Abstract

The literature on financial market design is predicated on the efficient market hypothesis (EMH), advocating transparency, liquidity and universal information with a view to capturing efficient prices. We provide a counterfactual: the 1995 formation of AIM, the London Stock Exchange’s junior market. AIM employs an alternative mode of market organization based on market imperfections. Our empirical study shows how AIM draws on reputation, social relationships and practitioner knowledge to organize market governance. We argue that the market’s design should be understood as capable of producing informationally efficient prices. We characterize AIM as having a ‘Whitean’ structure, compared with the ‘Fama’ structure of main markets. We conclude that the ‘Whitean’ producer market is a viable design option for financial markets.

1. Introduction

From its inception, the science and technology studies inflected analysis of markets – the study of ‘marketization’ (Çalışkan & Callon, Citation2010), the ‘new, new economic sociology’ (McFall & Ossandón, Citation2014), or simply ‘market studies’ (Roscoe & Loza, Citation2019) – has emphasized the performative construction of dispassionate, economized market relationships as a precondition for economic transaction, a process of ‘framing and disentangling’ (Callon, Citation1998) epitomized by the transformation of the strawberry market of Fontaines-en-Sologne (Garcia-Parpet, Citation2007). More recently, however, scholars have turned their attention to the role of entanglements in organizing market transactions (Deville, Citation2012; McFall et al., Citation2017). They see consumption and production sitting in a dialectical relation, bound by material and affective attachments, where market designers (and marketers) work to create new entanglements: social, technical, emotional, legal, sentimental and practical. Within the context of finance, the theoretical domain of the ‘social studies of finance’ (MacKenzie, Citation2009) scholarship has followed a similar trajectory, emphasizing first of all the performative nature of economic thought (MacKenzie, Citation2006a; MacKenzie & Millo, Citation2003) and more recently the role of affect and attachment in the mutual construction and qualification of financial services, goods and valuations (Muniesa et al., Citation2017; Vargha, Citation2011).

There is an intriguing link between these theoretical positions and the practical problem of organizing financial markets. On the one hand, we see a dominant conception of how financial markets ‘should’ work, a highly performative financial system based upon the eradication of social structures in markets (Castelle et al., Citation2016; Lee, Citation2011). We term this organizational conception a ‘Fama’ structure following Fama’s (Citation1970, Citation1991) ‘efficient market hypothesis’. On the other, we see the emergence of different mechanisms of organizing financial markets, following the structures established in producer markets. We term these a ‘Whitean’ structure after White’s (Citation1981, Citation2002) account of the organization of markets by reflexively aware participants. Both mechanisms pursue informational efficiency as a dominant design parameter: by informational efficiency, we mean that market participants can rely upon available information as a reasonable approximation of the state of investee companies, and that this is reflected in prices, an admittedly pragmatic definition. While the former arrangement – the Fama structure and variations – have been extensively theorized (see the contributions in Knorr Cetina & Preda, Citation2012), the latter has received much less attention. The omission is all the more striking for, as Castelle et al. (Citation2016, p. 169) note, ‘the exchange is a site which has aspects of both fixed-role markets – i.e. multiple exchanges may compete to provide trading services for brokers and dealers – and switch-role markets: i.e. the familiar, furious “trading floor”-style buying and selling of shares’. Exchanges exist as rivals in a Whitean market for the provision of Fama markets. The proliferation of the ‘Fama’ model in a product market for financial services suggests that it appeals as part of the business proposition of main board exchanges. This begs a question: would a more ‘Fama’ exchange outcompete a less ‘Fama’ exchange, in the sense of attracting more and higher quality investors and firms? We suggest that this may not be the case.

We illustrate our claim with an empirical analysis of the organization of the Alternative Investment Market (AIM) the London Stock Exchange’s (LSE) second market, founded in 1995 as a venue for higher-risk, smaller or growing businesses. We show how attachments – social bonds, reputation and esteem – have been fashioned into the regulatory backbone of a new genre of financial market that flourished internationally in the first decade of the new millennium (Mallin & Ow-Yong, Citation2013; Mendoza, Citation2008; Posner, Citation2009). We argue that AIM’s structure offers an effective mechanism for an informationally efficient market. In doing so, we offer an account of the importance of imperfections in market design as generative, rather than problematic, mechanisms.

1.1. Two visions of market governance at the London Stock Exchange

The LSE’s main market, the ‘Official List’, is able to trace its history back to the seventeenth century. Listing requirements are strict, and the LSE itself is responsible for the quality of new arrivals and the maintenance of a fair, informationally efficient market for securities. It does this using a mixture of external (national and trans-national) regulation and internal (private) regulation in pursuit of a ‘Fama’ structure. In regulatory terms, an extensive framework operating under the Financial Conduct Authority, the Prudential Regulatory Authority and the LSE’s own rulebook, is organized around certain key principles, notably transparent dealing and settlement, investor protection and competitive trading practices (Lee, Citation2011; Sanusi, Citation2018). This is underpinned by a principle of equal access to information – at least for those who pay appropriate fees (Davis, Citation2006; Sanusi, Citation2018). Full disclosure of trading information is mandated by the Exchange, and is provided by proprietary technological systems (Sanusi, Citation2018). In theoretical terms, as Lee (Citation2011) notes, the provision of competitive trading, clearing and settlement services should obviate the need for regulatory intervention in market infrastructures to promote efficiency. Fama-style organization is hardwired into the material structures of the Exchange: electronic networks disseminate prices instantly and on a continuous basis, while electronic order books, a fixture of the main market since the late 1990s, automate a continuous auction among anonymous participants (Pardo-Guerra, Citation2019).

AIM, on the other hand, enjoys lighter listing requirements, and is governed by a system of private regulation, with supervision delegated to Nominated Advisors or Nomads. Finance scholars disagree as to the effectiveness of this structure. Hornock’s (Citation2015) survey of the literature finds wide ranging estimates of underperformance (for example 28.6 per cent to 33.5 per cent over two years) and a strong association between capital raising and poor performance. As he notes, this is problematic for retail investors who are often only able to buy into AIM firms at IPO; Gerakos et al. (Citation2013) also find that unsophisticated retail investors are particularly exposed to poor performance. These effects are felt even in the strongest sectors: during the property boom from 2005 to 2015, AIM listed property stocks underperformed their counterparts on the Official List (Newell & Marzuki, Citation2018).

