Abstract

What resources help young people secure homeownership and housing wealth? We combine findings from two literatures, one which emphasizes the role of income, education, and inheritances and one which emphasizes the role of financial strategies, to evaluate whether a more comprehensive set of resources help young people aged 18–45 navigate the housing market in the United States. Using the 2019 Survey of Consumer Finances (SCF) and through logistic and Heckman regressions, we identify three main findings. First, financial strategies such as financial knowledge, credit card access, and financial risk-taking help explain homeownership and housing wealth for young people, over and above traditionally studied household and family resources. These are especially important for middle-income households. Second, different financial strategies matter for homeownership versus housing wealth. Third, ‘optimal’ financial strategies like good savings habits may not always be associated with success in the housing market. Combined, these findings imply that while in theory young people can leverage resources beyond their own income or the ‘Bank of Mum and Dad’, in practice the ideal combination is complex. To capture this complexity, we introduce the term ‘acquisition capital’ to represent the multiple sets of resources that young people leverage to secure homeownership and housing wealth.

1. Introduction

How do financial strategies in the United States (US) operate in tandem with, or in addition to, own and parental economic resources to help or hinder young people secure homeownership and the housing wealth that comes with it? It is well established that young people in high-income countries are increasingly shut out of homeownership, with pejorative media portrayals of millennials spending their earnings on avocado toast. Most research explaining homeownership among young people focuses on economic resources like income or inheritances. In this article, we confirm that these resources are important, but additionally find that financial strategies can help or hurt chances for homeownership and its resulting housing wealth. Combining research from welfare state and inequality studies with research emphasizing the financialization of everyday life, we estimate the effect of 13 potential determinants of homeownership and housing wealth for young people aged 18–45 (an extended version of millennials that includes the youngest of Gen X and the oldest of Gen Z) using the 2019 Survey of Consumer Finance (SCF). We find that dimensions such as financial knowledge, as well as credit card access and payoff habits, improve the likelihood of homeownership, while financial risk-taking worsens it. In fact, homeownership likelihood for median income households that adopt certain financial strategies increases by 29 percentage points, even after controlling for income effects. In addition, we find financial strategies matter in different ways for homeownership and housing wealth. For instance, financial risk-taking is associated with increased housing wealth for homeowners but a lower likelihood to own. Moreover, those strategies associated with ‘good’ personal finance are not always optimal for securing homeownership or housing wealth.

This article contributes to the field in three ways. First, much of what we know about young people’s homeownership and housing wealth opportunities is based on qualitative analyses or quantitative descriptive analyses (e.g. descriptive statistics). These studies highlight the increased difficulty younger generations face in the housing market, but it is hard to discern the relative impact of different factors. We build on these studies by estimating the effect of specific variables through logistic and Heckman regression analyses. While we make no claims about causality, these models do enable a more precise comparison of potential contributing factors. Second, we combine relevant resources identified in different literatures – household resources, family resources, and financial strategies. To our knowledge this is the first paper to combine these resource ‘sets’. As we describe later, we term the combination ‘acquisition capital’ to reflect the sets of resources young people can leverage to acquire homeownership and its associated housing wealth. Third, we engage with the popular narrative that good personal finance is necessary in contemporary financialized housing markets by problematizing what is meant by ‘good’. Indeed, some socially defined ‘optimal’ behaviours such as ‘good’ savings habits seem to matter less than might be expected, and other behaviours like financial risk-taking matter in different ways for homeownership and housing wealth. Our findings point to a more complicated story and show that accessing homeownership is just the first step in securing housing wealth.

Homeownership and housing wealth help young people reach important life milestones and mitigate financial risk through securing assets. This article provides a fuller picture of the first stages of that process. In what follows we assess the different strands of literature, linking the resources above to housing outcomes, identify the debates and gaps across these literatures, and describe why it is important to combine these literatures to extend the research on housing outcomes for young people. We then introduce our data, methods, and analytic framework followed by findings from logistic and Heckman regression analyses. We conclude with a discussion of the theoretical and practical implications of our findings, their potential generalizability to other countries, and suggestions for future research.

2. Contemporary trends in housing

Well-established in the social science literature is that young people in high-income countries are increasingly shut out from housing access at a time when welfare state retrenchment (Hacker, Citation2004; Pierson, Citation2001) and the shift to asset-based welfare and privatized Keynesianism (Crouch, Citation2009; Doling & Ronald, Citation2010; Köppe & Searle, Citation2017; Ronald et al., Citation2017) require individuals and households to manage their financial security with less collective risk-sharing. They often do so through homeownership, which young people continue to desire and believe an economically sound decision, despite often feeling it is out of reach (McKee, Citation2012; Bogardus Drew, Citation2014; Ratiu, Citation2021). Barriers to homeownership and its wealth-generating potential are a general feature faced by ‘generation rent’, but are nonetheless felt unevenly within the younger cohort because of the inter and intragenerational heterogeneity that exists in an era of increasing income and wealth inequality (Flynn & Schwartz, Citation2017). This unevenness – locking some out and creating extra security for others – also adds more precarity around the ‘edges’ of homeownership, where younger generations have a more difficult time sustaining ownership and accumulating wealth (Haffner et al., Citation2017).

To explain both the overall and uneven declines in homeownership in the younger generation, the literature has generally focused on the importance of household and family resources such as income, education, intergenerational transfers, and occasionally parental class status (Bond & Eriksen, Citation2021; Cook, Citation2021; Guiso & Jappelli, Citation2002; Lux et al., Citation2018; Mulder & Smits, Citation2013; Ronald & Lennartz, Citation2018). A second, smaller strand suggests that housing outcomes may also be linked to financial strategies (Artle & Varaiya, Citation1978; Barakova et al., Citation2003, Citation2014; Lee & Kim, Citation2022; Li et al., Citation2017; Shapiro, Citation2021), and aligns with the broader financialization of everyday life literature (Langley, Citation2008; van der Zwan, Citation2014). While most findings are not specific to young people, financial strategies should be particularly relevant to them given that stricter mortgage regulations in the wake of the 2007/2008 housing crisis and continued increases in housing prices since that time will disproportionately affect those earlier in their housing career. This section describes these two sets of literatures, one focusing on economic resources (household and family) and the other focusing on financial strategies, in turn.

