ABSTRACT

Climate change and associated coastal hazards can disrupt the United States shipbuilding and repair industry’s operations. These disruptions present risks to military and commercial ship orders, ship maintenance and repairs, and the nation’s overall shipbuilding strength. Through an online survey of representatives from 45 shipbuilding parent companies, individual shipyards, and ship repair and maintenance facilities, this research gauges how the industry considers coastal hazard resilience and addresses the possible impacts on shipbuilding and repair contracts and deliverables. Survey results suggest that the industry is ill-prepared for future coastal hazard events and that critical measures are needed to ensure a resilient shipbuilding and repair environment.

1. Introduction

Climate change amplifies coastal hazards and will become more impactful to coastal communities and industries. It will be a major challenge for the 21st century, with sea level rise being the most concerning and likely having the costliest effects (Sweet et al. Citation2022). The effects of coastal hazards on infrastructure systems (including shipyards) include accelerated degradation of infrastructure networks, exposure of infrastructure networks to disruptive events, and a greater propensity of cascading failures caused by interdependencies between infrastructure networks. Real coastal hazards effects may include destruction of critical infrastructure, immobilization due to transportation system breakages, power grid failures, and saltwater contamination all of which may result in prolonged disruption to economic activities and livelihoods. Land and infrastructure on all U.S. coasts are at risk from storm surge (and high tide flooding) and the coastal land and economic value at risk grows over time with sea level rise and more intense storms—making adaptation (and increased coastal hazard resilience) a cost-effective response (Neumann et al. Citation2014). The U.S. shipbuilding industry is highly vulnerable to these failures and disruptions which are clearly driving the need for higher levels of coastal hazard resilience.

Damaged shipyard infrastructure results in disruptions to shipyard build, repair, and maintenance operations. A developing key uncertainty is the degree to which national security could be affected by such disruptions. This research investigates how shipyard leaders and operators perceive these challenges to their operations, the types of preparations shipyards have or will complete towards attaining a needed level of coastal hazards resilience, and the extent to which major disruptions to shipyard operations resulting from coastal hazards events could weaken the shipbuilding industry. We conducted an online survey of U.S. parent shipbuilding companies and shipyards that build, repair, maintain, modernize, and supply the nation’s domestic fleet. The survey conducted in 2021 addressed three research questions about the shipbuilding industry’s consideration of coastal hazards resilience, as follows:

RQ1 What types and levels of coastal hazard events (e.g., storm surge, wind, waves, rain, tidal flooding) do respondents feel have or would pose challenges to shipbuilding and repair operations?

RQ2 Do the respondents feel their shipyards need to take additional, needed measures, practices, and policies to prepare for coastal hazards, weather events and/or climate conditions they expect 10–30 years from now?

RQ3 What levels and types of coastal hazard related disruptions do respondents feel would impact their production in terms of timelines, costs, and contract deliverables?

The results can inform the developing relationship between the U.S. shipbuilding industry and coastal hazards resiliency challenges. We intend this survey to establish a baseline regarding the industry’s coastal hazards concerns, resilience actions already taken, and those planned. This information can contribute to developing a continued safe, secure, healthy, sustainable, and resilient shipbuilding/repair industry.

2. Literature review and background

The following section provides background and context for the research. It begins with a broad discussion of climate change and natural hazards, with a focus on impacts to coastal areas. Next, it establishes the research gap that exists for the topic area of hazard risks to shipyards and ship repairs. This is followed by a discussion of the US shipbuilding industry trends and importance to the US economy and security, with emphasis on historical and future impacts from natural hazards driven by climate change.

2.1. Climate change and coastal resilience

U.S. shipyards are located on and near the nation’s coasts and tidal rivers and, as such, are highly susceptible to a variety of coastal hazard events, including flooding from increased and more powerful tropical storm systems, high tides, rain, and sea level rise. The global proportion of tropical cyclones that reach very intense levels (Category 4 and 5) is projected to increase, as are intense rainfall events (Knutson Citation2021). Sea level rise is accelerating, and adaptation planning should consider an additional 10–12 inches by 2050 (Sea Level Rise Tech Report, Citation2022) or more (Sweet et al. Citation2022). This creates a profound shift in coastal flood risks, with damaging flood waters expected to occur more than 10 times as often as it does now (Sweet et al. Citation2022). Coastal flooding events are expected to increase because of higher tides, more major precipitation events, storm surges, and sea level rise. These events can impact shipbuilding and ship repair operations in the U.S. East, West, and Gulf coastal regions. Major winter storms due to climate change could also impact shipyard operations in the Northwest Pacific, Northeast Atlantic, and the Great Lakes. Impacts can include interruption of crane, drydock and slipway operations; damages to fabrication structures and machinery and supply warehouses; disruption of supply chain flows; and interruption to critical support elements including roads, railways, and parking.

An additional coastal hazard threat gaining attention is the projected increase in ‘nuisance flooding’ (also referred to as high tide flooding, sunny-day flooding, and king tide flooding) along the U.S. coast. Nuisance flooding events are already causing public inconvenience, business disruptions, and economic losses due to road closures and degradation of infrastructure (Jacobs et al. Citation2018). Under the current global greenhouse gas emissions warming scenario, nuisance flooding could increase by 35% in 2050, resulting in significant socio-economic impacts to coastal communities and industries (Moftakhari et al. Citation2015). According to NOAA’s Office for Coastal Management, during the past twenty years, the U.S. Southeast Atlantic and Gulf Coast regions saw an increase of 400 to 1,100% in high tide flooding days. By 2030, the annual national median frequency rate will likely increase to seven to 15 days, and, by 2050, high tide flooding is likely to occur between 25 and 75 days per year (Sweet et al. Citation2022).

While there is significant literature regarding coastal hazard predictions caused by climate change and the resulting impacts on coastal communities, there is little literature regarding coastal hazard impacts specific to shipyards and ship repair facilities. Previous studies confirm that climate change poses a significant threat to larger seaports (e.g., PIANC (The World Association for Waterborne Transport Infrastructure) Citation2020; Izaguirre et al. Citation2020), maritime supply chains (e.g., Verschuur, Koks, and Hall Citation2020; Becker Citation2020), marinas (Lazarus and Ziros Citation2021), and coastal airports (e.g., Yesudian and Dawson Citation2021). For example, a survey of global ports conducted in 2012 found that 80% of port administrators surveyed felt concerned about the potential impacts of climate change, but that little had yet been done to address the issue (Becker et al. Citation2012). The same paper suggests the importance of understanding perceptions amongst decision makers as a foundation for future research. A baseline survey similar to the one described in this research was conducted to identify climate change and sea level rise perceptions amongst maritime infrastructure engineers. That survey found an industry-wide need for clear policies and guidance to help engineers incorporate sea level rise in structure design (Sweeney and Becker Citation2020).

Two sources discussed in Section 3.2,3 Historical Hazard Impacts to the U. S. Shipbuilding Industry, briefly speak to the effects of Hurricanes Katrina and Michael on U.S. Gulf Coast shipyards operations and contract deliverables, but little if any academic research has been conducted on the challenge facing shipyards and ship repair facilities. This paper aims to fill that gap and provide foundational, empirically based, data on how the U.S. shipyard industry is currently considering these challenges.