There is also widespread consensus that far fewer firms move to the main market than one might expect, particularly in view of the stated purpose of AIM as a nursery for growing companies (Jenkinson & Ramadorai, Citation2013; Revest & Sapio, Citation2016b). Jenkinson and Ramadorai (Citation2013) found that over the period 1996–2006 only 56 of approximately 1,600 firms made the move upwards, less than a quarter of the number moving from the main market to AIM. In fact, traffic flowed in the other direction: ‘upward’ movement decreased across the period whereas ‘downward’ movement increased. Importantly, moving ‘down’ to AIM does not lead to a long term decrease in shareholder returns, as might be expected if poor performance was the cause of the move. Jenkinson and Ramadorai explain this in terms of the different regulatory costs of the two markets as the trading technology and the framework of UK law are the same for both. They speculate that firms may have different regulatory preferences, based on costs.

From the perspective of issue numbers and capital raised, however, AIM has been a great success: the market has hosted a total of 3,929 companies, raising £124 billion.Footnote1 Nielsson (Citation2013, p. 336) proposes that high quality firms may choose to list in less regulated markets, and that a network of analysts, institutional investors, auditors, investment banks and the media may provide an ‘alternative bonding device’ to legal regulation. Vismara et al. (Citation2012) highlight the ability of companies listing on these markets to raise capital through IPO and to do so again through secondary or ‘seasoned’ offerings; AIM has contributed to the creation of new firms, particularly in sectors where larger sums of capital have already been raised (Revest & Sapio, Citation2016a). AIM ‘allows small companies to gradually mature in a public market environment’ until they are ready to move to a full listing (Hornock, Citation2015, p. 347), and provides a showroom for entrepreneurs wishing to sell their companies (Revest & Sapio, Citation2016b). ‘AIM’, writes Mendoza (Citation2008, p. 287) succeeds because it ‘supplies a scarce product to the marketplace: rapid, low-cost access to public equity for small firms with high growth potential’. It answers an ongoing problem where financial regulators adopt a one size fits all strategy that imposes excessive costs on many market participants (Piotroski, Citation2013, p. 216). Stringham and Chen (Citation2012, p. 42) conclude that ‘AIM’s system shows flexible private regulation can serve firms and investors better than bureaucratic government regulation … Private regulators have an entirely different set of knowledge and incentives from those of government bureaucrats’.

These more positive accounts anticipate the claims of our sociological perspective. As informational efficiency emerges as the dominant design principle for financial markets, we show how the market’s structure draws on social relationships and practitioner knowledge to achieve this. Design choices were shaped by existing market relationships and practices as well as the institution’s strategic commitments and organizational path dependencies. In practical terms, the market’s regulation would seem fit-for-purpose; in theoretical terms, we suggest AIM’s ‘Whitean’ structure provides a counterfactual to the Fama market found on main-board exchanges.

The structure of the paper is as follows. In the next section, we examine the link between economic theory and the design of financial markets, with particular reference to market ‘efficiency’. We then turn in Section 3 to the analysis of social structure within financial markets and the relationship between social structure and informational efficiency. Section 4 outlines methods. Section 5 presents the empirical data on the AIM market. Section 6 discusses, while section 7 offers concluding thoughts on implications and wider issues.

2. Economic theory and financial markets

When Ronald Coase (Citation1988) described financial markets as examples of perfect competition he was describing the views of the economics profession, rather than the practice of markets. Paradoxically, as Coase also points out, the conditions of a perfect market require an authority structure to secure the market ‘involving an intricate system of rules and regulations’ to prevent malfeasance (Coase, Citation1988, p. 9). As many researchers in the sociology of finance tradition have noted, financial markets are deliberately designed structures (e.g. MacKenzie, Citation2009); the additional insight available from the Coase approach is that, once designed, these ‘market wrapped in a hierarchy’ devices must be regulated and maintained in order to avoid the emergence of market imperfections.

Since Coase (Citation1988) wrote, the number of financial exchanges has expanded substantially. There has been a growth in geographical coverage (Weber et al., Citation2009), and in specialization (for example, carbon futures exchanges). The vast majority of exchanges are firms, either publicly quoted – for example the London Stock Exchange is a firm whose stock is traded on the London main market – or privately owned (MacKenzie, Citation2017). It is now possible to speak of an exchange ‘industry’ in which competition, collaboration and mergers occur, a position underscored by the European ‘MiFID’ regulation, with its intention to create a market in markets (Lenglet & Mol, Citation2016). Empirically, Coase’s ‘market in a hierarchy’ description has been robust at an industry level.

Exchanges exist to bring together investors in and sellers of securities – for example firms in equity markets and governments in bond markets. They do so by building platforms that minimize the transaction costs of trades, maximize trading completion speeds and generate pools of liquidity so that trading can be continuous. There are huge network effects and exchanges seek to maximize order flow. Competition between exchanges may be on cost and speed, but also by differentiation, perhaps by specialization on specific securities, or by ease of listing. Revenues consist of fees for transactions clearing and settlement, membership fees for firms to be listed and, most importantly, charges for quote and price information (Lee, Citation1998). However, such information is not costless to produce, so the business models of financial market exchanges require that access to price information be restricted to a set of identified actors (Lee, Citation1998, pp. 46–67). There arises, therefore, a necessary tension between the commercial concerns of financial exchanges and the principles of perfect market organization on which they are based, namely anonymity, continuous auctions, homogeneous and standardized commodities, liquidity and effective enforcement (Garcia-Parpet, Citation2007). For financial markets, the core issue is price information, and the key theorists are Walras and Fama.

