ABSTRACT

The Dutch Water Bank (NWB), which was created in the 1950s, still provides long-term, low-cost, low-risk patient and appropriate financing to public entities. It is a model that has worked, but not without room for improvement. The NWB has an opportunity to untap its support of Dutch drinking water companies’ sustainability transitions. To do so, it needs to embrace its ‘publicness’: leveraging its position within the Dutch public sector to catalyse water investments in the public interest. The NWB offers important lessons for global debates on public banks and sustainable transitions.

Introduction

The study of public banks is resurgent following decades of relative scholarly and public policy malaise. The combined impacts of the global financial, ecological and Covid-19 crises on economy and society, taken alongside decades of persistent social inequalities under neoliberal strategies of market-led development, have reinforced doubts about the promised ability of private banks and financiers to resolve global grand challenges in anyone’s but their own private interests. Public banks have persisted throughout this period, amassing nearly US$50 trillion in combined assets among their more than 900 institutions worldwide (Marois, Citation2021). It is a mistake, however, to assume public banks share a common purpose or undertake standard roles. From funding mortgages to municipal infrastructure to exports to housing retrofits, there is no one model of public bank. Nor is there a self-evident pathway between what public banks do and the interests they predominantly serve. As dynamic and contested institutions within global capitalism, public banks are pulled between contending public and private interests (Marois, Citation2022). How the ‘public purpose’ of a public bank is embedded within the institution and how it is held to account by society proves consequential to ‘who benefits and why’ from how the bank functions (Barrowclough & Marois, Citation2022; McDonald et al., Citation2020; Ray et al., Citation2020). This dynamic view offers a novel and alternative conceptualization – one that subjects what public banks do and why to changing historical, social, political and economic determinations within the structural confines of gendered, racialized and class-divided capitalist society (Marois & Güngen, Citation2016; Marois, Citation2021).

The Nederlandse Waterschapsbank (NWB – Dutch Water Bank), recently rebranded as ‘the Sustainable Water Bank’ in response to the global climate crisis and Sustainable Development Goals (SDGs), offers a unique insight into the world of dynamic public banks. It is neither among the newest nor the oldest of public banks. The NWB is also not among the most systematically important financial institutions of the world. It is nevertheless significant for the society in which it operates: the Netherlands. The NWB is a goal-oriented public purpose public bank designed to work by and for the Dutch public sector. The NWB is, however, the first public bank founded on the premise of providing supportive public financing for water infrastructure and service provisioning. Thus, it offers an important vantage point in public banking, which we explore through the lens of financing drinking water.

Our exploration of the NWB’s funding of Dutch drinking water companies (DWCs) is framed around the concept of public purpose. By public purpose we refer to the purposive actions taken by a government, public board, public corporate entity or public authority to provide some material benefit for its affected community, population or constituency as a whole or in some substantive part.

While neoliberal theory and neoclassical economists hold faith over private interests and self-interest as best able to fulfil public purposes, this work contributes to a large and diverse body of theory and evidence demonstrating tangible benefits to the public provisioning of essential public services (Hanna, Citation2018; McDonald, Citation2016b). That said, nowhere are public services without room for improvement or the need to be made better and to be better aligned with the public interest. For this reason, the NWB becoming ‘the sustainable’ water bank is of enormous importance as we confront the global climate crisis. Public finances are being pulled between contending public and private interests (Marois, Citation2021). Private finance is aggressively pushing for public money to de-risk their green investment strategies – and this can come at the expense of public policy and the public good (Griffith-Jones et al., Citation2022; Marshall & Rochon, Citation2022).

As illustrated below, public purpose guides the NWB’s relationship with the DWCs in the public interest. There are important processes and public sector synergies that we need to learn from in its financing of public water provisioning. Yet the relationship is not without room for improvement, particularly as Dutch society seeks to safeguard a sustainable water supply. We argue that to most effectively address the challenge of sustainable water provisioning, the NWB needs to better embrace its ‘publicness’. That is, to untap its ability to provide the quality and scale of sustainable water financing needed, the NWB needs to be enabled to leverage its position within the Dutch public sector to catalyse water investments in the public interest. This involves the Dutch government providing the DWCs with explicit guarantees against credit default (which are now implicit) so that the NWB can lend to DWCs without limit. The Netherlands is in an advantageous situation to realize this ambition as both public water and public banking have the institutional and material legacies needed to address the sustainable water challenge.

We develop this argument in three sections. We first explore the history of the Dutch water supply sector to illustrate that it has evolved in ways favourable to confronting contemporary demands for sustainable water. Given current conditions, however, the financing strategies of the DWCs tend to privilege competitive conditions that are agnostic as to whether financing is public or private in origin. This is inefficient and unnecessary. We then turn to the NWB, which has amassed the financial capacity and expertise needed to catalyse sustainable transformations, particularly in water supply. Its funding strategy, however, prioritizes protecting its triple-A credit rating. This is at odds with financing public water sustainably and it is a direct consequence of the DWCs not being formally backed by government. We conclude by offering a policy pathway capable of more fully untapping the NWB’s ability to meet the sustainability challenges of the Dutch DWCs.

The article is based on a review of the primary, secondary and grey literature on the Dutch drinking water sector. The primary and secondary literature on the Dutch public banks, by contrast, is largely non-existent, although there is a renewed literature on public banks more broadly from which we draw. In the case of the NWB, we rely more on the grey literature, in particular NWB annual reports. In both water and banking, our research is complemented by interviews with NWB representatives and representatives from two water utility clients of the NWB: Evides and Vitens. We employed a semi-structured interview methodology and used similar sets of interview questions as the other contributors to the public bank/public water research project that are part of this special issue.

The Dutch DWCs

The Dutch water services sector is characterized by an organizational separation of water supply, sewerage and wastewater treatment. The DWCs are tasked with water supply provision, whereas Dutch municipalities are responsible for sewerage. The water boards (or water authorities) are responsible for wastewater treatment. For their part, the public purpose of the Dutch DWCs is to provide a clean and universal supply of water across the Netherlands. In doing so, ensuring security of supply is of prime importance. In fulfilling this purpose, the Dutch drinking water supply sector has evolved over the last century to meet demand and to do so efficiently. Its challenge now is providing for a sustainable water future.

The initial development of the Dutch water supply sector in the late 19th and early 20th centuries was mainly characterized by local initiative. Although the Dutch national government recognized the importance of water supply, it did little to stimulate its development. This was left to local initiatives that usually involved private water companies supplying water to promising urban markets. Only in the 1910s did the Dutch government start to promote the development of the water supply sector to achieve universal coverage. In 1913, ‘a permanent advisory committee to the government and a national bureau were established to advise on and assist with drinking water supply development’ (Blokland, Citation1999, p. 37). Its main focus was on ensuring access to water in rural areas that were not yet catered to by private entrepreneurs. This first of three distinct phases of water supply sector development, from 1910 onwards, is thus characterized by a strong focus on service expansion and on ensuring universal service coverage. Expansion of water supply was financed by the DWCs and through grants provided by the national government.

