?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

We re-examine the role of monetary policy and its transmission mechanism through the credit channel while focusing on securitisation. We empirically investigate the interactions between securitisation activities and monetary policy using data from 1995 to 2015 for a panel of 10 European countries. We employ a panel VAR model, and estimate it using a GMM system. Our findings indicate that a contractionary monetary policy shock immediately increases securitisation activities and decreases the growth rate of traditional (non-securitised) loans. The evidence supports the argument that merely raising interest rate is not sufficient to control credit booms, but, on the contrary, may induce credit intermediation, which in turn can increase system risk. Any modern central bank should re-examine and redefine its role as a ‘banker’s bank’ taking into consideration the future developments in shadow banking and financial innovation in order to ensure financial stability.

1. Introduction

Financial development matters. Over the last few decades, the relationship between economic and financial development has been a reoccurring research theme in economics and the recent financial crisis has only made the issue more important. The increasing importance of financial sector since the 1980s has been termed as ‘Financialisation’ by several economists (see, Epstein Citation2005; Hein Citation2012; Onaran, Stockhammer, and Grafl Citation2011; Palley Citation2013 amongst others). Financialisation is a multi-dimensional phenomenon (see, e.g., Braga et al. Citation2017; Guttmann Citation2017), which in the context of monetary economics usually refers to the increasing dominance of the financial sector, fuelled by a rise in shadow banking activities and the introduction of new financial instruments — all of which have made the financial system more complex than ever. While there is little doubt that increased financial sophistication is closely linked with long term economic growth (Levine Citation1997), the effects of excessive financialisation can be harmful and lead to negative long-term effects (Lavoie Citation2012; Greenwood and Scharfstein Citation2013).

One of the most important characteristics of financialisation is the rapid growth of the financial innovations such as securitisation, which falls under the umbrella of shadow banking activities. Prior to the 2008 crisis, it was widely believed that financial innovation, through credit intermediation and liquidity transformation, had diversified the risk and added stability to the system. In fact, the efficient financial intermediation was considered important for efficient resource allocation in the economy. The 2008 crisis, however, revealed that this process as a whole has made the entire economic system vulnerable to more serious crises in the long-run. It is now widely believed that increasing level of securitisation played a crucial role in contributing to the recent global financial crisis (see, e.g., Dymski Citation2010; Lavoie Citation2012). Such instabilities inherited in the financial system were identified by Minsky a long time ago. Minsky in his later writings (Minsky Citation1996) used the term ‘money manager capitalism’ to refer to an era of financial practices that characterise our current day financial system. He describes this as an era in which the banking business model, instead of building a stable financial system that can serve the overall economy, is dominated by risky short-term behaviour. The relevant empirical literature supports this view, indicating a strong tendency towards risky short-term behaviour at an institutional level in most advanced countries (see, e.g., Stockhammer Citation2004; Orhangazi Citation2008; Barradas Citation2017; Tori and Onaran Citation2018).

In contrast to the rapid innovations in financial markets, the role of central banks has not evolved with the same pace, e.g., the primary objective of monetary policy is still limited to a more traditional problem of price and output stability while paying less attention to the introduction of complex financial instruments in the markets.Footnote1 One of the main transmission channels of monetary policy is the credit channel, according to which, contractionary monetary policy would lead to a decline in the supply of loans, thereby affecting investment in the economy.Footnote2 However, an important question is that how effective is monetary policy in affecting the supply of loans in practice? The process of securitisation has transformed the banking model from ‘originate and hold’ to ‘originate and distribute’ (Lapavitsas Citation2010). Securitisation involves transforming illiquid assets to liquid ones, creating more liquidity but at the same time lowering lending standards, and increasing risk taking, which in turn have increased banks ability to create liquidity. Consequently, the influence of central banks in the credit markets in general has become limited.

Given the effects of securitisation, it is therefore important to re-examine the role of monetary policy and its transmission mechanism through the bank credit channel. This paper aims to address the question of whether, and how securitisation limits the effects of monetary policy on banks balance sheets. We empirically investigate the interdependencies between monetary policy and banking activities using data from 1995 to 2015 for a panel of 10 countries. Our sample falls in the period known as the ‘Financialisation era’. We particularly focus on the interactions between securitisation activities and monetary policy using a panel VAR model, estimated using a GMM system. While there are a few previous attempts to study the relationship between monetary policy and securitisation (see, e.g., Altunbas, Gambacorta, and Marques-Ibanez Citation2009; Altunbas, Gambacorta, and Marques-Ibanez Citation2010; Berger and Bouwman Citation2013), this is the first paper that empirically investigates the interactions between monetary policy and securitisation activities using a panel VAR approach. The VAR approach, despite having its own pitfalls, is considered a useful tool to study the effects of monetary policy. Overall, our paper contributes to the literature by offering further empirical evidence to the scarce empirical literature in this area.

This paper has four main sections. Section Two explains the process of securitisation while focusing on some key aspects, including the role of monetary policy. Section Three presents data and methodology used to explore the interactions between monetary policy and securitisation activities, and discusses the results of the model. Section Four concludes this paper.

