Abstract

The BRICS (Brazil, Russia, India, China and South Africa) countries have agreed to strengthen their economic ties, thus paving the way for enhanced trade and investment performance. South Africa's strategic value in BRICS is that it is a gateway to the opportunity-rich Southern African Development Community (SADC). By using South Africa as a production hub for exports to the surrounding region, foreign investors would have ready access to neighbouring markets. This article addresses the question of whether, and in what ways, foreign direct investment (FDI) from the BRIC (Brazil, Russia, India and China) countries to the SADC influences the SADC's export performance. A series of empirical analyses revealed a positive causation between BRIC FDI and SADC exports, offering a clear incentive for the SADC to rejuvenate its trade and investment policies and structures, and strengthen its ties with BRIC countries in the interests of attracting more FDI and building a strong and sustainable export sector.

1. Introduction

The interest in African countries is growing. Ernst & Young's (Citation2013) attractiveness survey on Africa revealed that the negative perceptions of Africa can be traced to those companies that as yet have no involvement on the continent. The multinational enterprises (MNEs) that do find themselves in Africa are extending their footprint within the region, reinvesting, employing locals and looking for ways to take advantage of the unfolding growth potential.

In 2012, foreign direct investment (FDI) from developing countries to Africa was impressive, with the main sources of such FDI being Malaysia, South Africa, China and India. FDI from the BRIC (Brazil, Russia, India and China) countries has also been growing. For example, Brazil's public financial institutions have become significant investors in Africa, while Russian MNEs have been lured to the continent by the array of raw materials and expanding local consumer markets. In addition, Indian investors have been drawn to the tax benefits offered to purveyors of FDI in countries such as Mauritius, and China has afforded South Africa the status of main recipient of its FDI on the continent (UNCTAD, Citation2013).

The BRIC countries became the BRICS grouping when South Africa joined as an additional member in 2010 (Dubbelman, Citation2011). The BRICS partners, all prominent in their respective regions, have pledged to strengthen their economic ties and open up their borders to one another to stimulate intra-group trade and investment (Gordhan, Citation2011; BRICS Report, Citation2012).

With the inclusion of South Africa in the BRICS partnership and the members being spread over four continents, the question has been raised as to whether the Southern African Development Community (SADC) will benefit from this evolving alliance. South Africa, for example, derives its strategic value in BRICS from the fact that it constitutes a convenient gateway to other southern African countries. By investing in South Africa and using the country as the production hub for exports to the surrounding region, foreign investors in the BRIC countries would benefit from the preferential tariff regime and other advantages enjoyed by South Africa vis-à-vis its SADC partners. The leading role of South Africa within the SADC has also been established by Kabundi & Loots (Citation2007), where the co-movement between South Africa and the SADC has been explained. As the SADC's integration efforts continue to advance, intra-regional trade is a more viable option now than in the past (ITC, Citation2011), which strengthens South Africa's position as an intermediary between Africa and the rest of the world (Battersby & Lu, Citation2011). This could potentially stimulate South Africa's trade with, and attract more inward FDI from, the BRIC countries, which in turn would benefit the African continent as a whole (Chun, Citation2011).

African countries in general, and SADC countries in particular, are keen to attract FDI to strengthen their capacity and wherewithal to gain access to foreign markets, acquire managerial expertise, attract technological transfers and innovation-rich business opportunities, and boost employment (Mwilima, Citation2003). Notwithstanding the important role played by FDI, exports are still viewed as the main engine of countries’ growth. In fact, it is generally recognised that one of the benefits of FDI is the positive impact it has on the export performance of host countries. One of the key reasons why the SADC is intent on securing more inward FDI is that such investment has the potential to increase export competitiveness (SADC, Citation2011; TRALAC, Citation2012; DTI, Citation2013).

In recent years there has been an expanding body of literature on the FDI–export link in various countries (see, for example, UNCTAD, Citation2002; ITC, Citation2011; Reis & Farole, Citation2012). It is postulated that the effects of FDI can be separated into supply capacity-increasing effects and FDI-specific effects. The supply capacity-increasing effects arise when FDI inflows increase the host country's or region's production capacity, which in turn increases the export supply potential (Kutan & Vukšić, Citation2007). The FDI-specific effects refer to FDI having a specific effect on one or other element within the economy; that is, MNEs having a competitive advantage compared with local firms in the market. While the quantitative analyses offered by most of the existing literature are useful and informative, empirical analyses of the BRIC FDI–SADC exports nexus have not yet been attempted.

An empirical assessment of the role of FDI in export performance is important (SADC, Citation2011; TRALAC, Citation2012; DTI, Citation2013). This article tests the relationship between BRIC FDI inflows into the SADC and exports from the SADC, during the period 2003–11, with a view to establishing whether the region is benefitting from the BRIC FDI–SADC exports nexus.

