ABSTRACT

The race to rapidly decarbonise and digitalise the global economy by 2030 to avoid temperatures rising above 1.5C has been subsumed by geopolitics that remains anchored in realist power struggles, now revolving around Sino-American hyper-competition. The Russian invasion of Ukraine further undermined interdependence and prompted unprecedented levels of economic statecraft. Access to indispensable minerals for a net zero future has thus become more securitised. The European Union (EU) has pushed back against bipolar geopolitics by utilising its normative, economic and regulatory power and strong networks of global institutional relations to maintain a competitive but working relationship with the People’s Republic of China (PRC). Such an approach may help broker broader global institutional collaboration to ensure that decarbonisation is for all, not just for the few.

The growing rivalry between the People’s Republic of China (PRC) and the United States (US) has favoured the ongoing construction of world politics around bipolar imaginaries, that promote bilateral, ad hoc side deals that at best duplicate and at worst undermine global efforts, including those to rapidly decarbonise and digitalise the global economy and avoid temperatures rising above 1.5C. This power struggle dominates the airwaves, influences and shapes the global discourse, and reduces opportunities for fruitful multilateral cooperation.

Russia’s invasion of Ukraine in 2022 further complicated the already fraught geopolitical landscape and drove an even deeper wedge into the world order. The shock has dealt a severe blow to an already fragile post-pandemic economic recovery and has tilted the balance toward more securitised assessments of global interdependence. Indeed, interdependence is now predominantly portrayed as a liability rather than an asset. For years, integration – financial and technological – was championed by major powers as the ultimate goal. As Thomas Wright (Citation2017) argues, however, now that power struggles have intensified, states can use the extraordinary levels of global interdependence in ways that impact their rivals even without resorting to direct conflict. The war in Ukraine, which resulted in the disruption of rail and truck transportation, the rerouting of ships and unprecedented levels of economic statecraft, have all contributed to a scramble for supply-chain diversification and onshoring in response to the weaponisation of interdependence (Farrell and Newman Citation2019). In the words of Rosa Brooks, globalisation has created a world in which “everything became war” (Brooks Citation2017). In fact, continuous supply-chain disruptions, the spike and volatility of fossil fuel prices, the steep rise of food costs and growing inflation, further augmented global insecurity and cemented this narrative.

Economic statecraft had previously and repeatedly been used by the US and at times also the EU to modify the actions of certain actors: on Russia, for instance, over the annexation of Crimea in 2014, and on Iran in an “effort” to “persuade” the country to give up its nuclear ambitions. The measures were justified as actions taken in “defence” of globalisation, stability and peace, and as ways to discourage “rogue” powers from threatening other states and the international order. The PRC, for its part, used economic statecraft by “unofficially” curtailing rare earth shipments to Japan in 2010. However, these kinds of measures have over time prompted sanctioned nations to carve out spheres of independence in order to withstand the impacts of “coercive” measures. Though a costly option, some actors like Putin’s Russia intentionally chose to hedge so as not to remain overly reliant on one country that is not as dependent on them (Hirschman Citation1945). Ahead of the war in Ukraine, Putin strengthened Russia’s political and economic relations with the PRC, prepared a war chest from a windfall of fossil fuel sales and took measures to protect and expand domestic consumer good production ahead of possible future sanctions. Still, while these developments were already afoot, little attention was given to the risks of expanding networks of exchange because a bipolar world was considered a thing of the past. Conditions, however, have changed. Rivalry and hyper-competition are upending the post-Cold War world order. Some experts are openly declaring that the days of stability, unipolarity and global liberalism are over (Badré and Tiberghien Citation2022). Sino-American rivalry is both accelerating global power re-alignments but is also forcing the hand of many nations to choose a side even though their economic and political interests remain deeply intertwined in global networks of interdependence.

This geopolitical minefield, moreover, raises questions about the pace by which the decarbonisation and digitalisation projects will be able to proceed, the timeline by which nations will be able to fulfil their already ambitious climate commitments, cybersecurity concerns and the precariousness of essential supply chains, especially those of critical minerals (Vakulchuk et al. Citation2020). The unravelling of these global supply chains is particularly worrisome because they had enabled green technologies to rapidly be designed, built and scaled-up (Nahm Citation2021). Severing them, therefore, would also jeopardise the commercialisation of end products and their design for mass production at a critical time when an already narrow window for constructing new sustainable infrastructure and deploying green technology is rapidly closing.

The world now stands at a crossroads. Bipolar Sino-American rivalry has already undermined interdependence and prompted the scramble to re-shore, renationalise and decouple supply chains from rival powers and in some cases even friendly competitors. This article, however, argues that there is another pathway available given the urgent timeframe in which nations must honour their commitments to effectively tackle the climate crisis which poses the greatest threat to worldwide stability. The EU’s distinctive approach and policy blueprint for a net zero future prioritises resilience and the circular economy versus decoupling, and values multilateralism and liberal-institutionalism. It thus offers a workable alternative to realist and increasingly securitised frames fuelled by the politics of contention. Even after the Russian invasion helped strengthen Euro-Atlantic relations and revived NATO, the EU continued to push back against direct opposition to the PRC, because it views this bras de fer as pushing geopolitical rivalries beyond planetary boundaries. European norms, values and governance structures more closely resemble those of the US. Still, Brussels’ policy frameworks and Green Deal goals explicitly prioritise the building of more diverse and resilient global supply chains, without directly opposing or excluding the PRC.

The article explores ways in which the EU, as a normative, economic and regulatory power with strong links to a network of global institutions, can help broker wider global collaborations, so that decarbonisation can be achieved by all. The strengthening of EU networks in the developing world, especially after the announcement of its Global Gateway Initiative (European Commission Citation2021) to support investment in climate-resilient infrastructure in the developing world, as well as its competitive but working relations with the PRC, could also help to diffuse some of the growing Sino-American tensions and prevent a return to a bipolar configuration that undermines global efforts to tackle climate change.

Fraught geopolitics

Already under George W. Bush, the US became determined to take a tougher stance on the PRC and demonstrated greater support for Taiwan. The events of 9/11, however, recalibrated priorities. The US would collaborate with Beijing in the context of “responsible stakeholders” managing global issues (Sutter Citation2020, 217). During the Obama administration, concerns that the PRC’s spectacular rise posed an imminent threat to US global leadership solidified. The 2008 financial crisis had, moreover, given rise to voices in the Chinese establishment suggesting that US global hegemony was waning. The Obama administration sought to rebalance the US global footprint by focusing on the Asia-Pacific region and withdrawing from the Middle East (Kalantzakos Citation2017).

In 2009, the White House called for a “return to Asia”. Building on many of the previous administration’s initiatives, such as the China-US Strategic Economic Dialogue (SED), the US combined several innovative and proactive policies in the region. For instance, it signed the ASEAN Treaty of Amity and Cooperation and joined the East Asia Summit, a regional collaboration forum. Washington’s political rhetoric changed noticeably to refer to the twenty-first century as America’s “Pacific Century” (Obama Citation2011; Flournoy and Davidson Citation2012; Goldberg Citation2016; Clinton Citation2011; U.S. Department of Defense Citation2012). Chinese leaders perceived this shift as an indication that the PRC had become the main opponent to Washington’s goal of continued dominance of the world order.