2.2. The U.S. shipbuilding industry: a snapshot

This section provides an overview of the current shipbuilding industry in the U.S. It begins by identifying the industry’s capability and capacity and is followed by the impact of coastal hazards on shipyard operations. Also included are the number of military (Navy and Coast Guard) build orders needed for the next 30 years.

2.2.1. U.S. shipbuilding industry shipyards and facilities

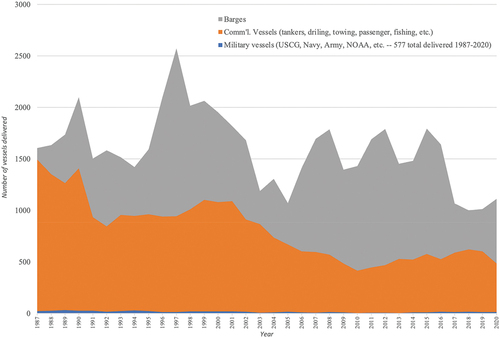

The U.S. Shipbuilding Industry includes repair and build operations, both of which play a critical role in supporting the U.S. maritime economy. Between 1987 and 2020, the U.S. shipbuilding industry delivered over 54,000 ships, boats, and ocean-going and inland barges, including 577 military vessels (shipbuildinghistory.com 2022) (). The U.S. maritime industry is supported by U.S. government policies that include the Merchant Marine Act of 1920 (a.k.a. the Jones Act), which mandates that commerce between U.S. ports must be conducted by U.S.-built, owned, flagged, and crewed vessels (Clark et al., Citation2019). The Jones Act helps sustain the U.S. shipbuilding industry. The seven major shipyards that construct Navy and Coast Guard ships generally do not build commercial vessels and smaller shipyards which may have contracts to build smaller military ships depend on Jones-compliant commercial vessel orders to stay in business. Of 40,000 vessels in the U.S. Domestic Fleet (tugs, barges, ferries, dredges, offshore supply vessels, etc.), fewer than 100 are large Jones Act-compliance vessels (Clark et al., Citation2019).

Figure 1. Vessel deliveries from U.S. Shipyards 1987–2020 (From Colton Citationn.d., http://shipbuildinghistory.com/statistics/recent.htm, accessed 5/12/2022).

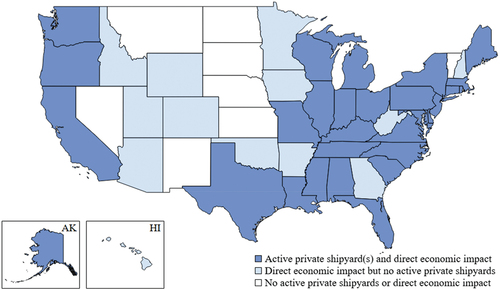

The Maritime Administration’s (MARAD) 2021 report on the economic importance of private U.S. shipyards and repair facilities identifies 154 active, private shipyards across 29 U.S. states and the U.S. Virgin Island and more than 300 yards engaged in repair operations but not actively engaged in build operations (). From 2015–2020, U.S. shipyards delivered 5,024 vessels including tugs, towboats, passenger vessels, commercial and fishing vessels, and oceangoing and inland barges. From 2015–2020, 60% of all vessels built in the U.S, were inland tank and dry cargo barges. The industry supported nearly 400,000 direct and indirect jobs and contributed $42 billion to the U.S. GDP (MARAD (US Maritime Administration) Citation2021).

Figure 2. States with Active Private Shipbuilders and Direct Economic Impact from the Private Shipbuilding and Repairing Industry (Figure from MARAD (US Maritime Administration) Citation2021).

2.2.2. Shipbuilding industry critical for military ship orders and maintenance

In addition to supporting the commercial fleet, U.S. repair and build yards serve the nation’s military interests. In 2021, the Navy’s planned for 321–372 manned ships and 77–140 large unmanned underwater and surface vehicles (O’Rourke, Citation2022b) for the next 30 years. The annual cost to maintain the fleet is projected to grow from $24 billion in 2024 to $40 billion in 2034 (Eckstein Citation2019). The Coast Guard’s program of record (POR), which dates to 2004, calls for procuring eight National Security Cutters (NSCs), 25 Offshore Patrol Cutters (OPCs), and 58 Fast Response Cutters (FRCs) as replacements for 90 aging Coast Guard High-Endurance Cutters, Medium-Endurance Cutters, and patrol craft. The Coast Guard’s proposed FY2022 budget requests a total of $695 million in procurement funding for the NSC, OPC, and FRC programs, including $597 million for the OPC program (O’Rourke, Citation2022a). In sum, there was a considerable amount of ship building and repair demand expected from the U.S. military in support of strategic missions in the next three decades.

2.2.3. Historical coastal hazard impacts to U.S. shipbuilding industry

The ability of early U.S. shipbuilders to adapt to coastal hazards was critical towards the startup and successful development of a resilient and strategic U.S. shipbuilding and repair industry. From the North American colonial era, through the U.S. Civil War, the World Wars, the Cold War, and through the decline of the industry as China, South Korea, and Japan became the industry leaders, until today, the U.S. shipbuilding industry continues to be a weakened yet viable, strategic industry primarily due to U.S. military and government and domestic use build and repair operations. The earliest documented coastal hazard event affecting U.S. shipbuilding was the 1635 Great Colonial Hurricane, which produced heavy winds and rainfall and a storm surge of 14–20 feet in some parts of the U.S. Northeast (Ludlam Citation1963). Wind and flooding likely disrupted the then-existing building and repair operations throughout New England’s coastal areas. More recently, Superstorm Sandy in 2012 reminded coastal communities and industries that the Northeast is still not immune from coastal hazards.

Another recent example is the wind and flood damage caused by Category 5 Hurricane Katrina in 2005 on the U.S. Gulf Coast, which resulted in a $16 billion project to bolster the New Orleans levee system which held back flood waters during Category 4 Hurricane Ida in 2021. Hurricane Katrina disrupted the lives of some 20,000 shipyard workers in the region’s shipbuilding sector and brought two of the nation’s leading shipyards to a standstill, along with a combined $1 billion in damages (Junglas and Ives Citation2007). In another example, flooding from a slow-moving Hurricane Harvey in 2017 and unrelenting rains devastated Houston and marine operations along the Houston Channel.

Hurricane Michael in 2019 also disrupted shipbuilding operations at major shipyards in Florida, on the Gulf Coast, and along the Mississippi River. Major shipyards, with both government and commercial contracts, have since repaired or replaced damaged equipment, buildings, and other infrastructure (O’Rourke, Citation2022b). The shipbuilding companies’ efforts along with federal and state partnerships ensured the shipbuilding industry has had continued health and has also provided new job opportunities in an otherwise devastated area (O’Rourke, Citation2022b).

