?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The Eurozone crisis has been wrongly interpreted as either a crisis of fiscal profligacy or of deteriorating unit-labor cost competitiveness (caused by rigid labor markets), or a combination of both. Based on these diagnoses, crisis countries have been treated with the bitter medicines of fiscal austerity, wage reductions, and labor market deregulation—all in the expectation that these would restore cost competitiveness and revive growth (through exports), while at the same time allowing for fiscal consolidation and private debt deleveraging. The medicines did not work and almost killed the patients. The problem lies with the diagnoses: the real cause of the crisis resides in unsustainable private sector debt leverage, which was aided and abetted by the liberalization of European financial markets and a “global banking glut.”

THE NEVER-ENDING CRISIS OF THE EUROZONE

The Eurozone entered a recession in the first quarter of 2008, and quarterly growth rates collapsed in the first quarter of 2009, when the financial crisis hit Europe full-force. The combined real gross domestic product (GDP) (2008Q1 = 100) of the eighteen Eurozone countries fell by a cumulative 5.8 percentage points over six successive quarters (2009Q2 = 94.2), then crept up to 98.1 during 2011Q1–2011Q3, but next declined for seven consecutive quarters (to 96.8 in 2013Q2) to finally climb up again to 98.1 in 2014Q4. Eurozone GDP, in other words, is still not back to its precrisis level after six whole years. A few countries, most notably Germany, have been able to recover from the crisis-induced GDP contraction—but their recovery is far from imposing (Storm and Naastepad Citation2015b). Southern Europe’s crisis countries do not dare to think of recovery—in most cases, the freefall they were in has just about stopped. Greece’s GDP in 2014Q4 is down by 26.3 percentage points, Spain’s GDP by 5.7 percentage points, Portugal’s by 6.8 percentage points, and Italy’s GDP shrank by as much as 9.6 percentage points (all compared to 2008Q1).

Inevitably, unemployment has shot up and as many as 19 million workers are jobless in the Eurozone as a whole (in 2013)—7 million more unemployed people than in 2008. The average Eurozone unemployment rate is now 12 percent, but the employment crisis is far deeper in Southern Europe. Greece, Italy, Portugal, and Spain (the data are for 2013) count an unprecedented 11.3 million unemployed workers—6.3 million more than during 2008. The unemployment rate (in 2013) is 27.5 percent in Greece, 12.2 percent in Italy, 26.1 percent in Spain, and 16.4 percent in Portugal. Such a degree of joblessness has not happened since the 1930s. Poverty is on the rise: income poverty rates have increased during 2008–11 by 4.4, 2.4, and 5.1 percentage points in Greece, Italy, and Spain, respectively. Inequality in these countries is rising: the lowest income deciles cope with much larger declines in their disposable incomes than the top 10 percent, and the income ratio of the top 10 percent to the bottom 10 percent has gone up. The result is an even more polarized society, turning the Southern Eurozone into a depressing world of closing of possibilities, hopes, and dreams, high unemployment, pay cuts, rising in-work poverty, and people going hungry, hunting for food through garbage cans—as there is no (longer a) welfare state to fall back on (Storm and Naastepad Citation2015a: Table 1).

Eurozone recovery is widely expected to be slow: according to the International Monetary Fund (IMF) World Economic Outlook (Citation2015a), Eurozone growth will be 1.2 percent in 2015 and 1.4 percent in 2016, while a more optimistic European Commission (2015) expects the euro area to grow by 1.3 percent in 2015 and 1.9 percent in 2016. The point is not that growth forecasts for Greece and Spain are higher than the Eurozone average, while they are lower for France, Italy, and Portugal, but that the recovery process is tardy and fragile. Even if Greek GDP grew by as much 3 percent in 2015, it is starting from a base level that is 26.3 percent lower than it was in 2008, and in the happy circumstances that this 3 percent growth were to continue, it will be 2026 before Greece’s GDP is back at its precrisis level: eighteen lost years. For Italy, Portugal, and Spain, it will also take many years for their GDP to make up the loss caused by the crisis. But it is not clear what would drive such growth: the fiscal policy stance is contractionary, households and firms (almost everywhere) suffer from hefty debt overhangs, and external demand remains weak (mostly because each member country is cutting spending and wages). In line with this, forecasts of unemployment show that joblessness remains rampant—the expected unemployment rate for 2016 is divined to be 22 percent of the labor force in Greece, 20.7 percent in Spain, and 12.6 percent in Italy and Portugal (European Commission 2015). Those who believe the Eurozone’s trials are now past must assume either an extraordinary acceleration of the recovery process or a willingness of those trapped in deep recessions to just soldier on. Neither scenario seems plausible.

We argue that this never-ending crisis of the Eurozone is in no small measure caused by a mishandling of the crisis, based on wrong diagnoses. We distinguish two dominant narratives about the Eurozone crisis, the first one emphasizing fiscal profligacy as the ultimate cause of the crisis, the other focused on (cost) competitiveness. In the first narrative the crisis is seen as a sovereign debt crisis, in the second, it is viewed as a competitiveness crisis. Both narratives monopolize Eurozone policy discussions. But, as Tolstoy (1882/1987: 158) wrote in A Confession, “wrong does not cease to be wrong, because the majority share in it”—and this holds true in this case as well: both diagnoses are inaccurate and wrong, and these diagnostic errors lead to the wrong treatment in terms of policy prescriptions. The economic—and social as well as political—costs of this mishandling are huge, and—sadly—largely avoidable. It is no understatement to say that the patient is barely surviving the therapy. Better therapy requires an improved diagnosis, and to this task, the remainder of this article is devoted.

MYTH #1: THE EUROZONE CRISIS IS DUE TO FISCAL PROFLIGACY AND IS A SOVEREIGN DEBT CRISIS RIGHT FROM THE START

This first myth holds that the Eurozone crisis was driven by fiscal indiscipline, even profligacy in Southern Europe—where national debts supposedly had soared already before the crisis. “It is an indisputable fact,” wrote Wolfgang Schäuble (Citation2011), Germany’s finance minister, in the Financial Times that “excessive state spending has led to unsustainable levels of debt and deficits that now threaten our economic welfare.” Jean-Claude Trichet (Citation2010), former president of the European Central Bank (ECB), agrees: “The roots of the sovereign debt tensions we face today lie in the neglect of the rules for fiscal discipline that the founding fathers of Economic and Monetary Union laid out in the Maastricht Treaty.” Christian Noyer (Citation2012), governor of the Bank of France, repeats the point, stating: the “main origin of the crisis lies in the lack of fiscal discipline on the part of most Member States … . [These Member States] ran up deficits and debts, including during times of growth. As a result in 2008, when the crisis started, these countries had no more fiscal room and their public finances deteriorated substantially.” Sinn (Citation2010) concurs, writing that the “lesson to be learned from the crisis is that a currency union needs ironclad budget discipline to avert a boom-and-bust cycle in the first place.” Mainstream analysts (e.g., Costa and Ricciuti Citation2013; Schuknecht et al. Citation2011) share the same view.

If fiscal overspending is the problem and the Eurozone crisis is indeed a sovereign debt crisis, as this argument goes, fiscal austerity must be the solution,Footnote1 with public thrift serving to revive investor confidence. First, significant belt tightening is only “normal” after years of fiscal profligacy and rising public debts—peripheral states simply cannot continue overspending now at the expense of the future. Second, financial markets will punish countries not doing enough to slash their deficits by making it even more expensive for these cash-strapped countries to borrow. Hence, the leaders of the Eurozone’s core countries have been demanding substantial budget cuts as the price of rescue loans to Greece, Portugal, Spain, and Italy. The ECB has been cheering this on and pushing it further. Of course, it is understood that “the necessary comprehensive fiscal adjustment is weighing on near-term economic growth,” as Mario Draghi explained (at an ECB press conference on May 3, Citation2012), but “its successful implementation will contribute to the sustainability of public finances and thereby to the lowering of sovereign risk premia. In an environment of enhanced confidence in fiscal balances, private sector activity should also be fostered, supporting private investment and medium-term growth.” Draghi’s optimism is founded upon the doctrine of “expansionary fiscal austerity,” which insists that governments should slash spending even in the face of high unemployment, because the fiscal consolidation (if credible) raises households’ expected future disposable income and consumption, and increases investors’ confidence and hence investment (Alesina and Ardagna Citation2010). In line with this doctrine, Reinhart and Rogoff (Citation2010) claimed that economic growth drops off sharply, when debt exceeds 90 percent of GDP. The “austerity is good + debt is bad” doctrine received wholehearted enthusiasm in policy circles in Brussels, Frankfurt, Berlin, and Washington, also because it created hope that the crisis countries could actually help themselves without much further support of or adjustment in Europe’s North. Belief in it became so strong that Europe’s Stability and Growth Pact was reformed so as to prevent any fiscal faux pas by Eurozone states in future.

