ABSTRACT

Public banks are pervasive, with more than 900 worldwide, and powerful, having assets nearing $49 trillion. Yet they are too often perceived as static financial institutions, based on economic theories that begin from fixed notions of what it is to be a publicly owned bank. This has given rise to polarized debate wherein public banks are characterized as being either essentially good or bad. This is unrealistic and unhelpful as we seek ways to confront the crises of finance and of climate finance. We need instead to rethink public banks as dynamic and contested institutions within the public spheres of states. In this view, public ownership itself predetermines nothing but it does open up a particular public realm of possibilities. Change becomes possible and is a result of social forces making it so, if within the structural confines of gendered, racialized, and class-divided capitalist society. A dynamic theory of public banks provides a novel theoretical alternative and a practical pathway towards financing green and just transitions in the public interest.

1. Introduction

We need now to rethink public banks. There are over 900 of them worldwide with combined financial assets nearing $49 trillion dollars (McDonald, Marois, and Spronk Citation2021). These public commercial/retail, universal, and development banks operate at all levels, from the local and sub-national to the national, regional, and global scales. Over the last decade or so these public banks are resurgent, re-asserting their established capacity and expertise in order to confront recurrent financial crises and assume a catalytic role in tackling the crisis of climate finance (Marois Citation2021). They are, however, anything but new. Public banks have an institutional legacy going back more than six centuries to the first municipal banks founded in Barcelona and Genoa, followed by Venice, Naples, Amsterdam, and Hamburg. Since the late nineteenth century and with the consolidation of capitalism globally, public banks have acquired a diverse set of political, economic, and social functions. Yet contemporary thinking about public banks has failed to account for such heterogeneity. Instead, the idea of ‘public banks’ has been pushed into two opposing theoretical corners: an orthodox political view, typically negative, and a heterodox development view, often positive. Despite this apparent polarization, political and development views share common and foundational conceptual ground: in both views, the public ownership form of these banks logically precedes their institutional functions. Put otherwise, the functions of public banks (what they do) does not alter the meaning of being ‘public’ within either view. This matters because historical actions and future changes in how public banks function appear to be outside of and trivial to what public banks are in time- and place-bound contexts. Economic theory confines the actual practices of public banks and constrains our intellectual ability to be realistically critical or creatively optimistic. For those concerned with, for example, trying to find better means of financing a green and just transition to a sustainable and equitable future, these fixed and polarized conceptualizations present real barriers to securing sober alternatives in the public interest. We need now to be able to rethink public banks, warts and wonders alike, to innovatively direct their institutional capacity and transformative potential without the straight jackets of existing economic theory.

I argue that an alternative dynamic view of public banks enables us to rethink public banks within contemporary capitalism. A dynamic view does so without recourse to essentializing tropes of ‘public’ banks being meant to do this or essentially failing to achieve that. It is an anti-essentialist approach that exposes public banks to changing historical, social, political, and economic determinations. To do so, a dynamic view positions the socially contested institutional functions of public banks prior to their ownership form. Change becomes possible and is a result of social forces making it so, if within the structural confines of gendered, racialized, and class-divided capitalist society. This provides a novel and substantive theoretical alternative to orthodox political and heterodox development views.

2. Political and Development Views: Ownership Form Before Institutional Function

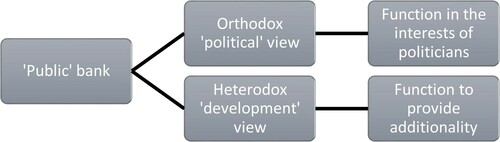

Despite otherwise contending worldviews on economic development, markets, and states in capitalism, the orthodox ‘political’ and heterodox ‘development’ views within economics share a common interpretive approach vis-à-vis public banks. Ownership form is foundational, logically coming before institutional functions in ways that fundamentally shape their otherwise polarized understanding of what public banks are and, importantly, what public banks are a priori meant to do. Orthodox and heterodox economic approaches, that is, tend to share a pre-social conceptualization of being publicly owned. Mine is not a necessarily disputed observation, nor is the political versus development divergence derived from ownership form unacknowledged within the economic literature on public banks. In one of the most widely cited studies on the subject, economists La Porta, Lopez-de-Silanes, and Shleifer (Citation2002, p. 67; my emphasis) write that the ‘[o]wnership of banks thus promotes the government’s goals in both the “development” and the “political” theories. … In both theories, the government finances projects that would not get privately financed. In the development theories, these projects are socially desirable. In the political theories, they are not.’ The line of thinking is unequivocal: ownership form logically precedes institutional function, even if the outcomes differ radically in terms of corruption or economic additionality (; elaborated below). It has also constituted a remarkably sticky narrative organizing the theory, evidence, and policy of public banks in economic development literature (see Barth, Caprio, and Levine Citation2006; Levy Yeyati, Micco, and Panizza Citation2007; World Bank Citation2012; Andrianova, Demetriades, and Shortland Citation2012; Marcelin and Mathur Citation2015; Scherrer Citation2017; Bircan and Saka Citation2018).

Figure 1. Political and development views: Ownership form precedes institutional function.

On the one hand, there is the orthodox ‘political’ view. Typically advanced by neoclassical economists and liberal political economists, the political view of public banks is characteristically negative. Adherents argue that ‘governments acquire control of enterprises and banks in order to provide employment, subsidies, and other benefits to supporters, who return the favor in the form of votes, political contributions, and bribes’ (La Porta, Lopez-de-Silanes, and Shleifer Citation2002, p. 266). There is no ambiguity, no room for divergence, and no possibility for change. Public enterprises, like public banks, are political firms that are ‘predestined for political uses’ and therefore ‘subject to political interference from politicians, special pressure or interest groups’ (Marcelin and Mathur Citation2015, p. 529). Political influence entails corruption, and this in turn generates interference in financial markets (Barth, Caprio, and Levine Citation2006; Demirgüç-Kunt and Servén Citation2010). Neoclassical case study and large-scale quantitative evidence affirm that public banks correlate with (and are sometimes said to cause) economic inefficiencies, under-development, and corruption (Caprio et al. Citation2004; Cull, Martinez Peria, and Verrier Citation2017). In this worldview, the public ownership of banks is seen as a deliberate political deviation meant to displace or preempt private ownership (Megginson Citation2005, p. 34).