Walras provides the theoretical account underpinning notions ‘informational efficiency’ in markets. He proposed the existence of a notional auctioneer in a market who conducts continuous auctions around the price of commodities, adjusting the price to supply and demand (see Lee, Citation1998, pp. 216–217). Under Walrasian assumptions, there exists a unique market clearing price for each commodity and the price contains all relevant information such that agents in the market do not need to engage in costly search about either the underlying value of the commodity or the actions of other market participants. This Walrasian approach has been adapted by Fama (Citation1970, Citation1991) to financial markets in the ‘efficient markets hypothesis’ (EMH). For Fama, a market is efficient where prices fully and instantaneously reflect all available relevant information about a security.Footnote2 With such informational efficiency, prices thus become the key signals in capital allocation decisions so that informational efficiency yields allocative efficiency. Individual agents trade to maximize profits so, for example, if they have private positive information about a security, they will buy it and the private information becomes public by showing up in the price. Given that the current price should be the best estimate of the future price, prices in an efficient market should follow a random walk as unpredictable new information – a hot summer, perhaps, or a pandemic – influences prices. As Lee puts it:

Fama’s notion of efficient markets has come to underpin much regulation concerning the dissemination of price and quote information in financial markets … . Without the publication of prices and quotes … market participants will not have sufficient information to be adequately informed, that the prices of assets traded in the market will therefore not be informationally efficient and that allocative efficiency will therefore not obtain. (Citation1998, p. 222)

3. Social structure and efficiency

The most general points to make about the economic approach to financial markets are as follows. The Coaseian idea of a financial market as a perfect ‘market wrapped in a hierarchy’ rests on the strong assumption that the two forms of social structure can be kept separate. As Lee notes above, the hypothesis has been extremely influential in its impact on the design and regulation of exchanges. The interplay of social structure and regulatory form may here be characterized by the Granovetterian position, where markets are constructed as efficient and social structures emerge within them as mechanisms to protect individual market agents from downside risk or unexpected volatility. If social structures emerge in efficient markets they are likely to act in favour of market participants and against broader welfare issues (cf. Lee, Citation2011). Such structures will be diagnosed as imperfections to be regulated away. This logic characterizes Fama designed markets, including the LSE main market – indeed, Davis’s (Citation2006, p. 7) empirical study of price formation on the LSE shows exactly this tension, where ‘market regulations and metrological practices are as likely to develop as a response to actor-driven “cycles of opportunism and restraint” (Abolafia, Citation1996)’. It implies the primacy of external market regulation as a control mechanism.

Yet the EMH, if taken seriously, presents market operators with an intractable problem. It depends upon the existence of arbitrage, where mis-pricing can be traded away without risk. This could, for example, be a miscalculation of value or an arbitrage based on geographical and temporal difference, the favoured strategy of high-frequency traders. As Zuckerman (Citation2012) argues, this arbitrage is both central to the generation of informational efficiency and yet, by Fama’s own reasoning, highly unlikely. For if prices were informationally efficient, arbitrage would have very low returns to the arbitrageur, and it would be irrational to engage in it. If no market actor participates in arbitrageur activities, however, prices do not reflect value: ‘ … if all investors believe in the EMH, the market cannot be efficient’ (Zuckerman, Citation2012, p. 230, original emphasis). Market efficiency degrades into a collective action problem where, put colloquially, some of the people need to believe in efficient markets all of the time or all of the people some of the time, but not all of the people all of the time. Empirically, Willman et al. (Citation2001) and Roscoe (Citation2015) reach similar conclusions, arguing that traders in markets hold contradictory beliefs: that the EMH broadly works but that they can also beat the market. This overconfident trading on inadequate private information is noise, and efficient markets depend upon it (Black, Citation1986; Preda, Citation2017).

In practice, most financial markets solve the arbitrage problem through mechanisms of social structure: by defining a role of ‘market maker’ who performs the arbitrage role of buying when there is excess supply and selling when there is excess demand, transacting against the market. Willman et al. (Citation2006, p. 1362) point out that sociological research has been successful in theorizing the issue, with explanations centring on the interrelated processes of learning, information search, reciprocity and network building. The most substantial account of these roles is that of Abolafia (Citation1996), but his study resonates with other findings about the working of exchanges in the sociology of finance literature on both open outcry and electronic markets (see for example the collection on pp. 115–223 in Knorr Cetina & Preda, Citation2012): there appear to be formal and informal controls, conventions and norms and values other than self-interest in most financial markets.

Exchanges themselves have a dual social structure, serving two distinct purposes: as a locus of financial transactions (markets) and as a provider of exchange services (firms). As exchange ‘producers’ they provide a switch-role Fama market to buyers and sellers of securities, and occupy a fixed-role producer market (Aspers, Citation2007; Castelle et al., Citation2016) where the market’s basic organization stems from the producers’ mutual and reflexive awareness of themselves and their rivals. This latter was theorized by Harrison White, for whom ‘knowing oneself, and being known, to be in a given market is the single most important aspect of getting established in business’ (White, Citation2002, p. 121). For White, social structures emerge or are designed to provide a framework for specific sets of transactions between market participants. They help to organize the market per se, rather than subvert its operation; they provide economic benefits to market participants only to the extent that they do not jeopardize or undermine the social structure that constitutes the market.

To recap, economic theory of financial markets positions informational efficiency as the dominant design parameter for financial markets. The problem of noise, as theorized by sociological studies, makes clear that the structure that Fama suggests generates such efficiency – irrational arbitrage in an atomistic market – is neither logically or empirically possible in its pure form. Social structure becomes essential in the maintenance of market function. We may thus examine elements of social structure in terms of whether they facilitate, impede or are neutral with respect to informational efficiency, and more generally, the commercial positioning of exchanges as firms, specifically whether a more ‘Fama’ exchange might outcompete a less ‘Fama’ exchange.

4. Methodology

Data were collected as part of a larger project that sought to document, from a sociological perspective, the interconnected history of two stock-markets founded in London in the mid-1990s. One, AIM, is the subject of this paper. The other, OFEX (latterly PLUS), effectively ceased trading at the time of the financial crisis. Both emerged from the same milieu of regulatory and technological changes, as a result of the same strategic moves by the London Stock Exchange, and through the same social networks. Over a period of 18 months, from 2016 to 2017, the first author conducted 54 interviews with almost all of the major participants in the new markets (39 participants, totalling 73 hours). Many interviews were conducted on a named basis appropriate to the historical nature of the project. Interviewees are listed in Appendix. Interviews followed the pattern of career/life history (Yow, Citation2005), asking interviewees to recollect their entire careers in the financial sector (often from early apprenticeships on the floor of the old London Stock Exchange from which rich social networks arose). Interview data were supplemented by personal communications and informal conversations as well as textual sources, amounting to over 1,000 pages and included newspaper articles, company documents, prospectuses and annual reports, newsletters and lobbying materials, regulatory disclosures, press releases and marketing materials. Data were compiled into a narrative account of the formation of AIM. We also use previous published and unpublished work on the operation of the AIM market (Yu, Citation2010). Our data did not show interviewees discussing the merits of Fama versus Whitean markets; these are theoretical categories we have imposed on the analysis. Interviewees discussed emotive and effective notions such as trust, reputation, ‘good companies’ and ‘reliable management’, and relationships built up over decades. Equally, the administration of main board markets is couched in terms of efficiency, transparency and investor protection (cf. Lee, Citation2011).

