Abstract

The regulation of financial markets according to Environmental, Social and Governance (ESG) criteria has become a priority for the European Union (EU). Recent legislation, such as the EU Green Taxonomy, aims to identify sustainable investments enhancing transparency and accountability while steering private finance toward environmental objectives. The introduction of ESG criteria poses specific questions for Social Housing Organisations (SHOs), particularly as the decarbonisation of the housing stock is also incorporated into national legislation. This article contributes to the social housing finance literature by breaking ground on ESG, an area of intensive legislative activity currently re-shaping financial markets. The study draws from interviews with SHOs’ finance directors, banking officers, rating agencies and public officials to answer the question: How does the introduction of ESG legislation affect the financing of social housing decarbonisation? First, the results show that ESG legislation is broadening reporting responsibilities while producing only limited additional finance ultimately geared towards large and commercially oriented SHOs. Second, the expansion of energy-efficiency requirements is resulting in higher costs creating tensions with SHOs’ social mission of building homes at affordable rents. Third, the adoption of ESG financing is producing inequalities in access to capital across national financing systems and individual providers.

1. Introduction

In 2020, Clarion, one of the largest Social Housing Organisations (SHOs) in England, issued a record-breaking 15-year bond resulting in a 1.88% all-in rate. This is among the lowest interest rates that the sector had seen so far in the UK. Although English SHOs have become forerunners at raising private finance in capital markets since the adoption of the 1988 Housing Act (Whitehead, Citation1999), Clarion’s bond was among the first underlined by adherence to non-financial indicators including high energy efficiency standards in new construction. According to Clarion’s press release, the demand for the bond was strengthened by the SHO’s accreditation as a Certified Sustainable Housing Label, an accreditation on corporate level for demonstrating Environmental Social and Governance (ESG) credentials. The label is issued by Ritterwald, a pan-European consultancy firm (Clarion, Citation2020).

Over the last decades, ESG debt issuance, through green, social or sustainability-linked loans and bonds has become increasingly common. Financial markets have hailed the adoption of ESG indicators as a tool to align capital investments with environmental and social goals, such as the decarbonisation of the social housing stock. According to the Climate Bonds Initiative (CBI), the green debt market has experienced a 50% growth over the last five years (CBI, Citation2021). However, the lack of clearly established indicators and objectives has tainted the growth of green finance with a series of high-level scandals and accusations of green-washing, unjustified claims of a company’s green credentials. For example, a fraud investigation by German prosecutors into Deutsche Bank’s asset manager, DWS, has found that ESG factors were not taken into account in a large number of investments despite this being stated in the fund’s prospectus (Reuters, Citation2022).

To curb greenwashing and improve transparency and accountability in green investments, the EU has embarked on an ambitious legislative agenda. This includes the first classification of environmentally sustainable economic activities: the EU Green Taxonomy (Regulation 2020/852). When it comes to real estate, the accompanying Delegated Act (Regulation 2021/2139) introduced very specific criteria for green investments. New buildings should improve over national Nearly-Zero-Energy Buildings (NZEB) standards by reducing energy consumption a further 10% (Regulation 2021/2139). Regarding decarbonisation, the Taxonomy requires undertaking ‘major renovations’ as defined in the Energy Performance of Buildings Directive (EPBD) (COM(2021)) or reducing energy consumption for the final user by at least 30%. The Taxonomy is directly linked to the European Commission’s decarbonisation strategy, the Renovation Wave (COM(2020) 662), which relies on a combination of private and public finance to deliver the investment needed for the decarbonisation of social housing. Energy efficiency targets have become increasingly stringent as the EPBD and its successive recasts (COM(2021)) have been incorporated into national legislation; see for example the French Loi Climate et Resilience (2021-1104, 2021). Consequently, capital expenses for SHOs are set to increase considerably. For example, in the Netherlands, according to a Housing Europe (Citation2020) report, attaining the 2035 energy efficiency targets set by the Dutch government will cost €116bn. Sustainable finance legislation constitutes an expansion of the financial measures implemented by the EU in the last decades to incentivise energy efficiency standards and renovations in the built environment, see Economidou et al. (Citation2020) and and Bertoldi et al. (Citation2021) for more detail on prior EU policies. It is because of the increased ties between finance and energy performance that the shift toward ESG poses particular questions for SHOs’ access to capital markets.

The rapidly expanding finance literature on green bonds draws from econometric models to explore the links between investors’ preferences and yields (Fama & French, Citation2007). This body of literature on asset pricing relies on the introduction of non-pecuniary preferences in investors’ utility functions together with returns and risks to explain fluctuations in the equilibrium price of capital. Drawing from a comparison between green and conventional bonds, Hachenberg and Schiereck (Citation2018) find evidence of the former being priced at a premium. Similarly, Zerbib (Citation2019) also shows a low but significant negative yield premium for green bonds resulting from both investors’ environmental preferences and lower risk levels. The European Commission’s Joint Research Centre (Fatica & Panzica, Citation2021) documents the dependency of premiums on the issuer with significant estimates for supranational institutions and corporations, but not for financial institutions. While these econometric approaches offer relevant insight into the pricing of green bonds and the incentives for issuers and investors, they do not account for the institutional particularities of social housing, a highly regulated sector usually covered by varying forms of state guarantees and subsidisation (Lawson, Citation2013).

In the authors’ understanding, this is the first article to approach the growing significance of ESG finance in social rental housing through a comparative approach across a set of North-Western European countries. A dedicated study of SHOs’ finances and ESG in this region is particularly apposite since SHOs are responsible for the renovation and maintenance of vast swathes of the existing housing stock (OECD, Citation2020). This article draws from semi-structured interviews with finance directors, banking officers, rating agencies and public officials to answer the question: How does the introduction of ESG legislation affect the financing of social rental housing decarbonisation?

In the following section, this paper introduces the current legislative changes on ESG at the EU level. The next section briefly covers some methodological aspects of policy comparison and discusses the data collection approach. The fourth section constitutes the central empirical analysis and is structured around four research sub questions answered through a literature study and a qualitative data analysis. The fifth section discusses the findings positioning them within the existing literature. Finally, the sixth section concludes, offers policy recommendations and introduces questions for future research.

2. Policy background: ESG and decarbonisation

Throughout the last two decades, the term ESG finance has evolved to include a large number of financial vehicles of which green bonds have become the most popular (Cortellini & Panetta, Citation2021). In the social housing sector, ESG comprises a broad array of tools from sustainability-linked loans to less conventional forms of finance such as carbon credits.Footnote1 When it comes to bonds, there is a wide variation in the sustainability credentials among the different types. Broadly speaking, green and social bonds are issued under specific ‘use of proceeds’, which means the funds raised must be used to finance projects producing clear environmental or social benefits. Issuance of these types of bond requires a sustainable finance framework which is usually assessed by a third party emitting an opinion on its robustness. Sustainability-linked bonds (SLBs) are an alternative to ‘use of proceeds’. Funds raised in this manner are not earmarked for sustainable projects, but can be used for general purposes. SLBs are linked to the attainment of certain company-wide Key Performance Indicators (KPIs), for example an average EPC-C in an SHO’s housing stock. These indicators and objectives usually result in a price premium for Sustainable Bonds, or a rebate in interest rates in the case of SLBs or sustainability-linked loans (SLLs) (Cortellini & Panetta, Citation2021).