Here the root problem with ‘bureaucrats as bankers’ is that of individual incentives (Shirley Citation1999). This is a theoretical proposition derived from timeless liberal conceptions of human nature (Demirgüç-Kunt and Servén Citation2010, p. 99):

As often the case in finance, incentive problems are at the root of this issue since bureaucrats do not face incentives designed to reward efficient resource allocation. Not only do government officials often lack the expertise to be effective managers, they also face conflicts of interest due to their desire to secure their political base and reward supporters, which often goes against efficient resource allocation.

On the other hand, there is the heterodox ‘development’ view. Typically advanced by Keynesian-inspired economists, the development view of public banks is characteristically positive. The ideas common to this view include public banks being able and willing to facilitate economic development in ways that private banks are unwilling or incapable of doing, particularly when it comes to longer-term investments and less profitable but no less socially-significant sectors and public goods (Gerschenkron Citation1962; Bennett and Sharpe Citation1980). In contrast to political views, however, very little is said on public ownership per se as a conceptual category. The nature of public ownership is often assumed or snuck in the back door, even though it remains the sine qua non of why public banks do what they do.

As with orthodox views, substantiating evidence is in no short supply within heterodoxy. Scholars argue that the ‘evidence that the prevalence of state ownership in the banking sector conspires against its ultimate development thus appears to be weaker than suggested by previous studies’ (Levy Yeyati, Micco, and Panizza Citation2007, pp. 237–8). Whereas political views attest to slow growth, development views demonstrate higher average growth rates (Andrianova, Demetriades, and Shortland Citation2012, p. 449). Heterodox studies even empirically challenge the bread and butter of political views, that is, endemic public bank corruption, arguing instead that the evidence of corruption is more inconclusive than political views lead us to believe (Frigerio and Vandone Citation2020) This is not to say public banks are incorruptible, for they are, if not any more so than a private bank. On top of this, a growing body of evidence details how public banks are effective counter-cyclical lenders capable of stabilizing increasingly unstable financial globalization processes and recurrent crises (Vidal, Marshall, and Correa Citation2011; Brei and Schclarek Citation2013; Griffith-Jones et al. Citation2018). These conclusions are now acknowledged by the World Bank (Citation2012) and IMF (Citation2020).

Here too public ownership remains foundational and logically prior. For example, development view advocates elaborate on what ‘public banks are expected to do a priori’, posed in contrast to orthodox views (Levy Yeyati, Micco, and Panizza Citation2007, pp. 223–24; cf. Griffith-Jones et al. Citation2018; Di John Citation2020). There are different expectations brought to bear, again based on a bank being owned publicly. Development views advocate that public banks should be most active where there are market failures and should do so without competing with the private sector. Public banks should operate where there is poor institutional development and do so to support private sector financial growth. Others push what public banks should do beyond market failures and financial gaps, to include regulating competitive markets, creating new markets, and functioning counter-cyclically at times of instability (often drawing more on Minsky’s financial fragility thesis) (Mazzucato and Penna Citation2016; Ribeiro de Mendonça and Deos Citation2017). There is an important shared commitment within heterodox development views, however, that logically and causally link public bank ownership to institutional functions, particularly to additionality (Skidelsky, Martin, and Westerlind Wigstrom Citation2011; Mazzucato Citation2015 [2013]). Additionality is described as the impact beyond that which would have occurred without a public bank acting or intervening, and it is often seen as functioning to crowd in private investment (Spratt and Ryan-Collins Citation2012, p. 1; Griffith-Jones et al. Citation2018). The essential meaning of being public is unequivocal. As Ribeiro de Mendonça and Deos (Citation2017, p. 24; my emphasis) specify, ‘the presence of institutions [public banks] with a logic of action that differs from that of the market is necessary in order to counteract destabilization’, in addition to assuming other roles in financial markets. It is this oft-unproblematized logic of action for public banks that also situates ownership form prior and as foundational to institutional functions in development views.

While critically engaging with how heterodox economists otherwise deal with credit policy and public banking, post-Keynesian economists Marshall and Rochon nonetheless reinforce fixed views on what public banks are meant to do by virtue of their ownership form. They write, for example, that ‘public banks are not subject to the discipline of the market’ and that they ‘do not operate for profit’ (Citation2019, pp. 65; 67). The intent is to suggest public banks are more open to functioning differently than private corporate banks, which are compelled to maximize returns, but the wording mirrors established patterns within the literature. In doing so it obscures that public banks in countries as diverse as Turkey, Canada, and Costa Rica have been made subject to market forces and that others in political jurisdictions as different as North Dakota and the Nordic region of Europe not only operate for profit but regularly reward their government shareholders with pay-outs (Marois Citation2021). Once you assign a variable function to public banks as an invariable feature, it is soon belied by cases that do not conform to the model but are yet ‘public’ banks. They are simply public banks made differently within the public sphere, a point economic theory has had trouble capturing.

That said, unlike in orthodox political views there is in heterodox development views a liveliness to debate and analytical room for conceptual innovation (see Scherrer Citation2017; Butzbach, Rotondo, and Desiato Citation2020; Mazzucato Citation2018). Marshall and Rochon, for example, recognize that public banks ‘are subject to the discipline of the voter’, signaling that the functioning of public banks ‘should be left to society’s discretion, voiced through a democratic process’, in turn pointing towards ‘constructing’ public banks around ‘probity, not profit’ (Marshall and Rochon Citation2019, pp. 65; 71). This suggests that society has a say in how a public bank functions and, ultimately, in institutional change (a point I return to shortly). Yet most Keynesian scholars of public banks have yet to walk through that door conceptually. The issue is not in what they see public banks doing, for indeed there are cases of public banks undertaking institutional functions just as elaborated in development approaches. It is the why that remains problematic, insofar as why a public bank does (or is meant to do) this or that often, implicitly or explicitly, boils down to it being a ‘public’ bank. The inner, contested, and ever-evolving social forces and power relations within global capitalism that motivate the varied institutional functions of public banks rarely receive explicit conceptual treatment.