2.2.4. Future impacts to shipbuilding industry

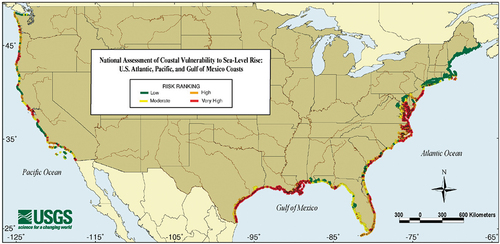

The Intergovernmental Panel on Climate Change (IPCC) Fifth Assessment Report (AR5) indicates there has been little research focused on climate change and manufacturing, though a 2011 study suggests it is one of the most sensitive U.S. sectors to weather conditions (Lazo et al. Citation2011). Coastal industries (such as shipbuilding and repair) and their supporting infrastructure (ports, roads, rail, airports) are highly susceptible to coastal hazards such as flooding due to extreme precipitation, high winds, storm surges, and sea level rise ().

Figure 3. Map of US vulnerability to Sea Level Rise from USGS (https://d9-wrets3.us-west-2.amazonaws.com/assets/palladium/production/s3fs-public/thumbnails/image/largenat.jpg).

Supporting transportation systems are typically in their original design location and any new supporting infrastructure must consider climate change drivers and variability (Wong et al. Citation2014). AR5 notes that vulnerability to flooding of railroad, tunnels, ports, roads, industrial (shipyard) infrastructure in coastal areas will be amplified by sea level rise and more frequent and intense tropical storms, resulting in ‘more frequent and more serious’ damage and disruption of services for many regions in the U.S (Wong et al. Citation2014). identifies major U.S. private shipyards (active yards, other yards with building positions, repair yards with drydock facilities, and topside repair yards) as classified by the Maritime Administration. (MARAD (US Maritime Administration) Citation2018/updated 2018). The table also identifies North American regions and current coastal hazards and 2100 sea level rise predictions per region (Reidmiller et al. Citation2017).

Table 1. Major Shipbuilding Regions, Major Shipyards, Current Coastal Hazard Threats, 2100 Predictions (Reidmiller, Citation2017).

In this section, we provided some context for the changing environmental conditions faced by U.S. shipyard. Next, we will describe our approach to generating empirical data that can be used to better understand how shipyards plan to address these challenges.

3. Methods

A nationwide online survey conducted in 2021 targeted shipyard senior management and engineering leaders from ship and boat building and repair shipyards and facilities regarding their consideration of coastal hazards resilience. This section details the research methods used in this project, including an overview of the survey instrument and the approach to recruiting participants. The survey was designed to be anonymous, with no specific shipyard, facility, company, or person mentioned by name in any follow-on paper or report (URI Institutional Review Board (IRB) approval number IRB2021-077).

3.1. Online survey instrument

The research questions and supporting online survey instrument were created with input from a nine-person project steering committee consisting of members from the shipbuilding industry, the national security policy community (Naval and National War Colleges, and the Eisenhower School for National Security and Resource Strategy), and the Maritime Administration. The Congressional Research Service was also represented in an observer status. Monthly online steering committee meetings were conducted throughout the development of the survey, including a pilot test. The survey consisted of five sections and 20 questions (See survey instrument in Appendix A) to collect respondents’ perceptions in order to answer the research questions described in the Introduction section of this paper.

3.2. Survey distribution

In consultation with the project steering committee, a list of over 300 active private U.S. shipyards, boatyards, and ship/boat maintenance and repair facilities, and five public yards, was compiled from various sources, including a MARAD list of active shipyards (MARAD (US Maritime Administration) Citation2018) and the Shipbuilding History website (www.shipbuildinghistory.com). Additionally, shipbuilding periodicals were reviewed, and the list was further refined by adding yards and facilities based on shipbuilding industry news reports. Of the 300 facilities, contact information was obtained for 149 (Appendix B). An email invitation to participate in the survey provided information on the research project and its importance. Additionally, a ‘one-pager’ was developed and forwarded to multiple shipbuilding, academia, and policy community members to promote the project and garner support. The survey was announced and promoted in LinkedIn groups Maritime Executive and Shipbuilding Industry and Professionals, and an article was published in Professional Mariner’s online publication. Information about the survey and a link were included in both Shipbuilders Association of America and Small Shipyard Federal Grant Coalition member newsletters, along with several port and operator groups. Additionally, information flyers with a QR Code survey linkage were distributed at the 2021 Navy League Sea, Air, and Space Exposition.

Over 300 email invitations were sent to shipyard email addresses. Every attempt was made to send an invitation to a specific shipyard person (CEO, president, industrial engineer, etc.). If specific individuals could not be identified, emails were sent to general addresses with requests to forward to the shipyards’ best prospective respondents. At least two rounds of reminder, follow up emails were sent. During the survey, follow-up phone calls were made to shipyard and facility employees, explaining the research project and requesting that a survey be completed and submitted. Since the survey was anonymous, specific shipyards and facilities responses were not tracked.

4. Results and key findings

This section provides respondent information and the main results and key findings of the survey. Of the over 300 email invitations to participate emailed, over 45 responses were received, with 38 complete and an additional seven partially completed. Answers to questions in partially completed surveys were used in analysis of results associated with those questions.

4.1. Respondent information

This sub-section details the state and regional location of the shipyards represented, the shipyard positions of the respondents and their years of shipbuilding and repair experience, and also their level of involvement in coastal hazards resilience planning and response and recovery operations.

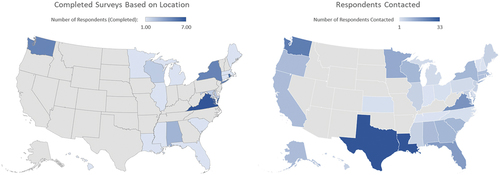

indicates the location of shipyards that were asked to participate in the survey and the total number of responses per state. The survey did not identify the specific shipyards in which representatives submitted the survey, but it did ask respondents to identify their regions and state. Shipyards in 33 states representing all U.S. coastal regions, the Great Lakes, and Hawaii and Alaska, were asked to participate, with shipyards from 19 states responding. Shipyards and repair facilities represented from the Northeast coast comprised 37% of all represented; the Mid-Atlantic coast followed with 14%. Of note is the high rate of return in Virginia which is possibly due to the proactive climate change strategy and partnerships between the City of Norfolk, the Navy, and the community. Participation from Rhode Island was also high, possibly due to interest in the Narragansett Bay region and knowledge of URI coastal research. Also of note is the lack of surveys submitted from shipyards on western half of the Gulf Coast—a region which is highly vulnerable to tropical storm system damage.

Figure 4. Location of survey respondents (left side) and location of shipyards invited to participate in the survey (right side).

Forty-two U.S. facilities were represented in the 45 usable surveys (thus in not more than three instances, only one response was received per shipyard). Of the five total public U.S. Navy and U.S. Coast Guard yards operating in the U.S., four are represented in the survey response data. Seven respondents indicated that they represent shipyard parent companies that oversee multiple facilities. All respondents indicated their facilities were engaged in repairs of working commercial vessel/boat (tugs, barges, OSVs, etc.) maintenance, repair order, and ship new construction orders.

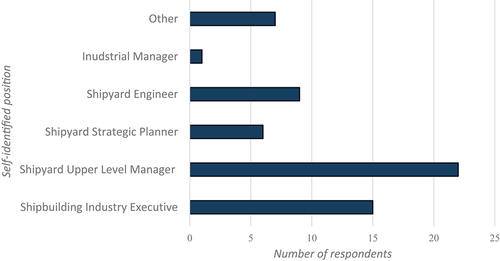

Respondents were asked to identify their shipyard positions and were able to select multiple options (). Thirty-seven respondents identified themselves as upper-level managers and industry executives, while 11 respondents identified themselves as shipyard engineers. Of 27 shipyard upper-level managers (CEOs, presidents), 22 had more than 20 years of experience suggesting that respondents had deep experience in shipyard management.