In 2011, the “strategic pivot” towards Asia was announced and involved not only a transfer of resources or a mere exercise of smarter, more systematic US policy. It demonstrated unequivocal resolve to sustain global leadership, secure US interests and promote its values. Until that time, the US and the EU had greatly encouraged and facilitated the PRC’s integration into the world system. Beijing’s ascendance, its growing global impact, increased assertiveness and, latterly, the heavy-handed autocratic policies frequently launched under Xi Jinping’s leadership, changed the thinking in Washington not only in the executive branch but also in Congress. The pivot to Asia marked the start of a divergence in US and EU policy towards the PRC because it ushered in a new cycle of bipolar competition that troubled Brussels (Sverdrup-Thygeson et al. Citation2016).

Under Trump, rivalry turned into hyper-competition with the PRC. Wariness of Beijing’s threat to US technology dominance, its military activities in the South China Sea and tensions with Taiwan produced bipartisan Congressional support for a tougher stance on the PRC. The trade wars underscored this shift, but they also undermined the centrality of the World Trade Organisation, heightened political rivalries, reduced scientific collaboration and revealed a pronounced clash of economic and leadership ambitions (Wei Citation2019; Feder Citation2019). Scepticism toward the PRC’s signature Belt and Road Initiative (BRI) turned into open critique. In the eyes of its detractors, and particularly the US, the BRI aims to consolidate China’s “stranglehold” on the world. More widespread critique of what Beijing presented as the sole comprehensive vision to spur economic growth in the developing world, revolved around the PRC’s production of a carbon-intensive, rather than a green, BRI. Furthermore, Beijing was seen as creating a vehicle to spread the PRC’s top-down, centralised one-party governance and technocracy-driven policy-making, its preference for setting quantitative goals and targets and adopting mechanistic approaches to policy design, as well as environmental authoritarianism to modify citizen behaviour and realise government targets (Li and Shapiro Citation2020). Compounding the worries of its rivals, Beijing had also been actively deepening its engagement with global institutions and exerting growing influence over them (Kalantzakos Citation2021a, xi-xxxii).

Calls to urgently “desinicise” supply chains became more pronounced in Washington policy circles. The Trump administration called for an end to interdependence and supply networks reliant on the PRC as its central policy priority. Critical minerals took a front seat in this effort to significantly reduce reliance on Beijing framed as indispensable to the defence and the tech industry. In December 2017, Trump signed Executive Order 13817 (“A Federal Strategy to Ensure Secure and Reliable Supplies of Critical Minerals”) and on 30 September 2020, Executive Order 13953 addressing the “Threat to the Domestic Supply Chain from Reliance on Critical Minerals from Foreign Adversaries” (Federal Register Citation2020). In 2019, the Trump administration announced plans to collaborate with Australia (Reuters Citation2019) to finance and develop critical materials projects, and the State Department launched the Energy Resource Governance Initiative (U.S. Department of State Citation2019) as a critical materials initiative (Kalantzakos Citation2021a).

Anti-China sentiment continues unabated under the Biden administration (Toosi Citation2021). Moreover, having made it his goal to urgently decarbonise the US economy and lead in the production of new green technologies, Biden has continued to underwrite efforts to build US resilience, prioritising the desinicisation of supply chains as his predecessor had done. On 24 February 2021, Biden signed an executive order, asking for a “report identifying risks in the supply chain for critical minerals and other identified strategic materials, including rare earth elements (as determined by the Secretary of Defense), and policy recommendations to address these risks” (The White House Citation2021a). In June 2021, the findings of the “Critical Minerals Supply Chain Review” were made public (The White House Citation2021b).

In December 2021, Biden signed the “Uyghur Forced Labor Prevention Act” into law, with bipartisan support (Sonmez Citation2021). In December 2021, Biden held a Democracy Summit in which he underscored that the US was “committed to working with all those who share those values to shape the rules of the road”, and added that the US would stand by those “who give their people the ability to breathe free and not seek to suffocate their people with an iron hand” (Taipei Times Citation2021; Hilman Citation2021). In January 2022, the bill “On Restoring Essential Energy and Security Holdings Onshore for Rare Earths Act of 2022” was introduced in the US Senate, aimed at forcing defence contractors to stop purchasing Chinese rare earths by 2026 (Scheyder Citation2022). Standing up to China garners bipartisan support. Indeed, minimising reliance on the PRC for critical minerals constitutes a core priority for both defence and green industrial policies.

On the other side of the Atlantic, however, the EU maintains a historically distinct approach to its relations with the PRC. The EU may view Beijing as a systemic rival, but it is pushing back against the US model of bipolar competition. While the EU applies critical pressure on issues such as human rights, it has not turned squarely against the PRC and has sought avenues of collaboration and exchange, in line with its own wider strategic goals and views of the world order. Although the EU acknowledges that the world has become more complex and contested and recognises growing tensions and threats to multipolarity especially after the Russian invasion of Ukraine, it remains committed to deepening rules-based multilateralism and setting common standards with its partners (EEAS Citation2019; EEAS Citation2022). It believes it can stay true to its values and principles and pursue “variable geometry multilateralism” in recognition that there are no longer fixed sets of like-minded countries that agree on all issues. In that way, it can form the best possible group of varied stakeholders to deal with any specific issue (Kalantzakos Citation2021b, 41-7). After all, the EU views itself as a liberal and civilian power of a normative persuasion that champions liberal political rights, collective security and multilateralism. Following the end of the Cold War, as transatlantic discords multiplied and divergence in perspectives became more crystalised, the EU pursued its own global agenda and developed domestic and foreign policy instruments in support of it (Telò Citation2019; Lucarelli and Manners Citation2006; Youngs Citation2010). The sharp contrast between the transatlantic partners brings to mind Robert Kagan’s Citation2003 observation that “Europe is turning away from power, or to put it a little differently, it is moving beyond power into a self-contained world of laws and rules and transnational negotiation and cooperation […]. Meanwhile, the United States remains mired in history, exercising power in the anarchic Hobbesian world where international laws and rules are unreliable” (Kagan Citation2003).

Admittedly, relations between the PRC and the EU have become more difficult following a barrage of tit-for-tat measures over events in Hong Kong and the treatment of the Uyghurs. Still, the EU insists that relations with the PRC are multi-faceted and engagement should continue (Ridgwell Citation2021). EU-China relations also became strained over the PRC’s ambiguous position in relation to the Russian invasion of Ukraine which blamed NATO for the war and expressed disapproval for the “return” to a cold war mentality, advocating instead for common, comprehensive, cooperative and sustainable security (Ministry of Foreign Affairs of the People’s Republic of China Citation2022). European Commission President Ursula von der Leyen, European Council President Charles Michel, and High Representative Josep Borrell vocalised these concerns directly to Beijing. In contrast to the Biden-Xi summit on that same issue, however, the EU did not point a finger directly at Beijing, but rather spoke of the centrality of China-EU trade relations, areas of overlapping strategic interest and extensive opportunities to deepen collaboration (Liboreiro and Scandura Citation2022). EU leaders simultaneously kept the agenda more open to include other interrelated matters, such as cooperation on global food security, climate change and the fight against COVID (European Council Citation2022). The EU underscored its continued resolve toward decarbonisation while drastically reducing reliance on Russian fossil fuels (European Commission Citation2022a; Consilium Citation2022; Abnett Citation2022).