2. What Is Securitisation?

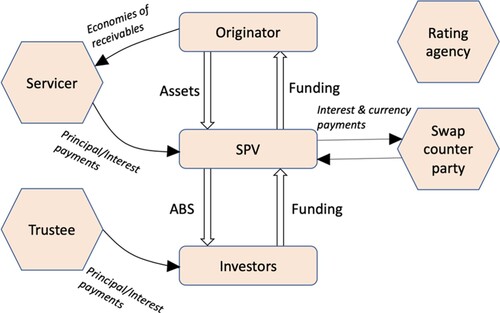

The securitisation process starts when banks (originators) sell their accounts receivables, such as residential and commercial mortgages, auto loans, credit cards and student loans, which are known as ‘true sale’, to special purpose vehicles (SPVs). The SPVs create pools of loans and issue securities against these loans, depending on maturities and interest rates. These securities are then sold in ‘tranches’ (senior, mezzanine, and unrated equity tranches) to investors. At the same time, the SPVs appoint a servicer, usually banks, to collect interest and principal payments on the underlying loans (Marques-Ibanez and Scheicher Citation2010). This process guarantees the separation of the underlying assets from the solvency of the originator. In addition, there are three other parties involved in the process: the swap counter party, the trustee, and the rating agency. The swap counter party is usually involved in hedging the interest rate and currency risk, while the trustee ensures that (i) the money is transferred from the servicer to SPV, and (ii) investors are paid. Rating agencies are responsible for rating senior and mezzanine tranches using credit risk analysis (see ).

Figure 1. Simplified securitisation process. Source: Marques-Ibanez and Scheicher (Citation2010).

From the perspective of banking sector, we can identify three main motives for securitisation. First, to increase liquidity and profitability, where banks sell their loans to SPVs, and obtain a lump-sum value by using off-balance sheet techniques. By doing so the banking system can obtain additional funding, and they can satisfy the demand for credit (Gorton and Pennacchi Citation1995). Moreover, when banks service the securitsed loans, they also obtain revenues from this process. Second, securitisation allows banks to transfer credit risk to SPVs and other financial institutions, and acquire funds at a lower cost (Pennacchi Citation1988; Minton, Sanders, and Strahan Citation2004; Bannier and Hansel Citation2008). Third, to obtain regulatory capital relief by the removal of loans from banks balance sheets, as also argued by Pennacchi (Citation1988).

2.1. The Rise of Securitisation

The process of securitisation is not new. The idea can be traced backed to the 1930s in the US when the Federal National Mortgage Association was created to federally buy and sell insured mortgages. However, it was not until 1970s that securitisation was extended to residential mortgage market. The US was the first country to implement this financial innovation by law, where the Government National Mortgage Association (GNMA or Ginnie Mae) purchased mortgage loans and issued securities against these loans to support under-capitalized regions (Kotz Citation2009). The market for assets backed securities (ABS) started to develop by means of government sponsored agencies, such as the Federal National Mortgage Association, known as Fannie Mae, and the Federal Home Loan Mortgage Corporation, known as Freddie Mack. These agencies enhanced mortgage loan liquidity by issuing and guaranteeing ABS. Mortgage-backed securities (MBS) in the secondary market were worth around 7.5 trillion dollars in mid-2008. Securitisation in the US evolved under the framework set by the Glass-Steagall Act (1933), where investment banking, commercial banking, and securities firms were separated. In 1999, this regulation was replaced by the Gramm-Leach-Bliley Act (GLBA), which allowed banks to associate with securities firms in order to accommodate the needs of the financial sector.

In contrast to the US experience, the development of asset securitisation market in Europe started in the 1990s, which was driven by a number of factors, including technological and financial innovations, the introduction of the Euro, and the rising demand for ABS. The increasing level of financial integration and the removal of exchange rate risk amongst member countries contributed to the growth of the securitisation market (Baele et al. Citation2004). The growth of securitisation in the Euro area was supported by the financial sector regulatory framework, which adapted to the needs of this sector. For instance, with the introduction of Law 130 (1999), known as The Italian Securitisation Law, Italian financial institutions were allowed to securitise and act as SPVs. The increase in securitisation activities was different amongst Euro area countries. However, countries such as Italy, Spain, Portugal, Ireland and the Netherlands experienced a significant increase due to the rise of real estate prices. Commercial and residential mortgage-backed securities represented approximately 68 per cent of all Euro area securities by 2005 (European Securitisation Forum Citation2006).

2.2. Financial Regulations, Monetary Policy, and Securitisation

In general, financial institutions have a tendency of raising various challenges for central banks through financial innovations. This tendency was highlighted by Minsky in his earlier work, arguing that tight monetary conditions such as high interest rates provide an incentive for financial institutions to find new ways of financing (financial innovation) in order to meet credit demands and extend liquidity, which in turn may offset policy effects and induce financial instability (Minsky Citation1957). Theoretically, this also applies to the process of securitisation, which offers to best match market participants’ preferred risk/return and holding-period profiles, and this process systematically leads to underestimation of risk by investors and rating agencies (Coval, Jurek, and Stafford Citation2009). The expansion of securitisation permitted deeper linkages between the major banks originating credit with non-bank financial firms in need of higher return assets to purchase. While securitisation improved banks balance sheets and improved their profitability in the short-run, it hid vulnerabilities that were eventually exposed by the subprime crisis in 2007–08.

In general, the scale and complexity of the securitisation process has raised various challenges for regulators. The increased importance of shadow banking and non-transparent financial transactions has made the credit circulation as a whole more opaque: loans that are securitised, disappear from banks balance sheets, and the process is more reliant on short-term non-deposit funding (Kroszner and Strahan Citation2011). In this process, banks liquidity risk — a key indicator of vulnerability in banking regulations — appears low despite high credit in the financial system. Hence, liquidity-risk pressure by the regulation as a constraint on lending is less effective as highlighted by Dymski (Citation2010).