MIX-UP #1: THE CLAIM PROVED TOO GOOD TO BE TRUE

The difficulty with the “fiscal profligacy” argument is that the data do not support it. As Eurostat data in Table show, in the eight years prior to the crisis (2000–2007), government debt (percent of GDP) in the Eurozone declined, on average, by 6 percentage points. Sovereign debt of Italy declined by 7 percentage points during 2000–2007, in Ireland by 8 percentage points, and in Spain by as much as 24 percentage points. It is true that the public debt of Greece increased by 4 percentage points during those years, but to call this “profligate,” “reckless,” or “excessive” makes little sense; it would mean that the German and French states have been profligate as well, as their debts increased by as much as 5 percentage points during 2000–2007. Bond markets were not apprehensive about sovereign default risks as member-country-specific risk premiums came down to very low levels and interest rate spreads remained stable and very low until the onset of the crisis (Chen, Milesi-Ferretti, and Tressel Citation2012). The spread of the Greek bond rate over the German one, for instance, remained as low as 30 basis points even until the end of 2007. As far as financial markets were concerned, all countries using euros could borrow at the same interest rate. There is therefore no basis to claim that national debts had already soared well before the crisis—they rose sharply only after the crisis, once governments felt forced to bail out collapsing insolvent banks and once GDP started to contract. As a result, public debt in the Eurozone increased by a full 33 percentage points of GDP during 2008–12—and by 78 percentage points in Ireland, 44 percentage points in Greece, 48 percentage points in Portugal, and 45 percentage points in Spain. We do not need the help of Granger-causality testing to conclude that it is the socialization of private debts, especially the debts of banks going belly up, which turned the Eurozone crisis into a sovereign debt crisis ex post facto.

TABLE 1 Increase in Indebtedness (Percent of GDP), 2000–2007

A second point that is clearly illustrated in Table is that the Eurozone’s aggregate debt dynamics is almost completely driven by private sector indebtedness—and specifically the dramatically rising debt of financial corporations which, on average and percent of GDP for the Eurozone, increased by 132 percentage points during 2000–2007. Household (mortgage) debts increased by 21 percentage points of GDP, while the liabilities of nonfinancial corporations rose by 12 percentage points during the precrisis years. Growing private-sector debts dwarf the changes in sovereign debts—particularly so in the crisis countries. In Greece, household indebtedness rose by 32 percentage points, corporate indebtedness by 13 percentage points, and financial sector indebtedness by 41 percentage points—trivializing the 4 percentage point increase in public debt. Spain experienced a massive increase in the debts of nonfinancial corporations (of 78 percentage points during 2000–2007), of banks (of 74 percentage points) as well as households (of 34 percentage points)—all participants in Spain’s massive property bubble—in a period when sovereign indebtedness was sharply reduced. Undeniably, the Eurozone crisis was triggered by a gigantic unsustainable increase in indebtedness—but why would one single out trifling increases in sovereign debts as the main factor, while neglecting the significant growth in private indebtedness?

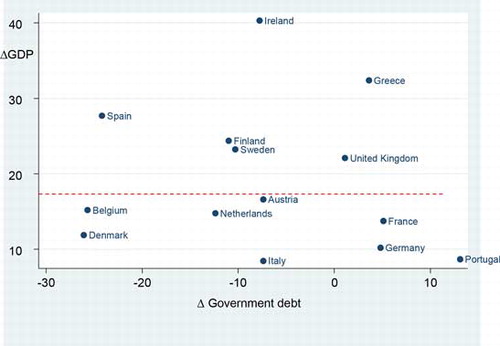

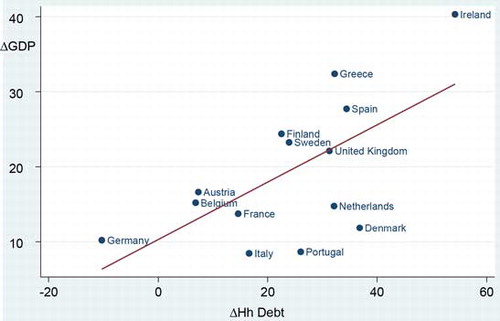

This point can be further substantiated. Using the debt data (2000–2007) for the fourteen European countries in Table , we find that there is no (statistically significant) association between higher indebtedness and economic growth, defined here as the percentage increase in real GDP over the period 2000–2007. This is illustrated in Figure . The lack of correlation is important as it means that we cannot attribute higher growth in the Eurozone periphery to excessive state spending, and hence cannot logically attribute higher real wage growth, loss of cost competitiveness, higher imports and growing current-account deficits to a supposed lack of fiscal discipline in Southern Europe (Storm and Naastepad Citation2015a). Likewise, we find no (statistically significant) correlation between economic growth and (higher) indebtedness of nonfinancial corporations, and between growth and the exploding indebtedness of financial corporations. However, we do find a statistically significant positive association between real GDP growth and household debts in the run-up (2000–2007) to the crisis (Figure ). We are aware that this correlation may be spurious (as growth and household debts may not be related but influenced by the same hidden factor) and that it does not necessarily indicate causality from household indebtedness to growth. But there are good reasons to assume that rising household debts were an important driver of growth (Chmelar Citation2013): there was an unprecedented loosening of credit constraints, an unparalleled rise in household indebtedness, and higher debt-financed spending on consumption and residential investment, which was fully in line with decisions made by the reference groups to which those household decision makers turn for guidance (Cynamon and Fazzari Citation2013). According to the regression result, a one point increase in household debt (percent of GDP) is associated with an increase in real GDP of 0.25 percentage points. (This regression result does not depend on the inclusion of Ireland, which is an outlier. The result does not change when we exclude any one country from the sample.) The increased household debt fed back into higher spending—directly by loosening households’ liquidity constraints and indirectly because the credit was used to drive up asset (home) prices and create wealth gains (Barba and Pivetti 2008)—which means that higher household debt contributed to higher aggregate demand and growth. Our estimated coefficient—of 0.25—can thus be used (with the usual caveats) to estimate the contribution of higher household debt (during 2000–2007) to real GDP growth (in the precrisis period). The proportions of economic growth “explained” by higher household indebtedness are given in Table for each country. On average, for the Eurozone, higher household debts explain about 27 percent of economic growth (Chmelar Citation2013). The proportions are much higher for Italy (48 percent), the Netherlands (53 percent), and Portugal (74 percent), but lower in the case of Greece (24 percent). Germany is the only country where households deleveraged debt (after the unification boom and the Neuer Markt information technology (IT) debacle around 2000)—and this explains sluggish domestic demand and poor growth in Germany during most of 2000–2007 (Storm and Naastepad Citation2015b).

Figure 1 The Eurozone: The Increase in Sovereign Debt Is Not Associated with Increased Real GDP (2000–2007)

Sources: See sources to Table .

Notes: Δ real GDP = the percentage increase in real GDP (2000–2007); Δ government debt = the increase in government debt as a percentage of GDP (during 2000–2007). The (dashed) horizontal line indicates that there is no statistically significant (at 10 percent or less) association between Δ government debt and Δ GDP.

Figure 2 The Eurozone: The Increase in Household Debt Is Associated with an Increase in Real GDP (2000–2007)

Sources: See sources for Table .

Notes: The regression line is based on the following ordinary least squares (OLS) regression:

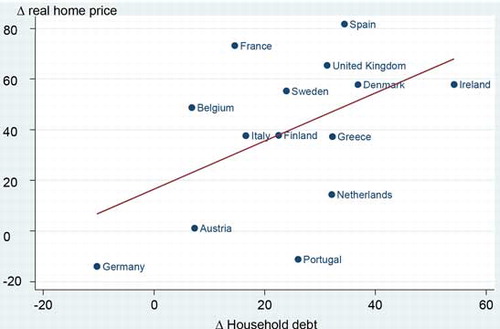

The role of household debt can be investigated in more detail, since higher household debts in the Eurozone were a major factor in driving up home prices—which, in turn, enabled households to take on more debt. Figure plots the increase in household debt (as a percentage of GDP, during 2001–7) and the increase in real home price (as given by official Organization for Economic Cooperation and Development [OECD] statistics). The correlation between household debts and house prices is positive and statistically very significant (at 0.1 percent), as indicated by the strongly upward regression line. The result does not change when we drop any country from the sample—the correlation remains very significant. If we assume that causality runs from debt to house prices and apply the estimated coefficient (1.44) to the average increase in household debt for the Eurozone as a whole (21 percentage points), we get an estimated real home price increase of 30.9 percent, which is close to the actual home price increase of 28.3 percent. In the same manner, we can almost fully “explain” the increase in real home prices in Denmark and Germany, and about 60–85 percent of the real home price increase in Finland, Italy, Spain, Sweden, and the UK. (Our regression does “overexplain” the real home price change in Austria, Ireland, the Netherlands, and Portugal). The evidence of a household-debt-funded home-price climb is strong.Footnote2

Figure 3 Higher Household Debt Is Associated with Higher Home Prices in the Eurozone

Sources: See sources for Table .