Figure 5. Number of respondents that self-identified in various leadership positions (Respondents may select more than one) (N = 44 total respondents).

Thirty respondents were either ‘very’ or ‘somewhat engaged’ in long-term planning for risk mitigation. Twenty-eight were ‘somewhat’ or ‘very engaged’ in emergency preparedness and disaster response. Twenty-six were ‘somewhat’ or ‘very engaged’ with recovery efforts after a storm event. These results suggest that the respondents were generally very experienced with coastal hazards management.

The next three sections (5.2–5.4) detail key findings, based on respondent survey responses, that address the three key research questions posed at the start of this paper.

4.2. Consideration of Coastal Hazards Affecting Shipyard Operations

Research Question Supported: RQ1 What types and levels of coastal hazard events (e.g., storm surge, wind, waves, rain, tidal flooding) do respondents feel have or would pose challenges to shipbuilding and repair operations?

This sub-section details the coastal hazards shipyard respondents identified that have impacted operations and what their coastal hazards expectations are for the future. Coastal hazards identified include wind, flooding, waves, and snow.

4.2.1. Key findings: coastal hazards and shipyard operations

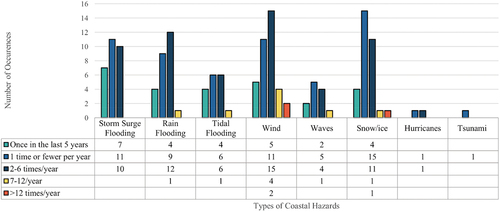

As indicated in , respondents indicated that wind interrupted some shipyard operations as much as six times a year, likely due to crane operation limitations which affect all shipyard operations regardless of location. They indicated that flooding from storm surges, precipitation and high tides occurs as much as six to 12 times per year. The Great Lakes and Northeast respondents indicated 15 interruptions per year at their facilities due to snow and ice conditions.

Figure 6. Respondent perceptions of types and frequency of coastal hazards that impact their shipyard operations in the last five years (N = 43 respondents).

Additionally, respondents indicated the average duration of each coastal hazard (over the last five years) as being mostly hours (55%) or days (35%) which correlates to wind and high tide and precipitation flooding events, while 10% of events reported longer durations (weeks, months, years). Longer durations are likely due to tropical storms resulting in infrastructure damage and loss of workforce.

4.2.2. Key findings—leadership expectations for sea level rise and tropical storm systems

Shipyard leadership perceptions of current and future coastal hazard resilience can influence strategic decision making, especially as relates to ensuring adequate preparations are planned for and resourced. For the purpose of this survey, shipyard industry leadership is defined as executives, presidents, chief executive officers, chief operating officers, and senior industrial and facility engineers. In this section, the survey asked respondents to report on how they felt their leadership perceives coastal hazard risks.

Per the survey results, the person/position at shipyards who respondents identified as ‘knows the most about coastal hazards impacts on shipyard operations’ was the Chief Executive Officer (CEO) (30 responses) followed by the industrial engineer (13) and the facilities engineer (11). This finding suggests an expectation that CEOs are knowledgeable and experienced with coastal storms, how they can impact operations, and that they would be in a strong leadership position to address future (changing) levels of risk from coastal hazards.

Of the 30 respondents who self-identified as ‘upper-level leadership’ (and that were not from Great Lakes or inland ports), six indicated that leadership did not expect any SLR by 2050, five indicated 0–0.5 feet, three indicated 0.5–1 foot, five indicated 1.5 to 3 feet, and one indicated 3–6 feet. Of note, 10 did not know if they expected any amount of SLR by 2050. According to the 2022 NOAA report (Sweet et al. Citation2022), the expected range of SLR for the U.S. is from approximately 0.7–2.3 feet above 2000 levels by 2050. Thus, eight respondents’ expectations were aligned with the latest scientific consensus, with 21 (or 70%) either not knowing or having expectations that do not align.

Using the same selection criteria (e.g., not from inland or Great Lakes and self-identified as upper-level leadership), we analyzed how leadership perceived potential changes to storm frequency and intensity. Twelve respondents expected such an increase, six did not, and 12 did not know. According to the IPCC, it is very likely that extreme storm events will increase in frequency and intensity with climate change (IPCC (Intergovernmental Panel on Climate Change) Citation2021).

In sum, most respondents either do not know or do not expect any changes to SLR or storm patterns between now and 2050. This is in contrast with the scientific consensus and suggests that there is a need for leadership to better understand how this aspect of climate change may affect their resilience planning and risk management.

4.3. Current status of preparations for coastal hazards and operational resiliency

Research Question Supported: RQ2 Do the respondents feel their shipyards need to take additional, needed measures, practices, and policies to prepare for coastal hazards, weather events and/or climate conditions they expect 10–30 years from now?

This sub-section details the resiliency and/or adaptation actions that respondents’ shipyards have taken or plan to take. In consultation with the steering committee, we identified 17 common adaptation actions that shipyards might implement to improve coastal hazard resilience (). Across the 38 responses to this survey question, 115 unique actions had been implemented prior to 2015; 60 were implemented from 2015–2020; 22 actions are under design or construction; 19 are planned to be implemented by 2025, and no actions are currently planned beyond 2025 ().

Table 2. Resilience actions at shipyards, according to survey respondents (N = 38 respondents).

4.3.1. Key findings: current and planned resilience actions

As indicates, armoring resilience actions (raising docks, strengthening facilities, etc.,) and policy or method resilience actions (partnerships, relocation of some operations inland, etc.) were at the same action item levels prior to 2015 and between 2015 and 2020. Moving into the future, armoring actions under design or construction or planned for implementation by 2025 are more numerous than policy or method actions, suggesting policies and methods will be in place and armoring or mitigation actions will follow. Of note, implementing a shipyard hurricane or winter storm plan and the installation of backup power comprised the most actions taken prior to 2015 and, more recently raising electrical equipment and strengthening facilities and structures were the most actions taken between 2015 and 2020. Eighty-two percent of respondent shipyards did not have cooperative or joint with other builders or other ‘work arounds’ to satisfy contract deliverables should operations be degraded due to coastal hazard events. 13% indicated they did; 5% indicated they did not know.

An analysis of responses suggests three major takeaways: (1) resilience preparedness actions beyond 2025 were generally not on a shipyard’s strategic agenda; (2) the majority of actions taken thus far were in response to current and past coastal hazard events and, (3) future planning in terms of coastal hazard resilience appeared to be minimal. This lack of planning beyond 2025 suggests that the impacts of climate change were not yet being fully considered in long range strategic and capital improvement initiatives.

4.4. Coastal hazard impacts on shipyard operations

Research Question Supported: RQ3 What levels and types of coastal hazard related disruptions do respondents feel would impact their production in terms of timelines, costs, and contract deliverables?