This stumbling block derives from long-standing heterodox commitments to advocating for a greater role for the ‘machinery of government’ in stabilizing inherently unstable and uneven capitalist development via extra-market coordination mechanisms, including public banks (Gerschenkron Citation1962; Shonfield Citation1969; Minsky Citation2008 [1986]). As John Maynard Keynes wrote, ‘[t]he important thing for government is not to do things which individuals are doing already, and to do them a little better or a little worse; but to do those things which at present are not done at all.’ (Citation1926, p. 46; emphasis added) Keynes’ position on the proper role of government in capitalist economies has had a decided influence on the development view of public banks, anchoring ownership form prior to institutional function. It is this ‘extra-market coordination’ commitment that Joseph Stiglitz refers to when arguing that there ‘exist forms of government intervention that will not only make these [financial] markets function better but will also improve the performance of the economy’ (Citation1994, p. 20). Public banks, by virtue of being public, are meant to provide market stability, filling and correcting for market failures and investor reticence, and for generating positive externalities (cf. Xu, Ren, and Wu Citation2019, pp. 6–8).

Again, the issue is not that public banks do not engage in these functions. They do. Indeed, the heterodox and institutional literature on public banks has certainly bested orthodoxy in capturing operational diversity and historical variegations across time and place (von Mettenheim and Del Tedesco Lins Citation2008; Mettenheim and Butzbach Citation2017; Scherrer Citation2017; Griffith-Jones et al. Citation2018; Ray, Gallagher, and Sanborn Citation2020). Heterodox scholars, too, are leveraging traditional ideas for novel ends, driving new debate around public banks and patient public finance as being more innovative and able to take on government missions in order to drive forward public purpose (Mazzucato Citation2018). Importantly, there is a strong underlying normative public interest commitment to public banks funding socially significant but low-return public good projects, especially in infrastructure (Griffith-Jones et al. Citation2018). Where I diverge is in connecting any such functions or any such public interest orientation to public ownership in and of itself. I see being public as rather more indeterminate and contested, being made and remade by class-divided social forces in capitalism. In short, more needs to be done to historicize our theories of public banks rather than continuing to let theory over-determine diverse institutional histories.

3. An Alternative Dynamic View: Institutional Function Before Ownership Form

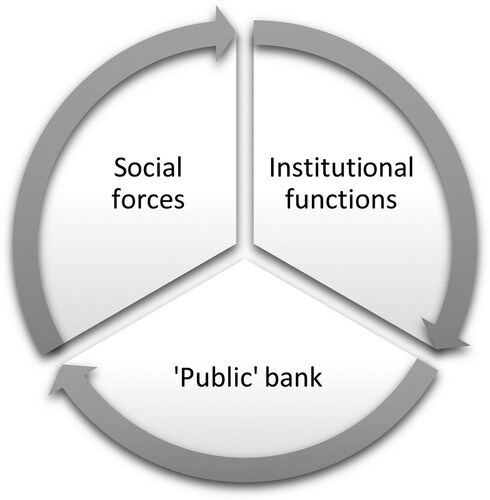

Orthodox political and heterodox development views of public banks are stuck in fixed and opposing corners. To rethink public banks there is thus the need to shift the terrain of debate and to elaborate an alternative conceptual framework capable of making place- and time-bound context matter to the meanings of public banks. This can only be broached by first jettisoning the perceived need to resolve the ultimate benefits, or not, of public banks in capitalist development. An alternative approach reverses causality, so that what people make public banks do matters. This means positioning institutional functions, which are socially contested, as logically prior to ownership form. In this conceptualization, social forces shape and reshape the institutional functions of public banks, which in turn recurrently change the meaning of being a public bank in time and place (). In turn, the evolving meaning of a public bank will again inform the struggles and strategies of social forces as they seek to shape and reshape what it is that a public bank does, how it functions, and for whom. This again leads to an evolution in the meaning of being a public bank, endlessly making and remaking a public bank in time- and place-bound contexts. This is the foundation of an alternative ‘dynamic’ view of public banks.

Figure 2. Dynamic view: Evolving because socially contested.

The historical, empirical, and case study evidence on public banks and financial institutions informing this alternative ‘function before form’ approach to public banks has been developed elsewhere (Marois and Güngen Citation2016; Ho and Marois Citation2019; McDonald, Marois, and Barrowclough Citation2020; Marois Citation2021). My purpose here is limited to setting out the conceptual framework of a dynamic view, drawing on historical institutional and materialist political economy. This involves, first and foremost, pulling the ‘public’ in public banks back into the historical specificity and structural influences of capitalist social reproduction that affect the actions and intentions of social forces, individual and collective. A dynamic view then interprets these institutions from the bottom up: public banks are first theorized as institutions in the public spheres of states within global financialized capitalism. This allows us to connect the shifting strategies and interests of social forces to the institutional functions and reproduction of public banks within the confines of capitalism.

At first glance, then, public banks are institutions. Institutions represent, crystallize, and perform patterns of behavior, customs, laws, rules, and norms in society. They are often complex in their histories, contemporary make up, and underlying power relations. Institutions, at one level of understanding, are entities onto themselves, but they are never so independently of all else. Institutions develop and evolve within a societal whole, acted upon and acting onto larger and smaller scales of existence. This leads one scholar to see institutions as ‘endogenously shaped, context-determined social rules’ (Ho Citation2017, pp. 9–10). Moreover, institutions are historical and dynamic because they are ‘the resultant of social actors’ and economic agents’ interaction’ (Ho Citation2013, pp. 1091–92; emphasis added). Put otherwise, individual and collective agents make and remake institutions, such that they are inevitably time- and place-bound entities (cf. Lefebvre Citation2016 [Citation1972], p. 63). While we can identify and speak of specific institutional entities (like individual public banking institutions), these are inherently relational entities reproduced within the wider totality of capitalist social reproduction (Hanieh Citation2018, p. 15).

