ABSTRACT

Mozambique is one of the most promising African countries for producing biofuels and the national biofuel policy of 2009 identifies measures to incentivize biofuel production. Demand for biofuels in the Southern African Development Community is expected to increase over the next few years as 7 of its 15 member states have implemented or proposed the implementation of blending mandates by 2020. South Africa is one of these countries. Using a dynamic recursive computable general equilibrium (CGE) model, we estimate the impacts of expanding biofuel production in Mozambique under both commercial and smallholder-type farming models, including and excluding bagasse cogeneration.

1. Introduction

The role of biofuels in sustainable mobility has increased in importance over the last 10 years. This is evident by the growth in biofuels supply as well as the rising adoption of biofuel blending targets, mandates and subsidies in both developed and developing countries (Braude, Citation2015; IEA, Citation2015). The uptake of biofuel related policies was initially driven by country strategies to reduce greenhouse gas emissions in the transport sector while securing a renewable and sustainable source of energy. For developing countries, the potential benefits of biofuels extend beyond this as biofuel production and consumption is argued to aid in economic and rural development by stimulating the agriculture sector while at the same time reducing country exposure to foreign shocks through energy imports (Ferede et al., Citation2013).

Biofuel related policies have also gained traction in the Southern African Development Community (SADC) where dependence on imported liquid fuels is high and development, particularly rural development, remains a high priority. The biofuel mandates introduced in South Africa in 2014 is of particularly significant for the SADC region as biofuel demand from the country would provide a sufficiently large market to incentivise biofuel production and the development of a biofuel market in the southern African region (Stone et al., Citation2015).

Mozambique is uniquely placed to become a major supplier to such a market given its biophysical characteristics, significantly underutilised agriculture potential, well-developed sugar production sector and own blending mandates. The government of Mozambique has acknowledged this potential through the release of its National Biofuel Policy Strategy (Resolution No. 22/2009; OGM, Citation2009) in March 2009, which provides a framework and general set of guidelines for the development of a biofuels industry.

This paper, derived from Hartley et al. (Citation2016) and based on similar studies undertaken in Mozambique, Tanzania, Malawi and Zambia (Arndt et al., Citation2010; Arndt et al., Citation2012; Hartley et al., Citation2017; Schuenemann et al., Citation2017), assesses the economic, welfare and food security impacts of the development of such an industry in Mozambique using a dynamic computable general equilibrium (DCGE) model. Four scenarios are considered to assess the impacts of various elements in the biofuels debate. These include single versus multiple value chains; different farming models; and agricultural land displacement.

2. Potential for biofuel production in Mozambique

This study considers the use of sugarcane as a feedstock crop for bioethanol production. Sugarcane, due to its energy efficiency and associated low production costs, has been approved by the government of Mozambique as a feedstock crop for bioethanol production in the National Biofuel Policy Strategy. Support in Mozambique also seems to be strongest for sugarcane given the well-established sugar industry, high sugarcane crop output, and non-food crop status of the commodity – very little of the sugarcane produced and refined in Mozambique is used for domestic consumption. Sugarcane is the third largest agriculture crop produced in Mozambique and experiences the highest crop yield. Sugarcane yields increased significantly in the 2000s reaching an average of 50.4 tonnes per ha (t/ha) in 2000–2009 and 74.2 t/ha in 2010–2014 (FAOSTAT, Citation2016). The Centro de Estudos de Políticas e Programas Agroalimentares (CEPPAG) anticipates commercial and community yields to increase further in 2016/17 to 92.3 and 90.5 t/ha (CEPPAG, Citation2016). The motivation for considering sugarcane is also driven by global developments in the sector, i.e. the removal of limits for beet sugar production in the European Union (EU) from 2017 along with lower global sugar prices, which are likely to result in lower demand for Mozambican sugar highlighting the need for an alternative market for sugarcane output.

Sugarcane is primarily produced by sugar producing companies, namely Marromeu, Mafambisse, Maragra, and Xinavane. Xinavane is the largest sugar producer, accounting for around 50% of total production in Mozambique. Under the Xinavane structure, 70% of the required sugarcane for milling operations is produced by the company. The remaining 30% is sourced from private medium-sized and community farmers as the sugar companies’ farm lands are fully utilised. The sugar company plays an important role in non-company sugarcane farming, particularly in the case of community farmers, who account for 12.5% of total sugarcane output in the country. The company enters sugarcane purchasing agreements with community farmers and provides most of the needed inputs, including irrigation infrastructure (sugarcane in Mozambique is largely irrigated) and fertiliser inputs. Community farmers provide their labour and land. Payment for the sugar company inputs are deducted from receipts by community farmers for the sugarcane produced. Sugar companies also provide technical training to assist medium-scale and community farmers achieve high crop yields (Tostão et al., Citation2016).