This subsection focuses on coastal hazard interruptions to shipyard operations and potential risks to contract deliverables. Twenty-seven of 30 respondents indicated that they agree with the statement that, ‘The level of the U.S. shipbuilding industry’s coastal hazards resilience will have a significant impact on the industry’s ability to build, maintain, and repair the U.S. military and commercial fleet for the next 30 years.’ (Q20). This sub-section details some of the risks that they are concerned about and further exemplifies the mismatch between concerns, knowledge about climate drivers, and actions.

4.4.1. Key finding: risks to contract deliverables primarily from physical damage to shipyard infrastructure, supply chain interruptions, and labor costs

Identifying potential and perceived risks to contract deliverables caused by coastal hazards is significant in the consideration and planning of a climate-ready shipbuilding industry and is important in shipyard self-assessments of coastal hazards vulnerability. Understanding the impact of each risk category is essential in strategic planning, in terms of where to apply resources and how to modify policies and programs so as to build needed resilience.

In coordination with the project steering committee, the research team developed a list of five major risks posed to contract deliverables due to coastal hazard impacts on shipyard operations. Respondents rank-ordered these risks to contract deliverables. The list below shows frequency (in parenthesis) of each risk being ranked as one of the top three concerns listed by survey respondents (n = 30 respondents):

Physical Damage to Shipyard Infrastructure (28)

Supply Chain Interruptions (28)

Labor Costs (28)

Material Cost Increases (15)

Retention of Workforce (8)

Other Risks (0)

We note that 24 of 30 respondents ranked ‘physical damage to shipyard infrastructure’ as the #1 greatest risk to fulfilling contract deliverables, in terms of build, repair, and maintenance timelines and completion dates. Supply chain interruptions were the next biggest factor with 12 of 30 respondents identifying impacts on transportation systems as the second greatest, potential risk. Increased labor material cost increases because of coastal hazards ranked third and fourth, respectively. The long-term impact of workforce retention was identified as a potential risk because of stoppage of build and repair operations for long periods of time with primarily the trades workforce moving to other work sectors for employment as well as higher wages, likely realized as a result of post-event recovery construction opportunities.

In addition to the resilience actions identified in Section 5.3, there are steps shipyards can take to reduce the specific risk posed to contract deliverables. For example, shipyards can develop contingency plans with partners to enhance redundancy in the event of a natural disaster. Survey results show that most (28 of 37 respondents) do not cooperate or partner with other shipyards to satisfy contracts when operations are threatened or interrupted. Only four respondents indicated that their shipyards did have such partnerships in place.

Results from these survey questions reinforce the risk from cascading consequences of coastal hazard events, especially to contract deliverables. This suggests that such downstream impacts should be considered when shipyards undertake vulnerability assessments.

4.4.2. Key finding: largest coastal hazard threats are hurricane and flooding from high tides

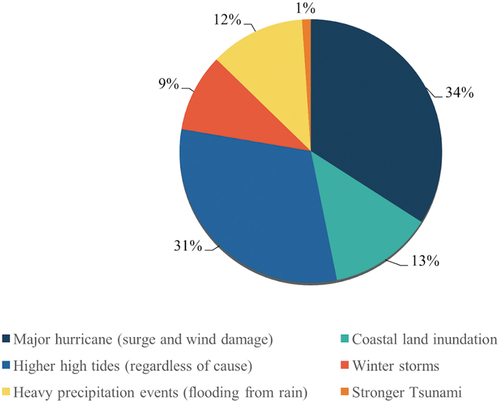

When asked if coastal hazards will have a negative impact on shipyard operations over the next 10–30 years, 29 of 41 respondents agreed or strongly agreed. Similarly, 26 of 37 respondents agreed or strongly agreed with the statement, ‘The level of the U.S. shipbuilding industry’s coastal hazards resilience will have a significant impact on the industry’s ability to build, maintain, and repair the US military and commercial fleet for the next 30 years.’ The perceived biggest coastal hazard threat out to 2050 is major hurricanes and related surge and tide flooding, and wind. indicates that the three largest coastal hazard threats to the U.S. shipbuilding and repair industry identified by survey respondents were: (1) major hurricane surge and wind damage (Category 3 to 5); (2) high tides (regardless of cause); and (3) coastal land inundation and heavy precipitation events. Winter storms (9%) threats are mostly relevant to Great Lakes and northern U.S. shipyards.

Figure 7. Answers to the question ‘What are the three biggest coastal hazard threats’ (n = 38 respondents).

Here again, identifying perceived coastal hazard threats and the associated disruptions to shipyard operations is essential to coastal hazard vulnerability assessment and resilience strategic planning. As an example, armoring against the operational impacts of major hurricane surge and wind damage for shipyards in areas prone to tropical system landfall is essential in matching resources, and policy and program changes, with that high-consequence risk.

5. Discussion

This U.S. shipbuilding and ship repair industry baseline survey focused on:

the types and levels of coastal hazard events which pose shipyard operational challenges;

operational resiliency preparedness;

measures, practices, and policies for future coastal hazard conditions;

the types and levels of coastal hazards which would impact shipyard production in terms of production timelines, costs, and contract deliverables.

Overall, survey respondents reported significant concerns about coastal hazards and resilience in the next 10–30 years. The majority of respondents indicated sea level rise will cause a problem, though there was variation in how much (if any) SLR was expected. The respondents had a similar split as to the threat from increases in tropical storm frequency and intensity out to 2050, with less than half indicating that they anticipated increases, and more than half indicating no, or they didn’t know. We note that there is clear consensus in the scientific community about both SLR and an increasing frequency/intensity of storms and extreme events (e.g., Sweet et al. Citation2022; IPCC (Intergovernmental Panel on Climate Change) Citation2021).

Increased flooding events can be addressed through mitigation actions such as raising electrical equipment and installing drainage pumps, but results suggest that few such projects were planned. Resilience actions taken thus far included responsive fixes to past coast hazard events, such as adding backup power supply capability and raising electrical systems. More significant actions have included strengthening facilities and structures (likely following coastal hazard related damages), installing drainage pumps, and moving some operations indoors. Overall, limited plans to strengthen facilities and structures in the future could be attributed to damage previously sustained as well as plans to replace aging infrastructure. As reported in the survey, there were few plans for resilience improvements that looked out to expected environmental conditions beyond the very near term.

The survey responses suggest a significant mismatch between shipbuilding industry goals and objectives in meeting the U.S. military and commercial fleet’s building, repair, and maintenance needs and requirements, and the industry’s coastal hazard resiliency planning. This mismatch centers on the reality of increasing coastal hazards and threats to operations, and the industry’s overall climate change readiness. There are many logical, rational, explanations for this, as discussed in detail in other works (e.g., McLean and Becker Citation2021). For other sectors, reasons typically include a lack of funding, uncertainty about what future conditions will look like, a lack of understanding of the risk, or a lack of incentives to take action. While such lines of inquiry were outside the scope of this paper, discovering the decision-making barriers unique to the shipyard industry would go a long way toward helping build capacity for resilience building for the sector as a whole.