2.1. Economic resources (household and family)

Among young people, resources such as income, education, intergenerational transfers, and occasionally parental class status have been linked to homeownership. Unsurprisingly, income seems to be among the most important resources enabling young people to attain homeownership. In a comprehensive review of the literature on homeownership among millennials, Xu et al. (Citation2015) find the transition from renter to homeowner is often determined by changes in family composition (moving from a single to dual-income household) which improves levels of household income (Fisher & Gervais, Citation2011) and makes homeownership more affordable and accessible (Hendershott et al., Citation2009).

Increasingly, younger generations rely on parental support to help them navigate the housing market. This support takes different forms. Intergenerational transfers influence young adult’s homeownership experiences and preferences (Adkins et al., Citation2020; Lux et al., Citation2018; Ronald & Lennartz, Citation2018). In the US, Lee et al. (Citation2020) find a 5000 dollar transfer to adult children increased homeownership entry from 1998 to 2004. Bond & Eriksen (Citation2021) found similar results for the 2000–2012 period. To date, these analyses have not considered whether expecting an inheritance – but not yet receiving it – operates in the same way. Beyond concrete transfers, coresidence with parents serves as an increasingly common form of in-kind transfer as adult children save up for a down payment while living rent free (Köppe, Citation2018).

Less fungible types of resources seem to matter too. For instance, parental class status correlates with homeownership in the subsequent generation, at least in the UK. There, children of parents with lucrative occupations are more likely to be homeowners (Coulter, Citation2018). In the Czech Republic, socialized attitudes towards homeownership are higher where parents have high incomes and intergenerational transfers are large (Lux et al., Citation2018). The link between a young person’s educational attainment and homeownership is less clear. Drawing on Bourdieu’s concepts of cultural, social, and economic capital (Citation1986), sociologists suggest that while young people have higher levels of educational attainment than past generations, homeownership may be depressed or delayed if high education is coupled with low incomes (Crawford & McKee, Citation2018). As applied to the US, higher education should lead to greater income potential for young people, but high student loan debt may serve to delay homeownership (Bricker & Thomson, Citation2016; Mezza et al., Citation2020). Relatedly, higher education financial support from parents (Williams, Citation2017) may help the future housing careers of their children. Young people without student loan debt may be able to better save for a down payment and enter homeownership.

Homeownership is important for many reasons, but particularly for its wealth-generating potential. Housing wealth may serve as a resource-replacement in later life (Kemeny, Citation1980), but even earlier in the life course it enables equity borrowing to fund current consumption, which is especially important for younger and lower income households (Ong et al., Citation2013; Smith et al., Citation2022; Wood et al., Citation2013). The small body of literature that focuses on the housing wealth of young people has continued to grow over time (Arundel, Citation2017; Dewilde & Flynn, Citation2021; Squires et al., Citation2022). These studies operationalize housing wealth using measures of home equity (a typical measure of net housing wealth) or home values (a typical measure of gross housing wealth) and consistently find housing wealth concentrated among young people with high household incomes. In a UK study, Arundel (Citation2017) finds a decline of housing equity among young homeowners aged 20–39 compared to older generations, but that within this generation most housing wealth is concentrated in the top 20 and top 40 per cent of homeowners. In a comparative study of the US and Europe, Dewilde & Flynn (Citation2021) similarly find that the accumulation of housing assets is concentrated among high-income homeowners aged 22–44. Further, what counts as ‘young’ is often extending into middle age precisely because milestones like buying a home are increasingly delayed.

Overall, an evaluation of the links between economic resources and homeownership and housing wealth suggests several important explanatory factors, but debates and gaps in the literature persist. These include to what extent education correlates with homeownership, if expecting to receive an inheritance matters for housing outcomes, and whether and to what extent the factors contributing to homeownership similarly contribute to housing wealth.

2.2. Financial strategies

The growing importance of household and parental resources in the bid to become a homeowner has coincided with the financialization of everyday life. This literature suggests the financialization of the everyday occurred through a combination of the shift towards financial markets for everyday needs (‘the democratization of finance’), technological advances in investing and banking, and cultural representations and narratives of ‘good’ personal finance. The democratization of finance has been channelled through mediums such as financial education programs as well as financial advertisements and literacy campaigns promoting the importance of financial literacy, risk-taking, and credit worthiness (Campbell, Citation2006; Davidson, Citation2012; Langley, Citation2008; Maman & Roshenek, Citation2020; Martin, Citation2002; van der Zwan, Citation2014). Of course, what constitutes as ‘good’ personal finance is socially constructed and up for debate. Nonetheless, personal finance is an important factor for housing access among young people (Hackel & Shan, Citation2014), especially in the US where credit rating systems require individuals to micromanage and often manipulate their spending and credit behaviour in the lead-up to homeownership to secure favourable mortgage terms (Kear, Citation2017). Therefore, we suggest personal financial strategies are an important missing dimension to the literature on housing access for young people, leading to a potential overestimation of the degree to which household or parental resources affect homeownership.

To be sure, scholars have operationalized financial strategies and relationships with housing outcomes, though this literature is sparse with only few pieces that focus on the housing outcomes of young people. Perhaps most prevalent in this literature strand is how credit access, quality, and worthiness are linked to homeownership (Barakova et al., Citation2003, Citation2014; Brown & Caldwell, Citation2013; Hackel & Shan, Citation2014). For instance, in a study of homeownership among households with a head between 21 and 50 years of age in the US who had moved within the last 2 years, Barakova et al. (Citation2003) summarize that homeownership is directly linked to mortgage credit accessibility and credit quality (measured by credit score and number and type of accounts). Other studies find that higher levels of financial literacy are associated with homeownership (Shapiro, Citation2021) and that these relationships vary by race and ethnicity (Lee & Kim, Citation2022). Incorporating the use of a self-reported risk assessment, in a Chinese study, Li et al. (Citation2017) find that more conservative attitudes towards financial risk-taking are associated with lower housing value appreciation that can negatively impact households’ overall wealth.

Savings behaviours, though important in the financialization of the everyday, are barely studied in relation to housing outcomes, and especially housing outcomes of young people. Summarizing Artle & Varaiya (Citation1978), Xu et al. (Citation2015, p. 203) suggest a life cycle model might explain millennials decisions to either own or rent, emphasizing the shift into homeownership as soon as a household has the down payment to do so. In the sample of US households with heads aged 21–50, Barakova et al. (Citation2003) also find that wealth constraints (inclusive of household savings) were the largest factor hindering homeownership. Bhutta et al. (Citation2020a, Citation2020b) find that households have a higher propensity to save in 2019 compared to earlier years, and note a shift towards the internet, personal connections, and business professionals for securing financial advice.