It is also instructive to highlight the EU’s distinct approaches to both the decarbonisation and the digitalisation of its economy, as they differ from those of the US. Some policies discussed in this article of course reflect similarities and share the objective of securing uninterrupted access to critical materials and their important applications. One telling difference, however, is that the EU speaks of building resilient supply chains and moving toward a circular economy (European Commission Citation2020) while encouraging global investment, building new networks of interdependence and strengthening existing ones, without alienating the PRC. This is not surprising given the extent of trade relations with the PRC but more importantly the architecture of the EU-China Comprehensive Strategic Partnership (European Commission Citation2022c; Scott Citation2007; Zhongping and Jing Citation2014), which has made climate and the environment a central pillar of collaboration. Reflected in the EU-China joint summit statement of 2019, both parties agreed to closely cooperate on all three pillars of the UN (human rights, peace and security, and development), and on the 2030 Agenda.

More specifically, China and the EU placed significant emphasis on sustainable economic development and connectivity, the circular economy, biological diversity, ocean governance and regional peace and security (European Commission Citation2022c). In September 2020, moreover, the EU and the PRC agreed to begin a China-EU High-Level Environment and Climate Dialogue (HECD) and forge a China-EU green partnership (Mission of the People's Republic in the European Union Citation2020). Beijing has praised EU efforts in green finance and particularly the sustainable finance classification scheme. Importantly, since 2021, the PRC’s central bank has been co-operating with the EU to converge green investment taxonomies across the two markets to implement a jointly recognised classification system for the environmental credentials of businesses (Li and Yu Citation2021). Robust exchanges on Environmental, Social and Governance (ESG) criteria are also ongoing.

These efforts of engagement, exchange and coordination stand in sharp contrast to the lack of a meaningful transatlantic strategy on climate. The triumphant passing of the $430 billion Inflation Reduction Act in the summer of 2022, for instance, while demonstrating US resolve to take climate action, has been highly criticised by its allies because in its effort to desinicise supply chains, Washington is also blocking US partners from partaking in its domestic transition (Deutsche Welle Citation2022; Korea Joongang Daily Citation2022; Baek Citation2022). Moreover, the terms by which the US seeks to build chip capacity domestically through the Chips Act of 2022 are also designed to significantly constrain those allies leading in chip production from continuing to also produce for the PRC market.

The EU as international agenda-setter for climate action

Recognising that the climate crisis radically influences growth models, development, poverty, international politics and leadership models, the EU has positioned itself as the international agenda-setter for climate action. Not only has it sought a leadership role in climate negotiations, but it has also focused on delivering concrete results at home. The EU’s leadership role has not been static and has displayed different approaches and styles which reflect its key strengths: its large economy, its bargaining skills and its diplomatic agility in fostering agreements. It has been able to redefine interests for a global audience by conceptualising notions of sustainability along with narratives of ecological modernisation and the transition to a low-carbon economic model for growth. Although EU member states have not always been able to speak with one voice, in the climate negotiations the EU has managed to project a position of long-term commitment to the process and has maintained coordination among its member states to display its strong political will at critical junctures. It has also kept multilateral climate negotiations alive. Even though the US under Obama and later Biden tried to supplant the EU as a climate leader through a joint commitment with the PRC, in reality, it is the EU that has worked behind the scenes through the difficult years, strategically building alliances with the developing world and creating groups of higher ambition. The Paris Agreement of 2015 was a hard-won victory for the climate, and even at COP 26 the EU stayed the course and made more concrete and transparent commitments both within the Union and to assist its partners in the developing world to reach net zero by mid-century. Case in point: at COP 27, EU Executive Vice President and climate chief Frans Timmermans demonstrated the EU’s strategic autonomy, singular climate ambition and desire to act as a bridge builder to accelerate the green transition. In the 11th hour, to overcome the impasse over the creation of a new loss and damage fund that was proposed by G77 plus China and opposed by developed nations including the US, the EU stepped up to agree under the condition that countries like China (the world’s second-largest economy that maintains a UN “developing nation” classification), the Gulf states and other emerging economies that could, would participate and thus broaden the fund's financial donor base, as these countries are among the largest emitters. While the EU initiative “forced” China’s hand to walk a fine line between expressing support for helping vulnerable developing nations and agreeing to contribute funds to that particular scheme, it facilitated the historic agreement on loss and damage at COP 27 (Harvey Citation2022).

Collaboration on environmental and climate issues has been an important pillar of Sino-European cooperation since 2005 (European Commission Citation2018). The EU, for instance, has supported low-carbon urban development in China and helped update local urban planning and technical standard guidelines by drawing on EU best practices. Other EU projects have helped small and medium enterprises (SMEs) adopt energy-efficient solutions to reduce their environmental impact. In Xi’an, for example, more than 50 local SMEs were provided with green financing to invest in clean production. The EU also engaged with the PRC via thematic and regional programs focused on areas of importance for sustainable and inclusive development in China and the broader Asian region. These programs include low carbon development and sustainable urbanisation, environmental management and governance, trade and the private sector, good governance and the rule of law, reducing vulnerabilities and inequalities, support for China-EU Sectoral Policy Dialogues and people-to-people exchanges (European Commission Citation2022c).

The EU's road to net zero

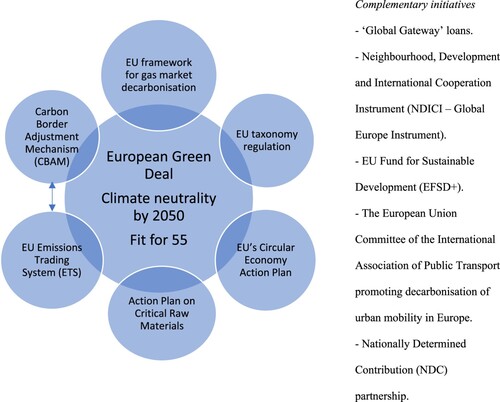

In December 2019, the EU announced the European Green Deal, with the stated goal of transforming the EU into a modern, resource-efficient and competitive economy by committing to net zero emissions of greenhouse gases by 2050; decoupling economic growth from resource use; and leaving no person and no place behind (European Commission Citation2022b). Ultimately, the EU’s objective was to become the first climate-neutral continent in the world. The Green Deal would help prepare all sectors of the economy to meet this challenge, while mapping out the path to fulfil the EU’s pledge to reduce emissions by at least 55 percent by 2030 compared to 1990 levels. The so-called “Fit for 55” Initiative (see ) solidifies the EU’s ambition via a web of policy proposals that include comprehensive changes to the existing EU Emissions Trading Scheme (EU ETS); a review of the 2009 Renewable Energy Directive to increase the current EU-level target of at least 32 percent of renewable energy sources in the overall energy mix to at least 40 percent by 2030; and a revision of the 2012 Energy Efficiency Directive by increasing the current EU-level target for energy efficiency from 32.5 percent to 36 percent for final energy consumption and to 39 percent for primary energy consumption. Measures also include a revision of the rules on CO2 emissions for cars and vans; a revision of existing legislation to accelerate the deployment of infrastructure for recharging vehicles or refuelling them with alternative fuels and to provide alternative power supplies for ships in ports and stationary aircraft; the introduction of a Carbon Border Adjustment Mechanism (CBAM); and the production of greener fuels for shipping and aviation. In addition, the EU expects that hydrogen produced using renewable energy (also known as “green” or “clean” hydrogen) will play a key role in decarbonising sectors where other alternatives may not be feasible or more expensive. These include transport and energy-intensive industrial processes and will be a crucial element in the EU strategy for energy system integration (European Commission Citation2022d).