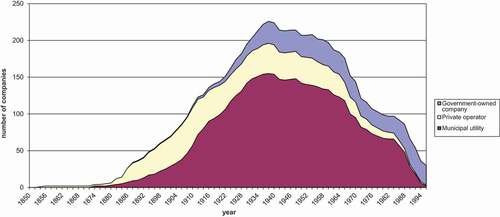

In promoting expansion and universal coverage, the Dutch government pushed the DWCs to merge to reap economies of scale and to allow larger water companies to absorb (or cross-subsidize) the costs of servicing difficult-to-connect rural areas. The organizational form for DWCs that became dominant in this phase is that of a private company operating under company law, whilst the shares of the company were owned by either provincial or municipal governments. In opting for this set-up, which was a common arrangement for public services in the Netherlands for most of the 20th century, DWCs were encouraged to operate as autonomous entities operating on the basis of cost recovery.Footnote1 The government, nonetheless, maintained strategic control. This expansionary phase persisted until the 1970s when rural areas were connected to the water supply.

A second phase emerged in the late 1970s as water supply priorities shifted from expansion to the challenge of realizing greater efficiency. Mergers again formed an important strategy (), though in this phase the DWCs, rather than the government, pushed for scale enlargement. At the same time, automatization of the water supply sector was pursued. This is illustrated by the reduction in water utility employees, which fell from 8504 employees in 1980 to 4881 employees in 2020 (Blokland & Warner, Citation1999; VEWIN, Citation2021). Fewer employees coincided with increased connections, which expanded from just under 5 million to 8.3 million by the end of 2019. Productivity improved from 1.7 to 0.6 staff/1000 connections. The initiative to improve efficiency was financed by the DWCs themselves.

Figure 1. Organization and number of water supply companies, 1854–1997.

The third phase currently characterizing the Dutch water supply sector is about ensuring a sustainable water supply. This sustainability challenge emerged in response to climate change, population growth and rising pollution of water resources. It has two main drivers. The first concerns the heightened value that Dutch society and the government place on sustainability, particularly in the context of climate change (Vitens, Citation2016). The Dutch DWCs are no longer held accountable for only supplying safe, universal, and adequate water services but also for their environmental impacts and for its sustainable provisioning (Vitens, Citation2016).

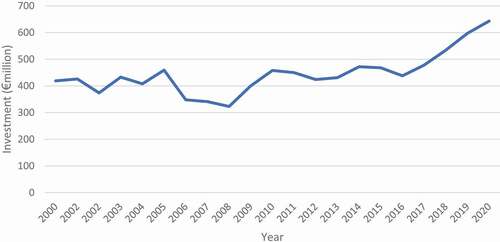

The second concerns operational challenges. The DWCs are more and more faced with droughts and water scarcity, rising water demands due to population growth, and with polluted water sources requiring more treatment. In response, the DWCs have evolved to adopt sustainability frameworks meant to safeguard future water provisioning. In 2020, the Dutch water company Vitens titled its strategic report Every Drop Sustainable, therein specifying its mission to become a fully ‘sustainable’ water utility by 2030 (Vitens, Citation2020). As part of this strategy, the utility wants, among others, to reduce CO2 emissions by 2030 and be completely ‘climate neutral’ by 2050. The sustainability challenge will demand substantial increases in water investments, and the DWCs’ financing strategies will have to evolve to meet this challenge effectively and equitably ().

Figure 2. Annual investment in the Dutch water supply sector, 2000–20.

A 2021 report by the Inspectie Leefomgeving en Transport (ILT – Human Environment and Transport Inspectorate), which is tasked with regulating the Dutch water supply sector, anticipates that the sustainable water challenge will lead to investments in 2029 that are 50–60% above investments in the period 2017–19 (ILT, Citation2021). This 60% increase by 2029, it should be added, represents a sector average. Individual DWCs may face either higher or lower increases depending on their specific circumstances. Either way, the aggregate amount is substantial. Over the coming decade invested capital in the water supply sector is expected to grow from €7.4 billion to over €11 billion, with combined annual investments currently exceeding €643 million (ILT, Citation2021; VEWIN, Citation2021).

In deciding on the timing and size of investments, DWCs are restricted by regulations setting out a maximum weighted average cost of capital (WACC). Article 11.2 of the Dutch water supply act states that DWCs should not exceed this WACC, which is set every three years by the Ministry of Infrastructure and Water Management (Article 10.3). The WACC was originally introduced to protect consumers from high tariff increases by limiting the amount of funds generated from the utility’s profit that can be used to finance investments (from either equity or debt). The WACC, which has been set at 2.95% for the period 2022–24,Footnote2 essentially limits the investment levels of DWCs. Although the DWCs argue that the WACC is too low to fund the necessary investments in the coming decade (Dijkgraaf & Vervaart, Citation2021), the ILT argues that the WACC provides sufficient room to finance needed investments.

Evides and Vitens are two important Dutch DWCs that are facing mounting investment needs. Vitens, for example, estimates that by 2040 demand for drinking water will increase by 30%, while at the same time the company is facing growing difficulties in accessing adequate groundwater resources (Vitens, Citation2021). Vitens indicates that the water supply sector is ‘at a crossroads’ in what it does and how as it tries to build capacity to store water to deal with droughts while protecting vulnerable groundwater sources from pollution ().

Table 1. Characteristics of Vitens and Evides, 2020.

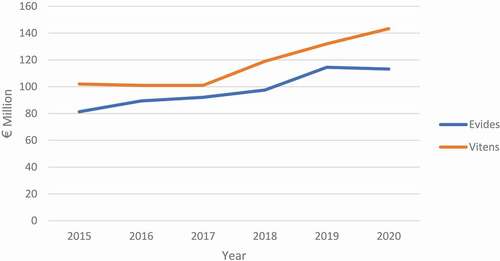

Evides and Vitens are illustrative of the Dutch drinking water sector. Investments have increased substantially (). For Evides, investments rose from a little over €81 million in 2015 to more than €113 million in 2020. For Vitens, investments rose from €102 million to €143 million. Expectations are that investments will need to continue growing. For 2020 to 2029, Vitens anticipates annual investments to exceed €180 million (see also ILT, Citation2021).Footnote3 Evides too expects to expand investments.Footnote4 A 2021 ILT report indicates that in 2019 Evides and Vitens are the two DWCs that used up most of the investment space offered by the WACC. In the case of Evides, it exceeded the WACC target by 0.09%.Footnote5 In the case of Vitens, it was 0.18% below the allowed WACC.Footnote6

Figure 3. Annual investments Evides and Vitens, 2015–20.