Public banking institutions are connected to the wider totality first through the public sphere. As employed here, I define the public sphere as that space within nation states where governing authorities can (but not necessarily do) exercise power, control, influence, and privilege over public institutions and discourses. It is similar to the ‘public sector’, if more expansive. It is in and through the public sphere that governing authorities can shape what public banks do, how they function, and for whom – sometimes directly and sometimes more distantly. At the same time, by seeking to influence governing authorities and/or by holding formal decision-making power within public banks’ governance structures themselves, social forces can also influence and shape public banks through the public sphere. This does not occur in predetermined ways or free of contending power relationships. Social forces, be they individual or collective and acting in the public or private interest, can work to sway public banks to function and operate according to reproductive logics and rationalities different than those of private banks exposed more directly to market competition. This is why we see that public banks have acquired functions seemingly unique to public banks (but which are not themselves derived from being publicly owned). However, it is equally the case that through the public sphere social forces can also make public banks function as-if they were private profit-seeking banks (that is, ‘corporatised’), strategically made to operate according to market-oriented and financialized performance indicators in the private interest (Marois Citation2012; cf. Shirley Citation1999; McDonald Citation2016). The public sphere is a field of potentiality in which social forces act and react rather than a source or site of structural determinations.

To shed the ontological surety of being this or that by virtue of being a public institution is not to suggest that the public sphere of a state may not provide potential shielding from competitive market and capitalist accumulation imperatives. It can and does. For public banks, such shielding can be quite direct. Public law can clearly define public banks’ operations and responsibilities while legally binding mandates and missions can set their orientation and pace of operations. Public guarantees and financial resources can release public banks from unmediated dependence on fast and fickle global financial markets. Democratic governance and popular representative structures can facilitate a credible public interest operating ethos. Yet so too can public sphere shielding be rather more indirect or even effectively non-existent. When public banks are legally corporatised and operationally financialized, specific social forces have made them operate according to market imperatives regardless of the public sphere. For this reason, as and when public banks are made and remade it is because they are pulled between contending public or private interests acting in and through the public sphere.

The public sphere, in turn, is internally connected to the state and class-divided society (and hence, to racialized and gendered power relations). States are larger and more complex than the public sphere, but they are no less evolving institutional social formations that within capitalism condense and crystallize historically specific, contested, and class-divided power relations in society (Jessop Citation1990; Harvey Citation2010, pp. 55–6). States are therefore not independent of capitalist markets and accumulation imperatives but interconnected through wider power relations and patterns of social reproduction (Poulantzas Citation2000 [Citation1978]). With the global consolidation of capitalism over the last century or so, states have evolved as integral to capital accumulation, that is, as the one institution capitalism cannot do without (Meiksins Wood Citation2002). Yet states, as complex institutional entities, are not smoothly determined by capitalist reproduction and accumulation as here too contentious social forces struggle over the meanings of states (Lefebvre Citation2016[Citation1972], p. 130). Capitalist states in class-divided, racialized, and gendered society are thus institutionalized social compromises that balance, to greater and lesser degrees, contradictory capital accumulation and social reproduction imperatives. States and their public spheres are therefore strategic sites of social struggles (which is one reason why privatization was perhaps the vanguard strategy of early neoliberal reformers around the world). Class-divided, gendered, and racialized forms of power, privilege, and exploitation find their way into public financial and banking institutions and how they function at different times and in different places (Dymski Citation2009; Roberts Citation2015; McNally Citation2020). Historically and intuitively we know this to be the case, yet to date, economic banking theory has failed to capture the reality.

In historical materialist worldviews global capitalism and capitalist social relations impart a ‘particular logic upon people and make a particular form of rationality plausible to them – a pressure that takes effect behind the backs of the subjects’ (Nachtwey and ten Brink Citation2008, p. 45). The public sphere, states, and society are all impacted and influenced, if not determined, by this shadow of capitalism (Jessop Citation2016). Moreover, contemporary global capitalism has taken on a particularly finance-based or financialized shadow (Lapavitsas Citation2009; Marois Citation2012; Chesnais Citation2016). My purpose in raising the specter of global financialized capitalism is neither to narrate its processes nor to scan the mounting definitional and conceptual debates (see Christophers Citation2015). Rather, it is to recognize as ontologically significant that public banks in public spheres in states are likewise located in and affected by (and in turn affect) this wider structural context (cf. Scherrer Citation2017). It is a feature of historical materialist scholarship that finance and its institutions be historicized within the totality of capitalism and its class-based exploitative structures (dos Santos Citation2009; Hilferding Citation2006 [Citation1981]; Harvey Citation2010; see Marois Citation2012, pp. 24–35). To be sure, public banks and their functions in society have long pre-dated capitalism (Hudson Citation2018). Yet public banks have thrived and evolved within capitalism, even persisting through the less-than-amenable conditions of neoliberalism and financialization (Marois Citation2021). What a dynamic view can illuminate is how private investors and neoliberal advocates are now seeking to bend public banks to ensuring their own accumulation ends as a strategic response to the crises of finance and of climate finance (also see the ‘Wall Street Consensus’ in Dafermos, Gabor, and Michell Citation2021). As an ontological and epistemological premise of analysis, individual and collective agencies shape the world around us, but rarely, to paraphrase Engels (Citation1959, p. 230), in the conditions of our own choosing and not always as intended. So when I speak of the shadow of capitalism over public banks what I refer to is the structural power and organizing logic of exploitative capitalist social reproduction processes, which represent the conditions of institutional existence and reproduction that can be differentially leveraged by contending public and private interests (cf. Lefebvre Citation2016 [Citation1972]; Palermo Citation2019).