Figure 1. EU decarbonisation strategy

Several funding mechanisms, totalling over one trillion dollars, have been established to facilitate the EU’s Green Deal. More than half of the funding (€528 billion) will come directly from the EU budget and the EU Emissions Trading Scheme. The remainder will be sourced from the InvestEU program, including €279 billion from the public and private sectors and €114 billion from national co-financing until 2030. The European Innovation Council has also set aside a €300 million budget to invest in market-creating innovations that contribute to the goals of the EU Green Deal.

Several additional policy instruments have been designed and deployed in order to support and facilitate the EU’s net zero ambitions. For instance, the EU’s Taxonomy Regulation helps to identify and classify “environmentally sustainable economic activities” (European Commission Citation2022e). According to the European Commission (Citation2022d), “the EU taxonomy would provide companies, investors and policymakers with appropriate definitions for which economic activities can be considered environmentally sustainable.” In addition, the EU adopted a Circular Economy Action Plan (CEAP) in 2015 that includes measures to enhance the share of recyclable and reused materials across a wide range of economic sectors and industries on its soil (Anastasio Citation2021). This in turn contributes to higher energy efficiency and facilitates the energy transition in the EU.

Importantly, driven primarily by the automotive industry’s realisation that the future lies in electric vehicles – especially after Volkswagen’s “Dieselgate” scandal of 2015—the EU has turned its attention squarely to related areas in which it was particularly vulnerable (The Guardian Citation2015; Jolly Citation2022). Battery technology and production were an important gap where the EU remained reliant on China, which has already designated electric vehicle production as a particular niche. In 2017, the European Battery Alliance (EBA) was set up to address the need for efficient batteries that were essential for transport, power and industrial applications. Around 750 industry and innovation actors from mining to recycling have come together under the EBA to help build a strong and competitive European battery industry. Chinese and other Asian companies are already investing in the EU because the opportunities for collaboration are highly attractive from a business standpoint. In January 2021, for instance, the European Commission approved €2.9 billion in public support from 12 member states (Austria, Belgium, Croatia, Finland, France, Germany, Greece, Italy, Poland, Slovakia, Spain and Sweden) to fund research and innovation in the battery value chain, as part of a new project, European Battery Innovation (EuBatIn). The Commission’s expectation is that the project will attract a further €9 billion in private investment. In other words, numerous member states now have a real stake in the success of this transition.

The EU followed a similar logic in launching the European Raw Materials Alliance (ERMA) in the fall of 2020 (ERMA Citation2022). With the input of a vast network of partners from 600 organisations across 50 countries, ERMA – the world’s largest raw materials consortium – is designed to support a multi-sourcing strategy for rare earths, ensure resilient and transparent supply chains and increase the EU’s industrial competitiveness (ERMA Citation2021). ERMA’s first goal is to focus on the most pressing need: increasing EU resilience in the rare earth magnet and motor value chain. The reason for this is that 95 percent of electric vehicles use traction motors containing rare earth magnets. Over 100,000 tons of rare earth permanent magnets are used annually in renewable energy, machine tools, robotics, loudspeakers, water pumps, the mobility sector and information and communication technologies (ICT). China ships 16,000 tons of rare earth permanent magnets to the EU each year, representing approximately 98 percent of the EU’s supply (Gauß et al. Citation2021). These figures highlight the EU’s potential vulnerability and existing dependence on the PRC, but a low-carbon future will in any case be extremely mineral intensive.

ERMA prioritises securing uninterrupted access to rare earth elements that are indispensable to magnet production, particularly neodymium, praseodymium, dysprosium and terbium. These four rare earths constitute only 25 percent of the total volume of global rare earth production but represent 80 to 90 percent of the total market value of rare earths. The EU’s need to secure its rare earth supply is among the most pressing. A significant alternative supply at the time of writing came from Russia, but the political red lines drawn by the war indicate that the EU cannot strategically or realistically end its dependence on Chinese rare earths. It can, however, strengthen efforts for diversification. Moreover, clean energy technologies need more materials than fossil-fuel-based electricity generation technologies. For instance, according to a 2020 World Bank report (Hund et al. Citation2020), the production of lithium and cobalt may need to increase by 1000 percent by 2030 to meet clean energy demand alone (see ).

Table 1. Demand growth for selected critical materials used for clean energy technologies.

In its 2021 World Economic Outlook, the IMF projected that in the “Net Zero by 2050” emissions scenario, “booming demand for the four energy transition metals alone [that is, nickel, copper, cobalt, lithium] would boost their production value sixfold to $12.9 trillion over two decades. This could rival the roughly estimated value of oil production in a net-zero scenario over that period” (Boer et al. Citation2021).

In the case of global electricity generation, for instance, the share of renewables jumped to nearly 30 percent in 2021, according to the IEA (Citation2021). Post-Covid, renewables are expected to have provided more than half of the increase in global electricity supply in 2021, while solar photovoltaics (PV) and wind are expected to have contributed two-thirds of the growth in renewables during the same period. Wind is on track to record the largest increase in renewable generation, growing by 275 TWh, or around 17 percent compared to 2020, while solar PV electricity generation is expected to have risen by 145 TWh or almost 18 percent and to have approached 1,000 TWh in 2021 (IEA Citation2021). The PRC is expected to account for over 50 percent of renewable electricity generation estimated at over 900 TWh from solar PV and wind in 2021. The EU, however, is also poised to have generated around 580 TWh, followed closely by the US with 550 TWh (IEA Citation2021).

In 2021, global electric car sales (included both fully electric and plug-in hybrids) reached nearly 10 percent of all cars sold, setting a record of 6.6 million (IEA Citation2022) and major global car manufacturers have committed to electrify transport. Despite supply chain disruptions, sales of electric vehicles have continued to grow steeply in 2022. China and the EU are leading electric vehicle and plug-in registrations, followed by the US. The market for fast electric recharging stations is growing correspondingly. The European Parliament voted to ban the sale of diesel and gasoline cars in the EU from 2035, mandating that automobile companies must cut their emissions by 100 percent by that year. Though the automotive industry has pushed back against such a tight deadline, the vote underscores the EU’s resolve to electrify transportation (Tidey Citation2022).

Lithium and possibly cobalt are indispensable inputs for the electrification of transport. Production of lithium has almost quadrupled between 2015 and 2021 to keep up with the manufacture of lithium-ion batteries used in electric and hybrid vehicles, as well as electric tools, grid storage applications and portable electronic devices. Indeed, demand may exceed supply in 2022 and producers are therefore ramping-up production. Lithium prices have also jumped significantly: spot prices for lithium carbonate in the PRC have climbed 170 percent in 2021, to RMB142,000 ($22,000) per ton, their highest since April 2018. In June 2022 the price reached $60,000 per ton. Prices of spodumene, a source of lithium mainly mined in Australia, have climbed 144% in 2022, to $990 per ton and $5,250 per ton in June 2022 (Argus Citation2022; SMM Citation2022).

Cobalt is a key ingredient in the highest-performance batteries, smartphones, laptops and electric cars. Sixty percent of the world’s mine production originates in the Democratic Republic of Congo that boasts by far the largest reserves of cobalt in the world, estimated at three times those found in Australia. The price for cobalt has also increased due to demand: in September 2022 it reached $80 per kilo (Argus Citation2022).

