ABSTRACT

To date, regional automotive value chains have not developed to any significant extent in Africa. Growing demand for vehicles across the continent, closer economic integration and the desire on the part of some larger African countries to establish an automotive industry have improved prospects. But major obstacles remain: the political geography of the subcontinent and the tendency of the industry to cluster in a few locations indicate that many smaller countries are likely to miss out on attracting investments. This should not matter if they are attracting investment in other sectors. It does however imply that it is unlikely that the automotive industry will drive regional integration independently of a broader integration process which sees the development of regional value chains across a multitude of sectors helping to bind the continent into a larger common market.

1. Introduction

Africa is characterised by low levels of industrialisation and intra-regional trade (African Development Bank, Citation2019). However, in contrast to global developments, progress is being made towards closer economic integration on the continent. The recently ratified African Continental Free Trade Area (AfCFTA) is an important step in this regard and could be a major catalyst for regional trade and industrialisation. Growing trade links create the potential to facilitate further economic integration and the development of regional value chains. In several regional arrangements such as NAFTA, ASEAN, Mercosur and indeed in the development of the European integration project, the automotive sector played an important role in driving regional integration.Footnote1 But ongoing progress with integration will require that all participants see tangible benefits. This in turn means that policy makers will need to pay attention to spreading the gains to all participant countries. This is key to the developmental regionalism approachFootnote2 which has some traction in the AfCFTA negotiations (Ismail, Citation2020).

Unbalanced trade between South Africa and the region is already an issue. According to the 2018 African Trade Report, South Africa contributed over a quarter of intra-African trade and has a significant trade surplus with the rest of the continent (Afreximbank, Citation2018). In 2018, South Africa’s total exports to southern Africa were US$19.2 billion, while imports amounted to only US$6.1 billion. South Africa’s trade surplus with the region has fluctuated between US$11.7 and US$15.2 billion since 2010 (UN Comtrade) and this ongoing dominance of trade presents a challenge to successful regional integration. Indeed it has already led to creeping protectionism. For example, member states of the Southern African Development Community (SADC) have imposed trade restrictions and local content requirements on imports of certain food products from South Africa (das Nair et al., Citation2018).

The objective of this paper is to examine the dynamic interplay between regional integration and the development of regional value chains (RVCs) through the lens of the automotive industry. Closer regional integration can provide the foundation for RVCs and RVCs in turn promote regional integration in a variety of ways including the establishment of backward, forward and horizontal linkages between firms across borders (Black et al., Citation2021). These linkages can also provide political pressure for further integration. But from a national policy perspective, for political momentum to be maintained, it is important that all participants perceive themselves to be gaining from the process.

Section 2 considers the links between regional integration and the automotive industry by briefly assessing international experience. The current state of the automotive industry in sub-Saharan Africa, both from a market and production perspective, is outlined in section 3. In section 4, the prospects for regional automotive value chains in Sub-Saharan Africa (SSA) are assessed. Section 5 concludes.

2. Regional integration and the automotive industry

The automotive industry plays a major role in global value chains (GVCs) and developing countries have become increasingly central as locations for vehicle assembly and component production (Sturgeon & van Biesebroeck, Citation2011; de Backer & Miroudot, Citation2014). But regional production remains important. This is because of the political importance of the sector and the perceived need to locate close to home markets as well and the power of lead firms who can require that component suppliers locate close to assembly plants (Sturgeon & Van Biesebroeck, Citation2011). The industry is also extremely scale intensive. For example, vehicle production volumes of around 80,000 units per annum are required to justify investment in a single greenfield assembly plant.Footnote3 International evidence suggests that the establishment of a plant operating at efficient scale typically requires investments of over US$200 million (Barnes et al., Citation2016a: 30). For the sector to grow in SSA, any new vehicle production plants will therefore need to supply products to regional and/or broader international markets. Individual domestic SSA markets are simply too small to support modern vehicle production. And herein lies a central conundrum. How does an SSA country attract automotive investments when its domestic market is too small to support required output levels, and its neighbours have no interest in supporting investments outside of their boundaries? The development of competitive regional value chains is clearly critical in this regard. While many countries may not have the market size, infrastructure, or skills to attract a large-scale vehicle production plant, they may be able to manufacture specific components for vehicle production plants in proximate markets, thereby providing them access to the regional portion of automotive GVCs.

This is a critical consideration, as the development of the automotive industry in Africa faces a range of complications. Most notably, the continent is comprised of a multitude of mainly small economies, whose combined GDP is less than that of France (African Development Bank, Citation2019). In SSA, even the two largest economies (South Africa and Nigeria) lack the market size to constitute a viable market, as defined by Sturgeon and Florida (Citation1999). If these two markets are excluded, the average market size of the eight next largest SSA markets in 2017 was less than 50,000 vehicles per annum. Moreover, this includes new and imported used vehicles.

For vehicle production to be viable, it needs an ‘automotive space’, which could be a large single domestic market such as China and India, or a large adjoining market such as the US in relation to Mexico, or more recently the EU in relation to Turkey or Morocco. Alternatively, a regional trade agreement can effectively enlarge a set of smaller proximate markets and create a viable automotive space that lends itself to the scale requirements of modern vehicle production (Sturgeon & Florida, Citation1999; Humphrey & Oeter, Citation2000). Global examples of these viable regional spaces include the Association of Southeast Asian Nations (ASEAN) and the Mercado Común del Sur (Mercosur) in Latin America (Laplane & Sarti, Citation2004; Techakanont, Citation2014).

