?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The political economy literature on international bailouts has repeatedly shown that the domestic politics of rescued countries influence international bailout compliance. However, we know less about the domestic politics of bailout negotiations, and especially the type of conditions negotiated by governments of more developed countries with strong ties to international lenders. This paper puts forward an argument about the role of a government’s partisanship in shaping the conditions stipulated between international lenders and developed countries when crises confront the latter. Consistent with political cover theories, we argue that governments of crisis countries seek to scapegoat international institutions in order to push domestically unpleasant reforms. However, when crises affect countries significantly close to international lenders, international institutions may tolerate the scapegoating attitude and accept to emphasize governments’ reforms in the direction of their core ideological constituencies. Focusing on bailout negotiations during the Eurocrisis (2008–2016), we maintain that while important and painful reforms were discussed at the negotiation tables, the involved international lenders also accommodated the policy preferences of both left and right governments of crisis-ridden countries, everything else constant. So, conditionality came with duress, but governments were also able to emphasize reforms on the opponents’ policy issues, hence systematically obtaining fewer measures on their voters’ main policy areas. Regression analyses of an original country-quarter dataset of EU bailout conditionality measures provide support to our hypothesis. The findings are relevant to the analysis of partisan politics in economic negotiations and of democratic deficits in international organizations. Furthermore, this study contributes to understanding the political accessibility and ideological dynamics of international lending beyond the Eurocrisis.

La literatura de economía política sobre los rescates internacionales ha demostrado, una y otra vez, que la política interna de los países rescatados influye en el cumplimiento de los rescates internacionales. Sin embargo, sabemos menos sobre la política interna de las negociaciones de rescate y, especialmente, sobre el tipo de condiciones negociadas por los gobiernos de los países más desarrollados con fuertes vínculos con los prestamistas internacionales. Este artículo presenta un argumento sobre el papel del partidismo de los gobiernos en la configuración de las condiciones estipuladas entre los prestamistas internacionales y los países desarrollados cuando estos últimos se enfrentan a una crisis. En consonancia con las teorías de la cobertura política, sostenemos que los gobiernos de los países en crisis tratan de convertir a las instituciones internacionales en chivos expiatorios para impulsar reformas que resultan menos agradables a nivel nacional. Sin embargo, cuando las crisis afectan a países significativamente cercanos a los prestamistas internacionales, las instituciones internacionales pueden tolerar esta actitud de convertirles en chivo expiatorio y pueden aceptar enfatizar las reformas de los gobiernos hacia su principal electorado ideológico. Centrándonos en las negociaciones de los rescates durante la Crisis de la zona euro (2008-2016), sostenemos que, aunque en las mesas de negociación se discutieron reformas importantes y dolorosas, los prestamistas internacionales implicados también se acogieron a las preferencias políticas de los gobiernos de izquierda y derecha de los países en crisis, manteniendo constante todo lo demás. De este modo, la condicionalidad llegó con coacción, pero al margen los gobiernos pudieron enfatizar aquellas reformas sobre las cuestiones políticas de la oposición, con lo que alcanzaron sistemáticamente menos medidas con respecto a las principales áreas políticas de sus votantes. Los análisis de regresión de un conjunto de datos originales por país-trimestre de las medidas de condicionalidad de los rescates de la UE respaldan nuestra hipótesis. Los resultados son relevantes para el análisis de la política partidista en las negociaciones económicas y los déficits democráticos en las organizaciones internacionales. Además, este estudio contribuye a comprender la accesibilidad política y la dinámica ideológica de los préstamos internacionales más allá de la crisis de la zona euro.

La recherche en économie politique portant sur les opérations de sauvetage financier internationales a montré à de nombreuses reprises que la politique intérieure des pays renfloués influençait la conformité desdites opérations. Néanmoins, nous disposons de moins d’informations concernant les politiques internes des négociations pour sauvetage financier, et notamment sur les conditions négociées par les gouvernements de pays davantage développés, bénéficiant de liens étroits avec des prêteurs internationaux. Cet article met en avant le rôle d’un soutien partisan à un gouvernement dans l’élaboration de conditions définies entre des prêteurs internationaux et des pays développés confrontés à une crise. En nous appuyant sur des théories relatives à la notion de couverture politique, nous affirmons que les gouvernements de pays en crise rejettent la faute sur les institutions internationales de manière à mettre en place des réformes intérieures contraignantes. Toutefois, lorsque les crises affectent des pays entretenant des liens particulièrement étroits avec des prêteurs internationaux, on constate que les institutions internationales peuvent tolérer cette attitude et accepter d’appuyer les réformes de ces gouvernements en allant dans le sens idéologique de la majorité de leurs électeurs. En nous appuyant sur les négociations relatives aux opérations de sauvetage lors de la crise de la zone euro (2008-2016), nous affirmons que, tandis que d’importantes et difficiles réformes étaient débattues, les prêteurs internationaux impliqués s’adaptaient aux préférences politiques des gouvernements touchés par la crise, de droite comme de gauche, toutes choses égales par ailleurs. Si la conditionnalité était faite de contraintes, dans les marges, les gouvernements étaient en mesure de défendre des réformes face à leurs opposants politiques, ce qui leur permettait d’obtenir systématiquement une réduction du nombre de mesures dans les principaux domaines intéressant leurs électeurs. Notre hypothèse est étayée par une analyse de régression d’un ensemble de données original, par pays et par trimestre, concernant les conditions de sauvetage financier dans l’UE. Les résultats permettent d’informer une analyse des politiques partisanes lors de négociations économiques et en présence d’un déficit démocratique au sein des organisations internationales. Par ailleurs, cet article éclaire les questions d’accessibilité politique et de dynamique idéologique des prêts internationaux, au-delà de la crise de la zone euro.

Introduction

Economic downturns have long sparked interest in the politics of lending conditions by international financial institutions (IFIs). Recently, a voluminous literature has shed light on the political roots and ramifications of bailouts, increasingly focusing on developing countries. This trend has however left two areas of analysis relatively unexplored. First, while the literature assumes that conditionality is an important mechanism driving international financial negotiations (Copelovitch Citation2010b), recent works have concentrated on the effect of IFI conditionality on policy compliance (Blanton, Blanton, and Peksen Citation2015; Rickard and Caraway Citation2019) rather than on the politics leading to conditionality. Furthermore, much attention has been placed on the preferences of influential investors and lenders when bailouts regard emerging economies, for example in Latin America and in former Soviet Union countries (Appel and Orenstein Citation2013; Grittersová Citation2017). Relatively little research has investigated what determines varying conditionality when crisis-stricken countries are close allies—if not even “principals”—of international creditors. This relevant research gap has emerged since the post-2008 global recession, when a number of developed economies were forced to negotiate bailouts with international lending institutions. Yet, aside from a few case studies, we still know little about the way politics has shaped bailout conditionality across advanced democracies.Footnote1

Against this background, this paper studies the politics of bailout negotiations between IFIs and crisis-ridden developed countries, focusing on the case of Europe. Our point of departure is that, while the domestic politics of troubled countries is a matter of relevance to IFIs about to negotiate reforms anywhere (Stone Citation2002), it is especially important when international institutions deal with established developed democracies. When dealing with these countries, IFIs need to balance between signalling resolve to potentially contagious economic turmoil and managing the risks of popular backlash and long-run moral hazard (Bird Citation2007). So, politically, IFIs want to fill a significant yet bystander role, for the sake of avoiding public unrest and disobedience (Genovese, Schneider, and Wassmann Citation2016). Along these lines, we claim that IFIs let cues about the bargaining government’s willingness and capacity to implement policy reforms lead the direction of the bailout negotiations, even if at the cost of scapegoating (Vreeland Citation1999). These cues, we argue, are captured by the partisan ideology of the negotiating government.