Notes: The regression line is based on the following OLS regression:

Higher (real) home prices, in turn, are associated with more rapid GDP growth—as is illustrated by Figure . The slope coefficient of the fitted regression line (which takes a value of +0.14) is statistically significant (at 5 percent) and does not change when we drop Ireland or any other country from the sample. Higher home prices, raising households’ (paper) wealth, enabled them to increase borrowing, and these loans were used for spending and further driving up asset (home) prices—the result has been an unsustainable private leverage boom, especially in Spain and Ireland (IMF 2012a; Martin and Philippon Citation2014). While our estimations (based on ordinary least squares [OLS] regression) have to be treated as indicative and evocative, they are remarkably robust and consistent. For instance, when we combine the estimated coefficients of Figures and to obtain the derived impact on real GDP growth of higher household debt, we get:

Figure 4 Higher Home Prices Are Correlated with Higher GDP Growth in the Eurozone

Sources: See sources for Table .

Notes: The regression line is based on the following OLS regression:

A 1 percentage point rise in household indebtedness led to an increase in the real home price by 1.44 percentage points, which in turn is associated with a rise in real GDP of 0.21 percentage points—which is close to our direct estimate of 0.25 percentage points in Figure . Clearly, Figures , , and paint a consistent picture: the Eurozone was blighted by private debt—not public debt (see Bornhorst and Ruiz-Arranz Citation2013; Chmelar Citation2013).

Hence, the focus on sovereign debt is badly misplaced. Eurozone households, corporations, and banks have all been taking on debts on an unprecedented scale (Table ). For the Eurozone as a whole, household debt in 2012 was equal to 79 percent of GDP, ranging from 131 percent in the Netherlands to 51 percent in crisis-struck Italy. Corporate debt in 2012 stood at 212 percent of Eurozone GDP—being comparatively low in Greece (117 percent) and Italy (182 percent), but higher elsewhere. Banks’ indebtedness in 2012 stood at 522 percent—with Ireland and the Netherlands representing cases of hyperfinancialization. Excessive bank indebtedness is typical not just of the Irish and the Dutch, however, but also of Germany and France, where the ratio of bank debt to GDP in 2012 was 401 percent and 363 percent, which is considerably higher than the ratio of bank debt to GDP of 272 percent on average for Greece, Italy, Portugal, and Spain. Faced with the need to strengthen and repair balance sheets, all sectors are now—postcrisis—deleveraging, which reduces economic activity and is causing a full-fledged balance-sheet recession, impossible to resolve by reducing sovereign debts. The real issue is how governments can help to clean up the Augean stables of households, corporations, and particularly banks. Not surprisingly, in light of the massive private-sector debt buildup, recent research, such as that of Bank for International Settlements (BIS) economists Cecchetti, Mohanty, and Zampoli (Citation2011), finds that high corporate and household debt acts as a drag on growth. IMF economists Bornhorst and Ruiz-Arranz (Citation2013) conclude for the euro area that high private debt is more detrimental to growth than high public debt.

TABLE 2 Debts (percent of GDP), 2012

MISHANDLING #1: FISCAL AUSTERITY: WRONG MEDICINE

If the crisis is due to fiscal excess, then austerity must be the remedy—at least, this is what Schäuble (Citation2011), in the same Financial Times article, claims: “The recipe is as simple as it is hard to implement in practice: Western democracies and other countries faced with high levels of debt and deficits need to cut expenditures, increase revenues and remove the structural hindrances in their economies, however politically painful.” Hence, in the hope that these would at some point become expansionary, tough austerity programs were (and still are) imposed on the crisis countries. Public spending was cut, while taxes were raised in order to reduce the fiscal deficit and public debt. By far the largest of such fiscal consolidations has taken place in Greece, 9 percent of GDP on the basis of the change in the structural balance over 2011–13. Portugal has also undertaken large consolidations, close to 7 percent of GDP, while the adjustment in Ireland amounted to 4 percent over these years. Consolidation measures in France, Italy, and Spain amounted to more than 3.7 percent, 4 percent, and 4.5 percent of GDP, respectively, while Germany also undertook large consolidation measures, despite a larger fiscal space and record low borrowing costs due to a “flight to safety.” The results were unequivocally counterproductive, as in many cases, the (synchronized) austerity packages led to a greater decline in GDP than in sovereign debt. Poul Thomsen, a leading architect of the IMF austerity program in Greece, openly admitted that it failed to work and trapped the country in a vicious cycle where austerity generates recession, followed by more austerity and deeper recession that strangles any prospects for recovery and undermines social cohesion. Thomsen’s admission reflected a larger transformation of his employer, the IMF—from a strong voice for strict austerity to a strong voice against. In its World Economic Outlook of October 2012, the IMF (Citation2012b) presents research to show that austerity harms growth (see also Guajardo, Leigh, and Pescaroti Citation2011).

This means that the belt tightening by the government was not just nonexpansionary, but more harmful than economists believed it to be—by a lot. Most economists had assumed that cutting the government deficit by 1 percentage point cuts about half a percentage point off economic output, but the actual decline according to the IMF is more like 0.9 percentage points to as much as 1.7 percentage points. The IMF estimates of the fiscal multiplier are, if anything, still on the conservative side. Eichengreen and O’Rourke (Citation2012) find that the fiscal multiplier takes a value of 1.6, while Gordon and Krenn (Citation2010) argue that the relevant multiplier value in a deep recession is 1.8. If we assume the fiscal multiplier to equal 1.8, then the fiscal consolidation of 9 percentage points of GDP undertaken by Greece must have reduced Greek GDP by more than 16 percent—which, in turn, would have raised the public debt–GDP ratio by about 24 percentage points if we assume public debt to be constant. Thus, austerity explains almost the entire collapse of Greek GDP after Citation2009 (see Gechert and Rannenberg Citation2015). Such contractionary outcomes are typical of fiscal austerity, as shown by Ball et al. (Citation2013) who looked at 173 episodes of fiscal austerity in the OECD economies over the past thirty years. Fiscal austerity, argued to be necessary to pacify investor Angst, has starved the crisis economies in which the private sector is hard struck by a debt overhang (Tables and ) of the public investment (and essential public services) that could get the system moving again. Even worse, the programs have failed to decrease governments’ debt-to-GDP ratios, often even worsening them. The “eat your peas” approach, as austerity is called, is failing big time. Notwithstanding this, fiscal stimulus remains anathema in Europe.

MYTH #2: THE EUROZONE CRISIS IS A CRISIS OF (UNIT LABOR) COST COMPETITIVENESS IN COMBINATION WITH FISCAL IRRESPONSIBILITY

The second explanation focuses on the divergence in cost competitiveness (under a common currency) between the Eurozone core and periphery. It is summarized well by Lorenzo Bini Smaghi (Citation2013) who argues that “countries which lost competitiveness prior to the crisis experienced the lowest growth after the crisis.” Competitiveness here must be read as meaning cost competitiveness—specifically nominal unit labor cost (ULC) competitiveness—as is done by Trichet (Citation2011) who defines “competitiveness, as revealed by developments in nominal unit labor costs,” or by Draghi (Citation2012), who thinks that a “useful way to measure excessive imbalances is to look at unit labor costs, as these reflect developments in both productivity and labor costs.” The Eurozone crisis, in Draghi’s view, is caused by the fact that “since the introduction of the euro, unit labor costs have increased by 28 percent in deficit countries, 2.5 times as much as in surplus countries.” Or in the opinion of Sinn (Citation2014: 3), “the countries in the southern and western periphery lost their competitiveness simply by becoming too expensive.” This loss of competitiveness is argued to have resulted, over time, in growing current account deficits, rising foreign indebtedness and reduced fiscal policy room in the Eurozone periphery, and hence, when the crisis started, these countries lacked the resilience to absorb the shock (unlike the more competitive, stronger German economy, which could cope with the fallout from the Financial Crash). The mistake made by Greece, Italy, Portugal, and Spain was—paraphrasing Benjamin Franklin—that by failing to prepare, they were preparing to fail.