SSA represents a potential example of another major regional market opportunity. It comprises 48 countries and seven trade blocs which form a complex ‘spaghetti bowl’ of overlapping trade arrangements. The level of intra-regional trade is low although there are important regional differences, with evidence of growing trade within SADC, for instance (Black et al., Citation2021). In 2011 the decision was taken to start negotiations towards a Tripartite Free Trade Area. Discussions were then expanded to include the rest of Africa in a continent-wide agreement. This has culminated in the launch of the AfCFTA in March 2018, bringing together 55 countries with a population of more than one billion people and a combined GDP of over US$2 trillion (Ismail, Citation2016: 6). While this is an important step forward, it is important to note that considerable work needs to be done and the continent remains some way off from the common market objective.

In both of the regional trade agreement cases relevant to SSA (ASEAN and Mercosur) the automotive industry and multinational firms have been strong supporters of trade integration but the development of agglomeration advantages in preferred regions and countries has created political challenges for further integration. An example in Mercosur is the dominance of the Brazilian automotive industry in relation to that of Argentina (Laplane & Sarti, Citation2004).

ASEAN has been more successful and the region has become a major production and export hub (Markowitz & Black, Citation2019). But even so, ASEAN has been dominated by the Thai automotive industry, which has become the primary regional platform for Japanese investment (Techakanont, Citation2014; Kobayashi et al., Citation2015). Japanese vehicle producers pushed for the establishment of the ASEAN Industrial Cooperation (AICO) scheme, which was introduced in 1996. It enabled two different firms or corporate divisions operating in two different ASEAN countries to form an ‘AICO arrangement’ and receive preferential ASEAN Free Trade Area (AFTA) tariff rates of 0–5 per cent for raw material, intermediate and finished goods (Markowitz & Black, Citation2019). It helped that all four participating countries had attained a certain level of industrial development on the basis of prior protection so that regional cooperation generated benefits for all countries. Difficulties did, however, result from Indonesia and Malaysia trying to develop their own indigenous car brands (Farrell & Findlay, Citation2001; Natsuda et al., Citation2013). The Malaysian government was particularly worried about AICO’s effect on the country’s domestically owned car producers (Fujita, Citation1998). This concern was confirmed by the subsequent decline of indigenous vehicle production in both Malaysia and Indonesia, although increases in multinational vehicle production have more than compensated for these losses.

A key question which is germane to the SSA situation is whether ASEAN arrangements will lead to integrated production across the region, which includes the lesser developed newer members such as Cambodia, Laos, Myanmar and Vietnam. While Cambodia, Laos and Myanmar do supply the Thai industry with labour-intensive parts such as wiring harnesses and seat covers on a small but expanding scale, there is little sign to date of them becoming fully integrated into regional automotive value chains (Kobayashi et al., Citation2015).

In Mercosur, the results have been less impressive, with progress being frustrated by the national interests of Argentina and Brazil as well as economic difficulties across the region (Laplane & Sarti, Citation2004; Sturgeon et al., Citation2017). While there has been trade creation, Arza (Citation2011) and Sturgeon et al. (Citation2017) argue that Mercosur agreements have not enabled the region to become a competitive platform for exports to external markets.

3. The current state of the automotive industry in SSA

Driven by an expanding middle class, the market for motor vehicles in Africa is growing rapidly albeit from a low base. However, much of this demand is being met by imports because outside of South Africa and certain countries in North Africa, production is still very limited (Black et al., Citation2019). In most countries, the market is dominated by imports of mainly used vehicles. The same applies to components, most of which are imported. Furthermore, the fact that only 5.4% of the continent’s component imports are from within Africa (Stuart, Citation2020: 30) is evidence of weakly developed regional value chains. Will the continent continue to rely on imports? Or can it develop its own industry which draws in a number of countries to create competitive regional automotive value chains? And can this huge multinational-dominated global industry play a role in driving regional integration (Black et al., Citation2019)?

The market has huge potential. Imports into SSA, excluding South Africa, of light vehicles (new and used) grew at a compound rate of 14% per annum from 2003 to 2013 (Black et al., Citation2017). Demand has since slumped following the commodity price collapse and serious economic problems in potentially large markets such as Nigeria (). In that country, poorly managed oil revenues led to boom and bust cycles which are magnified in the auto sector. Currency collapses and foreign exchange constraints have accordingly severely impacted on vehicle sales since 2013.

Table 1. Estimated SSA vehicle sales (new vehicles and used imports), 2007–17.

The small number of new car sales as a share of most markets is evident in . With the exception of South Africa, vehicle consumption is dominated by used vehicle imports. The lack of vehicle finance and vehicle and personal insurance in most SSA markets makes new vehicle acquisition inaccessible (cash up front is required) and risky (the threat of potential theft and accidents cannot be easily mitigated), thereby increasing the relative attractiveness of cheap second-hand vehicle imports. The prevalence of used vehicle imports is also increased by the discounting of used vehicle exports into SSA. This discounting is tied to End of Life Vehicle legislation in the EU and punitive vehicle taxes on ageing vehicles in Japan. Second-hand vehicle import prices into SSA are therefore discounted, making them very attractive relative to new vehicles.