Land availability is not expected to be a constraint to the expansion of sugarcane farming and bioethanol production. As part of their study to identify the constraints to biofuel production in Mozambique, Tostão et al. (Citation2016) identify approximately 3 million ha of land appropriate for sugarcane farming in the country. An additional 19 million ha was identified as being moderately appropriate. Furthermore, about 80 000 ha of the available land is already equipped with irrigation infrastructure. The use of this land, however, has not been determined and is dependent on local priorities.

The availability of infrastructure to transport bioethanol to neighbouring countries is necessary for the success of the sector. Schut et al. (Citation2010) explored biofuel projects formally submitted to government, expressions of interest, and the inventory of implemented projects and found that biofuel projects have generally been proposed in areas with good infrastructure where sufficient access to ports is available. Ports, and road infrastructure used to access these ports, are reported to be in good condition. Ports are also equipped with fuel storage facilities, which the government is planning to rehabilitate, expand and modernise (Tostão et al., Citation2016).

3. Methodology

A dynamic recursive CGE model for Mozambique, presented in section 3.1., is used to quantify the economy-wide impacts of introducing a bioethanol industry in the country. The model is based on a newly developed 2012 Social Accounting Matrix (SAM) for Mozambique developed by van Seventer (Citation2015) using data from the Instituto Nacional de Estatística and the International Monetary Fund (IMF). The SAM is extended to include biofuel crop farming and bioethanol production using the technology vectors described in section 3.2. Sugarcane farming for bioethanol use is separated from general sugarcane farming for ease of modelling.

We distinguish between commercial and community bioethanol crop farming and assume that both, along with bioethanol processing firms, use capital from foreign markets. This is a reasonable assumption as community farmers produce for sugar companies which are modelled to be foreign owned. Mozambique has also received significant interest from international investors for biofuel production since 2004 when the government announced its support for biodiesel production using jatropha (Schut et al., Citation2010). Almost all post-tax capital returns are therefore repatriated to foreign commercial lenders, adding little to domestic incomes. We assume that 0.1% of capital returns go to the wealthiest urban household group. New capital factor accounts are introduced into the SAM to capture this. In the baseline scenario, bioethanol crop and processing production is set to (almost) zero, providing a counterfactual for assessing the economic impacts of bioethanol production.

The introduction of the new industry creates a demand for bioethanol crops, which is supplied by the local market. To simulate the expansion in ethanol production, we exogenously increase the supply of land made available to feedstock farmers for the specific scenario. Farmers draw (foreign) capital, labour, and intermediate inputs into their production process. Feedstock outputs are used by the processing sector, along with capital, labour, and intermediate inputs, to produce bioethanol.

The development and upgrading of bioethanol processing infrastructure, if coupled with the development of cogeneration capacity, can add to electricity supply. Sugarcane waste, i.e. bagasse, is typically used to meet the energy needs of the sugar mill, but in most cases there exists excess supply that can be sold to the national grid. Mauritius has been successful in this producing around 475 GWh (Gigawatt hours) of electricity – about 16% of total electricity production and 20% of local electricity demand – from bagasse in 2013 (MEPU, Citation2015). Deepchand (Citation2005) estimates that, in Africa, 70–110 KWh of electricity can be produced from the waste of 1MT of sugarcane. To illustrate the benefit of a multiple product bioethanol industry, the SAM is further adapted to include the potential for cogeneration using bagasse. The technology vector for this sector is like that of the sugarcane bioethanol processing sector but also includes the cost of capital of generating electricity. Electricity is a by-product from bioethanol production, adding to the domestic supply in the country. Based on Deepchand (Citation2005) estimates, we assume that 70 kWh of electricity is produced per MT of sugarcane. Since cogeneration is essentially free, the value of the electricity produced is added to the operating surplus of the bioethanol industry. As a result, this activity becomes more profitable.

All bioethanol is assumed to be exported. It is likely, particularly in Mozambique given blending mandates, that some of the bioethanol produced may be used domestically. Previous biofuels projects proposed, however, were for meeting international demand (Schut et al., Citation2010). Either way, this does not have a significant impact on the results as the country is dependent on imports for its fuel needs. Domestic use of bioethanol would reduce exports of bioethanol but also reduce imports of petroleum.

3.1. A dynamic recursive CGE model for Mozambique

As indicated, the dynamic recursive CGE model for Mozambique is based on a 2012 SAM. The SAM consists of 55 industries and commodities, 4 labour groups, and 10 representative household groups which are defined by quintile for rural and urban areas using per capita expenditure data. Labour categories are defined by educational attainment and are categorised into incomplete primary, complete primary, complete secondary, and complete tertiary education. Other institutions (i.e. government, enterprises, and the rest of the world) are also represented. The SAM includes household production for own consumption, which comprises a large share of total rural household consumption.