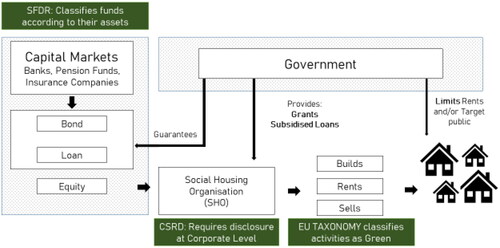

While there are international standards for the categorisation of green projects such as the Green Bond Principle or the Climate Bonds Strategy, strict adherence is optional and there are few legally-binding requirements resulting in a large divergence in reporting practices and external auditing. To solve these issues and prevent greenwashing, the EU has been the first regulator to embark in the formulation of a legal basis for green finance through a series of acts targeting the labelling of economic activities, investors, corporations and financial vehicles. First, the EU Green Taxonomy (Regulation (EU) 2020/852) is the cornerstone of this new legislation since it classifies economic activities attending to their alignment with the objectives set in the European Green Deal (EGD). When it comes to housing, as presented in the introduction, the EU Taxonomy requires specific energy efficiency levels for a project to be deemed ‘taxonomy aligned’. Second, the Sustainable Finance Disclosure Regulation (SFDR) (Regulation (EU) 2019/2088) mandates ESG reporting on funds, which tend to consist of exchange-traded collections of real assets, bonds or stocks. Funds are required to self-classify under article 6 with no sustainability scope, ‘light green’ article 8 which incorporates some sustainability elements, and article 9 ‘dark green’ for funds only investing in sustainability objectives. Under the SFDR, which entered into effect in January 2023, fund managers are required to report the proportion of energy inefficient real estate assets as calculated by a specific formula taking into account the proportion of ‘nearly zero-energy building (NZEB)’, ‘primary energy demand (PED)’ and ‘energy performance certificate (EPC)’ (Conrads, Citation2022). Third, the Corporate Sustainability Reporting Directive (CSRD)(COM(2021) 189) increases disclosure requirements for corporations along Taxonomy lines. Also entering into effect in 2023, the CSRD will be progressively rolled out starting from larger and listed companies, expanding throughout this decade. Provisions have been made for charities and non-profits to be exempted. However, one of the key consequences of disclosure requirements over funds through the SFDR is its waterfall effect; that is the imposition of indirect reporting requirements as investors pass-on their reporting responsibilities to their borrowers. Fourth, the proposed EU Green Bonds Standards (EU-GBS) COM(2021) 391 aims to gear bond proceedings toward Taxonomy-aligned projects and increase transparency through detailed reporting and external reviewing by auditors certified by the European Security Markets Authorities (ESMA). The main objectives of these legislative changes is to create additionality, that is, steer new finance into green activities (see ).

Figure 1. Impact of ESG legislation, approved at the time of the interviews, on social housing financing.

While this new legislation is poised to increase accountability and transparency, it also aims to encourage a better management of environmental risks. According to a recent report on banking supervision by the European Central Bank (ECB), real estate is one of the major sources of risk exposure for the financial sector (ECB, Citation2022). This includes both physical risks, those resulting from flooding or drought and, more relevant in this case, transitional risks, that is those derived from changes in legislation such as the EPBD and transposing national legislation. The ECB points to the need for a better understanding of risk transmission channels from real estate portfolios into the financial sector through enhanced data collection and better assessments of energy efficiency, renovation costs and investing capacity. At its most extreme, non-compliance with EU regulations could result in premature devaluation and stranded assets (ECB, Citation2022).

The introduction of reporting and oversight mechanisms connects legislation on housing’s built fabric, namely the EPBD, to financial circuits. On the one hand, the EU has been strengthening its requirements vis-à-vis energy efficiency over the last decades. The Energy Efficiency Directive (EED) suggested the introduction of Minimum Energy Performance Standards (MEPS) by member states (Economidou et al., Citation2020), a rationale followed by France and the Netherlands for certain parts of the housing stock. Furthermore, at the time of writing, it is being debated whether the EPBD’s recast (COM/2021/802) may incorporate MEPS making decarbonisation an obligation for SHOs across the EU. On the other hand, legislation on green finance aims to produce incentives and oversight over investments in energy efficient renovation and new build, mobilising the private sector to cater to green projects (Renovation Wave (COM(2020) 662)). This paper aims to identify and assess the changes that the introduction of ESG indicators is having on SHO finance by answering the following research sub questions:

What are the main underlying differences between social housing financing systems in Europe?

How are reporting and disclosure obligations affecting SHOs’ access to capital markets and ultimate borrowing costs?

How are renovation requirements and MEPS impacting SHOs’ social objectives?

How are national SHO management practices and organisation characteristics interacting with “greening” capital markets?

3. Methodology

Across North-Western Europe, SHOs are usually heavily regulated through rent-setting policies and governance standards. SHOs also have a long history of strong financial ties to the state, through public funds and grants, for instance Haffner et al. (Citation2009). As a result, the capacity of ESG finance to produce additional investment and affect the cost of capital in the sector is deeply contingent on country-based institutional arrangements. While the comparative study of social housing finance from a social policy perspective is a well-researched topic, for instance OECD (Citation2020), the exploration of bond finance in social housing has only been the focus of a few country-based studies; for example Wainwright and Manville (Citation2017) in England. The literature on social housing green bonds is even more scarce and, as far as the literature review has shown, limited to Mangold and Mjörnell (Citation2022) for the Swedish case.

To explore ESG financing for social housing, this paper develops a qualitative approach inscribed in the housing studies literature to account for the particularities that differentiate social housing financing across national borders. Conceptually, it draws from a body of literature operating at the intersection between particularistic and universalist approaches. On the one hand, the particularistic view contends that housing phenomena can only be interpreted within the context of individual countries. In this vein, Ruonavaara (Citation1993) argues that, for example, tenure should be seen both as ideal types and specific geographical and historical forms. On the other hand, the convergence or universalistic approach, as developed for example by Kleniewski and Harloe (Citation1996) or Boelhouwer and Van der Heijden (Citation1992), emphasises the translation of housing categories across contexts.

In dealing with particularistic and universalistic methodological differences, Haffner et al. (Citation2010) compare the private rental sector from both perspectives and arrive at a compromise middle way that takes into account commensurability while cautioning for a contextual use of theory. More recently, Aalbers (Citation2022) proposes focusing on ‘common trajectories’. He argues for a focus on uneven development together with interdependencies between convergent or homogenising and, divergent or, heterogenising forces. As opposed to classification under ideal types, discussed above, this approach focuses on the dynamic forces at the intersection of state, finance and real estate shaping housing provision. Aalbers (Citation2017) has also emphasised how changes in housing finance do not unfold coherently across widely heterogenous housing systems but through the production of tensions and contradictions.

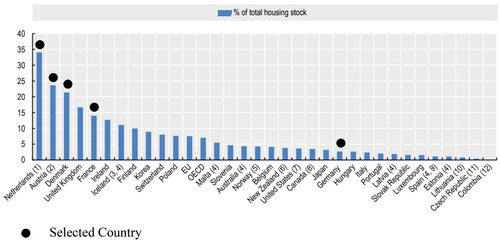

Drawing on Aalbers (Citation2022), this paper analyses the heterogeneising and homogenising forces shaping social housing financing as a consequence of ESG-related legislative changes. As a result, rather than generating a comprehensive classification, the research is focused on key regulatory changes and their impact on social housing financing landscapes. The policy background in Section 2 has identified three main homogenising forces resulting from the shift towards ESG finance: (1) reporting and disclosure obligations (2) renovation requirements and MEPS (3) “greening” of capital markets. While departing from the description of current SHO financing systems, this study focuses on identifying forces emanating from EU legislation that reshape these financing systems. The main objective is to account for the national particularities playing a role in explaining the varying degrees of incorporation of ESG into social housing finance. To answer the first research sub question, this paper analyses the existing literature on national social housing financing systems. Then, the qualitative approach consisted of thirty three in-depth semi-structured interviews across five European countries with large social rental housing stocks: France, the Netherlands, Denmark, Austria and GermanyFootnote2 ().