To rethink public banks dynamically is to move reflexively from and between the institution, the public sphere, the state, and global financialized capitalism as interconnected scales of reproductive existence, power, and privilege. Public banks are exposed to influence as far as the bounds of global capitalism extend while at the same moment enclosed within a hierarchy of internal relations and boundaries. Far from being this or that by virtue of being publicly owned, public banks emerge in thought and practice as complex hybridizations of social struggles and power relations that seldom correspond to any idealized notion or intended outcome. Put otherwise, public ownership itself predetermines nothing. It does, however, open a particular public realm of possibilities. In this, we can think of public banks as dynamic and socially constructed and reconstructed institutionalized social relations that reflect historically specific relations of power and reproduction between banks, firms, states, and contentious individual and collective social forces (cf. Marois Citation2012, p. 29).

It this way a dynamic view meaningfully and logically positions institutional function prior to ownership form. While couched in historical materialist terms, the positioning of function before form draws on a related institutional political economy literature, notably that of scholar Peter Ho. Ho argues that by focusing on historical institutional ‘functions’ we need not rely on timeless and essentialized notions of ‘ownership’ form. In this line of reasoning, public and private institutions are not essentially good or bad things, but socially constituted (Ho Citation2013, Citation2016). Where and when institutions persist, it is by virtue of context-specific factors, prevailing as ‘the reflection of actors’ cumulative perceptions of endogenously emerged institutions as a common arrangement’ (Ho Citation2016, p. 1125). Institutions endure not for idealized notions of public ownership but for complex and often contradictory reasons connected to what they do, how they function, and for whom (Ho Citation2020; Marois Citation2021). In terms of public banks, this leads to a novel understanding and to unique insights. Public ownership bestows no essential or ultimate purpose on a bank. Public banks’ functions are instead subject to the pull of public and private interests in class-divided society, each struggling to shape for whom the bank predominantly functions.

A dynamic view allows us to rethink public banks as irreducible to the ‘public’ ownership form yet subject to struggle. Ownership by a government, public authority, or other public enterprise becomes but one way of positioning a bank within the public sphere. Ownership, however, is also not the only way.Footnote2 Having a binding public mandate and mission, being operated under public law, being subject to consequential democratic public representation and control mechanisms, and variations therein can likewise position a bank within the public sphere as a public bank. This then becomes the first dimension of a public bank, namely, being located within the public sphere (if not necessarily being ‘publicly’ owned). A dynamic view sets out three additional dimensions of what constitutes a public bank (see Marois Citation2021). A second dimension of a public bank is that it also performs financial intermediation and banking functions but without an innate purpose or policy orientation (reflected in the fact of their multiple mandates and missions). A third dimension is that a public bank can function in both public and private interests. A final dimension of a public bank is that it persists as a credible, contested, and evolving institution.

These four dimensions of a public bank open up research to a far wider swath of historical and empirical determinations than allowed for in existing orthodox political and heterodox development views, which assign a priori meanings and orientations to public banks by virtue of ownership. By contrast, these four dimensions are mean to capture their diverse histories and indeterminant futures by setting public banks in capitalist society and the class-divided struggles endemic to it without pre-determining an essential or ultimate end. The consequence of a dynamic view is neither politically vacuous nor normatively agnostic. Precisely the opposite. By eschewing a pre-social and ultimate end, public banks become (as in fact they are) dynamic resultants of contentious struggles within capitalism. As historical and contemporary case study research attests, public banks are made and re-made in many ways, acquiring and casting off multiple institutional functions depending on how contentious social forces struggle to make the bank within states with the shadow of capitalism.

4. Conclusion, or Why It Matters

Public banks are enjoying nothing less than a modern-day resurgence within neoliberalism and financialisation. Decades of bank privatization advocacy have quieted as public banks have proven integral to smoothing out the 2008–09 global financial crisis and in catalyzing now desperately needed low-carbon and green transition financial investments (not to mention helping to overcome the crisis of Covid-19) (Griffith-Jones et al. Citation2018; Mazzucato and Semieniuk Citation2018; UNCTAD Citation2019; Xu, Ren, and Wu Citation2019; McDonald, Marois, and Barrowclough Citation2020; McDonald, Marois, and Spronk Citation2021; Marois Citation2021). Yet without public banks that can be democratically commanded to function in the public interest, there is no hope of sustainable and equitable development, let alone green and just transitions for people and planet, as financial investors maneuver to control the functions of public banks for private ends. For this reason, it matters how we think about public banks. A dynamic view opens the realm of the possible public interest while being realistic about the social forces at play and struggles to come.

By contrast, orthodox political views are still desperate to constrain the potential of public banks and to gear what public banks currently do to supporting private interests and endless capital accumulation. This is the core message of the World Bank’s Maximizing Finance for Development agenda and the United Nations’ Finance for Sustainable Development strategy (IMF/World Bank Citation2015; Badré Citation2018; UN IATF Citation2019; cf. Dafermos, Gabor, and Michell Citation2021). In this new neoliberal narrative, public banks must only wrap projects in public guarantees, bending themselves to underwriting acceptable levels of private returns by socializing their risks.

Heterodox development views hold more diverse aspirations for public banks. There are calls for patient public finance and public development banks to green investments and to launch a global green new deal (Mazzucato and McPherson Citation2018). Others emphasize the necessity of building up public banking capacity and influence to confront the overwhelming power of private finance and global financialization (Beitel Citation2016; Marshall and Rochon Citation2019; Brown Citation2019). Too often, however, heterodox approaches graft specific roles and sets of expectations onto public banks, asserting a very particular vision of public banks’ ‘reasons to be’ (notably, variations of ‘additionality’). The problem is not one of imagining or advocating progressive roles and responsibilities for public banks. No. Rather, the problem resides in granting otherwise normative and contestable aspirations (which are indeed an indispensable part of being a social and political being!) a timeless status that in turn seemingly bestows fundamental meaning on a bank by virtue of it being ‘public’. Far from catalyzing positive change this can overly constrain possibilities, obscure pitfalls, and undermine meaningful democratization. What good is it to command a representative and democratic say over public banks if what they are meant to do is already predetermined? Little, I suggest. Similarly, it is a grave strategic mistake to assume that, by virtue of being publicly owned, any institution, let alone public banks, will advance a green and just transition for people and planet without supportive and motivated social forces actively shaping the institution and holding it accountable to the democratic public interest. At a time when public banks are resurgent, it is a blunder of colossal proportions to either dismiss the creative energies of pro-public social forces or to underestimate the structural power of private interests to bend public banks to their own accumulation ends. Hence the practical need to rethink public banks.