The dynamic recursive CGE model is based on the generic static and dynamic models described in Lofgren et al. (Citation2002) and Diao & Thurlow (Citation2012). Behavioural equations in CGE models capture the decision-making process of industries and households that maximise profits and utility subject to costs and purchasing power respectively. Producers consume both domestic and imported intermediate goods and services as well as factors of production. Production factors include capital, labour, and, in the case of agriculture, land. Intermediate goods and services consumption is governed by Leontief functions, while the consumption of production factors is guided by constant elasticity of substitution. As a result, fixed shares of goods and services are required in the production process, but production factors can be substituted according to changes in their relative prices.

For this specific model, we assume that each activity only produces one commodity. Commodities are sold to other industries as intermediate inputs; households, government, and the rest of the world for final consumption; and as investment goods. The level of commodities supplied to domestic versus international markets is based on relative prices and is governed by a constant elasticity of transformation function. Similarly, the volume of goods and services imported is also based on relative prices and is represented by an Armington function. We assume that Mozambique is too small to directly affect global prices, which therefore remain fixed.

Households earn an income from providing labour, land, and capital to industries; and from government and foreign transfers. Returns to foreign labour, land, and capital are repatriated. Households consume both domestic and foreign commodities, pay taxes, transfer money abroad, and save. Consumption is based on a linear expenditure system of demand.

Structural equations ensure macroeconomic consistency between incomes and expenditures within the model. Closure rules are used to describe the functioning of the economy; these include the behaviour of exchange rates, investment, government savings, prices and quantities of production factors supplies. In this exercise, we assume that the exchange rate adjusts to absorb shocks to the economy while foreign savings remain fixed. The level of investment is determined by total savings in the economy (private, government, and foreign). Government savings adjusts to changes in income and expenditure – all tax rates remain unchanged. The domestic price index is used as the model numéraire. To fully assess the impact on resource shifts, we assume that all labour and land in the economy is initially fully employed. Capital, not used in the biofuel industry, is also fully employed but is activity-specific. Existing capital can therefore not shift to other sectors in the economy.

3.2. Bioethanol feedstock and production technology vectors

To inform the feedstock technology vectors, sugarcane production costs and farming yields were collected by CEPPAG. The data collected by CEPPAG was based on the Xinavane sugarcane farming operations (including own farm costs as well as outsourced sugarcane operations). This data is used to inform the feedstock crop technology vectors included in the modelling exercise. Sugarcane yields are used to calculate the amount of land needed for sugarcane farming. CEPPAG has advised that the costs of other operators are similar to the Xinavane operations and that these costs would therefore fairly reflect average new sugarcane production costs in the country. The budget data did not offer information on the returns to the capital production factor. We therefore use shares derived in a similar study for Zambia (see Hartley et al., Citation2017).

The sugarcane-to-ethanol conversion rate is reported to be 10 L per tonne via the molasses route and 80 L per tonne through direct conversion (Shumba et al., Citation2011). In this study, we assume that additional sugarcane grown is for bioethanol use only. Thus, we apply the direct conversion rate in line with other studies (Arndt et al., Citation2012; Sinkala et al., Citation2013; Hartley et al., Citation2016). illustrates the potential cost of sugarcane feedstock in Mozambique. Due to data confidentiality, information is presented in aggregate form. Feedstock costs are found to be less than US$0.20 per litre (/L).

Table 1. Bioethanol feedstock costs in Mozambique.

Very little bioethanol production occurs in Mozambique. Production that does take place is largely for own use with no large-scale commercial production taking place (Tostão et al., Citation2016). Thus, there is no Mozambique-specific data available for bioethanol processing. Following the approaches of Sinkala et al. (Citation2013) and Hartley et al. (Citation2017), estimates from international experience are used. Specifically, we use information from Sinkala et al. (Citation2013), which is based on a 2010 study by the Asia Pacific Economic Cooperation Secretariat (APEC, Citation2010) in which the processing costs for Brazil, Malaysia, and the USA are considered over a 10-year period. reports the bioethanol costs used. Including the costs of the sugarcane feedstock from , it would cost between US$0.32 and US$0.33 to produce 1 L of bioethanol in Mozambique.

Table 2. Bioethanol processing costs.

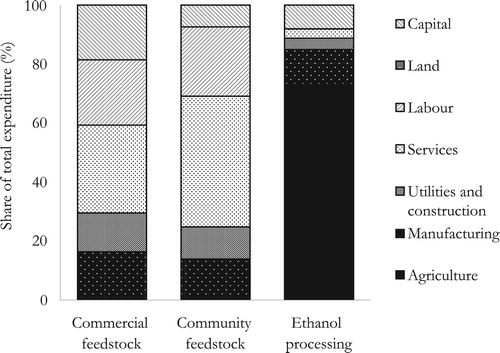

The production structures of commercial and community farmers are very similar, as illustrated in . This is because community farmers receive the bulk of their inputs from the sugar company that owns the commercial farms. The result is also influenced, however, by the government’s ban on mechanisation for harvesting. Labour is therefore a relatively large share of costs for both commercial and community farmers. Capital costs make up a smaller share of community farmer budgets who spend a larger share of their budget on labour and intermediate goods and services. They therefore have stronger links to the domestic economy. Commercial feedstock producers spend 20% of their budgets on capital returns, most of which are likely to be offshore payments. In terms of intermediate consumption, farmers spend a large share of their budgets on services, primarily on transportation and storage.