5. Analysis: A market built from networks

Our premise is that exchanges must design some kind of governance mechanisms into their organizational structure to avoid malfeasance and promote informational efficiency, and that their choice of mechanism may be governed by the logics of competitive positioning within a market for exchange services. We focus on AIM as a market that has implemented – successfully – a distinctive kind of governance based on social ties. In this, we suggest, it has a Whitean structure rather than the idealized ‘Fama’ structure.

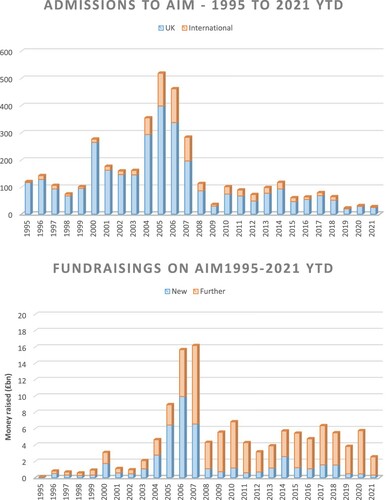

The stated intention of a junior market is to offer listing facilities to younger and smaller companies that could subsequently list on ‘main board’ exchanges. Despite increasing competition among global exchanges, AIM’s champions argue that it has established itself as the world’s leading stock market for companies with high growth potential (Arcot et al., Citation2007; Hornock, Citation2015). and show admissions and fundraising data from inception (1995) to the present. They make clear how AIM succeeded in both areas, particularly in the period from the end of the first dot-com boom in 2001 until 2008. The market is now smaller than in 2008, but fundraising activity remains strong. In 2018, approximately 950 companies were listed, with an average market capitalization of approximately £100 million; by 2021 the concentration of capital had increased, and 822 companies were listed with an aggregate value of £145bn.

Figure 1 Admission and fundraising activity on the AIM market

Source: LSE.

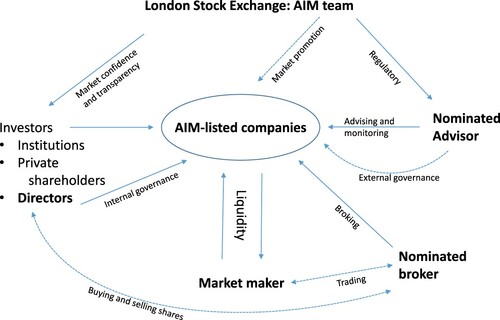

Figure 2 Key participants in the Alternative Investment Market

Source: Mallin and Ow-Yong (Citation1998).

AIM has also drawn international attention as an exemplar of market structure. Following the collapse of the dot-com bubble the AIM model gained popularity as growth-company exchanges spread across Europe and beyond (Mendoza, Citation2008; Posner, Citation2009). It has been replicated in Italy (AIM Italia) and Japan (Tokyo AIM) (Mallin & Ow-Yong, Citation2013).

As our review of the sociological literature made clear, the building of a ‘Fama’ market requires a sustained effort in removing social ties. AIM, on the other hand, made no such endeavour: it was built from social relationships from the outset. It was launched at a difficult moment in the Exchange’s history as the financial community pressured the LSE to rethink its closure of an earlier junior market, the Used Serviceable Material (USM) market. The Exchange’s management sought to placate the community, to position the LSE as a supporter of the nation’s entrepreneurial dynamism, especially in view of dissatisfaction with the role of banks and venture capital houses in funding small firms, and in doing so to make use of networks of regional stockbrokers and exchange members left behind after the closure of the UK’s regional bourses in 1973. It sought also to open the pockets of wealthy investors in Scotland, Northern Ireland and the English regions by offering them a chance to invest in firms based in those regions. Theresa Wallis, the executive placed in charge of developing the market, recalls how the logic of social ties extended to investment in risky ‘growth firms’:

One of the things I heard and learnt when I first came on with the role was … investors, when it comes to small companies, they’d rather invest close to home where they can go and visit the companies and they look them in the eye and all that sort of thing. (Wallis)

You’d be invited round for dinner at Clifford Chance [a legal firm], or something. It was all about the market, getting to understand it, and that engagement. You could tell that the relationship was very close. You could tell that it was understood why it was important … there was never anyone who was not willing to engage properly. (Hughes)

Yet, as we have argued above, a market needs a mechanism to avoid malfeasance and to ensure some kind of informational efficiency. Such light touch requirements were only possible due to the dense social networks and interpersonal-knowledge within London’s financial community, which the market’s designers co-opted into a new species of private regulator: the Nomad.

Table 1 Listing requirements and obligations, LSE main market and AIM compared

5.1. Nomad-based regulation

The disclosure and corporate governance provisions for AIM companies follow the UK tradition of principles-based regulation.Footnote3 The consultation had initially hoped to avoid the expensive requirement of sponsorship (a corporate advisory firm responsible for vetting the applications to list on the market) and the associated administrative burden on the LSE’s own supervisory offices. According to Simon Brickles, one of Wallis’ team who subsequently became Head of AIM, a stock exchange ‘should be the high temple of capitalism, we should allow as much choice and freedom as compatible with a reasonable level of investor protection’. The consultation settled on a ‘disclosure-based’ based structure reliant upon the principle of caveat emptor, focusing regulatory efforts around ensuring full disclosure of financial information and assuming that investors have sufficient sophistication to act accordingly. Nonetheless, those involved in the consultation argued that some kind of oversight would be necessary involving quality control outsourced to a network of professional advisers in a structure of private regulation. illustrates the key participants in AIM.

At the forefront of this network are the Nomads, the corporate finance firms bringing issues to market. Listed companies are required to retain a Nomad, and if they are unable to do so will be forced to leave the market. Nomads have an ongoing responsibility to their client firms to provide advice, mandate adequate disclosure and oversee compliance with regulation. Nomads themselves are policed by reputation and a concern for repeat business among clients and investors. AIM is a ‘reputational market’ (Mendoza, Citation2008, p. 333) where social relations become the structure underlying informational efficiency. Offenders will be disciplined by public exposure. This is epitomized by the Telegraph's conclusion to the story of one market misdemeanour: ‘a good public flogging serve[s] to remind brokerage houses to show a little caution in who they bring to market in the first place – and the importance of never, ever misleading investors’ (quoted by Stringham & Chen, Citation2012, p. 42).