An alternative dynamic view thus matters because in rethinking public banks it internalizes struggle and acknowledges the normative orientations of contending social forces. It looks to the historical and material conditions of public banks’ reproduction. By doing so, a dynamic view allows us to see the operational contradictions of public banks and understand the relationships of power and politics at play within class-divided, gendered, and racialized capitalist society. In this way contending public and private interests can be brought into the light as we act on the possibilities for change. It follows that a dynamic view does not rest upon any conceptual surety that a public bank, by virtue of being public, is meant to do this or that. Nor does a dynamic view blithely right off the catalytic and public interest potential of public banks merely because they are deemed ultimately corrupt and essentially inefficient. Instead, a dynamic view concedes that this cannot be known in advance. Rather, how public banks function and for whom are the results of historical social forces acting within the shadow of capitalism. The functions that public banks do inform the evolving meaning of being a public bank. For those social forces concerned with a green and just future for people and planet, this historically and evidence-based conceptualization opens the possibility, if never the necessity, of public banks being made to respond in the public interest. It also accepts that public banks can be made to privilege environmentally destructive and decidedly unjust ends. What a public bank is thus ultimately depends, and that, in the final analysis, is what is most liberating about a dynamic view of public banks and why it matters.

Acknowledgement

I would like to express my gratitude to the reviewers. It is a true pleasure to have readers thoughtfully engage with your work with an eye to improving its quality and clarity. The feedback received was enormously helpful, even if my revisions do not fully give justice to their inputs.

Disclosure Statement

No potential conflict of interest was reported by the author(s).

Notes

2 Again, to challenge the ontological primacy of legal ownership is not to dismiss its importance. Without determining its meaning, ownership can position a bank within the public sphere. Moreover, formal ownership is often by default one of the only ways to empirically measure levels of public bank numbers and assets in existing databases, notably in Orbis BankFocus. A dynamic view offers a less quantitatively rigid but more qualitatively accurate determination that builds on scholarship already concerned with alternative banks and interested in the complex and multiple forms by which other institutions are in fact ‘public’ institutions, be it by full or partial state or municipal ownership, worker-owned, or producer and consumer cooperatives (see Cumbers Citation2012; Butzbach and von Mettenheim Citation2014; Hanna Citation2018). It too recognizes the acknowledged limits to analysis reliant on pure ‘ownership’ categorizations taken in the absence of understanding effective ‘control’ over a bank (Butzbach, Rotondo, and Desiato Citation2020).

References

- Andrianova, S., P. Demetriades, and A. Shortland. 2012. ‘Government Ownership of Banks, Institutions and Economic Growth.’ Economica 79: 449–469.

- Badré, B. 2018. Can Finance Save the World? Regaining Power Over Money to Serve the Common Good. Oakland, CA: Berrett-Koehler Publishers.

- Barth, J. R., Jr., G. Caprio, and R. Levine. 2006. Rethinking Bank Regulation: Till Angels Govern. New York: Cambridge University Press.

- Beitel, K. 2016. The Municipal Public Bank: Regulatory Compliance, Capitalization, Liquidity, and Risk. Roosevelt Institute. www.rooseveltinstitute.org.

- Bennett, D., and K. Sharpe. 1980. ‘The State as Banker and Entrepreneur: The Last-Resort Character of the Mexican State’s Economic Intervention, 1917–76.' Comparative Politics 12 (2): 165–189.

- Bircan, Ç, and O. Saka. 2018. ‘Lending Cycles and Real Outcomes: Costs of Political Misalignment.’ LSE ‘Europe in Question’ Discussion Paper Series. LEQS Paper No. 139/2018. London: London School of Economics.

- Brei, M., and A. Schclarek. 2013. ‘Public Bank Lending in Times of Crisis.’ Journal of Financial Stability 9 (4): 820–830.

- Brown, E. 2019. Banking on the People: Democratizing Money in the Digital Age. Washington: The Democracy Collaborative. https://democracycollaborative.org/.

- Butzbach, O., G. Rotondo, and T. Desiato. 2020. ‘Can Banks Be Owned?’ Accounting, Economics, and Law: A Convivium 10 (1): 1–21.

- Butzbach, O., and K. von Mettenheim, eds. 2014. Alternative Banking and Financial Crisis. London: Pickering & Chatto.

- Calomiris, C. W., and S. Haber. 2014. Fragile by Design: Banking Crises, Scarce Credit, and Political Bargains. Princeton: Princeton University Press.

- Caprio, G., J. L. Fiechter, R. E. Litan, and M. Pomerleano, eds. 2004. The Future of State-Owned Financial Institutions. Washington: Brookings Institution Press.

- Chesnais, F. 2016. Finance Capital Today: Corporations and Banks in the Lasting Global Slump. Boston, MA: Brill.

- Christophers, B. 2015. ‘The Limits to Financialization.’ Dialogues in Human Geography 5 (2): 183–200.

- Cull, R., M. S. Martinez Peria, and J. Verrier. 2017. ‘Bank Ownership: Trends and Implications.’ IMF Working Paper. WP/17/60. Washington: International Monetary Fund.

- Cumbers, A. 2012. Reclaiming Public Ownership: Making Space for Economic Democracy. London: Zed Books.

- Dafermos, Y., D. Gabor, and J. Michell. 2021. ‘The Wall Street Consensus in Pandemic Times: What Does it Mean for Climate-Aligned Development?’ Canadian Journal of Development Studies/Revue canadienne d'études du développement. doi:https://doi.org/10.1080/02255189.2020.1865137.