A large part of the way people navigate money (financial attitudes and behaviours) is learned during childhood and adolescence. The literature on consumer and financial socialization has a long history (Hira, Citation1997; Ward, Citation1974) and aligns with the more general field of behavioural science that emphasizes the importance of learned attitudes and behaviours rooted in early life-course socialization processes. A sub-section of research in this area (Ammerman & Stueve, Citation2019; Bendall, Citation2022; Shim et al., Citation2010; Robertson-Rose, Citation2020; Ullah & Yusheng, Citation2020; Webley & Nyhus, Citation2006) contends that financial attitudes around such topics such as savings, borrowing, and financial literacy are learned directly from parents and that this learning takes place during childhood, adolescence, and sometimes into young adulthood (notably with regard to retirement savings behaviour). While financial strategies can be a distinct potential contributor to the acquisition of homeownership and housing wealth, they also point to yet another way in which resources transfer from one generation to the next. It also points to the likelihood that such habits develop before homeownership, not the other way around.

We contend this literature provides a good starting point for assessing how the financial strategies millennial households adopt are associated with housing outcomes. To that end, we combine the different strands of literature explained above to evaluate the links between a more comprehensive set of resources and the housing outcomes among young people in the US. While the US is a good test case, liberalizing financial markets (Aalbers, Citation2008) and the growing reliance on credit histories in Europe (Whitehead and Williams, Citation2017) may mean that dynamics in the US could be a bellwether for trends more broadly across high-income countries.

In this article, our more comprehensive set of resources include both household and parental resources, the focus of most previous research in this area, but also include personal finance strategies. Specifically, we construct 13 variables that may affect how young people navigate the housing market to secure homeownership and its associated housing wealth. These resources are: household income, household educational attainment, student loans, receipt of inheritance, the expectation to receive an inheritance, parental educational attainmentFootnote1, household spending/savings behaviour, credit card payoff habits, information sources for saving and investing, information sources for credit and borrowing, financial knowledge, financial risk-taking, and seeking the best credit terms.

We expect four household and family resources (household income, household educational attainment, receipt of an inheritance, and parents’ educational attainment) to be associated with homeownership and gross housing wealth (Hypothesis 1a) among millennials. However, the cross-cutting dynamics of educational attainment and student debt, plus the introduction of the expectation to receive an inheritance in addition to already receiving one, may attenuate the relationship for these two variables (Hypothesis 1b). Adapting the literature on the financialization of the everyday, we expect six of the seven financial strategies (household spending/savings behaviour, credit card payoff habits, information sources for saving and investing, information sources for credit and borrowing, financial knowledge, and seeking the best credit terms) to also predict homeownership and gross housing wealth (Hypothesis 2). However, we expect financial risk-taking to operate in opposite ways for each outcome of interest. Specifically, we expect the odds of homeownership to be lower among financial risk-takers (Hypothesis 3a) but that gross housing wealth will be higher among those households that take financial risks (Hypothesis 3b).

3. Data, empirical design, and limitations

3.1. Data, ‘acquisition capital’ conceptualization, and sample

We use the 2019 SCF data to carry out this study. The SCF is a triennial cross-sectional survey of the financial situation of US Households conducted by the US Federal Reserve Bank. Due to the high rate of survey non-response, the SCF uses a multiple imputation method and creates five imputed datasets that, when combined and weighted, provide plausible scenarios of household financial situations and are nationally representative of US households (US Federal Reserve, n.d.). The 2019 SCF data is the best choice because the breadth of information collected in this data year allows us to operationalize and measure the three resource sets of interest. Moreover, to our knowledge, no other dataset exists that includes all variables of interest.

We identified relevant SCF variables to measure three sets of resources – household and family resources along with household financial strategies (see ). We used theoretical, empirical, and logical justifications based on the literature strands identified earlier to determine how to operationalize and, when relevant, order the original SCF variables that had no previous or obvious hierarchy. Throughout, we refer to these three sets of resources as ‘acquisition capital’ – a collective body of resources that young people hold through various means, that when combined, lead them to navigate the housing market in a particular way. Others (e.g. Bourdieu, Citation1986; Putnam, Citation1993; Savage, Citation2015) have broadened the way we think of capital beyond economic resources. We follow that same logic here but depart slightly by focusing less on the ‘form’ that capital takes and more on the way it is used to secure homeownership and housing wealth. We allow for the possibility that young people can and do draw on different resources to successfully enter homeownership and build housing wealth. In this way we can ask whether and to what extent non-economic resources can make up for having less income.

Table 1. Dependent and independent variables.

The analytic sample size is 1520 households for homeownership and 723 households for gross housing wealth. The sample includes independent households (only one economic unit, with no additional adults in the household) where both the reference person and the spouse/partner are between 18 and 45 years of age and not in full-time education. We followed Dewilde & Flynn (Citation2021) who selected a similar age range because it is well-documented that first-time homeownership is increasingly delayed. In the US the median age of first-time homebuyers increased from 30 in 2010 (Wong & Herman, Citation2020) to 33 in 2019 (National Association of Realtors, Citation2021).Footnote2 For context, a 45-year-old in 2019 was 34 at the beginning of the 2008 housing crash. Our definition is therefore inclusive of young homeowners navigating the housing market in the post-recession era. For practical purposes, this also ensures a sufficient sample for the housing wealth regressions.

3.2. Empirical design

The two dependent variables of interest are homeownership for the full sample and gross housing wealth (logged) for the sub-sample of homeowners. Logistic and Heckman regressions are used to determine the relationship among acquisition capital and the two housing outcomes. The Inverse Mills ratios (IMRs) that account for selection into homeownership are included in the Heckman regressions of logged gross housing wealth (see online supplemental appendix Table A1 for the probit models from which the IMRs are estimated). Appropriate socio-demographic controls are included in all regressions.Footnote3 We then plot predicted odds of homeownership and predicted gross housing wealth for households at two points on the income spectrum (fiftieth and ninetieth percentiles) combined with selected financial strategy types, holding other variables constant at their means. For all analyses, mi svy set with bootstrapping (PSU is the case ID yy1) for multiply imputed data with a complex survey design was used. We applied replicate weights (999) over the five implicate to obtain bootstrapped standard errors.Footnote4

Further details on conceptual and methodological design considerations are available in the online supplemental appendix.