Figure 2. Relative size of the social rental stock in Europe. Source: OECD Figure PH4.2.1.

The selection of interview participants attended to saliency in two criteria. The first was organisation size, since mid to large SHOs tend to access capital from multiple sources to fulfil their complex financial needs. Second, in an attempt to control for SHO’s legal status, participant selection also considered organisation’s objectives (public/private; for-profit/limited profit) based on the specific regulations of each country. Initially, the interviews were geared towards SHO’s treasury and sustainability managers. However, complex SHO’s financing structures reliant on guarantees and subsidisation have resulted in the inclusion of credit rating agencies, public and private banks as well as public administration officials depending on the country in question (see ). While the interview protocol was adapted ad hoc to the national context and type of agent, the questions covered the following topics: (1) business-as-usual, main investors and sources of finance, (2) role of ESG finance (bonds, loans) and reporting obligations, (3) financing renovation and energy efficiency requirements, and (4) risks, challenges and recommendations. Interviews were conducted between October 2022 and February 2023, mostly online but also in person at different Brussels locations. The interviews were recorded and the data gathered was coded in ATLAS.ti. Answers to research sub questions 2, 3 and 4 emerged from this coding process as the overarching themes structuring the cleavages across country and SHO lines (see Appendix A and B for methodological detail).

Table 1. Breakdown of interviewees by sector and country.

This qualitative approach complements that of the quantitative literature presented in the introduction. Instead of focusing on the identification of a green premium, the rationale behind ESG uptake through the institutional particularities identified in the literature and the first-hand experience of those involved in SHO debt issuance are explored. This approach aims to overcome the limitations of different green standards for debt-issuance together with current volatility in financial markets. These different standards overlapping over time complicate comparisons between regular and ESG bonds within the social housing sector. Even though this study draws on a substantial sample of interviewees and covers key stakeholders across SHOs of various sizes and financial situations, limitations inherent to qualitative research apply. For instance, while the questionnaire included discussions about the pricing of green and traditional capital, these findings are interpreted in dialogue with quantitative evidence.

4. ESG finance and the decarbonisation of the social housing stock

4.1. What are the main underlying differences between social housing financing systems in Europe?

This section draws from academic literature to identify the main features of the selected social housing financing systems. First, iin the Netherlands, the transition from a government-provided grant to a guarantee fund [Waarborgfonds Sociale Woningbouw] (WSW) has pushed Dutch SHOs towards raising debt in capital markets (Boelhouwer, Citation1997). In its most extreme cases, liberalisation resulting from the end of government grant subsidisation allowed SHOs to undertake riskier operations, namely speculation with derivatives. In 2011, the resulting losses amounted to €2.1bn for the largest social landlord, Vestia, which had to be covered by the WSW and ultimately Dutch SHOs (Elsinga & Wassenberg, Citation2014). Eventually, this proved the strength of the guarantee system which allows Dutch SHOs to borrow at a very low spread over sovereign issuanceFootnote3 with their debt rated triple AAA, as that of the Dutch state (S&P, Citation2022). Currently, most of the financing of SHOs comes from two public promotional banks, Dutch Local Authorities’ Bank [Bank Nederlandse Gemeenten] (BNG) and Dutch Water Authorities Bank [De Nederlandse Waterschapsbank] (NWB), which lend on their own bond proceedings to SHOs (BNG Bank, Citation2021; NWB Bank, Citation2021).

Germany followed a similar path to the Netherlands in which direct subsidies, used to lower the costs for tenants in both social and private renting, have been substituted by lower interest and subsidized loans by the public Bank for Reconstruction [Kreditanstalt für Wiederaufbau] (KfW) (Droste & Knorr-Siedow, Citation2014). However, these subsidies are temporary and result in the conversion of subsidised housing into private market units once the loans are fully repaid, particularly in the case of for-profit landlords. However, a number of SHOs, either publicly owned by municipalities and regions or charitable institutions, retain lower rents after the end of the subsidy period (Haffner, Citation2021). The concession system of German subsidies results in a very low proportion of social housing despite the existence of a large below-market rental stock in the hands of landlords with varying profit motivations (Kofner, Citation2017). Together with loans, larger SHOs have started to tap onto capital markets directly through bonds such as the one presented in the introduction.

The French social housing system is managed by a mix of Public Offices owned by local authorities and privately-run charitable housing companies. The state regulates their rents which are linked to the financing provided by the Caisse des Dépôts et Consignations (CDC), a public bank. Their long-term debt is usually guaranteed by local authorities or by the Mutual Fund for Guarantees of Rental Social Housing (Caisse de Garantie du Logement Locatif Social; CGLLS) (Schaefer, Citation2003). New construction is financed to a high percentage through different sets of loans issued by the CDC, with varying levels of subsidisation depending on the income of the targeted household (Tutin & Vorms, Citation2016). The remaining funding needs are covered by market loans and bonds, local authority equity and grants (Lévy-Vroelant et al., Citation2014).

The Austrian system is based on a combination of state subsidies and cost-based rents. This rent-setting strategy allows SHOs to recover the costs without adding a profit and jeopardizing housing affordability (Mundt & Springler, Citation2016). As a result, a revolving fund is created once the original loans are repaid, which facilitates constant reinvestment into new projects and maintenance by SHOs with remarkably high levels of own-equity. This system is backed by a set of low-interest public loans and to a lesser extent on grants implemented by the regional level of government (Kadi & Lilius, Citation2022; Kössl, Citation2022). Austrian SHOs strongly intertwine the state and the banking system through subsidization and de-risking allowing for a steady flow of capital from private banks and European sources such as the European Investment Bank (EIB) (Citation2019).

Similarly, one of the key features of the Danish social housing system is the National Building Fund (LBF), [Landsbyggefonden]. LBF is financed by tenants’ contributions after the main mortgage loan of a property is repaid. LBF’s main mission is to mitigate the individual risks of SHOs offering loans and subsidies to SHOs undertaking renovations or new build projects (Blackwell & Bengtsson, Citation2023). As in the Netherlands, social housing financing has also shifted from public subsidies toward market loans (Norris & Byrne, Citation2021). However, these loans are framed within the heavily regulated Danish mortgage-bond market system [realkredit(-lignende) lan]. Since 2017, these bonds are issued through government financed guarantees (Lunde & Whitehead, Citation2016). This is beneficial to both the mortgage institutes, the bond issuers, since these bonds are exempt from capital requirements; and the housing providers since they access capital at a premium as investors are willing to pay more for government securities. The national bank acquires the securities issued in this way (Bindslev, Citation2018).