Figure 1. Feedstock and processing expenditure by component.

As expected, feedstock crops are the largest input into the ethanol production process. This is presented by the share of expenditure on agriculture. Relative to commercial and community feedstock budgets, labour makes up a very small share of ethanol processing costs. This indicates that employment gains are likely to come from feedstock farming rather than ethanol processing.

3.3. Baseline growth path

Apart from the service sector, agriculture is the largest contributor to gross domestic product (GDP) in Mozambique. In 2012, the agriculture, fishing, and forestry sector accounted for 28.5% of total GDP and employed more than 75% of the working population. More than 90% of workers in the sector are unskilled with primary education or less.

Mozambique is dependent on imports for food security. In 2012, imports accounted for 20.3% of total food crop demand and 40.4% of processed food demand. Almost 40% of cereal crops supplied to the market are imported. Food crops and processed foods account for a relatively small share of exports (8.7%) and total output (7.8%).

Mozambique is a net exporter of mining commodities. In 2012, 64.3% of total mining output was sold on the world market. Manufactured metals and metal products were the largest exported commodity, with about 70% of total output exported, accounting for 27% of total exports. The service sector is the largest contributor to GDP and main consumer of capital and high-skilled labour ().

Table 3. Structure of Mozambique economy, 2012.

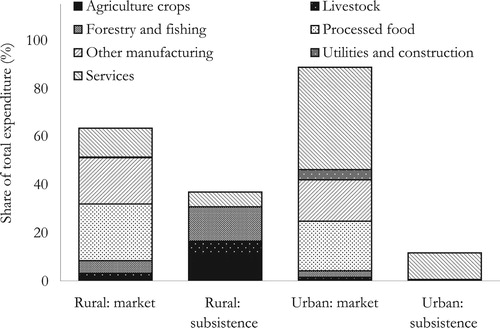

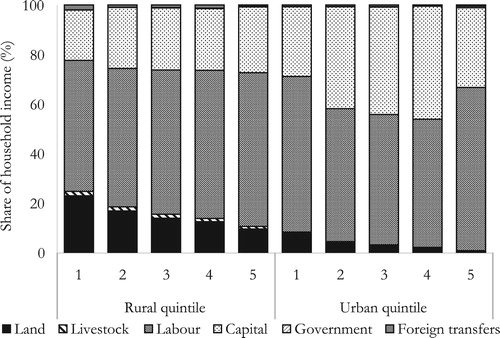

illustrates household consumption by main commodity group. In 2012, subsistence consumption accounted for more than 40% of total household consumption in Mozambique. For rural households, production for own use comprised 36.7% of total consumption and almost 80% of agriculture, fishing, and forestry consumption. This highlights the importance of subsistence farming for food security to poorer households in Mozambique. Subsistence consumption is not as important for urban households, accounting for less than 12% of total consumption and around only 9% of agriculture, fishing, and forestry consumption. Rural and urban households receive the bulk of their incomes from the supply of low-skilled labour. Urban households, however, also receive a large share of income from capital returns while rural households receive additional income from land returns (see and ).

Figure 2. Household consumption, 2012.

Figure 3. Household income by source.

The baseline scenario represents a potential growth path for the Mozambique economy for 2012–25. The 2012 SAM is used as the starting point for defining relationships and parameters used in the CGE model. This structure is extended to 2025 using endogenous model solutions and exogenous growth assumptions for labour, livestock, and land supply; government expenditure and foreign savings. Capital stocks are updated in each period by investment from the previous period, after accounting for depreciation. Increases in sector capital stocks are a function of profitability in the previous period as well as share of total capital stock. Total factor productivity is adjusted for broad industry groups (agriculture, industry, and services) such that the baseline reflects historical and projected growth trends. Real GDP growth over the period reflects the IMF projection of about 7.2% per annum (IMF, Citation2016). On average, sector total factor productivity is adjusted upward by 2.8% per annum. The first column of illustrates the core macroeconomic assumptions used in the development of the baseline scenario.

Table 4. Core macroeconomic assumptions and results, 2015–25.

While we have attempted to include a realistic baseline scenario, the choice thereof is not critical for the purposes of this study. The focus of this study is to assess the economy-wide impact of bioethanol production in Mozambique as a result we are therefore mainly interested in the differences between the base and various scenario outcomes.

