , let

be an arbitrary tuple such that

. Choose

. Obviously, each

satisfies (3.8). It also holds

(3.9)

(3.9) which gives

. To see (3.9), we note that, since

, the tuple

satisfies

for all k. Integrating both sides over

then gives

The first equality in the above equations follows from , and the second from

in view of (2.4).

3.4 Hilbertian PLM

We discuss briefly the estimation of the Hilbertian partially linear model (HPLM): , where m is allowed to be nonadditive, that is, m may not belong to

. It deserves being discussed in this article since there has been no study on this model for Hilbertian responses, to the best of our knowledge, and it helps to understand our numerical results to be presented in Section 5.

Let be a multivariate kernel estimator of

defined by

(3.10)

(3.10)

Likewise, let be a multivariate kernel estimator of

, which is obtained by changing

in (3.10) to

and the vector operations for

to those for

. Let

, which should be differentiated from

. Put

. Also, let

and

. Define

Applying the idea of profiling, explored in Section 3.2 for the HPLAM, now to the HPLM, we may estimate by

(3.11)

(3.11) and

by

, where

is the jth entry of

. We note that

takes the same form as

at (3.7) with

and

taking the roles of

and

, respectively.

Let . Note that

if all

are additive maps, that is, belong to

. According to the theory in Section 7.1, under the HPLAM model (3.1), the asymptotic variances of

are equal to or larger than those of the respective

, see the EquationEquation (7.2)

(7.2)

(7.2) . The gains by

against

get larger as the diagonal entries of

grow farther away from the respective diagonal entries of

.

4 Hilbertian PLAM with Hilbertian Covariates

In this section we consider the case where the covariates in the parametric part are also Hilbertian. We continue to use the notation for Hilbertian

. Assume that

for all

.

4.1 The Model

Here, we assume that the Hilbert spaces for are the same as

. In Section 4.3, we discuss the case where the spaces for

are different from each other or from

. We study the following Hilbertian partially linear additive model

(4.1)

(4.1) where

is an unknown constant in

but βj for

are now unknown constants in

. The component maps

and the error term

are as in the model (3.1) with the constraints (3.2). As in Section 3.1, we find

and thus may rewrite the model (4.1) as

(4.2)

(4.2)

where

and

.

Under a weak assumption, the constraints (3.2) also entail the identifiability of the model (4.1). To state a proposition for the identifiability, we introduce new symbols for matrices and vectors of Hilbertian elements. Let for

and

denote the p × p matrix whose (j, k) element equals

. Also, let

and

for

and

denote

and

vectors, respectively, whose jth entries are

and

. In this notation,

denotes the p × p matrix whose (j, k)th element equals

. We make the following assumption.

(B0) The joint distribution has a density with respect to the product measure

, which is bounded away from zero on the support of

. The marginal distribution

has a density f with respect to the Lebesgue measure such that

for all

, and the matrix

is positive-definite.

Proposition 4.1.

Let and

for

be constants and

for

satisfy

and

. Assume the condition (B0). Then,

(4.3)

(4.3) implies

and

a.s. for all

and

.

A proof of Proposition 4.1 can be found in the supplement S.2.

4.2 Estimation of the Model

Put . From (4.2), it holds that

where

. Noting that

with

, and using that

is linear in W for any Hilbertian W, we get

Let and

. We estimate

by

(4.4)

(4.4)

Put and let

denote the p × p matrix whose (j, k)th element is given by

. Also, let

denote the p-vector whose jth element is given by

. By taking the Gâteaux derivative of the objective functional in (4.4), we find that

(4.5)

(4.5) provided that

is invertible. In Section 7.2, we show that

is invertible with probability tending to one. With

defined at (4.5) we estimate

in the model (4.1) by

, where

and

.

We also estimate by the solution

of the system of Equationequations (2.5)

(2.5)

(2.5) with

By arguing as in Section 3.3, we may show that is uniquely decomposed into

with the constraints at (3.8).