Summarising, to varying extents, these countries implement different forms of state backing or mutual sector guarantees that allow SHOs to tap into the private sector finance at advantageous rates (see ). A comparative study by Lawson (Citation2013) including France and the Netherlands, shows how these guarantees not only play a compliance and overseeing role, but are also key in de-risking and directing investment to SHOs at lower interests. Similarly, Whitehead (Citation2014) highlights the strengthened role of private debt finance across a majority of European countries in the last decades. Noticeably, while bricks and mortar subsidies have been substituted by interest subsidies and loans to a certain extent across most countries, Austria and Denmark have retained revolving models which allow for the reinvestment of limited profits within the social housing sector (Scanlon et al., Citation2015).

Table 2. Summary social housing financing features.

4.2. How are reporting and disclosure statement obligations affecting SHOs’ access to capital markets and ultimate borrowing costs?

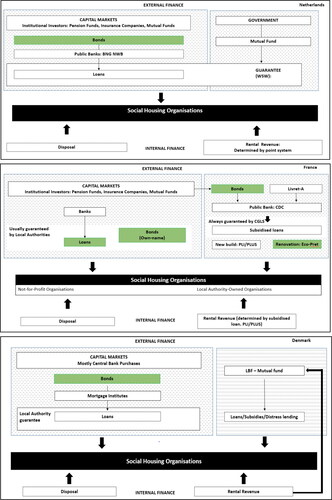

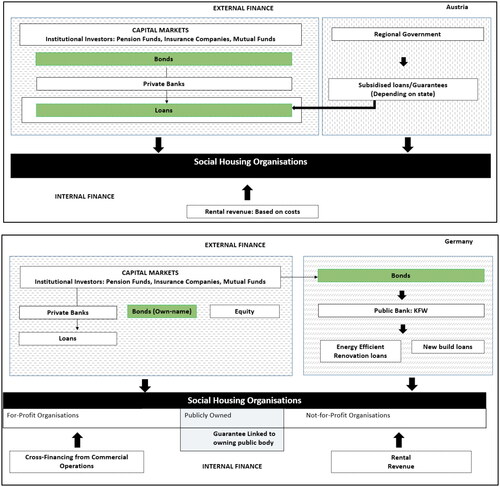

Environmental disclosure obligations are a key feature of ESG frameworks and they aim to lower capital costs for activities aligned with environmental objectives, as presented in section two. However, through grant funding and guarantees SHOs already have access to very low interest rate debt in most countries, particularly in France, The Netherlands, Denmark and Austria, as shows in detail.

Figure 3. Greening of social housing finance by country. Source: Prepared by authors.

The margin for the bank is EURIBOR plus 1.5 or 2% or swap rate + 1.5. If you have a fixed long term fixed loan, it’s a swap rate plus one 1.4 to 2%. In our sector, we are between the indicator plus 0.6 to maximum 1%, so our interest rates are between 0.5 and 1% lower than the rest, but already before ESG. This is coming out of the high equity portion and the low rent as we have no profit in the rent and if we have a cost-based system our rents are around 30% lower than market rents. By these lower rents, we have no problem of renting out [homes] because anyway people come to us. (CEO, large SHO, Austria)

Despite the lack of grants, the funding of Dutch SHOs presents similar characteristics to that of their Austrian counterparts through a state guarantee by the WSW. As a result, the greening of funding streams has a limited impact on SHOs’ capital costs since these are already covered by the state guarantee, while Austrian SHOs have access to grants resulting in highly-rated debt.

Investors like to invest in banks with green assets, green loans and products like that. The combination [SFDR & Taxonomy] formalizes this process (…). It’s more reporting what you do, but it doesn’t make a difference [in financing]. (…) I think that’s reverse causality there [between ESG and reporting]. (Finance expert, sector organisation, The Netherlands)

These two testimonies raise questions on the additional value of greening existing funding sources and where additionality actually accrues: whether it is at the SHO, or the fund manager. A Dutch public bank already issuing social and sustainability bonds, see -NL, also questioned the relevance of ESG granular reporting following the taxonomy indicators:

How big is the reward for the punishment? I mean, in our market we have two public sector agencies, (…) and we are very much in competition on the lending side. So all our clients, they ask both of us a quote and then it really can be up to half a basis point difference. So when you look at sustainability linked, then you can say, well, maybe you should have a reward like 20 or 25 base points to make it substantial [green premium], but now I still think we have one or two [bps]. (Bonds expert, public bank, The Netherlands)

When we issued the bond, we got 10 basis point greenium. (…) We’ve issued more than 4 billion in green and social format. As a proxy, let’s say 5 basis points of benefit, ‘greenium’. That means annual savings of about 2 million. (Head of Treasury, large SHO, Germany)

At the moment, [Green Issuance] is not the way to get the cheap money and to provide it to social housing […] When the first SFDR Reports are published, I think that this will be a new step for further input that could be traced in the funding. (Lending officer, bank, Austria)

4.3. How are renovation requirements and MEPS impacting SHOs’ social objectives?

The introduction of enhanced energy performance requirements at both EU and national level is steering providers towards environmental objectives. However, increased leveraging for renovation is reducing the available resources to deliver on other social priorities.

[SHOs] have to renovate their G dwellings right to be able to rent them out and this drives their CapEx Plans. The main ratio that we look at when we rate them is the net debt to EBIDTA ratio. In that, you have the CapEx included because they have to borrow for renovating their dwellings. (Associate Director, credit rating agency, France)

Credit risk indicators, such as net debt to EBIDTA,Footnote4 measure leverage against assets and revenue and result in variations in capital costs. As energy efficiency requirements are engrained into national frameworks, SHOs on a less solid financial situation are having to renegotiate their debt. Although SHOs operate in a highly regulated environment with different forms of state-backing, their borrowing remains constrained by financial risk ratios occasionally leading to refinancing operations. As improving energy efficiency in the housing stock becomes a sine-qua non criterion to access funding and decarbonisation deadlines are rolled out, SHOs have to compromise on other fronts. In the interviews, the most commonly raised trade-off has been new construction, as is confirmed by Housing Europe (Citation2020). ESG finance, through the introduction of environmental reporting criteria for investors, is strengthening the centrality of renovation in SHOs financial plans.

Depending on national rules around rent-setting, renovation requirements produce split incentives, where SHOs have a new financial obligation without the expectation of return, as highlighted by rating agencies. The subsequent cost increase is compensated in some cases by rent increases or the introduction of ‘warm rents’ which allow SHOs to recoup their investment in renovation and partially circumvent the split incentives problem through rent rises.

In the Netherlands, different types of fees have been proposed to incorporate renovation costs into rents after deep renovations (van Hal et al., Citation2019). In France, SHOs use a particular form of ‘warm rent’ called 3rd receipt line [3ème ligne de quittance]: ‘We do a 3rd receipt line by telling tenants we’re going to isolate your building from the exterior. In exchange, you will have lower heating costs and conversely we ask you to pay more in rent’ (in French in the original). However, differences by provider apply. Another French provider implements a continuous rent raising strategy to the legal maximum and highlights the need to balance renovation operations not at the level of building but at the level of the operator through cross-financing of internal resources, see also Joint Research Centre (2014) for a review of policies targeting split incentives. In Germany, renovation can lead to rent increases since after 30 years social housing can be reverted to market rates and rent remains controlled just through the national legislation.