The article is structured as follows: Section 2 explores the relationship between FDI and export performance, according to the latest literature on the topic; Section 3 presents the results of the empirical analysis of the BRIC FDI and SADC exports relationship; and Section 4 offers a summary of the findings, as well as some concluding remarks and recommendations.

2. The link between FDI and exports: literature overview

Against the backdrop of the growing literature on the FDI–export link, recent studies have used causality tests and regression models to test the relationship between FDI and export performance in developed, developing and African countries (Sun, Citation2001; Chédor et al., Citation2002; Dritsaki et al., Citation2004; Wong & Tang, Citation2007; Bezuidenhout & Naudé, Citation2010). Much of this research concludes that a bi-directional causal relationship exists, indicating that inward FDI has a positive influence on exports, and vice versa.

The extent of research conducted on the relationship between inward FDI and exports in developing countries exceeds that conducted on these variables in developed countries. One of the reasons for this could be that the need to improve the development status of developing countries attracts more attention than that of the developed countries. China is a developing country that has been the focus of many recent studies covering a variety of time series and country levels, with almost all of these studies providing evidence of a bi-directional causality between inward FDI and exports (Zhang & Song, Citation2001; Marchant et al., Citation2002; Zhang, Citation2005, Citation2006). The vast number of studies on China is a clear indication of the increasingly important role played by the country in the world economy.

In 2011, for the first time, the developing and transition economies attracted more than 50% of global FDI, while FDI flows to developed countries continued to decline (UNCTAD, Citation2011). This trend persisted in 2012, when developing economies received 52% of global FDI (UNCTAD, Citation2013).

Although a large number of studies have been conducted across the spectrum of developed and developing countries, few studies have focused specifically on the relationship between FDI and exports in Africa. The reasons for this are related to data constraints (a dearth of inward FDI data in previous years as well as unreliable trade data) and (perhaps) previously a lack of interest in Africa as the subject of research. The more prominent recent studies on Africa include Anyanwu (Citation2012), Wilson & Cacho (Citation2007), Ahmed et al. (Citation2007), Bezuidenhout (Citation2007) and Bezuidenhout & Naudé (Citation2008, Citation2010).

Anyanwu (Citation2012) asserted that African countries with a larger export base tend to attract more FDI. This view is supported by earlier studies that have focused on Africa, sub-Saharan Africa and the SADC's FDI–export relationship, respectively (Ahmed et al., Citation2007; Bezuidenhout, Citation2007; Hailu, Citation2010), which have also pointed to the existence of a bi-directional causal relationship between exports and FDI.

It is thus somewhat surprising that the study conducted by Samake & Yang (Citation2011) revealed that the correlation between outward FDI from the BRIC group and least industrialised countries' trade (exports and imports) with the BRIC countries is insignificant. One would expect FDI to induce positive spill-over effects in developing host countries, most noticeably through exports. However, the insignificant correlation most probably reflects the (still) early stages of BRIC FDI in the least industrialised countries as well as the dominance of BRIC economic growth (rather than FDI) in driving least industrialised countries’ trade performance.

The main recommendations that emerge from the literature with regard to Africa are that African countries should promote and attract FDI, create a favourable economic and commercial environment, adopt liberal policy reforms, and promote regional integration. Furthermore, greater efforts need to be made within the region to minimise the negative impacts and neighbouring country fallout effects that political instability can have on FDI (Ahmed et al., Citation2007; Bezuidenhout, Citation2007; Bezuidenhout & Naudé, Citation2008, Citation2010). Recommendations from MNEs with regard to Africa are that African countries should improve their transport and logistics infrastructure, and enforce anti-bribery and corruption initiatives in order to smooth the way for FDI inflows (Ernst & Young, Citation2013).

The earlier studies on SADC covered the period up to 2007 only. This study extends the analysis to 2011, making an important contribution to the literature because it takes into account the dynamics of the global financial crisis and its lingering after-effects, the increasing attention being paid to Africa, and the rising prominence of BRICS in the world economy.

3. Empirical analysis of the effects of BRIC FDI on SADC exports

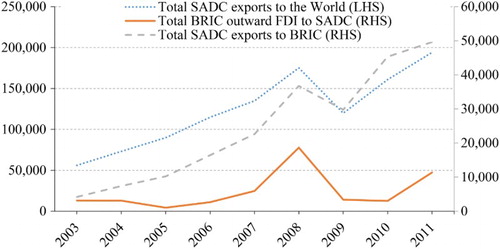

The case of BRIC countries and the SADC is of special significance. SADC member countries’ combined increase in exports, from US$56 billion in 2003 to US$194 billion in 2011, was accompanied by a substantial rise in FDI inflows (specifically from the BRIC countries), from about US$3 billion in 2003 to almost US$19 billion in 2008. FDI fell back to about US$3 billion by the end of 2010 but recovered to about US$11 billion in 2011 (see and ). Exports from the SADC region to the world rose much faster than those from the SADC to the BRIC countries (although from a lower base), resulting in BRIC's share in SADC's total exports being 26% in 2011.