The AIM rules legislate for social and reputational entanglements. The Nomad must be independent of the issuer, must be a firm that has practiced corporate finance for at least the previous two years, has acted on at least three relevant transactions during that period, and has employed at least four qualified executives. Qualified executives are full-time employees who have acted in a corporate finance advisory role for at least three years and who have acted as the lead on at least three appropriate capital market transactions in the previous three years. Tim Ward, responsible for drafting the initial specification of the governance role, explains:

The Exchange did not want firms which did not have a reputation to suddenly pop on this market and build their reputation on the back of the market. It was necessary for the firms that were Nominated Advisors to have a reputation that they needed to protect and enhance, rather than one to create. So it was not one for new boys to come in saying we are going to build our business off the back of this …

When it came to AIM, there was a network underneath which says, that company, don’t touch it. And so an awful lot of this stuff was unwritten, unrecorded, but by and large, one of the reasons why AIM survived better than most was because we did things like that. Can’t discuss it publicly, deny all knowledge. (Vardey)

[x] and [x] had a ‘cerebral database’. [x] would phone [x] and ask do you know about so-and-so and would get a yes, no, don’t touch with a bargepole answer. But you couldn’t write any of it down so they called it a cerebral database. (Hocken)

the black-balling and … the censure was the thing, a private censure … [and] the public censure, which was really only ever used when you were trying to give a signal that somebody was a wrong ‘un. (Brickles)

5.2. Investor-based regulation

Although the Nomads carry legal responsibility for supervision, the tight network of institutional investors that operates in the market also assists in information flow. AIM has developed a strong track record in raising money for growing businesses. Roughly 60 per cent of this capital has been raised through secondary, or follow-on issues. AIM has attracted a particularly well-developed base of institutional investors, including Fidelity, Goldman Sachs and UBS, which lead a deep and highly sophisticated pool of institutional capital dedicated to small and mid-cap shares. The market is dominated by institutional investors to a much greater extent than, for example, NASDAQ in the United States (Arcot et al., Citation2007). Unlike retail investors that trade more frequently for short-term benefits, institutional investors are potentially stable, long-term holders of these shares. Furthermore, with relatively few retail shareholders, most IPOs and secondary offerings on AIM take the form of placings with institutions. A significant number of AIM-listed companies seek to raise additional capital from their existing shareholder base over time and so managers and advisors must act in the expectation that they will return to the same buyer in due course.

The day-to-day work of investors involves meeting with and building relationships with the managers of potential and actual investee firms, who in turn maintain tight links with a small number of investors. One specialist fund manager comments:

I probably see them [investee management] once every six months. But I’ve known them … I must have known them pretty much for, well 25 years. The chief exec’s been there probably for 15 … . People ring me up and say, I’ve got a really interesting company I’d love you to see, and I say fine, here’s a spot in the diary. (Williams)

They [brokers] come and see you and they do a presentation … and they say, we want 10p and you say, maybe five, eight, two? I’ve been spoken to by brokers and financial advisers to companies many a time saying, well, if we make it 7p would you do half a million quid or something to which the answer is, no, it’s going to be 5p or nothing and I’ll do a million quid at 5p or, you know … I’m not going to pay the wrong price as I see it for a smaller sum of money. It’s right or wrong. The sum of money is irrelevant. It’s right or wrong. (Buchanan)

The market price, the price you see on the screen, is generally set by the retail investor, the balance of buyers and sellers, all these five grands and 10 grands and 20 grands worth of stock. … so they will interact with our market makers, which will adjust the price depending on the supply and demand in the market. The institutional investors generally stay out of that. They don’t deal in small amounts. But if they want to sell a million pounds worth of stock … I can ring up another institutional investor, and if he agrees to buy it at that price, we match them. So the million pounds worth of stock goes through the market, one’s sold, one’s bought. But it doesn’t change the market price. Someone can come on and buy £10,000 worth and it will put it up, or if they buy or sell, it could put it up or down by five to ten per cent. (Norcross)

6. Discussion: Fama and White markets

For Coase, the ‘market within a hierarchy’ constitutes a ‘private legal system’ and

enforcement of the rules is possible because the opportunity to trade on the exchange is of great value and the withholding of permission to trade is a sanction sufficiently severe to induce most traders to observe the rules of the exchange. (Citation1988, p. 10)

We do not claim here that the LSE’s main board is Fama efficient. We have drawn attention to the empirical improbability of the Fama structure, a situation likely to result in practice in the hybrid described by Abolafia (Citation1996), where regulators and market practitioners conduct an ongoing dialogue between external regulation and the internally generated rules and conventions of the market. Empirical research has indeed shown that the LSE falls some way short of the Fama ideal, with investment activity embedded in dense social networks within a community dominated by a small number of large institutions (Davis, Citation2006). This picture has been complicated in the last decade by the expansion of automated high-frequency trading (HFT), to the point where the vast majority of equity trading (over 90 per cent globally and by extension on the LSE) is conducted by algorithms (Hayes, Citation2019). HFT strips out social relations and brings additional complexities of black boxing, organizational ignorance and epistemic difference into play (see Coombs, Citation2016; Lange, Citation2016; Lenglet & Mol, Citation2016; Seyfert, Citation2016, and other contributions to issue 45 of this journal). Centralized exchange systems can be circumvented by anonymous ‘dark pools’ (Lagna & Lenglet, Citation2019).

Our point here is that the design of the LSE’s main market, understood both in terms of regulation and this socio-technical structures, is driven by and adheres to Fama principles, an observation borne out by Davis’ (Citation2006) finding that social relationships and regulation are antagonistic in the LSE. Where social networks and norms emerge in such a market, they are to be viewed with suspicion as market imperfections and eradicated. This is the Granovetterian position: social networks emerging to benefit existing market agents. It is beyond the scope of this study to document the extent to which these mechanisms have been successful in removing social networks from the operation of the LSE’s main board. We draw a comparison between the organizational intention of the main board – the pursuit of efficiency through the removal of social content, an ‘abstract transparency’ invoking the neoclassical ideal of the mechanical auctioneer (see Grossman et al., Citation2006) – and a regulatory intention in AIM that deliberately invokes social relationships as a means of pursuing informational efficiency.