Inevitably, questions surrounding the adequate and unhindered supply of critical minerals have become a principal concern. The supply problem, however, has several distinct aspects: the rate at which mining and processing can expand, the absolute availability of reserves and resources, and the geographical and geopolitical risks related to supply (Gielen Citation2021).

To address these challenges, the EU’s objectives are: to secure access to sustainably produced magnets that contain rare earths at competitive prices from primary and recycled sources; to make the EU a global leader in the production of rare earth metals, alloys and magnets; and to sustain and expand the EU’s global leadership in electric motor and generator design. The Russian invasion of Ukraine drove the point home and underscored the importance of diversification to build resilience. In the case of rare earths, for example, the only industrial-scale commercially-operating separation facility in Europe – based in Estonia owned by Neo Performance Materials – is 70 percent dependent on Russian feedstock. Before the war Russian feedstock constituted 100 percent of the supply. The 30 percent balance was achieved from a unique supply chain arrangement between the US-based Uranium company Energy Fuels and Neo Performance Materials, that utilised by-product chemistry and a sound economic plan to make a viable business case for this deal (Neo Performance Materials Citation2021). In an effort to further diversify away from Russia, Neo Performance Materials bought a rare earth mining project in Greenland owned by Hudson Resources (Reuters Citation2022) and was awarded, in November 2022, €18.7 million from the EU Just Transition Fund to launch a magnet plant in Estonia. This was a key development for the EU given that more than 90 percent of rare earth magnets are still produced in China (Gauß et al. Citation2021).

In June 2021, the Canada-EU Strategic Partnership on Raw Materials was announced, focusing on the Integration of Canada-EU raw material value chains, science, technology and innovation collaboration; and efforts to advance world-class environmental, social and governance criteria and standards. These efforts are meant to encourage private and public investment between the two parties and build up resilient raw material and downstream value chains. The EU and Canada also intend their partnership to strengthen alignment in strategic downstream industries, particularly batteries, clean technologies and other advanced manufacturing sectors.

The challenge of effective multilateral collaboration

Each major industrial nation is currently engaged in a flurry of activity both to secure uninterrupted access to critical minerals and to diversify and strengthen the resilience of its supply chains away from the PRC. This is producing a landscape of fragmented, cumbersome and more expensive alternatives. Importantly, these uncoordinated responses are out of sync with the pressing 2030 deadline by which countries need to deepen and expand decarbonisation plans globally. Moreover, some of the strategies deployed thus far further exacerbate geopolitical tensions by securitising the decarbonisation drive. Some industrial countries are working within geopolitical alliances that overtly exclude the PRC, while also reflecting a logic that largely overlooks the aspirations and needs of the developing world. A globally recognised institution is needed to coordinate the decarbonisation race, which currently looks more like a scramble than an inclusive strategy towards a green global economy. The EU, as an influential actor with both convening and regulatory power and ties to developing and developed countries, is well placed to identify the most appropriate institution and to make a case for coordinated efforts to decarbonise the world economy.

The time is ripe for such an endeavour. Progress thus far has been difficult and has not achieved the kind of strategic multilateral cooperation on critical minerals and their supply chains that the world needs. The numerous initiatives currently underway have kept major powers preoccupied with their siloed strategies. For instance, the G7 and the G20 have both – in separate initiatives – turned their attention to critical minerals and their supply chains. The Organization for Economic Co-operation and Development (OECD) has also delivered useful guidance to businesses on how to respect human rights and avoid contributing to conflict when sourcing their mineral inputs (OECD Citation2022). Securitising initiatives have also been playing out, with a reinvigorated Quadrilateral Security Dialogue (QUAD), comprised of Australia, India, Japan and the US, turning its attention to protecting supply chains in the Indo-Pacific region. The Five Eyes – the long-standing intelligence-sharing alliance of the US, the UK, Canada, Australia and New Zealand – is said to be considering an expansion of its mission to include strategic collaboration on the development of non-Chinese supply chains for critical minerals and their applications. Moreover, since the 2010 rare earth crisis during which the PRC “unofficially” curtailed exports of rare earths to Japan during a geopolitical dispute, a trilateral cooperation forum between the US, the EU and Japan (expanded to include Australia and Canada) was organised to find ways to reduce reliance on rare earths by substituting, recycling and innovating a way out of high demand for the materials. This collaboration will certainly deepen and expand in the coming years as participants work on both technical and policy formulations to address the growing mineral intensity of the decarbonisation drive. Critical minerals strategy discussions are also being held by the National Technology and Industrial Base (NTIB) group, which focuses on issues of national security and dual-use research and development as they pertain to Australia, Canada, the UK and the US. Supply chains have quickly become a central issue in that forum.

These strategic responses reflect the extent of the securitisation and fragmentation of the decarbonisation drive and can further fuel geopolitical upheaval. Importantly, the solutions and approaches being developed are not in line with the global consensus that the response to the climate crisis should produce equitable and inclusive solutions. The UN Sustainable Development Goals, ESG standards and the fervent COP 26 and COP 27 declarations all emphasise that the mining of critical minerals for decarbonisation must adhere to a binding commitment to source them responsibly.

In the quest to identify which institution might be best suited to spearheading a multilateral response, some suggest the International Energy Agency (IEA) should take the lead. It has a long track record in helping nations maintain reserves of fossil fuels to avoid an energy crunch, produces valuable reports on major developments in the energy sector and thus may be suitable to coordinate strategies for access to critical minerals and their supply chains. However, the IEA is exclusively an organisation of OECD member states and excludes non-OECD countries. There is an alternative candidate, however: an intergovernmental organisation established in 2009 with a vibrant membership located at the crossroads of East and West, whose mission is dedicated to the energy transition. Headquartered in Abu Dhabi, where COP 28 will take place in 2023, the International Renewable Energy Agency (IRENA) boasts a membership of 167 countries. IRENA constitutes a centre of excellence for knowledge and innovation, a global voice for renewables, a network hub and a source of advice and support for member states. IRENA has produced high-level reporting on technology choices, investment needs, policy frameworks and the socio-economic impacts of achieving a sustainable, resilient and inclusive energy future.

For the EU, which plays an active role in IRENA, championing IRENA's institutional suitability would complement its own distinctive strategy to build resilience and formulate new and diversified networks of interdependence across the critical minerals supply chains. This would be in line with the EU’s Global Gateway Initiative, with a projected budget of €300 billion, that is designed as a template for how Europe can build more resilient connections with the rest of the world. It could also enable the EU to mobilise its partnership with the African Union and reinvigorate the trilateral dialogue with the PRC and its African partners. Finding resources and a suitable institutional home for efforts to offset, or at the very least temper, the narratives of the PRC as the existential threat in everything from politics and governance systems to economic might and defence capabilities, is in line with the EU’s pursuit of climate and ecological diplomacy.