This argument leads us to expect that, contrary to those who believe in an unequivocally conservative position of the Troika on structural reforms, international lenders at the European bailout negotiations did not a priori prefer to dictate certain types of national policies, or at least allowed the counter-parts to state their preferences on a bundle of conditions. In concordance with the “political cover” theory of conditionality (Vreeland Citation2003), we maintain that partisan governments had room to steer the negotiations toward their favorite types of conditions. Furthermore, and in line with the logic of policy prescription and manipulation by partisan lines (Caraway, Rickard, and Anner Citation2012; Gunaydin Citation2018; Nelson Citation2014), we expect that bailout-seeking governments aimed to marginalize their partisan opponents with policy conditionality, and successfully settled on a basket of reforms that shielded their main voters, everything else constant. We contend that this is especially clear in recent European bailouts, because here IFIs’ preferences resulted in an adaptable creditor position (Henning Citation2017), and this flexibility translated in some tolerance for conceding different types of conditions to different partisan governments. Hence, governments across the ideological spectrum used the negotiation with the Troika as a way to pursue reforms that would have otherwise met tremendous domestic opposition.

Our argument is novel because, differently from research that paints IFIs as categorical austerity-biased lenders (Featherstone Citation2015), we claim that, when confronted with developed democracies and specifically countries in close proximity to creditor states, international institutions accept to underplay a certain type of bailout conditions that is more politically costly and less in line with the domestic government’s policy manifesto. So, in contrast to studies that stress the disparities of international financial treatment toward left and right governments (Beazer and Woo Citation2016; Cho Citation2014), we propose that in certain circumstances the IFI’s approach to bailout conditionality may work similarly for right- and left-wing governments. Pending the arrangement of bailout negotiations and the leverage the rescue countries have over its creditors, conditionality bargaining may be systematically stacked in ways to at least partly satisfy the partisan base of the national government, everything else equal.

We interrogate our hypothesis focusing on the case of the European financial crisis (or “Eurocrisis”) that unfolded after 2008. This is a useful empirical ground, because the crisis hit many European democracies in a matter of months, but yielded a number of national packages with different financing conditions and reforms (Karagiannis and Konstantinidis Citation2015). The macroeconomic circumstances of the exposed countries varied, but within the context of the European Union (EU) many policy levers were constrained, therefore making all the countries in similar ways reliant on immediate financial relief from international institutions.Footnote2 Importantly, each national government sought to independently negotiate their external funds. This means that governments with different ideological backgrounds engaged with the international lenders around the same time, therefore providing a rich range of country-level variation on the partisanship front while keeping other factors fixed.

We first present the background to rescue programmes in Europe during the global recession, and introduce our theory of partisan effects on EU bailout negotiations and the resulting conditionality. We then present originally collected country-quarter data that covers all the twelve bailouts that stroke in Europe between 2008 and 2016.Footnote3 In line with disaggregated studies of conditionality (Vreeland Citation2006), our data separate conditions with respect to their policy outcomes. Given our theoretical framework, we distinguish conditions targeting finance (capital) sector measures and public sector labour reforms, among others. Our statistical analyses of the varying conditions negotiated in eight EU countries throughout a decade indicate two important patterns. We find that the bailout conditions for a more conservative government include fewer finance-related requests such as capital controls or market liberalisation constraints. By contrast, the conditions for a more left-wing government include fewer public sector reforms such as cuts to wages for labour. So, while the results confirm that government partisanship matters a great deal in the course of bailout negotiations, they also indicate that governments of different ideological types come out of the negotiations with conditions that are consistent with the policy preferences of their core ideological group.

The findings provide insights to the study of international conditional policies and the politics of international organisations more broadly. First, with respect to European politics, our results challenge blank notions of “technocratic dictatorship” (Giddens Citation2012) and suggest that IFIs dealing with crisis-ridden governments in the European Union indeed indicated painful directions of domestic adjustments, but also allowed governments to get there with their democratically elected policy preferences. Our empirical findings also speak to classical research on conditionality and the politics of lending (Pop-Eleches Citation2008; Vreeland Citation2003) because we show that left and right governments do not have differential treatments, and either side of government can get more of their favorite type of policy reforms. Furthermore, our theory suggests that this is not just solo manoeuvring by governments: in the case of European bailouts, the Troika, on average, allowed governments to refine conditionality in favour of their partisan base. In sum, our paper supports the view that, when borrowers are close to shareholders such as in the case of European countries, technocratic institutions may discriminate across the partisan interests of the governments at the negotiation table. This may have worked in favor of leaders and lobby groups of European nations in the early 2000s; however, it may be one of the political reasons why developing countries feel mistreated by Western IFIs and are increasingly moving toward other lenders of last resort.

Theoretical Framework

Negotiating Rescue Funds during the Global Recession: The Role of Governments’ Partisanship

Soon after the outbreak of the 2008 Great Recession in the United States, Europe became the main epicentre of the global financial crisis. Faced with pressing deficits, quick drying-out of external financial flows and the uncertainty of default, the governments of several European countries turned to international financial institutions for assistance. The International Monetary Fund (IMF), the European Central Bank (ECB) and the European Commission (EC) reacted promptly to the necessity of the affected countries in order to diffuse concerns with moral hazard and crisis spillover. Between 2008 and 2016 (and effectively until 2018), these three institutions, together referred to as the “Troika,” designed most bailout plans in the European continent.Footnote4

As for many similar programs across the world, the Troika offered rescue in exchange for economic conditions that had to restore the confidence of markets and legitimise the borrowing in donor countries. The lenders systematically requested adjustment programmes centred on a number of cardinal measures, including fiscal austerity and competitiveness through reforms. All these measures were devised and revised together with the government of the state seeking support. Consequently, each bailout package was subject to negotiations that eventually led to different bailout programmes described in the so-called Memoranda of Understanding (MoU).

It is noteworthy that each EU-based MoU included a varying number and depth of reforms. In the case of Greece in 2011–2012, more than 100 conditions were listed in the negotiated contracts. By contrast, Ireland’s 2012 MoU featured less than 50 conditions. Classical theories of international lending suggest that this variation is a function of the steepness of financial demands in the crisis countries, for the more troubled the economy the harsher the conditions for rescue (Dreher and Gassebner Citation2012; Mosley, Harrigan, and Toye Citation1995). However, with perhaps the exception of Greece, the scale of the crisis within each country does not seem to be a conclusive explanation for different forms of conditionality in the EU.

To give some perspective, Cyprus aimed for a 10 billion Euro bailout, which corresponded to one third of its annual GDP. Latvia aimed for less than 5 billion, reflecting a much smaller fraction of national income; nonetheless, Latvia received in total a similar amount of conditions as Cyprus. Also importantly, the MoUs stressed different sets of conditional measures. The bailout in Cyprus put emphasis on financial market conditions, such as the regulation of firms and especially banks (including capital targets and controls). By contrast, the Latvia bailout included significant measures on the public sector (such as social benefit cuts and labour deregulation). Evidently, fundamental differences in crisis mechanisms, explaining the built-up of fiscal vulnerabilities across these countries, called for different policy measures and could perhaps explain this variation. But even then, there is substantive variation among the bailout-related policy reforms among similarly fiscally vulnerable countries. For example, Spain and Cyprus (with similar trends of national debt and sovereign bond yields, and roots of the crisis in the banking system) had different levels of labour conditions in relation to the public sector.