The increase in nominal ULC in the Southern Eurozone meant nominal wages were growing faster than labor productivity (+the inflation target of 2 percent)—a trend argued to be caused by their “rigid” inflexible labor markets, strong unions, and strong employment protection (e.g., Dadush Citation2010; Sinn Citation2014). The peripheral economies were growing rapidly, mostly because the adoption of the single currency helped lower (real) interest rates and create a surge in (financial market) confidence in Greece, Italy, Portugal, and Spain. It was, at least up to the crisis outbreak, considered part of a healthy convergence process that Europe’s financial integration led capital to flow from the capital-abundant core (Germany) to the relatively capital-scarce countries in the periphery—driving up domestic demand, output as well as imports (Blanchard and Giavazzi Citation2002; Lane and Pels Citation2012). In this short era of “Great Expectations,” the hope was that (labor market) institutions and incomes in the periphery would converge to those of Europe’s Northern core countries. With hindsight, southern Europe’s “rigid” labor markets are now seen as the party pooper: by enabling workers to obtain higher wage growth they contributed to a process of wage-push and rising relative unit labor costs, which—in this narrative—killed Southern Europe’s export growth, raised current account deficits, and created huge external debts. According to Sinn (Citation2014: 2), “The unresolved problem underlying the financial crisis is the lack of competitiveness of the southern European countries and France. If anything, placating investors with taxpayer guarantees postpones the necessary painful adjustments through which competitiveness could be restored.” In this view, the only way out of the crisis is for the deficit countries to reduce their nominal unit labor costs (relative to the surplus countries), by drastically reducing wages (“internal devaluation”) and by a drastic deregulation of their supposedly rigid labor markets. To rebalance their current accounts, Greece, Portugal, and Spain should cut their wages by 25–35 percent, France by 15–25 percent, and Italy by 5–15 percent—according to Sinn (Citation2014). This view has become codified in policy in the Euro Plus Pact (adopted by the European Council in March 2011), the core aim of which is to foster Eurozone (unit labor cost) competitiveness and net exports via labor market deregulation and welfare state reform, in conjunction with fiscal austerity (Gabrisch and Staehr Citation2014). The latest statement by the Informal European Council (February Citation2015) merely repeats these points.

MIX-UP #2: NOMINAL UNIT LABOR COSTS ARE FAR LESS IMPORTANT TO A COUNTRY’S COMPETITIVENESS THAN IS GENERALLY BELIEVED

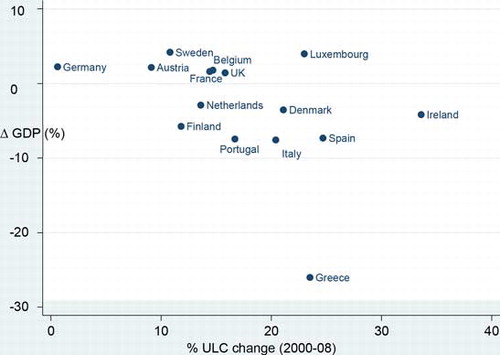

The problem with the “labor cost competitiveness” explanation is not that the data—as given in Figure —prove Bini Smaghi wrong, as there is no statistically significant correlation between precrisis increases in nominal unit labor costs (ULC) and postcrisis growth performance for Europe and the Eurozone. The problem is a much deeper one as it concerns a leap of logic, a misleading use of the term “competitiveness,” which philosophers would label equivocation, by which the—broad—concept of “competitiveness” is reduced, with remarkable sleight of hand, to competitiveness in terms of only relative nominal unit-labor costs (or RULC). This is no trivial issue, because first, it is no secret that economics lacks an agreed definition and measure of “international competitiveness” (Storm and Naastepad Citation2015a; Wyplosz Citation2013), and second, often-used competitiveness indicators, such as RULC and/or current account imbalances, are known to be weak predictors of future export and import performance (Gaulier and Vicard Citation2012; Gros Citation2011). Our own research for the Eurozone countries (Storm and Naastepad Citation2015a, Citation2015b) shows that the RULC elasticities of export and import demand of Germany, Greece, Italy, Portugal, and Spain (and the Eurozone as a whole) are mostly not statistically significantly different from zero and tiny. Instead, we (and others) find that:Footnote3

Figure 5 Postcrisis GDP Growth (2009–2013) Is Not Correlated with Precrisis Changes in Unit Labor Costs (2000–2008)

Sources: Authors’ estimations based on Eurostat Data on nominal unit labor costs (http://ec.europa.eu/eurostat/tgm/table.do?tab=table&init=1&language=en&pcode=tipslm20&plugin=1) and unemployment (http://ec.europa.eu/eurostat/tgm/table.do?tab=table&init=1&language=en&pcode=tipsun20&plugin=1).

Notes: The conclusion from the OLS regression analysis is that there is no statistically significant association between the (percentage) change in unit labor costs (2000–2008) and real GDP growth (2009–13). The results are sensitive to the outlier observations for Greece, Luxembourg, and even Italy and Spain; when we control for these “outliers” (using country dummies for the mentioned countries), the estimated coefficient of percentage of ULC change on real GDP growth is not significant (at 10 percent)

Most goods and services imported into the Eurozone are “noncompeting” imports used as intermediate inputs in manufacturing or for consumption—hence, imports depend almost completely on domestic income (Bussière et al. Citation2013).

Export performance by Eurozone members is overwhelmingly determined by world income growth (Danninger and Joutz Citation2007; European Commission Citation2009a, Citation2009b; Schröder Citation2015). Countries (such as Germany) exporting to fast-growing markets (such as China) experienced rapid export growth, whereas countries (such as Greece, Italy, and Portugal) catering to slowly growing markets had much lower export growth (ECB Citation2012).

Eurozone current account imbalances are not statistically significantly affected by changes in RULC (Diaz Sanchez and Varoudakis Citation2013; Gabrisch and Staehr Citation2014; Gaulier and Vicard Citation2012).

Nominal wage costs do not matter very much for competitiveness, in other words.Footnote4 Why this is so, is not difficult to understand (see Storm and Naastepad Citation2015a, Citation2015b for a detailed explanation). Nominal unit labor cost (ULC) in tradable manufacturing makes up only about 15–24 percent of the manufacturing gross output price, as is shown in Table ; intermediate input costs account for 67–74 percent of total costs and the profit markup is generally around 10–12 percent. This means that if manufacturing ULC increases by one percentage point, the gross output price increases by just 0.15–0.24 percent, when we assume the complete “pass-through” of higher labor costs onto prices. This in turn implies that a price elasticity of export demand of (say) −1 is consistent with a ULC elasticity of export demand of around −0.2. However, if cost pass-through is not complete, but, say, only half (which is realistic),Footnote5 a relative price elasticity of export demand of −1 is consistent with an RULC elasticity of export demand of just −0.10, which is close to findings for Germany by Onaran and Galanis (Citation2012) and Storm and Naastepad (Citation2012)—the only two studies directly estimating the RULC elasticity of exports. Accordingly, RULC trade elasticities by definition take a value of only one-fourth to one-eighth of the respective price elasticities (in absolute terms). Draghi has it wrong, therefore, when he attributes the gain in Germany’s international competitiveness to the decline in its RULC and the loss in Southern Europe’s competitiveness to the growth in its RULC.

TABLE 3 Unit Labor Costs and Gross Output Prices (mid-2000s)

However, all this does not mean that “competitiveness” is unimportant. It is nonprice or technological competitiveness that matters—not price or cost competitiveness—which was recognized by Schumpeter (Citation1943: 84) when he wrote that in capitalist reality, what counts is “the competition from the new commodity, the new technology, the new source of supply, the new type of organization.” The importance of technological (nonprice) competitiveness and (high-tech) productive capabilities is brought out in studies by the ECB (Citation2005, Citation2010), Abdon et al. (2010), Felipe and Kumar (Citation2011), Mazzucato and Perez (Citation2014), and Storm and Naastepad (Citation2015a, Citation2015b). The Mediterranean export structure (in terms of its complexity) is similar to that of China and there are few Mediterranean names that can rival BMW, Bosch, Mercedes, SAP, or Siemens. This is where the real problem of the peripheral countries lies: their lack of competitiveness vis-à-vis Germany is not caused by the fact that their RULCs are too high, their problem is that they are locked in to lower and middle levels of technology. Reducing wages and lowering RULC is never going to solve that problem.