A second part of our argument is, therefore, that the balance between external regulation and internal self-regulation is an important design choice and source of variation in systems of private law for financial markets. We have shown how AIM established a system of internal private regulation based on pre-existing social structures (an ‘equity culture’) and how that system is designed to facilitate information flow in an otherwise informationally opaque and often illiquid market. Evidence of stable networks, and thus counterparty identity, are central to AIM. We have shown that social structures were designed into AIM from its very outset, and that its distinctive regulatory identity depends upon relations of interpersonal knowledge, obligation, reputation and other affectual bonds between participants. AIM has been successful in terms of attracting firms and investors; its structure is informationally efficient because AIM is an example of a ‘Whitean’ producer market.

For White, producer markets are characterized as stable networks of mutually aware actors sending reputationally weighted signals of quality and volume within identifiable market boundaries. Producers

come to treat each other and to be treated by the outside world as structurally equivalent through the evolution of input and output networks of ties … . Knowing oneself, and being known, to be in a given market is the single most important aspect of getting established in business. (White, Citation2002, p. 121)

7. Concluding remarks

What does this mean for the design of markets and the accompanying sociology of heterogeneous market types (Frankel et al., Citation2019)?

Despite the prevalence of the Fama market as a business offering among main board exchanges, we suggest that there may be alternative social structural options to achieve a given level of informational efficiency, and that that alternative structures may, in fact, be just as successful as the established ‘Fama’ market. Expectations that AIM would function as a feeder for the main market (Hornock, Citation2015) have been disappointed, for AIM seems to have been successful on its own terms. The transaction costs of switching from AIM to the Official List are high and these costs include loss of social capital. AIM remains a tight network, comprising specialized investors and advisory firms skilled in smaller company work. AIM is viable both as a commercial proposition in a Whitean market for exchange services and as an informationally efficient Whitean market for investors and firms.

It remains only to look to the future and to challenges that might confront the Whitean model. In emphasizing that financial markets can be understood as systems of emergent social dynamics rather than organized performances of economic theory, we do not suggest that Whitean markets are any less in need of maintenance. On the contrary, the social relations that underpin AIM must be constantly replenished through the socialization of new advisors into the norms of the community. It cannot be expected that this will take place without supervision and it remains the responsibility of the Exchange to reinforce these norms: ‘It was always implicit … we would shoot one [Nomad] a year pour encourager les autres’ (Vardey). Several interviewees felt that an emphasis on AIM’s growth had caused the LSE to stay such executions unnecessarily. More significantly, in AIM’s first decades the entanglements of the community flowed from relationships forged on the floor of a pre-digital exchange. By 2021 there are few who remember that era, and a pre-existing tapestry of social relations can no longer be taken for granted. The extent to which AIM remains a ‘club’ and can be supervised like one is, therefore, open for debate.

It may also be that such Whitean systems reproduce and gloss forms of social closure, and this is worthy of future research. The regulatory emphasis on qualified individuals appears to preclude new entrants, and those not attuned to the habitus of the community may be disbarred. Advisory firms complain that the same rules precipitate conflict between the qualified executives and the firms. If a firm loses its fourth executive it loses its licence to operate, and it is easy for four executives to cooperate in bidding up salaries. As Callon (Citation1998) and those following have noticed, markets ‘overflow’ with unexpected consequences, some of which may permanently disrupt market operation.

Overall, however, we conclude that a producer market is a viable design option for a financial exchange. This claim is of increasing relevance in an era where market design is dominated by concerns over the fragility of markets dominated by HFT. Academics and regulators have recognized the dangers of excessive interpersonal efficiency (Aldridge & Krawciw, Citation2017; Beunza et al., Citation2012). The homogeneity and interconnectedness of global main board exchanges might usefully be tempered by alternative mechanisms of market governance. In a producer market, ties of reputation, practitioner knowledge and sociality – market imperfections – underpin the effective functioning of the market. As economists seek to tackle social problems using markets as ‘boutique information processors’ (Nik-Khah & Mirowski, Citation2019) and activists search for new models of market arrangement and participation (Callon, Citation2017; Geiger & Gross, Citation2018), we emphasize the importance of these entanglements, not only to those engaged in market design, but also to scholars commenting thereon.

Acknowledgements

This paper has greatly benefitted from the comments of editor Dr Samantha Ashenden and the journal’s anonymous reviewers. An early version of the paper was presented at the EGOS Colloquium, Edinburgh, 2019, and the authors thank the sub-theme participants for their comments and support. The first author would also like to thank the interviewees for giving up their time so generously. Errors and omissions remain the responsibility of the authors.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Philip Roscoe

Philip Roscoe is Reader in Management at the University of St Andrews. He is interested in innovation and organization in markets and has researched empirical sites from online dating to small company stock exchanges. He has been a Leverhulme Trust Research Fellow and has published in leading sociology and management journals, including Organization Studies, Human Relations, Accounting Organizations and Society and Organization, with monographs published by Oxford University Press and Penguin. In 2011 he was one of the 10 winners of the inaugural AHRC BBC Radio 3 ‘New Generation Thinkers’ scheme and was shortlisted for the 2014 Deutscher Wirtschaftsbuchpreis. He is Associate Editor of the Journal of Cultural Economy.

Paul Willman

Paul Willman is an Emeritus Professor of Management in the Department of Management at the LSE and Academic Director of LSE’s Executive Courses. He has held Visiting Professorships at Sidney and Macquarie Universities and Senior Research Fellowships at Imperial College and Nuffield College, Oxford. Until 2006, he was Professorial Fellow of Balliol College, Oxford and the inaugural Ernest Butten Professor of Management Studies in the Said Business School, Oxford University. He was Director of Executive Education at Oxford 2001–2003 and founding Director of the Oxford EMBA. He was Editor in Chief of Human Relations (2000–2006). He was Professor of Organizational Behaviour and Industrial Relations at London Business School from 1991–2000. He is the author of 10 books and numerous papers in academic journals.

Notes

1 https://www.londonstockexchange.com/statistics/markets/aim/aim.htm (accessed 7 May 2021).