Apart from raising regulatory challenges, securitisation poses a clear challenge to the effectiveness of monetary policy, as banks have become more dependent on financial market conditions than on bank deposits. Altunbas, Gambacorta, and Marques-Ibanez (Citation2009) used European banks data to demonstrate that securitising banks are less responsive to monetary policy. Altunbas, Gambacorta, and Marques-Ibanez (Citation2010) and Berger and Bouwman (Citation2013) studied the influence of monetary policy of banks liquidity creation (on and off balance sheet) in the US, finding that medium and large banks liquidity creation is not significantly affected by monetary policy. They found that during economic crisis banks liquidity creation is even less responsive to monetary policy. In contrast, Aysun and Hepp (Citation2011) found that the higher the degree of securitisation, the higher the bank’s responsiveness to monetary policy.

Securitisation has also adversely affected the lending standards of banks. Diamond (Citation1984) and Gorton and Pennacchi (Citation1995) have pointed out that the profitability of transferring assets from banks balance sheets to markets has discouraged the screening of borrowers, changing the monitoring function of banks. This is consistent with the lowering of lending standards observed in economies with a high securitisation rates, such as the US (Dell’Ariccia, Igan, and Laeven Citation2012), and with the fact that securitisation allows banks to create more loans (Altunbas, Gambacorta, and Marques-Ibanez Citation2009). Similarly, Maddaloni and Peydro (Citation2011) studied the determinants of banks lending standards in the US and Euro zone, finding that low interest rates for extended periods of time (‘cheap money’) lowered lending standards regardless of borrowers creditworthiness, while increasing banks risk-taking. The latter is accentuated by the use of securitisation in a short-term low interest rate environment, along with weak lending standards supervision.

2.2.1. Regulatory Failures

The increasing dominance of global financial markets prior to the crisis was neither seen as a problem for the effectiveness of monetary policy nor a threat to economic stability. Ben Bernanke, the then Fed Chairman, in his speech in March 2007 argued that globalisation of financial markets has added a dimension of complexity but has not reduced the ability of the Fed to influence financial conditions (Bernanke Citation2007). To highlight the effectiveness of US monetary policy on financial conditions, Bernanke pointed towards the impact of Fed fund rates on other short-term and long-term rates in the economy. Overall, it was widely argued that the core objective of the central banks should only be price stability (’strict inflation targeting’). And in some cases, there was also a consensus for a ‘flexible inflation targeting’ which takes into account both price and output stability. Most central banks considered financial conditions only to the extent that they can impact inflation and output gap. Transparency and financial matters in the markets were not considered primary responsibilities of central banks.Footnote3 Thus, persistent high growth rates and low stable inflation rates in the pre-crisis period were perceived as indicators of macroeconomic stability and the increased dominance of financial sector — perceived as financial efficiency — was not considered as a major concern (Woodford Citation2002). Most economists — while focusing on what we can call ‘short-term’ real business cycle fluctuations (when compared with the span of a financial cycle as discussed in Borio (Citation2014)) — did neglect the build-up of the financial cycle. Hence, it is not surprising that no conflict was observed between the price and economic stability objectives of the central banks. However, when one takes into account the behaviour of financial markets, the trade-off between price stability and financial stability becomes obvious. This trade-off, now well-recognised in the discipline, was emphasised by Hyman Minsky a long time ago, who argued that the central bank in its attempts to fight inflation — via interest rate increases — can create a wave of bankruptcies, leading to asset price collapse, which can endanger the entire financial system (Minsky Citation1980).Footnote4 Central banks, according to Minsky (Citation1957), should focus on reducing the effect of financial crises, which might be the result of instability induced by financial innovations during the boom phase. Furthermore, he argues that when the structure of the financial markets goes through rapid changes, then the efficacy of central bank actions should be re-assessed as changes in the mode of financing tend to undermine policy effects. This description also fits well the process of securitisation as discussed earlier. We now proceed to testing, through which mechanism, if at all, does securitisation pose challenges to the effectiveness of monetary policy.

3. Empirical Analysis

3.1. Data and Methodology

To explore the efficacy of monetary policy, and understand its transmission channels through the credit channel, we use annual data from 1995 to 2015 for a panel of 10 European countries (9 Eurozone countries and the UK).Footnote5

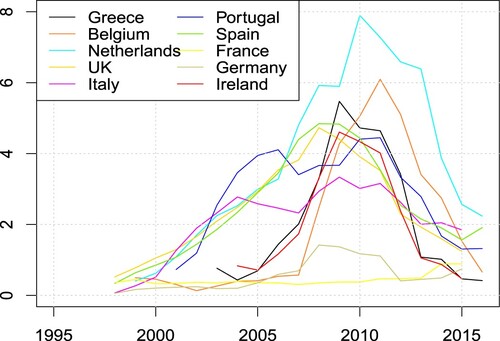

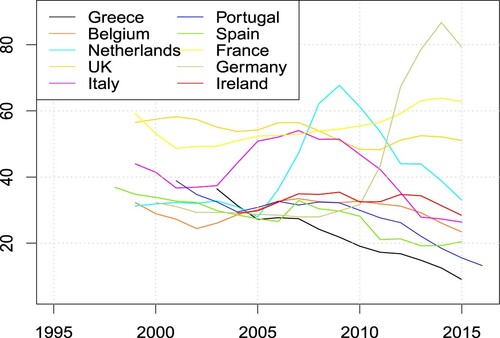

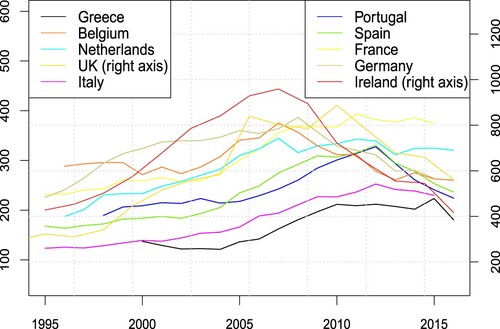

, , and show some important indicators, reflecting the size and activities of the banks in the countries used in our model. The size of the financial sector relative to real economic sector (as measured by total assets of monetary financial institutions (excluding the central bank) relative to real GDP) follows an upward trend in all countries as shown in . There is also an increase in the degree of securitisation as indicated by the ratio of securitised loans to total outstanding traditional (non-securitised) loans as shown in . The upward trend in this series before the crisis reflects banks tendency of securitising a larger portion of their total outstanding loans. Finally, the liquidity ratio, defined as the ratio of liquid assets to total deposits and short-term funding of the banks, in some countries has declined whereas in some cases it has increased as shown in .