In order to explain the variation expressed in the EU bailout agreements, recent research focuses on the explanatory role of political factors. Anner and Caraway (Citation2010); Caraway, Rickard, and Anner (Citation2012), for example, show evidence that in recent decades, democracies with stronger domestic labour institutions received less intrusive conditions in their loan programs. Others have focused on politicians’ sensitivity to forthcoming elections. Along these lines, Schneider (Citation2019) suggests that upcoming elections in EU countries have had significant effects on budgetary as well as bailout negotiations for borrowing and borrower countries (see also Rickard and Caraway Citation2019).

This research relies on the institutional variation influencing the national politics of bailouts, stressing the effect of electoral uncertainty and the outcome of domestic coalition building. Surprisingly, this scholarship gives small emphasis to executive partisanship and how this might explain different outcomes of bailout conditionality (Dreher, Sturm, and Vreeland Citation2015; Nelson Citation2014). Drawing on this latter research, we contend the partisan ideology of the negotiating executive creates significant leverage on the conditional agreements for a number of reasons. First, technocrats pay particular attention to cues that signal the genuine commitment of borrowing governments (Pop-Eleches Citation2008). This may be especially true if IFIs care about the shared interests of their donors (Mosley Citation2003), and if the reputation of donors is linked to borrowing countries, like in the case of the EU (Gray Citation2009; Walter, Ray, and Redeker Citation2020). In Europe, the Troika may have tried to set up the representatives of the borrowers so to succeed, hence opening to the the domestic preferences of their ideological base (Bearce Citation2003; Quinn and Toyoda Citation2007).

Additionally, partisanship may be important for the relations between international lenders and borrowing developed countries because partisan ideology locks the negotiating governments onto an agenda that is scrutinised by domestic oppositions (Beazer and Woo Citation2016; Boin, Hart, and McConnell Citation2009). By letting an ideological government request certain programmes instead of others in exchange for rescue, IFIs may create additional domestic watchdogs for the reform programmes. As others have indicated, these considerations are relevant in the context of the Eurocrisis, given the strong voice of domestic groups and opposition parties in the course of the financial meltdown (Walter, Ray, and Redeker Citation2020). European governments meeting the Troika had plenty of domestic discussions on the positions to take at the negotiation table, and countries with different internal political motivations had different types of success at the bailout negotiations (Karagiannis and Konstantinidis Citation2015).

Evidently, executive positions seek to safeguard the governments’ core constituencies, and therefore to protect their ideological issue domains (Alesina and Roubini Citation1992; Hicks and Swank Citation1992). It is however up to debate what conditions may follow from each type of ideological bargaining. Some assume that right-wing governments prefer to take control of market-oriented reforms due to the fact that their political allies are pro-market. However, financial sector reforms can be burdensome if they require new standards of private behaviour (Lane Citation2012). Similarly, while left-wing governments are more tied to the public sector, it is unclear if they may systematically prefer to implement labour conditions, trying to shape them in favour of workers, or would rather leave it to others to handle.

We contend that governments would avoid reforms, especially if in their policy domain (i.e., if they are more likely to affect their salient domestic interest groups). Yet, and diverging from some recent research on international conditionality (e.g., Beazer and Woo Citation2016), we suggest that in the European case one side of partisanship did not burden governments more than the other. Evidently, left and right governments may still engage with—and perhaps sometimes even welcome—conditionality for catalytic purposes (Woo Citation2013). For example, left leaders in emerging economies may adopt financial conditions to improve their perceived creditworthiness in international markets (Cho Citation2014). However, partisan governments of advanced economies may have more influence in selectively choosing the type of preferred conditionality due to their ability to play off different creditors or use other financing channels (Henning Citation2017; Vaughn Citation2019). Consequently, we contend that both sets of ideology could work out agreements that would protect their base.Footnote5

Prima facie evidence that partisanship played an influential role in the agenda setting of conditionality in Europe, often at the expense of domestic opponents, is relatively easy to trace. Some comparisons provide important anecdotes. For example, throughout the bailout years, Latvia had a center-right government that settled on more public sector labour conditions (and specifically reductions to public sector wages) than, as a way of comparison, the Tsipras-headed left-wing government in Greece (Aslund Citation2013).Footnote6 Importantly, this observation suggests that both Latvia’s and Greece’s governments responded to their “power base.” Equally importantly, commentators claim that governments in these countries effectively “made EU institutions a scapegoat for […] the settled reforms” (Schranz Citation2014).Footnote7 This commentary suggests that the international institutions involved in EU bailouts tried to appease the core constituencies of the negotiating governments, and that these succeeded in pushing an agenda that would cost more to their ideological adversaries. Below we further explore the implications of this claim for Eurocrisis bailout conditionality.

Troika-Government Negotiations and Concessions during the Eurocrisis

We contend that crisis governments across the European continent were successful at pitching their policy interests to international lenders and therefore impose burdens for the opposition for one reason: the Troika’s approach to each bargaining country may have been intentionally malleable in order to converse with government-specific preferences, and hence resist further backlash.

The assumption that the Troika could maintain a certain political flexibility during financial negotiations is of course not new. Research on the political dynamics of the IFIs and the shareholder influence over the IMF (Caraway, Rickard, and Anner Citation2012; Copelovitch Citation2010a; Dreher Citation2004; Stone Citation2008) suggests that, if the politics of crises are particularly salient to the institutions’ shareholders, international bureaucrats may be willing to make concessions to governments in order to lessen the burden of reforms. In the case of the European bailouts, we expect this flexibility to be observable across governments with different partisan ideology. This is because of at least two reasons. First, in the Eurocrisis, the creditors—and especially the ECB and the EC—tried to ensure a particularly high level of responsiveness toward voters (Genovese, Schneider, and Wassmann Citation2016; Henning Citation2017; Schneider Citation2019). While some scholarship indicates that IFIs, and in particular the IMF, are more ideologically in line with right-wing governments (Lane Citation2012), this does not imply that the Troika—given its complex structure and the difficult politics of internal coordination—would only cater to the favoured reforms of right government while fighting left governments on their policy ground. As Beazer and Woo (Citation2016) show, international lenders have often struggled to find the optimal level of finance reforms and market liberalisation for right governments. Similarly, IFIs are aware that left governments concerned about workers’ opposition to labour-related loan conditions tend to be more aggressive, and have frequently appeased less labour measures for those governments (Rickard and Caraway Citation2014). In the specific case of the Troika, a coherent political preference seemed also particularly complex to arrange (Henning Citation2017). Some observers claim that in the Eurocrisis the IMF played a cushioned role because on the one hand it was there to back up the creditor European countries (e.g., Germany) but on the other it was not intended to upset European harmony.

Furthermore, the Troika may have well guaranteed European governments to shape bailouts toward conditions in affinity to their domestic policy agenda because of their rather central role in the international arena (Copelovitch Citation2010b), and in the EU itself. EU membership creates a special seal of credibility, so EU institutions not only decrease perceptions of risks, but also of policy recklessness. This means that during the global recessions, EU governments may have had enough clout to lobby the Troika for the policies that the domestic partisan base is less resentful of. The central question, then, is what set of conditions are most collectively preferable in a negotiation between the Troika and EU countries, given different types of ideological governments.

Common wisdom advocates that right politicians favour contracts that allow for privatisation and market liberalisation, while left politicians favour market restructuring in favour of public labour (Gunaydin Citation2018; Woo Citation2013). It follows that both would try to seek conditions on these respective fronts to have a monopoly of their policy fields. However, the so-called “political cover” hypothesis (Vreeland Citation2006) indicates that governments may ask for targeted loan conditions in order to make their desired reforms more politically feasible without IFIs on their back. This hypothesis is supported by evidence suggesting that the more politically savvy the government at a loan negotiation, the less politically controversial the proposed reforms (Dreher, Sturm, and Vreeland Citation2015; Rickard and Caraway Citation2014).