The capital used to make DWC investments is not provided by the government but is instead derived from fee income (tariffs and other direct user charges). Any additional capital required is then borrowed. In sourcing loans for investments, the DWCs are neither purposively public nor private in orientation.Footnote7 Both Evides and Vitens, however, are aware that they represent an interesting clientele for banks, public and private, as effectively public entities. While technically organized as a private company, the shares of DWCs are owned by public authorities (municipal and/or provincial governments), which provides an implicit safeguard or backstop should a crisis emerge.Footnote8 Yet the DWCs do not purposively align their financing strategies according to any understanding of ‘publicness’.

The attractiveness of the DWCs as clients for banks is underscored by the fact that water is a basic human and societal necessity. There is no substitute for water, and the demand for water is stable and predictable over time. Moreover, Dutch DWCs are monopoly providers as stipulated by law in the Water Supply Act. It is their purpose to deliver water. Those wanting water supply must purchase it from the DWCs. These characteristics make the Dutch DWCs a low-risk investment for any bank because the DWCs have guaranteed product demand and monopoly control of delivery. But the DWCs only enjoy an implicit guarantee against default. The government has not explicitly decreed in law that it will support DWCs at times of crisis. This is consequential. Without a formal public or state guarantee, the DWCs are subject to (perceived) market-based credit risks that both public and private banks must consider in their assessments. The DWCs are effectively perceived as if they were private companies that happen to deliver public water services. Nor can the Dutch public banks accord the DWCs special conditions outside of market conditions because they are not fully backed by the government. As a result, the DWCs seek to leverage their ‘natural monopoly’ advantages and manage their risks within effectively private financial markets, pushing to realize the best terms for themselves as relatively desirable clients in the market.

That the DWCs can access private bank financing and do so on competitive terms might lead some heterodox economists to suggest that there is no need for the NWB (or any other public bank) to be active in the drinking water sector. This is because the involvement of the NWB does not meet ‘additionality’ criteria (Skidelsky et al., Citation2011). The notion of additionality builds on the ideas of John Maynard Keynes, namely that the ‘important thing for government is not to do things which individuals are doing already, and to do them a little better or a little worse; but to do those things which at present are not done at all’ (Keynes, 1926, p. 46; also see Mazzucato, Citation2015). In this understanding of additionality, if private banks are willing to lend to the DWCs, and do so on relatively competitive terms, then public banks like the NWB should be lending elsewhere, that is, to where its additionality might be greater.

From a dynamic view of public banks, there are good reasons to be sceptical of this narrow interpretation, both in historical factual terms and for the prospects of financing green and just transitions (see Marois, Citation2021, pp. 66–68, for a fuller elaboration). These too apply to the Dutch case. In addition, however, the ‘additionality’ lens fails to account for ‘availability risk’ – that is, the risk of not being able to access financing when needed by the DWCs (discussed below). The private banks are willing to lend, but only when they want to and at the terms they prefer. They are pro-cyclical (lending when times are good) and primarily profit oriented in their responsibility to shareholders. They are never compelled to lend when funds are need. To abandon drinking water to pro-cyclical, profit-oriented finance is a huge risk – and the DWCs know this. By contrast, the NWB is mandated to help finance the water sector, but the lack of an explicit guarantee presents a barrier to the ability to do so within its mandate to preserve a triple-A credit rating. A government guarantee would erase limits to what the NWB could lend to the DWCs with no negative impact on its risk profile (as is the case with many other public banks in Europe).

Given the mandate of the DWCs to provide clean, universal water at all times, the Dutch DWCs pay particular attention to ‘availability risks’ (Beschikbaarheidsrisicos) in sourcing loans. Availability risks essentially revolve around guaranteeing that the water utility can access loans to match its planned investment needs at any given time. Two strategies help DWCs manage this challenge in current circumstances. The first involves purposively diversifying the public and private banks from which they take loans. The DWCs engage a variety of lenders to develop multiple relations over time but without prioritizing public or private bank provisioning (Evides, Citation2021, p. 19). In establishing a relationship, the DWCs consider the financial health of a bank, allowing for specific range of A, AA and AAA credit ratings. The DWCs then take loans with various banks to maintain and foster good and stable relationships with a diverse range of lenders that are, nevertheless, ultimately market based and self-interested. Relationship diversification is understood as strategically important because the DWCs may need emergency financing at a time of crisis. In the absence of an explicit government guarantee or formal commitment from the banks (public or private), the DWCs must manage this risk internally. The second availability risk strategy involves securing financial commitments well in advance of the loans being required. Vitens, for example, ensures that financial commitments are in place 12 months in advance. Although specific details of the loans may still require finalization, the financial commitment ensures that the water company will have financing when required.

It follows that the DWCs must also privilege the cost of financing capital needs when sourcing loans in the market. Again, in the absence of explicit government backing or public policy, the DWCs must do so without privileging public or private banks. The competitive pricing of loans dictates. Public and private banks compete among themselves to offer the best terms to the DWCs. The DWCs, in turn, select those providers that are most cost competitive – taking into account interest rates, fixed and variable rate options, and the tenure or length of the loan. The DWCs tend to prefer long-term and patient loans (that is, loans not focused on short-term returns but focused on extended developmental objectives) alongside fixed interest rates as a source of financial stability with limited exposure to risk.

In this context the NWB has enormous untapped potential to provide the type and scale of financing needed by the DWCs to ensure sustainable, predictable, reliable and equitable public water provisioning into the future.

Conundrums of the NWB’s public purpose

Much of the economics literature on public banks depends upon pre-social understandings of ‘public’ ownership such that being publicly owned is foundational to what a public bank is and does in ways prior to historical experience (Mazzucato & Penna, Citation2018; La Porta et al., Citation2002). That is, the bank’s public ownership form logically comes ‘before institutional functions’ in ways that fundamentally shape economists’ ‘polarized understanding of what public banks are and, importantly, what public banks are a priori meant to do’ (Marois, Citation2022, p. 357). Grafting pre-social meanings onto historically dynamic public entities impoverishes our ability to understand and represent institutional diversity and change.

To take a more historical approach it is important to define a bank as a ‘public bank’ without essentializing it. This is possible by identifying four objective conditions for a bank to be public: the bank is located within the public sphere (in a variety of ways); it performs financial intermediation and banking functions but with no innate purpose or policy orientation; it can function in public and private interests; and it persists as a credible, contested, and evolving institution (Marois, Citation2021, pp. 11–12). The first condition, being located within the public sphere, can be by virtue of dominant government, public authority, or public enterprise ownership; by a legally binding public interest mandate; by public law; by substantive public representation and control; or by some combinations of these. Notably absent is any inherent condition stipulating that public banks are meant to function in any particular way, including necessarily in the public interest. In this understanding being publicly owned does not give us much of an indication of a bank’s ‘publicness’. In a dynamic view of public banks there are no preordained notions of ‘if, how, when, or why’ it functions according to public purpose and in the public interest. The publicness of any given public bank is thus not easily determined – it is historical, political, contextual, shifting and contested (cf. Cassell, Citation2021).