Figure 2. Total assets to GDP.

Figure 3. Securitised loans to total loans.

Figure 4. Liquidity ratio.

We now proceed to explaining the variables used in our model. First, we construct a proxy for securitisation activities following the approach of Altunbas, Gambacorta, and Marques-Ibanez (Citation2009):

where (SL) stands for the flow of securitised lending in year t in country i. The data for SL includes mortgages-backed securities (MBS) and assets-backed securities (ABS).

represents total financial assets at the end of the previous year. Other variables included in our empirical analysis are policy rates (r) — representing monetary policy; total stock of outstanding traditional (non-securitised) loans (L), liquidity ratio (LIQ), and real GDP (Y). The data for securitised loans issuance are taken from Securities Industry and Financial Markets Associations (SIFMA) whereas the data for policy rate (r), real GDP (Y), liquidity ratio (LIQ), and stock of traditional loans (L) are taken from Eurostat.

We employ a panel VAR model, using GMM estimation technique. The implementation of a VAR model is a common practice in the literature to study the effects of monetary policy. The Panel VAR approach that we adopt has the same advantages as the tradition VAR model used for time series analysis. The panel VAR model can be represented as follows:

(1)

(1) where

represents a vector of endogenous stationary variables for every country (i = 1, 2, … , T),

represents a vector of country-fixed effects, A

is a matrix polynomial in the lag operator (L),

is the contemporaneous matrix of the disturbances

.

It is well-known that fixed effect estimation in a cross-sectional time series (panel data) is inconsistent due to the presence of lags of dependent variable, resulting in a correlation between fixed effects and regressors (Nickell Citation1981). In the presence of a correlation between fixed effects and regressors, the standard mean-differencing leads to biased estimates (Holtz-Eakin, Newey, and Rosen Citation1988). Following Love and Zicchino (Citation2006), we overcome this problem by adopting the GMM procedure, using the forward mean-differencing — known as the Helmert transformation. This procedure involves the transformation of all variables into deviations from forward means, which preserves the orthogonality between transformed variables and lagged regressors. The lagged regressors are used as instruments in the GMM estimation to obtain unbiased coefficients. In the case of an overidentified model, we test for over-identifying restrictions using Hansen (Citation1982) J-statistic to ensure that the overidentifying restrictions are valid.

We obtain orthogonal impulse response functions by following a Cholesky decomposition. The ordering of our benchmark model is as follows:

Our variables-ordering is an attempt to capture the behaviour of modern central banks. Monetary policy authorities directly respond to output fluctuations to fulfil the objective of stable economic growth. Therefore, output shocks have contemporaneous effects on output whereas policy rates affect output with a lag. Monetary policy authorities do not respond directly to credit growth in the economy whereas the banking behaviour is directly affected by monetary policy decisions. Thus, monetary policy shocks contemporaneously affect the banking behaviour but banks behaviour in turn affects output and policy rates with a lag. Finally, our proxy of securitisation is directly affected by all variables whereas securitisation affects all variables in the system with a lag. The ordering of first two variables (i.e., real GDP and policy rates) is consistent with the vast empirical literature on the identification of monetary policy shocks in VAR models, where output precedes the policy rate (see, e.g., Christiano, Eichenbaum, and Evans Citation1996, Citation1999; Mojon and Peersman (Citation2001) amongst others). The ordering of last three variables is not addressed in the existing literature. In general, the results of Cholesky decomposition are usually sensitive to the ordering of variables, we therefore try different orders to test the sensitivity of our results, as will be discussed later.

Prior to the estimation of a VAR model, we apply several panel unit root tests. First, we apply a unit root test for heterogeneous panels proposed by Im, Pesaran, and Shin (Citation2003), known as IPS test. For completeness, we also apply Hadri (Citation2000), Levin, Lin, and Chu (Citation2002) (LLC), and Fisher-ADF test proposed by Maddala and Wu (Citation1999). If the variables are found to exhibit a unit root, we difference them and re-test them for a unit root. The purpose of this exercise is to ensure that all variables comprising our vector are stationary, which will result in a stationary dynamic VAR model. After performing a series of unit root tests, we estimate a panel while controlling for structural breaks.Footnote6

3.2. Empirical Results

shows the results of panel unit root tests. Overall, the results indicate that all variables except securitisation contain a unit root. The first-difference of the variables containing a unit root is found to be stationary. The construction of the proxy for securitisation is based on the flow of securitised loans, thus it is not surprising that this variable is stationary as the flow of loans (i.e., the first difference of the stock of loans) is stationary.

Table 1. Unit root tests.