Figure 1: BRIC outward FDI and SADC exports, 2003–11 (US$ million)

Sources: ITC (Citation2012), Zephyr (Citation2012) and FDImarkets® (Citation2012). Compiled by authors.

Table 1: BRIC outward FDI flows to SADC, SADC total exports and SADC exports to BRIC, 2003–11 (US$ million)

and reveal a connection between BRIC outward FDI to the SADC and SADC exports to the BRIC countries and the world, especially during the period 2006–09. The data suggest that BRIC FDI to the SADC might have a positive influence on SADC exports.

3.1 Data discussion

The following empirical analysis focuses on determining whether FDI stimulates exports, and aims to attach a weight to the influence of BRIC FDI on SADC member countries’ exports.

To run the analysis and have more data points, the examination was conducted on a per-deal basis.Footnote1 All FDI data used in the estimation of the models were taken from the FDImarkets® (Citation2012) and Zephyr (Citation2012) databases. Data on SADC exports to the world and to the BRIC countries were sourced from the ITC's (Citation2012) Trademap. For the purpose of this article, the period covered for FDI was from 2003 to 2010, and for exports was from 2003 to 2011. The reason for this difference is that FDI received in one year may only appear to have an impact on a specific country's/region's exports a year or more thereafter. This article specifically captures the impact of FDI on exports in the same year, as well as one year and two years ahead. Annual data for both FDI and exports were used, because monthly and quarterly statistics for the selected countries were not readily available. In addition, sectoral data were too limited for a meaningful econometric analysis to be conducted. However, it is interesting to note the dominance of a few industries – coal, oil and natural gas, and metals – within the SADC.

The total SADC exports to the world and to BRIC countries

were measured by total export values of the SADC countries, while the total aggregated BRIC FDI outflows (i.e.

) were calculated as the sum of the current values of mergers and acquisitions and Greenfield investments.Footnote2 Every SADC member country for which data for the relevant variables were available in the sources cited was included. As a result, there was no direct selection bias in the sample.

A number of statistical inference procedures were first analysed before the empirical methods employed were introduced. The descriptive statistics for all variables used in the regressions were tested and the data were, where necessary, transformed accordingly.

3.2 Correlation and covariance of SADC exports and BRIC FDI

presents correlation coefficients between SADC export destinations and BRIC FDI. There are notable and significant correlations in both cases – 96% of the variation in SADC exports to the world and 59% of the variation in SADC exports to BRIC. However, correlation does not necessarily imply causation. Yet this should not be taken to mean that correlation cannot potentially point to causal relations (Weinberg & Abramowitz, Citation2002:136). Whether a causal relationship exists is determined with the help of the Granger causality test.

Table 2: Correlation and covariance of SADC exports and BRIC FDI

A statistical problem that can be expected is the possibility that both FDI and exports, especially SADC exports to the world, are jointly increasing and decreasing due to an exogenous factor (not accounted for in the estimations performed). To address this issue, the authors conducted tests of first-order and second-order serial correlation in the residuals (see Section 3.5). It is important to note that one can adopt specification tests that detect serial correlation in the error term in a dynamic panel data model, where the disturbances are uncorrelated under the null hypothesis of no serial correlationFootnote3 and follow a moving average process under the alternative. The results of these specification tests provide stronger evidence of instrument validity than traditional over-identification tests which are known to have poor statistical power.

The preceding discussion and the bulk of the empirical work done to date suggest that FDI may have an impact on exports. If it can be established that there are positive FDI-specific effects on exports, then countries’ efforts in attracting FDI are warranted.

3.3 The regression estimation

The authors used an empirical model of exports to determine whether BRIC-specific FDI has contributed to the increase in SADC exports. In any study of the determinants of a country's or region's export performance, a number of empirical specifications can be considered. Since this article's focus is on the influence of FDI on exports, a simple model that captures and isolates the basis of this relationship was used.

BRIC FDI data used to capture the FDI-specific effects on SADC exports to the world were suspicious (with an exceptionally high R-square, adjusted R-square and t- and F-statistics), which appears to indicate that the impact of BRIC FDI on SADC exports to the world might be serially correlated. Corrective steps were taken and further hypothesis testing was carried out using ordinary least squares (OLS) estimates and the estimates corrected for serial correlation. It was found that the slope coefficients changed considerably, suggesting that misspecification rather than autocorrelation was the primary difficulty here. Accordingly, and given that the focus is on the link between FDI and exports, this model is not given further consideration in the ensuing discussion. Conversely, the estimations of the influence of BRIC-specific FDI on SADC exports to BRIC countries were robust with respect to heteroskedasticity and serial correlation, and are discussed in more detail.