4. Scenarios and assumptions

As highlighted in the introduction, the blending mandates announced in South Africa provide a key anchor market for biofuels in the SADC and Southern African region. Stone et al. (Citation2015), assuming an average annual real GDP growth rate of 2.7% between 2007–40, estimates that bioethanol demand in South Africa could potentially increase to between 300 and 1400 million litres per annum by 2025 under a 2 and 10% bioethanol blending mandate respectively. Based on this analysis we assume a bioethanol target of 1400 million litres per annum by 2025 for Mozambique. Production is assumed to increase incrementally over the period to reach this target.

We consider four scenarios in our analysis. Scenario 1 (Bioethanol, status quo) assesses the impact of developing a sugarcane bioethanol sector in Mozambique. We assume that the current structure of the sugarcane farming system is maintained (i.e. 87.5% of sugarcane is produced by commercial farmers and 12.5% by community farmers).

Scenario 2 (Bioethanol, 50–50) is the same as scenario 1 except that the sugarcane needed for bioethanol production comes equally from both commercial and community farmers. The implication of this is that marginally more land is needed for the same level of sugarcane production as community farmer yields are lower; and more labour resources are required as community farmers are more labour intensive. The purpose of this scenario is to assess whether there are significant welfare gains from using a larger share of community farmers relative to the status quo.

Scenario 3 (Bioethanol, status quo + cogeneration) is the same as scenario 1 but includes the impact of cogeneration as described under section 3.

While there is little evidence to suggest that growing sugarcane as a feedstock for ethanol production would result in the displacement of food crops – sugarcane is not considered a food crop and sugar companies have agreed with farmer associations to set aside 30% of irrigated community farm lands for food crop production – some farmers interested in bioethanol crop farming have indicated that they would move their livestock operations to rain-fed land. For this reason, as well as due to the importance of food security in Mozambique, we assess the impact of bioethanol production should 50% of the land needed by smallholder farmers for growing sugarcane farming displace other agricultural activities. All other assumptions in this scenario (i.e. scenario 4: Bioethanol, status quo + displacement) are the same as in scenario 1.

5. Results

This section reports the results from the modelling exercise. Unless otherwise specified, the results are presented as the percentage point (%pt) change in the average annual growth rate over 2015–25 relative to the baseline scenario. The ‘Total GDP’ result of 0.0032 for scenario 1 in is therefore interpreted as an increase in the average annual growth rate from 7.2% in the baseline to 7.2032% in scenario 1 (see ).

Table 5. Sector growth, 2015–25.

5.1. Macroeconomic impacts

The results show that the development of a bioethanol sector in Mozambique has the potential to increase average annual real GDP growth, particularly if the waste from the process is transformed into electricity (see and ). Average annual real GDP growth increases by 0.003%pts in scenario 1 versus 0.018%pts in scenario 3. This is equivalent to a 0.03% and 0.17% increase in the level of real GDP by 2025. Increasing the share of bioethanol feedstock grown by smallholder farmers results in a marginally smaller increase in average annual real GDP growth as does the switch to industrial crop farming (scenario 4).

To produce 1400 million litres of bioethanol by 2025, sugarcane output must increase by 17.5 million tonnes per annum, requiring about 19 000 ha of new land each year. We assume that land is acquired through the utilisation of idle arable land in Mozambique, expanding the total land supply used in the country. Land supply increases by about 1.3% per annum relative to 1% in the baseline (see ). In scenario 4, the expansion in land supply is smaller as we assume that 50% of the increase needed for smallholder farmers is acquired through the displacement of other agricultural activities.

As indicated in section 3.1, the supply of labour remains unchanged between scenarios, increasing by 4% per annum. The introduction of the bioethanol sector, however, increases the demand for labour. Thus, the average wage in the economy rises relative to the baseline. This increases the costs of production in the economy and negatively affects sectors with price sensitive demand. The decline in valued added in these sectors offset some of the gains from bioethanol production, thereby muting the positive impact on real GDP across all scenarios.

Sectors that experience a decrease in activity, however, release resources into the economy to be used elsewhere. This includes land which, across scenarios, is released primarily from maize production to more profitable agriculture sub-sectors such as pulses, cassava, sorghum, and groundnut. These crops account for about 50% of rural and lower income urban households’ food crop diets. The endogenous shift in land use therefore limits the negative impact of industrial crop production on food security. In scenario 4, however, bioethanol feedstock production reduces the amount of land available for normal agriculture use, leading to a decline in volume of agriculture food crops produced and available for consumption.

Food crop prices remain relatively unchanged in scenario 1 when bioethanol processing is introduced. Marginally lower food prices are experience in scenario 2 as the cost of land is lower due to larger increases in supply. Food prices increase in scenario 3 relative to the baseline as increased demand for labour stimulated by lower electricity prices places further upward pressure on wages. The largest food price increases are experienced in scenario 4 as food production decreases due to land constraints.