The last 20% of [energy] savings cost more than the first 80%. So for the last 20% if you go for that, you would have to increase the rent that much. That’s not affordable housing and you would have to kick out your tenants. So that makes it [full energy neutrality] wishful thinking. (Director, Sector Organisation, Germany)

Even in these instances, prior research has shown that recouping investments through rent rises may not be financially sound, as green premiums fail to compensate renovation costs (Galvin, Citation2023) Depending on the national context, decarbonisation pressures and energy efficiency requirements are producing a trade-off decision between renovation, new construction and affordability. These trade-offs, while taking place at SHO level are not only contingent on company finances, but have different implications across national financing systems. In Austria, state intervention has reduced the financial burden on SHOs through public subsidies combined with upper rent limits. Here, strong state intervention comes to join a particular favourable situation since renovation is already anticipated in cost-based rent setting.

The upper limit of the rent which they [SHOs] can ask when the subsidy is still going out is fixed. They can’t go over this upper limit of rent. The kind of deal we have is, that we as a state give them money to renovate their buildings and achieve a certain level of energy efficiency. And what we get back as a state is, on the one hand, climate protection and, on the other hand, affordable rents. (Director, regional authority, Austria)

Ultimately, SHOs are having to balance out energy efficiency and new build investments as these are the two main components of their leverage ratios together with rental income. According to the ECB (Citation2022), decarbonisation costs are a key transitional risk for real estate asset holders as these impinge on values. The EPBD, through renovation requirements, and the ESG legislation, through disclosure obligations, are embedding the transitional risks derived from decarbonisation obligations into SHOs capital expenditure plans. State guarantees and redistributive mechanisms, depending on the country, mitigate the transitional risks derived from changes in asset valuation resulting from renovation requirements.

We have this guarantee and it doesn’t really matter how high is the risk profile for a corporation or how green it is. At this moment, it doesn’t really matter because you have the guarantee and using the guarantee the BNG and NWB will give you funds immediately and other banks too. (Finance expert, sector organisation, The Netherlands)

In the Netherlands, it is common practice by rating agencies to rate SHO’s debt top-down, that is starting from the rate of the guarantor, ultimately the Dutch state, currently rated AAA. Similarly, an interviewee from a French public bank highlighted how interest is not determined based on the credit risk of the borrower, but on the energy efficiency and rent ambition of the project. In France and the Netherlands, state-backed operators are shielded from transitional risks. Despite this state guarantee, some of the interviewees raised concerns about guarantee coverage for SHOs with non-energy-efficiency assets in the future (see for cross-country details).

One of the interviewed consultants highlighted that, over the long run, the possibility of stranded assets due to chronic shortcomings in renovation poses risks for further deterioration of leverage ratios. Although this is unlikely to jeopardise access to capital for the sector, it may put increased pressure on individual organisations which are already reducing development activities and in some cases increasing rents. The ESG focus on environmental criteria, together with MEPS, pose the risk of stranding assets and are steering SHOs toward renovation investments. As a result, unless there is substantial non-market financing, SHOs are reducing their development pipelines and increasing rents where possible.

4.4. How are national management practices and organisation characteristics interacting with “greening” capital markets?

As presented in section two, the use of sustainability indicators, as introduced by the EU’s Sustainable Finance Framework, has the objective of identifying management activities and companies delivering on ESG priorities and steering capital markets towards them. However, our findings show that particular management practices and institutions make certain SHOs and countries more suitable to ESG finance. On the one hand, SHOs in the Netherlands raise finance on a portfolio basis that is finance their operations in bulk. In the other studied countries, SHOs tend to raise capital for specific projects. The EU’s legislation “greening” capital markets introduces granular disclosure at project level which poses administrative difficulties for Dutch SHOs and their funders:

We have what they call a balance financing […] and that makes it hard to report on an individual loan. (…) Our data, the impact reporting, is done by the umbrella organization of the social housing organizations, AEDES. (Finance expert, promotional bank, Netherlands)

Among the institutional investors, so all central banks, insurance company, asset managers that are really dedicated to invest in ESG project. [French Public Bank] is really flagged as an exemplary issuer. And it’s enabled us to in fact, accelerate the evolution of the market to accompany the transition also on the market side to encourage new issuers to enter in the market and to accelerate the building of new standards (Finance expert, promotional bank, France).

We’re also trying now to make some kind of a green labelling because many of these bonds, they are attached to buildings with a high energy efficiency. And we have all kind of registration and retaining system. We know who lives in our buildings, know how old they are and we know everything about them.[…] So just like that we can make a connexion between the energy efficiency of the building and the bond. (CEO, large SHO, Denmark)

So as soon as we get the money of the state […], it’s a proof that every regulation is really uphold and stated and for that reason the bank doesn’t ask anymore detailed questions to our company (CEO, large SHO, Austria)

So all Austrian non-profit housing associations have very strict criteria to fulfil regarding the new building. So if they want the a state funding they have to fulfil these criteria which are really like the Taxonomy criteria now. For them it’s really no problem to fulfill them, and just one sentence regarding the funding from state or public entities is enough. (Lending officer, bank, Austria)

We tried to prepare green bonds for housing associations, but they are not gonna meet the requirements because if you look to their housing stock, that’s what we call legacy housing stock. So that’s an aging housing stock with overall quite poor EPC ratings. And nowadays they say well, we are on an average of EPC-C, yeah, but C, I mean thumbs up, but that’s half your way. You can have a very complicated story about green bonds, but there is one simple reason. Housing associations, which have an ageing housing stock, simply cannot comply with the green bond principles [Taxonomy] and for instance, if you are in the UK, if you are a for-profit registered provider [SHO] of affordable housing and you have been able to build your portfolio from scratch, (….) you are already pretty close on meeting your green bond standard (Finance expert, consultancy, Europe)

5. Discussion

ESG legislation has triggered a series of forces that are reconfiguring social housing financing systems. Despite strong differences across national financing frameworks, this paper has identified three major homogenising forces: (1) reporting obligations, (2) renovation requirements and (3) “greening” of capital markets (see ). Within these homogenising forces, this study’s findings for five EU-countries evidence contradictory outcomes produced by the reorganisation of SHO financing along ESG lines. First, ESG legislation is expanding reporting responsibilities, while producing only limited additional finance ultimately reducing interest rates (Contradiction 1). According to the interviewees, ESG reporting is not always conducive to a lower cost of capital. Guarantees, revolving funds and strong equity are some of the factors preventing the materialisation of a lower interest rate that are explored at country level below. Second, the expansion of energy efficiency requirements increases capital expenditures creating tensions with SHOs’ social mission of providing new affordable homes (Contradiction 2). ESG together with legislation on energy efficiency accentuates the importance of housing decarbonisation as both a financial risk and a new standard. This has a direct impact on SHOs’ financing since their capacity to recoup investment is usually limited by rent caps. Notwithstanding wide differences across providers and countries, renovation requirements produce tensions with SHOs’ social mission as the differences impinge on the SHO’s capacity to maintain lower rents and build more homes. Third, instead of producing widespread easier access to debt, the reconfiguration of capital markets along ESG criteria favours particular social housing provision systems, with either strong government support or larger commercial providers (Contradiction 3). This comes about because ESG legislation intends to clearly label funds and bonds to increase transparency in the allocation of capital to aligned projects. However, practices such as portfolio financing and factors such as company size and data availability condition SHOs’ capacity to access “green” investments. This results in an uneven playing field where larger, more commercially oriented SHOs in particular countries are better suited to “green” investments.

Table 3. Overview of forces, effects and contradictions.