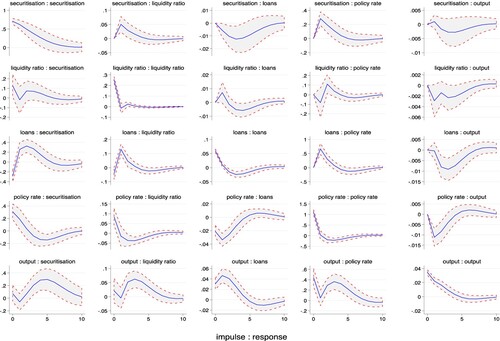

Having the variables tested for a unit root, we proceed to include stationary variables in our model and estimate a dynamic panel VAR model. We use several lag selection criteria, all indicating the inclusion of one lag in the estimation. shows the impulse responses obtained using a Cholesky decomposition at 90 per cent confidence interval. Our results should be interpreted with great caution and to understand the broader implications of our findings, one should take into account, the relevant evidence from the existing literature.

Figure 5. Impulse responses.

Note: Shock is defined as one standard deviation from the baseline in a variable.

We first focus on the interactions between monetary policy and the activities of the banking sector. An interesting result emerging from the impulse responses of our model is the response of securitisation to a monetary policy shock (see , row 4). In particular, a one standard deviation positive shock to monetary policy immediately increases securitisation activities, suggesting that banks increase credit intermediation and transfer risk in response to monetary policy tightening. Monetary policy shock also increases liquidity ratio which gives banks the ability to create loans without facing liquidity-risk pressures. In order to understand the broader implications of these results, it is important to consider the impact of securitisation on banks lending behaviour. There is empirical evidence in the case of US (Keys et al. Citation2010) and Euro area (Kara, Marques-Ibanez, and Ongena Citation2016) suggesting that those financial institutions which were aggressively involved in securitisation process also had a tendency of aggressively lowering their lending rates. Thus, our results combined with the existing evidence suggest that increased securitisation, apart from making monetary policy less effective, can also raise challenges for financial stability. Our findings are supportive of the conclusions drawn in Kashyap and Stein (Citation1995), Ashcraft (Citation2006), Altunbas, Gambacorta, and Marques-Ibanez (Citation2009, Citation2010), amongst others.

Focusing on the effect of monetary policy on non-securitised loans, our results indicate that the growth of traditional (non-securitised) loans declines in response to an increase in the interest rate. We can identify two important channels that can explain the reduction in growth of loans. First, an increase in the interest rates can reduce the issuance of new loans, leading to a reduction in growth of debt as implied by the credit channel. Second, an increase in interest rate can induce securitisation activity, which can reduce the growth of loans, i.e., when the banks securitise loans, they directly reduce the stock of outstanding loans on their balance sheets. The latter effect can be observed in our results where seuciritsation shock leads to a fall in growth of loans. This result is consistent with the findings of Nelson, Pinter, and Theodoridis (Citation2015), suggesting that contractionary monetary policy can lead to a reduction in the banks assets but an increase in the shadow banks assets due to an increase in securitisation activity. While our model is able to capture the second channel, it does not rule out the possibility of the existence of the credit channel. That is, our results do not necessarily imply that monetary policy is completely irrelevant, but suggest that increased securitisation has the potential of reducing the impact of monetary policy on credit growth due to various offsetting effects. Finally, in terms of the persistence of the shock, we can see that following a monetary policy shock, all variables — after experiencing an immediate impact — gradually rebound towards their pre-shock levels and stabilise as the effect of shock vanishes.

We now focus on the interaction between securitisation and other developments in the banking sector (see , column 1). A one standard deviation positive shock to the liquidity ratio has a positive impact on securitisation. A shock to securitisation activities in turn also raises liquidity ratio as discussed earlier. This result is consistent with the fundamental objective of securitisation, which involves the transformation of illiquid assets into liquid ones, thereby increasing liquidity in the system. Furthermore, our results suggest that a shock to the growth of loans has a positive effect on securitisation, as expected. It is well-known that an increase in the size of banks balance sheets has greatly strengthened their ability to securitise loans over the last few decades.

Focusing on the interactions between real economic growth and the banking sector, the evidence suggests that real economic growth increases securitisation as well as loans. This result simply implies that a rise in economic activity increases the activities in the financial markets, as well-documented in the empirical literature. Our findings in a broader context fit the theory of the endogenous money creation in a sense that the central bank has no direct control over credit supply. That is, banks can create and supply credit as long as there are interested parties who fulfil borrowing criteria (Wolfson Citation1996).Footnote7 The central bank can create temporary obstacles for credit creation through various tightening measures, however, in the long-run banks through innovations will create challenges for regulatory bodies.

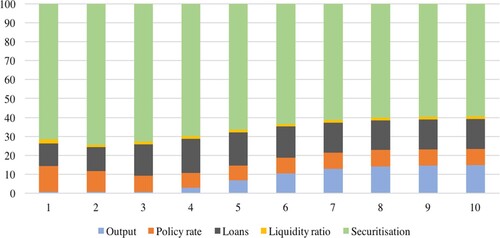

shows the forecast error variance decomposition of securitisation. The variation in securitisation activity in the model is largely explained by shocks to the growth of loans, interest rates, and output (apart from the shocks to securitisation itself). This implies that growing balance sheets (as a result of debt growth), monetary policy decisions, and financing needs of the economy are important indicators that can affect securitisation activities in the economy. Liquidity ratio seems to play a minor role in explaining the dynamics of securitisation.

Figure 6. Forecast error variance decomposition (FEVD).

3.2.1. Causality

reports the results of granger-causality, suggesting bidirectional causality in most cases. Focusing on securitisation, the evidence suggests that securitisation is caused by all variables in the model. There is also a causal feedback from securitisation to all variables with the exception of output. This implies securitisation mainly affects the financial activities in the system, which in turn can affect real side of the economy through various channels. Monetary policy and banking sector activities have bidirectional causality with the exception of monetary policy having no causal effect on liquidity ratio.

Table 2. Granger Causality.