- Demirgüç-Kunt, A., and L. Servén. 2010. ‘Are All the Sacred Cows Dead? Implications of the Financial Crisis for Macro- and Financial Policies.’ The World Bank Research Observer 25 (1): 91–124.

- Di John, J. 2020. ‘The Political Economy of Development Banking.’ In The Oxford Handbook of Industrial Policy, edited by A. Oqubay, C. Cramer, H.-J. Chang, and R. Kozul-Wright. Oxford: Oxford University Press.

- dos Santos, P. 2009. ‘On the Content of Banking in Contemporary Capitalism.’ Historical Materialism 17 (2): 180–213.

- Dymski, G. 2009. ‘Racial Exclusion and the Political Economy of the Subprime Crisis.’ Historical Materialism 17 (2): 149–179.

- Engels, F. 1959 [1888]. ‘Ludwig Feuerbach and the End of Classical German Philosophy.’ In Marx and Engels: Basic Writings on Politics and Philosophy, edited by L. S. Feuer, 195–242. New York: Anchor Books.

- Friedman, M. 1962. Capitalism and Freedom. Chicago: University of Chicago Press.

- Frigerio, M., and D. Vandone. 2020. ‘European Development Banks and the Political Cycle.’ European Journal of Political Economy 62 (March): 101852. doi:https://doi.org/10.1016/j.ejpoleco.2019.101852.

- Gerschenkron, A. 1962. Economic Backwardness in Historical Perspective. Boston: Harvard University Press.

- Griffith-Jones, S., J. A. Ocampo, F. Rezende, A. Schclarek, and M. Brei. 2018. ‘The Future of National Development Banks.’ In The Future of National Development Banks, edited by S. Griffith-Jones, and J. A. Ocampo, 1–36. Cambridge: Cambridge University Press.

- Hanieh, A. 2018. Money, Markets, and Monarchies: The Gulf Cooperation Council and the Political Economy of the Contemporary Middle East. Cambridge: Cambridge University Press.

- Hanna, T. M. 2018. Our Common Wealth: The Return of Public Ownership in the United States. Manchester: Manchester University Press.

- Harvey, D. 2010. The Enigma of Capital and the Crises of Capitalism. London: Profile Books.

- Hayek, F. A. 1984 [1967]. ‘The Principles of a Liberal Social Order.’ In The Essence of Hayek, edited by C. Nishiyama, and K. R. Leube, 363–381. Stanford, CA: Hoover Institution Press.

- Hilferding, R. 2006 [1981]. Finance Capital: A Study of the Latest Phase of Capitalist Development. London: Routledge.

- Ho, P. 2013. ‘In Defense of Endogenous, Spontaneously Ordered Development: Institutional Functionalism and Chinese Property Rights.’ Journal of Peasant Studies 40 (6): 1087–1118.

- Ho, P. 2016. ‘An Endogenous Theory of Property Rights: Opening the Black box of Institutions.’ The Journal of Peasant Studies 43 (6): 1121–1144.

- Ho, P. 2017. Unmaking China's Development: The Function and Credibility of Institutions. Cambridge: Cambridge University Press.

- Ho, P. 2020. ‘The Credibility of (in)Formality: Or, the Irrelevance of Institutional Form in Judging Performance.’ Cities 99 (April): 102609. doi:https://doi.org/10.1016/j.cities.2020.102609.

- Ho, S., and T. Marois. 2019. ‘China’s Asset Management Companies as State Spatial–Temporal Strategy.’ The China Quarterly 239: 728–751.

- Hudson, M. 2018. … and Forgive Them Their Debts: Lending, Foreclosure, and Redemption from Bronze Age to the Jubilee Year. Dresden, Germany: ILSET-Verlag.

- IMF. 2020. Fiscal Monitor: Policies to Support People During the COVID-19 Pandemic. Washington: International Monetary Fund.

- IMF/World Bank. 2015. From Billions to Trillions: Transforming Development Finance Post-2015 Financing for Development: Multilateral Development Finance. Development Committee, Joint Ministerial Committee of the Boards of Governors of the Bank and the Fund on the Transfer of Real Resources to Developing Countries. DC2015-0002. www.worldbank.org.

- Jessop, B. 1990. State Theory: Putting the Capitalist State in Its Place. Cambridge, UK: Polity Press.

- Jessop, B. 2016. ‘Territory, Politics, Governance and Multispatial Metagovernance.’ Territory, Politics, Governance 4 (1): 8–32.

- Keynes, J. M. 1926. The End of Laissez-Faire. London: I. and V. Woolf.

- Lapavitsas, C. 2009. ‘Financialised Capitalism: Crisis and Financial Expropriation.’ Historical Materialism 17 (2): 114–148.

- La Porta, R., F. Lopez-de-Silanes, and A. Shleifer. 2002. ‘Government Ownership of Banks.’ The Journal of Finance 57 (1): 265–301.

- Lefebvre, H. 2016 [1972]. Marxist Thought and the City. Trans. by R. Bononno. Foreword by S. Elden. Minneapolis: University of Minnesota Press.

- Levy Yeyati, E., A. Micco, and U. Panizza. 2007. ‘A Reappraisal of State-Owned Banks.’ Economia (pontificia Universidad Catolica Del Peru. Departamento De Economia) 7 (2): 209–247.

- Marcelin, I., and I. Mathur. 2015. ‘Privatization, Financial Development, Property Rights and Growth.’ Journal of Banking & Finance 50: 528–546.

- Marois, T. 2012. States, Banks, and Crisis: Emerging Finance Capitalism in Mexico and Turkey. Cheltenham, UK: Edward Elgar Publishing.

- Marois, T. 2021. Public Banks: Decarbonisation, Definancialisation, and Democratisation. Cambridge: Cambridge University Press.

- Marois, T., and A. R. Güngen. 2016. ‘Credibility and Class in the Evolution of Public Banks: The Case of Turkey.’ Journal of Peasant Studies 43 (6): 1285–1309.