To carry out the estimations of BRIC outward FDI on SADC exports to the BRIC countries, the following model was formulated:(1)

The addition of a constant term and a stochastic component to Equation (1) yielded the following econometric specification:(2)

where are export values (US$ millions) to the BRIC countries (

), respectively, with lags

(offering the best fit) to capture the two-year lagging effect of FDI on exports.

represents inward FDI to SADC countries originating in the BRIC countries, and

is a dummy to compensate for structural breaks.

The addition of a constant term and a stochastic component to Equation (1) yielded the econometric specifications: where is the value (US$ millions) change in exports with respect to FDI and

represents the ‘noise’ or error term.

and

represent the intercept and coefficients of the regression. The coefficient of regression

indicates how a unit change in BRIC FDI affects SADC exports to BRIC. Equation (2) constitutes the basis for the time-series analysis of the FDI and export data for the 13 SADC countries (excluding Swaziland and LesothoFootnote4) for 2003–11. For all variables, natural logarithms are taken. In both specifications, the dependent variable is the natural logarithm of real exports

.

The error term was included in Equation (2) to cater for other factors that might influence exports. Moreover, the power of the OLS method was determined by the Gauss–Markov assumptions. These assumptions are: that the dependent (exports) and independent (FDI) variables are linearly co-related; and that the estimators

are unbiased with an expected value of zero

. The latter suggests that on average the errors cancel each other out. Execution of the procedure includes specifying the dependent and independent variables (exports and FDI, respectively). However, given the aforementioned assumptions, the OLS results could be adversely affected by outliers. Also, although OLS can establish the reliance of either export on FDI, or vice versa, this does not infer direction of causation. Therefore, a different method, the Granger causality test, was used to further test for the direction of causality.

For the purpose of comparison, two variants of the model (see Equations (1) and (2)) for the full sample were estimated: one with dummy variables and the other without (see ). In each case, a regression was run which included FDI as the sole explanatory variable to show how important FDI is to a region's export performance. After experimentation with several lag lengths, the following estimated version of Equation 2 was found to fit the data satisfactorily. Finally, the significance of the error correction term suggests that exports and FDI are co-integrated.

Table 3: Estimates of the FDI–export link for all SADC countries

Given the aforementioned issues (i.e. stationarity and co-integration), all variables were transformed to logarithms and, according to both the Augmented Dickey Fuller and Phillips–Perron unit root tests, all variables were stationary in levels. After obtaining OLS results, White's test was used to test for heteroskedasticity. The null hypothesis of heteroskedasticity was not rejected as all of the p-values were significantly higher than the 0.05% level of statistical significance. Accordingly, White's heteroskedasticity-corrected standard errors and t-statistics were used in the final estimations to correct for heteroskedasticity.

The relationship underlying Equation 2 (reflected in ) was:

Firstly, the fit of the regressions in Models 1 and 2 was good with significant F-statistics at the 1% level.

BRIC FDI seems to have a significant influence on SADC exports to BRIC countries. This reinforces the notion that BRIC countries are investing in SADC countries with the aim of re-exporting to the home country. In all cases, the FDI variable had relatively large and statistically significant coefficients. The adjusted R-squared (0.53) of Model 2 in suggests that approximately 53% of the variance in the SADC exports to the BRIC countries is explained by BRIC FDI.

It should be pointed out that at least two aspects of the estimates reported here might seem troublesome. One is the possibility of heteroskedasticity in the disturbance term. This, however, has been compensated for by using White's heteroskedasticity-corrected standard errors and t-statistics in the final estimations. The other troublesome aspect is the feedback from the dependent variable. This can be addressed through causality tests, which will be discussed in the next section.

3.4 The Granger causality tests

Theory suggests that FDI and exports are interlinked and correlated through various channels. However, there is no theoretical or empirical evidence that conclusively indicates sequencing from either direction. Given this uncertainty, the question that now needs to be asked is: what is the relationship between FDI inflows and exports?

To answer this, Granger causality tests were carried out on the relationship between FDI and recipient country/region exports using a panel of the SADC countries. Given that the data were not strictly time series but rather a set of observations, they had to be restructured in the form of a panel so that the Granger causality test could be successfully performed. This was done by differentiating the aggregated data by SADC partner country and by year for BRIC FDI, as well as SADC exports to BRIC and to the world. A (panel) time series is said to Granger cause

if it can be shown that those

values provide statistically significant information about future values of

. This entailed running the following two regression equations using FDI and exports panels:

(3)

and(4)

where are total SADC exports, and alternatively, total exports to the world

and total exports to the BRIC

countries,

are total FDI inflows from BRIC to the SADC, and

and ε

are random errors. To test whether

‘Granger causes’

, or vice versa, the test for the joint significance of the

and γ

coefficients in Equations (3) and (4) under the null hypothesis of no causality was undertaken. The results of these tests, with

(the lag lengthFootnote5) = 1, 2 and 3 for both SADC exports to the world and to BRIC, are contained in .