For decades conventional economists have glazed over such historical and institutional complexity by reducing the nature of public banks to ownership form alone. Conventional economists then assign a series pre-social, ahistorical, and always detrimental characteristics to an institution being ‘public’ (Marcelin & Mathur, Citation2015; Megginson, Citation2005). To determine public ownership (and hence publicness), economists impose seemingly definitive quantitative measures of government ownership as both a necessary and sufficient condition – sometimes that measure is 50% plus and sometimes it is any level public ownership (World Bank, Citation2012; de Luna-Martínez et al., Citation2018).

The poverty of conventional views on public banks is well known (Butzbach et al., Citation2018; Marshall & Rochon, Citation2019; Marois, Citation2022). To acknowledge this is not to deny the importance of ownership, but it is to question the reductionism of economics wherein the public ownership form ultimately determines institutional functions (Ho, Citation2016). Instead we need to look at how public banks function as they do and ask ‘why’ in time- and place-bound contexts – and allow this to be a better measure of its publicness (Marois, Citation2022). In this way we can develop an enriched historical political economic understanding. There is resurgent interest in this type of case study knowledge of public banks (Clifton et al., Citation2021; McDonald et al., Citation2020; Griffith-Jones & Ocampo, Citation2018; Mertens et al., Citation2021; Scherrer, Citation2017). The present study contributes to this literature as the NWB has not yet garnered directed study.

The NWB in not the first or only national public bank in the Netherlands to finance water. The Bank Nederlandse Gemeenten (BNG – Dutch Municipalities Bank), is 40 years its senior, first founded in 1914 as the Gemeentelijke Credietbank (Municipal Credit Bureau) in close relation with the Vereninging Nederlandse Gemeenten (VNG - Association of Dutch Municipalities). The BNG is owned half by the Netherlands government and half by a combination of municipal and provincial authorities and a waterboard. It is a public-purpose public bank designed to support local authorities and public sector institutions by minimizing the financial costs of social provisioning of services: ‘Instead of maximising profits, our priority is to maximise the social impact of our activities’ (BNG, Citationn.d.).

For its part, the NWB came into being in the context of post-Second World War European reconstruction efforts and in the wake of a natural disaster in the Netherlands (Havekes et al., Citation2017). The idea of creating a new public bank dedicated to servicing the Dutch water authorities had originated in the interwar period, with plans discussed as early as 1939 (NWB Bank, Citationn.d.). Yet not until December 1952 did the Dutch water authorities association board decide to move forward (NWB, Citation2021, p. 11). Circumstances accelerated the decision. Within a few months, the 1953 North Sea flood hit the Netherlands, killing nearly 2000 people and leaving another 100,000 homeless, while causing widespread economic damage. Enormous, new infrastructure investments would be required to fortify the Netherlands against such water-related damage in the future. This gave impetus to the NWB, which came into being in May 1954.

The 1953 flood helped to forge the NWB’s original public purpose, namely, to provide low-cost, risk-free capital to the regional water authorities to enable them to protect the Netherlands against future flooding (NWB, Citation2010, p. 20). Public, not private, purpose was baked into the institution as, in the words of the NWB, ‘self-interest did not play a part in this endeavour’ (NWB Bank, Citationn.d.). Since then, according to a senior NWB executive, the NWB ‘only funds public tasks’ (confidential interview, 18 August 2021).

In pursuing public tasks over the last seven decades, the NWB has expanded operations beyond the water sector to support the Dutch public sphere more broadly. It understands itself as a ‘bank of and for the Dutch public sector’ with ‘a special responsibility towards society’ (NWB, Citation2011, pp. 20, 32). A core mission is to provide cheap and patient finance to the public sector. This does not come without contradictions. The funding of unguaranteed DWCs impacts the NWBs to deliver cheap and patient finance elsewhere (see below).

The NWB is a bank solidly located within the Dutch public sphere, both by public ownership and by mandated purpose (). It is fully owned by public authorities, with public ownership legally enshrined in law in the NWB Articles of Association. Only the Dutch state or entities governed by public law can ever be owners (NWB, Citation2011, p. 20; Citation2021, p. 109). As of late 2021, the Dutch Water Boards hold 81%, the State of the Netherlands 17%, and provincial authorities 2% of NWB. Because the NWB is positioned within public sphere, it can, but not necessarily, be shielded from direct exposure to competitive market and profit imperatives (cf. Marois, Citation2022). In terms of structural pressure to generate short-term returns experienced by private banks, the NWB is shielded from market imperatives. It does not target profit maximization, and this distinguishes the NWB from its private competitors. Yet because the NWB accesses funds in global financial markets, and aims to do so cheaply, it seeks to protect its creditworthiness.

Table 2. The NWB at a glance, 2020.

How the NWB governs itself, moreover, is in some ways more akin to private corporate governance models. That is, governance is not directly exercised by representatives of its public owners or by specified representatives the public in general, either wholly or in part. This is unlike other public banks in Europe, such as the German KfW or the Nordic Investment Bank, which have direct political representation on their boards (Marois, Citation2021). Instead, the NWB has a seven-member supervisory board selected not according to set conditions (e.g., being the Minister of Finance or a trade union representative) but according to preferred expertise and backgrounds capable of ‘assessing national and international social, economic, political and other developments that are relevant to NWB Bank’ (NWB, Citation2016, p. 16; NWB, Citation2021, p. 110). The NWB board is expected to function independently, if not in isolation, from its public owners. NWB staff stay in regular contact with governing authorities, water boards, municipalities and the Ministry of Finance (NWB, Citation2011, p. 32; Citation2021, p. 37). This, however, occurs at an informal and functional level as there is no formal policy on bilateral contacts with government (NWB, Citation2021, p. 109). While further historical research is required, governance and decision making appear to be guided by an ethos of public purpose and public sector collaboration rather than by de jure representation. In the Dutch context, this approach appears to function and to do so in ways that maintain public purpose. In its Annual Report 2020, the NWB (Citation2021, p. 39) states:

We are a bank of and for the public sector, which is why we enjoy good relationships with local authorities and the central government. We regularly participate in meetings with relevant Dutch government ministries, contributing our expertise on policy issues.

In pursuing its public purpose, the NWB has entered an aggressive expansionary phase over the last decade. It has nearly doubled total assets, which grew from €57 in 2010 to €107 billion in 2020 (). Annual lending now surpasses €10 billion. Since 2000, it has also captured a larger proportion of long-term public sector loans, which has tripled from 10% to 30% (NWB, Citation2011, p. 20). The NWB has done so without prioritizing profits. Its return on average assets (ROAA) since 2010 is on average 0.094, which is but 10% of what most private banks would minimally accept. The NWB nevertheless generates positive, if modest, income and from time to time pays dividends to its public owners.