MISHANDLING #2: CUTTING WAGES (INTERNAL DEVALUATION) AND DEREGULATING LABOR MARKETS UNDERMINE A COUNTRY’S COMPETITIVENESS AND STALL EXPORT GROWTH. COMBINED WITH FISCAL AUSTERITY THIS POLICY COCKTAIL IS LETHAL

In Myth #2, the Southern European economies are considered to “unfit,” not competitive enough—unlike “successful” Germany, which is held up as a role model of competitive strength, flexibility, and resilience. We have argued elsewhere the reasons that this view of Germany’s recovery from the crisis is inaccurate and misleading (Storm and Naastepad Citation2015b). Our focus here is on the mistreatment of the Eurozone periphery, which, in line with Myth #2, is pressed to reestablish cost competitiveness. This view is nowhere expressed better than in the February 12, 2015, high-level policy statement by the Informal European Council, which includes the twelfth president of the European Commission, Jean-Claude Juncker; the president of the European Council, Donald Tusk; the president of the Eurogroup and president of the Board of Governors of the European Stability Mechanism (ESM), Jeroen Dijsselbloem; and Mario Draghi of the ECB. The title of their analytical note is Preparing for Next Steps on Better Economic Governance in the Euro Area. According to Juncker–Tusk–Dijsselbloem–Draghi (henceforth: JTDD), deep down the Eurozone crisis is a crisis of cost competitiveness, caused by structural weaknesses and rigidities, especially in labor markets, which led to rising ULC in a number of euro area countries:

thereby reducing their competitiveness and leading to a negative balance of payments vis-à-vis other euro area countries which had kept labour unit cost stable or even lowered them. This brought about higher unemployment rates during the crisis (see Chart 4). In addition, the relatively favourable financing conditions in the first years of the euro led to a misallocation of sources of financing towards less productive forms of investment, such as real estate, and to a greater risk-taking and indebtedness of many private and public actors. When the crisis hit the euro area and markets reappraised the risk and growth potential of individual countries, the loss of competitiveness became visible and led to outflows of sources of finance strongly needed for investment, thereby further intensifying the impact of the crisis in these countries. (Informal European Council Citation2015: 4)

We reproduce JTDD’s Chart 4 as panel A in our Figure , as it is used to make the point that lowering wages—and hence ULC—is a condicio sine qua non for economic recovery.

Figure 6 Does higher unit labour cost lead to higher unemployment?” (a) Changes in ULC (2001–2009) and in the unemployment rate (2009–13) [reproduced from Informal European Council (Citation2015)]. (b) Changes in ULC (2009–13) and in the unemployment rate (2009–13) [reproduced from Janssen (Citation2015)].

Sources: See sources for Figure .

![Figure 6 Does higher unit labour cost lead to higher unemployment?” (a) Changes in ULC (2001–2009) and in the unemployment rate (2009–13) [reproduced from Informal European Council (Citation2015)]. (b) Changes in ULC (2009–13) and in the unemployment rate (2009–13) [reproduced from Janssen (Citation2015)].Sources: See sources for Figure 5.](/cms/asset/856c3d51-5267-456c-8c38-a468397dcca1/mijp_a_1159084_f0006_oc.jpg)

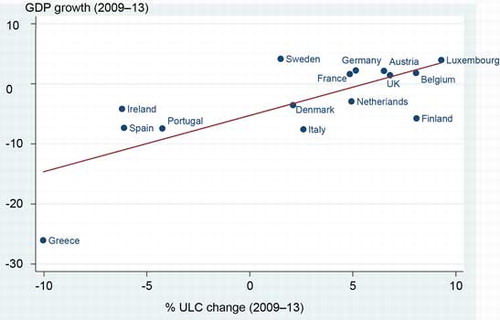

Panel A suggests that higher wages have led to higher unemployment, or conversely that lowering wages will help bring down unemployment. The graph is misleading however. First, the fitted regression line, which is upward sloping, is a statistical artifact because it depends on one outlier observation, namely, Greece. If we leave out Greece,Footnote6 the line turns horizontal—indicating no statistically significant association whatsoever between ULC increases and unemployment increases.Footnote7 Second, as Janssen (Citation2015) correctly observes, JTDD compare changes in unemployment after the crisis with increases in ULC before the crisis—which makes no sense. In panel B of Figure , we plot changes in both ULC and unemployment during 2009–13. The result is a statistically significant negative correlation—a declining regression line. The statistical significance of this result also holds true if Greece or any other country is left out of the estimation.Footnote8 Our findings in Panel B are confirmed in Figure , which plots changes in ULC against changes in real GDP during 2009–13—the statistically significant positive association tells us that internal devaluations are causing collapses in real GDP growth. Panel B of Figures and show the bleak reality: sharply declining wages in Greece, Ireland, Portugal, and Spain, leading to steep declines in aggregate demand and output, and corresponding increases in unemployment (see Storm and Naastepad Citation2015a).

Figure 7 Postcrisis Eurozone (2009–2013): Internal Devaluations Are Killing Economic Growth

Sources: See sources for Figure .

Notes: The OLS regression is:

The main plank of the Informal European Council’s “recovery strategy” is to ingrain (nominal and real) wage restraint into the fabric of the Eurozone by means of what are euphemistically called “modernizing structural reforms” in the cash-strapped economies, but what in practice are the deregulation of labor markets and the downsizing of welfare states—all as the price to pay for ECB rescue loans. Such “modernizing reforms” are supposed to create a more competitive and flexible system for firms by removing regulatory barriers and institutional “rigidities” by curbing union wage-bargaining power, reducing workers’ sense of entitlement to job security and welfare, and increasing labor mobility. However, new research by IMF staff, published in the World Economic Outlook of April 2015 (IMF Citation2015b: Box 3.5), remarkably concludes that “labor market regulation is not found to have statistically significant effects on total factor productivity.” This finding puts the effectiveness of JTDD’s recovery strategy into clear doubt.

What is, perhaps paradoxically, not understood by JTDD is that, as Solow (Citation1998) once remarked, every one of these regulations was intended to promote a desirable social purpose—often as a “second-best” response to a “market failure.” For example, working time regulations and minimum wages must be seen as responses to coordination failures among employers (Lee and McCann Citation2011) and employment protection legislation is helping to share employment and income risks between workers and firms (Agell Citation1999). In the absence of such regulations, the resulting levels of labor inputs and labor productivity will be suboptimal (Pissarides Citation2010). We can give further reasons why “flexible” labor markets are not good for productivity and innovation. In deregulated labor markets, firms will invest less in workers’ firm-specific human capital (Storm and Naastepad Citation2009; Kleinknecht et al. Citation2013; Lee and McCann Citation2011;); worker motivation becomes eroded as does mutual trust between employer and employees (Agell Citation1999; Storm and Naastepad Citation2012); lower wage costs will reduce the pace at which older vintages of capital stock are being scrapped and new equipment, embodying the latest more productive technologies, is being installed (Kleinknecht et al. Citation2013). Space prevents us from going into greater detail, but our main point is that it is impossible to see how Europe thinks it can reduce the large gaps in labor productivity and technological capabilities between the Eurozone core and periphery by cutting wages and breaking down “productivist” social overhead structures (Storm and Naastepad Citation2015c).

This brings us to the real problem of the Eurozone: the widening differentials in labor productivity and technological capabilities between members of the Eurozone. In the precrisis years, Germany managed to strengthen its production structure, but the Eurozone periphery lost ground—both its manufacturing activities and export bases became relatively narrower and technologically stagnant. This has been widely documented using a variety of structural indicators, ranging from technology and capital intensity and skill intensity to the innovation intensity of sectoral output (Janger et al. Citation2011; Simonazzi, Ginzburg, and Nocella Citation2013). We use Table to illustrate how Eurozone manufacturing production structures changed during 1999 and 2007—relative to Germany’s productive base, which became more high- and medium-tech intensive. While most EU countries failed to keep up with Germany’s pace of technological upgrading (meaning there was relative divergence), the value-added share of high- and medium-tech manufacturing did register an absolute decline in France (by 3.7 percentage points), Italy (by 1.4 percentage points), Portugal (by 1.7 percentage points), and Spain (by 3.6 percentage points)—which implies absolute divergence. At the same time, the value-added share of low-tech manufacturing in Germany was about 2.8 percentage points lower than the EU average in 1999; it was also far lower than that of Greece, Italy, and Portugal—and the difference grew wider between 1999 and 2007. The share of the low-tech sector in GDP was 3.6 percentage points higher in Greece than in Germany in 2007, 4.3 percentage points higher in Italy, and 6.7 percentage points higher in Portugal. We must note here that Germany’s manufacturing (export) strength is based on a highly coordinated and regulated “model” based on close links and effective “checks and balances” between (often high-tech) firms, skilled workers (through workers’ councils), and committed banks—and not on a system relying on cheap, flexible labor and uncommitted finance, as is being proposed for Europe’s periphery (Storm and Naastepad Citation2015b). JDTT who weigh almost exclusively on cutting nominal ULC, will only be slowing down the rate of labor-saving technological progress and stifling initiatives to diversify and technologically upgrade exports—thus locking the Southern Eurozone into low-wage, relatively nondynamic export specialization patterns and tourism (as employment option of last resort). The structural imbalances within the Eurozone can be reduced only if the peripheral countries succeed in catching up with German productivity and technological potential (Mazzucato Citation2013; Mazzucato and Perez Citation2014). Through its single-minded emphasis on wages and nominal unit labor cost, JDTT will be achieving the exact opposite.

TABLE 4 Value-Added Share (Relative to Germany’s), 1999 and 2007 (Percentage Differences)

HOW SHOULD ONE THEN THINK ABOUT THE EUROZONE CRISIS?