Admittedly, Sino-American hyper-competition and Beijing’s greater assertiveness in world affairs have produced scepticism and push-back against Xi Jinping’s China, particularly in some member states. Nonetheless, the EU continues to seek pathways to re-engage instead of dramatically and emphatically decoupling from the PRC. The long history of climate engagement between the two parties (Kalantzakos Citation2017) offers a solid base for the EU and the PRC to work together to avoid sacrificing global decarbonisation and digitalisation initiatives on the altar of geopolitical competition and nationalistic narratives. More importantly, the EU has a long-standing strategic partnership with the PRC that has produced concrete collaboration and projects to decarbonise their respective economies, protect biodiversity, construct carbon markets and coordinate and facilitate the taxonomy for green finance. Deepening engagement can be realised through markets and trade, the BRI and working with initiatives such as the Forum on China-Africa Cooperation (FOCAC), the African Union and the post-Cotonou negotiations around a new EU/Africa-Caribbean-Pacific partnership agreement. This type of collaboration is particularly important in light of the IEA’s Citation2021 report, according to which “almost 70% of the projected increase in global energy demand is in emerging markets and developing economies, where demand is set to rise to 3.4% above 2019 levels” (IEA Citation2021, 2).

Given that critical minerals and their supply chains have graduated from the realm of trade dispute to geopolitical arm wrestling, IRENA may find it difficult to navigate the power politics of decarbonisation and digitalisation. This is why having the EU as its champion would bolster its credentials and the likelihood that it might fit the bill. IRENA already has the convening power and the mandate to help formulate best-practices with respect to Renewable Energy Systems (RES) and electrification. Given global tensions and the skyrocketing demand for critical materials, IRENA could convene members from more fragmented fora to strategise more centrally and transparently about best practices to avoid a scramble for materials and supply-chain bottlenecks moving forward.

Key areas that could help build trust and multilateral cooperation include the detailed mapping of established mines for rare earths and other critical materials and their expansion capacity, the names of mining companies and the consortia operating them, as well as accurate assessments of the economics of new exploration. IRENA could also help to design strategies on how to build alternative but inclusive supply chains that are not dominated by geopolitical imperatives. It could also encourage and support the agency of developing nations where many of the mines are located, so that they are able to both share and protect their strategic reserves. Digitisation of supply chains, data analysis and Artificial Intelligence (AI) also offer opportunities to better analyse markets and identify vulnerabilities as well as opportunities. Finally, it could work on a protocol on material supply security for green technology, perhaps drawing on the example of ERMA (Ali et al. Citation2022). These cooperative strategies would enrich the roster of other policy tools, such as stockpiling – although this practice drives up prices and demand in the short term and creates market volatility in the medium term – and market transparency for the materials themselves.

Conclusion

The world is clearly at an inflection point. As interdependence becomes thought of as a liability rather than an asset, decoupling, renationalisation and reshoring narratives are being offered as paths forward given the level of geopolitical contention. This need not become an inevitable outcome for the global order. Moreover, it must not, because breaking ties of interdependence jeopardises the urgently needed decarbonisation and digitalisation transition that constitutes an important part of our response to the climate emergency. There is only a very narrow window to construct new sustainable infrastructure and to deploy green technology and this is quickly closing.

At the moment, the EU offers a distinct and concrete blueprint that steadfastly promotes the development of the global economy without capitulating to a realist bipolar logic of division, even while some member states have become more openly and vocally critical of China. The EU has the record, temperament, regulatory and economic power, and standard-bearing expertise that make it an ideal candidate to facilitate constructive negotiations on the greening of the global economy that will also help protect and restore biodiversity, strengthen global governance and ESG standards, and help ensure that the green transition is inclusive and equitable for the developing world. Moreover, the EU can constructively engage with the PRC at a time when even its climate collaboration with the US, severed in August 2022 and restarted in November 2022, remains on shaky ground while also ensuring that the Transatlantic Alliance remains a key driver and benchmark for climate leadership. While building resilience and defending its norms and values, the EU is resolved to achieve the goals of its Green Deal and work with its partners, through multilateral fora that include the developing world, in an effort to ensure that this new industrial transition does not become the starting pistol for geopolitically engineered supply chains and a scramble for resources.

Acknowledgments

This article was funded as part of the School of Civic Education (SCE) project supported by the Ministry of Foreign Affairs of Norway and carried out by the Norwegian Institute of International Affairs. Sophia Kalantzakos would like to thank New York University Abu Dhabi for generously supporting her research.

Additional information

Notes on contributors

Sophia Kalantzakos

Sophia Kalantzakos is Global Distinguished Professor in Environmental Studies and Public Policy at New York University Abu Dhabi, Abu Dhabi, the United Arab Emirates (UAE).

Indra Overland

Indra Overland is Research Professor at the Norwegian Institute of International Affairs (NUPI), Oslo, Norway. Email: [email protected]; Twitter: @IndraOverland

Roman Vakulchuk

Roman Vakulchuk is Senior Researcher at the Norwegian Institute of International Affairs (NUPI), Oslo, Norway. Email: [email protected]; Twitter: @RVakulchuk

References

- Ali, Saleem H., et. al. 2022. Closing the Infrastructure Gap for Decarbonization: The Case for an Integrated Mineral Supply Agreement. Environmental Science & Technology 56: 15280-9.

- Abnett, Kate. 2022. EU Rolls Out Plan to Cut Russia Gas Dependency This Year. Reuters, 8 March. https://www.reuters.com/business/energy/eu-rolls-out-plan-cut-russia-gas-dependency-this-year-end-it-within-decade-2022-03-08/.

- Anastasio, Mauro. 2021. One Year of the EÙs Circular Economy Action Plan. 11 March. https://eeb.org/one-year-of-the-eus-circular-economy-action-plan/.

- Argus. 2022. Argus Metals International: Global Non-Ferrous Market Prices. News and Analysis Issue 22-107. 8 June.

- Baek, Byung-yeul. 2022. Gov’t, Businesses Team up to Address US CHIPS Act. The Korea Times, 25 August. https://www.koreatimes.co.kr/www/tech/2022/09/419_335024.html.

- Badré, Bertrand, and Tiberghien, Yves. 2022. Navigating a World in Shock. Project Syndicate, 20 September. https://www.project-syndicate.org/commentary/global-governance-after-geopolitical-economic-climate-breakdown-by-bertrand-badre-and-yves-tiberghien-1-2022-09.

- Boer, Lukas, Pescatori, Andrea, Stuermer, Martin, and Valckx, Nico. 2021. Soaring Metal Prices May Delay Energy Transition. IMF Blog. 10 November. https://blogs.imf.org/2021/11/10/soaring-metal-prices-may-delay-energy-transition/.

- Brooks, Rosa. 2017. How Everything Became War and the Military Became Everything: Tales from the Pentagon. New York: Simon & Schuster.

- Clinton, Hilary. 2011. America’s Pacific Century. Remarks by Secretary of State to East-West Center, Honolulu, 10 November. https://2009-2017.state.gov/secretary/20092013clinton/rm/2011/11/176999.htm.

- Consilium. 2022. “Versailles Declaration”. Informal Meeting of EU Heads of State or Government, 1 March. https://www.consilium.europa.eu/media/54773/20220311-versailles-declaration-en.pdf.

- Deutsche Welle. 2022. US House Passes Key $430 Billion Inflation Package. 12 August. https://www.dw.com/en/us-house-passes-key-430-billion-inflation-package/a-62795785.

- EEAS (European External Action Service). 2019. The European Union’s Global Strategy: Three Years Looking On, Looking Forward. https://www.eeas.europa.eu/sites/default/files/eu_global_strategy_2019.pdf.

- EEAS. 2022. EU@UNGA77: Multilateralism at Work in Times of Trisis. 18 September. https://www.eeas.europa.eu/eeas/euunga77-multilateralism-work-times-crisis_en.