The three contractions therefore show that the common intended trajectories do not materialise equally across the different social housing financing systems. Following Aalbers (Citation2017), the tensions between homogeneising and heterogeneising forces result in variegation across national social housing financing systems (see ). The first contradiction mainly results from the existence of strong guarantees and public intermediaries which reduce the margin on which ESG reporting can produce further price differentiation. Countries with these features rely heavily on public promotional banks, as in The Netherlands and France and to a certain extent Denmark and Austria, where state backing takes the form of sizeable grants and bond-purchases (see also ). In these cases, greening social housing financing produces, for now, low green premiums. Quantitative evidence on sovereign debt issuance backs these views, as the econometric analysis by Doronzo et al. (Citation2021) also found little evidence of premiums being related to ESG public debt issuance. In contrast with the lack of interest rate incentives in Germany, which tends to have more commercially geared SHOs, the adoption of ESG debt instruments is driven more directly by reductions in the cost of debt. In summary, the introduction of homogenising ESG reporting standards is having a differentiated impact producing divisions across social housing financing systems. Ultimately, interest rate rebates are not perceived as the main driving force toward green debt for a majority of the interviewees but more as a cultural shift toward the engraining of environmental indicators in lending. While ESG certifications broaden the investor base and make SHOs more “legible” to investors, it is only in those systems that are more dependent on private finance that ESG disclosures produce higher green premiums.

Table 4. Contradictions, heterogeneising and homogeneising forces.

The second contradiction of higher finance costs jeopardising SHOs’ social mission is a consequence of renovation requirements, a homogenising force (see ). Renovation requirements affect the capital expenditures of organisations differently depending on whether these rely on grant or debt funding. Grants result in lower leverage ratios which strengthen the risk profile of SHOs in the eyes of rating agencies, for example in Austria (see also ). In ‘guarantee’ countries, where SHOs have strong linkages to the sovereign, rating is done top-down, which shields them from environmental risks: de-risking their borrowing. This phenomenon offers similarities with the de-risking of for-profit real estate portfolios through state intervention analysed by Aalbers et al. (Citation2023). However, in the case of limited profit SHOs, leveraging limits are constraining those in more financially fragile situations, despite the state-backing. Guarantee-providers, key actors in state backing, are still discussing how to incorporate environmental and transitional risks in the analysis of SHOs to mitigate the impact it may carry on their access to debt. In response to renovation requirements impinging on costs and increasing borrowing, most of the interviewed SHOs are reducing their new-build pipelines, passing on costs to residents where the rent-setting system allows it and also considering disposing of their less energy efficient stock. On a similar note to that of Knuth (Citation2016), the emphasis on environmental indicators disregards the social objectives in SHOs activities. Austria and Denmark operate more independently from financial markets because of the provision for renovation having been included in rent-setting and the existence of revolving funds (see ). As also highlighted by the literature (Kössl, Citation2022), cost-based rent setting is one of the key features which allows the renewable renovation and new social production in Austria together with high levels of government grant.

The third contradiction results from the uneven impact greening capital markets are having over providers in the studied countries. Both decarbonisation and ESG debt issuance reward economies of scale, underlining the role of aggregators and banks. As reporting of use of proceeds becomes more detailed, ‘project’ finance countries have an advantage over ‘portfolio/balance’ ones. However, SHOs are not only passive actors in financial systems, and the incorporation of transitional risk indicators into banking is producing positive effects in some countries. For example, in Austria the good quality of the housing stock together with its self-financing mechanism is strengthening the perceived position of private banks. ESG issuance seems to be embedded in a process of cream-skimming rather than on the spreading of investment where it can produce a higher impact.

To sum up, the identified contradictions between ESG and decarbonisation trace the limitations of market-based green financing of social housing. The interplay between national social housing financing systems and the homogenising force of ESG finance results in a range of outcomes. On the one hand, in Austria and Denmark, with relatively more countercyclical reliance on self- and public-financing mechanisms, SHOs are relatively independent of ESG finance. In France and the Netherlands, public support by banks and guarantees is protecting SHOs in their transition efforts towards ESG finance. Finally, when it comes to the German more commercialised operators with only occasional links to the state, ESG finance impacts on social housing financing are larger in terms of heterogeneity across SHOs and cyclicality.

6. Conclusion

This article has focused on the multi-faceted interlock between ESG finance and the decarbonisation of the social housing stock. The results show that ESG legislation is expanding reporting responsibilities while producing only limited additional finance ultimately geared towards large and commercially oriented SHOs and debt aggregator organisations. Furthermore, the expansion of MEPS in countries like France and the Netherlands is already resulting in higher costs creating tensions with SHOs’ social mission of building homes at affordable rents. Finally, the adoption of ESG financing is producing inequalities in access to capital across national financing systems and individual providers.

These results signal that the greening of SHO debt together with the incorporation of transitional and environmental risks is affecting the financial systems’ configuration and opening up a number of questions and scenarios requiring further research. First, the accrual of green premiums could be taking place at fund and investor level and not yet having materialised into interest rebates for SHOs. Second, the ECB’s ‘tilting’ toward green securities may reinforce green premiums in the secondary market as inflation recedes and Quantitative Easing (QE) is re-established.

Ultimately, the three contradictions identified in this study are not posited as definitive flaws in green finance, but could well be the result of adjustment pressures instead of the establishment of systemic tensions. Fully evaluating the impact of ESG indicators on social housing financing will require more research in the longer run, also drawing from quantitative evidence. Moreover, ESG-related acts and directives are just one set of policies in a broader regulatory landscape that includes multiple tools and renovation models for example Energy Service Companies (ESCOs) and One-Stop-Shops (OSS). Also, the future expansion of the Emissions Trading Scheme (ETS) to buildings and transport may also increase the financial viability of housing renovation. Fertile ground for future research lies at the intersections of these stimuli that combine financial incentives with institutional design.

Our research highlights how debt-aggregators have become a relevant response to increasingly complex capital markets requiring large debt issuances. These institutions provide both access to financial markets and data management and reporting expertise producing economies of scale and improving access to finance for smaller SHOs. When it comes to mid-term policy recommendations, the development of aggregators through regional public banks could further access to ESG capital for a wider array of SHOs. Furthermore, one of the most immediate changes of ESG legislation that could improve SHO access to private capital could be the introduction of housing affordability as a Principal Adverse Indicator (PAI) extending the ‘do no harm’ principle of ESG in a social dimension. Finally, over the longer run, there is a need to advance the ‘S’ in ESG to showcase SHOs’ work in financial markets. The Social Taxonomy, but also the labelling of debt emitters as ESG-only, could reduce administrative burdens and further the access to sustainability-labelled debt.

Acknowledgement

The fieldwork was mostly conducted during an academic secondment at Housing Europe. We thank the whole Housing Europe team and Alice Pittini in particular for their invaluable support in gaining access to interviewees.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Alejandro Fernández

Alejandro Fernández is a PhD candidate in comparative housing policy at the Department of Management in the Built Environment at Delft University of Technology. He has a background in economics and policy analysis. His research focuses on housing taxation, affordability, energy efficiency and ESG finance.

Marietta Haffner

Marietta Haffner is an Assistant Professor at the Faculty of Architecture and the Built Environment at Delft University of Technology. Marietta’s interests include financial and economic aspects of housing, including housing affordability, tenure, policy and equity issues.

Marja Elsinga

Marja Elsinga is professor of Housing Institutions & Governance at the Faculty of Architecture and the Built Environment at Delft University of Technology. Her research focusses on how to make adequate housing work in different contexts and how countries can learn from each other.