While SSA consists of a large number of mostly small economies, the combined GDP and vehicle market is significant. India, which Sturgeon and Florida (Citation1999) defined as a viable future automotive space, had a roughly comparable GDP, per capita income and vehicle market size in 2013. India had a large trade surplus (US$8.3 billion) in the automotive sector in that year, while SSA had an automotive trade deficit of US$16.3 billion (Black et al., Citation2017). The Indian automotive industry has continued to prosper, running large trade surpluses through to 2017, while the SSA trade deficit narrowed to US$6.8 billion in 2017 as foreign exchange pressures and the reversal of the commodity boom reduced vehicle consumption (Barnes et al., Citation2019). The key difference is that India has an integrated single market and this market is protected by a high, common external tariff, while SSA remains divided into many small markets which are far from being fully integrated and remain open to imports.

Africa consequently accounted for only 1.2% of global production in 2018. South Africa and Morocco accounted for the bulk of this output, followed by Egypt and Algeria. These figures exclude nascent, very low value assembly operations in several SSA countries such as Kenya, Nigeria, Ghana, and Ethiopia.

South Africa dominates output in SSA, but in 2018 this only amounted to 611,000 vehicles (AIEC, Citation2019). The industry has a long history in the country but its growth over the past decade has been constrained by anaemic domestic economic growth. Following a history of heavy protection, the first steps to liberalise the sector began in 1989. Major structural change then took place in 1995 with the introduction of the Motor Industry Development Programme (MIDP). Since the introduction of the MIDP, South Africa’s automotive industry has become increasingly exposed to international competition as government has sought to make it more competitive and also to encourage exports and a more rational industry structure (Black et al., Citation2017). Lower tariffs in the automotive sector were accompanied by the introduction of import-export complementation arrangements, which enabled local vehicle assemblers to rebate import duties by exporting. The MIDP was replaced in 2013 by the Automotive Production and Development Programme (APDP), which provides a vehicle assembly incentive and production incentive together with stable tariffs of 25% on imported vehicles. As a result of these measures, the industry has been through a period of rapid international integration and structural change (Black et al., Citation2017). Imports accounted for 56% of the domestic light vehicle market in 2018, while 60% of output was exported, with 70% of this volume destined for Europe, and the rest of Africa also being a major market. The South African Automotive Masterplan (SAAM) has recently been developed with ambitious objectives of raising local content to 60% (from 38%) and expanding output to 1.4 million units by 2035 (Barnes et al., Citation2016b). One of the cornerstones of the SAAM is increased vehicle and component production sales into the regional market.

The key question then concerns the rest of SSA. What are the prospects for the sector in respect of greater regional integration and can the sector help drive further integration through the development of a viable automotive production space?

After independence in the late 1950s and early 1960s, small-scale assembly was established in several SSA countries such as Nigeria, Ghana and Kenya. The scale of these plants was however tiny, and they assembled imported completely knocked down (CKD)Footnote4 kits with minimal use of domestic content (Black et al., Citation2017).

There was also some small-scale production of peripheral and aftermarket parts. Much of this small-scale industry was swept away by a combination of economic decline from the early 1980s and ‘structural adjustment’ policies imposed by the IMF and World Bank. Sweeping tariff reductions led to de-industrialisation, which included the demise of small-scale vehicle assembly and component production. Liberalisation allowed cheap used vehicles to flood into the region from advanced countries. The systematic way this happened in Nigeria is explored by Ugwueze et al. (Citation2020). The component sector was also heavily affected although industrialists have shown some resilience in dealing with these adverse conditions, partly by targeting the aftermarket (Brautigam, Citation1997).

Conditions for automotive development in SSA are now more favourable. The expanding African market, growing regional integration between the countries of the region, and the desire on the part of some larger countries in SSA to re-establish domestic production through the imposition of necessary policy interventions are all important factors.

In SSA outside of South Africa, a number of countries including Nigeria, Ethiopia, Kenya and Angola have started small-scale assembly operations (Markowitz & Black, Citation2019). Many major multinational assemblers are investigating possibilities. Most of these operations are however very small-scale and involve minor semi-knocked down (SKD) assembly. SKD assembly involves final assembly of partly assembled vehicles with minimal or no local content and adds minimal economic value. There is also some components production, especially for the aftermarket, and significant clusters of parts producers exist, for instance in Nnewi in Nigeria and Suame in Ghana (Abiola, Citation2008; Adeya, Citation2008).

Nevertheless, with the exception of South Africa, SSA countries remain extremely reliant on imports and export very little. This is illustrated in for Nigeria, Kenya and Ghana. All three countries show rapidly rising imports, especially of vehicles, although these have since slumped, particularly in Nigeria along with falling oil revenues. The three countries all exhibit large automotive trade deficits.

Table 2. Automotive imports and exports, Nigeria, Kenya and Ghana, 2007–17 (US$ million).