4.3 Discussion

One may wonder if the linear part of the model (4.1) covers the standard function-on-function linear regression model when and Y are functional variables of infinite-dimension. In fact, such a functional linear model reduces to the model (3.1), not to the one at (4.1). To see this, consider the case with p = 1 for simplicity, that is, in the linear part of the model, there is only one covariate, say X, taking values in

with

. Let the response variable

take values in

for some

. The standard function-on-function linear regression model (Ramsay and Silverman Citation2005; Yao, Müller, and Wang Citation2005; Benatia, Carrasco, and Florens Citation2017) with the covariate

is given by

such that

(4.6)

(4.6) where

and

are considered as parameters. Let

and

be known bases of

and

, respectively. An approach in, for example, Ramsay and Silverman (Citation2005) is to take, as the space for

, a tensor product of finite-dimensional subspaces of

and

. In this approach θ is represented as

(4.7)

(4.7)

for some

. In our discussion, we allow

while we assume L1 is finite and fixed. For the functional covariate

, put

Then, plugging the representation at (4.7) into the model (4.6) we get

(4.8)

(4.8)

Letting ξj and take the respective roles of Xj and

in the model (3.1), the model (4.8) reduces to a special case of the linear part of the model (3.1) in Section 3.1. The above observation manifests that our model at (3.1) accommodates even infinite-dimensional θ in the standard function-on-function linear regression model (4.6), and the theory developed in Section 7.1 applies directly to this case.

One may think of an alternative basis generating θ, based on the functional principal components of and

. In this way, θ is represented as at (4.7) but now with

and ψk being the eigenfunctions of the respective covariance operators of

and

. The main difference from the previous approach is that

and ψk are unknown. Thus, incorporating the unknown basis into the model at (4.6), ξj at (4.8) are not observed but need to be estimated. Put

where

are the eigenfunctions of the sample covariance operator based on

. Then, the estimation of the model (3.1), which incorporates (4.8) into the linear part, boils down to an errors-in-variables problem with “small” errors in observing the true covariate values

. Certainly, the “measurement errors,”

, affect the estimation of

and

in the model (3.1). However, it is different from a typical errors-in-variables problem since the measurement errors are vanishing as

. Elaborating more on this, we let

now diverge as

. If

and the eigenvalues λj corresponding to

satisfy the standard separation condition that

for some constants C > 0 and

as in, for example, Hall and Horowitz (Citation2007), then Lemma 2.3 in Horváth and Kokoszka (Citation2012) assures that

. The latter implies that

for each i. If we further assume that

for some constant

, then we may show that

. Following the arguments as in, for example, Jeon and Van Bever (Citation2022), we expect that this would add an extra error of size

to the errors of

and

presented in Section 7.1.

The model (4.1), as it stands, assumes that the spaces for are the same as

, the space for Y. However, the limitation is not essential. Basically, there is an isometric isomorphism that maps the space for

, say

, to

, provided that

. Let it be called

. Then, one may let Y depend on

, via

, so that one may postulate

(4.9)

(4.9)

The methodology of estimating the above model (4.9) and the associated theory follow directly from those for the model (4.1) by letting in the model (4.9) take the roles of

in the model (4.1).

One may be also interested in the case where the covariates in the nonparametric part, now denoted by for

, are also Hilbertian. Here, we briefly discuss a method designed for finite-dimensional

. Dealing with infinite-dimensional

in our framework is infeasible since then one needs to estimate nonparametric functions defined on infinite-dimensional domains. Let

take values in a compact subset

of a qk-dimensional Hilbert space

. Then, one may consider a version of the model (3.1) or of the model (4.1) with

now being defined as a map from

to

. For a general Hilbertian W, one may also obtain the following version of the system of equations at (2.5):

(4.10)

(4.10)

Here, μk is the pushforward measure induced by the qk-dimensional Lebesgue measure given by

for

, and

is an isometric isomorphism. Also,

and

are kernel-based estimators of

, the density fj of

and fjk of

, respectively. We refer to Jeon, Park, and Van Keilegom (Citation2021) for concrete forms of these estimators. Then, one is able to estimate the model with Hilbertian

in the same way as we estimate the models (3.1) and (4.1), solving the system of Equationequations (4.10)

(4.10)

(4.10) for various choices of W.