The real cause of the Eurozone crisis is actually quite prosaic: during the first eight years of the European Monetary Union (EMU), massive financial flows, originating from the stagnating Eurozone core (Germany), fed into asset-price bubbles and debt-based spending booms in the periphery, which in turn raised peripheral demand, also for imports, lowered unemployment, and pushed up wages and inflation (O’Connell Citation2015). Econometric evidence strongly indicates that current account deficits in Europe’s periphery increased first, and their RULC started to increase only later (Gabrisch and Staehr Citation2014; Gaulier and Vicard Citation2012). Hence, Eurozone imbalances arose as a result of strong domestic demand growth in the periphery, spurred by a domestic credit boom made possible by European financial integration, which removed the obstacles discouraging the flow of private debt from the core to the periphery (Chen, Milesi-Ferretti, and Tressel Citation2012; Diaz Sanchez and Varoudakis Citation2013; Lane and McQuade Citation2013). Cross-border financial flows increased far more than cross-border trade in goods and services, especially during 2003–7 when there was a striking increase in debt (not equity) flows from Eurozone core banks to the periphery (Lane and McQuade Citation2013; Waysand, Ross, and de Guzman Citation2010). Hence, unsustainable current account imbalances were driven by changes in the capital account—as higher debt-financed domestic demand spilled over into higher imports (O’Connell Citation2015)

The prime factor underlying the credit boom in the periphery was the unusually low long-term interest rates prevailing in the early 2000s (Lane Citation2012). The ECB decided to lower the interest rate in response to the low inflation and the absence of any inflation threat (given the lackluster growth and high long-term unemployment) in the Eurozone core—and specifically in wage-led Germany where growth slowed down and inflation fell as a result of deliberate nominal wage moderation (Storm and Naastepad Citation2015c). It is here that German wage moderation created fatal consequences, as German stagnation prompted the ECB to lower the “one-size-fits-all” nominal interest rate for the whole Eurozone; this next led to below-average real interest rates in the Eurozone periphery where both growth and inflation were higher—particularly after country-specific risk premiums had fallen to historically very low levels. This is shown in Table . While real interest rates in France, Greece, Italy, and Spain were higher than those in Germany in the 1990s, they fell—often far—below Germany’s real interest rate after monetary unification. The Spanish real interest rate during 2000–2007 was a historically low 0.4 percent, while Greece and Portugal had an unusually low average real rate of interest of around 1.4 percent over the same period. Markets apparently did not expect substantial default risk because the bonds of euro area debtor countries became close substitutes for German Bunds—and they definitely did not expect a fiscal crisis of the scale that would threaten the Eurosystem as a whole (Temin and Vines Citation2013). What banks and investors (in the core) actually did was to develop a false sense of security—even euphoria—about lending to peripheral economies. In any case, with their home market stagnating, there was a “German credit glut” because internationalizing German banks were all too eager to lend and/or invest abroad (Atoyan, Jaeger, and Smith Citation2012), as BIS data show, whether in U.S. or Spanish mortgage bonds, in interbank lending, or sovereign bonds in the euro area (Ma and McCauley 2013; O’Connell Citation2015). Debt and asset-price booms (which were driving growth in the periphery) could, of course, not last forever—and the end this time came in 2008/9, after the governments of Greece, Ireland, Portugal, and Spain had socialized mountains of private-sector debt, only to find themselves punished by what Ronald Janssen (Citation2015) aptly calls a “financial sector strike.” The rest is history.

TABLE 5 Eurozone: Real Interest Rates and Domestic Demand Growth (1992–1999 and 2000–2007)

The cheap credit was indeed misallocated, as JTDD (2015) claim, toward real estate and other nontraded, low-tech activities, but JTDD are mistaken when they blame this on “significant nominal and real rigidities,” especially in labor markets. The “misallocation” was the result of impeccable capitalist logic—as capital was allocated to those activities with the highest private returns. We document this process in Table , which presents evidence on the composition of aggregate fixed investment in Germany, Italy, and Spain in the 1990s and early 2000s as well as the industry-wise (ex post) rates of return on capital for six broad sectors during the 1990s and 2000–2007 (see Storm and Naastepad Citation2015c). What the numbers show is that, in all three economies, average rates of return on manufacturing are generally lower than in construction—but in Germany the gap in returns earned in these sectors narrowed from 21.9 percent in the 1990s to 6.9 percent during 2000–2007, whereas in Spain it more than doubled from 10.2 percent to 21.2 percent. These trends explain why construction investment (as a share of GDP) came down in Germany, while it went up in Spain. Moreover, returns to investment were generally low in (stagnating) Germany across all activities, and this constituted a major push factor driving private capital flows to southern Europe, where returns were much higher.Footnote9 Spain’s construction and tourism sectors offered by far the highest returns on capital in the Eurozone—hence it is little wonder that German and French banks were lining up to offer credit to Spanish project developers and tourism businesses. This was a profoundly disturbing trend, because these investments amounted to nothing whatsoever when it came to building up productive capacity and technological capabilities. In this way, these massive financial flows within the monetary union reinforced existing structural differences in productive capabilities and export specialization between Europe’s core and periphery. The Eurozone periphery lost ground—both its manufacturing activities and export bases became relatively narrow and technologically stagnant. This is Europe’s real competitiveness problem. And now that debtor countries are forced to deregulate and cut wages, they get trapped in low-wage low-productivity activities with an export specialization that overlaps with even more-low-wage China.

TABLE 6 Real Gross Fixed Capital Formation and Rates of Return on Capital: Germany, Italy, and Spain (1992–1999 Versus 2000–2007)

Monetary and financial integration has thus been driving European economies and countries apart—and propelled by these centrifugal forces, the old debate about a political (and fiscal) union, which has been kept on the back burner ever since the Maastricht Treaty of 1992, has returned. Many observers see it as perhaps the only way to hold the Eurozone together. But in our opinion, as long as European integration remains (financial) market-led, even a fiscal union will be too weak a mechanism to counter the structural centrifugal forces that are entrenching a two-tier Europe with two classes of members, as Beck (Citation2013) feared, with the “second-class” members structurally dependent upon transfers from the “first-class” members. The center will not hold.

BREAKING THE DEEP SLUMBER OF DECIDED OPINION

Our conclusions are brief:

It is “an indisputable fact” that sovereign debt buildup was dwarfed by the accumulation of private-sector debts (especially household debts and financial-sector debts, see Tables and ), which fueled and were made possible by unsustainable asset-price booms (see Figures and ). Private debts are the real problem. Hence, austerity is the wrong medicine for the wrong disease, bringing only pain (first)—and no gain (later).

The rise in (relative) nominal unit labor costs did not lead to the higher current account deficits in the Eurozone periphery. International competitiveness is not about nominal wage costs, but about technology and innovation. Given a country’s technological capabilities as reflected by its productive structure, export growth and import growth are overwhelmingly determined, not by nominal ULC, but by (foreign and domestic) demand. Attempts to improve “competitiveness” by wage cuts and labor market deregulation can only backfire (see Figure , panel B)—no country has managed to climb up the technological ladder (upgrading exports and strengthening nonprice competitiveness) based on low wages and footloose, fractured, and flexible workers.

The only sensible way to think about the Eurozone crisis is in terms of a private-sector debt crisis, aided and abetted by the liberalization of (integrating) European financial markets and a “global banking glut.” With this understanding, we can start thinking about more effective, efficient, and just ways to bring about economic recovery in the Eurozone. Without doubt, such a recovery package must include a coordinated demand stimulus, a directing of credit toward productive investments and “smart” innovation, a bailing out of cash-strapped and insolvent governments (by the ECB), and “mission-oriented” industrial policies to restructure and upgrade peripheral manufacturing (Mazzucato and Perez Citation2014). This requires, at the EU level, coordination of economic decision making, or what Beck (Citation2013) calls a “new social contract for Europe”—not the beggar-thy-neighbor competition propagated by JTDD or the “eat your peas” solution of Schäuble.

Needless to say, none of these proposals is being seriously entertained by Eurozone leadership, such as the Informal European Council, as long as it dwells in J.S. Mill’s “deep slumber of a decided opinion” (Mill, On Liberty: 95). This unwillingness to tackle the true causes of the crisis is not without risk because the strains of ongoing divergence within the zone cannot be endured endlessly politically.

Additional information

Notes on contributors

Servaas Storm

Servaas Storm is a macroeconomist who works on growth, distribution, technological change, economic development, and climate change. He is one of the editors of the journal Development and Change.

C.W.M. Naastepad

C.W.M. (Ro) Naastepad has worked on real-financial computable general equilibrium (CGE) models and economic policies conducive to technological progress and productivity growth. Her current research concerns the “colonization” of society by technology (especially artificial intelligence) and the economy, and concepts of capital and technology that will enable human beings to give direction to both. Both authors work at the Faculty of Technology, Policy and Management of Delft University of Technology, The Netherlands. An earlier version of this paper was presented at the Annual Conference of the Institute for New Economic Thinking in Paris, April 11, 2015. The authors thank the two referees of the journal for their critical, gracious, and constructive comments.