5.2. Changes in sector production

Average annual growth in agriculture and manufacturing gross value added (GVA) increases across scenario 1 due to increased sugarcane production and bioethanol processing. Sub-sectors in agriculture and manufacturing with few links to the bioethanol industry, however, experience slower growth due to increased production costs from higher wages. The mining sector experiences the largest decrease in average annual growth as it is also negatively affected by the appreciation in the real exchange rate. The exchange rate appreciates relative to the baseline scenario to maintain the current account balance due to increased bioethanol exports. The services sector, primarily transport and financial services, experience an increase in average annual growth due to strong links (directly and indirectly) with the bioethanol industry.

The impacts on electricity-intensive sectors are less negative in scenario 3 where cogeneration is included. Approximately 1225 GWh of electricity is produced from bagasse by 2025, adding 4% to electricity supply and reducing the price of electricity by 0.14%. While, the higher labour price induces a shift to using more capital across all scenarios, this is amplified in scenario 3 due to the lower electricity price. Overall the inclusion of cogeneration leads to stronger real GDP gains.

Displacing other agricultural activities for sugarcane farming leads to smaller positive gains in real GDP growth relative to scenario 1, as food crop production declines. This increases prices and has knock-on effects on the rest of the economy through the linkages between sectors.

5.3. Sector employment shifts

The bioethanol industry is estimated to create around 56 000 jobs directly through feedstock and processing activities by 2025. In scenario 2, an additional 3000 jobs are created due to community farmers being more labour intensive than commercial farmers. The bulk of employment generated by bioethanol production occurs in the production of feedstocks as the processing activity is not very labour intensive.

The shift of labour into the bioethanol industry is matched by a shift of labour out of other sectors due to our assumption of full employment. Sectors that experience the largest declines in average annual growth are also those that experience the largest decreases in employment. Larger outflows are experienced in scenario 2 as more labour is needed in the bioethanol industry. Other manufacturing, and utilities and construction, experience smaller outflows of workers in scenario 3 as lower electricity prices reduce the decline in activity in these sectors. Sectors experiencing positive GVA growth relative to the baseline also experience smaller outflows of workers.

The employment shifts presented in illustrate the significance of employment constraints on the economy-wide impacts of bioethanol and cogeneration production in Mozambique. Constrained labour will result in decreased activity in sectors less able to compete and smaller overall economic benefits. If this constraint is released, the GDP gains from bioethanol processing may be higher and lead to increased employment.

Table 6. Sector employment, 2015–25.

5.4. Household welfare and food security

The impact on household welfare by quintile for rural and urban households is presented in . In this paper, we use real per capita consumption as an indicator of welfare as it measures the real purchasing power of households. Overall, the introduction of a bioethanol industry in Mozambique has small but positive impacts on welfare, as expected, more so for households in rural areas.

Table 7. Real per capita consumption, 2015–25.

In scenario 1, average annual growth in rural household welfare increases by 0.0012%pts with all quintiles experiencing an improvement in welfare. This is equivalent to an improvement of 0.01% by 2025. The increase in rural household welfare is the result of increased incomes from land and labour. Land incomes increase due to increased supply, while labour incomes rise due to higher wages. Welfare gains are marginally smaller for urban households as enterprise income (i.e. returns on capital) decreases due to lower non-bioethanol production.

Welfare impacts are only marginally stronger under scenario 2, as higher wage incomes are offset by lower land incomes. Land incomes are marginally smaller in scenario 2 than scenario 1 as the larger increase in supply lowers the return to land.

Larger welfare gains are achieved under scenario 3. This is expected as overall activity in the economy is higher. Gains to urban household welfare, however, are larger than to rural household as the additional electricity favours capital intensive industries.

Welfare losses are experienced under scenario 4 as lower land availability for non-bioethanol use results in lower production and hence less demand for other factors of production. Welfare is also negatively affected in this scenario by higher prices in the economy.

In all scenarios excluding scenario 4, household food consumption increases although there is a shift to consuming more processed foods by both rural and urban households. Urban households, primarily low-income households, decrease their consumption of own-produced foods, choosing instead to consume more store-bought foods. While rural households increase their consumption of both own-produced and purchased foods, the share of purchased foods consumed increases. This does however not mean that at the micro level certain households will not be affected.

5.5. Releasing the constraint of unskilled labour

In addition to the scenarios considered above, we also assess the impact on the Mozambique economy if sufficient unskilled labour (i.e. labour with primary school education or less) was available to meet the increase in labour demanded. Labour supply in these scenarios (as well as the baseline scenario here) is modelled as an upward sloping supply curve, which means that while labour can be drawn in by a higher wage, the supply of this labour is not infinite. This is in line with current operations where during peak harvesting times sugar companies import labour from other regions. Skilled labour is still assumed to be fully employed ().

Table 8. Economic impacts under unconstrained low-skilled labour.