The results of granger-causality are in line with the main results. In particular, we can see that one year lagged values of interest rate positively affect the current values of securitisation. Focusing on the relationship between securitisation and loans, we can see that one year lagged values of growth of loans increase current values of securitisation. Overall, these results lend support to the argument that securitisation activity can be triggered by both an increase in the banks balance sheets (as a result of debt accumulation) as well as an increase in the interest rates by monetary policy authorities. Finally, one year lagged values of securitisation activity have a negative impact on current values of loans, once again implying that securitisation process leads to a reduction in the outstanding debt as banks off-load their balance sheets in the process.

3.2.2. Robustness

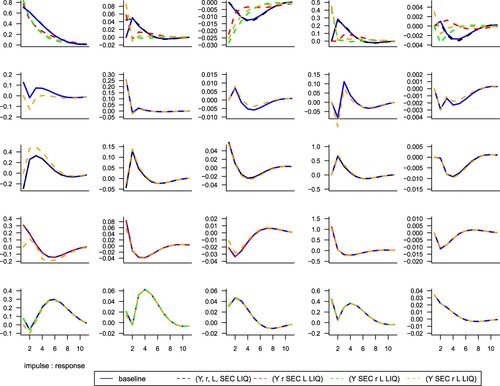

As discussed earlier, the results of VAR models are sensitive to the ordering of variables when Cholesky identification is used. We pay considerable attention to the model sensitivities that might emerge from our ordering assumptions. In this regard, we estimate the model using various orderings. In particular, we focus on the position of our variable of interest — securitisation, which is modelled in every possible position in the VAR matrix. It is natural to expect that the shapes of impulse responses would differ due to different constraints on contemporaneous effects as can be seen in the first row of . However, it is important to highlight that the results are quite robust to the ordering in a sense that they do not affect our overall conclusion in any fundamental way. This increases our confidence in the validity of the model.

Figure 7. Impulse responses.

4. Conclusion

The increasing importance of financial sector since the 1980s has been identified as ‘financialisation’ by several economists. One of the most important characteristics of financialisation phenomenon is the rapid growth of the financial innovations such as securitisation. The securitisation process transformed the banking model from ‘originate and hold’ to ‘originate and distribute’, i.e., selling loans and transforming illiquid assets into liquid ones. This process creates more liquidity which allows banks to expand their balance sheets (off-balance sheets activities), issuing more loans, lowering credit standards, taking more risk, and more importantly being more independent of central banks. The securitisation process naturally calls into question the effectiveness of monetary policy through its credit channel.

This paper re-examined the role of monetary policy and its transmission channels through the credit channel while focusing on securitisation. The evidence suggests that a contractionary monetary policy aimed at reducing credit, can induce securitisation activities. This in turn can increase liquidity ratio which empowers banks in expanding credit. The capability of banks to create their own liquidity in the financial market through shadow banking activities, makes them more powerful and independent of central bank action. Overall, our results imply that monetary policy is likely to be less effective for credit growth in the presence of such financial innovation.

The securitisation model by design entails greater financial risk. The credit-creation process, funnelled through securitisation processes, prioritise asset price booms over productive credit. As also argued by Keynes that when the goal of credit issuance is not to finance productive activities in the economy, but to create financial instruments, the practice is likely to be harmful for the economy.

There is a need for central banks to re-examine and redefine their role as a ‘banker’s bank’, taking into consideration the future developments in shadow banking and financial innovation in order to ensure financial stability. Traditionally, the role of central banks was limited to acting as a lender of last resort, which involved commitments to help illiquid but solvent banks. However, complex securitisation process has also changed this role; as described by Mehrling (Citation2012) central banks are also acting as a ‘dealer of last resort’ where they rescue the money market positions by which the banks fund themselves, so as to protect the interwoven circuits of borrowing and lending that support derivative and repurchase-agreement positions.

Acknowledgements

Open Access funding provided by the Qatar National Library. The authors would like to thank the two anonymous reviewers for their constructive feedback.

Disclosure Statement

No potential conflict of interest was reported by the author(s).

Notes

1 The developments in financial markets were not the primary concern of central banks until the 2008 crisis as will be discussed in Section Two.

2 see, e.g., Bernanke and Gertler (Citation1995).

3 For example, regarding the developments in financial markets, Jurgen Stark on 15 November 2007 in his speech at Bayerischer Bankenverband, Munich states,

… the private sector — in the case of the money market, the banks and investors that participate — should recognise their own responsibilities for making the market work. They cannot and should not rely on the authorities to ensure the efficiency of trading. Rather they have to create the appropriate conditions — transparency, honesty, trust — among themselves.

4 Also, see Minsky (Citation1992).

5 We use data from 1995–2015 for most countries; Netherlands and Belgium (sample: 1996–2015), Greece (sample: 2000–2015), Ireland (sample: 2001–2015), and Portugal (sample: 1998–2015). Note that the selection of panels and time is based on the availability of data.

6 We do so by using a dummy variable for 2008 crisis.

7 For a detailed discussion on the role of monetary policy when money is treated as endogenous, see, Lavoie (Citation1996), Chick and Dow (Citation2002), Arestis and Sawyer (Citation2006), Rochon (Citation2006), amongst others.

References

- Altunbas, Y., L. Gambacorta, and D. Marques-Ibanez. 2009. ‘Securitisation and the Bank Lending Channel.’ European Economic Review 53 (8): 996–1009.

- Altunbas, Y., L. Gambacorta, and D. Marques-Ibanez. 2010. ‘Does Monetary Policy Affect Bank Risk-taking?’ ECB Working Paper No. 1166.

- Arestis, P., and M. Sawyer. 2006. ‘The Nature and Role of Monetary Policy When Money Is Endogenous.’ Cambridge Journal of Economics 30 (6): 847–860.