3.3. Limitations

We note two data-driven caveats. First, no geographic variables exist in the SCF data out of privacy concerns. All results should be interpreted at the national level only, and the weighting of the variables enables this. Given the spatial variation in housing prices (and thus housing wealth), households in more expensive regions may have higher housing wealth than those that live in less expensive regions.Footnote5 However, while there are cities with very high and low house prices values, the majority of cities (72%) hover around a similar price-to-income ratio, meaning that most people, in most places, experience similar affordability constraints.Footnote6 Further, we expect few theoretical reasons that financial strategies would vary by geographic areas, meaning that it is unlikely that geography would be a confounding variable.

Second, our data and methods allow us to undertake an exploratory correlational study, and our findings should not be considered causal. Our literature review indicates that financial strategies develop before entry into homeownership, meaning such variables can plausibly be treated as independent variables. This is not to say that such habits never change over time. Assessing that possibility is outside the scope of this paper.

4. Findings

4.1. Housing outcomes and ‘acquisition capital’: regression results

Results from our regression models are shown in . In support of Hypothesis 1a, standard household and family resources significantly shape homeownership and logged gross housing wealth (hereafter, ‘housing wealth’) among young people in the US. However, the resources that matter differ across the two outcomes. First, the likelihood of homeownership is 8% and 5% higher (moving from M1 to M2) for every 10,000 dollar increase to household income; while housing wealth is 3% higher for every 10,000 dollar increase to household income (M1 and M2). Households with a bachelor’s degree are more likely to own a home and have higher housing wealth than those with some college/associates degree. Along with income, the magnitude of the association between educational attainment and homeownership declines when moving from M1 to M2. Homeownership odds for households with at least a bachelor’s degree is 60% higher than the reference group (M1) and falls to 42% higher than the reference group (M2) when financial strategies are included. These results begin to show that financial strategies matter to housing outcomes among young people in the US and provide evidence of omitted variable bias in previous studies.

Table 2. Logistic and Heckman regressions predicting housing outcomes among millennial households.

Partially confirming Hypothesis 1a, receipt of an inheritance significantly predicts homeownership among millennials but is not associated with higher housing wealth. Refuting Hypothesis 1a, parental educational attainment is not significantly associated with homeownership odds or housing wealth.

As expected, in support of Hypothesis 1b, the absence of student loans significantly predicts entry into homeownership and higher housing wealth when compared to households that report having student loans. Therefore, having student loans may potentially attenuate the effects of higher education. The expectation to receive an inheritance is significantly associated with housing wealth, but not the odds of homeownership – showing the possible interplay of already receiving, and the future expectation to receive an inheritance.

The inclusion of financial strategies in M2 for both housing outcomes show these acquisition capital resources significantly shape homeownership odds and housing wealth among millennials in the US. These results further solidify past studies may be suffering from omitted variable bias, though more so for homeownership than for housing wealth. In support of Hypothesis 2, the likelihood of homeownership is higher for households that spend less than their income, receive savings and investing advice from different sources (including personal networks, advertisements, and professional advice), and have medium-high to high financial knowledge, compared to the respective reference groups.

However, refuting Hypothesis 2, the results also show that for some financial strategies the most ‘optimal’ strategy types are not necessarily those associated with homeownership or housing wealth. Having access to credit cards but carrying revolving credit is significantly associated with homeownership compared to those that report more consistent payoff habits, while spending more than income is significantly associated with higher housing wealth. Households that report regularly spending more than their income have housing wealth that is 16% higher than those who report spending the same as their income. Both high and low financial risk-taking predicts lower homeownership odds than households that report sometimes taking financial risks, at best a partial confirmation of Hypothesis 3a. Households often willing to take financial risks have housing wealth that is 14% higher than households that report sometimes taking financial risks, a confirmation of Hypothesis 3b.

The regression results indicate that household resources, family resources, and financial strategies all have an impact on homeownership and housing wealth among millennials. This joint set of resources, which we term ‘acquisition capital,’ seems to hold promise as a heuristic and empirical construct for understanding the collective body of resources that shape the ways in which young people navigate the housing market.

For the more traditionally used economic resources, the regression results support past literature that homeownership odds increase with household income and receipt of an inheritance (Bond & Eriksen, Citation2021; Flynn & Schwartz, Citation2017; Lux et al., Citation2018; Ronald & Lennartz, Citation2018). We contribute to the field by also showing how these variables correlate with housing wealth. Our findings refine past research about the link among household and parental educational attainment and the two housing outcomes (Crawford & McKee, Citation2018). The models suggest household educational attainment correlates with homeownership odds and housing wealth among millennials, in addition to not holding student loan debt. These findings continue to fuel the debate about how higher education coupled with familial financial educational support influences housing outcomes, which is especially important in the US given the prevalence of student loans. Our findings regarding parental educational attainment suggest this proxy of family class status is surprisingly not important for either homeownership or housing wealth.

Our finding that expecting an inheritance predicts higher housing wealth but is not related to homeownership suggests different strategies may be at work. Some young people may intentionally time housing purchases with an infusion of cash, thereby delaying homeownership. However, those that do nonetheless become homeowners may anticipate an easier ability to service their mortgage down the road, and in a sense, borrow against the expected inheritance when buying a house. These results, coupled with the results for receipt of an inheritance, show the links between inheritances and housing market outcomes among millennials is more complicated than the ‘Bank of Mum and Dad’ moniker would suggest.

As for the financial strategy variables, the regression results indicate that several financial strategy types relate to millennials’ success in the housing market. That homeownership odds are linked to higher levels of financial knowledge among millennials extends past research in this area (Lee & Kim, Citation2022; Shapiro, Citation2021) and, new to the literature, suggests financial knowledge may not be linked to housing wealth. The findings on credit and borrowing information support what we know from descriptive findings of household finance and the financialization of everyday life (Bhutta et al., Citation2020a, Citation2020b; van der Zwan, Citation2014). However, new to the literature, we showed empirically that specific habits and behaviours are more likely to correspond with millennials’ success in the housing market. For instance, credit card access is more important than whether credit cards are paid in full every month, which supports the literature that credit access is a good proxy for mortgage access (Barakova et al., Citation2003, Citation2014). The positive relationship between housing wealth and regularly spending more than income is compatible with the literature indicating that equity borrowing might be used to fund current consumption (Ong et al., Citation2013; Wood et al., Citation2013). In general, our findings suggest that popular narratives about the necessity for millennials to save and ‘quit buying the avocado toast’ to be able to purchase a home or build housing wealth are not rooted in empirical findings.