This line of thought entails that the optimal strategy for governments from either side of the ideological spectrum is to accept relatively fewer measures from their most salient policy domain. For example, everything else equal, right governments would accept fewer international financial measures (i.e., economic restructuring and bank monitoring) than left-leaning governments, which would be more focused on protecting the labour force. Of course, more subtle (but meaningful) differences in conditionality packages may exist due to the composition of left and right parties’ electoral base (Bulfone and Tassinari Citation2021) and the possible nature of broad coalitions in a country (Armingeon, Guthmann, and Weisstanner Citation2016). However, we can leverage this simplification as some studies on the role of partisan effects during the Eurocrisis suggest that left-right partisan divisions made for different positions on austerity and therefore on policy reforms (Genovese and Schneider Citation2020; Hübscher Citation2016). Thus, our intuition is that governments would try to scapegoat international lenders for reforms in the opponents’ fields, and is consistent with research that indicates that right governments have more difficulty committing to IFI-imposed financial conditions and would rather prefer to organically do market reforms without conditionality.Footnote8 We extend the “scapegoating” hypothesis by claiming that, in the context of the EU, both right- and left-governments may be successful at anchoring the negotiations to their most salient domestic principals.

Right governments can convince IFIs to let them pursue (more) labor reforms because they have the political capability to implement them compared to left leaders, who are usually more tied by unions (Lee and Woo Citation2021; Reinsberg, Kentikelenis, and Stubbs Citation2021). But also and perhaps differently from developing countries, financial actors in developed democracies do not need a boost of confidence from lenders and would thus rather deal with financial sector reforms without international authorities (Claessense, Demirguc-Kunt, and Huizinga Citation2001). The Troika’s goal during the Eurocrisis was first and foremost to provide credit at the scope of calming markets in the short run. Consequently, we conjecture that the lenders conceded to the right governments’ preferences to, on the one hand, pursue fewer financial sector reforms without conditionality sticks and, on the other hand, to play scapegoat for labour sector reforms, given the higher chance these pass with a conservative executive.

Vice versa, left governments can convince lenders to prioritize conditions related to the taxation and regulation of capital because these—at least in moderate cases of international economic competition—tend to be successfully deployed by the left. We believe the Troika accepted this position because left governments often threaten to leave rescue negotiations altogether, even at the cost of finding another lender of last resort (Gunaydin Citation2018; Nooruddin and Woo Citation2015). In the context of the Eurocrisis, where international lenders were placed at the bailout negotiation table to discuss credit but also as independent watchdogs, we believe that left governments used these credibility and escape threats to their advantage. Consequently, we expect that these partisan preferences were at least partially received, and that the Troika allowed for scapegoating also with left governments.

The envisioned interactions between partisan governments and the Troika and the resulting bailout conditions can be formalized in a game theoretic model, which we report in the Appendix. There, we present a non-cooperative finite extensive form game in the tradition of Hart and Mas-Colell (Citation1996). The government is the agent of its stronger domestic principals—for example, finance-oriented interest groups for the right, and labour-oriented groups for the left. It commits to a policy that is congruous to its internal interest, and reveals this political affinity in the negotiations with the lenders by signalling a bailout preference that matches its policy affinity. So, a right government proposes an agreement that protects its capital-oriented voters from, for example, more state-bound finance regulations. Vice versa, a left government proposes an agreement that protects labour interests from, for example, restructuring and deregulation, especially in the public sector.

The equilibrium exists in a condition in which the Troika and the government are better off agreeing on the policy affinity-driven outcome rather than outside options (see the proof in the Appendix). The nuance stands on the fact that the Troika is a non-partisan institution whose main goal is to achieve a bailout, and therefore whose utility to settle on an agreement is not sensitive to the policy preferences of the government.Footnote9 The main inference of the model is that the unique subgame perfect equilibrium outcome of the envisioned bargaining process tends to respect domestic governments’ political affinities without making either partisan inclination diverge the behaviour of the Troika.

The formal model yields two empirically testable implications. First and most importantly, the model makes a clear suggestion on the directional effects of partisanship on different forms of bailout conditions. Because left-wing governments have a stronger synergy with their domestic labour powers than they do with their domestic capital powers (and vice-versa for right-wing governments), left-wing governments obtain bailout agreements with more financial-oriented conditions, whereas right-wing governments obtain bailout agreements with more public sector oriented conditions.

The second order implication is a qualitative suggestion about the types of conditions settled by the negotiations. Deviating from previous research (Karagiannis and Konstantinidis Citation2015), the model does not imply that more bailout conditions are received by any type of government. In other words, there is no clear prediction on whether right governments should receive fewer conditions on average, as others have suggested. Similarly, there is no indication that reforms without a clear partisan nature may be linked to one type of partisan government more than another. Whilst these implications may be intrinsically interesting, we think they do not interject our quantity of interest (i.e., the effect of government partisanship on issue-based conditionality), and are therefore beyond the scope of this paper. Nonetheless, we also investigate them in the statistical analysis later in the paper.

Qualitative Insights and Empirical Considerations

The details of a number of European bailouts seem to confirm the interchange across types of reforms based on governments’ partisan ideology. We focus here on financial and public sector reforms, with particular emphasis on banking on the one hand, and labour on the other hand. Surely, historical accounts indicate that in the crisis years the status quo in the financial sector prevailed, for the orthodox insistence on the financial system’s role as a fundamental economic intermediary dominated in the European public discourse (Kotarski Citation2018; Walter, Ray, and Redeker Citation2020). This, however, does not mean that the financial sector remained unscathed. In fact, banking sector conditions—in the form of, for example, higher capital targets and new capital requirement schedules—remained a crucial item in many MoUs. Evidently, financial sector conditions have different impacts depending on whether they target public or private banks, and the extent to which the credit is externally owned. Nonetheless, financial reforms still remain in the capital market domain, and mostly affect investors. By contrast, other reforms spill over to other markets and affect different vulnerable groups. For example, public sector reforms directly affect the labour force.

Quite remarkably, several accounts of the EU bailout negotiations indicate that bailout conditions varied as right and left wing governments positioned themselves toward internal adjustments and domestic policy reforms. As Morlino and Sottilotta (Citation2019) report, in June 2012 the Spanish government led by right leader Mariano Rajoy accepted (up to) 100 billion euros as a “loan” to recapitalise the country’s ailing banks. In order to contain the risk of a financial meltdown, the Spanish government accepted harsh conditions. These reforms included choices that the left found extremely undesirable, such as the nationalization of banks, job cuts and losses on creditor bondholders. Notably, the Troika quickly consented to these choices. Additionally, ECB governing council member Panicos Demetriades said in an interview in September 2012 that one reason the ECB would not have to buy Spanish bonds was “that Spanish politics will get in a way of a rapid solution.” These words show the relatively openness of the EU institutions to the nature of preferred reforms (Boesler Citation2012).