Table 3. NWB’s operational data, 2010–20.

The relationship between government or state guarantees and NWB lending to the public sector is significant. The NWB provides financing across the public sector, which includes to water utilities; local authorities, municipalities and provinces; housing associations; healthcare and medical institutions; universities; and vocational institutions – if backed by state guarantees (NWB Bank, Citationn.d.). The NWB will also finance foundations, associations, and other entities with government guarantees (e.g., sports clubs or schools) – again, if backed by the state. State guarantees render NWB loans as effectively zero risk of default, with no negative implications for preserving its triple-A credit rating in international markets. The relationship effectively shields the loans from market determinations.

Loans without state guarantees are made by the NWB, but these can weigh on their credit rating. While loans to the Dutch water authorities are fully backed, the Dutch DWCs fall into this latter category – and this exposes loans to DWCs to market-based credit weightings. While the NWB has no formal policy specifying lending limits to DWCs as a result of this market exposure, the bank places an (informal) internal ceiling on lending amounts for this reason (confidential interviews, 18 and 25 August 2021). In other words, if the NWB extends too much in the way of non-guaranteed loans to the DWCs it is at risk of losing its top-ranking creditworthiness in financial markets. This contradicts its public purpose of ensuring access to the cheapest possible sources of capital in international markets, which is used to support the public sector in general. In this instance, the public purpose of the NWB is working at odds with itself. Even as the Dutch water bank, the NWB cannot fully fund the needs of public DWCs – even though it has the financial capacity and institutional mandate to do so – because this would undermine its credit rating in private markets.

What is of great importance here is the function of state guarantees. With it, NWB financing is no problem – recipients are fully shielded by the public sphere. Without it, projects fall in a different category of scrutiny and are exposed to market discipline and creditworthiness.

It is worth emphasizing the importance of NWB access to international capital markets. For much of the 20th century the NWB sourced long-term capital domestically. Over the last 20 years or so, it instead draws finance globally (NWB, Citation2011, p. 20). The maintenance of its access to global markets is now deeply rooted in NWB operational strategy – the institution is fundamentally oriented towards accessing cheap finance abroad to invest it at home in ways that are affordable, long-term and sustainable (NWB, Citation2021, p. 113). This is what enables the NWB to provide highly competitive long-term financing to the public sector, including water, with periods of up to 50 years and with often flexible repayment schedules. This is, no doubt, an important public purpose – one that would be the envy of many state authorities. In places as diverse as North Dakota and India, the capacity of public banks to pull in and fix otherwise globally mobile flows of private finance has helped to definancialize economies (Marois, Citation2021, pp. 147–155). Public banks are able to give ‘policy steer’ from their borrowing in global markets, maximizing the developmental impacts of public financial resources (Griffith-Jones et al., Citation2022, p. 200).

To access the near limitless pools of money in global markets cheaply, the NWB rigorously safeguards its triple-A credit rating (NWB, Citation2021, p. 113; confidential interviews, 18 and 25 August 2021). To support its credit rating, however, the NWB predominantly lends to public authorities and to entities that are explicitly backed against any possible credit default by the government. This renders the loans as essentially zero risk (as fully shielded by the public sphere). With backed loans, there is effectively no limit to how much the NWB could lend to public entities (confidential interview, 18 August 2021). The NWB’s public–public financial relationships are a ‘a major precondition for keeping its AAA ratings’, ratings that provide benefit to NWB public sector clients by enabling them to finance social operations with high-quality, low-cost credits (NWB, Citation2011, p. 22). It is worth pointing out, moreover, that by targeting long-term, low-cost, low-risk public–public financing, ‘throughout its history, NWB Bank has never suffered a loan loss’ (NWB, Citation2011, p. 26; confidential interview, 18 August 2021). This is an achievement that perhaps no private bank in the world could claim (but which other public banks can, as outlined by other articles in this special issue).

In this way the NWB argues that it meets the water sector’s financial needs and can provide for a sustainable future (NWB, Citation2021, p. 45). But is it the best way? And are the Dutch DWCs equal partners in this? We see that there are trade-offs, even contradictions, to the NWB strategy of sourcing capital from global capital markets – in certain circumstances. This has material implications for the DWCs because they are not rated as zero-risk clients by the NWB for lack of an explicit state guarantee.

The problem is therefore not that the NWB sees DWCs as outside the public sphere (NWB, Citation2021, p. 47). Nor is the problem any lack of understanding of the importance of the DWCs or that they are facing increasing demand for financing to meet mounting infrastructure investment challenges (pumping stations, pipelines and wastewater treatment plants), which climate change and climate impacts are exacerbating (NWB, Citation2021, pp. 45, 47; confidential interviews, 18 and 25 August 2021). The problem is also not one of recognizing the suitability of the NWB for providing the right kinds of financing, even within a competitive market, at the terms and scale needed by the DWCs (NWB, Citation2020, p. 34; Citation2019, p. 27; confidential interview, 18 August 2021). While NWB lending to DWCs has been variable to date, it is substantial and remains consistently in the hundreds of millions of euros annually and this is expected to grow ().

Table 4. NWB’s lending to drinking water companies (€ million).

It is thus not the significance or relevance of the DWCs to the public purpose of the NWB that is a barrier. It is that the DWCs are not explicitly backed by government guarantees. This fact disproportionately shapes funding portfolio decisions as the DWCs are not zero-risk weighted and ‘loans provided to Dutch drinking water companies … are included in the 100% weighting category’, meaning they are more costly to offer and riskier to hold as assets (NWB, Citation2019, p. 164; confidential interview, 25 August 2021). Lending to the DWCs increases the operating costs of the bank and, if the portfolio grows significantly, challenges the NWB’s triple-A credit rating (although presumably this depends on whether the DWCs in fact pose any risk at all, which has not really been tested in the market). As a result, the NWB internally limits loans to the DWCs to the extent that its DWC loan portfolio is perceived by the NWB as potentially undermining its ability to provide cheap, long-term capital in general to the public sector. In this sense, the ‘sustainable water bank’ strategy exhibits a more financial than environmental reading of ‘sustainable’, which implies a limited appetite for risks to its triple-A rating.Footnote9

This is at odds with the historical legacy of the NWB – a public bank built on supporting the provisioning of water. In the words of the NWB Bank (Citationn.d.):

We are an important financer in the drinking water sector. Drinking water companies have the crucial task of providing consumers and companies with a sufficient supply of high-quality drinking water. Properly fulfilling this task requires constant investment in the drinking water infrastructure (in pumping stations, treatment plants and the pipeline network, for instance). The activities of drinking water companies are regulated by law, which is why they have been a client at our bank for a long time.