The survey results suggest that the U.S. did not yet have a climate-ready shipbuilding industry. Like the seaport industry reported on in 2012 (Becker et al. Citation2012), the shipyard industry did, however, recognize the implications of continued sea level rise, more intense tropical storms, higher tides, and flooding from a variety of causes. Respondents do believe that coastal hazards pose risks to contract deliverables and, overall, will weaken the overall ability to build, repair and maintain the U.S. fleet in the next 30 years. However, results also suggest that few concrete steps had been taken to enhance resilience in preparation for these environmental changes. As stated in the 4th National Climate Assessment, ‘Without adaptation, climate change will continue to degrade infrastructure performance over the rest of the century, with the potential for cascading impacts that threaten our economy, national security, essential services, and health and well-being.’ (USGCRP Citation2018). For shipyards, such actions may include hardening infrastructure, system redundancy, or moving operations inland where possible. However, results from this survey suggest that shipyard decision makers were not yet undertaking or planning for such adaptation.

A vulnerability and resilience assessment can also serve as a foundational step for shipyards to better understand these challenges. Guidance on this is forthcoming (CISA and ERDC Citationforthcoming, In review), but typical steps include: (1) Explore hazards, including developing an inventory of assets and hazards faced; (2) Assess vulnerability and risks; (3) Investigate options for adaptation, primarily using the more than 140 cases studies across all U.S. regions which identify data, expertise, methods and other resources used; (4) Prioritize and plan, accounting for the magnitude of a consequence and its probability of occurring (Gardner et al., Citation2019). The U.S. Climate Resilience Toolkit (https://toolkit.climate.gov/) also offers leaders, engineers and planners who are concerned or uncertain about current and future coastal hazards and impacts on build and repair operations. All of these guidance documents underscore the importance of sector partnerships in reducing vulnerabilities, minimizing consequences, and developing joint federal, state, and local protective programs and resiliency strategies.

5.1. Recommendations

The effects of coastal hazards as amplified by climate change could weaken the U.S. shipbuilding and ship repair industry. Based on survey results, recommendations to advance shipyard coastal hazards resilience include:

Shipyards should conduct a thorough coastal hazards vulnerability assessment.

Based on climate change predictions, shipyards should develop resourced strategic and action plans with specific objectives for improving coastal hazards resilience.

Incentives for shipbuilders and repairers to mitigate coastal hazard threats should be addressed and identified by the industry and appropriate federal agencies.

The Shipbuilders Council of America and other domestic shipbuilding professional organizations should compile and disseminate shipyard best climate change adaptation and resilience policies and practices.

The implications of a weakened shipbuilding industry due to climate change on national interests, both security and economic, should be further researched by the appropriate agencies and DOD senior service schools.

U.S. policymakers should continue to be informed of coastal hazard risks to coastal populations and infrastructures. The Congressional Research Service’s (CRS) Sea-Level Rise and U.S. Coasts: Science and Policy Considerations (2016) should be updated to include risks to coastal strategic industries, including the shipbuilding and repair industry (Folger and Carter Citation2016)

5.2. Limitations

Research and data analysis limitations include the number of respondents, accounting for the size and type of shipyards, and the scope of aggregate build and repair orders. As seen in , large areas of the U.S. are not included in our survey responses (e.g., California and Texas). We note that the U.S., being a very large country, presents different hazard challenges in different regions. For example, the West Coast is more prone to earthquakes and wildfires, while the Northeast gets snowstorms and hurricanes. Thus, survey respondents from different regions framed ‘coastal hazards’ differently. For this initial baseline survey, we felt it was important to gauge how the industry as a whole considered coastal hazard resilience by analyzing the types of hazards which posed challenges to shipyard operations, the extent of shipyard preparations based on future coastal hazard predictions, and the potential impact on contract deliverables. There would be value in considering variation in responses according to shipyard geographical and physical infrastructure characteristics. Unfortunately, such analysis proved to be outside the scope of this study for a two main reasons. First, the U.S. shipbuilding and repair industry is very competitive as to commercial and government build and repair contracts and, as such, to maximize survey response, we conducted this as an industry-wide anonymous survey and promised to report the results in aggregate form only. Second, our sample size was not large enough to be able to make meaningful comparisons within our dataset. We received responses from 45 of the 149 active shipyards that we contacted in our sample population, equating to a response rate of 30%, which represents about 15% of the full population of 300 shipyards identified. We felt this was an adequate response rate to report results in aggregate, but not to compare within our sample. Recruitment of participants proved to be an incredible challenge, despite having a strong steering committee consisting of well-known figures in the shipyard industry to lend credibility and validity to the project. Many man hours were spent emailing and calling shipyard representatives to encourage them to assist. Additional targeted surveys, along with case studies, are needed to explore other aspects of the hazards-challenge for shipyards, along with the consequences to US economic and military security that may result from a climate vulnerable strategic U.S. shipbuilding and repair industry.

6. Conclusions

This research project provides a baseline understanding of the U.S. shipbuilding industry’s considerations of coastal hazard resilience. The overall results of the survey suggest the U.S. shipbuilding and ship repair industry was not adequately responding to climate change predictions, was overall not well-informed about the scientific consensus on these issues and was not preparing and planning for the level of resiliency needed due to amplified coastal hazards. Most resilience actions which had been taken have been a result of past weather events. As the reality of climate changes takes hold, more actions will likely be planned, and resilience improved. A few yards already had and/or were planning to strengthen facilities, structures, and bulkheads—a good but inadequate start, given the increased rate of climate change expected. Lack of planning will likely impact operations and ship build, repair, and maintenance orders, potentially affecting U.S. national security interests.

We hope that this baseline survey provides empirical support for new research that can benefit the resilience building process for this critical industry. Naturally, other countries face similar or worse challenges and additional research is necessary to identify the best path forward for the maritime industry as a whole. New knowledge is needed to bridge the gap between the priorities of private sector industry like major ship and repair yards and the public benefits derived from the business they conduct. Additional research questions include: What strategies can be implemented to incentivize resilience for the shipyard industry? How can federal funding support be equitably distributed to support these private industries to the benefit of the national goals? How might shipyard and repair facilities be consolidated if all individual facilities cannot be protected? Before researchers can begin to address such issues, they must start with the foundational knowledge that there is, indeed, a problem in need of solutions. The results of this survey suggest that shipyard decision makers had not yet taken action to address the increase in natural hazard events associated with climate change. We sincerely hope that future researchers will use this paper as a platform from which to conduct more quality research.

Acknowledgments

We wish to thank the survey respondents and also the members of the Steering Committee, who were invaluable in helping to develop the distribution list, spreading the word, and encouraging survey participation, identifying the right survey questions, and providing feedback on all aspects of the research projects. Those steering committee members are:

RADM Chris McMahon, USMM (Ret,), MARAD, Naval War College

Mr. Ron O’Rourke, Specialist in Naval Affairs, Congressional Research Service (observer)

CAPT Christopher Mills, USN, National War College, National Defense University

CAPT Curtis Duncan, USN, Director Maritime Domain Industry Group, Eisenhower School, National Defense University

Mr. Charles Younger, Jr., (former) VP Technology and Business Development, Halter Marine

CAPT David Obermeier, USCG, Industrial Manager, U.S. Coast Guard Yard

Mr. David Heller, Director Shipyards, Maritime Administration

LT Richard Rodriguez, LT, USN, National War College

Mr. David Matsuda, Director, Small Shipyard Grant Coalition

We would also like to acknowledge the members of the University of Rhode Island Marine Affairs Coastal Resilience Laboratory students for their input into the development of this research project.