A similar—although directionally opposite—story emerges from the interactions between the Troika and the Irish government. The Irish case is interesting because the first MoU was negotiated by the minority governing party led by the conservative Fianna Fáil, and then renegotiated after the 2012 election by the new government of Fine Gael and Labour. In the first MoU signed by the conservative government, the minimum wage was cut by 12.5% and unemployment benefits by €750 m. Importantly, “the deal did not involve any change to Ireland’s jealously-guarded 12.5% corporate tax rate” preferred by the conservative elites (Strupczewski and Toyer Citation2010). Vice versa, the first thing the progressive government did in 2012 was to reverse the cut in the minimum wage, reduce the proportion of the consolidation taken by cuts, and increase targeted taxes. It is also noteworthy that, while the Irish MoUs were written under duress, some reports indicate that the interactions with the institutions were mixed. In the words of the chief economist with the Irish Congress of Trade Unions, Paul Sweeney (Citation2015) “the IMF was substantially easier and more open to deal with than the Commission and the ECB”. But even then, the EU institutions allowed the new Irish government to obtain major renegotiations that steered policies in new directions. Whilst these were not necessarily seen as a success by the public, tweaks to conditional reforms left a partisan mark and relieved in part the public servants from major pressure (Sweeney Citation2015).

Our theory sheds light on both these case studies. Furthermore, it suggests that, in case of more neutral/centrist governments and keeping everything else constant, the mix of bargained conditions was possibly more balanced. This is the case of the early stages of the Hungarian bailout negotiations, for example. Finding itself on the verge of financial collapse, in 2009 the non-partisan caretaker administration of Gordon Bajnai turned to the European Union and the IMF to secure bailout funding. Hungary had many of the Greek and Irish features: whereas the fiscal statistics of the country were off the charts (like in Greece), the radical financial reforms during the early 2000s set in motion an unseen private credit-boom bust cycle amidst weak fiscal fundamentals (like in Ireland). Our theory would suggest that, against this background and in light of the (non) partisan nature of the government, a mix of financial reforms and labor market reforms would have been needed to revive the Hungarian economy. This is what we find in the data—namely a relative balance of conditions on different issue spaces.Footnote10

Note that the role of partisan governments described in these cases and denoted in our theory does not hinge on the imminence of elections. In fact, our theory is based on the assumption that at the moment of the bailout negotiations, a domestic government is fully in power and committed to enact the negotiated reforms in a credible shadow of the future. Clearly, this assumption is weak if incumbents are expected to run an election not too far from the time of a bailout negotiation. Furthermore and perhaps more importantly, unexpected government crises and unscheduled elections may undermine this assumption. Public opinion may shift swiftly during a financial crisis, governments can easily lose a confidence vote, and in non-cyclical elections voters may choose a given party because that party promises to deal with a given sector (e.g., the financial sector or the public sector) to regain economic confidence. In that case, it perhaps makes no sense for international lenders to discuss that sector as part of the package to begin with, and the distinction between the packages demanded from left vs. right leaning governments may have little to do with the logic of IFI acceptance proposed here. Our theory does not address this potential source of reverse causality (nor does our formal model). But while we cannot a priori exclude these alternative explanations, our empirical analyses can account for the effect of drivers of public opinion that may affect voters’ choices in cyclical elections as well the effect of non-cyclical elections. We can control for significant public mood changes as well as de facto unexpected elections that might undermine the credibility of a party negotiating bailout terms, assuming it may be out of government in the future. Presumably, there may be no substantive differences between partisan types of bailout reforms on the onset of these events. However, if we were to find different levels of financial and public reforms exist following these events, then our theory would still have relevance. We tackle these and other potential empirical questions in the analyses below.

Research Design

We test the implications of our theoretical argument with a statistical analysis based on originally collected data. In this section we introduce the new dataset and the variables used to perform the analysis. We then discuss the findings from our econometric models.

Dataset and Variables

Our argument suggests that the ideology of a European government, be it right or left, influenced the type of conditional policies agreed in the EU rescue programmes. We conjecture that, everything else constant, European governments were able to strike conditions that would impose more reforms on the policy domains of their ideological opposition. It is fair to note that some important characteristics varied across the observed bailout countries. For instance, our countries had different trade deficits and debts, and scholars have noted that these characteristics determine bailout vulnerability (Walter, Ray, and Redeker Citation2020). Similarly and as highlighted in the previous section, the observed governments had various forms of partisan bases, and in some of them coalitions were more likely than in others (Armingeon, Guthmann, and Weisstanner Citation2016). While we recognize these caveats, we nevertheless rely on the scholarship that underscores how left and right parties behaved differently policy-wise in the course of the Eurocrisis (Hübscher Citation2016). Accordingly, both sides of the ideological spectrum tried to protect core groups of voters in the course of the crisis years (Afonso and Bulfone Citation2019) and thus, presumably, when interacting with the Troika.

Consequently, we expect that right-wing governments negotiated relatively fewer conditions in economic policies directed to private financial sectors: for example, regulations of financial activities, tighter banking supervision, and corrective actions in the banking sector (Claessense, Demirguc-Kunt, and Huizinga Citation2001; Woo Citation2013). By contrast, right-wing governments stipulated relatively more conditions traditionally rejected by the left, such as reduction of public spending and the liberalization of public sector labour markets (Caraway, Rickard, and Anner Citation2012; Gunaydin Citation2018). Seeking to test this conjecture, we collected data that measure the multiple types of bailout conditions settled across the continent during the Eurocrisis.

Our unit of analysis is country-quarters. Our time unit is quarters for two reasons. First, bailouts are usually quarterly reviewed and potentially renegotiated on a quarter premise. The MoUs mention quarters themselves (e.g., actions to be completed by the end of Q1 in Ireland, or end of April/end of December in Romania). Additionally, we have refined information at the quarterly level for the bailout negotiation decisions, executive partisanship and other relevant macroeconomic variables. We collected information for all quarters between the beginning of 2008, which corresponded to the beginning of the global crisis, and the end of 2015, when the data collection concluded. The dataset includes all relevant EU bailout programmes; it truncates on the last Greek rescue package, but it includes information on the Greek executive reshuffles in the last quarter of 2015 and the beginning of the third bailout round of negotiations. The dataset contains all eight EU countries rescued by the Troika, for a total of 30 observations per case. refers to the relevant bailout negotiations, their timeline, and the scale of the targeted funds.Footnote11

Table 1. EU bailouts.

Our main outcome variables capture different types of bailout conditions. We distinguish these by the main policy domains belonging to right and left governments. Following classical literature on issue ownership and partisan policy making (Alesina and Roubini Citation1992; Hicks and Swank Citation1992), we expect left-wing governments to prefer policies that increase government spending and induce growth in the public sector. By contrast, we expect right ones to favour policies that induce lower spending and more balanced budgets in favour of private sector development. We keep a distinction between “financial sector” measures and “public sector labour” measures to represent the more right- and left-oriented domains, respectively. The distinction between these mutually exclusive sets of conditionality measures is simple but is used in the relevant literature (Dreher and Jensen Citation2007). We therefore construct two separate outcome variables: Financial Sector Conditions and Public Sector Labour Conditions. These variables are a count of all the conditions that fall into each type.Footnote12 In the Appendix, we report illustrative examples of the reforms that we code for each of these two variables, respectively (Table A.1). Some reforms can be envisioned as policies of right wing governments and vice versa. Interestingly, while some financial reforms seem to naturally represent conservative free market policies (e.g., in terms of expected volumes of capital injection in the banking sector and banking liberalization), others seem reasonably acceptable for left governments (e.g., Romania’s 2012–2013 schedule of national inspections of private banks).