The results for financial risk-taking additionally suggest ambiguities around both popular financialization narratives of risk taking and measures of risk. Popular financial narratives suggest that financial risk-taking is good for economic security (Martin, Citation2002). However, current definitions of risk-taking lack clarity, and more work needs to be done to better understand what households have in mind when they answer such survey questions. That the results show both too little or too much risk is linked to lower homeownership odds among millennials suggests we need to better understand what it specifically means for households to be ‘sometimes risk-takers’ and why the ‘sometimes risk-takers’ are rewarded with homeownership, but only ‘often-willing’ risk-takers are rewarded with slightly higher housing wealth.

Beyond the concept of acquisition capital, our findings about socio-demographic characteristics are in line with past research about how such characteristics are linked to winners and losers in the housing market (Coulter, Citation2018; Hackel & Shan, Citation2014; Lee et al., Citation2020; Lux et al., Citation2018). Namely, the likelihood of homeownership increases if the respondent is male (M1 only), older, and white, and at the household level if at least the reference person or spouse is employed (M1 only), the household is coupled, or if children are present. Far fewer socio-demographic factors matter for housing wealth compared to homeownership – only partner status and age significantly correlate with higher housing wealth.

Our results also hold new and unexpected findings when it comes to housing wealth and race. While all three racial groups have significantly lower homeownership odds compared to white households, the results show that all three groups have higher housing wealth than white homeowners. Contrary to the well-established descriptive findings that illustrate a Black-white racial wealth gap, Black homeowners have housing wealth 16% higher than white homeowners (M2, weak association). Our results likely differ in part because log-transforming the gross housing wealth variable de-emphasizes gross housing wealth outliers, which are almost exclusively white households, in addition to controlling for other characteristics in the model that are not controlled for in descriptive statistics, illustrating a gap.Footnote7

Our housing-related outcome controls (not included in our concept of acquisition capital but potentially important for homeowners) indicate that among homeowning households, those that reside in at least their second primary home or own other residential real estate have higher housing wealth than the respective reference groups. Being a second-time owner or owing other real estate may be prime ways for homeowners to build on and consolidate housing wealth over time.

4.2. Financial strategies across the income distribution: predicted probabilities

To enhance our understanding of how financial strategies shape housing outcomes for millennials in the US, and show how select financial strategies shape homeownership odds and levels of housing wealth for households at the fiftieth and ninetieth percentiles of the income distribution. The first scenario at each income percentile is for household income only (the ‘base category’). The subsequent scenarios combine household income with various financial strategies, chosen for their statistical significance in each model, to show how the likelihood of homeownership and levels of gross housing wealth increase with certain combinations of income and financial strategies.Footnote8 For all scenarios, all other variables are held constant at their means.

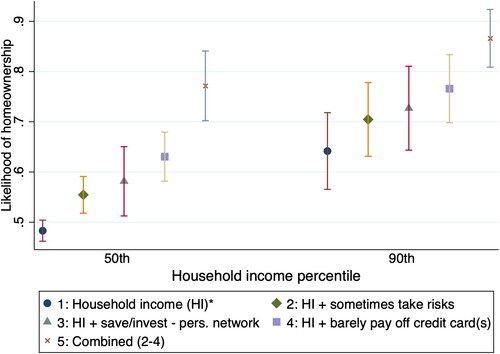

Figure 1. Predicted values of homeownership likelihood for households at two income percentiles. Notes: *Comparison scenario is scenario 1. For households at the median, significant differences are shown comparing scenarios 2–5 to scenario 1. For households at ninetieth percentile, signficant differences are shown comparing scenario 5 to scenario 1.

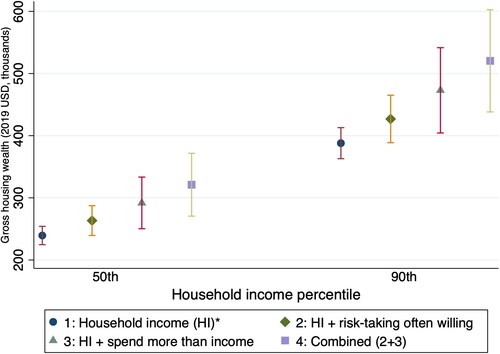

Figure 2. Predicted gross housing wealth for households at two income percentiles. Notes: *Comparison scenario is scenario 1. For households at the median and ninetieth percentiles, significant differences are shown comparing scenario 4 to scenario 1.

First, homeownership odds increase if households take moderate financial risks, use their personal network for savings and investing advice, and have some revolving credit, especially for households with median incomes (). Significant differences exist for households at the median when compared to households at the ninetieth percentile. When the financial strategy types are combined in scenario five, the likelihood for households with median incomes to own a home is 29 percentage points higher than the base category (compared to 22 percentage points higher at the ninetieth percentile). Not only are these strategies substantively important for median households, but the predicted probabilities imply there is a set of financial strategies that put some median earners at the same likelihood of ownership as some earners at the ninetieth percentile. illustrates households at both the fiftieth and ninetieth percentiles of income that are often willing to take financial risks and spend more than their income (scenario four) have predicted housing wealth that significantly differs from the base category.Footnote9

We draw two conclusions from the figures. First, financial strategies are important for households at the median compared to households at the top, especially for homeownership odds. In some ways, this is good news for those concerned about growing inequality: there are at least some strategies that help make up for having less income. The second is that young people seemingly face trade-offs when it comes to choosing the ‘right’ financial strategies to both enter homeownership and grow housing wealth. This is because the financial strategy types that correlate with homeownership differ than those that correlate with housing wealth. Extending the findings in the regression results, in several cases the financial strategy types that are not the most ‘optimal’ may better predict housing outcomes than those strategies that are widely promoted by narratives around the financial strategies young people should acquire to successfully navigate the housing market.

5. Conclusions

Overall, our results show that all three sets of acquisition capital resources – household, family, and financial strategies – matter for housing outcomes among millennials in the US, suggesting a complex path to homeownership for this group. The financial strategies households adopt matter for housing outcomes, over and above traditionally studied economic resources. Certain financial strategies can partially substitute (at least statistically) for household and family resources, indicating that growing income and wealth inequality may not completely block some middle-income households from securing homeownership and its associated housing wealth. However, the types of strategies that matter may not always be the most ‘optimal’ strategy type and different types of strategies may matter for homeownership (especially for households at the median), versus building housing wealth.