The Dutch DWCs thus represent a conundrum for the publicness of the NWB. The DWCs are a preferred target of lending for the NWB yet by doing so the DWCs become a potential threat to bank’s public purpose to provide cheap lending to the whole public sector. Furthermore, by limiting cheap funding to the Dutch DWCs, the NWB may unintentionally make the DWCs transition to sustainability more costly, less efficient, and more lengthy than need be, thus putting in question the NWB’s rebranding as ‘the sustainable water bank’. What can be done to align the NWB and to the needs of the Dutch DWCs according to public purpose?

Untapping the NWB’s publicness, aligning government policy

In the coming decades, the Dutch water supply sector needs to address the challenges of population growth, pollution of water sources, and climate variability (including droughts). This has given rise to an expected increase of annual investments by 50–60% by 2029, making the delivery of safe and clean water for all increasingly costly and complex. As one Vitens respondent noted, things were simpler five years ago when the risk profile in the water supply sector was lower (confidential interview, Vitens, 29 November 2021). By untapping the NWB’s publicness by aligning government policy, a more efficient and effective pathway to sustainability can be opened.

Current financing to the DWCs does not dominate the NWB portfolio. DWC loans account for only around 2–3% of new NWB lending each year, which amounts to about €250–300 million annually (by contrast, the larger, state-backed water authorities account for about 11–12% of NWB total lending). This lending is significant for the DWCs but comparatively less significant to the NWB’s overall portfolio. It is unlikely that even a substantive increase in lending to the non-backed DWCs would have much, if any, effect on the NWB’s overall credit rating. For the DWCs, at the same time, it is unclear whether or not they would welcome the NWB taking a more, or even the, dominant lending position given their concerns over availability risks.

However, from a public policy and public purpose perspective, particularly in light of the challenge of catalysing sustainable transitions, the NWB is ideally situated to be the catalyst. It is fully capable of providing the low-cost, long-term financing required, backed by appropriate knowledge and expertise, to enable the DWCs to achieve their goal of sustainable water in the next decade. The current practice of leaving DWC financing up to competitive markets among all banks and as exposed to perceived availability risks from public and private may be undermining this ambition.

What can be done? The NWB should be enabled to embrace its ‘publicness’ and to leverage its position within the Dutch public sector to untap its water investments in the public interest. To do so, Dutch public policy needs to align and re-enforce ‘a whole-of-public sector approach’ in ways that would empower the NWB to maximize the advantages of being a bank within the public sphere. A relatively straightforward policy fix could help catalyse this shift, namely, extending state guarantees for DWCs to provide sustainable drinking water.

An immediately impactful policy measure would be for the Dutch government to extend explicit state guarantees to the DWCs for all sustainability related water investment requirements (guarantees that also relax WACC restrictions vis-à-vis sustainability). Government backing to funds provided through the NWB would enable the NWB to lend to the DWCs at whatever scale of financing is required to achieve nationally agreed sustainability objectives. Like other public entities, the DWCs would be fully shielded by the public sphere. Currently, the NWB cannot open the credit issuing flood gates because of its strategy of protecting its credit rating. This mandate has thus emerged as an unintended barrier to it fully being a bank of and for the public sector and becoming the sustainable water bank. The barrier can be removed by the government, and its removal is justified as an effective response to the climate crisis (a policy orientation that has social credibility within Dutch society and globally, particularly in the form of Sustainable Development Goal 6: ‘Clean Water and Sanitation’; McDonald et al., Citation2021). The move would raise the quality of shielding provided by the Dutch public sphere to the delivery of NWB financing for sustainable water services. It would also eliminate the availability risks experienced by the DWCs – as a matter of aligned public policy, the NWB would be bound to providing all needed financing as and when necessary. This public–public collaboration would enhance operational efficiencies and help accelerate realizing the sustainable water challenge.

The state guarantee for sustainability financing would help to further align sustainability standards and conditionalities within the Dutch public banks. There are signs of promising practices and aspirations that substantiate a turn in this direction. The DWCs Vitens and Evides have already signalled a willingness to leverage their desirable creditworthiness to demand certain environment, social and governance (ESG) conditions from their financial suppliers. They increasingly prefer to engage with banks that can combine a focus on (environmental) sustainability with appealing financing arrangements. In Vitens’ long-term infrastructure vision (2016–40), notably, the utility acknowledges that rather than solely basing infrastructure decisions on engineering criteria, ‘social, economic and physical trends determine how we develop, maintain and manage our infrastructure’ (Vitens, Citation2016, p. 9). A state guarantee on sustainability projects would be welcomed.

If aligned purposively across the public sphere, and in particular with the NWB, a strong sustainability impetus would emerge, providing directionality within and across the public sphere, financial markets, and society. Rather than promoting a competitive race to the bottom by setting loan conditions that disproportionately favour cost/benefit analysis over all else, the DWCs could signal a race to ESG for financial providers (and the public banks could signal they would not fund non-ESG compliant projects for lack of a state guarantee) (see Ray et al., Citation2020, for further discussion on ESG standards and races to the bottom). This would not be without potential higher costs or public responsibility. It is one thing to request green and equitable supplying of public goods and services. It is another to ensure this is not simply greenwashing. New metrics and reporting standards will need to follow that hold public and private entities to account, transparently. As a public purpose entity, the NWB could lead on this initiative, in collaboration with other public banks in the Netherlands and across Europe. There is an urgent need to better understand how public banks’ metrics can matter more to green and just transitions.

The provisioning of a state guarantee, moreover, would enable the DWCs to rethink how they define and act upon current conceptions of ‘availability risk’ and ‘cost’. Their current approach is to privilege a mix of financial providers, with a roughly 50/50 split between public and private banking providers. If explicitly backed by state guarantees, this effort would be unnecessary (as with the state-backed water authorities, which almost exclusively source financing from the public banks). Indeed, the DWCs are aware that the private banks are likely to withdraw or withhold funding at times of crisis (hence why they foster public relationships as well). The DWCs are compelled to build and maintain relationships with private banks that they know are unlikely to pay off when most needed. That is, public water–private bank relationships are more likely to result in stranded relationships: that is, fair-weather financial collaborations that collapse at times of crisis. This approach to mitigating availability risks heaps greater risk onto public sector banks, which are called upon at times of crisis when private banks withdraw. That private banks inevitably do so at times of crisis, and that public banks and authorities are left to socialize these costs, is a well-established and well-documented empirical and historical fact (Griffith-Jones & Ocampo, Citation2018; Marois, Citation2012). Thus, current DWC borrowing practices disproportionately benefit private banks, which benefit in the good times and withdraw in the bad times, as and when they see it in their private interests. By contrast, public banks must maintain a stable foundation through thick and thin. For the NWB, it knows it is an institution that must always be there for the public water sector (confidential interview, 18 August 2021) – but the contradictions erected by misaligned public policy and guarantees raises questions as to whether that is in fact true. Aligned policy and state guarantees for sustainability projects eliminate wasteful DWC efforts to court fair-weather private banks while serving to accelerate sustainable transitions more rapidly.