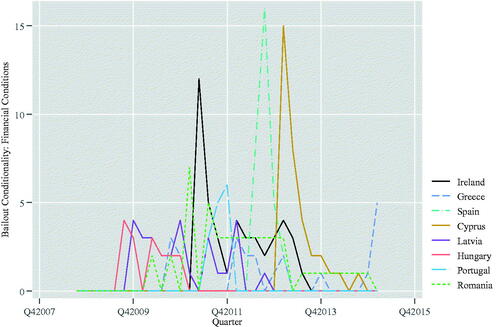

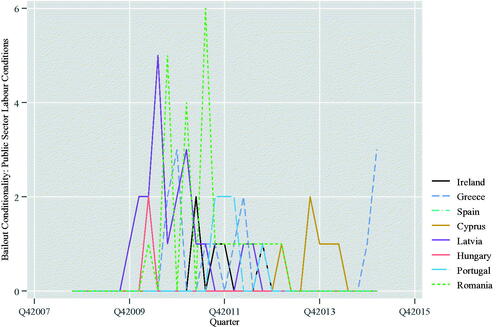

To collect data for these outcome variables, we retrieved all published texts of the bailout agreements.Footnote13 All the conditions the crisis country agreed to take on each given yearly quarter were added together, so to construct non-negative count variables. For Financial Sector Conditions, we identified policies such as financial sector surveillance, banks restructuring and banking regulations. For Public Sector Labour Conditions, we identified policies such as wage freezes and pension reforms. and show the agreed reforms across countries for the period from the first quarter of 2008 to the first quarter of 2015. The figures indicate that the policy reforms observed in the MoUs regard more the financial sector than anything else. A given quarter of any country in the sample has on average one financial measure, and some countries (e.g., Cyprus and Greece) reached up to 16 such measures in one single quarter. However, a substantive amount of conditions regard public sector labour reforms, with some countries (e.g., Romania) reaching up to 6 such measures at one point in time. According to our coding, when there is no ongoing bailout or the bailout schedules no measures for a particular quarter, this variable adopts the value of 0.Footnote14

Figure 1. Financial conditions across countries and time.

Figure 2. Public sector labour conditions across countries and time.

Our empirical test concentrates on the finance-oriented and public sector labour conditions, with the expectation that right and left EU governments would negotiate less of these respective types of measures. However, we also collected information on other measures, which we use to gauge with more precision whether our results are indeed driven by our theoretical expectations. Specifically, we generated a Bailout Conditionality Sum variable, which aggregates all the conditions listed in each MoU without any issue-specific distinction. Additionally, we created the Other (Non-Public) Labour Conditions variable that collects more technical issues related to specific, non public jobs (these are, for example, quotas on specific licenses for general practitioners). These variables are described in . We present these results for the purposes of further corroborating our main findings.

Table 2. Variables summary.

To get at the heart of our argument, we exploit Government Partisanship as our main explanatory variable. There are, of course, several possible ways to conceptualize and compute the partisanship of any given government. Here, we seek to measure the partisan inclination (or “balance”) of the executive on the premise of each party included in government, in order to capture ideological nuances that exist in multi-party, coalition-based European governments (Bulfone and Tassinari Citation2021). Our measure is generated via ParlGov (Döring, Constantin, and Manow Citation2022), a cabinet-party database containing Chapel Hill Expert Surveys Series (CHESS) data, and public information about institutional seats (Döring and Manow Citation2017).Footnote15 This database scales the ideology for each party and counts the number of seats of each party on the national Parliament. We then followed a two-step procedure. In the first step, we computed the total number of seats of each party in a given cabinet over the total number of parliamentary seats of the cabinet; we then multiplied this quantity by the ideology of each party in the government coalition according to the CHESS scale. In the second step, we averaged the values obtained in the first step over all parties in a given cabinet in a country-year. The analytic formulation of our two-step procedure is as follows: first, for each party (p) in the government (g), we computed

(1)

(1)

and then, we obtained our final measure of government partisanship by computing

(2)

(2)

where

indicates the number of parties in the government. In doing so, we generated a weighted average of each cabinet ideology that ranges from 1.1 to 8.4, with an average of 5.4 (and a median of 5.6). On this scale, the lowest values indicate a remarkably left-wing ideology (e.g., Cyprus’s AKEL experience) while the highest values indicate a clear-cut right-wing ideology (e.g., Spain’s People’s Party government). Given the regular update to the underlying data, the measure captures ideological changes occurring throughout the quarters under analysis.

Our measure combines the ideological direction of each party in the government with its relative institutional weight, thus providing a distinct and refined measure of government partisan inclination. Obviously, there are other possible ways to capture the partisanship of any given government. For example, it would be possible to assume that the ideology of a government is simply the ideology of its largest party (or the ideology of the party the president belongs to), or that each party in cabinet has the same weight, so that the cabinet ideology is the non-weighted average ideology of all its parties. There is one additional approach that differs from ours: namely, to weigh each party according to the number of ministries each of them has. But while equating the ideology of the cabinet with that of its main party would certainly work well for single-party governments, it would not for multi-party ones. We believe so because making such an assumption boils down to accepting that the main party in government can pursue its preferred policy despite the other members in the governing coalition. This, in our view, is an assumption that does not often match reality: if they have the votes, parties will govern by themselves; and smaller parties do not enter the government unless they can influence policy outcomes. Hence, we consider the ideology of all parties in the government.Footnote16

Besides these measures, our statistical models are estimated using a set of control variables that capture the state of the Eurocrisis and the domestic macroeconomic conditions (see ). Given the central role that debt played in the politics of the European recession (Genovese and Schneider Citation2020), we control for Public Debt as a percentage of GDP, which is defined as the quarterly general government consolidated gross debt as a percentage of national income. Current accounts have also played a key role when defining bailout conditionality (Walter, Ray, and Redeker Citation2020). Hence, Balance of Payments is defined as the quarterly balance of payments as a percentage of GDP. We also control for countries’ risk premium, to capture the additional margin that creditors demand for a risky bond in comparison to a neutral-risk bond, like the German one. Along these lines, the variable Sovereign Interest Rate is the quarterly ten years bonds interest rate. All the macroeconomic variables are gathered from Eurostat, and are first differenced to control for the change of macroeconomic conditions in the past. Concentrating on the short-time change (first difference) of the macroeconomic control variables not only makes for a parsimonious model but is also warranted because in the unfolding of the bailout negotiations, the changing state of the financial crisis seemed to be crucial. However, it is also true that differences in trade deficits and debt levels may have influenced the outset of the negotiations and the terms of necessary bailouts. As we describe below, we address this type of time-sticky heterogeneity by estimating fixed effects and clustering errors at the country level. Nonetheless, alternative models show that including the absolute levels of the macroeconomic variables and running more general dynamic models does not affect the estimates of government partisanship (Table A.16 in the Appendix).

In addition to the level differences, in other models we also considered alternative relevant variables. For example, we coded the timing of presidential and parliamentary elections as well as the inclusion of partisan (versus independent) finance ministers in the cabinet. Our main models exclude these indicators, since EU bailout talks were systematically delayed or halted whenever national elections were approaching,Footnote17 but alternative models in the Appendix estimate variables that may underline public voters’ moods. The changes in cabinet composition are inherently included in the transformations to our partisanship index that we investigate in additional analyses, but below we also discuss the implications of non-cyclical elections.

Specification

Our outcomes are non-negative count variables with an excess of zeroes and over-dispersion.Footnote18 While in alternative estimations we focus only on the onset of conditions, we retain the whole series of observations for our main analyses. In our main models, we choose to estimate a zero-inflated negative binomial (ZINB) regression, which assumes that there are two different data generating processes for the zeroes. Specifically, it is assumed that there is a majority of zeroes generated by the fact that there was no bailout going on; but there is also a smaller set of zeroes generated because some bailout package entailed no measures for a certain period. Our ZINB models then estimate a regression with two separate stages, similarly to other two-step models in this literature (Reinsberg, Kentikelenis, and Stubbs Citation2021): one is a logit model that explains if a count is a true zero or otherwise, and the other is a negative binomial that predicts the value of the count when the count is not a true zero. In the first stage model we include a dummy that captures the occurrence of a bailout and a constant to predict the true zeroes.