Automotive policies are also being developed. For example, in 2013 Nigeria introduced the National Automotive Industry Development Plan (NAIDP). Tariffs were set at 70% for built up cars, consisting of a 35% duty as well as a 35% levy (Ugwueze et al., Citation2020). Local assembly operations can import cars without the levy and require minimal initial investments as vehicles can be assembled on an SKD basis for five years before moving to CKD production. This has led to the rapid proliferation of SKD ‘assembly plants’ which now number 35 (Ugwueze et al., Citation2020) and have been described by one commentator as ‘glorified joineries’.Footnote5

Ghana similarly announced plans to establish an automotive industry in 2018; and has moved rapidly to establish a new automotive policy. Again, following an initial SKD path, several vehicle assemblers have announced plans to establish plants in the country, including Toyota and Suzuki in a joint venture (Auto Trend Ghana, Citation2019).

With its large population and rapid economic growth rate, Ethiopia has a large potential market. It also has ambitions in the automotive industry and high tariffs and taxes hugely inflate purchase costs. With this high level of protection, there are a large number of small-scale, mainly SKD, assemblers operating in the country. Chinese vehicle assemblers are also increasingly in evidence.

Kenya has three very small assembly plants mainly assembling medium and heavy commercial vehicles on an SKD basis and with virtually no local components. There is also a small component industry making aftermarket parts, and some minor domestic assembly of motorcycles (Black et al., Citation2017).

Small-scale production in Zimbabwe dates to the country’s import substitution economic development phase of the 1960s. In the 1990s, Willowvale Mazda Motor Industries in Zimbabwe had a capacity of 10,000 vehicles per year (Black & Muradzikwa, Citation2004) but it shut down in 2012 following years of turbulence in the national economy. Small-scale assembly has restarted with the company establishing a joint venture with the Chinese automaker, BAIC (Black et al., Citation2019). In Botswana, an assembly plant was established under licence from Hyundai in 1993. To conform with South African regulations, it was required to invest in full CKD production. It benefited from its proximity to South Africa and initially enjoyed relative success but closed down in 2000 (Zizhou, Citation2009).

Angola has a potentially large market and has expressed the intention to develop the automotive industry as a part of efforts to diversify from oil production, and minor SKD assembly has been established (Markowitz & Black, Citation2019). In Zambia, it was announced in 2016 that China’s Gonow would build a US$175 million assembly plant outside Lusaka but this investment has failed to materialise. This is in line with the familiar pattern that ambitious plans are announced to great political fanfare, but actual investments turn out to be, at best, small-scale SKD plants (Markowitz & Black, Citation2019). The tiny scale of the above-mentioned plants has resulted in there being minimal original equipment component manufacture with the small local component industries catering mainly for the aftermarket. Furthermore, the national strategies being developed by various countries may run counter to continental integration objectives.

South Africa is currently the only country with a production base of any significance. But other countries have an interest in vehicle production, although their current facilities are essentially SKD plants, which add minimal value and use virtually no domestically produced parts (Markowitz & Black, Citation2019). The result of this lopsided development is that automotive trade within SSA is essentially in one direction, consisting of exports from South Africa to other African countries (Markowitz & Black, Citation2019). The bulk of South Africa’s exports to Africa are to Southern African Customs Union (SACU) and SADC countries (). Total automotive exports to SADC amounted to US$1.91 billion in 2017, 16 per cent of South Africa’s total automotive exports. Apart from vehicles, component exports to Africa are also significant, amounting to $982 million in 2017. These are mainly aftermarket parts such as tyres, filters and batteries.

Table 3. South African automotive exports to Africa (US$ million).

While South Africa is a major exporter to the region, it imports very little from neighbouring countries. Angola, Botswana (wiring harnesses), Lesotho (leather seats) and Zambia collectively supply less than US$100 million of component exports annually to South Africa, illustrating the virtual absence of regional value chains (Markowitz & Black, Citation2019). There has been some limited relocation of labour-intensive suppliers to Botswana and Lesotho, where labour costs are lower and the labour relations environment seemingly more stable. These relocation decisions were met with strong opposition by South African trade unions. The relocation in 2015 of Pasdec, a wiring harness manufacturer, from South Africa to Botswana is a further example of these perceived advantages, although it has encountered significant strike action. While such developments represent a small step in developing value chains within the region, as South Africa continues to support the deepening of its own components production base, this process is likely to be limited in both scope and scale (Markowitz & Black, Citation2019).

4. The prospects for regional automotive value chains in SSA

Regional value chains are starting to develop in parts of Africa, for example in the garment and associated textile sector (Morris et al., Citation2016). But as we have discussed, outside of the supply of completed final products from South Africa into SSA, and very limited intermediate component supply from Botswana and Lesotho into South Africa, they hardly exist in the automotive industry. This contrasts with ASEAN, where regional automotive value chains have become increasingly developed in support of a dynamic and growing automotive industry (Kobayashi et al., Citation2015).

While not specific to the automotive industry, a prime constraint to the development of SSA automotive value chains is weak manufacturing capabilities and serious infrastructure constraints. Shortages of skills and the poor supply of automotive value chain prerequisites such as power and advanced transport links need to be addressed (Markowitz & Black, Citation2019). For instance, in Nigeria, electricity supply is intermittent and complex Just in Time (JIT) supply chains are compromised by ‘handling fees’ that accompany necessary trade linkages (Ugwueze et al., Citation2020).