5 Simulation Studies

5.1 Bandwidth Selection

The construction of or

for

and

in computing

, requires choosing a set of bandwidths

. There is another set of bandwidths we need to select to construct

, solving (2.5) with

. In our theoretical development in Section 7, we allow these bandwidth sets to be different from each other. In our numerical study, however, we simply took

from the already calculated

,

and

based on a set of bandwidths

. To choose the single bandwidth set, we used the CBS (Coordinate-wise Bandwidth Selection) algorithm introduced in Jeon and Park (Citation2020), instead of a full-dimensional grid search. The algorithm is reproduced in the supplement S.3. However, for the approach of HPLM without additive modeling introduced in Section 3.4, we used the bandwidths obtained from a full-dimensional grid search. The CBS algorithm is based on a cross-validation criterion. In our simulation study discussed below within Section 5, we used a 10-fold cross-validation, while in the real data applications presented in Section 6, we employed a 5-fold cross-validation. For numerical integration in the implementation of the iterative algorithm at (2.6), we used a trapezoidal rule with 101 equally spaced grid points.

5.2 Data Generating Models

We conducted simulation studies for the model (3.1) with a density response taking values in the Bayes-Hilbert space

defined in the supplement S.4. We considered several cases with p = 2 and d = 2 or 3. For the covariates Zj in the nonparametric part, we took

, where

is the cumulative distribution function of N(0, 1) and

is a multivariate normal random vectors with

and

for all

. This allows for dependence among Zj when

. For X1 in the parametric part, we took

with

Here, is

independent of Z and

We note that is nonadditive while

is additive such that

(5.1)

(5.1)

(5.2)

(5.2) for all

with

for some gj. For X2, we set

, where

is

independent of Z and

, and η2 is given by

so that it is nonadditive with

(5.3)

(5.3)

We note that, if α = 0, then . Because of (5.2),

is perpendicular to

when ρ = 0, in which case Z1 and Z2 are independent with densities

, in the sense that

for all

. This implies that

when ρ = 0, and thus

gets farther away from

as α increases, so that α controls the degree of departure of

from

. We also note that (5.1) and (5.3) give

(5.4)

(5.4)

We considered four models to generate . The first model is given by

For in Model 1 and others below, we took

where

is a linear interpolation of

for

and

are iid

, independent of

and

. Put

. Then,

where

is the norm for the space

defined through (S.6) in the supplementary materials. Since

are iid N(0, 1), we get

. The coefficients

, which themselves are densities on

, are chosen as follows:

where

and Cj are chosen so that

. Because of (5.4), it holds that

The components m1 and m2 are also normalized. Specifically,

where c1 and c2 are chosen so that

for j = 1, 2.

As discussed briefly in Section 3.4 and demonstrated by our theory in Section 7.1, our estimator gets more stable than

at (3.11), which ignores the additivity structure in the nonparametric part of the model, if

grows farther away from the zero vector. Put

(5.5)

(5.5)

In Model 1 where ρ = 0, we may find exact formulas for and

. Indeed, when ρ = 0, we get

from (5.2) and

, where

is the projection of η2 onto

. Since

and

are independent,

and

are also independent conditional on Z. From these, we may find that the ith diagonal entries

and

of

and

, respectively, are:

(5.6)

(5.6)

From the formula (5.6) and according to Theorem 7.1 with the discussion that follows, we get that, under Model 1, the asymptotic gains by against

are

(5.7)

(5.7)

Through the simulation with various values of α under Model 1, we may see how these theoretical gains by take effect empirically.

For the second model we specialized to

, that is, took α = 1, and also fix

in the generation of

. Other than that, it is the same as Model 1. The third and fourth models have the same parametric part as the second one. The third model has a nonadditive map in the nonparametric part, while the fourth has a three dimensional additive map. Specifically,

Here, the density-valued maps m3 and are given by

where c3 and

are chosen so that

. We considered Model 3 to see the sensitivity of our approach to the violation of additivity in the nonparametric part, and Model 4 to learn the effect of increased dimension of Z, in comparison with Model 2.

5.3 Simulation Results

We generated N = 500 pseudo samples of sizes n = 200 and 400 according to the four models specified in Section 5.2. We computed Monte Carlo approximations of

(5.8)

(5.8) and those for

. For the estimators of the nonparametric parts, we approximated

(5.9)

(5.9)

and those for the PLM, based on the 500 pseudo samples. The target

in this computation was the centered version of

or

, that is, for Models 1 and 2, for example,

(5.10)

(5.10)

The centering introduces the coefficient , which for Models 1 and 2 is given by

.

reports the values of the measures for Model 1. For Model 1, the theoretical gain by against

does not depend on α as shown by (5.6) and (5.7). This is confirmed by the MSE values in the column of β2 in the table. For

against

, however, we get from (5.1) and (5.7) that

. The MSE values in the column of β1 are roughly in accordance with this formula. For example, in case α = 1 and n = 200, the theoretical value equals

while the corresponding empirical value is

. The results in the table also demonstrate that our approach leads to more accurate estimation for the nonparametric part as well.