Conclusions

By explicitly developing policy and processes that align public banks, like the NWB, with public water providers, like Vitens and Evides, trust can be institutionally ingrained and structurally safeguarded within the public sphere so that new ways of working can be formalized to confront one of the most pressing challenges of our time, sustainability, and do so along long-standing public interest priorities, like equitable and universal access. These changes will help to create new material and collaborative relationships, ones based in pre-existing legacies and histories but enhanced by aligned public purpose. This is not something understood as innate to being ‘publicly owned’ but as part of historically dynamic public banking entities and institutional relationships that are made and remade within the political economy of the Netherlands and global capitalism.

In the wake of four decades of neoliberal privatization and corporatization, contemporary scholars highlight the need to reclaim the state and public institutions (Cumbers, Citation2012; McDonald, Citation2016a). This involves ‘restoring public purpose in policies so that they are aimed at creating tangible benefits for citizens and setting goals that matter to people – driven by public-interest considerations rather than profit’ (Mazzucato, Citation2021, p. 6). This will need to be done in novel ways depending on the history, context, resources, challenges and power relations found in different societies. The NWB and the Dutch DWCs are in an enviable position to collaboratively tackle the challenge of sustainability. The question is whether the Netherlands will untap its public banks’ capacity to fund public water by better aligning public policy with public purpose and sustainability. These are lessons worth expanding upon in further case study research on public banks as policymakers, civil society, and scholars seek viable alternatives to the financing of green and just transitions globally.

Disclosure statement

No potential conflict of interest was reported by the authors.

Notes

1. The emphasis on cost recovery is also stipulated in the 2009 Dutch Water Supply Act, in which Article 11.1 stresses that DWCs are to operate on the basis of cost recovery.

2. Because the WACC is (partly) calculated on the basis of prevailing interest rates, it has declined over the past decade (from 6.0% in 2012 to 2.75% in 2020), whilst investment needs increased.

4. Interview with Evides, 15 September 2021.

5. The exceedance of the WACC has to be ‘repaid’ to consumers by lowering the WACC for that utility by the same amount in the following year.

6. In 2019, the WACC stood at 3.5%. Apart from Vitens and Evides all other water utilities realized a WACC between 1.07% and 2.78% (ILT, Citation2021).

7. This section is largely based on interviews with representatives from Evides (15 September 2021) and Vitens (29 November 2021).

8. This safeguarding is most aptly illustrated by the government intervention in one of the other water utilities in the Netherlands. The Water Company Drenthe WMD received an emergency loan of €8.5 million from the provincial government of Drenthe and the municipality of Emmen (both shareholders) in order to improve the ‘financial health’ of the water utility (see https://dvhn.nl/drenthe/Drents-waterbedrijf-WMD-wil-85-miljoen-euro-lenen-van-provincie-en-Emmen-24881094.html).

9. Illustrative of protecting the triple-A status is the Water Innovation Fund, which the NWB established as an independent entity to encourage innovation among the regional water authorities by supporting higher risk pilot projects (i.e., the fund can finance non-guaranteed entities without putting the NWB’s credit rating at risk; NWB, Citation2021, p. 47).

References

- Barrowclough, D. V., & Marois, T. (2022). Public banks, public purpose, and early actions in the face of covid-19. Review of Political Economy, 34(2), 372–390. https://doi.org/10.1080/09538259.2021.1996704

- Blokland, M. (1999). Evolution of the Dutch water supply sector. In M. Blokland, O. Braadbaart, & K. Schwartz (Eds.), Private business, public owners: Government shareholdings in water enterprises (pp. 35–48). Ministry of Housing, Spatial Planning and the Environment.

- Blokland, M., Warner, J. (1999). Labour productivity. In M. Blokland, O. Braadbaart, & K. Schwartz (Eds.), Private business, public owners: Government shareholdings in water enterprises (pp. 105–118). Ministry of Housing, Spatial Planning and the Environment.

- BNG. (n.d.) Driven by social impact. https://www.bngbank.com/About-BNG-Bank

- Butzbach, O., Rotondo, G., & Desiato, T. (2018). Can banks be owned? Accounting, economics, and law: A convivium. De Gruyter.https://doi.org/10.1515/ael-2017-0004

- Cassell, M. K. (2021). Banking on the state: The political economy of public savings banks. Agenda.

- Clifton, J., Díaz Fuentes, D., & Howarth, D. (eds.). (2021). Regional development banks in the world economy. Oxford University Press.

- Cumbers, A. (2012). Reclaiming public ownership: Making space for economic democracy. Zed Books.

- De Luna-Mart#237;nez, J., Vicente, C.L., Arshad, A. B., Tatucu, R., & Song, J. (2018). 2017 Survey of national development banks. World Bank Group.

- Dijkgraaf, E., & Vervaart, M. (2021). Andere winstregulering drinkwaterbedrijf nodig. Erasmus Competition and Regulation Institute, Erasmus University Rotterdam. https://ecri.nl/wp-content/uploads/2021/05/Andere-winstregulering-drinkwaterbedrijf-nodig-12-mei-2021.pdf

- Evides (2017). Jaarverslag 2016. Rotterdam, Netherlands.

- Evides (2019). Jaarverslag 2018. Rotterdam, Netherlands.

- Evides (2021). Jaarverslag 2020. Rotterdam, Netherlands.

- Griffith-Jones, S., & Ocampo, J. A. (eds.). (2018). The future of national development banks. Oxford University Press.

- Griffith-Jones, S., Spiegel, S., Xu, J., Carreras, M., & Naqvi, N. (2022). Matching risks with instruments in development banks. Review of Political Economy, 34(2), 197–223. https://doi.org/10.1080/09538259.2021.1978229

- Hanna, T. M. (2018). Our common wealth: The return of public ownership in the United States. Manchester University Press.

- Havekes, H., Koster, M., Dekking, W., Uijterlinde, R., Wensink, W., & Walkier, R. (2017). Water governance: The Dutch water authority model. https://dutchwaterauthorities.com/wp-content/uploads/2021/05/The-Dutch-water-authority-model.pdf

- Ho, P. (2016). An endogenous theory of property rights: Opening the black box of institutions. The Journal of Peasant Studies, 43(6), 1121–1144. https://doi.org/10.1080/03066150.2016.1253560

- Inspectie Leefomgeving en Transport (ILT). (2021). Financierbaarheid investeringsopgave drinkwatersector. Government of the Netherlands.