Another major obstacle facing the industry’s integration within the region is that of the costs of trade diversion, which are particularly high given the large presence of low-priced, imported second-hand cars in most national markets (Markowitz & Black, Citation2019). Though restrictions on the import of used vehicles would arguably be necessary to stimulate requisite demand for locally assembled vehicles, this would, of course, impact very negatively on consumers. Why, for instance, would Ugandans want to buy (potentially expensive) cars made in Kenya, rather than cheap, imported second-hand cars from Japan (Markowitz & Black, Citation2019)? While some progress has been made to resolve this in the East African Community (EAC) context, it is still a pressing issue. Kenya, which has over 25,000 units of surplus vehicle capacity, managed to negotiate a common external tariff (CET) of 25% in the EAC for vehicles, a relatively large increase from Tanzania and Uganda’s 0% (Black et al., Citation2017). However, the CET came to nothing as the member nations were granted a stay on the CET, with the result that Kenyan assemblers still face 25% duties for Rwanda and Burundi and unconstrained external competition in Tanzania and Uganda. CKD assemblers also face bureaucratic hurdles with kits needing to be imported under the individual tariff lines of the components in the kits, as well as a vague duty remission scheme (Black et al., Citation2017).

The Economic Community of West African States (ECOWAS) also established a CET in 2015, setting passenger vehicle tariffs of up to 20% depending on the size of engine. However, member states were able to add an Import Adjustment Tax (IAT). Nigeria used this to raise tariffs by up to 50% and the country also charged an additional levy on imported vehicles (Black et al., Citation2017). Nigerian auto assemblers therefore face uneven levels of protection across ECOWAS and smuggling has increased through other ECOWAS nations as a result of a lack of a common policy framework (Adeniyi, Citation2015; Black et al., Citation2017).

We have argued above that regional integration is critical to the development of the automotive industry. The automotive industry could also help drive regional integration as vehicle producers place pressure on governments to increase market access and improve cross-border infrastructure (Lung & van Tulder, Citation2004; Black et al., Citation2017). But it is also possible that it has the opposite effect in the short term as countries raise special tariffs to protect their industries and nurture the development of insular, small-scale SKD-type operations that assemble for domestic consumption only (Black et al., Citation2017). For example, higher tariffs in Nigeria and Algeria have resulted in a substantial decline in Toyota South Africa’s exports to the rest of the continent (AIEC, Citation2015).

There is an argument that the smaller economies could be drawn into the regional value chain as suppliers of major components for cars, which are assembled in South Africa. To some extent this is what has happened in Mercosur and ASEAN, where the automotive industry played a leading role in driving regional integration (Black et al., Citation2019). In ASEAN, in particular, a degree of specialisation and complementation has developed, with this involving Thailand, Malaysia, Indonesia and the Philippines (Markowitz & Black, Citation2019). But there is an important distinction with SADC. The aforementioned ASEAN countries are all medium to large sized markets and all have a history of automotive production. The small southern African automotive cluster is already spread across three major locations (Gauteng, Durban and the Eastern Cape), all of which are in South Africa. It is unlikely that many more such clusters will emerge in the southern African region, at least in the short to medium term. Even Lesotho with its central location with respect to the major car-producing regions in South Africa (Gauteng, Durban and the Eastern Cape) struggles to attract parts makers to invest in the country. While Lesotho is part of a customs union with South Africa, there is still a border to cross (Black, Citation2017).

There are other constraints as well. High quality, technical and delivery reliability standards in the automotive industry also constrain the development of a regional supply base. The shortage of skills meant that when there was a higher-level technical problem at a component plant in Botswana, costly delays were caused by experts having to be sent from South Africa (Markowitz & Black, Citation2019). SADC member states that have automotive industries protected as sensitive industries within SADC’s free trade area have indicated that the APDP and South Africa will undercut their own infant industries if they loosen domestic protection in favour of a regional tariff scheme. SADC rules of origin are also difficult to adhere to given the lack of capacity (especially for the export of completely built units), thus limiting the prospects for the regional free flow of goods (Markowitz, Citation2016). Other SADC countries also do not have the capacity or financial support to achieve the 40% local content levels prevalent in South Africa. Additionally, as a customs union, all countries within SACU must comply with the APDP. Although this creates the potential for countries to utilise APDP support, it also leads to many challenges, as Botswana, Lesotho, Namibia and Eswatini lack the capacity to comply with its complex suite of regulations. In order to receive a production rebate credit certificate (PRCC) for exporting under the APDP, they must achieve a level of domestic value addition that they currently cannot achieve (unless they export components only to South African vehicle assemblers that then apply for the PRCC). Thus, there are significant policy barriers in facilitating free trade within SACU narrowly or SADC more broadly.

For some of the countries of the region, the production of parts for the aftermarket may offer an industrialisation opportunity. There may also be scope for automotive industry cooperation between the larger economies in their respective regions, for example, Nigeria, Kenya and South Africa. But distances and especially transport costs are high between these countries.

One possibility is for South Africa to supply motor vehicles into the region, and to import motorcycles. This is identified as an opportunity within the SAAM. South Africa has indicated it is prepared to increase its motorcycle tariffs from 0% to 10% in support of motorcycle assembly in other SACU or SADC countries (Barnes et al., Citation2016b). This would provide preferential market access into a South African motorcycle market of 20,000–30,000 units per annum. Motorcycles are substantially easier to assemble than motor vehicles, and require less sophisticated infrastructure, potentially providing less developed economies an easier access point for automotive industry activity.