2 There is a difference between earlier and later versions of the hypothesis around the meaning of both ‘relevant’ and ‘available’. See Fenton-O’Creevy et al. (Citation2005).

3 A principles-based approach relies upon principles and outcome-focused rules rather than detailed rules prescribing how outcomes must be achieved (‘Principles-based regulation’, FSA, April 2007).

4 Speech by Tom Troubridge from PWC, at the Corporate Governance Research Seminar on AIM at the London School of Economics on 12 March 2008.

5 Speech by David Pinniger from Abingworth Life Sciences and Healthcare Investment in a seminar on AIM at LSE on 12 March 2008.

6 On 8 August 2005, the LSE issued its first public rebuke of a Nomad, Durlacher Corporation (a former investment banking company which has since merged with Panmure Gordon & Co.), for delaying a profits warning by its AIM-listed client Prestbury Holdings for eight days while the company carried out fundraising. In addition, there were a number of private censures of AIM companies and Nomads for breaches of the AIM Rules. (Source: Stock exchange AIM disciplinary notices and news, for example, MacDonald, Citation2007).

References

- Abolafia, M. (1996). Making markets: Opportunism and restraint on Wall Street. Harvard University Press.

- Aldridge, I. & Krawciw, S. (2017). Real-time risk: What investors should know about fintech, high-frequency trading, and flash crashes. John Wiley & Sons.

- Arcot, S., Black, J. & Owen, G. (2007). From local to global: The rise of AIM as a stock market for growing companies. London School of Economics.

- Aspers, P. (2007). Theory, reality, and performativity in markets. American Journal of Economics and Sociology, 66(2), 379–398.

- Beunza, D., Mackenzie, D., Millo, Y. & Pardo-Guerra, J. P. (2012). Impersonal efficiency and the dangers of a fully automated securities exchange. Foresight Driver Review 11. Foresight.

- Black, F. (1986). Noise. Journal of Finance, 41(3), 529–543.

- Çalışkan, K. & Callon, M. (2010). Economization, part 2: A research programme for the study of markets. Economy and Society, 39(1), 1–32.

- Callon, M. (1998). The embeddedness of economic markets in economics. In M. Callon (Ed.), The laws of the markets (pp. 1–58). Oxford University Press.

- Callon, M. (2017). L’emprise des marchés: Comprendre leur fonctionnement pour pouvoir les changer. La Découverte.

- Castelle, M., Millo, Y., Beunza, D. & Lubin, D. C. (2016). Where do electronic markets come from? Regulation and the transformation of financial exchanges. Economy and Society, 45(2), 166–200.

- Clemons, E. K. & Weber, B. W. (1990). London’s big bang: A case study of information technology, competitive impact, and organizational change. Journal of Management Information Systems, 6(4), 41–60.

- Coase, R. (1988). The firm, the market and the law. University of Chicago Press.

- Coombs, N. (2016). What is an algorithm? Financial regulation in the era of high-frequency trading. Economy and Society, 45(2), 278–302.

- Coslor, E. (2016). Transparency in an opaque market: Evaluative frictions between ‘thick’ valuation and ‘thin’ price data in the art market. Accounting, Organizations and Society, 50, 13–26.

- Davis, A. (2006). The limits of metrological performativity: Valuing equities in the London Stock Exchange. Competition & Change, 10(1), 3–21.

- Deville, J. (2012). Regenerating market attachments: Consumer credit debt collection and the capture of affect. Journal of Cultural Economy, 5(4), 423–439.

- Fama, E. (1970). Efficient capital markets: A review of theory and empirical work. Journal of Finance, 25(2), 383–417.

- Fama, E. (1991). Efficient capital markets: II. Journal of Finance, 46(5), 1575–1617.

- Fenton-O’Creevy, M., Nicholson, N., Soane, E. & Willman, P. (2005). Traders: Risks, decisions and management in financial markets. Oxford University Press.

- Frankel, C., Ossandón, J. & Pallesen, T. (2019). The organization of markets for collective concerns and their failures. Economy and Society, 48(2), 153–174.

- Garcia-Parpet, M.-F. (2007). The social construction of a perfect market: The strawberry auction at Fontaines-en-Sologne. In D. MacKenzie, F. Munesia & L. Siu (Eds.), Do economists make markets? (pp. 20–53). Princeton University Press.

- Geiger, S. & Gross, N. (2018). Market failures and market framings: Can a market be transformed from the inside? Organization Studies, 39(10), 1357–1376.

- Gerakos, J., Lang, M. & Maffett, M. (2013). Post-listing performance and private sector regulation: The experience of London’s Alternative Investment Market. Journal of Accounting and Economics, 56(2–3, Supplement 1), 189–215.

- Grossman, E., Muniesa, F. & Luque, E. (2006). Economies through transparency. halshs-00087886. Retrieved from https://halshs.archives-ouvertes.fr/halshs-00087886

- Hayes, A. (2019). The active construction of passive investors: Roboadvisors and algorithmic ‘low-finance’. Socio-Economic Review, early online. Retrieved from https://doi.org/https://doi.org/10.1093/ser/mwz046

- Hornock, J. (2015). The Alternative Investment Market: Helping small businesses grow. Ohio State Entrepreneurial Business Law Journal, 9(2), 323–377.

- Jenkinson, T. & Ramadorai, T. (2013). Does one size fit all? The consequences of switching markets with different regulatory standards. European Financial Management, 19(5), 852–886.

- Knorr Cetina, K. & Preda, A. (Eds.). (2012). The Oxford handbook of the sociology of finance. Oxford University Press.

- Lagna, A. & Lenglet, M. (2019). The dark side of liquidity: Shedding light on dark pools’ marketing and market-making. Consumption Markets & Culture, early online. Retrieved from https://doi.org/https://doi.org/10.1080/10253866.2019.1582415

- Lange, A.-C. (2016). Organizational ignorance: An ethnographic study of high-frequency trading. Economy and Society, 45(2), 230–250.

- Lee, R. (1998). What is an exchange? The automation, management and regulation of financial markets. Oxford University Press.

- Lee, R. (2011). Running the world’s markets: The governance of financial infrastructure. Princeton University Press.

- Lenglet, M. & Mol, J. (2016). Squaring the speed of light? Regulating market access in algorithmic finance. Economy and Society, 45(2), 201–229.

- MacDonald, A. (2007, October 20). AIM fines broker for poor conduct. The Wall Street Journal.