The release of the unskilled labour constraint in all scenarios, including the base, results in larger GDP gains as average wage increases in the economy are partly offset by the increase in labour supply. Welfare impacts remain positive and improve relative to the labour-constrained scenarios. Average annual employment growth also increases. As expected, the bulk of jobs are still created in the agriculture sector with the mining sector experiencing a decrease in activity and employment due to the stronger exchange rate.

6. Discussion

Developments in EU trade policy, Mozambique’s main sugar exporting market, along with the current global sugar surplus, has brought about the need for the government of Mozambique to think about reforming the sector to ensure continued growth and protect the workers in the sector. Biofuel production provides the country with an alternative market for its sugarcane. Expected demand from the SADC region, particularly from South Africa, provides a particularly good opportunity for Mozambique given existing relations between the countries, favourable tariffs under the SADC Protocol, and its proximity to this market. Transforming the sugar industry into a bioethanol industry will require very little change for large benefits (Schut et al., Citation2010). Furthermore, coupling bioethanol production with biomass cogeneration provides additional economic opportunities and can assist in energy security.

Studies by Schut et al. (Citation2010), Arndt et al. (Citation2012), and Tostão et al. (Citation2016) highlight that the country possesses the biophysical properties needed to become a key ethanol producer on the African continent. Furthermore, investor interest in previous attempts to develop a biodiesel sector (see Schut et al., Citation2010) indicates that the necessary investment for the development of the sector is highly likely to be available. Estimated sugarcane farming budgets from field studies by CEPPAG, coupled with international processing budgets, also show that Mozambique has the potential to produce bioethanol at internationally competitive prices of around US$0.30/L.

The outcomes presented in this paper assume that the expansion of biofuel production in Mozambique is undertaken in an efficient manner. For the benefits presented here to therefore transpire mistakes from previous experiences must be avoided. These include efficient access to land for production – Tostão et al. (Citation2016) indicates that under previous biofuel projects investors had difficulty in getting land licenses; and the purchase of bioethanol feedstock crops should be guaranteed – in previous biodiesel production cases many farmers were left stranded with jatropha which was supposed to be used in biodiesel production. Kegode (Citation2015) and Tostão et al. (Citation2016) provides a more in-depth analysis of the legal and social considerations of biofuels expansion in Mozambique.

Infrastructure and water supply constraints are not directly included in the modelling undertaken in this paper. Although, transport and logistic constraints are potentially avoidable through appropriate ethanol processing plant placement and Tostão et al. (Citation2016) indicates that sufficient water is available for additional sugarcane farming, particularly in the regional areas where such farming is suitable and attractive to investors, both these areas require further analysis. Furthermore, the vulnerability of the sector due to climatic changes, while not considered in this paper, is also important and should be considered in future research. While changes in climate may potentially have a small impact on sugarcane which is largely irrigated, drier and hotter climatic conditions are likely to lead to more frequent watering, which would raise the costs of irrigation. This would lead to higher sugarcane prices and increase the cost of bioethanol, potentially making it less competitive relative to alternative fuels and suppliers.

7. Conclusion

This paper assesses the economic implications of expanding sugarcane bioethanol production in Mozambique to a large enough scale to meet demand from South Africa. A dynamic recursive model is used. The results from the model indicates that the development of a bioethanol value chain in Mozambique has a positive impact on economic growth and employment. The magnitude of this impact increases when multiple value chains can be linked to the industry. This is illustrated by the generation of electricity from bagasse. The availability of sufficient labour resources also leads to larger economic and employment gains highlighting the importance of enabling efficient labour markets that allow labour mobility. The switch in farming systems to include community farmers has a minimal impact on GDP, employment and welfare gains and can be explained by the similar cost structures of commercial and community farmers as well as the dependence on foreign investment. The rise in aggregate rural and urban household food consumption suggests that food security, even under the case of 50% crop land displacement, is less of a concern at the national level in Mozambique. This does not mean that at the micro level certain households will not be affected. A deeper analysis at the microeconomic level is, however, needed to better understand the individual household effects.

Disclosure statement

No potential conflict of interest was reported by the authors.

ORCID

Faaiqa Hartley http://orcid.org/0000-0001-9799-3923

Channing Arndt http://orcid.org/0000-0003-2472-6300

References

- APEC (Asia-Pacific Economic Cooperation), 2010. Biofuel costs, technologies and economics in APEC economies. Report APEC#210-RE-01.21, APEC Energy Working Group.

- Arndt, C, Benfica, R, Tarp, F, Thurlow, J & Uaiene, R, 2010. Biofuels, poverty, and growth: A computable general equilibrium analysis of Mozambique. Environment and Development Economics 15(1), 81–105. doi:10.1017/S1355770X09990027.