Table 1 Mean squared error (MSE), squared bias (SB), and variance of , as defined at (5.8), and mean integrated squared error (MISE), integrated squared bias (ISB), and integrated variance (IV), as defined at (5.9), under Model 1, multiplied by 103.

Comparing the values for different sample sizes, we see that the results in obey the theoretical rates of convergence. The rate for the parametric part is for both PLAM and PLM, while those for the nonparametric part equal

for our method and

for the PLM, provided that the corresponding optimal bandwidth sizes are used. We find that, in estimating m0 and βj, the ratios of the MSE values for n = 400 against n = 200 roughly coincide with the theoretical value

. In estimating the nonparametric part

, the ratios of the MISE values are nearly identical to the theoretical values

and

, respectively, for our estimator and for the PLM. For instance, in case α = 0, the empirical ratio

for our estimator is roughly the same as 0.574, while

for the PLM approximates well the theoretical value 0.630.

reports the values of the measures at (5.8) and (5.9) for Models 2–4. Recall that, in these models, X1 is the same as the one under Model 1 when α = 1, but are correlated to each other via the correlation

among Uj. From the table, we first learn that our proposal continues to dominate the PLM when the covariates in the nonparametric part are correlated, when their effects are nonadditive, or when their number increases. The comparison between the values for Model 2 and those for Model 1 with α = 1 may reveal the effect of correlation among covariates. We observe that the presence of the correlation increased the values of MSE and MISE slightly for our estimators. For the PLM, in estimating βj, the asymptotic theory at (7.1) in Section 7.1 tells that introducing correlation between Zj does not affect the asymptotic MSE properties of

because

and

are independent of Z in our simulation setting. This is confirmed empirically by comparing the values, corresponding to the PLM, in the columns of βj for Model 2 in , with those for Model 1 (α = 1) in .

Table 2 Values of measures of performance for and

(

) under Models 2, 3, and 4 where Zj are correlated, multiplied by 103.

Now, we note that Models 3 and 4 differ from Model 2 only in the nonparametric part. In the computation of the values for Model 3, the target was actually the centered version as at (5.10) for

. The MSE values in the columns of βj for Model 3, in comparison with those for Model 2, demonstrate empirically the insensitivity of both

and

to non-additivity in the nonparametric part, as asserted by Theorem 7.1 and the discussion that follows. Indeed, our theory tells that

and

determine the asymptotic distributions of

and

, respectively, and these have nothing to do with the structure of the nonparametric part. As for the estimation of the nonparametric part, the MISE values of both our estimator and the PLM for Model 3 are smaller than the corresponding ones for Model 2. This is due to the fact that

is easier to estimate than

. Comparing the values for Models 2 and 4, we see that the increased dimension of Z does not affect the precision of the estimators of βj. It increases the MISE values of the nonparametric part, moderately for our estimator but substantially for the PLM. This illustrates the dimensionality problem with the PLM approach. Finally, we find that, as the results in , those in as well are in accordance with the corresponding theoretical rates of convergence.

and also report the average computing time, given a set of bandwidths chosen by a cross-validation criterion. The results indicate that the calculation of the Hilbertian PLAM estimators takes two or three times more than the computation of the Hilbertian PLM estimators, except in the case of Model 4 where the covariate dimension in the nonparametric part is higher than the other models. The comparison of computing time demonstrates how much extra computational time one needs to perform the smooth backfitting iteration, which the Hilbertian PLAM requires while the Hilbertian PLM does not.