A similar opportunity could apply in respect of electric vehicle (EV) assembly. EVs are much easier to assemble and have far fewer parts than their internal combustion engine (ICE)-based equivalents. The global shift towards EV consumption may therefore open more opportunities for SSA vehicle assembly.

Notwithstanding these potential developments, the South African-based industry could also assist in transferring skills and industrial capabilities to the region. The imperative lies in the economies of scale and increased foreign investments that are realised in the long term from developing integrated regional value chains. Even in the short term, the development of automotive industries outside South Africa could provide South African automotive component manufacturers the opportunity to export to infant assembly operations in the region (Black et al., Citation2019).

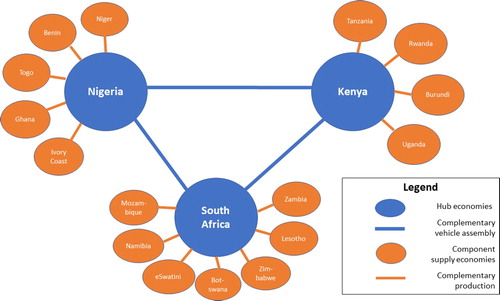

One important development is the launch of the African Association of Automotive Manufacturers (AAAM), a process which has been driven by the South African-based vehicle producers (Black et al., Citation2019). This association seeks to provide support to automotive industries on the African continent and together with South Africa’s Department of Trade and Industry and other stakeholders is promoting the establishment of a subcontinental ‘Automotive Pact’. Detailed proposals have been developed drawing on consultations with government and industry leaders in Nigeria, Ghana, Kenya and South Africa (Barnes et al., Citation2019). The idea is to promote the establishment of a number of regional production hubs () which would draw on regional supply chains that include networks of suppliers located in neighbouring countries. These hubs would include South Africa, Nigeria, Kenya and possibly also Ghana and Ethiopia. The Kenyan assembly hub would in turn draw on suppliers not only in Kenya but also in Tanzania, Uganda, Rwanda and Burundi, while the Nigerian or Ghanaian hub would draw on ECOWAS for broader component supply. This hub and spoke model has been endorsed by the AAAM, whose executive director was quoted by Venter (Citation2020) as arguing that ‘the goal for the next two to three years is to develop a sustainable vehicle manufacturing hub in West and East Africa, supported by spoke components manufacture in the respective regions’.

Figure 1. Hub and spoke model for SSA Automotive Pact development. Source: Barnes et al. (Citation2019).

The potential gains of the hub and spoke model for vehicle producers and for ‘hub’ countries, especially South Africa, are quite evident. However, it is much less likely that the ‘spoke’ countries will realise short-term gains unless there is closely coordinated industrial and associated trade policy development within the framework of the AfCFTA. Even if large-scale assembly operations were to develop in the hub countries, the prospects in the short term for far-flung supply chains across national boundaries appear limited without industrial and trade policy interventions that are simultaneously supported by technical infrastructure and skills development. The difficulties that Lesotho and Botswana have encountered in attracting component manufacturers that could potentially supply the well-established South African automotive industry are instructive in this regard.

The biggest challenge facing the development of a regional automotive industry, however, is that of used cars. For a large-scale vehicle assembly industry to have any future in the region, used car imports will have to be substantially restricted and this would impose large welfare costs for consumers who would lose access to the imports of these cheap vehicles. SSA country governments would also face reduced revenues from the import duties on used vehicles entering their markets. Reducing imports of used cars is therefore likely to be politically complicated.

5. Conclusion

This paper set out to examine the links between regional integration, RVCs and the development of the automotive industry in SSA. Regional integration is a developmental project of extreme importance for Africa. It will encourage regional trade and industrialisation and lead to the development of regional value chains. The development of regional value chains could in turn add momentum to further integration and expand the importance of the region within global value chains. This has the potential to crowd in further multinational investment and encourage rapid industrialisation, as has been observed for the ASEAN automotive industry.

While there is broad agreement that regional integration is essential for Africa to develop a significant automotive industry, more attention needs to be paid to how the benefits can be widely shared. Most countries, especially the smaller economies, are not likely to attract automotive investment. This should not matter if they are attracting investment in other sectors. One implication is that it is unlikely that the automotive industry will drive regional integration independently of a broader integration process which sees the development of regional value chains across a multitude of sectors helping to bind the continent into a larger common market. This will require improved infrastructure and the removal of remaining tariff and non-tariff barriers. In respect of the automotive industry it also means that any form of regional market and associated production model will need to be carefully crafted through a coordinated set of mutually beneficial regional and national policies.

It is this potential that frames the ideal scenario painted by the ex-South African Minister of Trade and Industry, Alec Erwin, who notes that:

A possible future scenario in Africa is a configuration where an OEM plant in South Africa produces models for the South African, Nigerian, African and world markets thereby gaining longer production runs for those models and increasing competitiveness. Then a plant from the same OEM in Nigeria could produce other models in its range for the Nigerian, South African, African and world markets. This lowers overall costs of production, lowering prices and increasing product choice in all economies. As other significant African production sites emerged they could likewise fit into a similar configuration. (Erwin, Citation2019)

Notwithstanding this expansive vision, regional integration gives rise to complex economic and political dimensions. It will bring major gains, but they will not necessarily be widely shared. Participants at an SSA AutoPact workshop in March 2019 expressed concerns that it ‘appears to be a South African initiative, with limited visible benefits for other countries’.Footnote6 In southern Africa there are already concerns about South Africa’s ongoing dominance of regional trade. In East Africa, industrial development is likely to be focused on Kenya where there is already a significant base. Policy makers will need to consider these aspects and devise remedies to ensure such tendencies are mitigated.