- Arndt, C, Pauw, K & Thurlow, J, 2012. Biofuels and economic development: A computable general equilibrium analysis for Tanzania. Energy Economics 34, 1922–30. doi: 10.1016/j.eneco.2012.07.020

- Braude, W, 2015. Towards a SADC fuel ethanol market from sugarcane, regulatory constraints and a model for regional sectoral integration. 2015 TIPS Forum, 14–15 July, Johannesburg, South Africa.

- CEPPAGG (Centro de Estudos de Políticas e Programas Agroalimentares), 2016. Technology package for sugar cane production and processing in Mozambique. Contribution to Regional Growth and Development Project. Email correspondence, 23 June 2016.

- Deepchand, K, 2005. Sugar can bagasse energy cogeneration – lessons from mauritius. Parliamentarian Forum on Energy Legislation and Sustainable Development, 5–7 October, Cape Town, South Africa.

- Diao, X & Thurlow, J, 2012. A recursive dynamic computable general equilibrium model. In Diao, X, Thurlow, J, Benin, S & Fan, S (Eds)., Strategies and priorities for African agriculture: Economywide perspectives from country studies. International Food Policy Research Institute, Washington, DC, USA, 17–50.

- FAOSTAT (Food and Agriculture Organisation Statistics), 2016. Food and agriculture data. www.fao.org/faostat/en/#home Accessed 23 January 2017.

- Ferede, T, Gebreegziabher, Z, Mekonnen, A, Guta, F, Levin, J & Köhlin, G, 2013. Biofuels, economic growth, and the external sector in Ethiopia. A computable general equilibrium analysis. Discussion Paper Series 12-08. Environment for Development, Environmental Economics Unit, University of Gothenburg, Sweden; Resources for the Future, Washington, DC.

- Hartley, F, van Seventer, D, Tostao, E & Arndt, C, 2016. Economic impacts of developing a biofuel industry in Mozambique. WIDER Working Paper 2016/177. United Nations University, Helsinki.

- Hartley, F, van Seventer, D, Samboko, PC & Arndt, C, 2017. Economy-wide implications of biofuel production in Zambia. WIDER Working Paper 2017/27. United Nations University, Helsinki.

- IEA (International Energy Agency), 2015. Medium-term renewable energy market report 2015. International Energy Agency, Paris.

- IMF (International Monetary Fund), 2016. World economic outlook database: April 2016. https://www.imf.org/external/pubs/ft/weo/2016/01/weodata/index.aspx Accessed 13 January 2017.

- Kegode, P, 2015. Sugar in Mozambique: Balancing competitiveness with protection. Mozambique Support Program for Economic and Enterprise Development (SPEED). USAID, Mozambique.

- Lofgren, H, Harris, RL & Robinson, S, 2002. A standard computable general equilibrium (CGE) model in GAMS. International Food Policy Research Institute, Washington, DC, USA.

- MEPU (Ministry of Energy and Public Utilities), 2015. Energy observatory report 2013. Energy Efficiency Management Office, Ministry of Energy and Public Utilities, Ebene, Mauritius.

- OGM (Official Gazette of Mozambique - Boletim da Republica), 2009. Biofuels policy and strategy (Politica e estrategia de biocombustiveis). Resolution 22/2009. Serie I, n. 20, 21 May.

- Schuenemann, F, Thurlow, J & Zeller, M, 2017. Leveling the field for biofuels: Comparing the economic and environmental impacts of biofuel and other export crops in Malawi. Agricultural Economics 48, 301–15. doi:10.1111/agec.12335.

- Schut, M, Slingerland, M & Locke, A, 2010. Biofuel developments in Mozambique: Update and analysis of policy, potential and reality. Energy Policy 38(9), 5151–65. doi: 10.1016/j.enpol.2010.04.048

- Shumba, E, Roberntz, P & Kuona, M, 2011. Assessment of sugarcane outgrower schemes for bio-fuel production in Zambia and Zimbabwe. World Wide Fund For Nature, Harare, Zimbabwe.

- Sinkala, T, Timilsina, GR & Ekanayake, IJ, 2013. Are biofuels economically competitive with their petroleum counterparts? Production cost analysis for Zambia. WPS6499, Environment and Energy Team, Development Research Group, World Bank.

- Stone, A, Henley, G & Maseela, T, 2015. Modelling growth scenarios for biofuels in South Africa’s transport sector. WIDER Working Paper 2015/148. United Nations University, Helsinki.

- Tostão, E, Henley, G, Tembe, J & Baloi, A, 2016. A review of social issues for biofuels investment in Mozambique. WIDER Working Paper 2016/178. UNU-WIDER, Helsinki.

- van Seventer, D, 2015. A 2012 social accounting matrix (SAM) for Mozambique’. Inclusive growth in Mozambique—scaling-up research and capacity project. UNU WIDER database. https://www.wider.unu.edu/database/2012-social-accounting-matrix-mozambique Accessed 23 January 2017.