Notes

One of the referees suggested that the undisputed increase in Eurozone sovereign debt following the Great Financial Crisis may have created a situation in which fiscal austerity became unavoidable. We beg to disagree: all countries (e.g., the United States, the UK, and China) having their own national central banks could and did resort to an unprecedented “emergency Keynesianism.” It is precisely because the Eurozone countries do not have their own central bank and because the ECB was/is unwilling by design to provide support that they were forced to rely on bond markets—and forced to adopt austerity measures. Alain Parguez (Citation1999) was perhaps the first to point out how this design feature could and would upend the monetary unification of Europe.

While we agree with both referees that “correlation” should not be mistaken for “causation,” we think it might be good to point out that that there are two approaches to the issue of causality in economics (Hoover Citation2001): the first one follows Hume and Wold and defines causality as “temporal precedence” (as in Granger causality testing), but the second approach (following Tinbergen, Haavelmo, and Simon) defines causality as a prior structural ordering of endogenous versus exogenous (instrumental) variables based on economic theory. We adhere to the second approach—the causal structure is the province of a priori economic theory (rather than something to be learned from data per se).

For a recent exchange on unit labor cost competitiveness and the Eurozone crisis, see Storm (Citation2016a, Citation2016b) and Bofinger (Citation2016).

This does not mean that nominal (and real) wage moderation in Germany was not important. It was—for two reasons. First, it led to a race to wage deflation throughout the Eurozone, depressing demand. Second, it slowed down German growth and lowered German inflation, which in turn prompted the ECB to reduce the interest rate for the whole of the Eurozone, as we argue below.

See Goldstein and Khan (Citation1985). Athanasoglou and Bardaka (Citation2010) find a pass-through of between 25 percent and 50 percent in the case of Greek manufacturing exports.

Determining outliers is always a subjective exercise. Here Greece is considered an outlier because the crisis-induced increase in its unemployment rate (2009–13) differs from the sample mean by about three times the standard deviation. In the case of a sample of 100 normally distributed observations, one such outlier would already be a cause for concern. This means that the Greek crisis is (still) so anomalous and extreme that causal mechanisms are different in Greece from those in the rest of the sample.

The coefficient (estimated by OLS) of percentage change ULC (2001–9) is 0.38 and statistically significantly different from zero (at the 10 percent level; t-value = 2.17). When we leave out the observation for Greece, the coefficient is 0.20 and is not statistically significant (at 10 percent; t-value = 1.46).

The OLS coefficient of percentage change ULC (2009–13) is −0.64 and statistically significantly different from zero (at the 5 percent level; t-value = −2.75). Without Greece, the coefficient is −0.37 and is statistically significant (at 10 percent; t-value = −2.22).

Atoyan, Jaeger, and Smith (Citation2012) conclude that push factors (low returns in the core), rather than pull factors (high returns in the destination countries) drove most of the capital flows coming from the Eurozone core. See also O’Connell (Citation2015).

REFERENCES

- Abdon, A., Bacate, M., Felipe, J., and Kumar, U. 2010. Product Complexity and Economic Development. The Levy Economics Institute Working Paper No. 616. New York: Bard College.

- Agell, J. 1999. “On the Benefits from Rigid Labour Markets: Norms, Market Failures, and Social Insurance.” Economic Journal 109:F143–F164.

- Alesina, A., and S. Ardagna. 2010. “Large Changes in Fiscal Policy: Taxes Versus Spending.” In Tax Policy and the Economy, vol. 24, ed. J.R. Brown, 35–68. Cambridge, MA: National Bureau of Economic Research.

- Athanasoglou, P.P., and I.C. Bardaka. 2010. “New Trade Theory, Non-Price Competitiveness and Export Performance.” Economic Modelling 27, no. 2: 217–28.

- Atoyan, R.; A. Jaeger; and D. Smith. 2012. “The Pre-Crisis Capital Flow Surge to Emerging Europe: Did Countercyclical Fiscal Policy Make a Difference?” IMF Working Paper WP/12/222.

- Ball, L.; D. Furceri; D. Leigh; and P. Loungani. 2013. “The Distributional Effects of Fiscal Consolidation.” IMF Working Paper WP/13/151. http://www.imf.org/external/pubs/ft/wp/2013/wp13151.pdf

- Barba, A., and M. Pivetti. 2009. “Rising Household Debt: Its Causes and Macroeconomic Implications: A Long-Period Analysis.” Cambridge Journal of Economics 33, no. 1: 113–37. doi:10.1093/cje/ben030.

- Beck, U. 2013. German Europe. Cambridge: Polity Press.

- Bini Smaghi, L. 2013. “Austerity and Stupidity.” VoxEU.org, November 6.

- Blanchard, O., and F. Giavazzi. 2002. “Current Account Deficits in the Euro Area: The End of the Feldstein–Horioka Puzzle? Brookings Papers on Economic Activity, no. 2: 147–86.

- Bofinger, P. 2016. “Friendly Fire.” http://ineteconomics.org/ideas-papers/blog/friendly-fire

- Bornhorst, F., and M. Ruiz-Arranz. 2013. “Indebtedness and Deleveraging in the Euro Area.” 2013 Article IV Consultation on Euro Area Policies: Selected Issues Paper, ch. 3, IMF Country Report 13/232.

- Bussière, M.; G. Callegari; F. Ghironi; G. Sestieri; and N. Yamano. 2013. “Estimating Trade Elasticities: Demand Composition and the Trade Collapse of 2008–9.” American Economic Journal, Macroeconomics 5, no. 3 (July): 118–51.

- Cecchetti, S.G.; M.S. Mohanty; and F. Zampolli. 2011. “The Real Effects of Debt.” BIS Working Paper No. 352.

- Chen, R.; G.M. Milesi-Ferretti; and T. Tressel. 2012. “External Imbalances in the Euro Area.” IMF Working Paper WP/12/236.

- Chmelar, A. 2013. Household Debt and the European Crisis. https://www.ceps.eu/system/files/Household%20Debt%20and%20the%20European%20Crisis.pdf

- Costa, J., and R. Ricciuti. 2013. “Sources for the Euro Crisis: Bad Regulation and Weak Institutions in Peripheral Europe.” Working Paper 15/2013, Department of Economics, University of Verona.

- Cynamon, B.Z., and S.M. Fazzari. 2013. “Inequality and Household Finance during the Consumer Age.” Levy Economics Institute of Bard College, Working Paper no. 752.

- Dadush, U., and contributors. 2010. Paradigm Lost: The Euro in Crisis. Washington, DC: The Carnegie Endowment for International Peace.

- Danninger, S., and F. Joutz. 2007. “What Explains Germany’s Rebounding Export Market Share?” IMF Working Paper WP/07/24.

- Diaz Sanchez, J.L., and A. Varoudakis. 2013. “Growth and Competitiveness as Factors of Eurozone External Imbalances.” World Bank Policy Research Working Paper 6732.

- Draghi, M. 2012. “Competitiveness of the Eurozone and Within the Eurozone.” Speech at the colloquium “Les défis de la compétitivité” [The Challenges of Competitiveness], Paris, March 13.

- Eichengreen, B., and K.H. O’Rourke. 2012. “Gauging the Multiplier: Lessons from History.” VoxEU.org.

- European Central Bank (ECB). 2005. “Competitiveness and the Export Performance of the Euro Area.” Occasional Paper Series no. 30.

- ———. 2012. “Competitiveness and External Imbalances within the Euro Area.” Occasional Paper Series no. 139.

- European Commission. 2009a. The Evolution of EU and Its Member States’ Competitiveness in International Trade. Final Report CEPII-CIREM ATLASS consortium. Brussels.

- ———. 2009b. “Competitiveness Developments Within the Euro Area.” Quarterly Report on the Euro Area 8, no. 1. Brussels: European Commission, Directorate-General for Economic and Financial Affairs.

- ———. 2010. “The Impact of the Global Crisis on Competitiveness and Current Account Divergences in the Euro Area.” Quarterly Report on the Euro Area. Special Issue. Brussels: European Commission, Directorate-General for Economic and Financial Affairs.

- ———. 2015. European Economic Forecasts Winter 2015. http://ec.europa.eu/economy_finance/publications/european_economy/2015/pdf/ee1_en.pdf

- Felipe, J., and U. Kumar. 2011. “Unit Labor Costs in the Eurozone: The Competitiveness Debate Again.” Levy Economics Institute of Bard College, Working Paper no. 651.

- Gabrisch, H., and K. Staehr. 2014. “The Euro Plus Pact: Cost Competitiveness and External Capital Flows in the EU Countries.” European Central Bank Working Paper Series no. 1650.

- Gaulier, G., and V. Vicard. 2012. “Current Account Imbalances in the Euro Area: Competitiveness or Demand Shock?” xsBanque de France Quarterly Selection of Articles no. 27.