- Marshall, W. C., and L.-P. Rochon. 2019. ‘Public Banking and Post-Keynesian Economic Theory.’ International Journal of Political Economy 48 (1): 60–75.

- Mazzucato, M. 2015 [2013]. The Entrepreneurial State. Revised Edition. London: Anthem Press.

- Mazzucato, M. 2018. The Value of Everything: Making and Taking in the Global Economy. London: Penguin-Allen Lane.

- Mazzucato, M., and M. McPherson. 2018. ‘The Green New Deal: A bold mission-oriented approach.’ IIPP Policy Brief (December). London: Institute for Innovation and Public Purpose.

- Mazzucato, M., and C. C. R. Penna. 2016. ‘Beyond Market Failures: the Market Creating and Shaping Roles of State Investment Banks.’ Journal of Economic Policy Reform 19 (4): 305–326.

- Mazzucato, M., and G. Semieniuk. 2018. ‘Financing Renewable Energy: Who Is Financing What and Why it Matters.’ Technological Forecasting & Social Change 127: 8–22.

- McDonald, D. A. 2016. ‘To Corporatize or Not to Corporatize (And if so How)?’ Utilities Policy 40: 107–114.

- McDonald, D. A., T. Marois, and D. V. Barrowclough (Eds.) 2020. Public Banks and Covid-19: Combatting the Pandemic With Public Finance. Municipal Services Project (Kingston), UNCTAD (Geneva), and Eurodad (Brussels). https://publicbankscovid19.org/.

- McDonald, D. A., T. Marois, and S. Spronk. 2021. ‘Public Banks + Public Water = SDG 6?’ Water Alternatives 14 (1): 117–134.

- McNally, D. 2020. Blood and Money: War, Slavery, Finance, and Empire. Chicago, Il: Haymarket Books.

- Megginson, W. L. 2005. The Financial Economics of Privatization. New York: Oxford University Press.

- Meiksins Wood, E. 2002. The Origin of Capitalism: A Longer View. London: Verso.

- Mettenheim, K., and O. Butzbach. 2017. ‘Back to the Future of Alternative Banks and Patient Capital.’ In Public Banks in the Age of Financialization: A Comparative Perspective, edited by C. Scherrer, 29–50. Cheltenham, UK: Edward Elgar Publishing.

- Minsky, H. P. 2008 [1986]. Stabilizing an Unstable Economy. London: McGraw-Hill.

- Nachtwey, O., and T. ten Brink. 2008. ‘Lost in Translation: The German World-Market Debate in the 1970s.’ Historical Materialism 16 (1): 37–70.

- Palermo, G. 2019. ‘Power: a Marxist View Coercion and Exploitation in the Capitalist Mode of Production.’ Cambridge Journal of Economics 43: 1353–1375.

- Poulantzas, N. 2000 [1978]. State, Power, Socialism. New York: Verso Classics.

- Ray, R., K. P. Gallagher, and C. A. Sanborn, eds. 2020. Development Banks and Sustainability in the Andean Amazon. Abingdon, UK: Routledge.

- Ribeiro de Mendonça, A. R., and S. Deos. 2017. ‘Beyond the Market Failure Argument: Public Banks as Stability Anchors.’ In Public Banks in the Age of Financialization, edited by C. Scherrer, 13–28. Cheltenham, UK: Edward Elgar Publishing.

- Roberts, A. 2015. ‘Gender, Financial Deepening and the Production of Embodied Finance: Towards a Critical Feminist Analysis.’ Global Society 29 (1): 107–127.

- Scherrer, C., ed. 2017. Public Banks in the Age of Financialization: A Comparative Perspective. Cheltenham, UK: Edward Elgar Publishing.

- Shirley, M. M. 1999. ‘Bureaucrats in Business: The Roles of Privatization Versus Corporatization in State-Owned Enterprise Reform.’ World Development 27 (1): 115–136.

- Shleifer, A. 1998. ‘State Versus Private Ownership.’ Journal of Economic Perspectives 12 (4): 133–150.

- Shonfield, A. 1969 [1965]. Modern Capitalism: The Changing Balance of Public and Private Power. New York: Oxford University Press.

- Skidelsky, R., F. Martin, and C. Westerlind Wigstrom. 2011. Blueprint for a British Investment Bank. London: Centre for Global Studies.

- Spratt, S., and L. Ryan-Collins. 2012. Development Finance Institutions and Infrastructure: A Systematic Review of Evidence for Development Additionality. A Report Commissioned by the Private Infrastructure Development Group. Brighton, UK: Institute of Development Studies.

- Stiglitz, J. 1994. ‘The Role of the State in Financial Markets.’ Proceedings of the World Bank Annual Conference on Development Economics 1993: 19–61.

- Vanberg, V. J. 2005. ‘Market and State: The Perspective of Constitutional Political Economy.’ Journal of Institutional Economics 1 (1): 23–49.

- von Mettenheim, K., and M. A. Del Tedesco Lins, eds. 2008. Government Banking: New Perspectives on Sustainable Development and Social Inclusion from Europe and South America. Rio de Janeiro and Berlin: Konrad Adenauer Foundation.

- UNCTAD. 2019. Trade and Development Report 2019: Financing a Global Green New Deal. Geneva: United Nations Conference on Trade and Development.

- UN IATF. 2019. Financing for Sustainable Development Report. New York: United Nations Inter-Agency Task Force on Financing for Development.

- Vidal, G., W. C. Marshall, and E. Correa. 2011. ‘Differing Effects of the Global Financial Crisis: Why Mexico has Been Harder hit Than Other Large Latin American Countries.’ Bulletin of Latin American Research 30 (4): 419–435.

- World Bank. 2012. Global Financial Development Report 2013: Rethinking the Role of State in Finance. Washington: World Bank.

- Xu, J., X. Ren, and X. Wu. 2019. Mapping Development Finance Institutions Worldwide: Definitions, Rationales, and Varieties. NSE Development Financing Research Report No. 1. Beijing, China: Peking University Institute of New Structural Economics.