Table 4: Granger causality test results: SADC exports and BRIC FDI, 2003–11 (US$ million)

The results in indicate that BRIC FDI inflows Granger cause SADC exports to the world, and vice versa (at least in the short run), but not to the BRIC countries. These results should, however, be viewed with caution since, as indicated in , SADC exports to the world have suspiciously high R-squared, adjusted R-squared, and t- and F-statistics, which might indicate that BRIC FDI and SADC exports to the world are serially correlated. However, the results presented in , together with the previous estimation, provide tentative evidence of a strong bi-directional relationship between BRIC FDI and SADC exports to the world.

3.5 Panel data analysis of FDI and exports

This section aims to build on the Granger causality results by analysing the empirical relationship between BRIC FDI and SADC exports to the world and to the BRIC countries, respectively. In particular, the panel data causality testing method developed by Holtz-Eakin et al. (Citation1989) (see also Anderson & Hsiao [Citation1981] for a similar discussion) was used and estimated by applying the system generalised method of moments (GMM) technique. Conventional GMM estimation is not optimal when the descriptive variables exhibit persistence over time, as may be expected with FDI. To control for this, the system GMM estimator is used – which pools the regression equation in first differences with that in levels, instrumented with lagged levels of the regressors in the former case and with lagged differences of the regressors in the latter case. The test involved an estimation of the following error correction equations:(5)

and(6)

where denotes exports,

signifies the outward FDI flows and

indicates the time effects. The parameters

and

represent the error correction term. The error correction term and the long-run coefficient were used to test long-run Granger causality. In particular, the question of whether or not

causes

can be tested with the hypothesis:

The key parameter of interest is the long-run impact of exports on FDI, and vice versa.

The equations were estimated using the one-step system GMM method with t-values and test statistics that were asymptotically robust to general heteroskedasticity and corrected for a small sample bias (Falk & Hake, Citation2008). The system GMM results used 104 observations on 13 SADC countries from 2003–11. Two types of diagnostic tests were conducted for the empirical models ( and ). Firstly, tests of first-order and second-order serial correlations in the residuals were conducted. The AR 2 test statistics of the residuals did not reject the specification of the error term. Secondly, in looking at the Sargan tests, one can see that the p-values of the regressions relating SADC exports to the world on BRIC FDI, as well as BRIC FDI on SADC exports to the world, did not indicate a decisive rejection of the models’ over-identifying restrictions. In contrast, for the impact of BRIC FDI on SADC exports to the BRIC countries, and vice versa, it was found that the instruments were invalid.

Table 5: Dynamic panel data estimates of the link between SADC exports to the world and BRIC FDI

Table 6: Dynamic panel data estimates of the link between SADC exports to BRIC and BRIC FDI

The results of the dynamic panel data estimations presented in show that BRIC FDI has a strong positive effect on SADC exports to the world. This implies that BRIC FDI Granger causes SADC exports to the world in the long run. The long-run elasticity is around 0.70, while the short-run elasticity is 0.49. The error correction coefficient is negative (−0.244) and statistically significant at the 5% level, indicating that there is an equilibrium relationship in the long run. Yet the speed of adjustment is quite low, indicating a large degree of perseverance. In contrast, no statistically significant long-run impact of BRIC FDI on SADC exports to the world was found. These results imply bi-directional causality between BRIC FDI and SADC exports to the world (only in the short run, since no notable long-run relationship exists).

The results of the dynamic panel data estimations presented in show that SADC exports to BRIC do not have a significant short-run impact, but do show a strong positive effect on BRIC FDI inflows in the long run. The long-run elasticity is around 0.72, while the short-run elasticity is 0.22. The error correction coefficient is negative (−0.490) and statistically significant at the 1% level, indicating that there is an equilibrium relationship in the long run. Similarly (and in contrast to the results in ), one can discern a statistically significant long-run impact of BRIC FDI in relation to SADC exports to the BRIC countries. However, in looking at the Sargan test results, one can see that the p-values of the regressions relating SADC exports to the BRIC countries on BRIC FDI, as well as BRIC FDI on SADC exports to the BRIC countries, indicate a decisive rejection of the models’ over-identifying restrictions, signifying that the instruments were invalid. Therefore, a significant influence from one to the other, or vice versa, could not be established.