6 Application to U.S. Presidential Election Data

We present a real data application for the model (4.1). Another real data application for the model (3.1) can be found in the supplement S.6. It is believed that the underlying political orientation and population characteristics of a region affect an election result for the region. To validate this belief in the United States, we analyzed the 2020 U.S. presidential election data. We put the observed proportions of votes earned by Democratic Party (), Repulican Party (

) and the rest (

) for the ith state into a vector

, and took the compositional vectors as the observations of the response Y. We considered such three categories since the first two parties received the major spotlight in the election. We note that Y satisfies the two constraints

and

, and thus, it takes values in

, which is a two-dimensional Hilbert space as detailed in the supplement S.5. As a covariate, we considered a compositional vector

that comprises the proportions of votes earned by the same parties in the 2016 U.S. presidential election. We added three other covariates in the model building, which are the proportion of people who have a bachelor or a higher degree (Z1), per capita income (Z2) and median age (Z3). The observations on these socio-demographic variables Zj were obtained from https://www.census.gov/acs/www/data/data-tables-and-tools/data-profiles/2019/. The observed value

of the Hilbertian covariate

is considered to represent the political orientation of the ith state, and the values of the socio-demographic covariates, Zij for

, measure the state’s education, wealth and age levels, respectively.

We applied the Hilbertian partially linear additive regression approach based on the model (4.1) with the covariates and Z3. In doing so, we applied trapezoidal rules based on two different grids to approximate the integrals in the iterative algorithm at (2.6): one with 101 equally spaced points (Dense) and the other with 21 (Sparse). We also used two different bandwidth selectors: one was the CBS bandwidth introduced in Section 5.1, and the other an optimally chosen bandwidth for density estimation (KDE) according to the R function “h.amise” in R package “kedd (version 1.0.3).” Based on these options we implemented the three combinations: Dense-CBS, Sparse-CBS, and Dense-KDE. As a competing approach, we also chose the Hilbertian additive regression approach of Jeon and Park (Citation2020), which uses only the scalar covariates

, with the Dense-CBS scheme. We compared the prediction performance of these approaches via the leave-one-out average squared prediction error (ASPE) defined by

where n = 51 and

is the predicted value of

obtained without the ith observation. The above definition of ASPE is based on the geometry of

given in the supplement S.5. The values of the ASPE for our approach with the Dense-CBS, Sparse-CBS, and Dense-KDE schemes were respectively 0.063, 0.063, and 0.070, while the application of Jeon and Park (Citation2020) gave 0.198. Thus, our partially linear additive modeling approach incorporating the compositional covariate improved the prediction performance greatly. It turned out that the size of grid in numerical integration does not have significant effects on the prediction performance. However, it turned out that the CBS scheme taking into account the values of Y outperforms the scheme based on KDE.

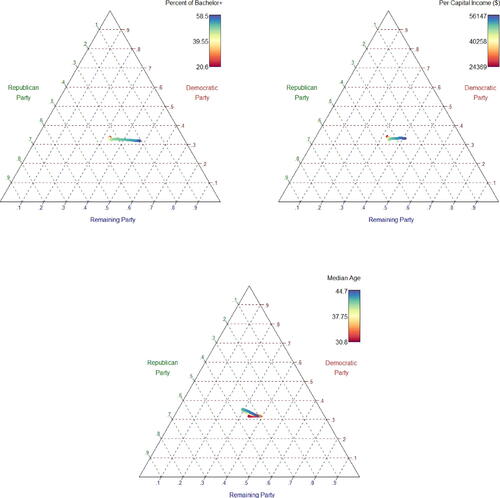

To see the effects of the covariates, we estimated the model (4.1) using the whole dataset with the Dense-CBS scheme. We obtained that . The result with such a large positive value demonstrates that the party supporting tendency in the 2020 U.S. election is tied strongly with that in the 2016 election. Thus, the empirical result provides a strong evidence that the underlying political orientation is an important determinant for the presidential election. The estimated component maps are depicted in , which visualize the effects of the socio-demographic variables on the election results. A clear lesson from the estimated maps is that the approval rate for the Democratic candidate remains unchanged as education level or income level increases, while it decreases for the Republican candidate and increases for the group of other candidates. The effects of age do not seem to have a monotone pattern.

Fig. 1 The estimated component maps for the population characteristics based on the proposed method applied to the U.S. election data.

7 Theoretical Development

7.1 Asymptotic Theory: Scalar Covariates

Here, we discuss the case where and

take values in

and

, respectively. We assume that

for

are iid copies of

such that

. Recall that

, for each

, is the solution of (2.3) with

,

and

. We let

denote the bandwidth set we use in the construction of

and

for

and

. Recall

, which solves (2.5) with

. We let

denote the bandwidth set we use in the construction of

with

and

at hand.

7.1.1 Technical Assumptions and Invertibility of

We collect the technical assumptions we use for our theoretical development.