- ERMA (European Raw Materials Alliance). 2021. ERMA Celebrates its First Anniversary Working Towards a More Resilient and Greener Europe. 23 November. https://erma.eu/erma-celebrates-its-first-anniversary-working-towards-a-more-resilient-and-greener-europe/.

- ERMA. 2022. EU Policy. Accessed 19 December 2022. https://erma.eu/eu-policy/.

- European Commission. 2018. Climate Action: China. Last update 16 July 2018. https://ec.europa.eu/clima/eu-action/international-action-climate-change/cooperation-non-eu-countries-regions/china_en.

- European Commission. 2020. Critical Raw Materials Resilience: Charting a Path towards Greater Security and Sustainability. 3 September. https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:52020DC0474&from=EN.

- European Commission. 2021. Global Gateway: Opening Remarks by President von Der Leyen. European Commission. 1 December. https://www.youtube.com/watch?app=desktop&v=CaVSPgYpJUY.

- European Commission. 2022a. “REPowerEU,” European Commission. Accessed 10 June 2022, https://ec.europa.eu/commission/presscorner/detail/en/IP_22_3131.

- European Commission. 2022b. A European Green Deal. Accessed 25 June 2022. https://ec.europa.eu/info/strategy/priorities-2019-2024/european-green-deal_en.

- European Commission. 2022c. European Commission, International Partnerships: China. Accessed 31 March 2022. https://ec.europa.eu/international-partnerships/where-we-work/china_en.

- European Commission. 2022d. EU Strategy on Energy System Integration. Accessed 24 April 2022. https://energy.ec.europa.eu/topics/energy-system-integration/eu-strategy-energy-system-integration_en.

- European Commission. 2022e. EU Taxonomy for Sustainable Activities. Accessed 28 February 2022. https://ec.europa.eu/info/business-economy-euro/banking-and-finance/sustainable-finance/eu-taxonomy-sustainable-activities_en.

- European Council. 2022. EU-China Summit: Restoring Peace and Stability in Ukraine Is a Shared Responsibility. 1 April. https://www.consilium.europa.eu/en/press/press-releases/2022/04/01/eu-china-summit-restoring-peace-and-stability-in-ukraine-is-a-shared-responsibility/.

- Farrell, Henry, and Abraham L. Newman. 2019. Weaponized Interdependence: How Global Economic Networks Shape State Coercion. International Security 44 (1): 42–79.

- Feder, Toni. 2019. Trade Wars and Other Geopolitical Tensions Strain US–China Scientific Collaborations. Physics Today 72 (11): 22.

- Federal Register. 2020. Addressing the Threat to the Domestic Supply Chain from Reliance on Critical Minerals from Foreign Adversaries and Supporting the Domestic Mining and Processing Industries, 5 October. https://www.federalregister.gov/documents/2020/10/05/2020-22064/addressing-the-threat-to-the-domestic-supply-chain-from-reliance-on-critical-minerals-from-foreign.

- Flournoy, Michele, and Janine, Davidson. 2012. Obamàs New Global Posture: The Logic of U.S. Foreign Deployment. Foreign Affairs 91 (4): 54-63.

- Gauß, Roland, et al. 2021. Rare Earth Magnets and Motors: A European Call for Action. A Report by the Rare Earth Magnets and Motors Cluster of the European Raw Materials Alliance. Berlin. https://erma.eu/app/uploads/2021/09/01227816.pdf.

- Gielen, Dolf. May 2021. Critical Materials for the Energy Transition. Abu Dhabi, United Arab Emirates: IRENA. https://www.irena.org/-/media/Files/IRENA/Agency/Technical-Papers/IRENA_Critical_Materials_2021.pdf

- Goldberg, Jeffrey. 2016. The Obama Doctrine. The Atlantic, April. https://www.theatlantic.com/magazine/archive/2016/04/the-obama-doctrine/471525/.

- Harvey, Fiona. 2022. EU Reversal of Stance on Loss and Damage Turns Tables on China at Cop27. The Guardian, 18 November. https://www.theguardian.com/environment/2022/nov/18/eu-reversal-stance-loss-damage-china-cop27

- Hilman, Jennifer. 2021. The Transatlantic Relationship Could Make or Break Biden’s Summit for Democracy. Council on Foreign Relations, 1 December. https://www.cfr.org/in-brief/transatlantic-relationship-could-make-or-break-bidens-summit-democracy

- Hirschman, Albert O. 1945. National Power and the Structure of Foreign Trade. Berkeley (CA): University of California Press.

- Hund, Kirsten, La Porta, Daniele, Fabregas, Thao P., Laing, Tim, and Drexhage, John. 2020. Minerals for Climate Action: The Mineral Intensity of the Clean Energy Transition. International Bank for Reconstruction and Development/The World Bank. http://pubdocs.worldbank.org/en/961711588875536384/Minerals-for-Climate-Action-The-Mineral-Intensity-of-the-Clean-Energy-Transition.pdf.

- IEA (International Energy Agency). 2021. Global Energy Review 2021. April. https://www.iea.org/reports/global-energy-review-2021.

- IEA. 2022. Global Electric Car Sales Have Continued Their Strong Growth in 2022 after Breaking Records Last Year - News. 23 May. https://www.iea.org/news/global-electric-car-sales-have-continued-their-strong-growth-in-2022-after-breaking-records-last-year.

- Jolly, Jasper. 2022. Volkswagen Settles Initial ‘Dieselgate’ Claims with £193 m Payout. The Guardian, 25 May. https://www.theguardian.com/business/2022/may/25/volkswagen-settles-uk-dieselgate-claims-with-193m-payout.

- Kagan, Robert. 2003. Of Paradise and Power: America and Europe in the New World Order. New York: Random House.

- Kalantzakos, Sophia. 2017. EU, US and China Tackling Climate Change: Policies and Alliances for the Anthropocene. Abingdon: Routledge.

- Kalantzakos, Sophia. 2021a. China and the Geopolitics of Rare Earths. New York: Oxford University Press.

- Kalantzakos, Sophia. 2021b. Ecological Diplomacy and EU International Partnerships: China, Africa, and Beyond. In Olivia Lazard, and Richard Youngs, eds. The EU and Climate Security: Toward Ecological Diplomacy. Carnegie Europe. https://carnegieeurope.eu/2021/07/12/ecological-diplomacy-and-eu-international-partnerships-china-africa-and-beyond-pub-84878

- Korea Joongang Daily. 2022. United Front with EU and Japan against U.S. EV Law Gains Stream. 25 August. https://koreajoongangdaily.joins.com/2022/08/25/business/industry/korea-IRA-us/20220825182304277.html.

- Li, Selena, and Yu, Robin. 2021. China Reveals Co-operation with EU on Green Investment Standards. Financial Times, 7 April. https://www.ft.com/content/cddd464f-9a37-41a0-8f35-62d98fa0cca0.

- Li, Yifei, and Shapiro, Judith. 2020. China Goes Green: Coercive Environmentalism for a Troubled Planet. Cambridge: Polity Press.

- Liboreiro, Jorge, and Scadura, Pedro. 2022. Ukraine War: EU Urges China to Stay Neutral but without Securing any Guarantees. Euronews, 1 April. https://www.euronews.com/my-europe/2022/04/01/ukraine-war-eu-urges-china-to-stay-neutral-but-without-securing-any-guarantees

- Lucarelli, Sonia, and Manners, Ian. 2006. Values and Principles in European Union Foreign Policy. London: Routledge.