In summary, this section examined the link between BRIC FDI to SADC exports to the world and to the BRIC countries, respectively, using the Holtz-Eakin panel causality tests. Estimates using system GMM estimators revealed that, despite the results presented in showing the link between SADC exports to the BRIC countries and BRIC FDI to the SADC to not be reliable, SADC exports to the world do matter from an FDI perspective, and vice versa.

The system GMM results are preferred over the fixed-effects regression results since no lagged endogenous effect of FDI on exports, and vice versa, are included in the latter. This implies that the static equation represents a long-run relationship only. Moreover, the results are consistent with the majority of recent empirical studies that have uncovered a bi-directional relationship, meaning that FDI and exports tend to be complements rather than substitutes.

4. Summary of key findings and concluding remarks

The authors have established the influence of BRIC FDI inflows on SADC exports both to the BRIC countries and to the world. In this study, FDI has emerged as an accelerator of the recipient country's or region's economic growth. One of the main ways in which FDI potentially contributes to growth is by boosting host countries’ or regions’ exports by increasing supply capacity.

The correlation analysis highlighted notable and significant correlations between FDI and exports, with a strongly positive and significant relationship between BRIC FDI inflows and SADC exports to the world (at 96%), as well as a positive correlation between BRIC FDI inflows and exports to the BRIC countries (at 59%). Moreover, the results agree with the correlation between FDI and exports as conducted in recent empirical studies, discussed earlier in Section 2 (Bezuidenhout & Naudé, Citation2008, Citation2010).

The regression analysis revealed that BRIC FDI and SADC exports to the world may be serially correlated, and furthermore that approximately 53% of the variance in SADC exports to the BRIC countries can be explained by BRIC FDI only. Also, the estimates of BRIC FDI are consistent with the theoretical prediction and widely held belief that SADC countries with more BRIC FDI inflows tend to export relatively more to the BRIC countries.

From the Granger causality results it is evident that there is a bi-directional relationship between BRIC FDI and SADC exports to the world, whereas the opposite is true for SADC exports to the BRIC countries. The null hypothesis of no causality could not be rejected. These results should nevertheless be viewed with caution since, as indicated in previous estimations, SADC exports to the world have suspiciously high R-squared, adjusted R-squared, and t- and F-statistics. These results might indicate that there are other factors not accounted for in the current analyses which might be driving both BRIC FDI and SADC exports to the world.

The panel data estimation built on the Granger causality results from analysing the empirical relationship between BRIC outward FDI and SADC exports to the world and to the BRIC countries, respectively. The FDI and export data were restructured in the form of a panel and a panel data causality testing method was applied, after which the link between BRIC FDI and SADC exports to the world and to the BRIC countries was examined using the Holtz-Eakin panel causality tests. Assessments using system GMM estimators showed that SADC exports to the world matter for FDI, and vice versa. Conversely, the results of the causality tests pertaining to SADC exports to the BRIC countries and BRIC FDI were not reliable. These findings are also consistent with the Granger causality results mentioned above.

Meanwhile, the impact of BRIC FDI to the SADC countries on SADC exports to BRIC does not conclusively indicate that FDI matters for exports, or vice versa. Regression results, however, show that 59% of variations in SADC exports to the BRIC countries are explained by BRIC FDI. Despite the possibility of other, existing factors that could lead to FDI and exports having similar tendencies, it should be noted that the influence of BRIC FDI matters to SADC exports to the world. These results are consistent with recent empirical studies that have revealed a bi-directional relationship between inward FDI and exports.

On the basis of this study, a number of recommendations can be directed at SADC's export and investment promotion organisations and industry associations.

Higher levels of cooperation among the SADC countries should be advocated if the SADC is to appear more attractive to BRIC investors, particularly because one of the prerequisites for FDI is the ease of access into neighbouring territories. South Africa, as the economic leader of the SADC, should play a more proactive role in order to be viewed by the BRIC countries as a desirable investment location well into the future.

The SADC should work on putting into place a stable support and a reliable infrastructure network to enable SADC member countries to improve their export potential and increase the investment received. This will benefit the economies of the member countries.

Owing to insufficient data regarding inward FDI at sectoral and country level within the SADC, and because the results of the study indicate that BRIC FDI inflows have contributed to higher exports from the SADC region (specifically SADC exports to the world), a continuous review of the situation at country and sectoral level is necessary as time goes by. The latter, moreover, would add to the authors’ understanding of the role of BRIC within the SADC's trade and investment environment.

Finally, the significance of BRIC FDI for SADC exports to the world should be an incentive for the SADC to motivate for greater co-integration, cooperation and participation within the BRICS grouping as a whole. A stronger BRICS partnership has the potential to drive more FDI to the SADC, with further positive spinoffs for the region's exports.

Disclosure statement

No potential conflict of interest was reported by the authors.