Disclosure statement

No potential conflict of interest was reported by the author(s).

References

- Azevedo de Almeida, B., and A. Mostafavi. 2016. “Resilience of Infrastructure Systems to Sea-Level Rise in Coastal Areas: Impacts, Adaptation Measures, and Implementation Challenges.” Sustainability 8 (11): 1115. doi:10.3390/su8111115.

- Becker, A. 2020. “Climate Change Impacts to Ports and Maritime Supply Chains.” Maritime Policy & Management 47 (7): 849–852. doi:10.1080/03088839.2020.1800854.

- Becker, A., S. Inoue, M. Fischer, and B. Schwegler. 2012. “Climate Change Impacts on International Seaports: Knowledge, Perceptions, and Planning Efforts among Port Administrators.” Climatic Change 110 (1–2): 5–29. doi:10.1007/s10584-011-0043-7.

- CISA (Cybersecurity and Infrastructure Security Agency) and ERDC (US Army Corps of Engineers Engineering Research and Development Center). forthcoming. In Review. Resilience Assessment Guide for Ports and the Maritime Transportation System Arlington VA and Washington D.C

- Clark, B., T. Walton, A. Lemon, B. Bergloff, and B. McGraph, (2019) CSBA Center for Strategic and Budgetary Assessments, National Security Contributions to the U. S. Maritime Industry. Accessed 28 February 2022. https://CSBAonline.org/research/publications/national-security-contributions-of-the-U.S.-Maritime-Industry

- Colton, T. n.d. “Shipbuilding History”. Accessed 6 January 2022. www.shipbuildinghistory.com

- Eckstein, M. 21 March 2019. “30-year Plan: Navy Puts 355-ship Cap on Fleet Size; Plans to Introduce Large Combatant, CHAMP Auxiliary Hull.” U.S. Naval Institute News. https://news.usni.org/2019/03/21/long-range-ship-plan-outlines-355-ship-cap-on-fleet-size-plans-to-introduce-large-combatant-champ-auxiliary-hull

- Folger, P., and N. T. Carter . “Sea-level Rise and U.S. Coasts: Science and Policy Considerations.” Congressional Research Service (CRS) Reports and Issue Briefs. 12 September 2016. https://crsreports.congress.gov/product/pdf/R/R44632

- Gardner, E., D. Herring, and J. Fox 2019. ”The U.S. Climate Resilience Toolkit: Evidence of Progress.” Climate Change 153 (4): 477–490. Accessed 26 Feburary 2022. doi:10.1007/s10584-018-2216-0.

- IPCC (Intergovernmental Panel on Climate Change). 2021. “Summary for Policymakers.” In V. Masson-Delmotte, P. Zhai, A. Pirani, S. L. Connors, C. Péan, S. Berger, N. Caud, et al. edited by, Climate Change 2021: The Physical Science Basis. Contribution of Working Group I to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change, Cambridge University Press, Cambridge, United Kingdom and New York, NY, USA. doi:10.1017/9781009157896.001.

- Izaguirre, C., I. J. Losada, P. Camus, J. L. Vigh, and V. Stenek. 2020. “Climate Change Risk to Global Port Operations.” Nature Climate Change. doi:10.1038/s41558-020-00937-z.

- Jacobs, J. M., L. R. Cattaneo, W. Sweet, and T. Mansfield. 2018. “Recent and Future Outlooks for Nuisance Flooding Impacts on Roadways on the U.S. East Coast.” Transportation Research Record: Journal of the Transportation Research Board 2672 (2): 1–10. doi:10.1177/0361198118756366.

- Junglas, I., and B. Ives. 2007. “Recovering IT in a Disaster: Lessons from Hurricane Katrina.” MIS Quarterly Executive 6 (1): 39–51. https://aisel.aisnet.org/misqe/vol6/iss1/7/

- Knutson, T. 9 August 2021. “Global Warming and Hurricanes. National Oceanic and Atmospheric Administration.” Geophysical Fluid Dynamics Laboratory. Accessed 15 January 2022. https://www.gfdl.noaa.gov/global-warming-and-hurricanes/

- Lazarus, E. D., and L. A. Ziros. 2021. “Yachts and Marinas as Hotspots of Coastal Risk.” Anthropocene Coasts 4 (1): 61–76. doi:10.1139/anc-2020-0012.

- Lazo, J. K., M. Lawson, P. H. Larsen, and D. M. Waldman. 1 June 2011. “U.S. Economic Sensitivity to Weather Variability.” Bulletin of the American Meteorological Society 92 (6): 709–720. 10.1175/2011BAMS2928.1.

- Ludlam, D. M. 1963. “Early American Hurricanes 1492-1870.” American Meteorological Society. University of Michigan Libraries. https://babel.hathitrust.org/cgi/pt?id=mdp.39015002912718&view=1up&seq=1

- MARAD (US Maritime Administration). 2018. “Report on Survey of U.S. Shipbuilding and Repair Facilities.” Office of Shipbuilding and Marine Technology. U.S. Department of Transportation. Accessed 15 Feburary 2022. https://www.maritime.dot.gov/sites/marad.dot.gov/files/docs/ports/national-maritime-resource-and-education-center/9491/2004-reportonsurveyofusshipbuildingandrepairfacilities.pdf

- MARAD (US Maritime Administration). 2021. “The Economic Importance of the U.S. Private Shipbuilding and Repairing Industry.” U.S. Department of Transportation. https://www.maritime.dot.gov/sites/marad.dot.gov/files/2021-06/Economic%20Contributions%20of%20U.S.%20Shipbuilding%20and%20Repairing%20Industry.pdf

- McLean, E. L., and A. Becker. 2021. “Advancing Seaport Resilience to Natural Hazards Due to Climate Change: Strategies to Overcome Decision Making Barriers.” Frontiers in Sustainability 2. doi:10.3389/frsus.2021.673630.

- Moftakhari, H. R., A. AghaKouchak, B. F. Sanders, D. L. Feldman, W. Sweet, R. A. Matthew, and A. Luke. 2015. “Increased Nuisance Flooding along the Coasts of the United States Due to Sea Level Rise: Past and Future.” Geophysical Research Letters 42 (22): 9846–9852. doi:10.1002/2015GL066072.

- Neumann, J. E., K. Emanuel, S. Ravela, L. Ludwig, P. Kirshen, K. Bosma, and J. Martinich. 2014. “Joint Effects of Storm Surge and sea-level Rise on US Coasts: New Economic Estimates of Impacts, Adaptation, and Benefits of Mitigation Policy.” Climatic Change 129 (1–2): 337–349. doi:10.1007/s10584-014-1304-z.

- O’Rourke, R. 2022a. “Coast Guard Cutter Procurement: Background and Issues for Congress.” Congressional Research Service (CRS) Reports and Issue Briefs. Accessed 3 January 2022. https://crsreports.congress.gov/product/pdf/R/R42567

- O’Rourke, R. 2022b. “Navy Force Structure and Shipbuilding Plans: Background and Issues for Congress.” Congressional Research Service Reports and Issue Briefs. Accessed 15 February 2022. https://sgp.fas.org/crs/weapons/RL32665.pdf

- PIANC (The World Association for Waterborne Transport Infrastructure). 2020. “Climate Change Adaptation Planning for Ports and Inland Waterways.” In PIANC Report No. 178, edited by Environmental Commission.