- Ashcraft, A. B. 2006. ‘New Evidence on the Lending Channel.’ Journal of Money, Credit, and Banking 38 (3): 751–775.

- Aysun, U., and R. Hepp. 2011. ‘Securitization and the Balance Sheet Channel of Monetary Transmission.’ Journal of Banking & Finance 35 (8): 2111–2122.

- Baele, L., A. Ferrando, P. Hordahl, E. Krylova, and C. Monnet. 2004. ‘Measuring European Financial Integration.’ Oxford Review of Economic Policy 20 (4): 509–530.

- Bannier, C. E., and D. N. Hansel. 2008. ‘Determinants of European Banks’ Engagement in Loan Securitization.’ Deutsche Bank Discussion Paper Series 2: Banking and Financial Studies No 10/2008.

- Barradas, R. 2017. ‘Financialisation and Real Investment in the European Union: Beneficial or Prejudicial Effects?’ Review of Political Economy 29 (3): 376–413.

- Berger, A. N., and C. H. Bouwman. 2013. ‘How Does Capital Affect Bank Performance During Financial Crises?’ Journal of Financial Economics 109 (1): 146–176.

- Bernanke, B. 2007. ‘Globalization and Monetary Policy.’ Technical Report, Speech at the Fourth Economic Summit, Stanford Institute for Economic Policy Research, Stanford, CA.

- Bernanke, B. S., and M. Gertler. 1995. ‘Inside the Black Box: The Credit Channel of Monetary Policy Transmission.’ Journal of Economic Perspectives 9 (4): 27–48.

- Borio, C. 2014. ‘The Financial Cycle and Macroeconomics: What Have We Learnt?’ Journal of Banking & Finance 45: 182–198.

- Braga, J. C., G. C. de Oliveira, P. J. W. Wolf, A. W. A. Palludeto, and S. S. de Deos. 2017. ‘For a Political Economy of Financialization: Theory and Evidence.’ Economia e Sociedade 26 (SPE): 829–856.

- Chick, V., and S. Dow. 2002. ‘Monetary Policy with Endogenous Money and Liquidity Preference: A Nondualistic Treatment.’ Journal of Post Keynesian Economics 24 (4): 587–607.

- Christiano, L. J., M. Eichenbaum, and C. Evans. 1996. ‘The Effects of Monetary Policy Shocks: Some Evidence from the Flow of Funds.’ The Review of Economics and Statistics 78 (2): 16–34.

- Christiano, L. J., M. Eichenbaum, and C. L. Evans. 1999. ‘Monetary Policy Shocks: What Have We Learned and to What End?’ Handbook of Macroeconomics 1: 65–148.

- Coval, J., J. Jurek, and E. Stafford. 2009. ‘The Economics of Structured Finance.’ Journal of Economic Perspectives 23 (1): 3–25.

- Dell’Ariccia, G., D. Igan, and L. U. Laeven. 2012. ‘Credit Booms and Lending Standards: Evidence from the Subprime Mortgage Market.’ Journal of Money, Credit and Banking 44 (2–3): 367–384.

- Diamond, D. W. 1984. ‘Financial Intermediation and Delegated Monitoring.’ The Review of Economic Studies 51 (3): 393–414.

- Dymski, G. A. 2010. ‘Why the Subprime Crisis is Different: A Minskyian Approach.’ Cambridge Journal of Economics 34 (2): 239–255.

- Epstein, G. A. 2005. Financialization and the World Economy. Cheltenham: Edward Elgar.

- European Securitisation Forum. 2006. ‘European Securitisation a Resource Guide.’ NYU Stern.

- Gorton, G. B., and G. G. Pennacchi. 1995. ‘Banks and Loan Sales Marketing Nonmarketable Assets.’ Journal of Monetary Economics 35 (3): 389–411.

- Greenwood, R., and D. Scharfstein. 2013. ‘The Growth of Modern Finance.’ Journal of Economic Perspectives 27 (2): 3–28.

- Guttmann, R. 2017. ‘Financialization Revisited: The Rise and Fall of Finance-Led Capitalism.’ Economia e Sociedade 26 (SPE): 857–877.

- Hadri, K. 2000. ‘Testing for Stationarity in Heterogeneous Panel Data.’ The Econometrics Journal 3 (2): 148–161.

- Hansen, L. P. 1982. ‘Large Sample Properties of Generalized Method of Moments Estimators.’ Econometrica: Journal of the Econometric Society 50 (4): 1029–1054.

- Hein, E. 2012. ‘Financialization, Distribution, Capital Accumulation, and Productivity Growth in a Post-Kaleckian Model.’ Journal of Post Keynesian Economics 34 (39): 475–496.

- Holtz-Eakin, D., W. Newey, and H. S. Rosen. 1988. ‘Estimating Vector Autoregressions with Panel Data.’ Econometrica 56 (6):1371–1395.

- Im, K. S., M. H. Pesaran, and Y. Shin. 2003. ‘Testing for Unit Roots in Heterogeneous Panels.’ Journal of Econometrics 115 (1): 53–74.

- Kara, A., D. Marques-Ibanez, and S. Ongena. 2016. ‘Securitization and Lending Standards: Evidence from the European Wholesale Loan Market.’ Journal of Financial Stability 26: 107–127.

- Kashyap, A. K., and J. C. Stein. 1995. ‘The Impact of Monetary Policy on Bank Balance Sheets.’ Carnegie-Rochester Conference Series on Public Policy 42: 151–195.

- Keys, B. J., T. Mukherjee, A. Seru, and V. Vig. 2010. ‘Did Securitization Lead to Lax Screening? Evidence from Subprime Loans.’ The Quarterly Journal of Economics 125 (1): 307–362.