- Ministry of Foreign Affairs of the People’s Republic of China. 2022. Wang Yi Expounds China’s Five-Point Position on the Current Ukraine Issue. Accessed 13 June 2022. https://www.fmprc.gov.cn/eng/zxxx_662805/202202/t20220226_10645855.html.

- Mission of the People's Republic in the European Union. 2020. China-EU Green Cooperation Has Huge Potential and a Promising Future. 18 November. http://eu.china-mission.gov.cn/eng/mh/202011/t20201120_8203690.htm.

- Nahm, Jonas. 2021. Collaborative Advantage: Forging Green Industries in the New Global Economy. New York: Oxford University Press.

- Neo Performance Materials. 2021. Energy Fuels and Neo Performance Materials Rare Earth Shipments. Neo Performance Materials, 7 July. https://www.neomaterials.com/energy-fuels-and-neo-performance-materials-contract/.

- Obama, Barack. 2011. Remarks by President Obama to the Australian Parliament. Canberra, 11 November. https://obamawhitehouse.archives.gov/the-press-office/2011/11/17/remarks-president-obama-australian-parliament.

- OECD (Organisation for Economic Co-operation and Development). 2022. Due Diligence Guidance for Responsible Supply Chains of Minerals from Conflict-Affected and High-Risk Areas – OECD. Accessed 13 June 2022. https://www.oecd.org/corporate/mne/mining.htm.

- Reuters. 2019. Australia, U.S., to Cooperate on Critical Minerals, Rare Earths. 20 November. https://www.reuters.com/article/us-australia-rare-earths-usa-idUSKBN1XU0NU.

- Reuters. 2022. Neo Agrees to Buy Greenland Rare Earth Project from Hudson Resources. 22 August. https://www.reuters.com/markets/commodities/neo-agrees-buy-greenland-rare-earth-project-hudson-resources-2022-08-22/.

- Ridgwell, Henry. 2021. EU Suspends China Trade Deal as Tensions Grow Over Xinjiang, Hong Kong. Voice of America, 10 May. https://www.voanews.com/a/east-asia-pacific_voa-news-china_eu-suspends-china-trade-deal-tensions-grow-over-xinjiang-hong-kong/6205673.html.

- Scheyder, Ernest. 2022. Exclusive U.S. Bill Would Block Defense Contractors from Using Chinese Rare Earths. Reuters, 14 January. https://www.reuters.com/business/energy/exclusive-us-bill-would-block-defense-contractors-using-chinese-rare-earths-2022-01-14/.

- Scott, David. 2007. China and the EU: A Strategic Axis for the Twenty-First Century? International Relations 21 (1): 23-45.

- SMM. 2022. Average Price of Spodumene Concentrates Broke Through $5,000/mt, and Battery-grade Lithium Carbonate Prices Gained Another 1,500 yuan/mt. 8 August. https://news.metal.com/newscontent/101913013/average-price-of-spodumene-concentrates-broke-through-5000mt-and-battery-grade-lithium-carbonate-prices-gained-another-1500-yuanmt/.

- Sonmez, Felicia. 2021. Biden Signs Uyghur Forced Labor Prevention Act into Law. The Washington Post, 23 December. https://www.washingtonpost.com/politics/biden-uyghur-labor-law/2021/12/23/99e8d048-6412-11ec-a7e8-3a8455b71fad_story.html.

- Sutter, Robert. 2020. China’s Relations with the United States. In David Shambaugh, ed. China and the World: 211-32. New York: Oxford University Press.

- Sverdrup-Thygeson, Bjørnar, Lanteigne, Marc, and Sverdrup, Ulf. 2016. For Every Action … The American Pivot to Asia and Fragmented European Responses, Brookings Institute, January. https://www.brookings.edu/wp-content/uploads/2016/07/The-American-pivot-to-Asia-and-fragmented-European-responses-2.pdf.

- Taipei Times. 2021. Biden Touts US as Democracy Champ, China Lashes Out. 12 December. https://www.taipeitimes.com/News/front/archives/2021/12/12/2003769444.

- Telò, Mario. 2019. European Union and New Regionalism: Europe and Globalization in Comparative Perspective: Europe and Globalization in Comparative Perspective. London: Routledge.

- The Guardian. 2015. Volkswagen Diesel Emissions: What the Carmaker Did, and Why – Video. 24 September. https://www.theguardian.com/business/video/2015/sep/24/vw-volkswagen-diesel-emissions-carmaker-why-video.

- The White House. 2021a. Executive Order on America’s Supply Chains. 24 February. https://www.whitehouse.gov/briefing-room/presidential-actions/2021/02/24/executive-order-on-americas-supply-chains/.

- The White House. 2021b. FACT SHEET: Biden-Harris Administration Announces Supply Chain Disruptions Task Force to Address Short-Term Supply Chain Discontinuities. 8 June. https://www.whitehouse.gov/briefing-room/statements-releases/2021/06/08/fact-sheet-biden-harris-administration-announces-supply-chain-disruptions-task-force-to-address-short-term-supply-chain-discontinuities/.

- Tidey, Alice. 2022. EU to Phase Out New Combustion Engines by 2035. Euronews, updated 28 October. https://www.euronews.com/my-europe/2022/10/28/eu-to-phase-out-new-combustion-engine-cars-by-2035.

- Toosi, Nahal. 2021. China and U.S. Open Alaska Meeting with Undiplomatic War of Words Politico, 19 March. https://www.politico.com/news/2021/03/18/china-us-alaska-meeting-undiplomatic-477118.

- U.S. Department of Defense. 2012. Sustaining U.S. Global Leadership: Priorities for 21st Century Defense. 5 January. https://www.globalsecurity.org/military/library/policy/dod/defense_guidance-201201.pdf.

- U.S. Department of State. 2019. Energy Resource Governance Initiative (ERGI). Bureau of Energy Resources, 6 June. https://www.state.gov/wp-content/uploads/2019/06/Energy-Resource-Governance-Initiative-ERGI-Fact-Sheet.pdf.

- Vakulchuk, Roman, and Overland, Indra 2021. Central Asia Is a Missing Link in Analyses of Critical Materials for the Global Clean Energy Transition. One Earth 4 (12): 1678–1692. https://doi.org/10.1016/j.oneear.2021.11.012.

- Vakulchuk, Roman, Overland, Indra, and Scholten, Daniel, 2020. Renewable Energy and Geopolitics: A Review. Renewable and Sustainable Energy Reviews 122: 109547. https://doi.org/10.1016/j.rser.2019.109547.

- Wei, Li. 2019. Towards Economic Decoupling? Mapping Chinese Discourse on the China–US Trade War. The Chinese Journal of International Politics 12 (4): 519–56.

- Wright, Th. J. 2017. All Measures Short of War: The Contest for the Twenty-First Century and the Future of American Power. New Haven (CT): Yale University Press.

- Youngs, Richard. 2010. The EU’s Role in World Politics: A Retreat from Liberal Internationalism. London: Taylor & Francis Group.

- Zhongping, Feng, and Jing, Huang. 2014. China's Strategic Partnership Diplomacy. ESPO Working Paper No. 8. 27 June. http://doi.org/10.2139/ssrn.2459948.