(A1) The joint density f is bounded away from zero and infinity on its support

(A2) The real-valued additive functions

(A3) The Hilbertian error variable

(A4) The p × p matrix

(A5) There exist constants

(A6) The baseline kernel K is symmetric and positive on

(A7) The bandwidths hk satisfy

(A8) The bandwidths bk satisfy that

The conditions (A1) and (A2) for are typically assumed in the smooth backfitting literature, see Jeon and Park (Citation2020). The moment conditions at (A3) ensure

for finite-dimensional

and

for infinite-dimensional

, so that the bandwidth ranges in (A7) make sense. The range for infinite-dimensional

does not cover the optimal size for univariate nonparametric smoothing, which is

, but we note that the bandwidths hk are for estimating the parametric part of the model, not for the nonparametric part. For the latter, we use bk for which we assume (A8). The condition (A4) ensures that the matrix

is invertible with probability tending to one, which we detail below. The exponential moment condition (A5) is assumed to use empirical process theory (e.g., van de Geer Citation2000) in developing technical discussion for

. The condition (A6) is stronger than the typical one in kernel smoothing that K itself is Lipschitz continuous. The latter condition is required to make our estimator

smoother, so that it belongs to an

-valued function class with a proper entropy.

We now state a proposition that demonstrates the invertibility of .

Proposition 7.1.

Assume (A1), (A2) for and (A4)–(A7). Then,

so that

is invertible with probability tending to one.

7.1.2 Estimation of Parametric Components

We present the limit distribution of defined at (3.7). For this we need to introduce several terminologies. First, we let

be equipped with an inner product

defined by

for

and

in

. Let

be the associated norm such that

. For

, define

, an outer product in

, by

For a general -valued random element V, a linear operator

such that

is called the covariance operator of V. For a random vector U taking values in

,

so that

, defined by

, is the covariance operator of

. Let

denote a Gaussian random element taking values in

with mean

and covariance operator S, that is, the real-valued random variable

for any

is normally distributed with mean 0 and variance

. Let

, which is the covariance operator of

. Note that, in case

is independent of

, then

reduces to

.

Theorem 7.1.

Under the assumptions (A1)–(A7), it holds that

The following corollary for is an immediate consequence of Theorem 7.1. Recall that

.

Corollary 7.1.

Under the assumptions (A1)–(A7), it holds that .

7.1.3 Comparison with HPLM

We make a theoretical comparison of and

, the latter of which is defined at (3.11). Let

. Then, along the lines of the proof of Theorem 7.1 in the supplement S.11, we may prove that, under suitable conditions,

(7.1)

(7.1)

A special case of (7.1) for and d = 1 has been derived by Liang (Citation2006). The result (7.1) for

is valid under the PLM and thus remains true under the PLAM as well. In case

is independent of

reduces to

. The following definition is an extension of the classical notion of “asymptotic efficiency” for real-valued parameters to that for Hilbertian parameters.

Definition 7.1.

Let and

be estimators of a parameter

in a separable Hilbert space

such that

for a sequence sn and covariance operators

for j = 1, 2. We say that

is asymptotically more efficient than

if

is a nonnegative definite operator, that is,

for all

.

We note that is nonnegative definite and it is zero only if

. A direct computation shows that

(7.2)

(7.2) which implies that

is asymptotically more efficient than

in the sense of Definition 7.1. Let dj denote the jth diagonal entry of

. Then, under the PLAM (3.1), it holds that

with

, which is the gain by

against

under (3.1).

7.1.4 Estimation of Nonparametric Components

As we discussed in Section 3.3, is uniquely decomposed into

with the constraints at (3.8). We study the error rates for

and

. The asymptotic results presented here do not follow immediately from the results in Jeon and Park (Citation2020) since

. Furthermore, as seen in the assumption (A8), our work allows for a flexible range for the bandwidths bk, instead of assuming

as in Jeon and Park (Citation2020). Put

for

and

. Also, let

.

Theorem 7.2.

Assume (A1)–(A8). Then, it holds that, for each ,

Consequently,

In the case where for all

, the rates in Theorem 7.2 reduce to the usual ones for univariate smoothing. Indeed, for each

,

We also derive the asymptotic distributions of and

, which we defer to the supplement S.15.