Disclosure statement

No potential conflict of interest was reported by the authors.

Notes

1 See, for example, Carrillo (Citation2004); Laplane & Sarti (Citation2004); Layan & Lung (Citation2004); and Markowitz (Citation2016).

2 For an early assessment of developmental regionalism in the developing country context, see Sloan (Citation1971).

3 Smaller plants could, of course, be viable where high effective rates of protection on vehicle assembly prevail.

4 Completely knocked down (CKD) assembly involves the full assembly of the car including body panels and requires much higher investment in the assembly plant than SKD.

5 Cited in Jeremiah (Citation2017).

6 Report on AutoPact Orientation Workshop, Annexure 5, p. 79, in Barnes et al. (Citation2019).

References

- Abiola, B, 2008. The Nnewi automotive components cluster in Nigeria. In Zeng, D (Ed.), Knowledge, technology and cluster-based growth in Africa. World Bank, Washington, 53–64.

- Adeniyi, R, 2015. ECOWAS CET: FG smuggles 70% duty, tax on used, new vehicles. National Daily (online), 27 April. http://www.nationaldailyng.com/business/maritime/3736-ecowas-cet-fg-smuggles-in-70-duty-tax-on-used-new-vehicles Accessed 16 April, 2018.

- Adeya, C, 2008. The Suame manufacturing cluster in Ghana. In Zeng, D (Ed.), Knowledge, technology and cluster-based growth in Africa. World Bank. African Development Bank, Washington, 15–24.

- African Development Bank, 2019. African economic outlook. African Development Bank, Abidjan.

- African Export-Import Bank, 2018. African Trade Report 2018. Afreximbank, Cairo.

- AIEC (Automotive Industry Export Council), 2015. South African automotive export manual 2015. AIEC, Pretoria.

- AIEC, 2017. South African automotive export manual 2017. AIEC, Pretoria.

- AIEC, 2019. South African automotive export manual 2019. AIEC, Pretoria.

- Arza, V, 2011. MERCOSUR as an export platform for the automotive industry. CEPAL Review 2011(103), 129–52.

- Auto Trend Ghana, 2019. http://moti.gov.gh/autopolicy.php Accessed 20 March 2019.

- Barnes, J, Black, A, Comrie, D & Hartogh, T, 2016a. Phase 2 report – Global automotive industry scan: Informing the development of the South African automotive industry masterplan to 2035. Compiled for the South African national government’s Department of Trade and Industry, 27 June.

- Barnes, J, Black, A, Comrie, D & Hartogh, T, 2016b. Phase 4 report – South African Automotive Masterplan to 2035. Compiled for the South African national government’s Department of Trade and Industry, 11 November.

- Barnes, J, Erwin, A & Ismail, F, 2019. Realising the potential of the Sub-Saharan African automotive market: The importance of establishing a sub-continental Automotive Pact: A Report for Trade & Industrial Policy Strategies (TIPS) and the African Association of Automotive Manufacturers (AAAM).

- Black, A, 2017. Diversifying Lesotho’s manufacturing economy: Automotive components mini-study. Unpublished report for the government of Lesotho.

- Black, A, Edwards, L, Ismail, F, Makundi, B & Morris, M, 2019. Spreading the gains? Prospects and policies for the development of regional value chains in Southern Africa. UNU-WIDER Working Paper 48/2019. UNU-WIDER, Helsinki.

- Black, A, Edwards, L, Ismail, F, Makundi, B & Morris, M, 2021. The role of regional value chains in fostering regional integration in Southern Africa. Development Southern Africa. doi:10.1080/0376835X.2020.1834354.

- Black, A, Makundi, B & McLennan, T, 2017. Africa’s automotive industry: Potential and challenges. Working Paper 282. African Development Bank, Abidjan.

- Black, A & Muradzikwa, S, 2004. The limits to regionalism: The automotive industry in the Southern African Development Community. In Carrillo, J, Lung, Y & van Tulder, R (Eds), Cars, carriers of regionalism? Palgrave Macmillan, London, 173–88.

- Brautigam, D, 1997. Substituting for the state: Institutions and industrial development in Eastern Nigeria. World Development 25(7), 1063–80.

- Carrillo, J, 2004. NAFTA: The process of regional integration of motor vehicle production. In Carrillo, J, Lung, Y & van Tulder, R (Eds), Cars, carriers of regionalism? Palgrave Macmillan, London, 104–17.

- Das Nair, R, Chisoro, S & Ziba, F, 2018. The implications for suppliers of the spread of supermarkets in Southern Africa. Development Southern Africa 35(3), 334–50.

- de Backer, K & Miroudot, S, 2014. Mapping global value chains. ECB Working Paper No. 1677. SSRN: https://ssrn.com/abstract=2436411.