Ours is the first study to combine these sets of resources in empirical models and should be considered exploratory. Future work should extend in several areas. First, the lack of data in some areas point to a need for future data collection. For instance, while ‘sets’ of resources are analytically useful, we are bounded by data availability of variables that capture acquisition capital. This necessitates deeper discussions about the potential mechanisms leading to homeownership, as well as more detailed definitional considerations, for instance, in defining what too much or too little financial risk-taking looks like. Current data also cannot address whether resources shift, and financial strategies change once homeownership is achieved. Further, the SCF, like most household surveys, often limits detailed data collection to the reference person or the spouse. In the US, nearly 20% of households include millennials living with their parents, relatives, or in other co-housing situations (authors’ own calculations using the SCF data). Future data collection efforts should address the housing aspirations and outcomes of this ‘hidden group’ both in the US and in other high-income countries, including the design of studies that can more precisely determine how financial strategies interact with geography.

Future research should also examine the generalizability of these findings to other high-income OECD countries. For instance, while we do not expect European mortgage markets to converge into an American-style market, recent initiatives like the Capital Markets Union agenda and the FinTech action plan show how the EU is moving towards deeper financial integration driven in part by FinTech solutions like big data and artificial intelligence. This makes Europe look more like the US, where sophisticated and algorithmic mortgage lending and credit rating systems have been present for decades. The enhanced technical ability to combine different forms of personal data to determine creditworthiness will likely strengthen the link between personal finance and creditworthiness in Europe and the US alike.

Generalizability to all high-income countries should not be assumed, however. To take two non-European examples, we might expect the relationships to be more apparent in a country such as Australia, where housing wealth drives economic decisions and trends such as equity borrowing are common. Cases such as that of Japan would be more complicated. There, the younger generation is experiencing fractured housing pathways and a greater need for financial literacy because of changing mortgage conditions. Yet, differences in land use and the subdued role of housing wealth point to clear differences in homeownership between Japan and the United States.Footnote10 A comparative study may be well-placed to assess the extent to which acquisition capital matters across different countries and housing systems.

In the US, millennials still believe in the American dream. However, political and media narratives that push the suggestion of just working hard and saving ignore how difficult these strategies may be to take up in the first place. These findings are policy relevant. Those seeking to extend the homeownership ladder further into the younger cohort can look beyond policies that redistribute income or offer housing-related grants and subsidies to include other proposals that might affect financial decisions. For instance, our results suggest student debt relief may positively impact housing outcomes by allowing young people to save for a down payment and enter into homeownership earlier in adulthood. While we are not advocating for financial marketing campaigns (and caution against adopting Horatio Alger style rags-to-riches narratives that moralize perseverance and hard work), we do recognize the possibility that young people have been justifiably scarred by multiple ‘once in a lifetime’ crises, including the Great Financial Crisis. In this context, public discussions around the financial soundness of homeownership may be warranted, especially given the precarious ‘edges’ of homeownership may be sharper and wider than in previous generations. Identifying the various sets of resources, which we include under the umbrella term acquisition capital, moves us towards that discussion.

Supplemental Material

Download PDF (212.1 KB)Supplemental Material

Download PDF (248.7 KB)Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

Notes

1 Parental occupational status, a more traditional measure of parental class (e.g., Köppe, Citation2018), is not available in the SCF data. Parental educational attainment is a close proxy.

2 In 2018, the median age of Black first time homebuyers was 37 years. Therefore, this extended age range is also more likely to include larger samples of non-white households (Wong & Herman, Citation2020, 10).

3 The variance inflation factor for all variables and categories is around the optimal cut-off of 2.5 based on statistician recommendations (Allison, Citation2012) that help ensure low multicollinearity.

4 See (Van Kerm, Citation2017) for more information on mi svy set commands that correct for both imputation and sample variability error.

5 A subsample analysis that proxies whether a household lives in an expensive area (measured as reference persons with earnings more than 50 percent greater than the earnings predicted based on occupational and socio-demographic characteristics (educational attainment, age, and gender, see also Bricker & Thompson, Citation2016)), confirms this point. Results can be obtained from the authors.

6 Authors’ calculations based on data from the Brookings Institute, available at: https://www.brookings.edu/research/housing-in-the-u-s-is-too-expensive-too-cheap-and-just-right-it-depends-on-where-you-live/.

7 Box plots of logged gross housing wealth and housing wealth on its original scale for each racial group visually display this possibility.

8 The gsem option for linear regressions is used to obtain the variance of errors and the standard error of variance to convert logged gross housing wealth back to real values (Huber, n.Citationd).

9 The wider confidence intervals for households at the ninetieth percentile compared to the fiftieth percentile suggests that housing wealth for households at the top of the income spectrum is more variable than for households at the median.

10 For further details on these trends, see Adkins et al. (Citation2020), Horioka & Niimi (Citation2020), Ronald et al. (Citation2018), and Sorensen (Citation2002).

References

- Aalbers, M. B. (2008) The financialization of home and the mortgage market crisis, Competition & Change, 12, pp. 148–166.

- Artle, R. & Varaiya, P. (1978) Life cycle consumption and homeownership, Journal of Economic Theory, 18, pp. 38–58.

- Adkins, L., Cooper, M. & Konigs, M. (2020) The Asset Economy (Cambridge: Polity Press).

- Allison, P. (2012) When can you safely ignore multicollinearity? Statistical Horizons. Available at https://statisticalhorizons.com/multicollinearity/

- Ammerman, D. A. & Stueve, C. (2019) Childhood financial socialization and debt-related financial well-being indicators in adulthood, Journal of Financial Counseling and Planning, 30, pp. 213–230.

- Arundel, R. (2017) Equity inequity: Housing wealth inequality, inter and intra-generational divergences, and the rise of private landlordism, Housing, Theory and Society, 34, pp. 176–200.

- Barakova, I., Bostic, R. W., Calem, P. S. & Wachter, S. M. (2003) Does credit quality matter for homeownership? Journal of Housing Economics, 12, pp. 318–336.

- Barakova, I., Calem, P. S. & Wachter, S. M. (2014) Borrowing constraints during the housing bubble, Journal of Housing Economics, 24, pp. 4–20.