7.2 Asymptotic Theory: Hilbertian Covariates

Here, we discuss the case where the covariates in the linear part of the model, which we denoted by for

, take values in

. Define now

. Recall that

is the p × p matrix whose (j, k) element equals

. We first introduce some technical assumptions for Hilbertian

. We note that the assumptions (A1), (A6) and (A8) in Section 7.1 still apply in the present case, which we call (B1), (B6), and (B8), respectively, here. The corresponding versions of the others are given below.

(B2) The

(B3) The Hilbertian error variable

(B4) The p × p matrix

(B5) There exist constants

(B7) The bandwidths hk satisfy

The conditions (B3) and (B7) are the same as (A3) and (A7), respectively, for finite-dimensional . In fact, for infinite-dimensional

, we are able to derive a slower rate for

and

, see below the second parts of Theorem 7.3 and Corollary 7.2. For such rate of convergence, we find that (B3) and (B7) are sufficient. The following proposition is an analogue of Proposition 7.1 for Hilbertian

.

Proposition 7.2.

Assume (B1), (B2) for and (B4)–(B7). Then,

so that

is invertible with probability tending to one.

We now derive the asymptotic properties of . Note that

is the p × p matrix whose (j, k) element is given by

. Define

Let denote the multivariate normal distribution with mean

and covariance matrix Σp.

Theorem 7.3.

Assume (B1)–(B7). If is finite-dimensional, then it holds that

If is infinite-dimensional, then

.

The following corollary for is an immediate consequence of Theorem 7.3. Recall that

.

Corollary 7.2.

Assume (B1)–(B7). If is finite-dimensional, then

. If

is infinite-dimensional, then

.

Next, we present the asymptotic properties of and

satisfying the constraints at (3.8). As in Section 7.1, we let

denote the set of bandwidths for defining (2.5) with

. Recall

and

. Put

if

is finite-dimensional, and

if

is infinite-dimensional.

Theorem 7.4.

Assume (B1)–(B8). Then, Theorem 7.2 remains to hold with δk being replaced by .

We also derive the asymptotic distributions of and

in the case of Hilbertian

, which we defer to the supplement S.18.

Supplementary Materials

The supplementary material contains the description of the CBS algorithm, the geometries of Bayes-Hilbert spaces and simplices, and an additional real data application. It also includes two additional theorems for the asymptotic distributions of the estimators of the nonparametric components of the partially linear additive models, and all technical proofs.

Supplemental Material

Download Zip (893.7 KB)Supplemental Material

Download PDF (1.2 MB)Supplemental Material

Download MS Word (41.4 KB)Acknowledgments

The authors thank an Associate Editor and two referees for giving thoughtful and constructive comments on the earlier versions of the article.

Additional information

Funding

Related Research Data

References

- Benatia, D., Carrasco, M., and Florens, J.-P. (2017), “Functional Linear Regression with Functional Response,” Journal of Econometrics, 201, 269–291. DOI: 10.1016/j.jeconom.2017.08.008.

- Bhattacharya, P. K., and Zhao, P.-L. (1997), “Semiparametric Inference in a Partial Linear Model,” The Annals of Statistics, 25, 244–262. DOI: 10.1214/aos/1034276628.

- Bissantz, N., Dette, H., Hildebrandt, T., and Bissantz, K. (2016), “Smooth Backfitting in Additive Inverse Regression,” Annals of the Institute of Statistical Mathematics, 68, 827–853. DOI: 10.1007/s10463-015-0517-x.

- Bosq, D. (2000), Linear Processes in Function Spaces, New York: Springer.

- Buja, A., Hastie, T., and Tibshirani, R. (1989), “Linear Smoothers and Additive Models,” (with discussion), The Annals of Statistics, 17, 453–555. DOI: 10.1214/aos/1176347115.

- Hall, P., and Horowitz, J. L. (2007), “Methodology and Convergence Rates for Functional Linear Regression,” The Annals of Statistics, 35, 70–91. DOI: 10.1214/009053606000000957.

- Han, K., and Park, B. U. (2018), “Smooth Backfitting for Errors-in-Variables Additive Models,” The Annals of Statistics, 46, 2216–2250. DOI: 10.1214/17-AOS1617.

- Han, K., Müller, H.-G., and Park, B. U. (2020), “Additive Functional Regression for Densities as Responses,” Journal of the American Statistical Association, 115, 997–1010. DOI: 10.1080/01621459.2019.1604365.