Notes

1Per-deal basis refers to a measure used to quantify an aspect of one deal concluded by a company. An example would be Barclays Bank (UK) acquiring a stake in ABSA Bank (South Africa) for US$5 billion in 2005.

2It is necessary to include both mergers and acquisitions and Greenfield investments into total FDI outflow data because both could potentially contribute to exports, whether through the production of raw materials, manufactured goods or facilitating exports through the availability of financial services. BRIC Greenfield investments dominate the SADC FDI scene with an average of 81% contribution to total FDI between 2003 and 2010 (FDImarkets, Citation2012; Zephyr, Citation2012).

3More specifically, the null hypothesis that the errors are serially uncorrelated is H0: p = 0.

4These two SADC member countries were excluded from the analyses due to no inward FDI flows from the BRIC group being recorded during the period under review.

5The minimum number of lags that can be added is one.

References

- Ahmed, A, Cheng, E & Messinis, G, 2007. Causal links between exports, FDI and output: Evidence from Sub-Saharan African countries. Working paper 35, Victoria University, Centre for Strategic Economic Studies.

- Anderson, TW & Hsiao, C, 1981. Estimation of dynamic models with error components. Journal of the American Statistical Association 76(375), 598–606. doi: 10.1080/01621459.1981.10477691

- Anyanwu, JC, 2012. Why does foreign direct investment go where it goes? New evidence from African countries. Annals of Economics and Finance 13(2), 425–62.

- Battersby, J & Lu, Y, 2011. More than just another BRIC in the wall. South Africa Info, 25 July. http://www.southafrica.info/business/trade/relations/brics-220711.htm Accessed 16 February 2012.

- Bezuidenhout, H, 2007. Trade patterns and foreign direct investment in the Southern African Development Community. PhD thesis, North-West University, Potchefstroom, South Africa.

- Bezuidenhout, H & Naudé, W, 2008. Foreign direct investment and trade in the Southern African Development Community. WIDER Research Paper no. 2008/88. http://www.wider.unu.edu/publications/working-papers/research-papers/2008/en_GB/rp2008-88/ Accessed 28 February 2012.

- Bezuidenhout, H & Naudé, W, 2010. Foreign direct investment and trade in the Southern African Development Community. In Santos-Paulino, A & Wan, G (Eds.), Southern engines of global growth, 263–82. Oxford University Press, New York.

- BRICS Report, 2012. A study of Brazil, Russia, India, China, and South Africa with special focus on synergies and complementarities. Oxford University Press, New Delhi.

- Chédor, S, Mucchielli, J & Soubaya, I, 2002. Intra-firm trade and foreign direct investment: An empirical analysis of French firms. In Mucchielli, JL & Lipsey, RE (Eds.), Multinational firms and impacts on employment, trade and technology: New perspectives for a new century, 84–100. Routledge, London.

- Chun, Z, 2011. South Africa's distinctiveness in BRICS. China-US Focus, 25 April. http://chinausfocus.com/foreign-policy/south-africa%E2%80%99s-distinctiveness-in-brics/ Accessed 16 February 2012.

- Dritsaki, M, Dritsaki, C & Adamopoulos, A, 2004. A causal relationship between trade, foreign direct investment and economic growth for Greece. American Journal of Applied Sciences 1(3), 230–35. doi: 10.3844/ajassp.2004.230.235

- DTI (Department of Trade and Industry). 2013. Trade and investment South Africa. http://www.thedti.gov.za/about_dti.jsp Accessed 10 January 2013.

- Dubbelman, B, 2011. South Africa's role in BRICS: Implications and effects. Creamer Media, July. http://uscdn.creamermedia.co.za/assets/articles/attachments/34069_sa_role_in_bricsreduced.pdf Accessed 14 February 2012.

- Ernst & Young. 2013. Ernst & Young's attractiveness survey, Africa 2012: Getting down to Business. http://www.ey.com/Publication/vwLUAssets/Africa_Attract_2013_Getting_down_tobusiness/$FILE/Africa_attractiveness_2013_web.pdf Accessed 5 November 2013.

- Falk, M & Hake, M, 2008. A panel data analysis on FDI and exports. FIW Research Reports series I-012, FIW. http://www.wifo.ac.at/jart/prj3/wifo/resources/person_dokument/person_dokument.jart?publikationsid=34229&mime_type=application/pdf Accessed 13 January 2013.

- FDImarkets®, 2012. FDImarkets®: Crossborder investment monitor. http://www.fdimarkets.com/ Accessed 29 July 2012.

- Gordhan, P, 2011. An emerging new world order. The Cairo Review of Global Affairs, 11 July. http://www.aucegypt.edu/gapp/cairoreview/pages/articleDetails.aspx?aid=75 Accessed 16 February 2012.