- Bendall, C. (2022) A family affair: The role of intergenerational norm transfer in shaping finances in adult relationships, Journal of Social Welfare and Family Law, 44, pp. 144–168.

- Bhutta, N., Bricker, J., Chang, A. C., Dettling, L. J., Goodman, S., Hsu, J. W., Moore, K. B., Reber, S., Volz, A. H. & Windle, R. A. (2020a) Changes in U.S. Family finances from 2016 to 2019: Evidence from the survey of consumer finances, Changes in U.S. Family Finances from 2016 to 2019: Evidence from the Survey of Consumer Finances, 106, pp. 1–42.

- Bhutta, N., Chang, A. C., Dettling, L. J. & Hsu, J. W. (2020b) Disparities in wealth by race and ethnicity in the 2019 survey of consumer finances, FEDS Notes. Washington: Board of Governors of the Federal Reserve System, September 28, 2020. doi: 10.17016/2380-7172.2797

- Bond, S. A. & Eriksen, M. D. (2021) The role of parents on the home ownership experience of their children: Evidence from the health and retirement study, Real Estate Economics, 49, pp. 433–458.

- Bourdieu, P. (1986) The forms of capital (English version), in J.C. Richardson (Ed) Handbook of Theory and Research for the Sociology of Education, pp. 241–258 (Westport, CT: Greenwood).

- Bricker, J. & Thompson, J. (2016) Does education loan debt influence household financial distress? An assessment using the 2007–2009 survey of consumer finances panel, Contemporary Economic Policy, 34, pp. 660–677.

- Brown, B. & Caldwell, S. (2013) Young student loan borrowers retreat from housing and auto markets. Available at http://libertystreeteconomics.newyorkfed.org/2013/ 04/young-student-loan-borrowers-retreat-from-housing-and-auto-markets.html#.VZRZKk3bKM8 (accessed 15 April 2022).

- Bogardus Drew, R. (2014) Believing in Homeownership: Behavioural Drivers of Housing Tenure Decisions, Working paper no. 14-3. Cambridge: Joint Center for Housing Studies at Harvard University.

- Campbell, J. Y. (2006) Household finance, The Journal of Finance, 61, pp. 1553–1604.

- Cook, J. (2021) Keeping it in the family: Understanding the negotiation of intergenerational transfers for entry into homeownership, Housing Studies, 36, pp. 1193–1211.

- Coulter, R. (2018) Parental background and housing outcomes in young adulthood, Housing Studies, 33, pp. 201–223.

- Crawford, J. & McKee, K. (2018) Hysteresis: Understanding the housing aspirations gap, Sociology, 52, pp. 182–197.

- Crouch, C. (2009) Privatised keynesianism: An unacknowledged policy regime, The British Journal of Politics and International Relations, 11, pp. 382–399.

- Davidson, R. (2012) The emergence of popular personal finance magazines and the risk shift in American society, Media, Culture & Society, 34, pp. 3–20.

- Dewilde, C. & Flynn, L. B. (2021) Post-crisis developments in young adults’ housing wealth, Journal of European Social Policy, 31, pp. 580–596.

- Doling, J. & Ronald, R. (2010) Home ownership and asset-based welfare, Journal of Housing and the Built Environment, 25, pp. 165–173.

- Federal Reserve. (n.d) Standard error calculations. Available at https://www.federalreserve.gov/econres/files/standard_error_documentation.pdf

- Fisher, J. D. M. & Gervais, M. (2011) Why has homeownership fallen among the young?, International Economic Review, 52, pp. 883–912.

- Flynn, L. & Schwartz, H. M. (2017) No exit: Social reproduction in an era of rising income inequality, Politics & Society, 45, pp. 471–503.

- Gibson-Davis, C. M. & Percheski, C. (2018) Children and the elderly: Wealth inequality among america’s dependents, Demography, 55, pp. 1009–1032.

- Guiso, L. & Jappelli, T. (2002) Private transfers, borrowing constraints and the timing of homeownership, Journal of Money, Credit and Banking, 34, pp. 315–339.

- Hackel, E. & Shan, H. (2014) Millennials: The Housing Edition (New York, NY: Goldman Sachs Global Investment Research).

- Hacker, J. S. (2004) Privatizing risk without privatizing the welfare state: The hidden politics of social policy retrenchment in the United States, American Political Science Review, 98, pp. 243–260.

- Haffner, M. E., Ong, R., Smith, S. J. & Wood, G. A. (2017) The edges of home ownership–the borders of sustainability, International Journal of Housing Policy, 17, pp. 169–176.

- Hendershott, P. H., Ong, R., Wood, G. A. & Flatau, P. (2009) Marital history and homeownership: Evidence from Australia, Journal of Housing Economics, 18, pp. 13–24.

- Hira, T. K. (1997) Financial attitudes, beliefs and behaviours: Differences by age, Journal of Consumer Studies and Home Economics, 21, pp. 271–290.

- Huber, C. (n.d) In the spotlight: Interpreting models for log transformed outcomes. Stata News32. Available at https://www.stata.com/stata-news/news34-2/spotlight/ (accessed 2 March 2022).

- Horioka, C. Y. & Niimi, Y. (2020) Was the expansion of housing credit in Japan good or bad? Japan and the World Economy, 53, pp. 100996.

- Kear, M. (2017) Playing the credit score game: Algorithms, ‘positive’ data and the personification of financial objects, Economy and Society, 46, pp. 346–368.

- Kemeny, J. (1980) Home ownership and privatisation, International Journal of Urban and Regional Research, 4, pp. 372–388.

- Köppe, S. & Searle, B. (2017) Housing wealth and welfare over the life course, in: R. Ronald & C. Dewilde (Eds) Housing Wealth and Welfare, pp. 85–107 (Cheltenham: Edward Elgar Publishing).

- Köppe, S. (2018) Passing it on: Inheritance, coresidence and the influence of parental support on homeownership and housing pathways, Housing Studies, 33, pp. 224–246.

- Langley, P. (2008) The Everyday Life of Global Finance: Saving and Borrowing in Anglo- America (Oxford: Oxford University Press).

- Lee, H., Myers, D., Painter, G., Thunell, J. & Zissimopoulos, J. (2020) The role of parental financial assistance in the transition to homeownership by young adults, Journal of Housing Economics, 47, pp. 101597.

- Lee, S. T. & Kim, K. T. (2022) A decomposition analysis of racial/ethnic differences in financial knowledge and overconfidence, Journal of Family and Economic Issues, 43, pp. 815–831.