- MacKenzie, D. (2006). An engine, not a camera: How financial models shape markets. MIT Press.

- MacKenzie, D. (2009). Material markets: How economic agents are constructed. Oxford University Press.

- MacKenzie, D. (2017). A material political economy: Automated trading desk and price prediction in high-frequency trading. Social Studies of Science, 47(2), 172–194.

- MacKenzie, D. (2019). Market devices and structural dependency: The origins and development of ‘dark pools’. Finance and Society, 5(1), 1–19.

- MacKenzie, D. & Millo, Y. (2003). Constructing a market, performing theory: The historical sociology of a financial derivatives exchange. American Journal of Sociology, 109(1), 107–145.

- Mallin, C. & Ow-Yong, K. (1998). Corporate Governance in Small Companies – The Alternative Investment Market. Corporate Governance: An International Review, 6(4), 224–232.

- Mallin, C. & Ow-Yong, K. (2013). The development of the UK Alternative Investment Market: Its growth and governance challenges. In R. Cressy, D. Cumming & C. Mallin (Eds.), Entrepreneurship, finance, governance and ethics (pp. 113–135). Springer.

- McFall, L., Deville, J. & Cochoy, F. (2017). Introduction. In F. Cochoy, J. Deville & L. McFall (Eds.), Markets and the arts of attachment (pp. 11–31). Routledge.

- McFall, L. & Ossandón, J. (2014). What’s new in the ‘new, new economic sociology’ and should organisation studies care? In P. Adler, P. Du Gay, G. Morgan & M. Reed (Eds.), Oxford handbook of sociology, social theory and organization studies: Contemporary currents (pp. 510–533). Oxford University Press.

- Mendoza, J. M. (2008). Securities regulation in low-tier listing venues: The rise of the Alternative Investment Market. Fordham Journal of Corporate & Financial Law, 13(2), 257–328.

- Muniesa, F., Doganova, L., Ortiz, H., Pina-Stranger, A., Paterson, F., Bourgoin, A., … Yon, G. (2017). Capitalization: A cultural guide. Presses des Mines.

- Newell, G. & Marzuki, M. J. B. (2018). The significance and performance of property companies on the AIM stock market. Journal of European Real Estate Research, 11(1), 28–43.

- Nielsson, U. (2013). Do less regulated markets attract lower quality firms? Evidence from the London AIM market. Journal of Financial Intermediation, 22(3), 335–352.

- Nik-Khah, E. & Mirowski, P. (2019). On going the market one better: Economic market design and the contradictions of building markets for public purposes. Economy and Society, 48(2), 268–294.

- Palo, T., Mason, K. & Roscoe, P. (2018). Performing a myth to make a market: The construction of the ‘magical world’ of Santa. Organization Studies, early online. Retrieved from https://doi.org/https://doi.org/10.1177/0170840618789192

- Pardo-Guerra, J. P. (2019). Automating finance: Infrastructures, engineers, and the making of electronic markets. Oxford University Press.

- Piotroski, J. D. (2013). The London Stock Exchange’s AIM experiment: Regulatory or market failure? A discussion of Gerakos, Lang and Maffett. Journal of Accounting and Economics, 56(2–3), 216–223.

- Posner, E. (2009). The origins of Europe's new stock markets. Harvard University Press.

- Preda, A. (2009). Framing finance: The boundaries of markets and modern capitalism. University of Chicago Press.

- Preda, A. (2017). Noise: Living and trading in electronic finance. University of Chicago Press.

- Revest, V. & Sapio, A. (2016a). The creation function of a junior listing venue: An empirical test on the Alternative Investment Market. LEM Working Paper Series. Laboratory of Economics and Management (LEM), Sant'Anna School of Advanced Studies.

- Revest, V. & Sapio, A. (2016b). Graduation and sell-out strategies in the Alternative Investment Market. Universita di Napoli.

- Roscoe, P. (2015). ‘Elephants can’t gallop’: Performativity, knowledge and power in the market for lay-investing. Journal of Marketing Management, 31(1–2), 193–218.

- Roscoe, P. & Loza, O. (2019). The-ography of markets (or: The responsibilities of market studies). Journal of Cultural Economy, 12(3), 215–227.

- Sanusi, M. S. (2018). A critical overview of the transparency and competitiveness of the London Stock Exchange. Risk Governance and Control: Financial Markets and Institutions, 8(2), 74–83.

- Seyfert, R. (2016). Bugs, predations or manipulations? Incompatible epistemic regimes of high-frequency trading. Economy and Society, 45(2), 251–277.

- Stringham, E. P. & Chen, I. (2012). The alternative of private regulation: The London Stock Exchange’s Alternative Investment Market as a model. Economic Affairs, 32(3), 37–43.

- Vargha, Z. (2011). From long-term savings to instant mortgages: Financial demonstration and the role of interaction in markets. Organization, 18(2), 215–235.

- Vismara, S., Paleari, S. & Ritter, J. R. (2012). Europe’s second markets for small companies. European Financial Management, 18(3), 352–388.

- Weber, K., Davis, G. F. & Lounsbury, M. (2009). Policy as myth and ceremony? The global spread of stock exchanges, 1980–2005. The Academy of Management Journal, 52(6), 1319–1347.

- White, H. C. (1981). Where do markets come from? American Sociological Review, 87(3), 517–547.

- White, H. C. (2002). Markets from networks: Socioeconomic models of production. Princeton University Press.

- Willman, P., Fenton O’Creevy, M., Nicholson, N. & Soane, E. (2006). Noise trading and the management of operational risk; firms, traders and irrationality in financial markets. Journal of Management Studies, 43(6), 1357–1374.

- Willman, P., Fenton O’Creevy, M. P., Nicholson, N. & Soane, E. (2001). Knowing the risks: Theory and practice in financial market trading. Human Relations, 54(7), 887–910.

- Yow, V. R. (2005). Recording oral history: A guide for the humanities and social sciences. Rowman Altamira.

- Yu, L. (2010). A reputational bonding perspective on financial markets: Studies on initial public offerings. Unpublished PhD thesis. University of Oxford.

- Zuckerman, E. W. (2012). Market efficiency: A sociological perspective. In K. Knorr Cetina & A. Preda (Eds.), The Oxford handbook of the sociology of finance (pp. 223–249). Oxford University Press.