- Reidmiller, D. R., C. W. Avery, D. R. Easterling, K. E. Kunkel, K. L. M. Lewis, T. K. Maycock, and B. C. Stewart. 2017. “Fourth National Climate Assessment Volume II: Impacts, Risks, and Adaptation in the United States.” U.S. Global Change Research Program. National Oceanic and Atmospheric Administration. https://doi.org/10.7930/NCA4.2018

- Sea Level Rise Technical Report, NOAA, U.S. Climate Resilience Toolkit 2022. Accessed Feburary 22 2022. https://Oceanservice.NOAA.Gov/Hazards/sealevelrise/sealevelrise-tech-report-sections.html

- Sweeney, B., and A. Becker. 2020. “Considering Future Sea Level Change in Maritime Infrastructure Design: A Survey of US Engineers.” Journal of Waterway, Port, Coastal, and Ocean Engineering 146 (4). doi:10.1061/(asce)ww.1943-5460.0000583.

- Sweet, W. V., B. D. Hamlington, R. E. Kopp, C. P. Weaver, P. L. Barnard, D. Bekaert, W. Brooks, et al. 2022. “Global and Regional Sea Level Rise Scenarios for the United States: Updated Mean Projections and Extreme Water Level Probabilities along U.S. Coastlines.” NOAA Technical Report NOS 01. Edited by National Oceanic and Atmospheric Administration. National Ocean Service, Silver Spring, MD.

- USGCRP (United States Global Change Research Program). 2018. Impacts, Risks, and Adaptation in the United States: Fourth National Climate Assessment, Volume II — Summary Findings. D. R. Reidmiller, C. W. Avery, D. R. Easterling, K. E. Kunkel, K. L. M. Lewis, T. K. Maycock, and B. C. StewartEd. Washington, DC: U.S. Global Change Research Program.

- Verschuur, J., E. E. Koks, and J. W. Hall. 2020. “Port Disruptions Due to Natural Disasters: Insights into Port and Logistics Resilience.” Transportation Research Part D: Transport and Environment 85: 102393. doi:10.1016/j.trd.2020.102393.

- Wong, P. P., I. J. Losada, J.-P. Gattuso, J. Hinkel, A. Khattabi, K. L. McInnes, Y. Saito, and A. Sallenger. 2014. “Climate Change 2014: Impacts, Adaptation, and Vulnerability, Coastal Systems and low-lying Areas.” ( Chapter 5) 361–409. Intergovernmental Panel on Climate Change. https://www.ipcc.ch/site/assets/uploads/2018/02/WGIIAR5-Chap5_FINAL.pdf

- Yesudian, A. N., and R. J. Dawson. 2021. “Global Analysis of Sea Level Rise Risk to Airports.” Climate Risk Management 31. doi:10.1016/j.crm.2020.100266.

Appendix

Section 1: Respondent Background Information (SQs 1-7) (Demographics)

SQ1. The person completing the survey is a (position in shipbuilding industry, position at shipyard, i.e., CEO, industrial engineer, etc.).

SQ2. The person completing this survey has how many years of professional experience in the maritime industries (1–5, 16–20, etc.)

SQ3. The person completing this survey represents (large, medium, small private yard, public yard, etc.)

SQ4. Which of the following does your shipyard build, repair and/or maintain (check all that apply (military ships, small commercial ships, tugs, barges, etc.: build, repair, maintain)?

SQ5. If representing a shipyard or ship repair yard, it is in the: (Northeast Coast, Mid Atlantic Coast, Gulf Coast, Great Lakes, etc.).

SQ6. In your opinion, the person(s) at your shipyard who probably knows the most about potential coastal hazard impacts on the shipyard is the (CEO, COD, Facilities Engineer, etc.)

SQ7. How involved are you in the shipyard’s emergency management of coastal hazard events (e.g., storm surge, wind, waves, rain, tidal flooding)? flooding, tidal flooding, winds, waves, snow/ice)? (Mitigation of risk, disaster response, recovery, etc.: Very involved, somewhat involved, etc.)

Section 2: Consideration of Coastal Hazards Affecting Operations (SQs 8–11)

SQ8. Over the last five years, how often have the following coastal hazard events interrupted your shipyard’s operations per year (e.g., storm surge flooding—never, once, 2–6 times, etc.)

SQ9. What was the average duration of coastal hazard events over the last five years? (Storm surge flooding, tidal flooding, wind, etc.; hours, days, weeks, months, years, etc.)

SQ10. What extent of sea level rise (if any) does your shipyard leadership expect at the shipyard by 2050? (None, 0-.5 feet, 1.5 to 3 feet, etc.)

SQ11. Does your shipyard leadership expect increased frequency and/or intensity of tropical storm systems by 2050? (Yes, no, I don’t know.)

Section 3: Current Status of Preparations for Coastal Hazards and Operational Resiliency (SQs 12–13)

SQ12. Which of the following resilience actions have you taken, or do you plan to take? (Raise docks, raise electrical equipment, relocate some operations inland, etc., not planned, implemented pre-2015, under design, etc.)

SQ13. Please rate your personal feeling on the following statement: Coastal hazards will have a direct negative impact on my shipyard’s operations during the next 10–30 years. (Range from strongly disagree to strongly agree.)

Section 4: Need for Additional Preparations for Coastal Hazards Resiliency: (SQs 14–16)

SQ14. In your opinion, are there constraints that prevent additional preparations or investment for coastal hazards resiliency at your shipyard? (No constraints, limited financial resources, physical constraints and/or geography, etc.)

SQ15. Regardless of your opinions about sea level rise, what amount of rise would threaten your shipyard’s operations as they exist today in your opinion? (0.5 feet or more, 1 foot, 3 feet, etc.)

SQ16. What scientific data does your shipyard use to help inform decision making regarding coastal hazards resilience (e.g., flood maps, sea level rise projects, storm models)? Note: We decided this question did not adequately support RQ3; as such, it was not included in the final data analysis.

Section 5: Coastal Hazards Impact on Shipyard Operations (SQs SQ17–20)

SQ17. From your perspective, what are the three biggest coastal hazard threats to the U.S. shipbuilding and repair industry between now and 2050: (major hurricane, coastal land inundation, heavy precipitation events, etc.)

SQ18. Does your shipyard have cooperative or joint plans with other builders or other ‘work arounds’ to satisfy contract deliverables should your shipyard’s operations be degraded due to coastal hazards events? (Yes, no, I don’t know)

SQ19. Please rank order the potential risks to contract deliverables due to coastal hazard impacts on your shipyard’s operations: (physical damage to infrastructure, supply chain disruption, labor costs, materials cost increases, retention of workforce, etc.)

SQ20. What is your opinion of the following statement: The level of the U.S. shipbuilding industry’s coastal hazards resilience will have a significant impact on the industry’s ability to build, maintain, and repair the U.S. military and commercial fleet for the next 30 years? (Range of strongly disagree to strongly agree.)