- Kotz, D. M. 2009. ‘The Financial and Economic Crisis of 2008: A Systemic Crisis of Neoliberal Capitalism.’ Review of Radical Political Economics 41 (3): 305–317.

- Kroszner, R. S., and P. E. Strahan. 2011. ‘Financial Regulatory Reform: Challenges Ahead.’ American Economic Review 101 (3): 242–246.

- Lapavitsas, C. 2010. Financialisation and Capitalist Accumulation: Structural Accounts of the Crisis of 2007–9. Research on Money and Finance Discussion Papers 16. London: SOAS.

- Lavoie, M. 1996. ‘Monetary Policy in an Economy with Endogenous Credit Money.’ In Money in Motion, edited by G. Deleplace and E. J. Nell. London: Macmillan..

- Lavoie, M. 2012. ‘Financialization, Neo-Liberalism, and Securitization.’ Journal of Post Keynesian Economics 35 (2): 215–233.

- Levin, A., C.-F. Lin, and C.-S. J. Chu. 2002. ‘Unit Root Tests in Panel Data: Asymptotic and Finite-Sample Properties.’ Journal of Econometrics 108 (1): 1–24.

- Levine, R. 1997. ‘Financial Development and Economic Growth: Views and Agenda.’ Journal of Economic Literature 35 (2):688–726.

- Love, I., and L. Zicchino. 2006. ‘Financial Development and Dynamic Investment Behavior: Evidence from Panel VAR.’ The Quarterly Review of Economics and Finance 46 (2): 190–210.

- Maddala, G. S., and S. Wu. 1999. ‘A Comparative Study of Unit Root Tests with Panel Data and a New Simple Test.’ Oxford Bulletin of Economics and Statistics 61 (S1): 631–652.

- Maddaloni, A., and J. L. Peydro. 2011. ‘Bank Risk-Taking, Securitization, Supervision, and Low Interest Rates: Evidence from the Euro-Area and the US Lending Standards.’ The Review of Financial Studies 24 (6): 2121–2165.

- Marques-Ibanez, D., and M. Scheicher. 2010. ‘Securitisation: Instruments and Implications.’ In The Oxford Handbook of Banking, edited by Allen Berger, Philip Molyneux and John O.S. Wilson. Oxford: Oxford University Press.

- Mehrling, P. 2012. ‘Three Principles for Market-Based Credit Regulation.’ American Economic Review 102 (3): 107–112.

- Minsky, H. P. 1957. ‘Central Banking and Money Market Changes.’ The Quarterly Journal of Economics 71 (2): 171–187.

- Minsky, H. P. 1980. ‘Between a Rock and a Hard Place: The Federal Reserve in 1980.’ Challenge 23 (2): 30–36.

- Minsky, H. P. 1992. ‘The Financial Instability Hypothesis.’ The Jerome Levy Economics Institute Working Paper (74), Annandale-On-Hudson.

- Minsky, H. P. 1996. ‘Uncertainty and the Institutional Structure of Capitalist Economies.’ Levy Working Paper No. 155.

- Minton, B., A. Sanders, and P. E. Strahan. 2004. ‘Securitization by Banks and Finance Companies: Efficient Financial Contracting or Regulatory Arbitrage?’ Technical Report, Ohio State University Working paper series.

- Mojon, B., and G. Peersman. 2001. ‘A VAR Description of the Effects of Monetary Policy in the Individual Countries of the Euro Area.’ ECB Working Paper No. 92.

- Nelson, B., G. Pinter, and K. Theodoridis. 2015. ‘Do Contractionary Monetary Policy Shocks Expand Shadow Banking?’ Journal of Applied Econometrics 33 (2): 198–211.

- Nickell, S. 1981. ‘Biases in Dynamic Models with Fixed Effects.’ Econometrica 49 (6): 1417–1426.

- Onaran, O., E. Stockhammer, and L. Grafl. 2011. ‘Financialisation, Income Distribution and Aggregate Demand in the USA.’ Cambridge Journal of Economics 35 (4): 637–661.

- Orhangazi, O. 2008. ‘Financialisation and Capital Accumulation in the Non-Financial Corporate Sector: A Theoretical and Empirical Investigation on the US Economy: 1973–2003.’ Cambridge Journal of Economics 32 (6): 863–886.

- Palley, T. I. 2013. ‘Financialization: What It Is and Why It Matters.’ In Financialization, edited By Thomas I. Palley. Springer.

- Pennacchi, G. G. 1988. ‘Loan Sales and the Cost of Bank Capital.’ The Journal of Finance 43 (2): 375–396.

- Rochon, L.-P. 2006. ‘Endogenous Money, Central Banks and the Banking System: Basil Moore and the Supply of Credit.’ In Complexity, Endogenous Money and Macroeconomic Theory: Essays in Honour of Basil J. Moore, edited by M. Setterfield. Elgar. Cheltenham, UK: Edward Elgar.

- Stockhammer, E. 2004. ‘Financialisation and the Slowdown of Accumulation.’ Cambridge Journal of Economics 28 (5): 719–741.

- Tori, D., and O. Onaran. 2018. ‘The Effects of Financialization on Investment: Evidence from Firm-Level Data for the UK.’ Cambridge Journal of Economics 42 (5): 1393–1416.

- Wolfson, M. H. 1996. ‘A Post Keynesian Theory of Credit Rationing.’ Journal of Post Keynesian Economics 18 (3): 443–470.

- Woodford, M. 2002. ‘Financial Market Efficiency and the Effectiveness of Monetary Policy.’ Federal Reserve Bank of New York Economic Policy Review 8 (1): 85–94.