- Hailu, ZA, 2010. Impact of foreign direct investment on trade of African countries. International Journal of Economics and Finance 2(3), 112–33. doi: 10.5539/ijef.v2n3p122

- Holtz-Eakin, D, Newey, WK & Rosen, HS, 1989. Implementing causality tests with panel data, with an example from local public finance. NBER Technical Working Papers no. 0048. http://www.nber.org/papers/t0048 Accessed 6 June 2012.

- ITC (International Trade Centre), 2011. National trade policy for export success. http://www.intracen.org/uploadedFiles/intracenorg/Content/Publications/National%20Trade%20Policy%20for%20Export%20Success_web.pdf Accessed 24 July 2012.

- ITC (International Trade Centre), 2012. Trademap. Trade statistics for international business development. http://www.trademap.org/Bilateral_TS.aspx Accessed March – December 2012.

- Kabundi, A & Loots, E, 2007. Co-movement between South Africa and the Southern African Development Community: An empirical analysis. Economic Modelling 24, 737–48. doi: 10.1016/j.econmod.2007.02.001

- Kutan, AM & Vukšić, G, 2007. Foreign direct investment and export performance: Empirical evidence. Comparative Economic Studies 49, 430–45. doi: 10.1057/palgrave.ces.8100216

- Marchant, MA, Cornell, DN, & Koo, W, 2002. International trade and foreign direct investment: Substitutes or complements? Journal of Agricultural and Applied Economics 34(2), 289–302.

- Mwilima, N, 2003. Foreign direct investment in Africa. African Labour Resource Unit (Final Draft Report). http://www.sarpn.org/documents/d0000883/P994African_Social_Observatory_PilotProject_FDI.pdf Accessed 8 June 2012.

- Reis, JG & Farole, T, 2012. Trade competitiveness diagnostic toolkit. World Bank Publications, Washington.

- SADC (Southern African Development Community), 2011. Regional indicative strategic development plan. http://www.sadc.int/files/5713/5292/8372/Regional_Indicative_Strategic_Development_Plan.pdf Accessed 8 January 2013.

- Samake, I & Yang, Y, 2011. Low-income countries’ BRIC linkage: Are there growth spillovers? IMF Working Paper no. WP/11/267. http://www.imf.org/external/pubs/ft/wp/2011/wp11267.pdf Accessed 6 December 2012.

- Sun, H, 2001. Foreign direct investment and regional export performance in China. Journal of Regional Science 41(2), 317–36. doi: 10.1111/0022-4146.00219

- TRALAC (Trade Law Centre), 2012. The regional indicative strategic development plan: SADC's trade-led integration agenda: how is SADC doing? TRALAC trade brief no. S12TB02/2012. http://www.tralac.org/files/2012/04/S12TB022012-SADC-RISDP-SADC-agenda-20120418.pdf Accessed 17 February 2013.

- UNCTAD (United Nations Conference on Trade and Development), 2002. World Investment Report (2001 and 2002). United Nations Publications, Geneva.

- UNCTAD (United Nations Conference on Trade and Development), 2011. World Investment Report 2011. Non-equity modes of international production and development. United Nations Publications, Geneva.

- UNCTAD (United Nations Conference on Trade and Development), 2013. World Investment Report 2013. Global value chains: investment and trade for development. United Nations Publications, Geneva.

- Weinberg, SL & Abramowitz, SK, 2002. Data analysis for the behaviour sciences using SPSS. Cambridge University Press, New York.

- Wilson, N & Cacho, J, 2007. Linkage between foreign direct investment, trade and trade policy: An economic analysis with application to the food sector in OECD countries and case studies in Ghana, Mozambique, Tunisia and Uganda. OECD Trade Policy Working Papers No. 50. http://search.oecd.org/officialdocuments/displaydocumentpdf/?doclanguage=en&cote=com/td/agr/wp(2004)45/final Accessed 1 May 2012.

- Wong, KN & Tang, TC, 2007. Foreign direct investment and electronics exports: Exploratory empirical evidence from Malaysia's top five electronics exports. Economics Bulletin 6(14), 1–8.

- Zephyr, 2012. Zephyr: comprehensive M&A data with integrated detailed company information. https://zephyr2.bvdep.com/version-2012628/Home.serv?product=zephyrneo Accessed 29 July 2012.

- Zhang, KH, 2005. How does FDI affect a host country's export performance? The case of China. http://faculty.washington.edu/karyiu/confer/xian05/papers/zhang.pdf Accessed 23 May 2012.

- Zhang, KH, 2006. FDI and host countries’ exports: The case of China. International Economics 59(1), 113–27.

- Zhang, KH & Song, S, 2001. Promoting exports: The role of inward FDI in China. China Economic Review 11, 385–96. doi: 10.1016/S1043-951X(01)00033-5