A frequent challenge with our type of panel data is unobserved time-persistent unit heterogeneity, which emerges when the outcome variable exhibits group-level variation beyond what can be explained by the covariates alone. This heterogeneity is modelled here using fixed effects, which also control for the different characteristics of each of the eight sampled countries.Footnote19 Additionally, while it may be reasonable to assume that governments and the Troika have good forecasting capacities, we lag our covariates. Specifically, we lag all the macroeconomic covariates by four quarters (one year), because we expect policy preferences to take a while to emerge and move away (if at all) from the status quo, which the literature usually takes as last year’s policy. By contrast, the government partisanship is lagged two quarters (half year), because we believe that the partisanship of the bargaining government—and not of future governments—principally affects the final agreement.Footnote20 Lagging also helps with addressing the strict exogeneity assumption behind our estimators. In their original form, our macroeconomic covariates—and especially public debt and the sovereign interest rate—fail this assumption. However, a Wooldridge test with the lagged covariates suggests that none is endogenous at the 10% level. We further differentiate the lagged macroeconomic covariates to make them stationary and avoid unit roots. The first differences of the lagged macroeconomic variables seem appropriate if the recent change of the economy matters for governments’ bargaining positions.Footnote21

Our ZINB estimations incorporate linear and a quadratic time trends for any unaccounted time dynamics. We cluster the standard errors on the country level, but alternative estimations that cluster the errors on the time variable do not alter the interpretation of the findings.

Analyses

Main Results

Our goal is to estimate if left- and right-leaning governments in European bailout countries were able to settle on more bailout conditions that belonged to the policy area of their opponents, hence de facto burdening interests outside of their voters’ group. Before running the regression models, we first descriptively investigated if the total number of conditions in European bailouts varied across different partisan governments—to check whether the driving form of variation in our data is the total sum of conditions. We coded each recipient country-quarter observation as either “left” or “right,” based on whether the partisanship score of a country in that quarter is less than the average value in the sample (5.4). Then, we ran a difference-in-means t-test to assess whether the average number of total conditions imposed to left country-quarter observations is larger than that imposed to right ones. On average left-wing recipient country-quarter are imposed 0.86 more conditions than right-wing ones, but this difference is not statistically significant (p-value = 0.64). So, left governments do not seem to be imposed more conditions than right ones, at least not unconditionally. This is important given that the literature on conditionality (in developing countries) has suggested that right governments often receive fewer conditions than left governments. It also suggests that at the bailout negotiations there were degrees of freedom and flexibility over policy, as assumed by our theory.

Based on this premise, we move to our econometric estimations. Our main regression results are presented in . Each column in the table presents the estimations for a model where the dependent variable is noted on top. The first column refers to a model of Financial Sector Conditions, while the second one refers to a model of Public Sector Labour Conditions. For each of the two outcome variables, the models include a linear and a quadratic time spline, as well as country fixed effects. We find that the first differenced macroeconomic variables have weak effects; only debt and balance of payments have a stable positive correlation with the public sector labour conditions—a result consistent with other findings about the politics of the Eurocrisis (Walter, Ray, and Redeker Citation2020). Importantly, we find that Government Partisanship has an effect on conditionality in line with our expectations. The variable estimates are negative and statistically significant for the finance sector conditions, and positive and statistically significant for the public sector labour conditions. This means that a right government is less likely to receive conditions related to the realm of private elites, capital banks, and other domestic actors closer to their policy agenda. By contrast, a left government is less likely to agree on conditions closer to their more salient interest groups, namely workers in the public sector.

Table 3. The effect of government partisanship on EU bailout conditions.

The parameter estimates indicate that the model predicts a substantive portion of the outcomes (i.e., whether or not a country is a certain zero). The dispersion parameter also suggests that the model is properly specified. In terms of meaningfulness, there are multiple ways to estimate the substantive effects of these models. By exponentiating the ZINB coefficients we estimate that, if a country were to become more right wing by one scale point, the expected number of financial conditions would decrease by a factor of circa 0.8 while holding all other variables constant. And vice versa, the expected number of public sector labour conditions would increase by a factor of 0.9. A unit change to the right on the partisanship scale corresponds roughly to the change Hungary went through with the 2014 elections (it went from a value of 5.6, close to the sample average, to a value of 6.6). In those elections, Viktor Orban’s Fidesz party managed to secure a larger majority in the parliament thanks to an electoral reform designed by Fidesz itself. Negative binomial estimates expect a change of this type to decrease, on average, the number of financial conditions by about 1. The effect size is thus about half of a standard deviation for this dependent variable (see ).

The estimates also expect an increment of 1 unit on the partisanship scale to increase, on average, the number of labour conditions by about 0.9. The effect is almost the size of one standard deviation for this dependent variable. Thus, the effect of partisanship (moving to the right) appears larger on labour conditions than on financial conditions when considering the distributions of the two dependent variables.

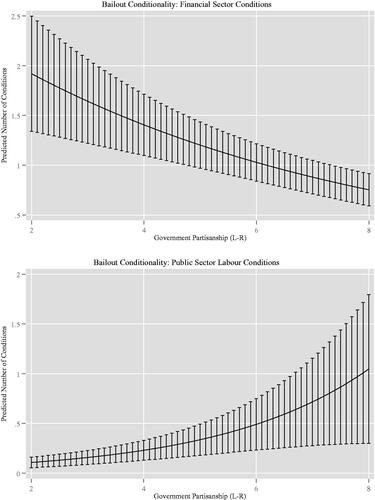

Furthermore, to illustrate the range of effects across the government partisanship spectrum, reports the predicted effects calculated for the varying values of Government Partisanship based respectively on Model 1 and Model 2, keeping the other variables at the mean. The top plot shows that moving from a left toward a right ideology halves the probability of financial sector conditions. By contrast, the bottom plot suggests that moving from the left toward the right almost doubles public sector conditions, though the uncertainty increases at higher values of the partisanship indicator.

Figure 3. The effect of government partisanship on bailout financial sector conditions. These plots report the predicted number of conditions as Government Partisanship goes from low to high values. The estimations of the predictions (solid line) are based on Model 1 and Model 2 in . The bars report 95% confidence intervals.

The results are largely in line with our theoretical claim, but do these partisanship findings reflect the mechanism in the theory, or does partisanship also correlate with other bailout conditionality metrics? Do the results veil the likelihood of left or right governments to strike more conditions or more technical bailouts? To respond to these concerns, we ran additional models where we analyse our additional conditionality measures: namely, Sum of All Conditions and Other (Non-Public Sector) Labour Conditions. Columns 3 and 4 in report the results. With regards to the sum of all conditions, we find that, while right governments seem to receive fewer conditions than left governments on average, the negative coefficients of partisanship are not significant. Similarly, right governments seem to agree on more technical labour issues, but this pattern is not statistically significant. In these estimations, the macroeconomic variables seem more relevant at explaining the conditionality measures in the bailout accords, as some literature has suggested (Mosley, Harrigan, and Toye Citation1995). Quite remarkably, these results are consistent with our underlying theory that negotiating governments would convince the Troika to place a strong focus on the most salient partisan politics driving government ideology—or, in fact, their opponents.