- Horváth, L., and Kokoszka, P. (2012), Inference for Functional Data with Applications, New York: Springer.

- Jeon, J. M., and Park, B. U. (2020), “Additive Regression with Hilbertian Responses,” The Annals of Statistics, 48, 2671–2697. DOI: 10.1214/19-AOS1902.

- Jeon, J. M., Park, B. U., and Van Keilegom, I. (2021), “Additive Regression with Non-Euclidean Responses and Predictors,” The Annals of Statistics, 49, 2611–2641. DOI: 10.1214/21-AOS2048.

- Jeon, J. M., and Van Bever, G. (2022), “Additive Regression with General Imperfect Variables,” arXiv:2212.05745.

- Lee, E. R., Han, K., and Park, B. U. (2018), “Estimation of Errors-in-Variables Partially Linear Additive Models,” Statistica Sinica, 28, 2353–2373.

- Lee, Y. K., Mammen, E., and Park, B. U. (2010), “Backfitting and Smooth Backfitting for Additive Quantile Models,” The Annals of Statistics, 38, 2857–2883. DOI: 10.1214/10-AOS808.

- Lee, Y. K., Mammen, E., and Park, B. U. (2012), “Flexible Generalized Varying Coefficient Regression Models,” The Annals of Statistics, 40, 1906–1933.

- Liang, H. (2006), “Estimation in Partially Linear Models and Numerical Comparisons,” Computational Statistics & Data Analysis, 50, 675–687. DOI: 10.1016/j.csda.2004.10.007.

- Liang, H., Thurston, S. W., Ruppert, D., Apanasovich, T., and Hauser, R. (2008), “Additive Partially Linear Models with Measurement Errors,” Biometrika, 95, 667–678. DOI: 10.1093/biomet/asn024.

- Lin, Z., Müller, H.-G., and Park, B. U. (2022), “Additive Models for Symmetric Positive-Definite Matrices and Lie Groups,” Biometrika (to appear). DOI: 10.1093/biomet/asac055.

- Linton, O., Sperlich, S., and van Keilegom, I. (2008), “Estimation of a Semiparametric Transformation Model,” The Annals of Statistics, 36, 686–718. DOI: 10.1214/009053607000000848.

- Mammen, E., Linton, O., and Nielsen, J. P. (1999), “The Existence and Asymptotic Properties of a Backfitting Projection Algorithm under Weak Conditions,” The Annals of Statistics, 27, 1443–1490. DOI: 10.1214/aos/1017939138.

- Opsomer, J. D., and Ruppert, D. (1997), “Fitting a Bivariate Additive Model by Local Polynomial Regression,” The Annals of Statistics, 25, 186–211. DOI: 10.1214/aos/1034276626.

- Opsomer, J. D., and Ruppert, D. (1999), “A Root-n Consistent Backfitting Estimator for Semiparametric Additive Modeling,” Journal of Computational and Graphical Statistics, 8, 715–732.

- Ramsay, J. O., and Silverman, B. W. (2005), Functional Data Analysis, New York: Springer.

- Severini, T., and Wong, W. (1992), “Profile Likelihood and Conditionally Parametric Models,” The Annals of Statistics, 20, 1768–1802. DOI: 10.1214/aos/1176348889.

- van de Geer, S. (2000), Empirical Processes in M-Estimation, Cambridge: Cambridge University Press.

- Yao, F., Müller, H.-G., and Wang, J.-L. (2005), “Functional Linear Regression Analysis for Longitudinal Data,” The Annals of Statistics, 33, 2873–2903. DOI: 10.1214/009053605000000660.

- Yu, K., Mammen, E., and Park, B. U. (2011), “Semi-Parametric Regression: Efficiency Gains from Modeling the Nonparametric Part,” Bernoulli, 17, 736–748. DOI: 10.3150/10-BEJ296.

- Yu, K., Park, B. U., and Mammen, E. (2008), “Smooth Backfitting in Generalized Additive Models,” The Annals of Statistics, 36, 228–260. DOI: 10.1214/009053607000000596.

- Zhang, X., Park, B. U., and Wang, J.-L. (2013), “Time-Varying Additive Models for Longitudinal Data,” Journal of the American Statistical Association, 108, 983–998. DOI: 10.1080/01621459.2013.778776.