- Li, S., Li, J. & Ouyang, A. Y. (2017) Housing and Household Wealth Inequality: Evidence from the People’s Republic of China, Working paper no. 671. Tokyo, Japan: Asian Development Bank Institute (ADBI).

- Lux, M., Samec, T., Bartos, V., Sunega, P., Palguta, J., Boumová, I. & Kážmér, L. (2018) Who actually decides? Parental influence on the housing tenure choice of their children, Urban Studies, 55, pp. 406–426.

- Maman, D. & Rosenhek, Z. (2020) Facing future uncertainties and risks through personal finance: Conventions in financial education, Journal of Cultural Economy, 13, pp. 303–317.

- Martin, R. (2002) Financialization of Daily Life (Philadelphia, PA: Temple University Press).

- Martinez, B. & Aja, A. (2021) How race counts for latinx homeownership, Critical Sociology, 47, pp. 993–1011.

- McKee, K. (2012) Young people, homeownership and future welfare, Housing Studies, 27, pp. 853–862.

- Mezza, A., Ringo, D., Sherlund, S. & Sommer, K. (2020) Student loans and homeownership, Journal of Labor Economics, 38, pp. 215–260.

- Mulder, C. H. & Smits, A. (2013) Inter-generational ties, financial transfers, and home-ownership support, Journal of Housing and the Built Environment, 28, pp. 95–112.

- National Association of Realtors. (2021) Profile of home buyers and sellers (Snapshot). Available at https://cdn.nar.realtor/sites/default/files/documents/2021-highlights-from-the-profile-of-home-buyers-and-sellers-11-11-2021.pdf.

- Nielsen, R. B. (2015) SCF Complex Sample Specification for Stata Technical Note (Athens, Georgia: University of Georgia Department of Financial Planning Housing and Consumer Economics). Available at https://www.researchgate.net/publication/291814973_SCF_Complex_Sample_Specification_for_Stata.

- Pierson, P. (2001) New Politics of the Welfare State (Oxford: Oxford University Press).

- Putnam, R. (1993) The prosperous community: Social capital and public life, The American Prospect, 13, pp. 35–42.

- Ong, R., Parkinson, S., Searle, B. A., Smith, S. J. & Wood, G. A. (2013) Channels from housing wealth to consumption, Housing Studies, 28, pp. 1012–1036.

- Ratiu, G. (2021) First time buyers embrace homeownership in challenging 2021 market, Realtor.com. March 25. Available at https://www.realtor.com/research/prospective-first-time-buyers-homeownership-2021 (accessed 15 February 2022).

- Robertson-Rose, L. (2020) ‘Because My father told me to’: Exploratory insights into parental influence on the retirement savings behavior of adult children, Journal of Family and Economic Issues, 41, pp. 364–376.

- Ronald, R., Druta, O. & Godzik, M. (2018) Japan’s urban singles: Negotiating alternatives to family households and standard housing pathways, Urban Geography, 39, pp. 1018–1040.

- Ronald, R. & Lennartz, C. (2018) Housing careers, intergenerational support, and family relations, Housing Studies, 33, pp. 147–159.

- Ronald, R., Lennartz, C. & Kadi, J. (2017) What ever happened to asset-based welfare? Shifting approaches to housing wealth and welfare security, Policy & Politics, 45, pp. 173–193.

- Savage, M. (2015) Social Class in the 21st Century. (London: Penguin UK).

- Shapiro, J. M. (2021) Common Cents: An analysis of financial literacy and socioeconomic mobility in the United States, Master’s Thesis, Georgetown University.

- Shim, S., Barber, B. L., Card, N. A., Xiao, J. J. & Serido, J. (2010) Financial socialization of First-Year college students: The roles of parents, work, and education, Journal of Youth and Adolescence, 39, pp. 1457–1470.

- Smith, S. J., Clark, W. A., Ong Vifor, J, R., Wood, G. A. Lisowski, W. & Truong, N. K. (2022) Housing and economic inequality in the long run: The retreat of owner occupation, Economy and Society, 51, pp. 161–186.

- Sorensen, A. (2002) The Making of Urban Japan: Cities and Planning from Edo to the Twenty-first Century (London: Routledge).

- Squires, G., Lowies, B., Rossini, P. & Mcgreal, S. (2022) Locked out: Generational inequalities of housing tenure and housing type, Property Management, 40, pp. 510–526.

- US Federal Reserve (n.d) About the survey of consumer finances (SCF). Available at https://www.federalreserve.gov/econres/aboutscf.htm (accessed 12 December 2022).

- Ullah, S. & Yusheng, K. (2020) Financial socialization, childhood experiences and financial Well-Being: The mediating role of locus of control, Frontiers in Psychology, 11, pp. 2162.

- van der Zwan, N. (2014) Making sense of financialization, Socio-Economic Review, 12, pp. 99–129.

- Xu, Y., Johnson, C., Bartholomae, S., O’Neill, B. & Gutter, M. S. (2015) Homeownership among millennials: The deferred American dream? Family and Consumer Sciences Research Journal, 44, pp. 201–212.

- Van Kerm, P. (2017) Estimation and inferences for quantiles and indices of inequality and poverty with survey data. 2017 UK Stata Users Group meeting, London, September 7-8, 2017. Available at https://www.stata.com/meeting/uk17/slides/uk17_VanKerm.pdf.

- Ward, S. (1974) Consumer socialization, Journal of Consumer Research, 1, pp. 1–14.

- Webley, P. & Nyhus, E. K. (2006) Parents’ influence on children’s future orientation and saving, Journal of Economic Psychology, 27, pp. 140–164.

- Whitehead, C. & Williams, P. (2017) Changes in the Regulation and Control of Mortgage Markets and Access to Owner-occupation among Younger Households. Working paper no. 196. Paris, France: OECD, Social, Employment and Migration Working Papers, No. 196.

- Williams, R. B. (2017) Wealth privilege and the racial wealth gap: A case study in economic stratification, The Review of Black Political Economy, 44, pp. 303–325.

- Wong, K. & Herman, L. (2020) Market Snapshot: First-time Homebuyers (Washington, DC: Consumer Financial Protection Bureau).

- Wood, G., Parkinson, S., Searle, B. & Smith, S. J. (2013) Motivations for equity borrowing: A welfare-switching effect, Urban Studies, 50, pp. 2588–2607.