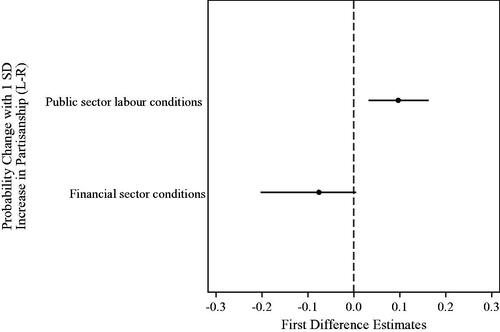

All observations, including those without Memoranda of Understanding (MoU), are used in our main analysis. However, excluding observations without MoU may be equally adequate, because it is when MoUs are decided when real negotiations are taking place, opening up the room for partisan effects. Hence, in , we report two other sets of models of the main dependent variables of interest (i.e., financial sector and public sector labour conditions). Columns 1 and 2 are naive ZINB models for the data subsample without ongoing bailouts. Columns 3 and 4 are Poisson models for a subsample of all observations with at least one condition. The first two models essentially replicate the results in , once again suggesting that the specification of the original model is justified and that ZINB models perform well in the prediction of the zeros. The latter models are also informative, because they suggest that the effects of the change of government partisanship on the left-to-right scale are not only an artefact of going from zero to one condition, but rather a function of the distribution of conditions. The Poisson models are also helpful to calculate substantive effects by allowing the calculation of first differences via simulation. Along these lines, we perform 1,000 draws from a multivariate distribution based on models 3 and 4 in , and calculate the quantities reported in . The graph shows that one standard deviation change of government partisanship (which is common in our dataset) increases conditions by about 0.1 for both categories of reforms. This is a meaningful quantity, especially for the public sector labour conditions, as the maximum value of this variable in our sample is 6.

Figure 4. Substantive effects for changes in government partisanship (from the mean to one standard deviation above the mean) on bailout conditions. The two dots refer to the substantive effects (first differences) estimated for the two models of Financial Sector Conditions and Public Sector Labour Conditions, respectively, based on 1,000 simulation draws with estimates of Models 3 and 4 in as specifications. Error bars indicate 83% confidence intervals, which show that the two mean effects are significantly different from each other.

Table 4. The effect of government partisanship: alternative specifications.

Robustness

Our findings are robust to a number of additional tests. In the Appendix, we show that the results hold if we cluster errors at the quarter level instead of the country level (Table A.2). The results remain also statistically consistent with our theoretical findings if we estimate linear models that ignore the structure of the zeros (Table A.3) or if we run population-averaged panel models for overdispersed outcome variables instead (Table A.4).

We ensure that the results are not sensitive to the time lags chosen for our main regression equation. Specifying one instead of two quarter lags for our government partisanship weakens the magnitude of the effects (as expected) but overall does not change the direction of our main results (see Table A.5 in the Appendix). We also estimated our models using a twice-lagged version of the macroeconomic control variables (Table A.6) and substituting one of the core macroeconomic variables—debt—with a more fine-grained IMF measure of government indebtedness toward the domestic financial sector (Table A.7). Across these alternative models, the coefficients of the partisanship variable are substantively the same in terms of size and magnitude, and the statistical significance is overall confirmed

To prove that our results are not merely driven by the construction of the main explanatory variables, in additional analyses reported in the Appendix (Table A.8) we exploit the three-level indicator for executive ideology from the 2017 version of the Database of Political Institutions (Scartascini, Cruz, and Keefer Citation2018). These models confirm the results of our main estimations, which however use a more refined and weighted measure of ideology. One may also be concerned with the fact that our sample includes two countries—namely, Romania and Hungary—that do not belong to the European Monetary Union (EMU), and which may not concern IFIs with the same pressure that Eurozone countries did. The non-EMU countries may place less relevance to Euro politics and approach bailouts differently, also because they have different (more) policy levers to implement reforms. In alternative estimations (Table A.9), we drop these two non-EMU countries. The results remain largely confirmed, and in fact are even stronger than those reported in the main findings.

We previously discussed the potential concerns with the possibility that election mechanisms may get in the way of the logic presented in the paper. Our executive partisanship measure de facto integrates information about cabinet changes and potential voting reshuffling; however, it is possible that voters’ moods before an election may already affect bailout negotiations. In order to investigate these dynamics, we focus on the yearly trends in labor mobilization (as captured by the percentage of trade union density rate) to measure concerns of public sector security that may stimulate left votes, and trends of incoming foreign investment (as GDP percentage) to measure concerns with capital inflows that may trigger right votes. The former measure comes from the ILO (we complemented this with OECD for Hungary 2013, which is missing from the ILO). The latter measures come from the World Bank. The models that control for these two variables are reported in Table A.10 in the Appendix. The negative and positive effect of government partisanship on financial and public sector conditions is statistically significant.

In a similar vain, there is a possibility that unemployment drove some form of labour and market frictions and influenced the crisis severity in the EU context. To control for unemployment, we retrieved the quarterly rates from the Eurostat dataset, as well as the yearly public sector and youth unemployment rate statistics (which we then spread across the quarters). The results that control for these measures are in the Appendix (Table A.11). The statistical effect and significance of government partisanship remain unaltered by these additional control variables.

What about the effect of a sudden replacement of the prime minister or, more generally, non-cyclical elections and unexpected government turnovers? To explore these questions, we ran two robustness checks controlling with a binary variable coding whether the government changed in a country-quarter and, separately, whether the government changed unexpectedly (i.e., outside cyclical elections, for example when heads of governments resigned from office or failed in receiving a vote of confidence from parliament; in our dataframe, we identify 13 unexpected government turnovers). When running the regression models using the lagged turnover variables, we find that the results are robust for all models, as we show in the Appendix (Table A.12).

We also explore if our logic of partisanship effects on bailout negotiations in the EU entails that more homogenous/stable cabinets are better able to achieve reforms in line with their political interest. While our original measure weighs a government’s ideology by a party’s representational magnitude in parliament, it may be possible that ideology may be more directly connected to the cabinet members. So, in divided or more ideologically heterogeneous cabinets, members of the opposing ideology may sometimes block such reforms, and bailout negotiations may get messier at the mercy of IFIs. In the Appendix, we show models that cluster errors around cabinets. The results reported in Table A.13 are overall consistent with our main findings.

Furthermore, in Table A.14, we report additional regressions of the financial sector and labour public sector conditions that substitute our main government partisanship indicators with a Cabinet Composition (Schmidt Index) measure retrieved from the Quality of Government (QoG) database.Footnote22 Overall, we find that there is some truth to the idea that cabinet composition, and specifically the clear-cut dominance of a party wing, motivates more scapegoating techniques and therefore more opponents’ policies in bailouts, especially with respect to financial conditions.

Along similar lines, we consider the party ideology of the finance ministry, which is often in charge of IFI negotiations. Data from the partisan identification of the minister comes from the WhoGov dataset Nyrup, Jacob and Stuart Bramwell. Citation2020.Footnote23 The relevant variable is rescaled so that it takes the value of –1 for left, 0 for independent, and 1 for right party identification. We find that a ministry of finance that is right-wing decreases the volume of financial sector conditions, and that controlling for this reduces the significance of the effect of the partisanship of government. However, given that right-wing governments tend to have right-wing finance ministries, this result implies that any variation to right cabinet composition matters little for the purpose of financial sector conditions because that partisan signal is already captured by the ministry of finance. Importantly, we also find that even controlling for the orientation of the ministry of finance does not affect the direction and significance of government partisanship for the public sector labour conditions: while having a right finance minister decreases the likelihood of conditions in the public sector, right cabinets still strike more public sector labour conditions than left cabinets. These results (reported in Table A.15) confirm the credibility of our argument: right cabinets negotiating with the Troika used the negotiations as a scapegoat mechanism.