- Erwin, A, 2019. Building an automotive industry in Africa. In Africa Policy Review. http://africapolicyreview.com/building-an-automotive-industry-in-africa/ Accessed 8 February 2019.

- Farrell, R & Findlay, C, 2001. Japan and the ASEAN-4 Automotive Industry. Australia–Japan Research Centre Working Paper 24/2001.

- Fujita, M, 1998. Industrial policies and trade liberalization: The automotive industry in Thailand and Malaysia. In Omura, K (Ed.), The deepening economic interdependence in the APEC region. APEC Study Center, Tokyo, 149–87.

- Humphrey, J & Oeter, A, 2000. Motor industry policies in emerging markets: Globalisation and the promotion of domestic industry. In Humphrey, J, Lecler, Y & Salerno, M (Eds), Global strategies and local realities: The auto industry in emerging markets. Macmillan, 42–71.

- Ismail, F, 2016. The changing global trade architecture: Implications for Sub-Saharan Africa’s development, Trade Hot Topics, Issue 131. The Commonwealth.

- Ismail, F, 2020. A call for a developmental regionalism approach to the African Continental Free Trade Area (AfCFTA). Great Insights 9(1).

- Jeremiah, K, 2017. Nigeria’s auto assemblers running glorified manufacturing plants. The Guardian (Lagos), 25 September. https://guardian.ng/business-services/nigerias-autoassemblers-running-glorified-manufacturing-plants/.

- Kobayashi, H, Jin, Y & Schroeder, M, 2015. ASEAN economic community and the regional automotive industry: Impact of ASEAN economic integration on two types of automotive production in Southeast Asia. International Journal of Automotive Technology and Management 15(3), 268–91.

- Laplane, M & Sarti, F, 2004. MERCOSUR: Interactions between governments and producers and the sustainability of the regional automotive industry. In Carrillo, J, Lung, Y & van Tulder, R (Eds), Cars, carriers of regionalism? Palgrave Macmillan, London, 121–38.

- Layan, J-B & Lung, Y, 2004. The dynamics of integration in the European car industry. In Carrillo, J, Lung, Y & van Tulder, R (Eds), Cars, carriers of regionalism? Palgrave Macmillan, London, 57–74.

- Lung, Y & van Tulder, R, 2004. Introduction: In search of a viable automotive space. In Carrillo, J, Lung, Y & van Tulder, R (Eds), Cars, carriers of regionalism? Palgrave Macmillan, London, 1–20.

- Markowitz, C, 2016. The potential for regional value chains in the automotive sector: Can SADC learn from the ASEAN experience? SAIIA Occasional Paper 231.

- Markowitz, C & Black, A, 2019. The prospects for regional value chains in the automotive sector in Southern Africa. In Scholvin, S, Black, A, Diez, J & Turok, I (Eds), Value chains in sub-Saharan Africa: Challenges of integration into the global economy. Springer, Cham, 27–42.

- Morris, M, Staritz, C & Plank, L. 2016. Regionalism, end markets and ownership matter: Shifting dynamics in the apparel export industry in sub Saharan Africa. Environment and Planning A: Economy and Space 48(7), 244–65.

- Natsuda, K, Segawa, N & Thoburn, J, 2013. Liberalization, industrial nationalism, and the Malaysian automotive industry. Global Economic Review 42(2), 113–34.

- OICA, 2017. 2016 sales statistics. http://www.oica.net/category/production-statistics/2017-statistics Accessed 26 June 2018.

- Sloan, J, 1971. The strategy of developmental regionalism: Benefits, distribution, obstacles and capabilities. Journal of Common Market Studies 10(2), 138–62.

- Stuart, J, 2020. The automotive component trade in Africa: Its place and potential. tralac Working Paper S20WP02/2020. tralac, Stellenbosch.

- Sturgeon, T, Chagas, L & Barnes, J, 2017. Rota 2030: Updating Brazil’s automotive industrial policy to meet the challenges of global value chains and the new digital economy; Report for the World Bank, October.

- Sturgeon, T & Florida, R, 1999. The world that changed the machine: Globalization and jobs in the automotive industry. Final report to the Alfred P Sloan Foundation, International Motor Vehicle Program.

- Sturgeon, T & Van Biesebroeck, J, 2011. Global value chains in the automotive industry: An enhanced role for developing countries? International Journal of Technological Learning, Innovation and Development 4(1/2/3), 181–205.

- Techakanont, K, 2014. Managing integration for better jobs and shared prosperity in the ASEAN economic community: The case of Thailand’s automotive sector. http://apirnet.ilo.org/resources/managing-integration-for-better-jobs-and-shared-prosperity-in-the-asean-economic-community-the-case-of-thailands-automotive-sector Accessed 25 May 2018.

- Ugwueze, M, Ezeibe, C & Onuoha, J, 2020. The political economy of automobile development in Nigeria. Review of African Political Economy 47(163), 115–25.

- Venter, I, 2020. An African automotive industry is starting to emerge, Engineering News, 20 April. https://m.engineeringnews.co.za/article/an-african-automotive-industry-is-starting-to-emerge-2020-04-10/rep_id:4433.

- Zizhou, F, 2009. Linkages between trade and industrial policies in Botswana. http://www.tips.org.za/files/botswana_paper.pdf Accessed 25 May 2018.