Notes

1 See for example Hact’s “Retrofit Credits” or the French “Certificat d’Économie d’Energie”.

2 In Germany, social rental housing is only considered as such while government subsidies are ongoing, see next section for detail. Even though the sector is small, Germany is included as a relevant case because of the existence of large landlords with high heterogeneity in their profit motivations facing renovation requirements.

3 A spread is the difference in yield between two bonds. The sovereign spread is the difference between any bond and that of a government with AAA rating.

4 Net debt to EBIDTA is the ratio of liabilities to Earnings Before Interest, Taxes, Depreciation and Amortization (EBIDTA) of a company.

References

- Aalbers, M. B. (2017) The variegated financialization of housing, International Journal of Urban and Regional Research, 41, pp. 542–554.

- Aalbers, M. B. (2022) Towards a relational and comparative rather than a contrastive global housing studies, Housing Studies, 37, pp. 1054–1072.

- Aalbers, M. B., Taylor, Z. J., Klinge, T. J. & Fernandez, R. (2023) In real estate investment We trust: State De-risking and the ownership of listed US and German residential real estate investment trusts, Economic Geography, 99, pp. 312–335.

- Bertoldi, P., Economidou, M., Palermo, V., Boza‐Kiss, B. & Todeschi, V. (2021) How to finance energy renovation of residential buildings: Review of current and emerging financing instruments in the EU, WIREs Energy and Environment, 10, pp. e384.

- Bindslev, J. (2018) New Financing of Social Housing Strengthens the Market for Danish Government Securities (Denmark: Danmarks National Bank). https://www.nationalbanken.dk/en/publications/Documents/2018/12/ANALYSIS_no%2024_New%20financing%20of%20social%20housing%20strengthens%20the%20market%20for%20Danish%20government%20securities.pdf (accessed December 2023).

- Blackwell, T. & Bengtsson, B. (2023) The resilience of social rental housing in the United Kingdom, Sweden and Denmark. How institutions matter, Housing Studies, 38, pp. 269–289.

- BNG Bank (2021) Annual Report 2021. BNG. https://www.bngbank.com/Financials/Annual-report-2021 (accessed December 2023).

- Boelhouwer, P. & Van der Heijden, H. (1992) Housing Systems in Europe: Part I (Delft, The Netherlands: Delft University Press).

- Boelhouwer, P. J. (Ed.). (1997) Financing the Social Rented Sector in Western Europe (Delft, The Netherlands: Delft University Press).

- CBI (2021) $500bn Green Issuance 2021: Social and sustainable acceleration: Annual green $1tn in sight: Market expansion forecasts for 2022 and 2025. https://www.climatebonds.net/2022/01/500bn-green-issuance-2021-social-and-sustainable-acceleration-annual-green-1tn-sight-market (accessed December 2023).

- Clarion (2020) Clarion Housing Group raises £350m in record breaking sustainable bond issue. https://www.clarionhg.com/news-and-media/2022/04/11/clarion-350m-in-record-breaking-sustainable-bond-issue (accessed December 2023).

- Conrads, C. (2022) Policy and regulation in the area of tension between shaping the ESG transformation and growing regulatory pressure, in: T. Veith, C. Conrads & F. Hackelberg (Eds) ESG and Real Estate: A Practical Guide for the Entire Real Estate and Investment Life Cycle (Freiburg, Germany: Haufe-Lexware). https://ebookcentral-proquest-com.tudelft.idm.oclc.org/lib/delft/detail.action?docID=6998863# (accessed December 2023).

- Cortellini, G. & Panetta, I. C. (2021) Green bond: A systematic literature review for future research agendas, Journal of Risk and Financial Management, 14, pp. 589.

- Doronzo, R., Siracusa, V. & Antonelli, S. (2021). Green bonds: the sovereign issuers’ perspective, Bank of Italy Markets, Infrastructures, Payment Systems Working Paper No. 3. Available at SSRN: https://ssrn.com/abstract=3854966 or doi: 10.2139/ssrn.3854966.

- Droste, C. & Knorr-Siedow, T. (2014) Social housing in Germany, in: K. Scanlon, C. Whitehead, & M. F. Arrigoitia (Eds.), Social Housing in Europe, pp. 183–202 (Oxford, UK: John Wiley & Sons, Ltd).

- Economidou, M., Todeschi, V., Bertoldi, P., D’Agostino, D., Zangheri, P. & Castellazzi, L. (2020) Review of 50 years of EU energy efficiency policies for buildings, Energy and Buildings, 225, pp. 110322.

- EIB (2019) Austria: EIB and Erste Bank promote affordable housing. https://www.eib.org/en/press/all/2019-133-eib-and-erste-bank-promote-affordable-housing-in-austria (accessed December 2023).

- Elsinga, M. & Wassenberg, F. (2014) Social housing in the Netherlands. In K. Scanlon, C. Whitehead, & M. F. Arrigoitia (Eds), Social Housing in Europe, pp. 21–40 (Oxford: John Wiley & Sons, Ltd).

- European Central Bank (2022) Good Practices on Climate-Related and Environmental Risk Management: Observations from the 2022 Thematic Review (Frankfurt, Germany: Publications Office). doi: 10.2866/417808

- European Commission. Joint Research Centre. Institute for Energy and Transport (2014) Overcoming the Split Incentive Barrier in the Building Sector: Workshop Summary (Ispra, Italy: Publications Office). doi: 10.2790/30582

- Fama, E. F. & French, K. R. (2007) Disagreement, tastes, and asset prices, $. Journal of Financial Economics, 83, pp. 667–689.

- Fatica, S. & Panzica, R. (2021) Green bonds as a tool against climate change? Business Strategy and the Environment, 30, pp. 2688–2701.

- Galvin, R. (2023) Do housing rental and sales markets incentivise energy-efficient retrofitting of Western Germany’s post-war apartments? Challenges for property owners, tenants, and policymakers, Energy Efficiency, 16, pp. 25.

- Hachenberg, B. & Schiereck, D. (2018) Are green bonds priced differently from conventional bonds?, Journal of Asset Management, 19, pp. 371–383.

- Haffner, M. E. A. (2021) Pathways of Dutch and German social renting, in: S. Tsenkova (Ed.) Cities and Affordable Housing, 1st ed., pp. 247–258 (New York, NY: Routledge).

- Haffner, M. E. A., Hoekstra, J., Oxley, M. J. & Heijden, H. v d (2009) Bridging the Gap Between Social and Market Rented Housing in Six European Countries? (Amsterdam, The Netherlands: IOS Press).

- Haffner, M., Hoekstra, J., Oxley, M. & Heijden, H. V. D. (2010) Universalistic, particularistic and Middle way approaches to comparing the private rental sector, International Journal of Housing Policy, 10, pp. 357–377.

- Housing Europe. (2020) The Cost of the Renovation Wave. https://www.housingeurope.eu/file/948/download (accessed December 2023).

- Kadi, J. & Lilius, J. (2022) The remarkable stability of social housing in Vienna and Helsinki: A multi-dimensional analysis, Housing Studies, pp. 1–25.

- Kleniewski, N. & Harloe, M. (1996) The people’s home? Social rented housing in Europe and america, Contemporary Sociology, 25, pp. 75.

- Knuth, S. (2016) Seeing green in San Francisco: City as resource frontier: Seeing green in san francisco, Antipode, 48, pp. 626–644.