- Gechert, S., and A. Rannenberg. 2015. “The Costs of Greece’s Fiscal Consolidation.” IMK Policy Brief. Hans Böckler Stiftung. http://www.boeckler.de/pdf/p_imk_pb_1_2015.pdf

- Goldstein, M., and M.S. Khan. 1985. “Income and Price Effects in Foreign Trade.” In Handbook of International Economics, vol. 2, ed. R.W. Jones and P.B. Kenen ch. 20, 1041–105. Amsterdam: North-Holland.

- Gordon, R.J., and R. Krenn. 2010. “The End of the Great Depression 1939–41: Policy Contributions and Fiscal Multipliers.” NBER Working Paper 16380 (September).

- Gros, D. 2011. “Competitiveness Pact: Flawed Economics.” Centre for European Policy Studies, CEPS Commentaries, March 18.

- Guajardo, J.; D. Leigh; and A. Pescatori. 2011. “Expansionary Austerity: New International Evidence.” IMF Working Paper WP/11/158. http://www.imf.org/external/pubs/ft/wp/2011/wp11158.pdf

- Hoover, K. 2001. Causality in Macroeconomics. Cambridge: Cambridge University Press.

- Informal European Council. 2015. Preparing for the Next Steps on Better Economic Governance in the Euro Area. Analytical Note, written by J.-C. Juncker, D. Tusk, J. Dijsselbloem, and M. Draghi. Brussels: European Commission. http://ec.europa.eu/priorities/sites/beta-political/files/analytical_note_en.pdf

- International Monetary Fund (IMF). 2012a. “Dealing with Household Debt.” World Economic Outlook: Growth Resuming, Dangers Remain, April, ch. 3.

- ———. 2012b. World Economic Outlook: Coping with High Debt and Sluggish Growth, October.

- ———. 2015a. World Economic Outlook Update. https://www.imf.org/external/pubs/ft/weo/2015/update/01/pdf/0115.pdf

- ———. 2015b. World Economic Outlook: Uneven Growth—Short- and Long-Term Factors. Washington, DC.

- Janger, J.; W. Hölzl; S. Kaniovski; J. Kutsam; M. Peneder; A. Reinstaller; S. Sieber; I. Stadler; and F. Unterlass. 2011. Structural Change and the Competitiveness of EU Member States: Final Report. http://ec.europa.eu/enterprise/policies/industrial-competitiveness/documents/files/structural_change_en.pdf

- Janssen, R. 2015. “European Economic Governance and Flawed Analysis.” Social Europe. http://www.socialeurope.eu/author/ronald-janssen/

- Kleinknecht, A.; C.W.M., Naastepad; S. Storm; and R. Vergeer. 2013. “Labour Market Rigidities Can Be Useful.” In Financial Crisis, Labour Markets and Institutions, ed. S. Fadda and P. Tridico, ch. 8, 175–191. London: Routledge.

- Lane, P.R. 2012. “The European Sovereign Debt Crisis.” Journal of Economic Perspectives 26, no. 3: 49–68.

- Lane, P.R., and P. McQuade. 2013. “Domestic Credit Growth and International Capital.” European Central Bank, Working Paper Series, no. 1566, European Central Bank, July. https://www.ecb.europa.eu/pub/pdf/scpwps/ecbwp1566.pdf?a95537eedcb2aaf27f7f34fb39ceaa44

- Lane, P.R., and B. Pels. 2012. “Current Account Imbalances in Europe.” IIIS Discussion Paper no. 397. Trinity College Dublin.

- Lee, S., and D. McCann, eds. 2011. Regulating for Decent Work. New Directions in Labour Market Regulation. London: Palgrave.

- Martin, P., and T. Philippon. 2014. “Inspecting the Mechanism: Leverage and the Great Recession in the Eurozone.” NBER Working Paper no. 20572.

- Mazzucato, M. 2013. The Entrepreneurial State: Debunking Public vs. Private Sector Myths. London: Anthem Press.

- Mazzucato, M., and C. Perez. 2014. “Innovation as Growth Policy: The Challenge for Europe.” SPRU Working Paper Series SWPS 2014–13. University of Sussex.

- Mill, J. S. 2002. On Liberty. London: Dover Publications.

- Noyer, C. 2012. “Remaining Challenges Facing the Euro Area.” http://www.bis.org/review/r121010b.pdf

- O’Connell, A. 2015. “European Crisis: A New Tale of Center–Periphery Relations in the World of Financial Liberalization/Globalization?” International Journal of Political Economy 44, no. 3: 174–95.

- Onaran, Ö., and G. Galanis. 2012. “Is Aggregate Demand Wage-Led or Profit-Led: National and Global Effects.” Conditions of Work and Employment Series no. 40. Geneva: ILO.

- Parguez, A. 1999. “The Expected Failure of the European Economic and Monetary Union: A False Money Against the Real Economy.” Eastern Economic Journal 25, no. 1: 63–76.

- Pissarides, C. 2010. “Why Do Firms Offer ‘Employment Protection?’” Economica 77, no. 301: 131–59.

- Reinhart, C.M., and K.S. Rogoff. 2010. “Growth in a Time of Debt.” American Economic Review: Papers and Proceedings 100 (May):573–78.

- Schäuble, W. 2011. “Why Austerity Is the Only Cure for the Eurozone.” Financial Times, September 5. http://www.ft.com/intl/cms/s/0/97b826e2-d7ab-11e0-a06b-00144feabdc0.html#axzz355KUI33.

- Schröder, E. 2015. “Eurozone Imbalances: Measuring the Contribution of Expenditure Switching and Expenditure Volumes 1990–2013.” New School University, Working Paper 08/2015. http://www.economicpolicyresearch.org/econ/2015/NSSR_WP_082015.pdf

- Schuknecht, L.; P. Moutot; P. Rother; and J. Stark. 2011. “The Stability and Growth Pact: Crisis and Reform.” ECB Occasional Paper Series no. 129.

- Schumpeter, J.A. 1943. Capitalism, Socialism and Democracy. London: Unwin.

- Simonazzi, A.; A. Ginzburg; and G. Nocella. 2013. “Economic Relations between Germany and Southern Europe.” Cambridge Journal of Economics 37, no. 3: 653–675.

- Sinn, H.W. 2010. “Reining in Europe’s Debtor Nations.” Project Syndicate, April.

- ———. 2014. “Austerity, Growth and Inflation: Remarks on the Eurozone’s Unresolved Competitiveness Problem.” World Economy 37, no. 1: 1–13.

- Solow, R.M. 1998. “What Is Labour-Market Flexibility? What Is It Good for?” Proceedings of the British Academy 97:189–211.

- Storm, S. 2016a. “German Wage Moderation and the Eurozone Crisis: A Critical Analysis.” http://ineteconomics.org/ideas-papers/blog/german-wage-moderation-and-the-eurozone-crisis-a-critical-analysis

- ———. 2016b. “Response to Peter Bofinger’s ‘Friendly Fire.’” http://ineteconomics.org/ideas-papers/blog/response-to-peter-bofinger

- Storm, S., and C. W.M. Naastepad. 2009. “Labour Market Regulation and Labour Productivity Growth: Evidence for 20 OECD Countries 1984–2004.” Industrial Relations 48, no. 4: 629–54.

- ———. 2012. Macroeconomics Beyond the NAIRU. Cambridge, MA: Harvard University Press.

- ———. 2015a. “Europe’s Hunger Games: Income Distribution, Cost Competitiveness and Crisis.” Cambridge Journal of Economics 39, no. 3 (May): 959–86.

- ———. 2015b. “Germany’s Recovery from Crisis: The Real Lessons.” Structural Change and Economic Dynamics 32 (March):11–24.

- ———. 2015c. “NAIRU Economics and the Eurozone Crisis.” International Review of Applied Economics 29, no. 6: 843–77.

- Temin, P., and D. Vines. 2013. The Leaderless Economy. Why the World Economy System Fell Apart and How to Fix It. Princeton, NJ: Princeton University Press.

- Tolstoy, L. (1882/1987). A Confession and Other Religious Writings. London: Penguin Classics.

- Trichet, J.-C. 2010. “Lessons from the Crisis: Speech by Jean-Claude Trichet, President of the ECB at the European American Press Club, Paris, 3 December 2010.” http://www.ecb.europa.eu/press/key/date/2010/html/sp101203.en.html

- ———. 2011. “Competitiveness and the Smooth Functioning of EMU.” Lecture at the University of Liège, February 23.

- Waysand, C.; K. Ross; and J. de Guzman. 2010. “European Financial Linkages: A New Look at Imbalances.” IMF Working Paper WP/10/295.

- Wyplosz, C. 2013. “Eurozone Crisis: It’s about Demand, Not Competitiveness.” https://www.tcd.ie/Economics/assets/pdf/Not_competitiveness.pdf.