- La Porta, R., Lopez-de-Silanes, F., & Shleifer, A. (2002). Government ownership of banks. The Journal of Finance, 57(1), 265–301. https://doi.org/10.1111/1540-6261.00422

- Marcelin, I., & Mathur, I. (2015). Privatization, financial development, property rights and growth. Journal of Banking & Finance, 50, 528–546. https://doi.org/10.1016/j.jbankfin.2014.03.034

- Marois, T. (2012). States, banks, and crisis: Emerging finance capitalism in Mexico and Turkey. Edward Elgar.

- Marois, T., & Güngen, A. R. (2016). Credibility and class in the evolution of public banks: The case of Turkey. Journal of Peasant Studies, 43(6), 1285–1309. https://doi.org/10.1080/03066150.2016.1176023

- Marois, T. (2021). Public banks: Decarbonisation, definancialisation and decarbonisation. Cambridge University Press.

- Marois, T. (2022). A dynamic theory of public banks (and why it matters). Review of Political Economy, 34(2), 356–371. https://doi.org/10.1080/09538259.2021.1898110

- Marshall, W. C., & Rochon, L.-P. (2019). Public banking and post-Keynesian economic theory. International Journal of Political Economy, 48(1), 60–75.

- Marshall, W. C., & Rochon, L.-P. (2022). Understanding full investment and the potential role of public banks. Review of Political Economy, 34(2), 340–355. https://doi.org/10.1080/09538259.2021.2013633

- Mazzucato, M. (2015[2013]). The entrepreneurial state. Revised edition. Anthem.

- Mazzucato, M., & Penna, C. C. R. (2018). National development banks and mission-oriented finance for innovation. In S. Griffith-Jones & J. A. Ocampo (Eds.), The Future of National Development Banks (pp. 255–277). Cambridge University Press.

- Mazzucato, M. (2021). Mission economy: A Moonshot guide to changing capitalism. Allen Lane.

- McDonald, D. A. (2016a). To corporatize or not to corporatize (and if so how)? Utilities Policy, 40, 107–114. https://doi.org/10.1016/j.jup.2016.01.002

- McDonald, D. A. (ed.). (2016b). Making public in a privatized world: The struggle for essential services. Zed Books.

- McDonald, D. A., Marois, T., & Barrowclough, D. V. (eds.). (2020). Public banks and Covid-19: Combatting the pandemic with public finance. Municipal Services Project (Kingston), UNCTAD (Geneva), and Eurodad (Brussels). https://www.municipalservicesproject.org/

- McDonald, D. A., Marois, T., & Spronk, S. (2021). Public banks + public water = SDG 6? Water Alternatives, 14(1), 117–134. https://www.water-alternatives.org/index.php/alldoc/articles/vol14/v14issue1/606-a14-1-1

- Megginson, W. L. (2005). The economics of bank privatization. Journal of Banking and Finance, 29(8–9), 1931–1980. https://doi.org/10.1016/j.jbankfin.2005.03.005

- Mertens, D., Thiemann, M., & Volberding, P. (eds.). (2021). The reinvention of development banking in the European union. Oxford University Press.

- NWB (2010). Annual Report 2009. Nederlandse Waterschapsbank NWD Bank. https://nwbbank.com/en/about-nwb-bank/publications

- NWB (2011). Annual Report 2010. Nederlandse Waterschapsbank NWD Bank. https://nwbbank.com/en/about-nwb-bank/publications

- NWB (2012). Annual Report 2011. Nederlandse Waterschapsbank NWD Bank. https://nwbbank.com/en/about-nwb-bank/publications

- NWB (2013). Annual Report 2012. Nederlandse Waterschapsbank NWD Bank. https://nwbbank.com/en/about-nwb-bank/publications

- NWB (2014). Annual Report 2013. Nederlandse Waterschapsbank NWD Bank. https://nwbbank.com/en/about-nwb-bank/publications

- NWB (2015). Annual Report 2014. Nederlandse Waterschapsbank NWD Bank. https://nwbbank.com/en/about-nwb-bank/publications

- NWB (2016). Annual Report 2015. Nederlandse Waterschapsbank NWD Bank. https://nwbbank.com/en/about-nwb-bank/publications

- NWB (2017). Annual Report 2016. Nederlandse Waterschapsbank NWD Bank. https://nwbbank.com/en/about-nwb-bank/publications

- NWB (2018). Annual Report 2017. Nederlandse Waterschapsbank NWD Bank. https://nwbbank.com/en/about-nwb-bank/publications

- NWB (2019). Annual Report 2018. Nederlandse Waterschapsbank NWD Bank. https://nwbbank.com/en/about-nwb-bank/publications

- NWB (2020). Annual Report 2019. Nederlandse Waterschapsbank NWD Bank. https://nwbbank.com/en/about-nwb-bank/publications

- NWB (2021). Annual Report 2020. Nederlandse Waterschapsbank NWD Bank. https://nwbbank.com/en/about-nwb-bank/publications

- NWB (n.d.) NWB Bank Sustainability Policy. https://nwbbank.com/en/investor-relations

- NWB Bank (n.d.). Our history. https://nwbbank.com/en/about-nwb-bank/our-history

- Orbis Bank Focus. (2021). Nederlandse Waterschapsbank NV. Online database inquiry 11 October 2021. Bureau van Dijk.

- Ray, R., Gallagher, K. P., & Sanborn, C. A. (2020). Standardizing sustainable development? Development Banks in the Andean Amazon. In R. Ray, K. P. Gallagher, & C. A. Sanborn (Eds.), Development banks and sustainability in the Andean Amazon (pp. 1–46). Routledge.

- Scherrer, C. (ed.). (2017). Public banks in the age of financialization: A comparative perspective. Edward Elgar.

- Skidelsky, R., Martin, F., & Westerlind Wigstrom, C. (2011). Blueprint for a British investment bank. Centre for Global Studies.

- VEWIN (2021). Drinking water factsheet. https://www.vewin.nl/SiteCollectionDocuments/Publicaties/Vewin-Drinking-Water-Fact-Sheet-2021-5253.pdf

- VEWIN (various years). Water Supply Statistics. Rijswijk, Netherlands.

- Vitens (2016). Resiliently Ahead: Longterm Vision on our Infrastructure 2016–2040. https://vitensinnovates.com/wp-content/uploads/2018/05/Vitens-LTV-LR.pdf

- Vitens (2017). Jaarverslag 2016. Zwolle, Netherlands.

- Vitens (2019). Jaarverslag 2018. Zwolle, Netherlands.

- Vitens (2020). Water voor Nu en Later: Langetermijnvisie op de Vitens Infrastructuur 2020–2025. https://www.vitens.nl/-/media/ltv-2020_def_jan21.pdf?la=nl-nl

- Vitens (2021). Jaarverslag 2020. Zwolle, Netherlands.

- World Bank (2012). Global financial development report 2013: Rethinking the role of state in finance.