- Kofner, S. (2017) Social housing in Germany: an inevitably shrinking sector?, Critical Housing Analysis, 4, pp. 61–71.

- Kössl, G. (2022) Affordable housing and social inclusion ‐ The case of Vienna and Austria, in: O. Heckmann (Ed.), Future Urban Habitation, 1st ed., pp. 115–129 (Oxford, UK: Wiley).

- Lawson, J. (2013) The use of guarantees in affordable housing investment—A selective international review (Melbourne, Australia: Australian Housing and Urban Research Institute).

- Lévy-Vroelant, C., Schaefer, J.-P. & Tutin, C. (2014) Social housing in France, in: K. Scanlon, C. Whitehead, & M. F. Arrigoitia (Eds.), Social Housing in Europe, pp. 123–142 (Oxford, UK: John Wiley & Sons, Ltd).

- Lunde, J. & Whitehead, C. (2016) Following on from a quarter of a century of mortgage debt, in: J. Lunde & C. Whitehead (Eds.), Milestones in European Housing Finance, pp. 433–446 (Oxford, UK: John Wiley & Sons, Ltd).

- Mangold, M. & Mjörnell, K. (2022) Swedish public and private housing companies’ access to the capital market for financing energy renovation, Journal of Housing and the Built Environment, 38, pp. 673–697.

- Mundt, A. & Springler, E. (2016) Milestones in housing finance in Austria over the last 25 years, in: J. Lunde & C. Whitehead (Eds.), Milestones in European Housing Finance, pp. 55–73 (Oxford, UK: John Wiley & Sons, Ltd).

- Norris, M. & Byrne, M. (2021) Funding resilient and fragile social housing systems in Ireland and Denmark, Housing Studies, 36, pp. 1469–1489.

- NWB Bank (2021) Annual Report 2021. NWB. https://nwbbank.com/application/files/9816/5468/9535/NWB_Bank_Annual_report_2021.pdf (accessed December 2023).

- OECD (2020) Social Housing: A key part of past and future housing Policy. https://read.oecd-ilibrary.org/view/?ref=137_137578-34brg1nxua&title=Social-Housing-A-Key-Part-of-Past-and-Future-Housing-Policy (accessed December 2023).

- Reuters (2022) German officials raid Deutsche Bank’s DWS over “greenwashing” claims. https://www.reuters.com/business/german-police-raid-deutsche-banks-dws-unit-2022-05-31/ (accessed December 2023).

- Ruonavaara, H. (1993) Types and forms of housing tenure: Towards solving the comparison/translation problem, Scandinavian Housing and Planning Research, 10, pp. 3–20.

- S&P. (2022) Ratings Direct: Waarborgfonds Sociale Woningbouw (Stockholm, Sweden: Global Ratings). https://www.wsw.nl/uploads/tx_dddownload/S_P_Global_juli_2022.pdf (accessed December 2023).

- Scanlon, K., Whitehead, C. & Arrigoitia, M. F. (2015) Social housing in Europe, European Policy Analysis, 17, pp. 1–12.

- Schaefer, J.-P. (2003) Financing social housing in France, Housing Finance International, 17, pp. 27–34. https://www.proquest.com/docview/216202047/fulltextPDF/25E7219DA494494EPQ/1?accountid=27026 (accessed December 2023).

- Tutin, C. & Vorms, B. (2016) Milestones of housing finance in France between 1988 and 2014: Is the French Credit System a Gallic Oddity?, in: J. Lunde & C. Whitehead (Eds.), Milestones in European Housing Finance, pp. 165–181 (Oxford, UK: John Wiley & Sons, Ltd.)

- van Hal, A., Coen, M. & Stutvoet, E. (2019) Energy performance fee to cover investments in the energy efficiency of affordable housing The Netherlands, in: G. van Bortel (Ed.), Affordable Housing Governance and Finance: Innovations, Partnerships and Comparative Perspectives (Oxford, UK: Routledge).

- Vonovia (2023) FY 2022: Earnings Call Presentation. https://investoren.vonovia.de/en/news-and-publications/presentations/ (accessed December 2023).

- Wainwright, T. & Manville, G. (2017) Financialization and the third sector: Innovation in social housing bond markets, Environment and Planning A: Economy and Space, 49, pp. 819–838.

- Whitehead, C. (2014) Financing social rented housing in Europe, in: K. Scanlon, C. Whitehead, & M. F. Arrigoitia (Eds.), Social housing in Europe, pp. 315–330 (Oxford, UK: John Wiley & Sons, Ltd).

- Whitehead, C. M. E. (1999) The provision of finance for social housing: The UK experience, Urban Studies, 36, pp. 657–672.

- Zerbib, O. D. (2019) The effect of pro-environmental preferences on bond prices: Evidence from green bonds, Journal of Banking & Finance, 98, pp. 39–60.

Appendix A:

Research questions, data collection and codes

Appendix B:

Interview protocol

Interview protocol

1. Business as usual

1.1. What are the main sources of external finance for your organisation?

1.1.1. Private – Bonds, private loans. Public – Grants, subsidised loans. Both – Combination

1.2. What are the main type of investors?

1.2.1. Institutional – Pension Funds, Insurance, Private Equity. Private Banks. Public Banks

1.3. How would you characterise your access to funding? Constrained? Easy? Cumbersome? Why?

1.4. What are the leading factors determining your access to finance? Do you expect them to undergo any fundamental changes in the near future?

1.5. In what ways if any has the increase in interest rates challenged your funding strategy?

2. ESG

2.1. Do you currently tap on to ESG for your financing needs?

2.2. Could you reflect on the main reasons for ESG uptake and whether they are likely to change?

2.2.1. Among these factors, which ones are most important?

2.3. There’s this term, additionally that shows up in the literature, do you perceive ESG as bringing additional funds into the company?

2.4. Do you use the new European regulation and framework for ESG (CSRD)(Taxonomy)? Is there a set of reporting standards would your organisation is more likely to follow?

2.5. What are the factors that would make you increase the ESG proportion of your funding in the future? If you plan to do so, do you have an explicit strategy to follow?

2.5.1.1. Which among the ESG indicators are your priority?

2.6. Which forms does (or would you like) ESG funding take, do you plan a green bond, an ESG loan from a bank etc.?

2.6.1. What are the likely consequences of these forms of financing?

2.7. ESG is usually linked to specific projects within companies? Within your organisation is ESG used in particular projects?

2.7.1. For example energy retrofit, improving energy efficiency?

2.7.2. Is it about new developments?

3. Financing renovation and energy efficiency requirements

3.1. How is your organisation working through the energy efficiency improvement of the stock? Do you have a number of plans in place?

3.1.1. Funding requirements?

3.2. Do you expect the energy transition to be a driving force toward ESG funding or would business as usual cover the needs of your organisation?

3.2.1. If not large-scale renovation, what would you say are the driving forces behind adopting ESG?

3.3. Do you conceive of ESG funding as a viable alternative to rent increases or progressive withdrawals of public increases in costs of private funding?

4. Risks, challenges and recommendations

4.1. What importance do you attach to your overall rating? How is this affected by ESG and renovation?

4.2. Do you have a designated team collecting non-financial data for ESG purposes?

4.3. Do current standards pose any particular issues for housing associations in general or your company in particular?

4.4. What changes would you like to see in the way ESG legislation is being formulated? What would make your access to ESG capital easier?